India Lighting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

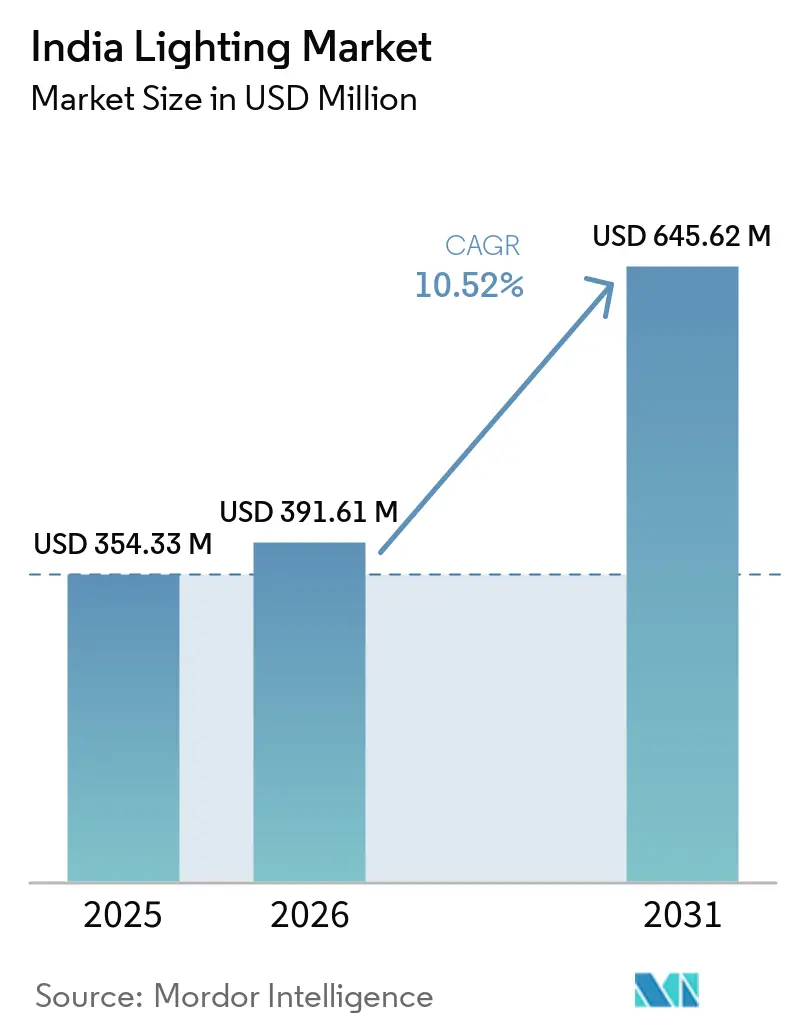

| Base Year Market Size (2025) | USD 354.33 Million |

| Market Size (2026) | USD 391.61 Million |

| Market Size (2031) | USD 645.62 Million |

| Growth Rate (2026 - 2031) | 10.52% CAGR |

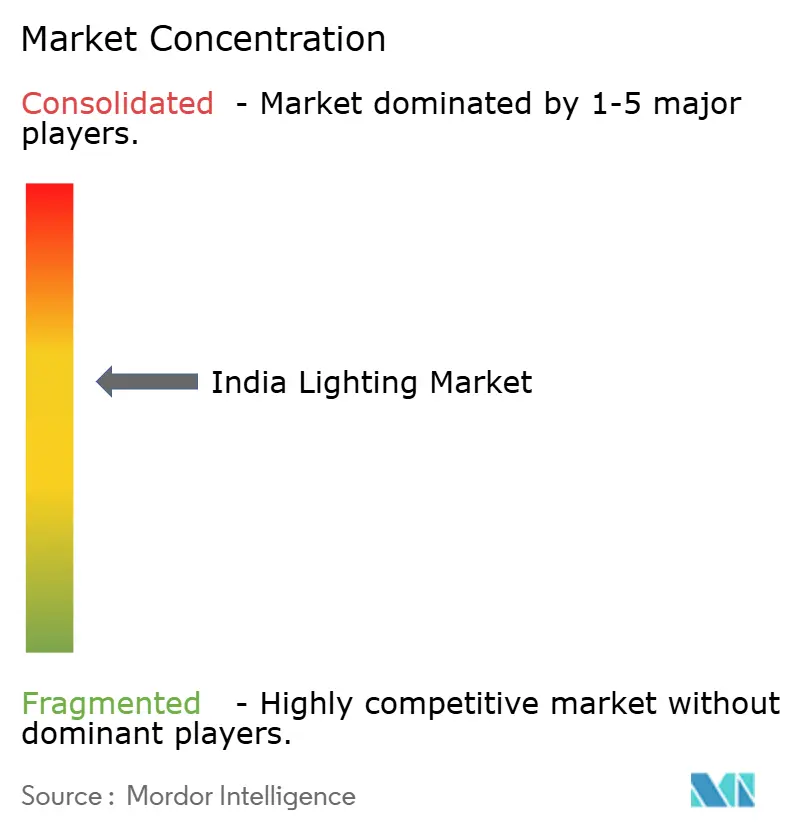

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Lighting Market Analysis by Mordor Intelligence

The India lighting market size is expected to grow from USD 354.33 million in 2025 to USD 391.61 million in 2026 and is forecast to reach USD 645.62 million by 2031 at 10.52% CAGR over 2026-2031. Urban infrastructure spending under the Smart Cities Mission, large-scale government procurement of LED bulbs, and mandatory energy-efficiency codes for buildings continue to anchor demand and reduce lifetime ownership costs. Bureau of Energy Efficiency (BEE) star-labeling and Energy Conservation Building Code (ECBC) rules keep shifting buyer preference toward high-performance luminaires, while bulk-tender price erosion has opened mass-market access to LED technology. Competitive intensity remains high as domestic majors, global multinationals, and regional specialists all race to bundle connected-lighting software, predictive-maintenance analytics, and façade-lighting design into turnkey offerings. Export opportunities are also expanding because India now functions as a cost-competitive manufacturing base for the wider Asia-Pacific supply chain and for fast-growing Middle East and Africa projects.

Key Report Takeaways

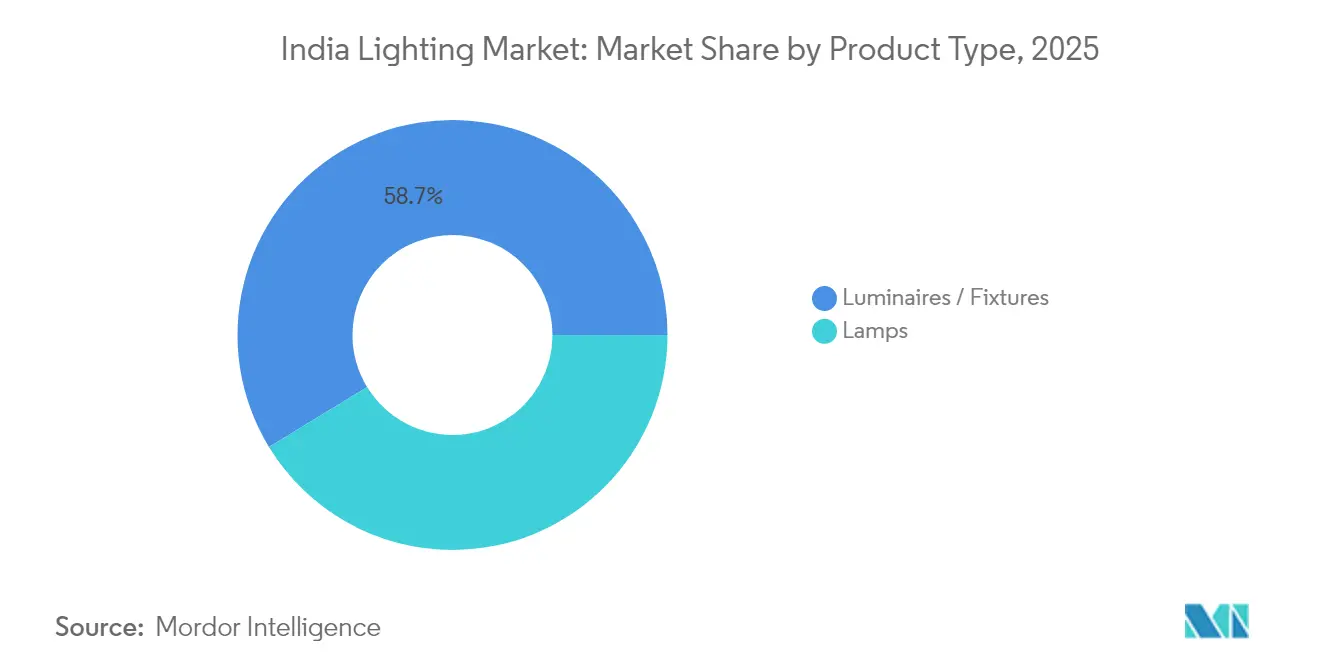

- By product type, luminaires/fixtures led with 58.72% revenue share of the India lighting market in 2025 and are projected to grow at 11.78% CAGR through 2031.

- By light source, LED technology accounted for 81.35% of the India lighting market share in 2025, while the same segment is set to advance at 12.05% CAGR to 2031.

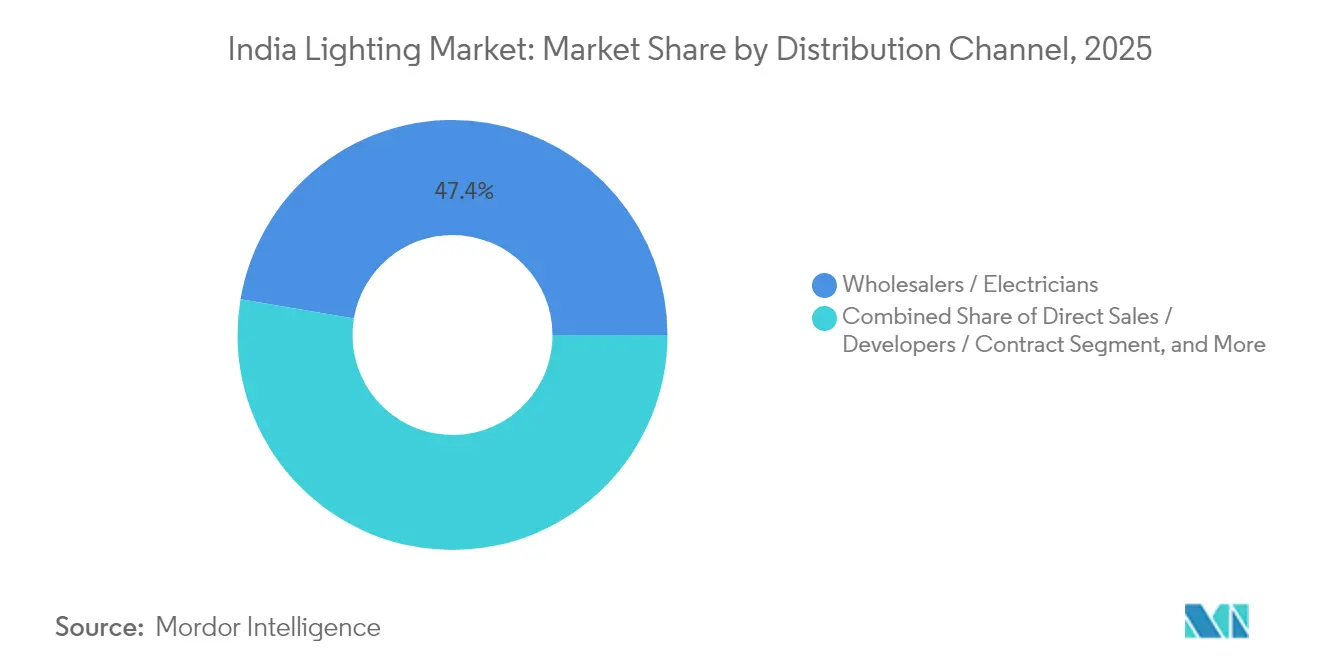

- By distribution channel, wholesalers/electricians held 47.35% share of the India lighting market size in 2025; lighting specialists and others are forecast to expand at 13.12% CAGR between 2026-2031.

- By application, commercial lighting commanded a 41.05% share of the India lighting market in 2025, and outdoor lighting is rising at a 12.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with India representing one among them. The global report on lighting market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

India Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| LED price erosion and energy-efficiency mandates | +1.20% | National, with concentrated impact in Tier-I cities | Short term (≤ 2 years) |

| Rapid urban infrastructure build-out (Smart Cities Mission) | +1.50% | 100 Smart Cities, spillover to Tier-II/III cities | Medium term (2-4 years) |

| Government procurement (UJALA and SLNP) | +0.80% | National, with priority in rural and semi-urban areas | Short term (≤ 2 years) |

| Growth of Tier-II/III city façade-lighting projects | +0.90% | Tier-II/III cities, particularly in Gujarat, Maharashtra, Karnataka | Medium term (2-4 years) |

| Emerging DC-micro-grid and off-grid solar lighting demand | +0.70% | Rural areas, particularly in Odisha, Chhattisgarh, remote villages | Long term (≥ 4 years) |

| Integration of Li-Fi pilots in enterprise campuses | +0.60% | Metro cities, enterprise hubs in Bangalore, Pune, Hyderabad | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

LED price erosion and energy-efficiency mandates

Mandatory ECBC compliance for new commercial buildings plus BEE star-label requirements have pushed developers toward high-efficacy fixtures that deliver 35%–50% energy savings relative to baseline codes.[1]Bureau of Energy Efficiency, “Energy Conservation Building Code,” BEEIndia.gov.in UJALA’s competitive tenders cut retail LED bulb prices by 90% from 2014 figures and distributed 36.87 crore units, making LEDs the universal default even beyond public-sector programs. As electricity tariffs climb and corporate net-zero pledges gain momentum, enterprises now treat lighting retrofits as first-wave decarbonization measures. The result is sustained double-digit volume demand for premium-efficiency chips, optics, and drivers across commercial, industrial, and high-end residential builds. Vendors that certify products under the latest Super ECBC thresholds are defending margins despite broader price competition.

Rapid urban infrastructure build-out (Smart Cities Mission)

The Smart Cities Mission has approved USD 24.7 billion in projects and completed 5,909 work orders by July 2024; each integrated command center specifies connected street, area, and façade lighting that can be monitored in real time.[2]ICC Technical Cooperation Association, “India’s Smart City Project—Updates and Future,” ICC-TCA.org Municipalities increasingly bundle lighting into traffic, safety, and environmental dashboards, turning luminaires into edge nodes for broader city-data platforms. Vendors able to supply interoperable controls, adaptive-dimming algorithms, and cyber-secure firmware are winning multiyear framework contracts. Because second-tier cities replicate flagship designs from metros such as Pune and Varanasi, contract pipelines extend well into the medium term. The clustering of projects also shortens payback cycles for specialized installers and keeps warehouse throughput high for component suppliers.

Government procurement (UJALA and SLNP)

Energy Efficiency Services Limited (EESL) has installed 1.30 crore LED streetlights under SLNP and continues to refresh tenders in five-year maintenance cycles that guarantee predictable volumes.[3]Press Information Bureau, “Year-End Review of Ministry of Power,” PIB.gov.inBulk orders enable domestic manufacturers to amortize capex and negotiate long-term silicon and phosphor supply deals at favorable hedged prices. UJALA’s Gram-level rollouts further anchor demand in cash-constrained rural zones, creating a national floor price that private brands must match. However, delayed municipal payments can stretch working capital for smaller contractors, a risk that favors well-capitalized companies or those partnered with infrastructure financiers. Replication of the EESL model by Southeast Asian and African governments positions Indian OEMs as template exporters.

Growth of Tier-II/III city façade-lighting projects

Projects such as the programmable illumination of Sudarshan Setu in Gujarat and riverfront upgrades in Surat showcase growing aesthetic ambitions outside metro centers.[4]Business Standard, “Orient Electric Illuminates Sudarshan Setu,” Business-Standard.com Local governments now insist on dynamic RGB programming, heritage-friendly color temperatures, and low-glare optics to boost tourism and civic pride. Mid-range control gear and IP-rated fixtures tailored for hot-humid zones are therefore in high demand. Regional EPC players able to offer end-to-end design, simulation, and commissioning win contracts over generic lamp sellers. This trend widens the addressable market for specialized luminaire makers and DMX-control software vendors targeting non-metro budgets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront retrofit cost for SMEs and households | -0.90% | National, with acute impact in rural and semi-urban areas | Short term (≤ 2 years) |

| Fragmented distribution and counterfeit products | -0.70% | National, concentrated in unorganized retail channels | Medium term (2-4 years) |

| Import-linked volatility in LED driver IC pricing | -0.50% | National, affecting all manufacturers dependent on imports | Short term (≤ 2 years) |

| Slow pay-out cycles in government EPC contracts | -0.40% | State and municipal levels, particularly in financially stressed states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High upfront retrofit cost for SMEs and households

Small factories and neighborhood retailers often face payback periods of 3-5 years on full-facility LED conversions, making many defer projects despite 40%–60% potential energy savings.[5]Council on Energy, Environment and Water, “Awareness and Adoption of Energy Efficiency in Indian Homes,” CEEW.in Limited awareness of lifecycle economics keeps decision-makers focused on sticker price rather than total cost of ownership. Although micro-finance and utility-on-bill schemes exist, uptake remains low in non-metro clusters because of cumbersome documentation and perceived technology risk. This capex hurdle slows penetration of connected fixtures and sensors that carry higher dollar-per-lumen pricing compared with basic retrofit bulbs.

Fragmented distribution and counterfeit products

Roughly 76% of LED bulbs sampled from informal retail outlets in 2023 failed basic BIS safety tests, eroding consumer trust and undercutting branded margins.[6]Reuters Staff, “India’s 76 percent LED bulbs found to be spurious—survey,” Reuters.com Because wholesalers-cum-electricians dominate 46.8% of the 2024 volume, every project involves multiple intermediaries where off-spec inventory can slip in. Enforcement of BIS compulsory registration remains uneven, and many small shops lack the technical means to verify holograms or QR authenticity codes. Organized players, therefore, spend heavily on channel audits and serialization technology, costs that dilute profitability and complicate rural expansion strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Luminaires Lead Value and Velocity

The luminaires and fixtures segment commanded a 58.72% revenue slice of the India lighting market in 2025 and is projected to grow at a 11.78% CAGR through 2031, underlining its dual role as both volume and value driver of the India lighting market. This category’s rise stems from Smart Cities Mission tenders that specify integrated, sensor-ready fixtures and from private developers bundling lighting with building-automation contracts to cut commissioning time. Luminaires frequently anchor façade-lighting packages, earning higher margins than commodity lamps because they embed optics, drivers, and on-board diagnostics that meet Bureau of Energy Efficiency specifications. Contractors targeting metro rail, airport-terminal, and data-center projects also prefer turnkey luminaires to minimize field wiring errors and accelerate sign-off, extending the segment’s edge in the India lighting market.

Second-order momentum comes from programmable RGB architectural jobs in Tier-II/III cities, where local authorities seek tourism branding without paying metro-grade premiums. Mid-range manufacturers that certify to BIS safety rules are winning here by pairing aluminum extrusion heat sinks with DMX controls that survive high-humidity coastal climates. Lamps, by contrast, continue to cede ground as price erosion compresses margins and government procurement resets bulk tender benchmarks. Even so, retrofit CFL-to-LED bulb swaps persist in the residential channel, cushioning lamps’ volume decline but not reversing the structural tilt toward higher-value luminaires.

By Light Source: LED Technology Sets the Benchmark

India LED lighting solutions held an 81.35% India lighting market share in 2025 and are projected to post the fastest 12.05% CAGR to 2031. The India lighting market size is tied to LEDs for commercial ceilings, roadway poles, and industrial high-bays, reflecting deeper penetration into price-sensitive rural installations. UJALA and Street Lighting National Program tenders normalized LED economics, while ECBC “Super” ratings funnel premium demand toward ≥150-lm/W luminaires that still command price premiums. Conventional fluorescent and HID technologies now survive mainly in legacy high-temperature factories where drivers face derating risks, but even those niches are shrinking as ruggedized LED engine platforms pass accelerated lifecycle tests.

LED adoption also benefits from emerging Li-Fi pilots that turn luminaires into data nodes, allowing facilities to overlay broadband capacity without radio-frequency congestion. Wipro Lighting’s alliance with pureLiFi exemplifies how vendors link illumination with connectivity to protect margins in a rapidly commoditizing diode market. At the same time, the Production-Linked Incentive Scheme for white goods subsidizes chip-on-board back-end lines, further localizing the LED bill of materials and improving cost resilience against import shocks, an upside for the India lighting industry as a whole.

By Distribution Channel: Specialists Accelerate

Wholesalers and electricians accounted for 47.35% of the India lighting market in 2025, reflecting entrenched contractor relationships and credit cycles. Yet the lighting specialists and “others” cohort is forecast to capture a 13.12% CAGR to 2031—more than double the wholesale channel’s pace—by bundling design consulting, IoT commissioning, and post-install analytics. These firms cater to airports, IT campuses, and luxury retail chains that budget for lifecycle performance rather than first-cost metrics, pushing connected-lighting attach rates above 40%.

The India lighting market’s shift toward specialists is further propelled by BIS counterfeit crackdowns that reward traceable supply chains. Signify’s smart-warehouse execution for Pilkington Automotive shows how specialists overlay asset-tracking beacons and predictive-maintenance dashboards to justify premiums. Meanwhile, direct sales to developers sustain share but face tighter working-capital cycles as real-estate firms press payment terms beyond 90 days. As a result, vendors diversify toward project-financing partnerships to secure early-stage cash flows, a trend likely to reshape the India lighting industry’s go-to-market mix through 2031.

By Application: Commercial Dominance, Outdoor Upside

Commercial installations generated 41.05% of 2025 India lighting market revenues on the back of rapid office-stock expansion and green-building certifications. Building operators weigh occupant wellness, glare indices, and circadian-tuning capabilities, which lift average selling prices far above residential norms. In contrast, outdoor lighting is set to clock the highest 12.96% CAGR, powered by Smart Cities and highway-corridor projects that insert adaptive-dimming clauses to cut municipal energy bills.

Industrial estates follow close behind as process manufacturers chase ESG scorecards that pledge 30%–40% power-use cuts. Warehouse operators like the e-commerce 3PLs in Bengaluru now embed occupancy sensors and daylight-harvesting logic to extend driver life past 60,000 hours, further boosting the India lighting market size tied to industrial retrofits. Residential demand remains volume-heavy but price-tethered, cushioning factory utilizations yet providing limited margin lift. Over the forecast window, commercial retrofits and outdoor smart-pole deployments will remain the core battlegrounds where vendors differentiate on controls, cybersecurity, and service SLAs.

Geography Analysis

India sits at the center of this supply web, and the Production-Linked Incentive scheme for white goods alone targets USD 23 billion in incremental output and USD 8.8 billion in exports over five years, reinforcing the India lighting market size advantages tied to local value addition. Component dependence remains a vulnerability; however, Indian buyers imported USD 12 billion worth of Chinese electronics and another USD 6 billion from Hong Kong in FY 2023-24, exposing LED driver costs to currency swings and freight bottlenecks. Even so, robust urban construction pipelines keep channel inventories fluid, and city-scale retrofits in Delhi, Bengaluru, and Pune continue to draw bid interest from global majors eager to tap the India lighting market share locked in municipal annual maintenance contracts. Rising foreign direct investment in smart-street-pole factories along the Delhi–Mumbai Industrial Corridor underpins a steady flow of high-Bay and facade-lighting exports to Southeast Asia.

Competitive Landscape

The India lighting market remains moderately fragmented, with the five largest vendors leaving ample room for fast-moving regional specialists. Signify continued to differentiate through connected-lighting software, announcing a proposed joint venture with Dixon Technologies to expand local manufacturing and shorten design-to-production cycles for consumer and professional SKUs. Havells India experienced operating-margin compression, prompting its management to double down on premium architectural fixtures and international diversification via a Delaware-incorporated vehicle under a joint venture with KRUT LED. Bajaj Electricals invested heavily in AI-enabled controls and predictive-maintenance analytics for industrial estates, positioning itself against global players seeking large-scale smart-factory rollouts.

Regional challengers such as Orient Electric widened resilience by embracing façade-lighting turnkey contracts, evidenced by the programmable illumination of Gujarat’s Sudarshan Setu that showcased a 256-scene DMX architecture and drew municipal inquiries from four additional coastal states. Syska’s equity infusion from Rare Enterprises underpins a channel-expansion push into Tier III cities, where counterfeit risk is high but branded share can climb quickly once distribution locks in electricians’ mindshare. On the component side, LED driver specialists in Bengaluru’s Electronics City have partnered with Taiwanese silicon foundries to localize micro-controller units, a strategic hedge against import-price volatility that previously clipped margins during the 2022 supply crunch.

Quality certification remains a critical moat: just 24% of more than 300 random LED bulb samples met BIS tests in 2023, prompting established players to highlight serialization, tamper-evident labels and QR code verification in marketing material. Firms embedding such safeguards not only stem grey-market leakage but also win preference in Smart Cities Mission tenders that explicitly score bids on traceability metrics. As price competition intensifies, success hinges on total lifecycle value rather than lumen-output parity. Vendors now bundle 5-year preventive-maintenance contracts, remote firmware upgrades and energy-savings dashboards, cementing annuity revenue streams that cushion diode price erosion. The resulting competitive theater blends hardware, software and service capabilities, demanding balance-sheet strength, rapid certification cycles and deep channel reach.

India Lighting Industry Leaders

Signify N.V.

Havells India Limited

SYSKA

Wipro Ltd.

Bajaj Electricals Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Bajaj Electricals’ profit doubled on a one-time gain coupled with robust consumer demand; leadership disclosed plans to channel the windfall into AI-driven lighting controls that promise subscription revenues beyond the initial hardware sale.

- March 2025: Signify and Dixon Technologies proposed a joint venture to co-manufacture LED bulbs and accessories, aiming to blend Signify’s optical-engineering IP with Dixon’s high-throughput surface-mount lines. The deal targets lower production lead times and export agility, reinforcing both firms’ pricing power in the connected-lighting tier.

- January 2025: Havells India posted a consolidated net profit dip even as revenue advanced, prompting management to accelerate premium-fixture launches and international joint ventures to recapture margins through higher average selling prices.

- August 2024: Rare Enterprises invested fresh capital into Syska LED, giving the brand the financial headroom to expand showroom footprints and roll out smart-home lighting bundles in aspirational Tier II towns.

India Lighting Market Report Scope

Lighting or illumination is the deliberate use of light to achieve practical or aesthetic effects. Lighting includes the use of both artificial light sources like lamps and light fixtures, as well as natural illumination by capturing daylight

The scope of the study focuses on the market analysis of light used in different applications in India. The study includes a detailed breakdown of the type of product, light source, distribution channel, and applications. The impact of COVID-19 on the market and affected segments are also covered under the scope of the study. Further, the disruption factors impacting the market's growth in the near future have been covered in the study regarding drivers and restraints.

India lighting market is segmented by product (luminaires/fixtures, lamps), light source (LED, conventional), distribution channel(direct sales/developers/contract, wholesalers/electricians, lighting specialists and others), application (commercial (offices, retail & hospitality,healthcare facilities), industrial (process industries,discrete industries,warehouses and other industrial setups),outdoor, residential). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Luminaires / Fixtures |

| Lamps |

| LED |

| Conventional |

| Direct Sales / Developers / Contract |

| Wholesalers / Electricians |

| Lighting Specialists |

| Others |

| Commercial | Offices |

| Retail and Hospitality | |

| Healthcare Facilities | |

| Others | |

| Industrial | Process Industries |

| Discrete Industries | |

| Warehouses and Other Industrial Set-ups | |

| Outdoor | |

| Residential |

| By Product Type | Luminaires / Fixtures | |

| Lamps | ||

| By Light Source | LED | |

| Conventional | ||

| By Distribution Channel | Direct Sales / Developers / Contract | |

| Wholesalers / Electricians | ||

| Lighting Specialists | ||

| Others | ||

| By Application | Commercial | Offices |

| Retail and Hospitality | ||

| Healthcare Facilities | ||

| Others | ||

| Industrial | Process Industries | |

| Discrete Industries | ||

| Warehouses and Other Industrial Set-ups | ||

| Outdoor | ||

| Residential | ||

Key Questions Answered in the Report

How large is the India lighting market in 2026?

The market is valued at USD 391.61 million in 2026 and is forecast to reach USD 645.62 million by 2031 at a 10.52% CAGR.

Which segment holds the biggest India lighting market share?

Luminaires and fixtures lead with 58.72% 2025 revenue share.

Why are LEDs dominant in Indian installations?

Government bulk-procurement programs and price erosion have pushed LED share to 81.35% in 2025, and they are still growing at 12.05% CAGR.

Which distribution channel is expanding fastest?

Lighting specialists are projected to grow at a 13.12% CAGR thanks to demand for smart-lighting integration services.

What is the main restraint on India's lighting adoption?

High upfront retrofit costs for SMEs and widespread counterfeit products in unorganized channels slow penetration rates.

Page last updated on: