India Furniture Hardware Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

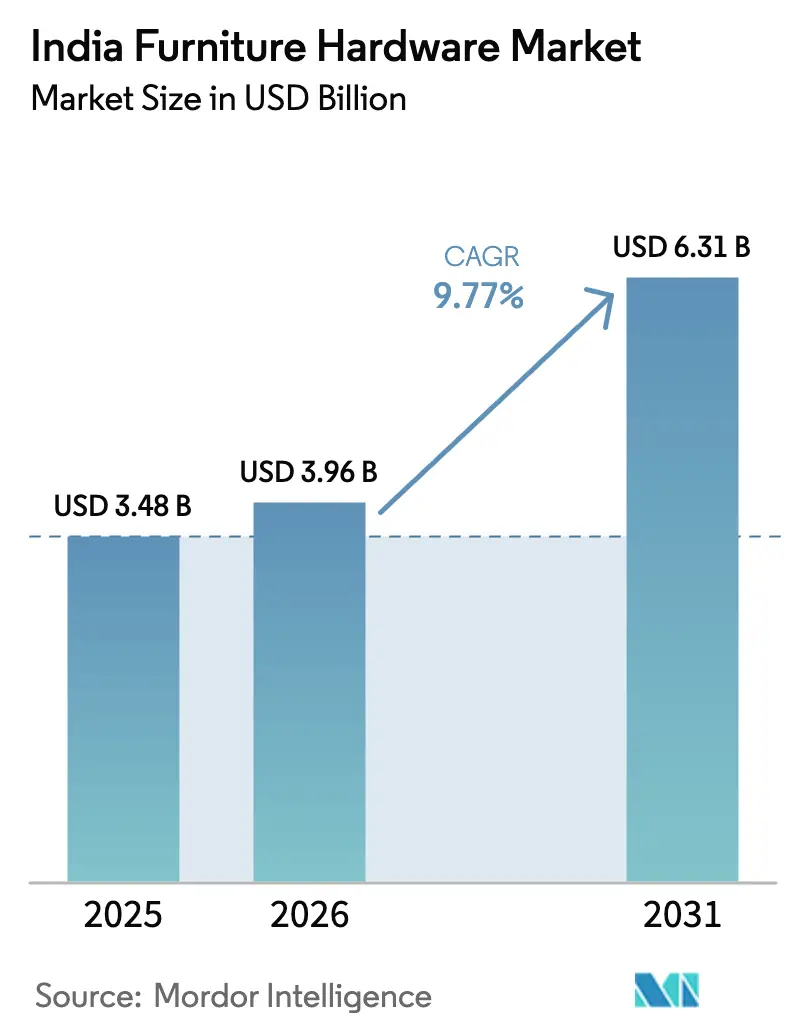

| Base Year Market Size (2025) | USD 3.48 Billion |

| Market Size (2026) | USD 3.96 Billion |

| Market Size (2031) | USD 6.31 Billion |

| Growth Rate (2026 - 2031) | 9.77% CAGR |

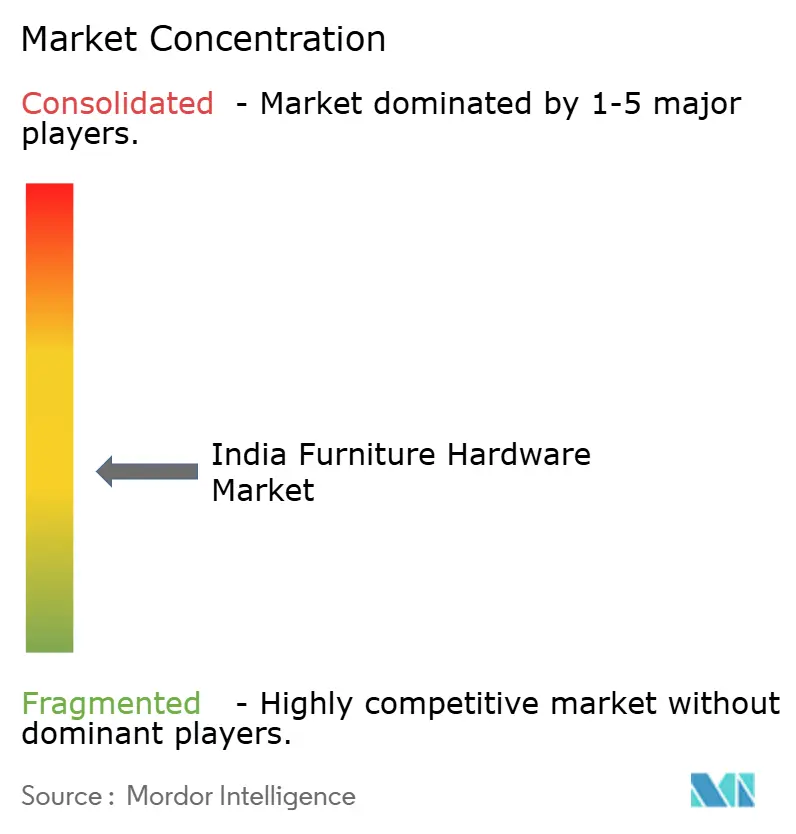

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Furniture Hardware Market Analysis by Mordor Intelligence

The India furniture hardware market size is expected to increase from USD 3.48 billion in 2025 to USD 3.96 billion in 2026 and reach USD 6.31 billion by 2031, growing at a CAGR of 9.77% over 2026-2031. A steady residential pipeline, rising penetration of modular kitchens and wardrobes, and quality-focused specifications in organized channels are lifting mid-premium and premium demand across urban and emerging tier-II hubs. Bureau of Indian Standards Quality Control Orders now in force for hinges and multiple furniture categories are pushing purchasing toward licensed brands and away from unlicensed imports and unorganized supply, consolidating volumes among compliant manufacturers[1]Bureau of Indian Standards, “Quality Control Orders for Furniture and Fittings,” Bureau of Indian Standards, bis.gov.in. Offline dealers remain the primary route to market, though online channels scale faster as brands bundle certified kits and installation guidance that bring discovery and selection online before showroom visits. Input-cost swings in steel, zinc, and polymers continue to challenge smaller assemblers who lack hedging and escalation clauses, tilting the advantage toward integrated producers with local capacity, multi-plant sourcing, and compliance-led differentiation. Tiered expansion strategies by leading brands that add showrooms, skill training, and localized production capacity are reinforcing share gains where developers standardize concealed mechanisms as a core feature set in new residential projects.

Key Report Takeaways

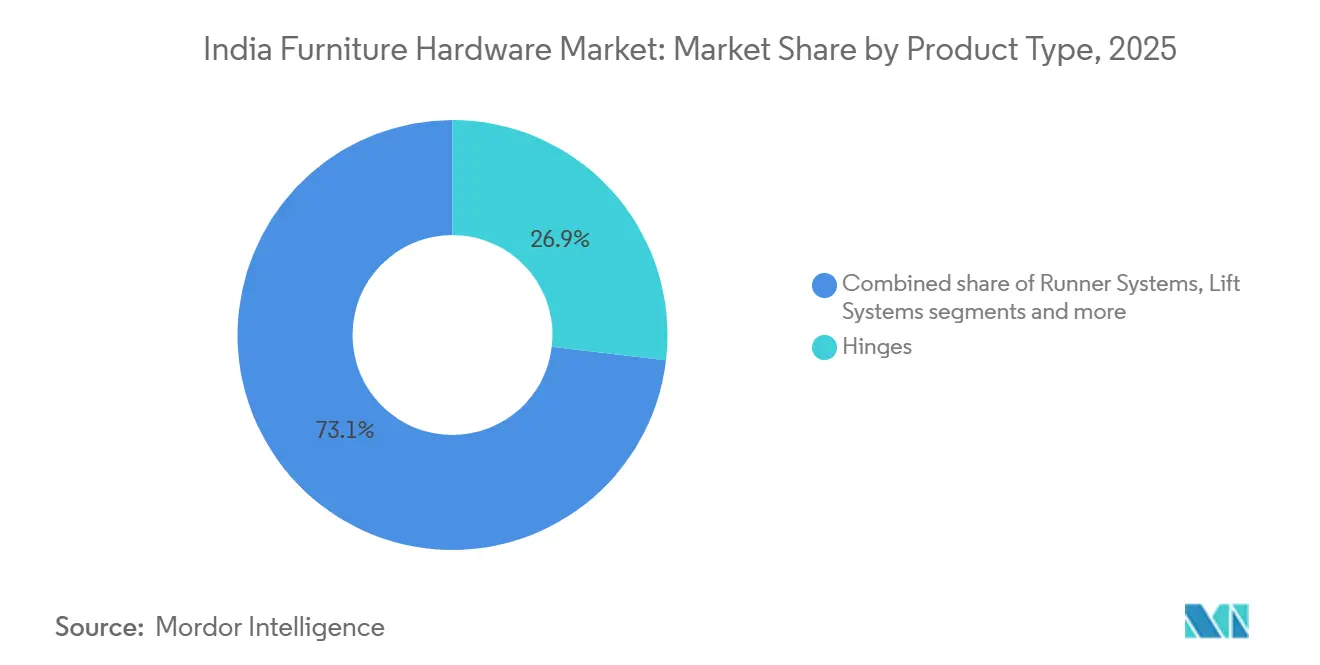

- By product type, hinges led with 26.88% revenue share in 2025 in the India furniture hardware market. Lift systems are projected to advance at a 9.85% CAGR through 2031.

- By material, steel accounted for 41.88% share in 2025 in the India furniture hardware market. Plastic and polymer-based fittings are forecast to post a 10.35% CAGR through 2031.

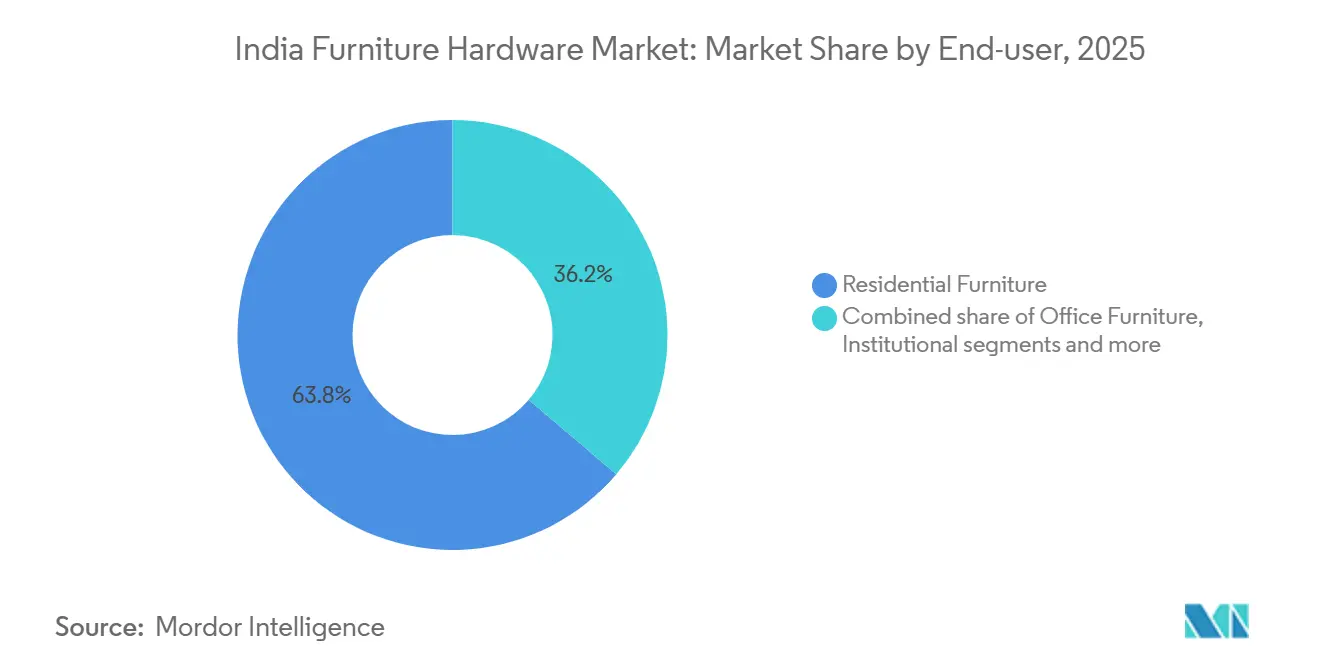

- By end user, residential commanded 63.78% of the 2025 India furniture hardware market. Hospitality and retail fixtures are projected to grow at a 10.02% CAGR to 2031.

- By distribution channel, offline dealers captured 74.35% of sales in 2025 in the India furniture hardware market. The online channel is projected to scale at an 11.05% CAGR through 2031.

- By region, South India held 34.86% in 2025. West India is set to record the fastest regional CAGR at 10.55% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Furniture Hardware Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising modular kitchen and wardrobe penetration across Tier 1–3 cities | +2.8% | Asia-Pacific core, strongest in West & South India metros, spilling into tier-II clusters (Pune, Coimbatore, Kochi) | Medium term (2–4 years) |

| Strong residential pipeline and premiumization boosting fit-out spending | +2.5% | National, concentrated in Mumbai, Bengaluru, NCR, and early gains in Chennai, Hyderabad | Medium term (2–4 years) |

| Shift to organized/RTA furniture and OEM standardization of fittings | +1.9% | Global manufacturing hubs (NCR, Gujarat), radiating to contract manufacturers nationwide | Long term (≥4 years) |

| Omnichannel expansion: e-commerce and brand D2C enable reach and assortment | +1.2% | Urban India (tier-I/II), accelerating in metros with last-mile logistics | Short term (≤2 years) |

| BIS Quality Control Orders elevating performance specs and premium mix | +0.9% | National enforcement, compliance-driven in formal retail & institutional segments | Short term (≤2 years) |

| Localization and India manufacturing capex by global majors | +0.5% | Manufacturing clusters (Gujarat, Maharashtra, Tamil Nadu), export-oriented units | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Modular Kitchen and Wardrobe Penetration Across Tier 1–3 Cities

Modular formats are scaling from tier-I into tier-II and tier-III catchments as developers integrate factory-built kitchens and wardrobes in mid-premium projects to shorten handovers and raise perceived quality. Each modular kitchen pulls through a dense bill of fittings that includes multiple pairs of drawer slides, numerous concealed hinges, and one or more lift systems per unit, which compounds category volumes as completions rise. This adoption encourages consistent SKU standards, since fabricators need compatible hinges, runners, and lift mechanisms across flat sizes and repeated layouts in multi-tower projects. Brands now tailor products to compact urban apartments by focusing on soft-close performance, tool-free assembly, and vertical-access solutions that free counter space while improving ergonomics in wall cabinets. Product displays and experience centers let buyers test mechanisms before selection, which reduces returns and builds trust for premium upgrades that expand the average hardware wallet per kitchen. As supply shifts toward certified components under national standards, modular OEMs favor licensed vendors for predictable cycle life and corrosion resistance aligned with warranty expectations in organized housing.

Strong Residential Pipeline and Premiumization Boosting Fit-Out Spending

In 2026, large residential pipelines in top cities anchor steady demand for kitchens, wardrobes, and storage units that default to soft-close drawers and concealed hinges in base specifications. Buyers allocate a larger share of unit value to interiors, and branded hardware can lift the kitchen bill of materials where aesthetics, finish consistency, and quiet operation are now standard preferences in urban homes. Developers in core markets pre-install modular wardrobes and kitchens to improve absorption, which further embeds hardware selection at the project specification stage rather than as an aftermarket choice. Financing support and curated packages from interior platforms simplify upgrades, and that nudges projects toward certified mechanisms that can carry longer warranties and stable sourcing over the build cycle. Training programs for carpenters and installation partners sponsored by leading brands reinforce correct fitting and after-sales performance, which enhances satisfaction and sustains repeat selection on future projects. The net effect is consistent volume pull-through into organized channels that reward compliant producers with broader acceptance and durable project relationships.

BIS Quality Control Orders Elevating Performance Specs and Premium Mix

The Bureau of Indian Standards now enforces Quality Control Orders that require hinges and multiple furniture categories to be licensed under Scheme-I, with the Standard Mark displayed, which formalizes minimum durability and safety metrics for fittings and furniture in the country. This compliance requirement shifts demand from unlicensed imports and informal workshops toward domestic or imported SKUs that carry valid BIS licenses, raising the share of organized supply across institutional and organized retail channels. Early movers among global brands completed licensing for priority hinges and slides ahead of full enforcement and used compliance to differentiate in dealer contracts and aggregator partnerships. Organized retailers and interior platforms now include BIS requirements in vendor agreements, which makes certification a baseline for participation in multi-city and institutional tenders. These rules favor integrated manufacturers that can spread inspection, testing, and surveillance costs across higher volumes and wider assortments, while unorganized vendors face exclusion if they cannot meet audits and documentation. Over time, the premium mix rises as developers and homeowners choose certified concealed mechanisms and cycle-tested runners, valuing quiet operation, corrosion resistance, and consistent tolerances aligned to multi-year performance.

Localization and India Manufacturing Capex by Global Majors

Established multinationals have increased local investments in manufacturing and assembly to hedge currency exposure, ease lead times, and align with compliance and service expectations in the India furniture hardware market. Capacity additions by leading brands span localized drawer-box systems, broader runner assortments, and product training centers that lift specification influence and improve the installer ecosystem. Experience centers enable architects and consumers to evaluate motion quality and finish choices in person, then complete transactions through omnichannel paths that tie showrooms to dealer supply and digital fulfillment. Localization also supports export potential for select SKUs, as India plants scale for regional distribution while precision components for high-end motion systems continue to leverage global centers of excellence[2]Häfele India Team, “India Manufacturing and Experience Centers,” Häfele India, hafeleindia.com. The combined effect is a more resilient supply base with shorter replenishment cycles, more predictable costs, and stronger compliance footprints that align with rising enforcement standards. This capacity buildout amplifies the differentiation gap with smaller assemblers, particularly where breadth of assortment, installer support, and license coverage weigh heavily in vendor selection.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material price volatility (steel, zinc, polymers) is compressing margins | -1.1% | National, acute for import-reliant assemblers in coastal hubs, hedged producers are less exposed | Short term (≤2 years) |

| Fragmentation and unorganized competition are pressuring prices/quality | -0.8% | Tier-II/III markets, peri-urban clusters with informal workshops | Medium term (2–4 years) |

| Installation skill gaps for advanced mechanisms | -0.3% | Rural and tier-III geographies, with limited technical training infrastructure | Medium term (2–4 years) |

| Import dependence on premium motion/precision components | -0.2% | High-end residential, logistics-sensitive | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility (Steel, Zinc, Polymers) Compressing Margins

Fluctuating prices for steel, zinc, and polymers have raised input-cost uncertainty for fittings manufacturers, especially for those without multi-quarter contracts or hedging capacity in place. Smaller assemblers that quote fixed-rate orders to builders can face margin compression if suppliers reset coil or resin prices during execution, which strains cash flow and jeopardizes delivery schedules. Integrated producers mitigate shocks through contracted buying, capacity planning, and tooling investments that lower scrap and stabilize per-unit conversion costs across plants. Even for scaled players, episodes of sharp volatility can trim near-term EBITDA, which encourages diversification across materials and specifications to rebalance profitability. Over the medium term, local manufacturing depth and balanced sourcing across geographies should reduce exposure to imported inputs for mid-range SKUs, though premium motion components may still rely on global supply chains. Brands that structure escalation clauses with OEM and project customers maintain pricing power more effectively when raw-material costs spike, improving resilience through cycles.

Fragmentation and Unorganized Competition Pressuring Prices/Quality

The India furniture hardware market remains moderately fragmented, with a long tail of regional workshops and import stockists that compete on price rather than documented cycle life or corrosion resistance. In tier-II and tier-III markets, non-certified fittings often undercut compliant SKUs, which compresses organized players’ margins when price points dominate over lifecycle performance. Certification-led enforcement is now curbing access to formal channels for unlicensed products, which should gradually improve quality baselines and reward organized suppliers. Brands are differentiating through installer training, onsite support, and multi-year warranties that embed soft-close damping and premium finishes as accepted standards in residential and institutional settings[3]. Over time, dealer education, tighter vendor agreements, and omnichannel transparency will reduce adverse selection in price-sensitive clusters and lift the compliance share of the category. The transition is gradual, where enforcement capacity is stretched, yet the direction is clear as national standards and organized retail scale together.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Standardization Elevates Soft-Close Variants and Vertical Storage

Hinges held the largest product-type position with 26.88% in 2025, while lift systems are set to grow the fastest at a 9.85% CAGR through 2031, reflecting ergonomic needs and premiumization in compact urban homes. Concealed hinges with integrated damping now attract higher preference because they deliver quieter operation and cleaner cabinet lines that match the design intent of modular formats. Vertical-access mechanisms address ceiling-height wall cabinets that expand storage without enlarging kitchen footprints, which is relevant in mid-size apartments across major cities. Drawer runner systems scale with the adoption of drawer-box formats, and localized production aims to cut lead times while maintaining reliable soft-close action across load categories. Handles and knobs continue to face heavier price pressure, though curated finishes and coordinated collections create small premiums where designers specify end-to-end packages. Complementary items such as cabinet lights and locks lift attach rates in organized retail, and brands that offer broader assortments benefit as dealers consolidate supplier rosters.

Lift systems are becoming a default upgrade in higher-value kitchens because they free workspace, reduce obstruction, and maintain alignment over longer use cycles in humid conditions. Runner systems that balance load ratings with smooth travel improve user experience, and tool-free assembly lowers installer time for projects with tight handover windows. In this context, specification training that helps carpenters choose the right crank, overlay, and slide rating reduces callbacks and supports repeat use of certified SKUs. Brands reinforce this with warranties that build confidence in cycle-tested products and align with developers’ preference for documented quality under national standards. As these patterns mature, hinges and runners remain the category backbone, while lift systems expand share from a lower base on the strength of ergonomic gains in premium and mid-premium kitchens.

By Material: Polymer-Based Fittings Disrupt Cost and Design Trade-Offs

Steel led materials with 41.88% share in 2025, supported by the strength and corrosion performance that kitchens and wardrobes require in diverse Indian climates. Plastic and polymer-based fittings are projected to grow at a 10.35% CAGR through 2031 as engineered compounds integrate damping, complex geometries, and lighter weights that reduce load on hinges and slides. The balance between aesthetics, durability, and cost favors steel in high-load applications, while polymers win in accessory and non-load-bearing roles where molded shapes deliver benefits. Aluminum fits use cases where weight saving and slim profiles command a premium, notably in sliding systems and some wardrobe components. Brass persists in luxury fittings where depth and tactile quality matter, though volumes concentrate around steel and advanced polymers in mainstream projects[4]Godrej Interio Corporate Team, “Institutional and Office Use Cases,” Godrej Interio, godrejinterio.com.

Supply reliability and certification alignment now influence material mix, because certified inputs support easier licensing under the BIS regime and reduce risk during surveillance audits. Localized runner and box production reduces exposure to currency swings for mainstream SKUs, while motion-critical dampers and precision parts may still rely on international centers of excellence. As polymer compounds improve in UV and wear resistance, substitution will increase where cycle loads are lower, but stainless and high-grade steel maintain leadership where load-bearing and corrosion resistance are non-negotiable. Growing awareness of recyclable inputs and traceability in resin sourcing should support formal suppliers as documentation becomes part of procurement, especially in institutional channels. Over the forecast window, polymers extend reach into organizers and auxiliary components, while steel remains the foundation of runners and hinges that define the user experience in high-frequency use zones.

By End-User: Hospitality Fixtures Outpace Residential on Standardization and Turnover

Residential accounted for 63.78% of the 2025 volume, with new home handovers converting directly into pull-through demand for hinges, runners, and lift mechanisms that form the core bill of materials. Institutional and hospitality projects are increasing specification intensity, and hospitality and retail fixtures are forecast to grow at a 10.02% CAGR as chains standardize fixtures that must withstand frequent use. Organized procurement in hospitals, schools, and public offices raises documentation and certification thresholds, which directs spending to licensed suppliers with stable quality. Office environments now rely on modular storage and adaptable layouts, which add consistent but measured demand for runners, cable management, and light-duty mechanisms centered on serviceability. Residential still dominates in units, yet hospitality and institutional orders can deliver higher value per site as projects specify soft-close features and cycle-tested components for heavy-duty usage.

Standardized SKUs and vendor frameworks in hospitality reduce variation between properties, resulting in multi-site orders that favor brands with breadth, inventory depth, and after-sales support. Retail formats and quick-service settings prize fast installation and durability under high traffic, which rewards tool-free assembly and documented cycle life as the basis for selection. These users often accept modest price premiums for fittings that avoid maintenance downtime, shifting the conversation from upfront cost to lifecycle value. Over time, the rise of organized procurement for public and private institutions should deepen category penetration for certified fittings and narrow the spread between residential and non-residential shares in value terms. The India furniture hardware market will continue to rely on residential momentum, while non-residential pockets sustain margin expansion through higher specification and repeat frameworks.

By Distribution Channel: Offline Strength Meets Online’s Assortment and Data Advantages

Offline dealers captured 74.35% of 2025 sales, reflecting the importance of local stock, credit terms, and installer support for small contractors and carpentry-led projects. The online channel is projected to scale at an 11.05% CAGR as platforms surface certified assortments and bundle clear installation guidance that lowers selection risk for first-time buyers. Hybrid journeys that begin with digital discovery and move to showrooms for product trials now account for a growing share of consideration, particularly in premium and mid-premium budgets. Franchise and partner store networks hosted by leading brands extend consistent displays and training into tier-II cities, which builds specification influence with installers and designers. As more SKUs meet compliance requirements, digital catalogs gain value by allowing filter-based selection and direct comparisons on load ratings, finish options, and license details. Although shipping costs can be higher for heavy steel components in direct-to-home models, scheduled delivery and verified packaging reduce returns and expand reach into cities without full-line dealers.

Dealer credit, local training, and rapid availability keep offline channels indispensable for project execution where timelines are tight and changes occur late in the building cycle. Online channels contribute scale by exposing smaller towns to premium, certified fittings that local stockists may not carry, creating new demand pools beyond metro centers. Brands that synchronize inventory and service across online and offline entry points raise satisfaction and capture data that refines assortments and forecasting. Over the forecast horizon, share is likely to normalize toward a balanced hybrid, where discovery and specification move online while installation and support remain intensely local. These shifts will favor manufacturers and distributors that unify catalogs, training, and compliance disclosures across channels without sacrificing availability and service quality at the last mile.

Geography Analysis

South India held 34.86% of the India furniture hardware market in 2025, anchored by early modular adoption and steady residential completions across Bengaluru, Chennai, and Hyderabad. Higher shares of mid-premium and premium units in these cities promote concealed mechanisms and soft-close drawers as standard features that increase the category wallet per dwelling. Installer training and brand experience centers remain a focus in this region, where humidity and coastal conditions influence a tilt toward stainless and corrosion-resistant choices that support lifecycle performance. Regulatory enforcement of BIS standards in organized retail channels strengthens the case for licensed vendors and narrows the space for unorganized alternatives.

West India shows the fastest projected regional expansion at a 10.55% CAGR through 2031, reflecting strong premiumization, large project pipelines, and developer focus on standardized modular interiors in the Mumbai Metropolitan Region and Pune. This translates to higher per-unit hardware content in premium and ultra-premium apartments that prioritize quiet operation, robust load ratings, and aligned finishes. Dealer networks with wide assortments and rapid replenishment underpin execution across multi-tower sites, a feature that favors national brands with consistent compliance and service footprints. Investment in localized production and assembly supports shorter lead times and improved cost control, which enhances competitiveness against imports in the mainstream range.

North India exhibits mixed patterns, with luxury-led growth in select corridors and cost-sensitive demand in investor-heavy micro-markets, which together sustain broad category presence at varied price points. Organized vendors benefit from established dealer ecosystems and reliable logistics that shorten service times across Delhi-NCR and neighboring cities. East and North-East India remain the smallest segments but show gradual improvements through better logistics and e-commerce access to certified SKUs, which raise quality baselines over time. As national standards and omnichannel access continue to expand, consistent vendor frameworks and installer training will drive steady uplift across lagging regions.

Competitive Landscape

The Indian furniture hardware market is moderately concentrated, with the top five organized players together holding a significant minority of the total share, while regional suppliers and unorganized workshops retain a large presence in value-conscious clusters. Leading brands emphasize compliance, breadth of assortment, and installer training to convert project specifications into stable demand across housing and institutional pipelines. BIS licensing has become a cornerstone of differentiation that determines access to formal retail and institutional channels, increasing the importance of documented testing and surveillance readiness. Localized capacity investments improve resilience, reduce landed costs, and support faster new-product rollouts tailored to market needs. Experience centers and franchise formats deepen engagement with carpenters and designers, shaping preference at the point of specification and training.

Strategic moves reflect these priorities. Hettich announced plans for a third India plant by 2026 and continues to scale training programs that support correct fitting and long-term performance of soft-close systems in kitchens and wardrobes. Häfele expanded localized production and partnerships to lift India sourcing for key product lines while expanding displays and training in tier-II hubs through curated showrooms. Blum scaled branded experience locations to reinforce premium positioning and provide hands-on evaluation for lift systems and drawer solutions that anchor high-end kitchens. Domestic champions continue to broaden assortments and invest in channel expansion to serve project-driven demand in housing, hospitality, offices, and public procurement.

Omnichannel integration connects discovery, selection, and installation across digital platforms and physical showrooms, enabling certified assortments to reach buyers well beyond metro centers in the India furniture hardware market. Investment activity underscores confidence in category growth, as ecosystem players link design, procurement, and installation to deliver integrated value propositions for residential and commercial clients. Brands also extend product ecosystems with lighting and accessory SKUs that raise attach rates and lift transaction value without adding complexity to installation. Over the forecast window, players with robust compliance, training, and localized capacity are positioned to capture gains from regulatory enforcement and rising specification standards across segments.

India Furniture Hardware Industry Leaders

Hettich India Pvt. Ltd

Häfele India Pvt. Ltd.

Godrej Locks & Architectural Fittings & Systems

Ebco Pvt. Ltd.

Ozone Overseas Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Hettich India announced plans to establish a third manufacturing plant by the end of 2026, complementing existing facilities in Vadodara and Indore, alongside expansion of the HeX franchise format targeting 100 experiential touchpoints over two years.

- August 2025: Livspace invested USD 5.5 million in TplusA India, a premium hardware supplier, to deepen vertical integration and secure supply for full-service kitchen and wardrobe packages.

- July 2025: MR.DIY expanded into South India with plans for over 40 new stores, increasing organized retail access to furniture hardware in tier-II cities.

- April 2025: Godrej Interio announced a Rs 55 crore investment to transform its B2B office-furniture portfolio with a focus on flexible, ergonomic products and allied solutions for workplaces.

India Furniture Hardware Market Report Scope

Furniture hardware comprises the fixings, fittings, and individual components essential for crafting functional and durable furniture pieces. This report will provide a detailed analysis of the Indian furniture hardware market. The report delves into the market dynamics, highlights emerging trends in the segment and regional markets, and offers insights into different product and application categories. It also analyses the key players and the competitive landscape.

The India furniture hardware market is segmented by product type, material, end-user, distribution channel, and region. By product type, the market is divided into hinges, runner systems, lift systems, box systems, wire baskets, sliding door systems, handles, pulls and knobs, fasteners (screws, bolts, nuts, etc.), and others. By material, the market includes steel, zinc alloy, aluminium, plastic and polymer-based materials, and brass and other metals. By end-user, the market is categorized into residential furniture, office furniture, hospitality and retail fixtures, and institutional applications (healthcare and education). By distribution channel, the market is segmented into offline – dealer and retail, and online – e-commerce and brand direct-to-consumer (D2C) channels. Geographically, the market analysis covers North India, West India, South India, and East and North-East India. The report provides market size and forecasts for the India furniture hardware market in value (USD) across all the above segments.

| Hinges |

| Runner Systems |

| Lift Systems |

| Box Systems |

| Wire Baskets |

| Sliding Door Systems |

| Handles, Pulls, and Knobs |

| Fasteners (Screw, Bolts, Nuts, etc.) |

| Others |

| Steel |

| Zinc Alloy |

| Aluminium |

| Plastic & Polymer-based |

| Brass & Other Metals |

| Residential Furniture |

| Office Furniture |

| Hospitality & Retail Fixtures |

| Institutional (Healthcare, Education) |

| Offline – Dealer & Retail |

| Online – E-commerce & Brand D2C |

| North India |

| West India |

| South India |

| East & North-East India |

| By Product Type | Hinges |

| Runner Systems | |

| Lift Systems | |

| Box Systems | |

| Wire Baskets | |

| Sliding Door Systems | |

| Handles, Pulls, and Knobs | |

| Fasteners (Screw, Bolts, Nuts, etc.) | |

| Others | |

| By Material | Steel |

| Zinc Alloy | |

| Aluminium | |

| Plastic & Polymer-based | |

| Brass & Other Metals | |

| By End-user | Residential Furniture |

| Office Furniture | |

| Hospitality & Retail Fixtures | |

| Institutional (Healthcare, Education) | |

| By Distribution Channel | Offline – Dealer & Retail |

| Online – E-commerce & Brand D2C | |

| By Region | North India |

| West India | |

| South India | |

| East & North-East India |

Key Questions Answered in the Report

What is the current size and growth outlook for the India furniture hardware market?

The India furniture hardware market size is USD 3.48 billion in 2025 and is projected to reach USD 6.31 billion by 2031 at a 9.77% CAGR over 2026–2031.

Which product categories are leading and growing the fastest in India?

Hinges led with 26.88% revenue share in 2025, while lift systems are set to grow the fastest at a 9.85% CAGR through 2031.

Which region is expected to expand the quickest in India?

West India is forecast to post the fastest regional CAGR at 10.55% through 2031, while South India held the highest 2025 share at 34.86%.

How are BIS Quality Control Orders changing competitive dynamics?

BIS licensing is steering volume toward certified vendors, raising performance baselines, and limiting access for unlicensed products in organized retail and institutional channels.

What distribution channels are winning in the India furniture hardware market?

Offline dealers held 74.35% of 2025 sales, and the online channel is scaling faster at an 11.05% CAGR as assortments and installation guidance move online.

Which end-user segments offer the strongest growth runway?

Residential anchors volume at 63.78% of 2025, while hospitality and retail fixtures are the fastest-growing at a 10.02% CAGR due to standardization and frequent use.

Page last updated on: