Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

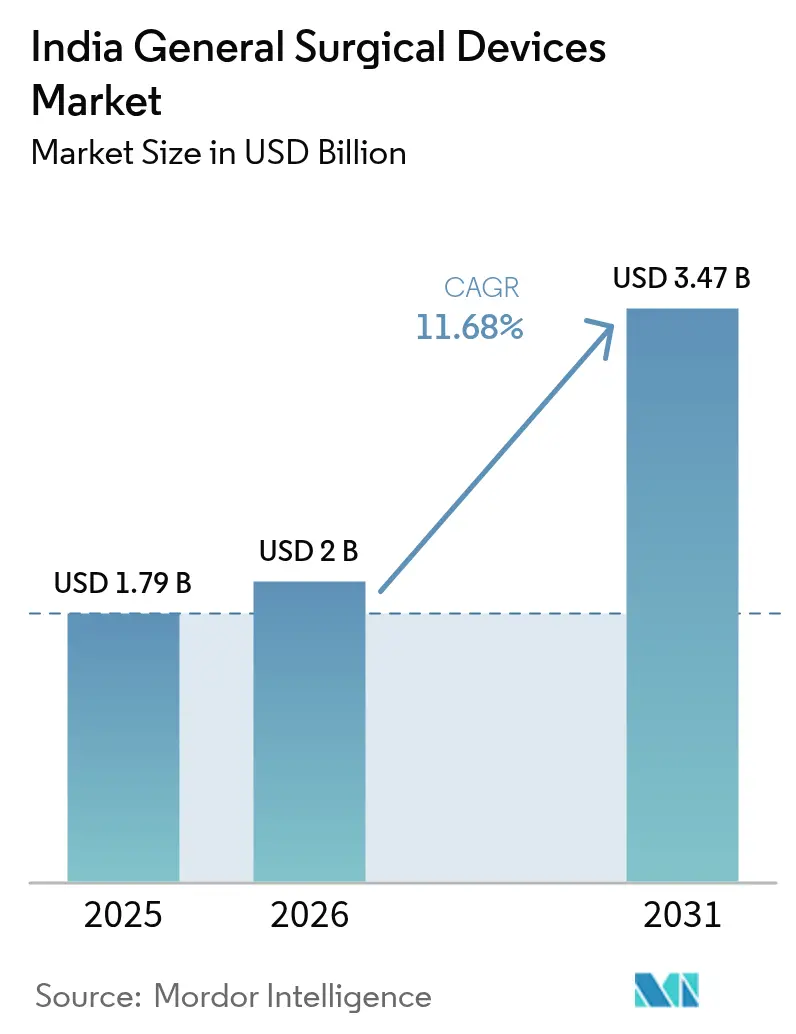

| Base Year Market Size (2025) | USD 1.79 Billion |

| Market Size (2026) | USD 2 Billion |

| Market Size (2031) | USD 3.47 Billion |

| Growth Rate (2026 - 2031) | 11.68% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India General Surgical Devices Market Analysis by Mordor Intelligence

The India General Surgical Devices Market size is expected to grow from USD 1.79 billion in 2025 to USD 2 billion in 2026 and is forecasted to reach USD 3.47 billion by 2031 at 11.68% CAGR over 2026-2031.

Momentum is driven by rising procedure volumes, policy-backed manufacturing incentives, and the rapid shift to minimally invasive techniques in both public and private hospitals. The Production Linked Incentive (PLI) scheme has already unlocked USD 411 million for 22 greenfield plants, trimming the sector’s historic 70-85% import dependence and fostering local capacity. Simultaneously, Ayushman Bharat’s expansion to 550 million beneficiaries and an 11% hike in Union Budget health allocations are channeling funding toward cost-efficient consumables in tier-2 and tier-3 districts. Multinational incumbents defend premium laparoscopic and energy platforms through surgeon training and service footprints, yet domestic manufacturers are scaling fast on cost leadership and export-oriented capacity. Overall, the Indian general surgical devices market continues to benefit from technology upgrades, chronic-disease-linked demand, and progressively supportive regulation.

Key Report Takeaways

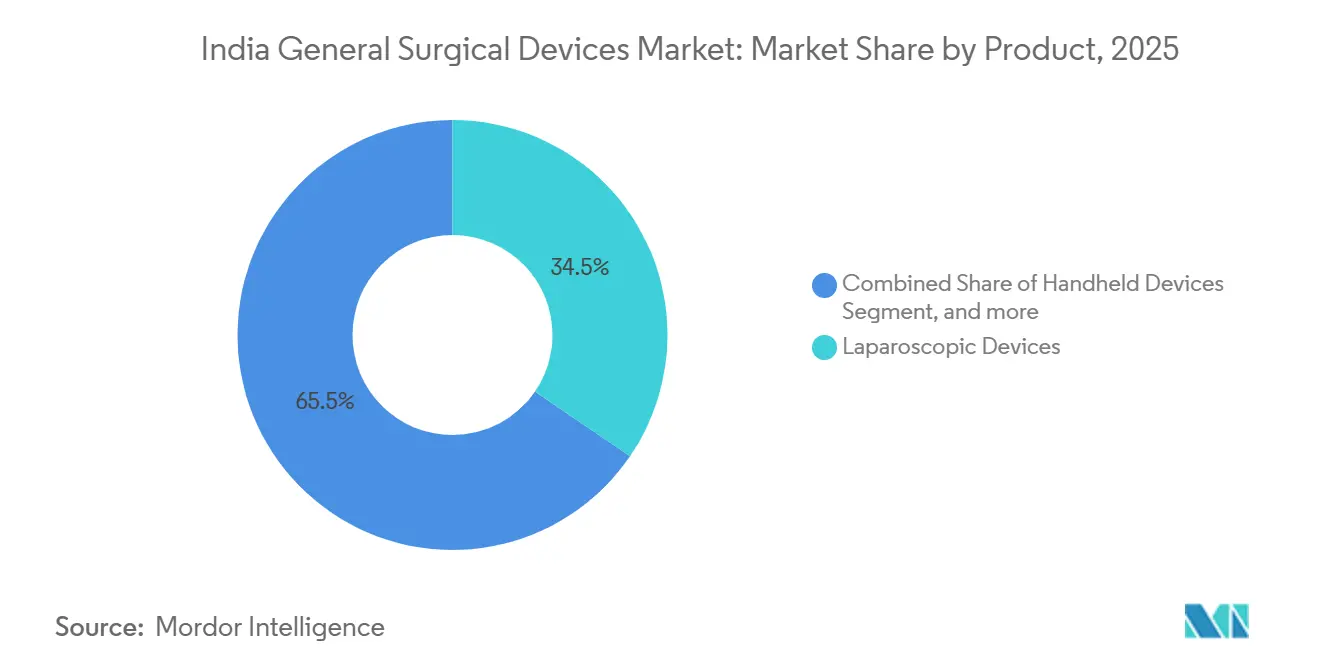

- By product, laparoscopic devices led with a 34.54% share of the India general surgical devices market in 2025. Electrosurgical devices are forecast to register the fastest growth, advancing at a 12.44% CAGR to 2031.

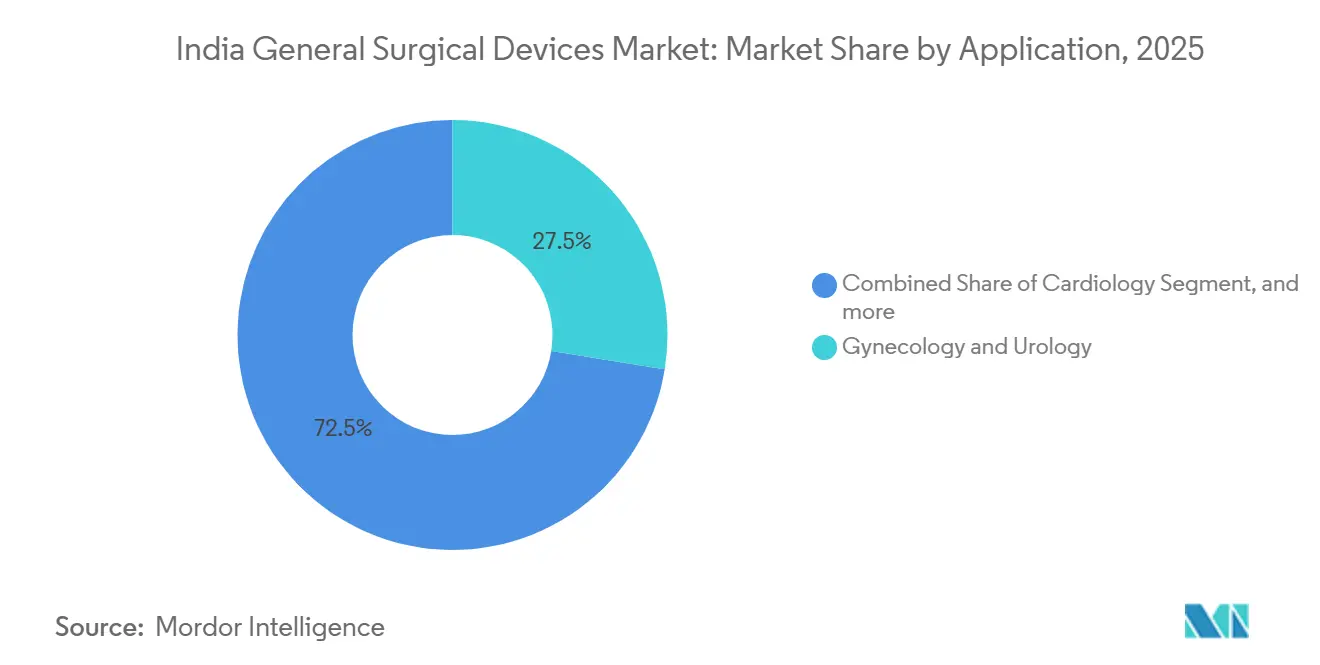

- By application, gynecology & urology accounted for 27.54% of the India general surgical devices market size in 2025. Gastro-intestinal & hepato-biliary interventions are projected to expand at a 13.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India General Surgical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | % (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological Advancements in Surgical Devices | +2.1% | Metro hospitals in Delhi, Mumbai, Bangalore, Chennai | Medium term (2-4 years) |

| Increasing Surgical Procedure Volumes | +2.5% | High-enrollment PMJAY states: Uttar Pradesh, Bihar, Rajasthan | Short term (≤ 2 years) |

| Government Healthcare Financing Expansion | +1.8% | Tier-2/3 cities benefitting from Ayushman Bharat scale-up | Long term (≥ 4 years) |

| Growth of Private Healthcare Infrastructure | +2.0% | Tier-1 hubs and medical-tourism corridors in Kerala and Tamil Nadu | Medium term (2-4 years) |

| Rising Medical Tourism Inflows | +1.2% | Delhi-NCR, Chennai, Mumbai, Bangalore | Medium term (2-4 years) |

| Escalating Burden of Chronic Diseases | +1.9% | Urban clusters where NCDs drive 68% of mortality | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Technological Advancements in Surgical Devices

Robotic assistants and energy-based sealing systems continue to elevate precision and shorten recovery times, though their rollout hinges on capital affordability and surgeon training rather than device efficacy. Medtronic introduced the LigaSure Maryland Jaw in 2025 to expand access to energy-based hemostasis across oncology and bariatric centers. Home-grown robotic platform SSI Mantra demonstrated outcomes comparable to those of da Vinci systems in a 2026 multi-center study, providing public teaching hospitals with a lower-cost pathway to minimally invasive capability. Johnson & Johnson cut maximum retail prices for key Ethicon staplers by 6-7% in September 2025, an aggressive step to defend share as PLI-backed Indian producers scale up. Infection-control mandates are nudging hospitals toward single-use instruments, yet cash-strapped facilities still rely on reusables, creating a dual-tiered demand profile. Overall, product innovation raises procedural safety but magnifies the need for training and financing solutions to unlock nationwide adoption.

Increasing Surgical Procedure Volumes

India performs roughly 1,385 surgeries per 100,000 population, far below the global benchmark of 5,000, indicating an unmet need of nearly 49 million operations annually. Within Ayushman Bharat, 65% of reimbursed procedures are surgical, and 82% of empaneled hospitals provide operative care. Rising cancer diagnoses—1.41 million new cases in 2022 led by breast, oral, and cervical tumors—are amplifying demand for resection instruments and wound-closure products[1]Indian Council of Medical Research, “GLOBOCAN 2022 India Factsheet,” icmr.gov.in. Private networks continue to add operating capacity, particularly in bariatric, geriatric, and cosmetic services, driving incremental sales of laparoscopic towers, energy devices, and closure systems. Despite overall growth, gender and rural-urban disparities persist, underlining the need for outreach and surgeon-training programs to match device availability with patient demand.

Government Healthcare Financing Expansion

Public health spending rose to INR 99,859 crore in Budget 2025-26, and Ayushman Bharat now covers 550 million residents. Out-of-pocket expenditure fell from 48.8% in 2019 to 39.4% in 2024, stabilizing demand for mid-tier consumables. Three centrally approved medical-device parks enable plug-and-play facilities, while the PRIP scheme set aside INR 5,000 crore for R&D, lowering entry barriers for innovation. Yet a nationwide review showed that many public facilities lack functional operating theaters or face maintenance backlogs, proving that funding alone cannot close the care gap without parallel investments in workforce and infrastructure. Still, broader insurance coverage is steadily channeling predictable volumes into both government and empaneled private hospitals, reinforcing the India general surgical devices market’s long-term growth.

Growth of Private Healthcare Infrastructure

Private hospital chains are pushing into tier-2 and tier-3 cities where rising incomes meet limited public capacity. New sites emphasize day-surgery models and Enhanced Recovery After Surgery protocols that favor minimally invasive instruments. Leading groups are also pooling procurement via group-buying organizations, rewarding vendors with broad catalogs and dependable after-sales service. Although formal investment figures remain confidential, expansion pipelines from Apollo, Fortis and Max signal steady demand for laparoscopic and energy platforms. These networks increasingly standardize product suites to negotiate sharper pricing, pushing suppliers to balance margin with volume in the India general surgical devices market.

Restraints Impact Analysis*

| Restraint | % (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pricing Controls and Reimbursement Delays | -1.4% | Public procurement and PMJAY hospitals nationwide | Short term (≤ 2 years) |

| High Import Dependence | -1.1% | More acute in tier-2/3 cities with thin distributor networks | Medium term (2-4 years) |

| Skill Gap Among Surgical Workforce | -0.9% | Pronounced in rural and northeastern regions | Long term (≥ 4 years) |

| Regulatory and Compliance Challenges | -0.7% | Smaller manufacturers and new entrants across India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pricing Controls and Reimbursement Delays

The National Pharmaceutical Pricing Authority has capped select implant prices and signals readiness to include more devices, compressing margins for premium lines. Under Ayushman Bharat, reimbursements often take 60-90 days to clear, stretching distributors' working capital and prompting hospitals to demand longer payment windows from suppliers. Johnson & Johnson’s 2025 price cuts reflect the need for aggressive tactics to retain volume in a cost-sensitive environment. Domestic producers compete on list prices 20-30% lower, but smaller firms lack the scale economies to survive a prolonged squeeze. Fragmented state reimbursement packages further complicate nationwide launch strategies within the India general surgical devices market.

High Import Dependence and Supply Vulnerability

India imported USD 237.86 million worth of surgical instruments in fiscal 2024-25, up 28.53% year on year; the United States, China and Germany together supplied 45% of that total[2]International Trade Administration, “India Medical Devices Market Snapshot 2025,” ita.doc.gov. Heavy reliance on foreign sources exposes buyers to currency fluctuations and geopolitical risks. A January 2025 CDSCO memo banning the import of refurbished devices safeguards patient safety but curtails a low-cost channel for capital equipment in budget-restricted hospitals. While PLI incentives spur new Indian capacity, advanced electrosurgical generators, robotic systems, and specialty laparoscopic tools still depend on imported sub-assemblies. Building a local component ecosystem and securing medical-grade raw materials remain top priorities to de-risk the India general surgical devices industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Minimally Invasive Platforms Drive Differentiation

Laparoscopic devices commanded 34.54% of the Indian general surgical devices market share in 2025, reflecting their broad use across gynecological and gastrointestinal surgeries. Electrosurgical devices are on track to post a 12.44% CAGR to 2031 as energy-based sealing becomes standard in oncologic and vascular cases. Trocars and access devices benefit from the shift toward single-use designs, while wound-closure items stay volume-driven and price-competitive. Handheld instruments remain commoditized, and ancillary equipment, such as smoke evacuators, rides on the laparoscopic growth. Domestic plants funded by PLI are already supplying endo-surgery lines, but multinationals still dominate premium imaging and robotic-assisted systems, where intellectual property and capital intensity deter new entrants.

Electrosurgical generators are gaining momentum as precise hemostasis reduces blood loss and operating time. Medtronic’s LigaSure launch and Johnson & Johnson’s strategic price adjustments sharpen competition. CDSCO’s clarified sterilization guidelines may help speed approvals for disposable electrodes and vessel-sealer tips, expanding local supply. Overall, minimally invasive platforms remain the critical battleground shaping future revenues in the India general surgical devices market.

By Application: Oncologic and Metabolic Procedures Accelerate

Gynecology & urology held 27.54% of value in 2025, buoyed by high-volume hysterectomies and prostatectomies. Meanwhile, gastrointestinal & hepato-biliary surgeries are projected to grow 13.21% annually through 2031, propelled by rising colorectal and liver cancer incidence. Cardiac, orthopedic, and neurologic applications demand specialized instruments, but volumes and device intensity vary. Oncology’s shift to minimally invasive esophagectomy and colorectal resection aligns with private-hospital incentives to shorten stays and improve throughput, bolstering uptake of advanced staplers and energy devices. Ayushman Bharat funding for cancer surgeries underpins sustained public-sector demand, though reimbursement caps press manufacturers to offer tiered portfolios. Gynecology’s large installed base ensures steady consumable demand, while bariatric and metabolic procedures offer upside as obesity prevalence rises and insurance coverage broadens. Collectively, application diversity spreads revenue risk and keeps the India general surgical devices market resilient to single-segment volatility.

Regulatory Landscape

General surgical devices in India are regulated under the Drugs and Cosmetics Act, 1940 and the Medical Devices Rules (MDR), 2017, administered by the Central Drugs Standard Control Organisation (CDSCO). The MDR uses a risk-based classification system (Class A to D) that determines licensing, clinical evidence, and post-market obligations, and in practice it shapes time-to-market and compliance costs for laparoscopic, electrosurgical, and wound-closure portfolios.

On standards and market access, the Bureau of Indian Standards (BIS) anchors conformance pathways for surgical instruments (including MHD committees) and aligns multiple specifications with ISO references, including material and corrosion-resistance related standards. Public procurement preferences under the Public Procurement (Preference to Make in India) Order, alongside the sector push under the National Medical Devices Policy (as referenced in government policy communications), reinforces localization, affecting tender eligibility, documentation, and supplier selection for hospitals buying high-volume surgical consumables through formal procurement channels.

Value Chain Analysis

The India general surgical devices value chain runs from raw materials and components (medical-grade steels and polymers, electronics for electrosurgery, and imaging sub-assemblies for minimally invasive platforms) to device design and manufacturing. Production is often split between domestic plants for consumables and imported high-end systems, with quality systems built around MDR 2017 requirements. Licensing and oversight vary by risk class, with CDSCO acting as the Central Licensing Authority for higher-risk devices and State Licensing Authorities covering many Class A and B manufacturing sites, making regulatory readiness and documentation a key upstream gate before commercialization.

Downstream, the channel mix includes direct sales to large private chains and importers/distributors serving a broader hospital base, including Ayushman Bharat-empaneled facilities where working-capital cycles can be constrained by reimbursement timing. Medical device parks and cluster-led infrastructure programs supported by the Government of India improve access to common utilities, testing, and logistics. At the qualification stage, BIS/ISO-aligned standards and public procurement localization preferences influence supplier eligibility and tender competitiveness across surgical instruments, laparoscopic kits, and single-use accessories.

Competitive Landscape

Metro clusters—Delhi-NCR, Mumbai, Bangalore, Chennai, and Hyderabad—contribute a disproportionate share of the Indian general surgical devices market due to dense private-hospital networks, surgeon expertise, and higher patient spending power. However, Ayushman Bharat financing is pushing incremental growth into tier-2 and tier-3 districts across Uttar Pradesh, Bihar, Rajasthan, and Madhya Pradesh, where procedure volumes are starting from a low base. The 176,500 operational Ayushman Arogya Mandirs illustrate their geographic reach, yet only 28% of amenable surgeries in the northeast used laparoscopy, compared with more than 50% in southern states like Tamil Nadu and Kerala[3]Ministry of Health and Family Welfare, “16th Common Review Mission Report,” mohfw.gov.in. Medical-tourism inflows cluster in Delhi-NCR, Chennai, and Mumbai, driving demand for FDA- and CE-cleared devices at premium price points.

Southern states host mature device-manufacturing corridors and medical technology parks, easing supply chain logistics. Western states—Maharashtra and Gujarat—benefit from PLI-funded plants, such as Meril’s USD 109 million expansion in Vapi that targets endo-surgery and orthopedic implants. Northern and eastern regions confront surgeon shortages and thin distributor coverage, yet represent substantial untapped volume as hospitals expand. Private chains are therefore accelerating site launches outside metros, tailoring product mixes to local affordability and investing in onsite training. Over the next five years, regional growth will diversify revenue sources for the India general surgical devices market, though metro centers will retain technological leadership and premium demand.

India General Surgical Devices Industry Leaders

Conmed Corporation

Boston Scientific Corporation

Johnson & Johnson

B. Braun SE

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Import substitution remains a clear whitespace across advanced general surgical device categories where India still relies heavily on overseas suppliers, and recent policy actions add execution pathways for manufacturers moving beyond basic consumables. In June 2026, the Department of Pharmaceuticals initiated applications for two support measures: the Marginal Investment Scheme for Reducing Import Dependence (capital subsidy up to INR 10 crore) and the Medical Device Clinical Studies Support Scheme (support up to INR 5 crore), with a July 23, 2026 submission deadline. These schemes target two recurring bottlenecks for general surgical devices, capex for scale-up and clinical evidence generation for regulated product lines, and create a structured on-ramp for firms pursuing electrosurgical systems, stapling platforms, and minimally invasive accessory lines.

Procurement and investment signals also reinforce opportunities tied to localized supply and deeper tier-2 and tier-3 penetration. The Government of India maintains a Global Tender Enquiry (GTE) Exemption List (354 medical devices, under periodic review with a July 15, 2026 suggestion deadline), which can expand accessible volumes for qualifying domestic manufacturers in public buying. On the private-capital side, April 2026 reporting on Jashvik Capital expanding its Futura Medtech platform through an investment in Rivarp Medical points to ongoing interest in scaling Indian device manufacturing capabilities. While Rivarp is not limited to general surgery, the transaction supports broader medtech capacity building that can spill into surgical categories through shared manufacturing, quality systems, and distribution infrastructure.

Recent Industry Developments

- July 2026: The Delhi High Court granted a permanent injunction and awarded about INR 3.34 crore in damages to Johnson & Johnson in a case involving counterfeit surgical devices bearing trademarks such as Surgicel, Ligaclip, and Ethicon. The judgment reinforces anti-counterfeit enforcement in surgical consumables, strengthening brand protection and patient-safety positioning in hospital procurement.

- December 2025: Healthium Medtech acquired a controlling stake in Paramount Surgimed, which manufactures and exports surgical blades, scalpels, and dermal biopsy products. The deal broadens Healthium's portfolio in high-volume surgical consumables and supports scale in distribution and export channels.

- September 2024: Stryker launched its 1788 Advanced Imaging Platform in India for surgical visualization. Upgraded imaging platforms improve minimally invasive workflow quality and support demand pull-through for compatible laparoscopic instruments and accessories across premium operating rooms.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of general surgical devices sold and used in India for routine and specialty procedures, counted at the point of sale to hospitals, clinics, and surgical centers, and tracked in USD for the study period.

Scope exclusions: We exclude dental, ophthalmic, diagnostic equipment, capital imaging systems, and non-device hospital consumables that are not used as surgical devices.

Segmentation Overview

- By Product

- Handheld Devices

- Laparoscopic Devices

- Electrosurgical Devices

- Wound-Closure Devices

- Trocars & Access Devices

- Other Products

- By Application

- Gynecology & Urology

- Cardiology

- Orthopedic

- Neurology

- Gastro-Intestinal & Hepato-Biliary

- Other Applications

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base for procedure volumes, healthcare capacity, and trade flows that influence demand for surgical devices in India. We referred to public sources such as the Ministry of Health and Family Welfare releases, National Health Accounts, the National Sample Survey where relevant, and import-export statistics published through official customs and trade portals.

To keep assumptions grounded, we also reviewed sources such as notified standards and guidance from Indian regulators, procurement notices and tender documents from large public buyers, and peer reviewed clinical publications that indicate procedure trends. Company annual reports and investor presentations were reviewed for India exposure and category signals. In a few places, paid subscriptions for company financials and intelligence, patent databases, and shipment-level trade data were used to cross-check manufacturer presence, category activity, and price direction. The desk sources listed here are only illustrative, and many other public and reputable materials were also referenced for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on verifying pricing and mix, adoption of laparoscopic and energy-based tools, and the demand split between high volume government hospitals and private hospital chains. We spoke with hospital procurement teams, surgeons, distributors, and device managers across major metro clusters and fast-growing tier 2 cities. This helped address gaps that desk sources do not explain well, especially around realized prices from tenders and category usage patterns per procedure.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 13% | |

| Mid tier: 51% | Functional/Unit leaders: 28% | |

| Smaller Players: 15% | Managers: 59% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up combination. Procedure volumes and care delivery capacity were used to reconstruct the demand pool for general surgical devices in India, followed by penetration and replacement assumptions for major product categories. To keep the total grounded, selective bottom-up approximations were added using sampled average selling prices times estimated unit consumption for key categories. These were then cross-checked with distributor channel checks, and used to tune the final totals.

Inputs that mattered most included the mix shift toward laparoscopic procedures, usage rates for wound-closure products per case, electrosurgical utilization in operating rooms, tender-led buying patterns in public facilities, import dependence for certain categories, and ASP movement driven by product standardization and competitive tendering. Forecasting relied on scenario analysis supported by expert consensus, where base, conservative, and faster-adoption cases were run around procedure growth, penetration of minimally invasive tools, and price erosion assumptions. Where bottom-up signals were missing for smaller product lines, gaps were handled by applying conservative utilization proxies from similar procedures, then validating the implied spend per surgery with interview feedback.

Data Validation & Update Cycle

Model outputs were checked against independent signals such as operating room expansion, reported device import trends, and observed procurement activity. We then reviewed the results for outliers before sign-off. When a variance was seen at the category level, the assumption was revisited, and we re-contacted sources to confirm whether the driver was pricing, mix, or a timing issue.

A multi-step analyst review is used so calculations, definitions, and conversions are consistent across years, and any one-off spikes are explained in plain terms. Reports are refreshed annually, with interim updates triggered by material events such as policy changes, major tender cycles, or sharp currency movement. Before delivery, a final pass is done so the client receives the most current view available.

Mordor Intelligence's India General Surgical Devices Market Sizing Compared With Other Published Estimates

Published market sizes for India general surgical devices often do not match because the product basket and the counting point vary, and the same words can cover different items. Differences also come from how firms treat imports versus local production, whether pricing is modeled at list price or realized tender price, and how quickly assumptions are refreshed.

The main gap comes from whether wound dressings and other non-device hospital consumables are bundled into general surgery spend, where Mordor Intelligence keeps the total limited to defined device categories like handheld, laparoscopic, electrosurgical, wound-closure, and trocars, and leaves out broader consumable lines that can inflate totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.00 B (2026) | |

| Industry Research House A | USD 0.62 B (2025) | Uses a narrower value definition that likely emphasizes selected device categories and may rely on reported company revenues, which can undercount distributor-led sales and tender-driven volumes. |

| Market Publisher B | USD 1.82 B (2024) | Anchors the time series on an earlier year and may apply a smoother growth path with limited category-level price and penetration checks, which can shift totals when procedure mix changes quickly. |

Across the three figures, the spread is mainly explained by what is included in the basket, which year is treated as the anchor, and how realized prices are handled in public tenders versus private buying. By keeping assumptions tied to procedure activity, utilization per case, and practical ASP checks, the sizing stays traceable to clear steps that can be repeated and reviewed.

Key Questions Answered in the Report

What is the projected value of the India general surgical devices market by 2031?

It is anticipated to reach USD 3.47 billion by 2031, advancing at an 11.68% CAGR from 2026.

Which product segment currently leads device sales?

Laparoscopic devices accounted for 34.54% of the India general surgical devices market share in 2025.

Which application area is forecast to grow fastest?

Gastro-intestinal & hepato-biliary surgeries are set to expand at a 13.21% CAGR through 2031.

How are government schemes influencing demand?

Ayushman Bharat's coverage of 550 million citizens is shifting procedure volumes into public and empaneled private hospitals, stabilizing demand for mid-tier consumables.

What role do domestic manufacturers play in supply?

PLI-assisted firms such as Healthium, Meril and Poly Medicure are scaling capacity and now supply a growing share of sutures, staplers and basic laparoscopic kits.

Which restraint most affects market profitability?

Price caps and delayed reimbursements in public procurement squeeze margins, especially for premium devices.

Page last updated on: