Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

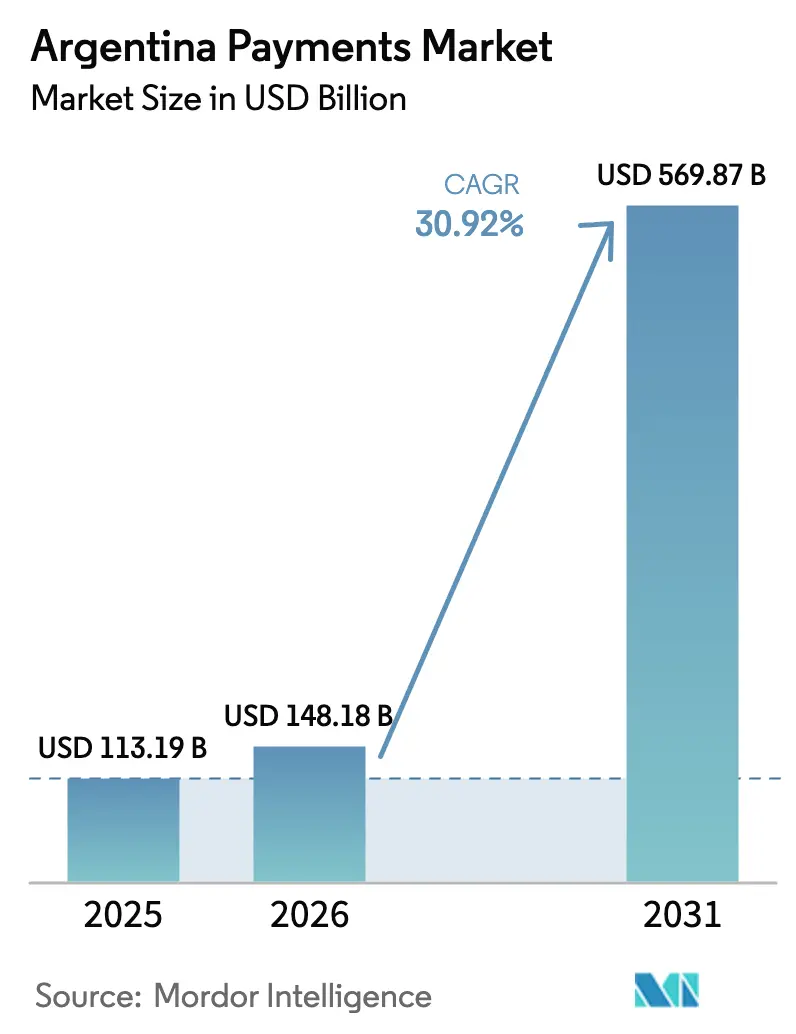

| Base Year Market Size (2025) | USD 113.19 Billion |

| Market Size (2026) | USD 148.18 Billion |

| Market Size (2031) | USD 569.87 Billion |

| Growth Rate (2026 - 2031) | 30.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Payments Market Analysis by Mordor Intelligence

The Argentina payments market size is expected to grow from USD 113.19 billion in 2025 to USD 148.18 billion in 2026 and is forecast to reach USD 569.87 billion by 2031 at 30.92% CAGR over 2026-2031. A synchronized policy mix of monetary tightening, gradual foreign-exchange liberalization, and nationwide QR-code interoperability is reshaping transaction habits at scale. Consumers and businesses are shifting from cash toward mobile wallets, account-to-account rails, and contactless POS cards in search of speed, transparency, and inflation protection. Network effects are accelerating because every new QR-accepting merchant increases the utility of virtual wallets, while rising smartphone penetration lowers onboarding costs. Competitive intensity is escalating as fintech challengers cultivate multi-service ecosystems around high-yield wallet balances, forcing incumbent banks to defend share with bundled offerings and biometric security upgrades. Emerging cross-border corridors, especially with Brazil, signal a new opportunity set for providers that can reconcile local compliance with instant settlement.

Key Report Takeaways

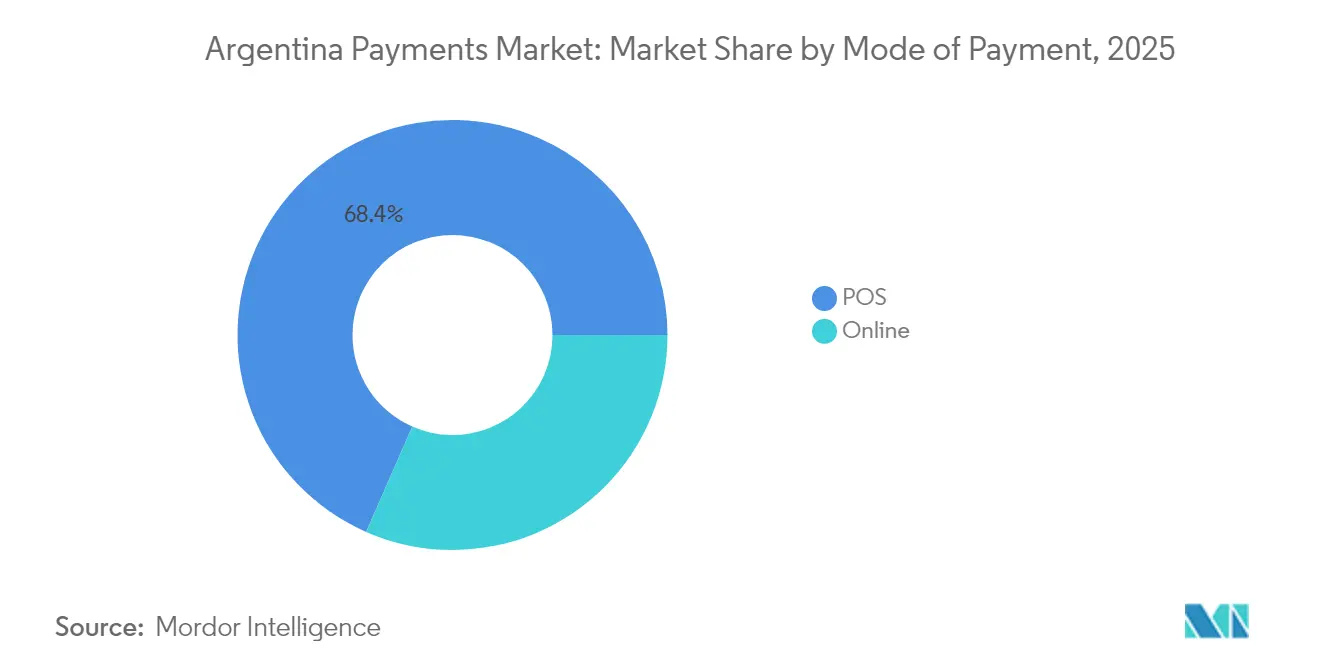

- By mode of payment, POS transactions led with 68.42% of Argentina payments market share in 2025, whereas online digital wallets and account-to-account transfers are expanding at 31.48% CAGR through 2031.

- By interaction channel, POS maintained a 70.36% revenue share in 2025; e-commerce and m-commerce are advancing at a 32.12% CAGR to 2031.

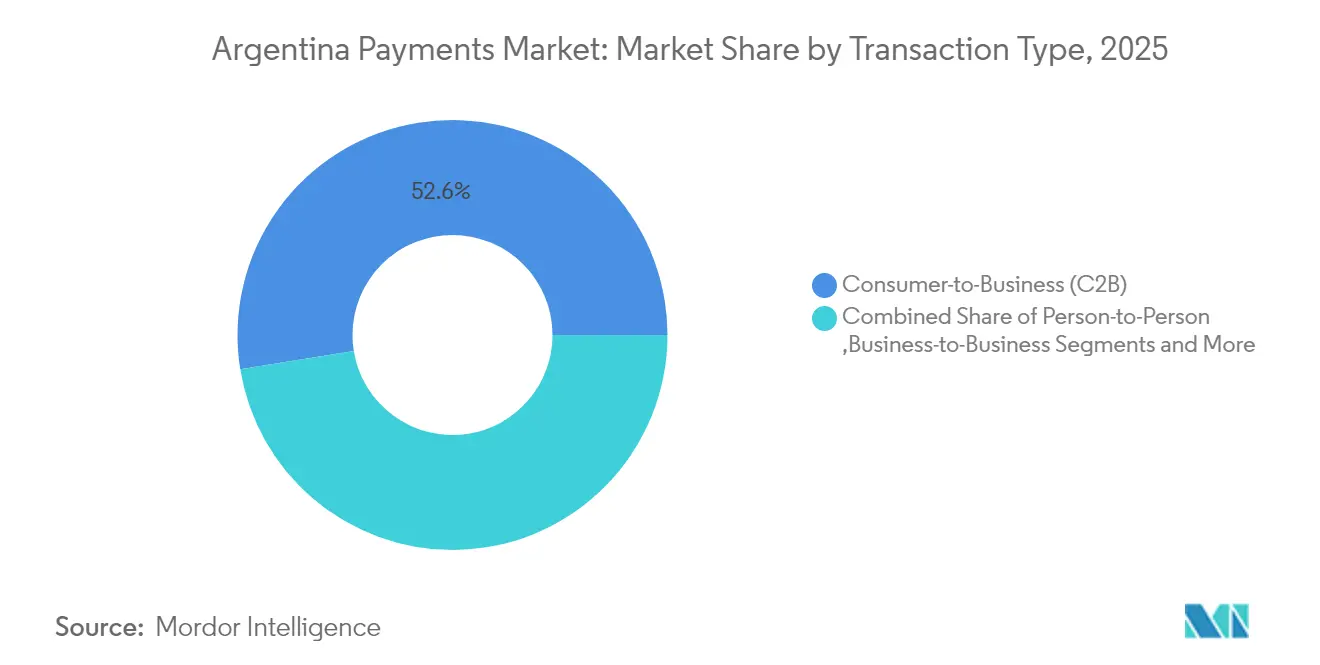

- By transaction type, C2B transactions held 52.55% share of the Argentina payments market size in 2025, while remittances and cross-border payments post the fastest 33.02% CAGR through 2031.

- By end-user industry, retail commanded 27.62% share of the Argentina payments market size in 2025; healthcare exhibits the highest 31.18% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce and m-commerce surge | +8.2% | National, with concentration in Buenos Aires, Córdoba, Rosario | Medium term (2-4 years) |

| Government digital-payment push (Transferencias 3.0) | +6.6% | National | Short term (≤ 2 years) |

| Smartphone penetration boom | +4.9% | National, with urban concentration | Medium term (2-4 years) |

| Real-time payments and interoperable QR rise | +5.9% | National, with early adoption in major urban centers | Short term (≤ 2 years) |

| Hyper-inflation fuels digital-wallet and crypto use | +3.9% | National | Short term (≤ 2 years) |

| Open-banking and embedded-finance ecosystems | +3.3% | National, initially concentrated in Buenos Aires | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce and m-commerce surge

Argentina’s online retail turnover reached USD26.7 billion in 2023 and is projected to grow 17% annually to 2027. Mobile transactions climbed 248% in H1 2024, establishing the handset as the primary checkout device for a broad demographic. Merchants respond with omnichannel gateways that support one-click payments and installment plans, tactics that stabilize sales despite macro volatility. Installments, once premium, are now baseline, allowing households to spread large-ticket purchases and manage inflation risk. The feedback loop between shopper expectations and payment optionality sustains double-digit online volume growth.

Government digital-payment push (Transferencias 3.0)

Transferencias 3.0 mandates that any QR code generated in Argentina must be readable by every licensed wallet, eliminating proprietary silos. Millions of interoperable account-to-account transactions now clear in 15 seconds or less, supporting financial inclusion in regions with scarce card terminals. The February 2025 extension into public transport sets the stage for daily-use micropayments at metro gates, buses, and trains. [1]Banco Central de la República Argentina, “Means of Payment,” bcra.gob.ar This expansion is expected to compress cash usage further and strengthen open-banking data flows that underpin embedded finance models.

Smartphone penetration boom

Handset ownership reached 81% of the population, enabling 68% of Argentinians to transact via mobile at least weekly. Wallet providers integrate biometric login and tokenized card credentials to improve security without adding friction. The device also functions as a budgeting dashboard, delivering push notifications on spending categories and savings yields. These value layers deepen engagement and raise switching costs, amplifying the network moat of leading platforms.

Real-time payments and interoperable QR rise

Real-time rails account for 36.6% of payouts and are expected to climb at 24.4% annually to 2028. Merchants can accept digital payments with only a printed QR, avoiding costly hardware and settlement delays. The February 2025 regulation that standardizes QR in public transport will introduce millions of daily commuters to the rail, accelerating mass-market adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating fraud and charge-backs | -4.9% | National, with higher impact in urban areas | Medium term (2-4 years) |

| FX controls hamper cross-border flows | -2.6% | National, with greater impact on import-dependent businesses | Short term (≤ 2 years) |

| Fragmented rails drive high merchant fees | -3.3% | National, with disproportionate impact on SMEs | Medium term (2-4 years) |

| Data-privacy / localization burden | -2.3% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating fraud and charge-backs

Rapid digitalization has exposed merchants to sophisticated phishing, synthetic identity, and AI-enabled card-testing scams. The resulting charge-back ratios threaten margins and can trigger scheme fines. Providers must deploy layered defenses—behavioral analytics, device fingerprinting, and consortium data sharing—to safeguard user trust. Smaller acquirers face cost barriers, fuelling consolidation as scale becomes essential for fraud-model training. [2]Bank for International Settlements, “Faster Digital Payments: Global and Regional Perspectives,” bis.org

FX controls hamper cross-border flows

Although April 2025 reforms allow instant access to U.S. dollars for imports, operational gaps persist as enterprises recalibrate treasury workflows and compliance rules. Until bank and customs systems fully synchronize, friction will remain in supplier payments and remittance corridors. Short-term uncertainty tempers the pace at which merchants integrate global checkout options, slowing the revenue potential of cross-border commerce.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Digital wallets reshape financial habits

Point-of-Sale retained 68.42% of the Argentina payments market share in 2025, with debit-card transactions rising to 2.979 billion and credit-card swipes to 1.913 billion. Familiarity, installment compatibility, and widespread terminal coverage underlie this resilience. Yet inflation-weary consumers increasingly favor wallets that credit daily interest on idle balances, eroding card primacy. The Argentina payments market size linked to online digital wallets and account-to-account transfers is projected to expand at 31.48% CAGR, powered by instant settlement and bonus yield features. Mercado Pago commands nearly 80% of wallet float, but challengers such as Naranja X entice users with 76% annual yields, nudging share away from incumbents.

Digital wallets now bundle bill pay, micro-insurance, and small-ticket investing, deepening user stickiness. Retailers accept wallet QR codes alongside cards, creating hybrid checkout flows that let customers split payment across instruments. Inflation-indexed savings vehicles embedded in wallets appeal to gig-economy workers who lack formal bank relationships. Consequently, the Argentina payments market demonstrates a shift toward multi-utility wallets rather than single-purpose payment apps.

By Interaction Channel: Mobile commerce accelerates

Physical POS captured 70.36% of 2025 revenue, confirming the centrality of in-store shopping. Tap-to-pay usage exceeds 70% of in-store volume, illustrating how contactless technologies refresh established channels. The Argentina payments market size processed through POS is expected to grow steadily, albeit slower than digital channels, as retailers modernize terminals to accept EMV-co-branded wallets.

Conversely, e-commerce and m-commerce record a 32.12% CAGR outlook on the back of 81% smartphone penetration. Social platforms embed storefronts that route payments via deep links to pre-credentialed wallets, reducing checkout abandonment. Transaction data gathered across mobile touchpoints feeds AI recommendation engines, enabling merchants to tailor offers by cohort. The convergence of transport QR codes with mobile wallets will elevate daily active users, boosting repeat purchase frequency and reinforcing brand loyalty.

By Transaction Type: Cross-border payments surge

C2B flows dominate at 52.55% share in 2025, underpinned by retail turnover and service-sector ubiquity. BNPL, valued at USD282 million in 2023, is gaining traction within C2B as consumers seek inflation-mitigation via installment spreads. Merchants integrate BNPL providers directly into checkout stacks, preserving cart conversion while outsourcing credit risk.

Remittances and cross-border transfers present the fastest 33.02% CAGR through 2031. Revised FX rules now allow businesses to settle imports on customs clearance, unlocking liquidity. Brazilian tourists already make instant peso payments through the Pix-Mercado Pago bridge without currency conversion, demonstrating the network’s utility. Payment providers that combine transparent FX pricing with real-time rails are positioned to capture wallet share from informal channels.

By End-user Industry: Healthcare digitalization accelerates

Retail held 27.62% of 2025 revenue, reflecting the sector’s transaction intensity and early QR adoption. Loyalty integration is the next competitive frontier as grocers and pharmacies link wallet IDs to reward engines that issue instant cashback at checkout. Data analytics from receipt-level information drive dynamic pricing strategies and personalised upsells.

Healthcare charts a 31.18% CAGR to 2031. Hospital groups embed card-on-file and wallet pay-by-link inside telemedicine portals, reducing admission time and improving cash collection. Outcome-based reimbursement models, encouraged by multilateral lenders, further digitize payment flows between insurers, providers, and patients. High ticket sizes and recurrent billing open scope for installment plans and medical BNPL, expanding average revenue per user for payment gateways.

Geography Analysis

Argentina’s metropolitan corridors spearhead digital adoption. Buenos Aires alone accounts for more than 35% of wallet transactions, followed by Córdoba and Rosario, where university populations drive mobile-first behavior. Transferencias 3.0 ensures any wallet can scan any QR nationwide, narrowing the urban-rural acceptance gap. As public transport integrates QR in the Buenos Aires subway, commuters in Greater Buenos Aires are expected to generate millions of micro-payments weekly, a template set for provincial roll-out within two years.

Border states observe heightened demand for interoperable FX-light solutions. The Pix linkage with Brazil allows instantaneous settlement in pesos while debiting reais, a feature attracting retailers in Misiones and Corrientes that rely on Brazilian shoppers. The International Monetary Fund underscores that regional payment interoperability could shave transaction costs by 50% and shorten settlement cycles from days to seconds.

Patagonia and the northwest provinces lag in digital density due to connectivity gaps but benefit from low-cost QR acceptance that circumvents card-terminal logistics. Government-subsidised fibre projects and 4G expansion will lift bandwidth, enabling wallet providers to extend cashback campaigns that accelerate on-boarding. Regional banks partner with fintechs to bundle micro-loans inside wallets, addressing credit deserts without branch build-outs.

Competitive Landscape

The Argentina payments market is shifting from fragmented to oligopolistic as scale economics favour platforms with large float balances and robust fraud-detection engines. Mercado Pago retains user primacy on back of its marketplace heritage and USD250 million debt raise in September 2024, earmarked for expanded credit lines and AI tooling. The firm’s antitrust action against 36 banks in August 2024 frames the debate over open access versus proprietary rails, with regulators balancing inclusion against systemic stability.

Traditional banks consolidate around MODO, positioning it as a joint defence against fintech incursion. However, competitive parity requires rapid iteration that bank governance sometimes slows. To compensate, BBVA Argentina reported that 93.9% of 2023 sales occurred on digital channels, illustrating a pivot to mobile origination. The bank deploys behavioural analytics to approve personal loans within minutes, mirroring fintech turnaround times.

Second-tier challengers such as Ualá leverage recent USD300 million Series E funding to build a full-stack offering: prepaid cards, wealth tools, and small-business acceptance kits. GeoPagos targets enterprise clients with white-label acquiring solutions, enabling retailers to circumvent card-network fees via direct account debits. Competitive vectors increasingly centre on yield, cross-border utility, and embedded-finance plug-ins that allow non-financial apps to hold and move value.

Argentina Payments Industry Leaders

Servicios Electrónicos de Pago S.A. (PagoFácil)

GIRE S.A. (Rapipago)

PayU Argentina S.R.L.

Paysafe Limited

Google Pay (Alphabet Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The Central Bank of Argentina (BCRA) removed foreign-exchange restrictions, allowing businesses to pay for imports immediately upon customs clearance and permitting unlimited U.S. dollar purchases through bank accounts, thereby easing cross-border payment friction.

- April 2025: The World Bank Group announced a USD12 billion support package for Argentina's economic reform program, including USD5.5 billion for private-sector investment that is expected to boost digital payment adoption across infrastructure, agribusiness, and energy.

- March 2025: Ualá raised USD300 million in Series E funding to expand its financial-services ecosystem and bolster payment infrastructure, signalling investor confidence in wallet-centric models.

- February 2025: BCRA issued Communication “A” 8206, setting QR standards for public transportation with implementation scheduled for May 12 2025, anchoring wallet usage in everyday commuting.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Argentina payments market as the gross monetary value of all consumer and business payment transactions routed through point-of-sale terminals, digital wallets, account-to-account rails, and cash at delivery, whether in-store, in-app, or online.

Scope Exclusion: Online purchases of motor vehicles, real-estate transfers, mortgage or loan repayments, utility bill payments, and securities trading are not counted.

Segmentation Overview

- By Mode of Payment

- Point-of-Sale

- Card (Debit, Credit, Pre-paid)

- Digital Wallets (Apple Pay, Google Pay, Interac Flash)

- Cash

- Other POS (Gift-cards, QR, Wearables)

- Online

- Card (Card-Not-Present)

- Digital Wallet and Account-to-Account (Interac e-Transfer, PayPal)

- Other Online (COD, BNPL, Bank Transfer)

- Point-of-Sale

- By Interaction Channel

- Point-of-Sale

- E-commerce/M-commerce

- By Transaction Type

- Person-to-Person (P2P)

- Consumer-to-Business (C2B)

- Business-to-Business (B2B)

- Remittances and Cross-border

- By End-user Industry

- Retail

- Entertainment and Digital Content

- Healthcare

- Hospitality and Travel

- Government and Utilities

- Other End-user Industries

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts then interview payment service providers, acquiring banks, fintech founders, card schemes, and regulators across Buenos Aires, Córdoba, and Rosario. These conversations test early findings, fill data gaps on fee structures and channel shifts, and help us fine-tune key assumptions before any numbers are locked in.

Desk Research

We begin with structured desk work that reviews tier-1 public datasets such as the Central Bank of Argentina's monthly Retail Payments Bulletin, the National Statistics Institute's household ICT surveys, Cámara Argentina de Comercio Electrónico annual e-commerce audits, World Bank Findex notes, and IMF BOP payment statistics. Company filings, investor presentations, and reputable press releases complement these basics, while D&B Hoovers and Dow Jones Factiva supply verified firm-level metrics that anchor service revenues. The illustrative sources listed here are not exhaustive; many additional publications informed our evidence base.

Market-Sizing & Forecasting

A top-down demand pool is built from total transaction volumes released by the central bank and e-commerce turnover reported by CACE, which are then split by channel and instrument using survey shares and merchant panels. Supplier roll-ups and sampled average-ticket-price × volume checks act as a selective bottom-up counterpoint that adjusts totals where variances appear. Variables such as smartphone penetration, QR-ready merchant density, inflation-adjusted consumer spend, real-time rail adoption, and card issuance growth feed a multivariate regression that drives our 2025-2030 outlook. Where bottom-up inputs are thin, gaps are bridged with narrow confidence ranges agreed with interviewees.

Data Validation & Update Cycle

Outputs run through automated variance tests against alternate data series, followed by two-step analyst peer review. Reports refresh each year, and interim updates are triggered whenever policy changes, exchange-rate shocks, or material M&A reshape the baseline.

Why Our Argentina Payment Baseline Commands Reliability

Published market values often diverge because each firm chooses its own transaction set, currency conversion point, and refresh cadence.

Key gap drivers include narrower channel coverage, single-year survey extrapolations, or models that ignore cash and prepaid flows; all issues our disciplined scope and annual recalibration avoid.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 113.19 B (2025) | Mordor Intelligence | - |

| USD 86.92 B (2024) | Regional Consultancy A | Excludes cash and prepaid transactions; relies on limited six-month data window |

| USD 26.7 B (2023) | Trade Journal B | Tracks only e-commerce payments; omits POS, P2P, and B2B flows |

In sum, our balanced mix of verified public sources, direct market voices, and dual-path modeling gives decision-makers a transparent, reproducible baseline that stands up to scrutiny even when competing figures vary widely.

Key Questions Answered in the Report

What is the current size of the Argentina payments market?

The Argentina payments market is valued at USD 148.18 billion in 2026.

How fast is the market expected to grow?

It is projected to expand at a 30.92% CAGR, reaching USD 569.87 billion by 2031.

Which payment method is growing the quickest?

Online digital wallets and account-to-account transfers are advancing at 31.48% CAGR through 2031.

Why are cross-border payments important for Argentina?

Liberalized FX rules and the Pix integration with Brazil position cross-border transfers as the fastest-growing segment at 33.02% CAGR.

How is government policy influencing payment adoption?

The Transferencias 3.0 framework mandates QR interoperability nationwide, boosting real-time account-to-account payments.

Which end-user industry offers the highest growth potential?

Healthcare payments, driven by telehealth and outcome-based financing, are forecast to grow 31.18% annually through 2031.

Page last updated on: