Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

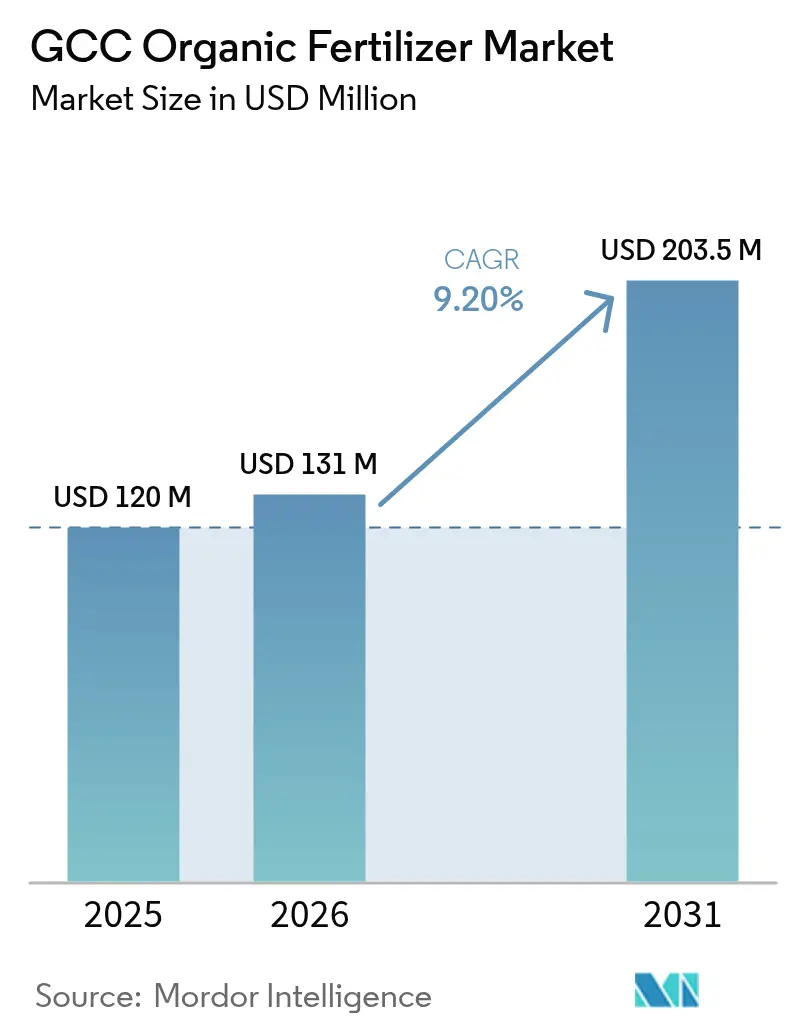

| Base Year Market Size (2025) | USD 120 Million |

| Market Size (2026) | USD 131 Million |

| Market Size (2031) | USD 203.5 Million |

| Growth Rate (2026 - 2031) | 9.20% CAGR |

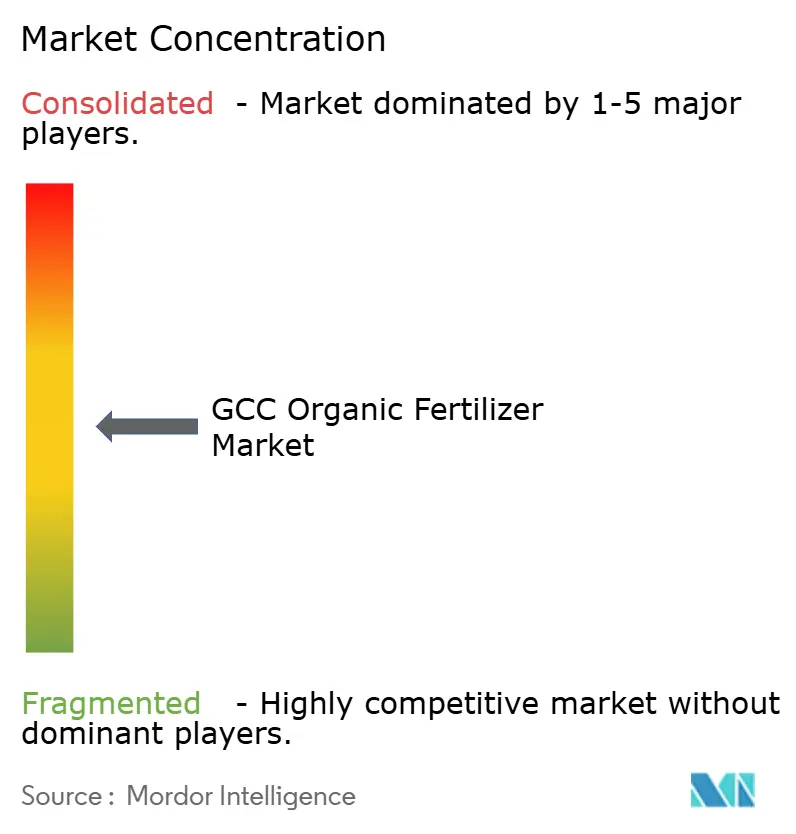

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Organic Fertilizer Market Analysis by Mordor Intelligence

The GCC organic fertilizer market size was valued at USD 120 million in 2025 and is projected to grow from USD 131 million in 2026 to USD 203.5 million by 2031, growing at a CAGR of 9.2% during the forecast period (2026–2031). Rising circular-economy policies, premium landscaping specifications in mega-tourism projects, and carbon-credit pilots are reinforcing demand even as synthetic-input subsidies taper. In 2025, Liquid formulations are scaling rapidly through drip-irrigation networks that now cover 48,000 hectares of area in the United Arab Emirates, while mineral-based blends derived from desalination brine attract precision-agriculture adopters seeking predictable NPK profiles. During the same period, Saudi Arabia anchors regional consumption on the back of 1.2 million hectares of date-palm orchards, but Oman is forecast to be the fastest-growing geography as eco-tourism resorts and organic date exports converge on robust incentive programs. Competitive intensity remains moderate, as the top five producers captured the majority of revenue and are integrating backward into organic waste collection and forward into site-specific application services to secure margins amid feedstock scarcity.

Key Report Takeaways

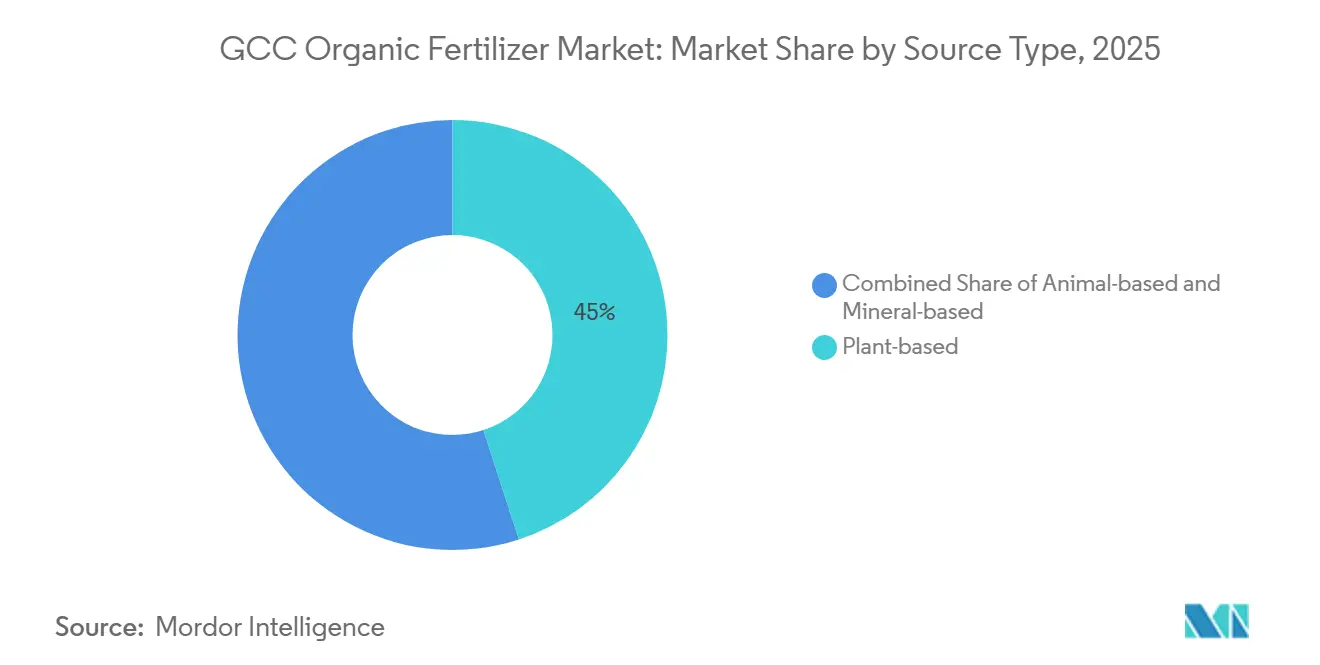

- By source type, plant-based formulations led the GCC organic fertilizer market with 45% in 2025, while mineral-based inputs are projected to expand at a 12.4% CAGR to 2031.

- By form, solid products accounted for 63% of the GCC organic fertilizer market size in 2025, and liquids are advancing at a 14.1% CAGR through 2031.

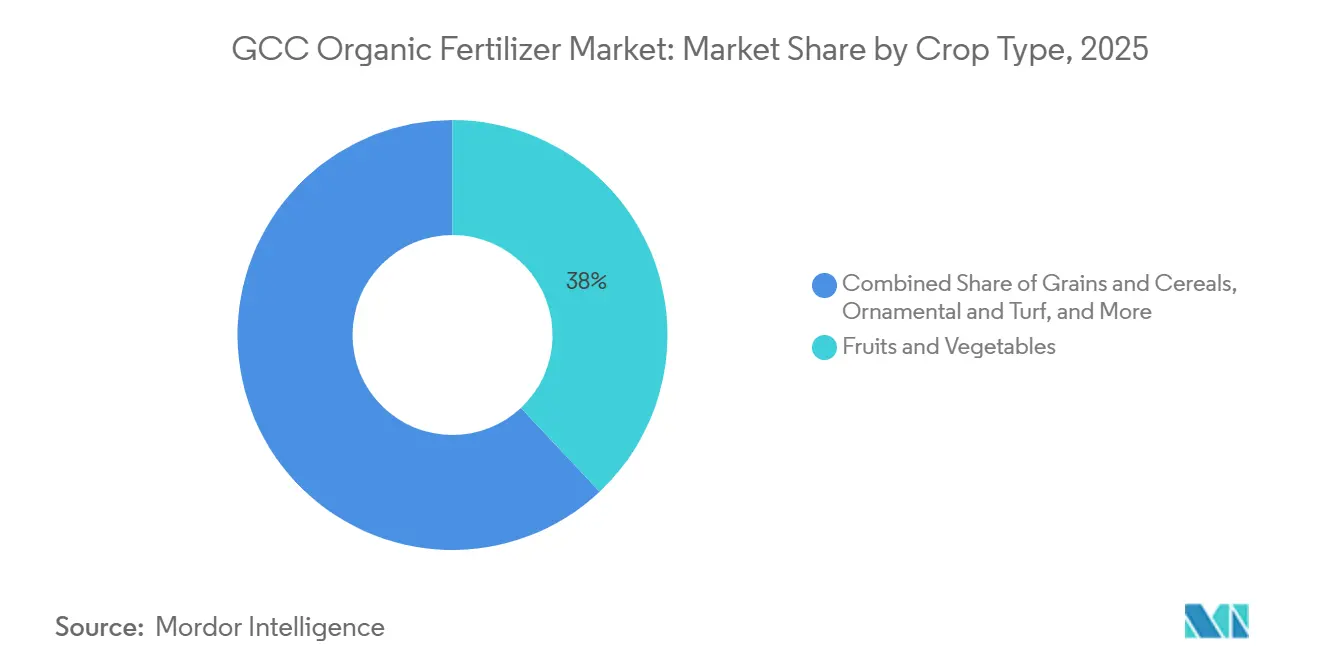

- By crop type, fruits and vegetables retained the largest 38% revenue share in 2025, while the ornamental and turf segment is projected to grow at a 11.7% CAGR between 2026-2031.

- By geography, Saudi Arabia accounted for 65% of the GCC organic fertilizer market share in 2025, and Oman is forecast to grow at the fastest, with a CAGR of 9.5% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Organic Fertilizer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidies for sustainable agriculture | +2.1% | Saudi Arabia, United Arab Emirates, Oman, and Qatar | Medium term (2-4 years) |

| Expanding organic food retail channels | +1.8% | United Arab Emirates and Saudi Arabia's urban centers, expanding to Kuwait and Bahrain | Short term (≤ 2 years) |

| Rising soil degradation concerns | +1.5% | GCC-wide, acute in Saudi Arabia and Oman | Long term (≥ 4 years) |

| Growing hotel and resort landscaping demand | +1.3% | Saudi Arabia, United Arab Emirates, and Qatar | Medium term (2-4 years) |

| Desalination brine reuse projects | +0.9% | United Arab Emirates, Saudi Arabia, and pilot in Oman | Long term (≥ 4 years) |

| Carbon-credit linked farming pilots | +0.6% | United Arab Emirates and Saudi Arabia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Subsidies for Sustainable Agriculture

Targeted fiscal programs narrow the price gap between organics and synthetics, converting hesitant growers. Saudi Arabia’s Agricultural Development Fund (ADF) is providing substantial funding to modernize agriculture, with approximately USD 220 million for high-tech greenhouses between 2021 and 2025[1]Source: Saudi Ministry of Environment Water and Agriculture, “National Center for Organic Agriculture Subsidy Program,” mewa.gov.sa. The United Arab Emirates’s Farmer Support Program, in the same year, established traceability compliance under the National Food Security Strategy to promote local farming using modern techniques, including sustainable practices. Oman followed up with projects such as rebates for smallholder date orchard growers. These incentives collectively trimmed the organic price premium from 50% to roughly 20% and embedded GSO standards as a qualification hurdle, effectively crowding out sub-scale suppliers lacking certification. By lowering adoption risk and enforcing quality floors, subsidies are forecast to keep demand elastic even if commodity fertilizer prices moderate post-2026.

Expanding Organic Food Retail Channels

Retail visibility is translating consumer willingness to pay into upstream fertilizer pull-through. Spinneys UAE, the premium retailer, reported strong growth in 2025, driven by a 12.4% increase in gross selling area to 906,000 sq ft across 13 new stores in the United Arab Emirates and Saudi Arabia. As part of its 2030 sustainability strategy, Spinneys aimed to have 20% of its fresh produce be organic by 2025. In the same period, Carrefour focused on strengthening its private-label "Carrefour BIO" range, with over 20% of all items in-store exclusive to its private brands in some formats. The company is expanding its organic, locally sourced, sustainable produce, supported by partnerships with local farms to enhance food security. E-commerce platforms such as Kibsons and NRTC Fresh expand access for expatriates, a demographic that over-indexes in health-label purchases. With shelf positioning and direct-to-consumer models assuring stable price premiums for certified produce, growers gain confidence to shift acreage and secure organic inputs on multiyear contracts, reinforcing a virtuous demand loop for the GCC organic fertilizer market.

Rising Soil Degradation Concerns

Roughly 60% of cultivated land exhibits moderate-to-severe salinity following decades of brackish irrigation and aggressive synthetic use. Organic amendments supply humic acids, which enhance cation-exchange capacity and encourage sodium leaching. Saudi Arabia’s 2024 soil survey recorded EC above 8 decisiemens per meter in 42% of sampled date plots, prompting mandatory incorporation of 3 metric tons of organic matter per hectare to renew water subsidies. The Ministry of Agriculture, Fisheries and Water Resources is actively involved in projects to revitalize rural areas, such as the Balad Sayt Agri-Tourism project, which supports the rehabilitation and sustainable management of agricultural terraces and Aflaj systems. Subsidized labs in the United Arab Emirates automatically recommend compost when organic matter dips below 1.5%[2].Source: Food and Agriculture Organization, “Price Comparison for Fertilizers,” fao.orgThese public mandates formalize soil-health thresholds that only bona fide organic inputs can meet, embedding recurring demand even without retailer pressure.

Growing Hotel and Resort Landscaping Demand

Mega-projects embed organic inputs in procurement specs to fulfill Estidama credits, accepting premiums well above field-crop benchmarks. NEOM’s Trojena resort pre-ordered 1,200 metric tons for 6 million square meters of landscaping slated for the 2026 opening. Dubai’s Sustainable City features 11 biodome greenhouses covering over 3,000 square meters for urban farming, with a mandate to use sustainable techniques, including organic farming. Golf courses pursuing Audubon certification pay 70%-90% premiums yet still lengthen application intervals to slow the release of granules. Because hospitality budgets favor aesthetics and compliance over input-cost minimization, this channel offers suppliers superior margin and volume visibility, fortifying the GCC organic fertilizer market against commodity price shocks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited domestic organic waste collection systems | −1.2% | GCC-wide, acute in Kuwait and Bahrain | Medium term (2–4 years) |

| Price premium over synthetic fertilizers | −0.9% | Region-wide, affecting cereal and fodder growers | Short term (≤ 2 years) |

| Inconsistent nutrient content across batches | −0.6% | Regional, concentrated among small producers | Medium term (2–4 years) |

| Water-salinity amplification risk | −0.4% | Saudi Arabia and Omani arid zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Domestic Organic Waste Collection Systems

Feedstock scarcity caps production scalability. Fewer than 30% of households separate waste, with Abu Dhabi leading at 42% while Kuwait lags at 18% in 2025. Tadweer diverted 185,000 metric tons in 2025, just 22% of total organics. Riyadh’s 2024 brown-bin pilot hit 28% uptake, yet nationwide expansion faces behavioral hurdles. The feedstock deficit compels imports of date pits from Tunisia and poultry manure from India, adding USD 40-60 per metric ton in logistics costs. Bahrain landfills organic waste or ships waste to the United Arab Emirates, while Kuwait awaits a 50,000 metric ton per year Salmi composting plant, not due until 2028. Uncertain supply throttles producers' capex appetites, limiting the pace at which the GCC organic fertilizer market can satisfy latent demand.

Price Premium Over Synthetic Fertilizers

In 2025, Retail prices ranged from USD 280-420 per metric ton versus USD 180-220 per metric ton for urea and DAP, a 40-60% disadvantage that discourages large-acreage crops[3]Source: UAE Ministry of Climate Change and Environment, “Farmer Support Program,” moccae.gov.ae. The delta stems from higher collection costs, 90-180 day composting cycles, and lower nutrient density. Mid-2024 gas disruptions inflated synthetics 35%, temporarily shrinking the gap, but organics stayed sticky due to labor and infrastructure components. Subsidy schemes exclude mega-farm operators and require multi-year certification, limiting reach. RNZ Agrotech’s solar-powered aeration cut energy 40% in 2025, showing a pathway to cost parity, yet replicability across the fragmented tail remains low. Until economies of scale plus technological gains compress unit costs, adoption among cereal growers will remain marginal.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Plant Residues Anchor Market Share

Plant-based inputs accounted for 45% of the GCC organic fertilizer market share in 2025, as the GCC organic fertilizer market leveraged a large volume of annual date-palm waste. Compost derived from pits and fronds has a C: N ratio of 25-35:1, ideal for sandy soils. Animal-based products are driven by higher nitrogen (2.5-3.5% N), but regulatory scrutiny on antibiotic residues is tightening. Mineral-based organics expand at a 12.4% CAGR through 2031, appealing to high-tech farms craving consistent nutrient delivery and lower salinity. uTerra’s Soil Elixir aligns to a 15-10-10 NPK profile, reflecting a new precision ethos. Amid rising compliance costs, mineral blends could erode plant-based share, yet the need to build soil carbon ensures plant residues remain foundational to the GCC organic fertilizer market.

The segment’s strategic pivot toward traceability underscores maturation. Al-Akhawain’s blockchain ledger enables buyers to verify the origin of the fruit at the farm level. Emirates Bio Fertilizer adopted a 60:30:10 recipe, reducing nitrogen variability to below 15% and boosting credibility among greenhouse operators. Animal-based suppliers face antibiotic limits; a 2025 ADAFSA ( Abu Dhabi Agriculture and Food Safety Authority) audit flagged 18% non-compliance. Mineral-based players monetize desalination-brine feedstocks, narrowing price gaps. The interplay of soil-building benefits and precision requirements will maintain a balanced demand mix, supporting multi-source strategies across the GCC organic fertilizers industry.

By Form: Liquid Formats Gain Traction in Drip Systems

Solid granules and powders accounted for 63% of the GCC organic fertilizer market size in 2025, driven by their low cost and soil-conditioning properties. The annual application of 3-5 metric tons of compost per hectare in date orchards ensures a consistent demand. However, liquid fertilizers are projected to grow at a CAGR of 14.1% through 2031, supported by the installation of new drip irrigation systems across Saudi Arabia and the United Arab Emirates in 2025. Fertigation enables daily nutrient dosing, reducing labor requirements by 60% and minimizing volatilization losses. Debbane Agri’s seaweed-potassium blend is designed for greenhouse crops requiring feeds tailored to specific growth stages. Additionally, the regulatory standard GSO 2501 now requires solubility and suspension stability, enhancing the professionalism of the liquid fertilizer category.

Hybrid application models are gaining traction. Growers apply solid compost annually to replenish organic matter and use liquid concentrates during peak nutrient uptake periods. Suppliers are adapting by offering bundled products. For instance, Desert Oasis combines a biochar granule with a 120-day release period and a micronutrient liquid booster, capturing nutrients throughout the growing season. While solid fertilizers will continue to dominate in terms of tonnage due to their role in soil building, liquid fertilizers are anticipated to contribute more significantly to market value, as their precision dosing commands a higher price per nutrient unit within the GCC organic fertilizer market.

By Crop Type: Ornamental Turf Outpaces Field Crops

Fruits and vegetables accounted for 38% of GCC organic fertilizer market in 2025, reflecting protected cultivation’s premium input profile. Cereals accounted for a lower share given their sensitivity to price premiums. Ornamental and turf posted the fastest 11.7% CAGR during the forecast period (2026-2031) as tourism megaprojects specify organic-only inputs. NEOM alone may consume 15,000 metric tons between 2026-2028. Golf courses pay USD 450-600 per metric ton for slow-release granules, funding R&D such as biochar-enhanced products that halve application frequency.

Date-palm growers sit at the convergence of soil-salinity challenges and export premiums. Oman’s transition grant of OMR 500 (USD 1,300) per hectare for three years eases cash-flow strain. The horticulture-heavy crop mix, coupled with landscaping’s tolerance for high unit prices, positions the GCC organic fertilizer market for resilient margin growth even if cereals remain reluctant adopters. Government procurement also drives demand as Abu Dhabi targets a 20% organic share in institutional food purchases, requiring compliant farms to scale up their inputs.

Geography Analysis

Saudi Arabia dominated the 2025 market with 65% of the market value, driven by 37 million palm trees and 7,800 hectares of protected vegetables with an output of 797,000 metric tons. Vision 2030 mandates slashing synthetic imports amid amplified demand, while mega-projects such as NEOM (New region in the Northwest of Saudi Arabia) and the Red Sea require organic-only landscaping inputs. Compost capacity reached 320,000 metric tons per year, yet it satisfies only 65% of demand, underscoring the need for imports from Oman and the United Arab Emirates. Carbon-credit pilots pay SAR 80 (USD 21.3) per metric ton of CO₂e, adding upside for adopters.

Oman is the fastest-growing country at a CAGR of 9.5%, buoyed by a large volume of organic date exports fetching 30-50% price premiums in 2025. Dhofar hosts most certified farms, with input subsidies covering 30% of organic purchases. Tourism body Omran specifies organic landscaping across eco-resorts, adding 4,200 metric tons of demand through 2026. Brine-derived potassium from Barka, forecast to reach 5,000 metric tons/year by 2027, will slash import reliance and moderate local prices.

The United Arab Emirates leads in retail maturity and food-safety regulation. Abu Dhabi alone procured 8,500 metric tons of organic-compliant produce in 2025. Qatar’s Lusail landscaping consumed 2,400 metric tons over 2024-2025, while Kuwait’s latent demand awaits the 2028 Salmi compost facility. Bahrain’s small but subsidy-backed sector invested BHD 1.2 million (USD 3.2 million) to support 2,800 farms. Divergent policy maturity means cross-border trade will persist, with Saudi Arabia and the United Arab Emirates importing surplus Omani and Bahraini production to balance seasonal deficits.

Regulatory Landscape

Organic fertilizer production and trade across the GCC operate under a dual layer of requirements: a regional framework (the GCC Fertilizers and Soil Conditioners Law) and country-level licensing and registration enforced by national competent authorities. The law anchors cross-border compliance by requiring licensure for fertilizer manufacturing and oversight to ensure products meet approved specifications, pushing producers toward documented quality systems and auditable supply chains to participate in inter-GCC trade.

At the national level, Saudi Arabia regulates fertilizer plants through the Ministry of Environment, Water and Agriculture (MEWA), while the United Arab Emirates routes market access through the Ministry of Climate Change and Environment (MOCCAE), which mandates registration of fertilizers and soil conditioners for local production, import, and trade on a five-year validity cycle and requires renewals. For organic-use claims in the UAE, registration typically requires certification from an approved certifying body aligned with major organic regimes (US/EU/Japanese standards) and use of the UAE organic logo, tightening the bar for smaller suppliers and strengthening the position of producers that can maintain certification, batch documentation, and facility licensing.

Competitive Landscape

Market concentration is moderate, with the top five firms accounting for a significant share by 2025. RNZ Agrotech leads the market by utilizing solar-powered aeration technology, reducing operational expenses by 40% and securing landscaping contracts for NEOM. Emirates Bio Fertilizer Factory witnessed growth in market share after obtaining Ecocert approval, enabling access to the market with a 15% price premium. Al-Akhawain has adopted blockchain traceability to attract greenhouse clients requiring comprehensive audit trails. Mid-tier players, such as uTerra and Debbane, have diversified their offerings to include liquid fertilizers and biochar granules, catering to fertigation hubs.

Strategic initiatives are focused on technology adoption, supply chain security, and carbon monetization. Tadweer’s collaboration with Aquagrain incorporates microbial inoculation at the Liwa plant, reducing salinity and nitrogen variability. Smaller entrants are targeting niche segments, such as golf-course turf and hydroponic lettuce, where established players lack specialization. Opportunities exist in brine-derived mineral blends and ISO-certified microbial inoculants, which represent untapped potential. Patent filings in the industry remain limited (fewer than 12 between 2020 and 2025), indicating significant opportunities for innovation and defensible intellectual property within the GCC organic fertilizer market.

RNZ Agrotech Industries Ltd. maintains market leadership through its vertically integrated composting facilities located near date-palm centers. Emirates Bio Fertilizer Factory benefits from government procurement contracts for public landscaping projects. The companies' strategic approaches center on vertical integration, government partnerships, and technology implementation to differentiate their products and serve premium market segments.

Start-ups are developing microbial inoculants specifically designed for desert soils, targeting a niche but high-value market segment. Turf product manufacturers are preparing for major events, such as Saudi Arabia's 2029 Asian Winter Games. Companies are forming strategic partnerships that combine agricultural software with fertilizer sales, establishing long-term service agreements with farmers.

GCC Organic Fertilizer Industry Leaders

RNZ Agrotech Industries Ltd. (RNZ Group)

Emirates Bio Fertilizer Factory (EBFF)

Al-Akhawain (Al-Akhawain Holding)

Debbane Agri (Debbane Saikali Group)

Al Yahar Organic Fertilizers Factory

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Technology-led water and nutrient management programs are opening whitespace for higher-value organic fertilizer formats that integrate into modern farm decision systems. In June 2026, a GCC-ICARDA initiative to integrate AI and IoT into farm management (a 2026-2030 roadmap) reinforced demand for more consistent inputs that fit fertigation and data-driven application, which aligns with the market shift toward liquid formulations used through drip irrigation networks (including 48,000 hectares covered in the UAE). This raises the opportunity set for suppliers that can deliver standardized nutrient profiles, solubility, and traceable batches, particularly for protected cultivation and high-tech farms that already purchase premium inputs.

Policy momentum around circular economy and approvals also supports investment-linked opportunities in waste-to-fertilizer conversion and faster commercialization cycles. UAE Cabinet Resolution No. 67 of 2024 is referenced in the market context as supporting incentives for organic waste conversion via carbon-credit mechanisms, while MOCCAE and FAO convened a July 2026 workshop on future legislation aimed at cutting agritech licensing timelines by 50%, signaling an operating environment that rewards compliant scale-up and new formulations. Given the documented feedstock constraint (limited household waste segregation and reliance on imported organics in parts of the GCC), projects that secure municipal or commercial organic waste streams, and facilities that can certify outputs for organic farming programs, stand out as practical pathways to expand supply while meeting tighter registration and labeling expectations.

Recent Industry Developments

- June 2026: Emirates Bio Fertilizer Factory (EBFF) announced expansion of its marine algae-based organic fertilizer line into commercial-scale production. The move strengthens EBFF's position in soil conditioning and premium horticulture channels and demonstrates continued investment in specialty inputs that support sustainable agriculture in the GCC.

- August 2025: The Royal Commission for AlUla (RCU) advanced a palm-waste-to-organic-fertilizer initiative to improve soil fertility and reduce environmental impacts from waste burning, alongside rehabilitation of more than 3,000 hectares of degraded farmland. This reinforces circular-economy commitments and expands the regional supply base for organic amendments.

- May 2024: RNZ Group showcased its circular-economy manufacturing model and sulphur-enhanced fertilizer offerings produced at its Kizad facility using Thiogro technology. The emphasis on process capability and portfolio diversification signals a push toward more specialized products for salinity and soil-performance needs in arid GCC conditions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of organic fertilizers used across GCC agriculture and landscaping, counted when the input is applied to soil or crops to improve nutrient availability and soil health. The sizing is expressed in USD and covers demand across GCC countries.

Scope exclusions: We exclude conventional chemical fertilizers and we do not count on-farm raw organic waste that is not processed and sold as a fertilizer product.

Segmentation Overview

- By Source Type

- Plant-based

- Animal-based

- Mineral-based

- By Form

- Solid (Granular and Powder)

- Liquid

- By Crop Type

- Cereals and Grains

- Fruits and Vegetables

- Ornamental and Turf

- Other Crops

- By Geography

- Saudi Arabia

- United Arab Emirates

- Oman

- Qatar

- Kuwait

- Bahrain

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the GCC context and to anchor the model with measurable agriculture and trade signals, before assumptions were tested in interviews. Public sources such as FAOSTAT, UN Comtrade, national ministries of environment and agriculture in GCC countries, and customs and standards authority updates were reviewed to understand crop area, import flows, and product definitions.

We also referenced company annual reports and product catalogs, investor presentations, association websites, and trusted news coverage to map product availability and pricing patterns. Where available, paid subscriptions for company financials and intelligence, and for shipment-level import and export data, were used to cross-check volumes and supplier presence. The sources named here are illustrative rather than exhaustive, and other public documents and references were also consulted for validation and clarification.

Primary Interviews and Surveys

Primary work was used to validate what is actually purchased and applied in GCC conditions, including differences between broad-acre crops and high-value horticulture, and between farm demand and landscaping demand. We spoke with producers, distributors, agronomists, large farm operators, and institutional buyers to confirm typical application rates, form preferences (solid versus liquid), and how pricing shifts with certification and nutrient content. Regional coverage emphasized the larger demand centers while still checking smaller markets, so the final assumptions did not lean on one country only.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 15% | |

| Mid tier: 49% | Functional/Unit leaders: 38% | |

| Smaller Players: 15% | Managers: 47% |

Market-Sizing & Forecasting

The market was sized using a top-down approach where cultivation area and cropping patterns were translated into an addressable nutrient-management demand pool, and then narrowed using organic input adoption rates and typical application intensity. To keep the model grounded, we used selective bottom-up approximations, such as sampled price per ton or liter multiplied by estimated consumption for key crop groups, followed by distributor and farm channel checks.

Inputs that were tracked include GCC crop area under cereals and grains and under fruits and vegetables, policy and certification signals that affect organic use, import dependence for organic inputs, the split between solid and liquid forms, and observed average selling price ranges by nutrient concentration and pack size. Forecasting was built using scenario analysis that ties adoption and pricing to practical drivers like water-scarcity driven soil programs, landscaping project pipelines, and availability of feedstock for composting. Where supplier coverage was thin, gaps were handled by using proxy prices from comparable GCC markets and then adjusting with interview-led conversion factors to reflect local product mixes.

Data Validation & Update Cycle

Model outputs were checked against independent signals, including import trends, reported cultivation and greenhouse expansion, and the direction of pricing shared by multiple respondent groups. If any estimate looked out of range, the assumptions were revisited, and respondents were re-contacted when the variance could not be explained by seasonality or one-off projects.

Before sign-off, a second analyst review is completed to verify calculations, unit conversions, and country roll-ups. Reports are refreshed annually, and interim updates are made when material events occur, such as major policy changes or visible shifts in trade flows. Right before delivery, one more pass is done so clients receive the latest updated view.

Mordor Intelligence's Organic Fertilizer Market Gcc Market Size Measured Against Other Published Estimates

Published market values for GCC organic fertilizers can vary quite a bit, and that difference usually comes from mismatches in what each source counts, which year the source treats as the base, and how it converts volumes into USD values. Differences also show up when some models lean more on stated capacity, while others rely on observed consumption behavior.

The table shows a wide spread for 2024 to 2025, and only organic fertilizers that are commercially sold and applied in GCC are counted in Mordor Intelligence's model, with form and crop-use splits used to keep adjacent soil conditioners and general compost uses outside scope.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 120.00 M (2025) | |

| Global Consultancy A | USD 420.15 M (2024) | Uses an earlier base year and appears to apply a broader product grouping that can bundle bio-based inputs and related soil enhancers into the same value pool, which inflates the counted spend versus a product-sold definition. |

| Advisory Firm B | USD 455.80 M (2025) | Likely includes a wider set of organic residues and microbial inputs across more end-user settings, and the value build may rely on higher assumed application intensity across landscaping and institutional demand than what channel checks typically support. |

In practice, the gap is mostly explained by scope and conversion assumptions, not by a different growth direction. When product boundaries are kept clear and the price times volume logic is tied back to crop area, adoption signals, and import checks, the resulting total is easier to trace and re-run as conditions change.

Key Questions Answered in the Report

What is the projected value of the GCC organic fertilizer market by 2031?

The GCC organic fertilizer market is forecast to reach USD 203.5 million by 2031.

Which segment is growing fastest within GCC organic fertilizers?

Liquid formulations are registering a 14.1% CAGR through 2031 as drip-irrigation adoption accelerates.

Why are Omani suppliers expected to grow quickest?

Oman combines 30% input subsidies, booming organic date exports, and eco-tourism landscaping projects, driving a country-level CAGR above the GCC average.

How do desalination brine projects impact fertilizer supply?

Brine-to-fertilizer initiatives extract minerals like magnesium sulfate, adding up to 20 000 metric tons of new mineral-based organic fertilizers annually by 2027.

What quality challenges face organic fertilizer buyers?

Batch-to-batch nutrient variability exceeds 30% among small producers, prompting larger farms to favor suppliers with near-infrared spectroscopy quality control.

Page last updated on: