Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

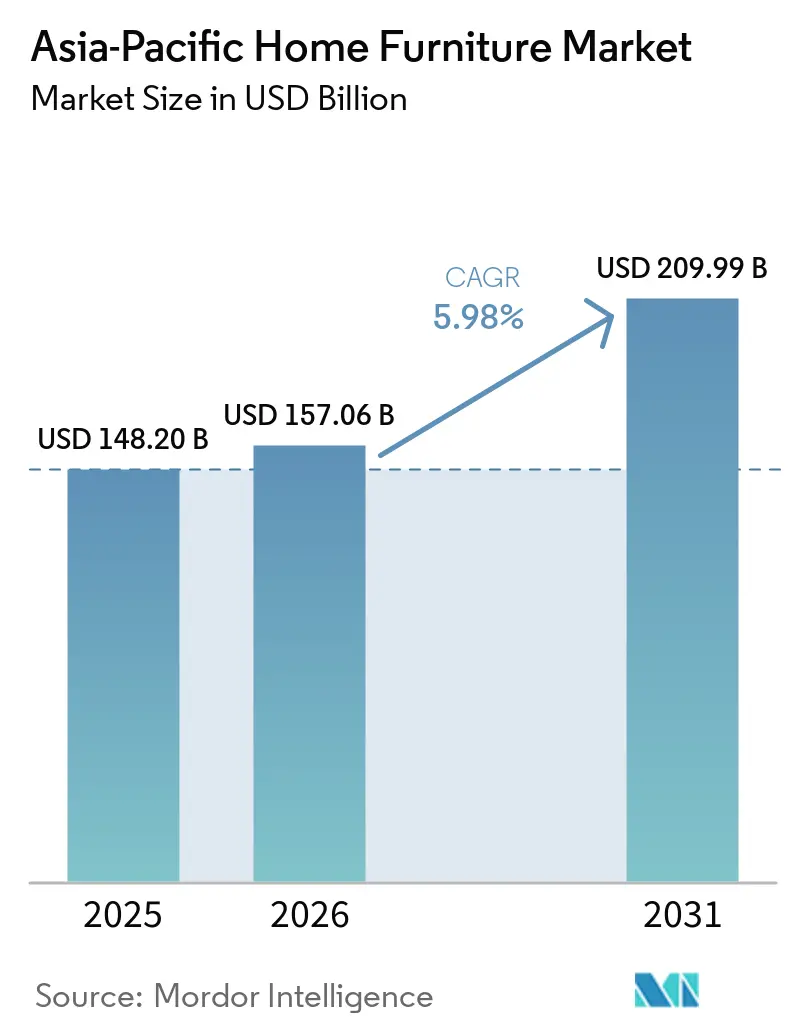

| Base Year Market Size (2025) | USD 148.20 Billion |

| Market Size (2026) | USD 157.06 Billion |

| Market Size (2031) | USD 209.99 Billion |

| Growth Rate (2026 - 2031) | 5.98% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Home Furniture Market Analysis by Mordor Intelligence

The Asia-Pacific home furniture market size is expected to grow from USD 148.20 billion in 2025 to USD 157.06 billion in 2026 and is forecast to reach USD 209.99 billion by 2031 at 5.98% CAGR over 2026-2031. E-commerce adoption continues to influence bulky-goods discovery, specification, and purchase, as global retailers deepen omnichannel investments and expand on leading digital platforms in China and across Southeast Asia[1]The Business Times Newsroom, “Ikea Bets on Online Growth in China with JD.com Launch,” The Business Times, asean.businesstimes.com.sg . Urban housing formation and ongoing renovation cycles sustain replacement demand, while aging populations in advanced economies shape needs for barrier-free layouts and higher durability standards that reinforce premium materials and compliant finishes. Regulatory shifts led by China’s new furniture emissions standards and the ENF formaldehyde grade elevate compliance baselines and push buyers toward verified low-VOC products and clear labeling. Trade policy changes, including United States duties on cabinets and upholstered goods, alter sourcing footprints, delivery routes, and final pricing structures across intra-APAC and trans-Pacific supply chains. Stronger sustainability signaling, including the expansion of forest certification and due-diligence requirements in end markets, drives certification-led procurement strategies in Vietnam, Malaysia, Indonesia, and supplier bases serving the European Union.

Key Report Takeaways

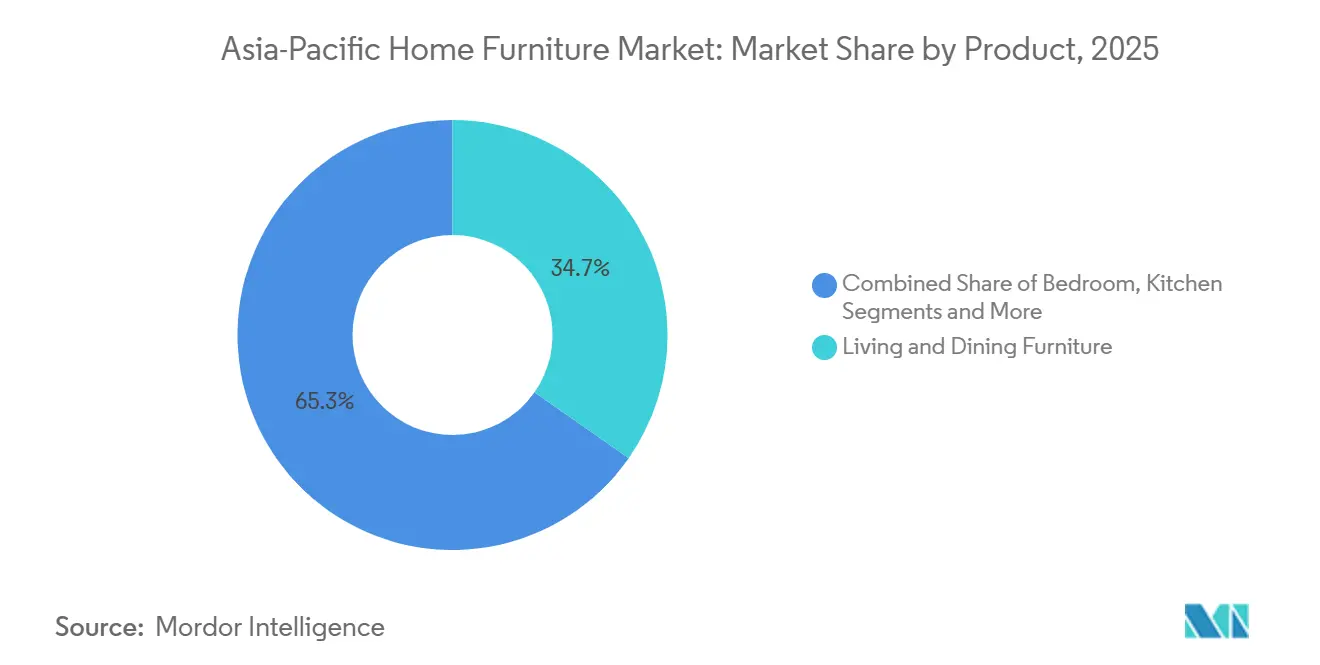

- By product type, living room and dining room furniture led with 34.72% of the Asia-Pacific home furniture market share in 2025, while home office furniture is projected to expand at a 6.55% CAGR through 2031.

- By material, wood held 54.56% of the Asia-Pacific home furniture market share in 2025, whereas plastic and polymer materials are forecast to grow at a 7.12% CAGR through 2031.

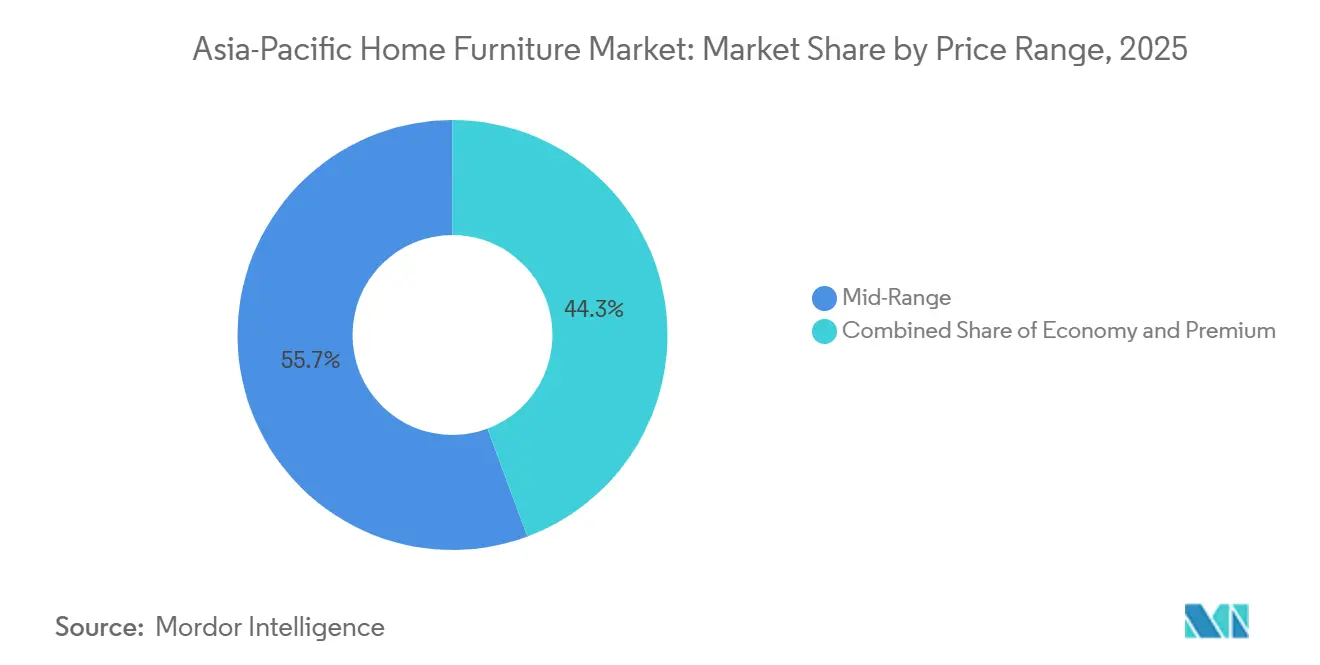

- By price range, mid-range captured 55.68% of the Asia-Pacific home furniture market share in 2025, while premium is expected to advance at a 7.01% CAGR through 2031.

- By distribution channel, specialty furniture stores accounted for 38.61% of the Asia-Pacific home furniture market share in 2025, whereas online channels are projected to grow at an 8.06% CAGR through 2031.

- By geography, China held 43.58% of the Asia-Pacific home furniture market share in 2025, while India is projected to record the fastest 10.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Home Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce penetration reshapes bulky-goods buying journeys | 1.2% | Global, strongest in China, India, Southeast Asia | Medium term (2-4 years) |

| Urban housing formation and renovations | 1.5% | Japan, India, China, Australia, South Korea | Medium to Long term (2-4+ years) |

| Rising disposable incomes and premiumization | 1.1% | India, China, ASEAN-6, emerging Tier-2/3 cities | Medium term (2-4 years) |

| Wood-preference and sustainability-led purchasing | 0.8% | Global, particularly Singapore, Australia, EU-facing exporters | Long term (≥4 years) |

| Micro-living drives modular/multifunctional designs | 0.9% | Urban cores: Hong Kong, Tokyo, Singapore, Mumbai, Manila | Short to Medium term (≤2-4 years) |

| Stricter low-VOC/formaldehyde standards push compliant products | 0.5% | China, Singapore, India (IGBC-certified projects) | Medium to Long term (2-4+ years) |

| Source: Mordor Intelligence | |||

E-Commerce Penetration Reshapes Bulky-Goods Buying Journeys

Digital channels account for over 10% of global furniture sales, and Asia-Pacific leads the adoption curve through omnichannel programs that blend online merchandising with showroom advisory and post-purchase installation[2]World Furniture Online Editorial Team, “Furniture Market Dynamics in 2025: Trade and Megatrends,” World Furniture Online, worldfurnitureonline.com . Regional growth is reinforced by large-format retailers launching dedicated stores on Chinese marketplaces that integrate national logistics networks for home delivery and returns. In India, online revenue contributions for leading global brands have exceeded industry norms as visualization tools, generous exchange policies, and faster delivery windows build confidence for high-involvement purchases. Operational friction persists in the last-mile and installation for bulky freight, which is why resolute cross-border, bulky-goods logistics services have expanded coverage across Thailand, Malaysia, Singapore, and Indonesia with in-house teams and regional hubs. Shifts in airfreight and parcel flows as customs thresholds evolve can redirect platform focus across lanes, which indirectly eases or tightens capacity for intra-APAC shipments, including furniture. As these logistics ecosystems mature, the Asia-Pacific home furniture market benefits from reduced delivery risk and broader assortment access that was previously constrained by store footprints.

Urban Housing Formation and Renovations

New residential construction and retrofit demand converge to sustain furniture replacement cycles. Japan's housing starts fell 0.4% year-on-year in January 2026, the mildest contraction since July 2024 ,but owner-occupied starts rebounded 6.6%, signaling stabilization in detached-home segments that favor higher-value, durable furnishings[3]Trading Economics Team, “Japan Housing Starts Drop Less Than Estimated,” Trading Economics, tradingeconomics.com. Housing attainability pressures continue to push first-time buyers toward smaller units across many urban centers in the region, which supports demand for modular, space-efficient designs and multi-functional pieces. Policy responses such as social housing and for-rent frameworks across select Asia-Pacific governments will influence the mix of fittings and durable finishes specified for high-occupancy settings. India’s steady uptick in premium demand within new housing underscores how home offices, wellness zones, and smart features translate into ergonomic desks, integrated storage, and tech-ready cabinetry. Migration inflows in major hubs also increase turnover for rental units, which raises baseline demand for flexible, durable furniture suited to frequent tenant changeovers and tighter floor plans.

Rising Disposable Incomes and Premiumization

Middle-class expansion and rising affluence are shifting household purchases toward better materials, craftsmanship, and design provenance. India, now one of the top global markets by size, recorded robust 2024 growth with a low import share that leaves headroom for higher-end domestic offerings and select luxury imports. As organized players align with green building and indoor air quality specifications, procurement that favors low-emission adhesives and coatings becomes a visible differentiator in corporate and institutional fit-outs. Brands across the region increasingly emphasize traceable wood, recycled components, and higher-performance finishes to serve informed buyers seeking health and sustainability benefits alongside aesthetics. Premium sales often accommodate bespoke consultations, longer lead times, and certification-backed materials, which together reinforce the value proposition that supports higher average selling prices. This structural preference for quality, durability, and verified sustainability continues to pull demand into upper tiers within the Asia-Pacific home furniture market.

Stricter Low-VOC/Formaldehyde Standards Push Compliant Products

A regulatory reset is underway. China’s GB 18584-2024 consolidates limits for formaldehyde, TVOCs, and other substances of concern, while the ENF grade tightens formaldehyde to a stringent threshold, making emissions compliance a competitive baseline for suppliers[4]CCL Lab, “Mandatory National Standard GB 18584-2024,” CCL Lab, ccllab.com.cn . Singapore’s enhanced Sustainability Furniture Mark brings third-party testing, tiered TVOC thresholds, and a public registry that raises the bar for indoor air quality signaling and opens procurement access in institutional settings. India’s Furniture Quality Control Order requires ISI certification across core furniture categories in 2026, consolidating demand toward organized, compliant manufacturers with documented processes. For exports, CARB P2 formaldehyde limits and EU REACH screening make third-party verification and chain-of-custody evidence table stakes for suppliers to the United States and Europe. Export development teams report that proactive certification, faster technical vetting, and well-documented quality systems accelerate sales cycles and support value-based pricing strategies that offset compliance costs. Restraints Impact Analysis

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material and freight cost volatility | -0.9% | Global, pronounced on trans-Pacific and Asia-Europe lanes | Short to Medium term (≤2-4 years) |

| Bulky last-mile logistics, damage and returns | -0.6% | Southeast Asia, India, Australia | Medium term (2-4 years) |

| Anti-dumping duties and intra-APAC trade frictions | -0.7% | China-centric supply chains, US-bound exports | Short to Medium term (≤2-4 years) |

| Tightening fire-safety and emissions compliance costs | -0.4% | China, Singapore, India (IGBC-certified projects), EU-facing exporters | Medium to Long term (2-4+ years) |

| Source: Mordor Intelligence | |||

Raw Material and Freight Cost Volatility

Wood prices rose in late 2025, supported by policy actions and supply curtailments, intensifying cost pressure on panels and solid wood inputs that remain core to category manufacturing. Supply constraints in key North American regions and labor shortages in logging and mills kept producers cautious as downstream housing starts showed signs of improvement for 2026. Northern European timber stakeholders highlighted raw material and currency swings that undercut profitability and triggered cost containment initiatives to stabilize operations. On the ocean side, Asia–United States West Coast container rates lifted in late 2025 while all-in delivered costs escalated further once accessories were included, shaping landed-price decisions for furniture importers. Route disruptions and canal constraints propped up rates and contributed to schedule variability, while a historically large vessel orderbook introduced uncertainty about how incoming capacity will affect rate cycles and service reliability. Regional lanes also saw short-term surges and congestion in late 2025, which added weeks to schedules and forced shippers to carry extra buffer stock that tied up working capital.

Anti-Dumping Duties and Intra-APAC Trade Frictions

The United States anti-dumping orders on Chinese wooden bedroom furniture and cabinets continued to shape sourcing decisions, with final margins reaffirmed in 2025 and duties lifting delivered costs for importers. Additional United States actions introduced duties on cabinets and vanities as well as upholstered wooden furniture under national security provisions, prompting manufacturers to diversify production footprints and consider new nearshoring options. Mexico imposed tariffs on a broad set of imports from countries without trade agreements in 2024, including furniture, which affected cost competitiveness for exporters targeting North America. Regional exporters with cost advantages and robust certification portfolios continued to maintain market access, although higher tariff ceilings introduced planning risks that require more active trade compliance. Combined, these measures reinforced the shift toward “China+1” strategies, where suppliers build redundancy across Vietnam, Indonesia, India, and others to preserve continuity and margin in the Asia-Pacific home furniture market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hybrid-Work Upside Reshapes Portfolio Mix

Living room & dining room furniture held 34.72% in 2025, while Home Office Furniture is the fastest-growing category at 6.55% CAGR over 2026-2031 within the Asia-Pacific home furniture market size. The leadership of living and dining reflects enduring family use cases and social needs, where sectional seating, extendable tables, and media units remain foundational to household layouts. Retailers continue to enhance value through curated bundles and availability of upholstery choices, as well as improved stain-resistant finishes for higher-use items. Home office momentum persists with ergonomic desks, sit-stand formats, and task seating that meet comfort and productivity needs in hybrid schedules. Online visualization and assisted selling help convert hesitant buyers for these high-involvement purchases, even as many still finalize choices in stores.

Bedroom furniture sustains steady replacement cycles through upholstered headboards, storage-integrated bed frames, and modular wardrobes that maximize utility in smaller footprints. Kitchen furniture and modular cabinetry gain from space optimization in dense urban housing, with performance surfaces, concealed storage, and silent hardware seen as baseline expectations in mid-range to premium brackets. Bathroom vanities move with renovation timing and premium finishes, while outdoor lines grow in tropical markets where humidity resistance and durability set product standards. FSC-certified outdoor ranges and engineered boards designed for weather exposure demonstrate how material innovation and sustainability credentials inform purchase criteria.

By Material: Wood Dominance Persists, Yet Polymer Innovation Accelerates

Wood accounted for 54.56% of the market in 2025 and continues to anchor quality perception and durability, while Plastic & Polymer materials are projected to grow at 7.12% CAGR during 2026-2031 in the Asia-Pacific home furniture market. Sustainability-linked certifications reinforce wood’s brand equity with traceable supply and chain-of-custody labeling for downstream buyers. Global certification coverage expanded in 2025, with Asia-Pacific responsible for a significant share of Chain of Custody certificates and growing adoption among exporters that serve the EU. Malaysia’s first certifications for bamboo and rubberwood add to the mix of renewable materials for furniture makers who serve buyers prioritizing due diligence and long-term availability. Vietnamese suppliers are integrating FSC and PEFC systems, field-testing geolocation-based compliance as European rules tighten, and using certified acacia, eucalyptus, and teak to serve policy-sensitive buyers.

Polymers gain share through lightweight, modular, and price-accessible designs that meet micro-living constraints. Composite innovations that blend fast-growing biomass with engineered polymers aim to raise durability, reduce weight, and improve moisture resistance for kitchens, baths, and entry-level storage. Metal-based designs continue to support office and outdoor use with powder-coated finishes and corrosion resistance, while glass, stone, and rattan offer accent and premium surface options that elevate aesthetic variety. Regulatory trends, including ENF-grade boards in China and CARB P2 for United States-bound goods, push manufacturers toward low-emission adhesives and water-based finishes to protect market access and program eligibility in the Asia-Pacific home furniture market.

By Price Range: Mid-Range Anchors Volume, Premium Gains Fastest

Mid-Range captured 55.68% share in 2025, while Premium is expected to grow the fastest at 7.01% CAGR over 2026-2031 in the Asia-Pacific home furniture market size. Mid-tier buyers seek functional design, reliable quality, and fair prices across sofas, dining sets, wardrobes, and storage furniture, making omnichannel breadth and stock depth decisive. Scale retailers show that consistent assortments, urban-format stores, and assisted digital journeys can widen reach and support steady growth even in price-sensitive segments. Premium gains are supported by affluent households and advanced specification standards in institutional and corporate environments that require verified emissions limits and certified materials. Compliance-led procurement and sustainability signaling allow organized players to command higher prices while improving conversion with consultative selling and bespoke services.

Premium demand reflects a willingness to wait for customs to finish, distinctive upholstery, and artisanal details validated by independent certifications. High-performance finishes on dining tables, long-wear leather, and FSC-certified hardwoods sustain longevity propositions that align with higher transaction values. The Asia-Pacific home furniture market continues to see consumers trading up as awareness of indoor air quality and material provenance becomes more prevalent in purchasing decisions.

By Distribution Channel: Online Surges, Yet Specialty Stores Retain Physical Primacy

Specialty Furniture Stores held 38.61% of the market in 2025, while online is projected to grow at 8.06% CAGR during 2026-2031 in the Asia-Pacific home furniture market. Store formats remain central for tactile evaluation of upholstery comfort, joinery quality, fabric hand-feel, and finish consistency, and for coordinating delivery and assembly services on higher-ticket purchases. Showrooms also act as design advisory hubs for custom cabinetry and wardrobe planning, which often require precise field measurements and iterative specification.

Online channels scale as mobile discovery and digital payments expand, while augmented reality and 3D configuration tools reduce uncertainty about size, color, and fit. High-velocity platforms in China carry curated selections from global brands with embedded logistics and last-mile orchestration, extending reach beyond physical catchments. New bulky-goods logistics programs in Southeast Asia further address pain points around transport, customs clearance, and installation by deploying in-house delivery personnel and regional hub coverage. As omnichannel capabilities mature, integrated inventory visibility, managed installation, and flexible returns help online channels capture a larger slice of the Asia-Pacific home furniture market over the forecast period.

Geography Analysis

China anchored 43.58% of the Asia-Pacific home furniture market share in 2025, underpinned by a large domestic base and an extensive manufacturing ecosystem that serves regional and global demand. Export momentum faced policy headwinds in 2025 as the United States anti-dumping orders and new national security tariffs on cabinets and upholstered wooden goods influenced product mix and route planning. Domestic adoption of AR and VR shopping features and platform partnerships supports high-end and mid-range online growth, while construction market fluctuations temper short-term raw material flows for wood-heavy categories. India is projected to be the fastest-growing market at a 10.88% CAGR from 2026 to 2031, supported by urbanization, rising incomes, and a broad base of mid-range buyers that is steadily trading up.

Investment signals from leading global retailers underscore India’s strategic priority and the runway for larger store networks and expanded online reach. On the policy front, India’s Furniture Quality Control Order enforces ISI certification for key categories from February 2026, a step that consolidates demand toward compliant, organized manufacturers. Across the rest of Asia-Pacific, Japan’s early 2026 housing data showed milder contractions and a rebound in owner-occupied starts, which supports demand for higher-quality, durable furnishing categories.

Southeast Asia continues to benefit from nearshoring dynamics, with Vietnam’s export base integrating FSC and PEFC systems and piloting geolocation tools to align with EU due diligence rules. Malaysia’s certification milestones for bamboo and rubberwood add renewable options, while Indonesia’s SVLK system embeds legal timber verification with geolocation features that support compliance pathways for EU-facing exporters. These shifts sustain a region-wide pivot toward traceable materials, lower emissions, and verified legality that align with the long-term outlook for the Asia-Pacific home furniture market.

Competitive Landscape

The Asia-Pacific home furniture market shows moderate fragmentation with local consolidation, where global incumbents and regional champions compete alongside a long tail of small and mid-sized producers. Scale players leverage sourcing density, logistics integration, and omnichannel platforms to defend share in mid-range and premium segments, while compliance-led differentiation has become a key lever for value capture. Retailers deepen digital engagement to convert online discovery into assured delivery and installation, which shapes store formats, service offerings, and capital allocation in core cities.

One leading global player plans to expand aggressively in India through higher investment, more stores, and faster online growth targets, signaling a long-term commitment to market development and local supplier integration. In China, platform partnerships and curated product assortments align brand visibility with national logistics networks that can support bulky-goods delivery and reverse logistics at scale. Regional players in India are investing in omnichannel reach, brand refresh programs, and product innovation to accelerate B2C and B2B growth. One major Indian brand has announced a multi-year investment plan focused on digital technology, store expansion into Tier-II and Tier-III cities, and design enhancements, together with a revenue target that would more than double its current scale by FY2029. Across Southeast Asia, bulky-goods logistics solutions aim to relieve friction in cross-border movement and last-mile installation, supporting pure-play e-commerce and omnichannel retailers alike.

As certification and compliance deepen, producers that document emissions limits and timber legality gain credibility with institutional buyers, accelerating deal cycles and supporting premium capture relative to generic supply. Competitive dynamics vary by segment. Living room and dining continue to draw mass and premium demand, yet the home office shows structural growth as hybrid routines normalize. Materials competition balances wood’s enduring appeal against polymer and composite innovation that serves micro-living and entry-level categories. Retail differentiation often turns on delivery quality, assembly services, and returns processing, areas where integrated logistics or managed partner networks can protect margin and support repeat purchases.

Asia-Pacific Home Furniture Industry Leaders

IKEA

Nitori Holdings

KUKA Home (Jason Furniture Hangzhou)

Man Wah Holdings (CHEERS)

Oppein Home Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: IKEA announced plans to more than double its investment in India to over 200 billion rupees (USD 3.2 billion) within five years, expanding from six to 30 stores, increasing online sales from 30% to a target 40%, and boosting local sourcing from 30% to 50% by 2030 through partnerships with 45 suppliers, signaling confidence in India's position as one of IKEA's most strategic global markets.

- December 2025: SF International unveiled a comprehensive bulky-goods logistics portfolio across Thailand, Malaysia, Singapore, and Indonesia on December 9, 2025, deploying 10,000+ in-house personnel, 20+ regional hubs, and 780 outlets to address cross-border bottlenecks in transport, last-mile delivery, and customs clearance for furniture and home appliances, with value-added services including delivery/installation, warehousing, and reverse logistics.

- November 2025: TCC Concept Limited, a Pune-based real estate service company, acquired 98.98% of Indian online furniture retailer Pepperfry for INR 661.47 crore via share-swap (approved by TCC board in November, deal completion mid-December 2025), marking a significant discount from Pepperfry's prior USD 300+ million valuation as the company grappled with logistics costs, premium pricing challenges, and FY24 revenues of INR 209 crores (-40% year-on-year).

- October 2025: IKEA inaugurated its second Philippines store, a 500-square-meter Plan and Order Shop at Ayala Malls TriNoma in Quezon City, on October 23, 2025, offering in-store purchase of selected items, online order pick-up, and complimentary design consultations from 14 trained interior designers, reinforcing IKEA's omnichannel strategy and collaboration with Ayala Malls.

Asia-Pacific Home Furniture Market Report Scope

The Asia-Pacific home furniture market features a broad spectrum of products tailored for residential use, such as seating, storage solutions, tables, beds, and decorative items. Characterized by its diverse offerings, the market caters to a multitude of consumer preferences, cultural nuances, and regional aesthetics. The report delves into a comprehensive background analysis of the Asia-Pacific home furniture market. This includes evaluating the economy and the contributions of various sectors, providing a market overview, estimating market sizes for key segments, highlighting emerging trends, analyzing market dynamics, and examining logistics spending by end-user industries.

The Asia-Pacific Home Furniture Market is segmented by product, material, price range, distribution channel, and geography. By product, the market is divided into living room & dining room furniture, bedroom furniture, kitchen furniture, home office furniture, bathroom furniture, outdoor furniture, and other furniture. By material, the market is categorized into wood, metal, plastic & polymer, and others. By price range, the market is segmented into economy, mid-range, and premium. By distribution channel, the market is divided into home centers, specialty furniture stores, online, and other distribution channels. Geographically, the market analysis covers India, China, Japan, Australia, South Korea, Southeast Asia, and the Rest of the Asia-Pacific. The report provides market size and forecasts for the Asia-Pacific home furniture market in value (USD) across all the above segments.

By Product

| Living Room & Dining Room Furniture |

| Bedroom Furniture |

| Kitchen Furniture |

| Home Office Furniture |

| Bathroom Furniture |

| Outdoor Furniture |

| Other Furniture |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Others |

By Price Range

| Economy |

| Mid-Range |

| Premium |

By Distribution Channel

| Home Centers |

| Specialty Furniture Stores |

| Online |

| Other Distribution Channels |

By Geography

| India |

| China |

| Japan |

| Australia |

| South Korea |

| South East Asia |

| Rest of Asia-Pacific |

| By Product | Living Room & Dining Room Furniture |

| Bedroom Furniture | |

| Kitchen Furniture | |

| Home Office Furniture | |

| Bathroom Furniture | |

| Outdoor Furniture | |

| Other Furniture | |

| By Material | Wood |

| Metal | |

| Plastic & Polymer | |

| Others | |

| By Price Range | Economy |

| Mid-Range | |

| Premium | |

| By Distribution Channel | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| By Geography | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current size and growth outlook for the Asia-Pacific home furniture market?

The Asia-Pacific home furniture market size is USD 148.20 billion in 2025, expected to reach USD 157.06 billion in 2026, and USD 209.99 billion by 2031 at a 5.98% CAGR.

Which product categories are leading and growing fastest in the Asia-Pacific home furniture market?

Living room & dining room furniture leads with 34.72% share in 2025, while home office furniture shows the fastest growth at 6.55% CAGR for 2026-2031.

How are materials trending in the Asia-Pacific home furniture industry?

Wood holds 54.56% share in 2025 due to durability and aesthetics, while plastic & polymer materials are growing fastest at 7.12% CAGR through 2031 on modular, lightweight designs.

Which channels are winning in Asia-Pacific furniture distribution?

Specialty furniture stores hold 38.61% share, and online is the fastest growing at 8.06% CAGR as AR tools, faster delivery, and bulky-goods logistics reduce purchase friction.

Which countries are most important in this region’s furniture demand?

China holds 43.58% share in 2025, and India is the fastest growing with a projected 10.88% CAGR to 2031, reflecting urbanization and rising incomes.

What regulatory changes will most affect suppliers to the Asia-Pacific?

ENF formaldehyde limits in China, Singapore’s Sustainability Furniture Mark, India’s Furniture QCO, CARB P2 for United States exports, and EU due diligence rules will shape compliance requirements and supplier selection.

Page last updated on: