India Baby Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 9.92 Billion |

| Market Size (2026) | USD 10.49 Billion |

| Market Size (2031) | USD 13.89 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Baby Food Market Analysis by Mordor Intelligence

The India Baby Food Market size was valued at USD 9.92 billion in 2025 and estimated to grow from USD 10.49 billion in 2026 to reach USD 13.89 billion by 2031, at a CAGR of 5.78% during the forecast period (2026-2031). This growth trajectory reflects the convergence of demographic shifts, evolving parental preferences, and technological innovations in infant nutrition. The market's resilience stems from its essential nature, yet its expansion is increasingly driven by premiumization trends and scientific advancements in formula composition rather than volume growth alone. Premium positioning around human-milk oligosaccharides (HMOs) is lifting average selling prices as parents favor clinically validated immune benefits. The combination of rising urban birth cohorts in Asia-Pacific, renewed fertility momentum in the United States, and scientific upgrades to formula composition is driving value rather than simple volume gains. E-commerce subscriptions improve product availability for time-pressed households, while investments in aseptic packaging broaden the adoption of ready-to-feed formats. However, the pace of growth is moderated by strong cultural adherence to breastfeeding, fragmented food-safety regulations, and cold-chain bottlenecks in parts of Africa and South-East Asia.

Key Report Takeaways

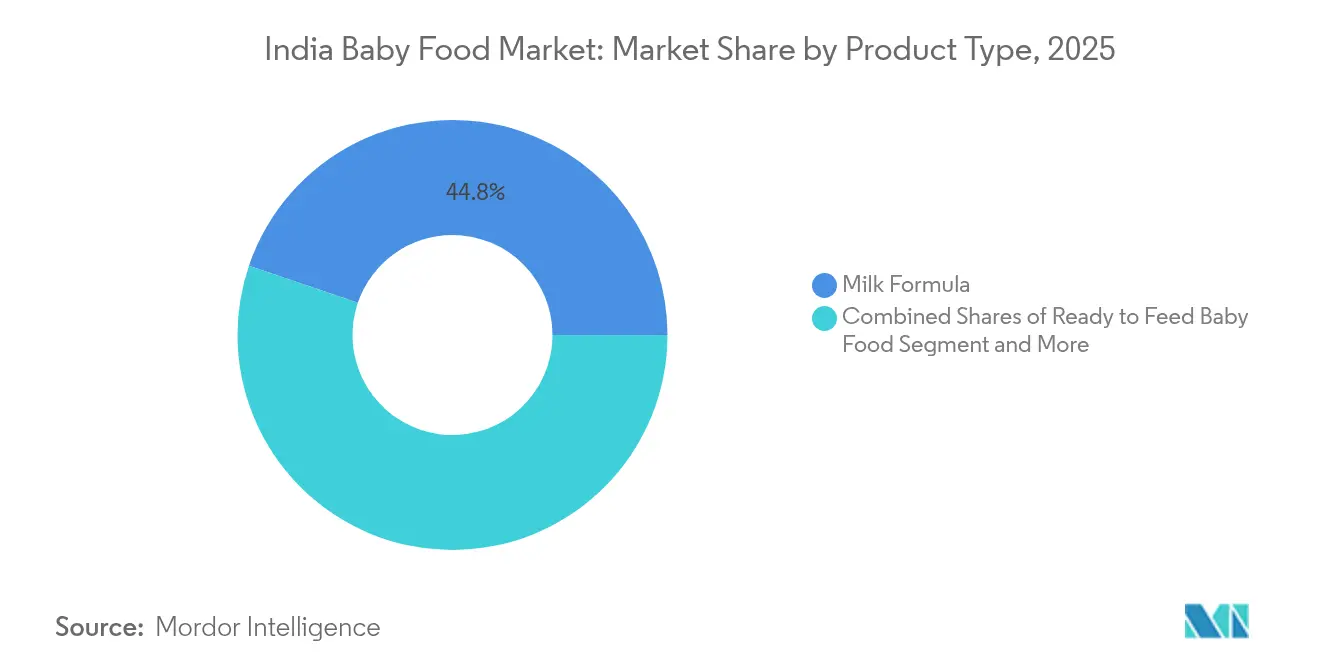

- By product type, Milk Formula led with 44.78% revenue share in 2025; Ready-to-Feed Baby Food is advancing at an 7.98% CAGR through 2031.

- By category, the Conventional segment held 85.12% of the baby food market share in 2025, whereas Organic is forecast to expand at a 7.05% CAGR to 2031.

- By product format, Powder commanded 59.48% share of the baby food market size in 2025, while Liquid Concentrate is set to grow at a 6.9% CAGR over the same period.

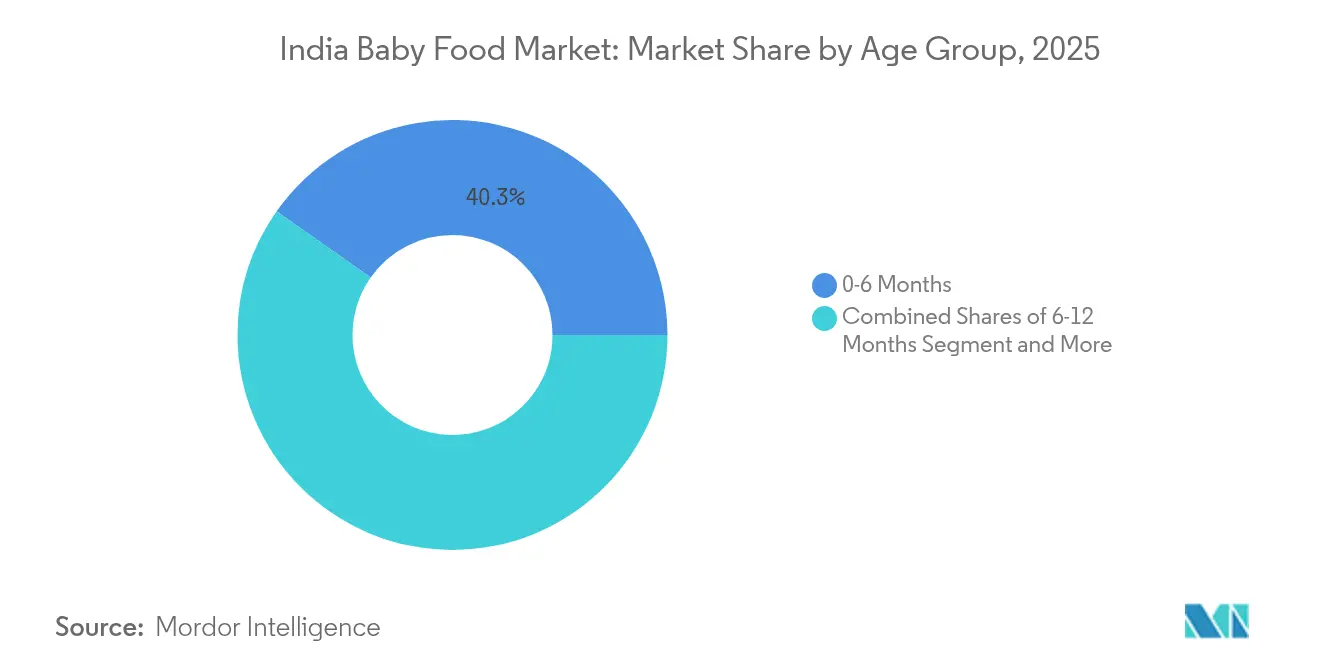

- By age-group, 0–6 Months products accounted for 40.25% of demand in 2025 and the 6–12 Months range is projected to register a 7.1% CAGR to 2031.

- By distribution channel, Supermarkets/Hypermarkets contributed 37.21% of 2025 sales; Online Retail is rising at a 7.02% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Baby Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Birth Rates Drive Growth in Baby Food Market | +0.8% | APAC (Asia-Pacific) core, spill-over to MEA, selective gains in North America | Medium term (2-4 years) |

| Premium Baby Food Segment Expands Among Affluent Families | +1.2% | Global, with concentration in North America, EU, and urban APAC | Short term (≤ 2 years) |

| Oligosaccharide Fortification Enhances Immune Benefits in Baby Formula | +0.9% | Global, led by North America and EU regulatory approvals | Long term (≥ 4 years) |

| Plant-Based Baby Food Options Meet Health-Conscious Consumer Demands | +0.7% | North America & EU primary, emerging in urban APAC | Medium term (2-4 years) |

| Ready-to-Eat Baby Food Formats Address Modern Lifestyle Needs | +1.1% | Global, strongest in urban centers across all regions | Short term (≤ 2 years) |

| E-commerce Growth Improves Access to Baby Food Products | +0.6% | Global, with accelerated adoption in APAC and MEA (Middle East and Africa) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Birth Rates Drive Growth in Baby Food Market

Demographic momentum provides fundamental support for market expansion, yet the relationship between birth rates and commercial baby food consumption reveals nuanced regional patterns. The United States experienced a 1% increase in birth rates during 2024, reversing a multi-year decline and creating renewed demand for infant nutrition products [1]Source: CDC (Centers for Disease Control and Prevention), "Birth Rates During 2024", cdc.gov. However, this demographic dividend varies significantly across geographies, with European markets like Germany and France continuing to experience fertility rate pressures despite supportive family policies. The strategic implication extends beyond raw population growth to encompass urbanization rates, as urban families demonstrate higher propensity for commercial baby food adoption compared to rural counterparts. This demographic-geographic intersection creates targeted growth opportunities for manufacturers willing to invest in localized distribution networks and culturally appropriate product formulations.

Premium Baby Food Segment Expands Among Affluent Families

Affluent consumer segments are driving market value growth through willingness to pay substantial premiums for perceived health benefits and convenience features. Deloitte's 2024 India FMCG report revealed that 67% of urban consumers express readiness to pay premium prices for health-focused baby nutrition products, with organic and fortified options commanding price premiums of 30-50% over conventional alternatives. This premiumization trend extends beyond organic certification to encompass functional ingredients, specialized formulations, and sustainable packaging. The strategic challenge for manufacturers lies in balancing premium positioning with accessibility, as excessive price differentiation risks creating market segmentation that limits overall penetration rates. Market research indicates that manufacturers are responding by introducing mid-tier premium products that incorporate select premium features while maintaining more moderate price points. Consumer surveys demonstrate that brand trust and clinical validation of health claims remain crucial factors in parents' willingness to pay premium prices, with 82% of respondents citing scientific evidence as a key purchase criterion.

Oligosaccharide Fortification Enhances Immune Benefits in Baby Formula

Scientific advances in human milk oligosaccharide (HMO) research are revolutionizing formula composition and creating competitive differentiation opportunities. Clinical studies published in 2024 demonstrated that 2'-fucosyllactose (2'-FL) supplementation in infant formula significantly reduces infection rates and supports immune system development comparable to breastfeeding benefits. Abbott, Nestlé, and other major manufacturers have accelerated HMO integration across their product portfolios, with some premium formulas now containing multiple HMO types. The regulatory approval process for novel HMO compounds creates temporary competitive moats for early adopters, yet the underlying science suggests that HMO fortification will become standard practice rather than premium differentiator within the forecast period. Research institutions and formula manufacturers are investing heavily in identifying and synthesizing additional HMO compounds that could further enhance infant nutrition and immune protection. The growing body of evidence supporting HMO benefits has prompted regulatory bodies worldwide to streamline approval processes for HMO-enriched infant formula products.

Plant-Based Baby Food Options Meet Health-Conscious Consumer Demands

Environmental consciousness and dietary preferences are driving innovation in plant-based infant nutrition, though regulatory hurdles and nutritional completeness requirements limit rapid market penetration. Danone launched a dairy-plant protein blend formula in European markets during 2024, targeting parents seeking reduced environmental impact without compromising nutritional adequacy. Australian company Sprout Organic has expanded its plant-based baby food portfolio, though regulatory frameworks in most jurisdictions require extensive clinical validation for plant-based formula alternatives. The strategic opportunity lies in complementary foods and weaning products where regulatory barriers are lower, allowing manufacturers to establish plant-based credentials before addressing formula market segments. Companies are investing significantly in research and development to overcome the technical challenges of matching breast milk's nutritional profile using plant-based ingredients. Market research indicates that parents are increasingly willing to pay premium prices for environmentally sustainable infant nutrition products that maintain optimal nutritional standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Traditional Breastfeeding Practices Impact Market Growth and Development | -1.4% | Global, strongest impact in developing regions and rural areas | Long term (≥ 4 years) |

| Regional Food Safety Standards Create Complex Regulatory Environment | -0.8% | Global, with varying intensity across regulatory jurisdictions | Medium term (2-4 years) |

| Storage and Refrigeration Infrastructure Challenges Affect Market Distribution | -0.6% | Primarily developing markets in APAC, MEA, and Latin America | Long term (≥ 4 years) |

| Rural Markets Show Low Adoption of Packaged Baby Foods | -0.9% | Global rural areas, concentrated in APAC and MEA regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Traditional Breastfeeding Practices Impact Market Growth and Development

Cultural preferences for breastfeeding, supported by WHO recommendations and healthcare advocacy, create fundamental constraints on commercial baby food market expansion. WHO guidelines emphasize exclusive breastfeeding for the first six months, with continued breastfeeding alongside complementary foods until 24 months or beyond [2]Source: WHO (World Health Organization), "Infant and young child feeding", who.int. Research published in developing countries indicates that traditional feeding practices remain deeply embedded in cultural norms, with commercial baby food adoption primarily occurring in urban, educated, and higher-income households. This cultural resistance extends beyond initial feeding decisions to encompass skepticism about processed foods and preference for home-prepared meals. The strategic challenge for manufacturers involves positioning products as complementary to breastfeeding rather than replacement options, requiring sensitive marketing approaches and healthcare professional engagement.

Regional Food Safety Standards Create Complex Regulatory Environment

Divergent regulatory frameworks across jurisdictions create compliance costs and market entry barriers that constrain industry growth and innovation speed. The complexity extends from ingredient approval processes to labeling requirements, manufacturing standards, and import/export procedures. FDA regulations in the United States require extensive clinical validation for new formula ingredients, while FSSAI standards in India emphasize different nutritional parameters and local sourcing requirements [3]Source: FSSAI, "Nutritional parameters and local sourcing requirements", fssai.gov.in. These regulatory variations force manufacturers to maintain multiple product formulations and compliance systems, increasing operational complexity and reducing economies of scale. The fragmented regulatory landscape also delays innovation adoption, as companies must navigate sequential approval processes across key markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Formula Innovation Drives Market Evolution

Milk Formula maintains its dominant position with 44.78% market share in 2025, reflecting its essential role in infant nutrition, yet Ready-to-Feed Baby Food emerges as the fastest-growing segment with 7.98% CAGR through 2031. This growth differential illustrates the market's evolution toward convenience-oriented solutions that address modern parenting challenges. Ready-to-feed formats eliminate preparation errors and contamination risks while providing portion control benefits that resonate with health-conscious parents. Clinical evidence supporting HMO fortification has strengthened milk formula's scientific credibility, with major manufacturers investing heavily in research-backed formulations that command premium pricing.

Dried Baby Food products serve specialized dietary needs and storage requirements, particularly in regions with limited refrigeration infrastructure, while Other Product Types encompass emerging categories like plant-based alternatives and specialized therapeutic formulations. The strategic shift toward functional ingredients and personalized nutrition creates opportunities for product differentiation beyond traditional categories. Abbott's introduction of HMO-enhanced formulas and Danone's dairy-plant protein blends exemplify how manufacturers are expanding beyond conventional product boundaries to capture evolving consumer preferences.

By Category: Organic Acceleration Reshapes Market Dynamics

The Conventional category commands 85.12% market share in 2025, demonstrating its continued relevance for price-sensitive consumers, while Organic products accelerate at 7.05% CAGR, driven by affluent families prioritizing perceived health benefits and environmental considerations. This growth disparity reflects deepening market segmentation where premium-positioned organic products capture disproportionate value despite limited volume share. Organic certification requirements create supply chain complexities and cost structures that support higher margins, yet regulatory standards vary significantly across jurisdictions, complicating global product strategies.

Consumer research indicates that organic baby food purchases often represent gateway decisions toward broader organic household adoption, creating strategic value beyond immediate category sales. The challenge lies in organic ingredient sourcing scalability, as demand growth outpaces certified organic agricultural capacity in many regions. Manufacturers are investing in vertical integration and supplier development programs to secure organic ingredient supplies while maintaining quality standards and cost competitiveness.

By Product Format: Liquid Convenience Gains Momentum

Powder format maintains dominance with 59.48% market share in 2025, benefiting from cost efficiency, extended shelf life, and transportation advantages, yet Liquid Concentrate accelerates at 6.9% CAGR as convenience preferences reshape purchasing decisions. Powder's market leadership reflects its practical benefits for bulk purchasing and storage, particularly important for families with multiple children or limited shopping frequency. However, liquid formats eliminate preparation steps and reduce contamination risks, appealing to time-constrained parents and premium market segments.

The format preference varies significantly by geographic region and income level, with liquid formats achieving higher penetration in developed markets where convenience premiums are acceptable. Packaging innovation in liquid formats, including shelf-stable technologies and portion-controlled packaging, addresses traditional limitations while maintaining nutritional integrity. Manufacturing investments in aseptic processing and packaging capabilities enable liquid format expansion, though capital requirements favor larger manufacturers with scale advantages.

By Age-Group: Early Months Drive Volume, Weaning Accelerates Growth

The 0-6 Months segment captures 40.25% market share in 2025, reflecting the critical importance of early infant nutrition, while the 6-12 Months segment grows fastest at 7.1% CAGR as weaning food innovation expands market opportunities. This age-based segmentation reveals distinct nutritional requirements and consumption patterns that manufacturers address through specialized formulations and packaging formats. The early months segment primarily consists of formula products with stringent regulatory requirements and limited differentiation opportunities beyond functional ingredients.

Weaning-age segments benefit from greater product variety and innovation potential, including texture progression, flavor introduction, and cultural adaptation opportunities. The 12-24 Months and 24-36 Months segments represent transition periods where commercial products compete directly with home-prepared foods, requiring value propositions that emphasize convenience, nutrition, and safety. Regulatory frameworks like FSSAI guidelines for complementary feeding create standardization requirements while allowing innovation in delivery formats and ingredient combinations.

By Distribution Channel: Digital Transformation Reshapes Retail

Supermarkets/Hypermarkets maintain 37.21% market share in 2025, leveraging their broad reach and trusted retail environment, yet Online Retail accelerates at 7.02% CAGR as digital commerce transforms baby food purchasing behaviors. Traditional retail channels benefit from immediate product availability and face-to-face consultation opportunities, particularly important for first-time parents seeking guidance and reassurance. However, online platforms enable subscription services, bulk purchasing discounts, and access to specialized products unavailable in physical stores.

Drugstores/Pharmacies serve specialized roles in formula distribution, particularly for therapeutic and hypoallergenic products requiring healthcare professional recommendations. Convenience Stores address immediate needs and emergency purchases, though their limited shelf space restricts product variety. The strategic challenge for manufacturers involves optimizing channel mix to balance reach, margins, and brand positioning while adapting to evolving consumer shopping preferences. E-commerce growth creates direct-to-consumer opportunities that bypass traditional retail margins while enabling data collection and personalized marketing approaches.

Geography Analysis

Regional market dynamics reflect the intersection of demographic trends, economic development, and cultural preferences, creating distinct growth opportunities and challenges across geographic segments. Asia-Pacific emerges as the primary growth engine, driven by rising birth rates, urbanization, and increasing disposable income in countries like India and Indonesia. The region benefits from large population bases and expanding middle-class segments willing to invest in premium infant nutrition products. However, traditional feeding practices and regulatory complexities create market entry barriers that require localized strategies and long-term investment commitments.

North America and Europe represent mature markets with stable demand patterns and premium product preferences, where growth depends on innovation, premiumization, and market share capture rather than category expansion. These regions lead in organic product adoption and functional ingredient integration, setting global trends that manufacturers adapt for emerging markets. Regulatory frameworks in developed markets often serve as templates for emerging market standards, creating competitive advantages for companies with established compliance capabilities. The strategic focus shifts toward value creation through product differentiation and direct-to-consumer channels that capture higher margins.

Latin America, Middle East, and Africa present emerging opportunities characterized by improving economic conditions and evolving consumer preferences, yet infrastructure limitations and regulatory uncertainties create implementation challenges. These regions require patient capital investment and partnership strategies that address local market conditions while building long-term competitive positions. Cold chain infrastructure development and retail channel expansion represent critical success factors that manufacturers must address through strategic partnerships and direct investment. The potential for rapid growth in these regions attracts increasing manufacturer attention, though execution complexity requires specialized regional expertise and risk management capabilities.

Competitive Landscape

The baby food market exhibits moderate concentration with established multinational corporations maintaining dominant positions while emerging brands capture niche segments through innovation and specialized positioning. Market leaders like Nestlé, Abbott, and Danone leverage scale advantages in research and development, regulatory compliance, and global distribution networks to maintain competitive moats. These companies invest heavily in quality control measures and safety protocols to maintain consumer trust and regulatory compliance. Their established manufacturing facilities and extensive supplier relationships create significant barriers to entry for new competitors.

However, the industry's moderate concentration indicates opportunities for disruption, particularly in premium segments and emerging markets where consumer preferences are evolving rapidly. Strategic patterns reveal increasing focus on functional ingredients, direct-to-consumer channels, and geographic expansion into high-growth emerging markets. The rise of health-conscious parenting has created new opportunities for brands offering organic and natural ingredients. Regional players are gaining market share by adapting products to local tastes and cultural preferences.

Technology adoption centers on manufacturing efficiency, supply chain optimization, and digital marketing capabilities that enable personalized consumer engagement. Patent filings in HMO research and plant-based formulations indicate the innovation battlegrounds where companies seek competitive differentiation. Emerging disruptors like ByHeart and various plant-based startups challenge established players by targeting specific consumer segments with specialized value propositions, forcing industry leaders to accelerate innovation cycles and consider acquisition strategies to maintain market position. Advanced analytics and artificial intelligence are increasingly employed to predict consumer behavior and optimize product development. Companies are also investing in sustainable packaging solutions and transparent supply chain practices to meet growing environmental concerns.

India Baby Food Industry Leaders

-

Nestlé S.A.

-

Danone

-

Abbott

-

Amway

-

Reckitt Benckiser Group PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Nestle India launched 14 variants of its baby food brand Cerelac without refined sugar. This development follows a global controversy regarding the company's practice of adding sugar to its baby food products in developing South Asian countries, including India. The company reports that it has decreased added sugar content by 30% in its products over the past five years.

- August 2024: Baby food startup brand Babe Burp funded INR 8 crore in a pre-series in collaboration with a venture capital fund, Gruhas Collective Consumer Fund. The purpose of this collaboration was to innovate baby food products.

- January 2024: Danone India strengthened its toddler nutrition portfolio with the national launch of AptaGrow. The product addresses nutritional requirements of children aged 3-6 years by providing 37 nutrients, including a prebiotic blend that enhances the absorption of vital nutrients supporting growth, brain development, and immunity.

India Baby Food Market Report Scope

Baby food is any soft, easily digestible meal created particularly for human babies aged 4-6 to two years old. The baby food market is segmented by category, product type, distribution channel, and geography. By category, the market is segmented into organic and conventional. By product type, the market is segmented into milk formula, dried baby food, ready-to-eat baby food, and other product types. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, pharmacies/drug stores, online retail stores, and other distribution channels. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Milk Formula |

| Ready to Feed Baby Food |

| Dried Baby Food |

| Other Product Type |

| Organic |

| Conventional |

| Powder |

| Liquid Concentrate |

| 0–6 Months |

| 6–12 Months |

| 12–24 Months |

| 24–36 Months |

| Supermarkets / Hypermarkets |

| Drugstores / Pharmacies |

| Convenience Stores |

| Online Retail |

| Other Distribution Channel |

| By Product Type | Milk Formula |

| Ready to Feed Baby Food | |

| Dried Baby Food | |

| Other Product Type | |

| By Category | Organic |

| Conventional | |

| By Product Format | Powder |

| Liquid Concentrate | |

| By Age-Group | 0–6 Months |

| 6–12 Months | |

| 12–24 Months | |

| 24–36 Months | |

| By Distribution Channel | Supermarkets / Hypermarkets |

| Drugstores / Pharmacies | |

| Convenience Stores | |

| Online Retail | |

| Other Distribution Channel |

Key Questions Answered in the Report

How fast is the baby food market expected to grow between 2026 and 2031?

It is projected to advance at a 5.78% CAGR, lifting value from USD 10.49 billion to USD 13.89 billion by 2031.

Which product segment is expanding the quickest?

Ready-to-Feed Baby Food is forecast to grow at an 7.98% CAGR on the back of convenience and aseptic-packaging adoption.

Why are HMOs important in infant formula?

Clinical studies show that adding HMOs such as 2'-FL strengthens infants’ immune defenses, making formula nutrition closer to breastmilk.

What role is e-commerce playing in baby food sales?

Online Retail is rising at a 7.02% CAGR as subscription services and rapid-delivery options improve access and loyalty.

Page last updated on: