Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

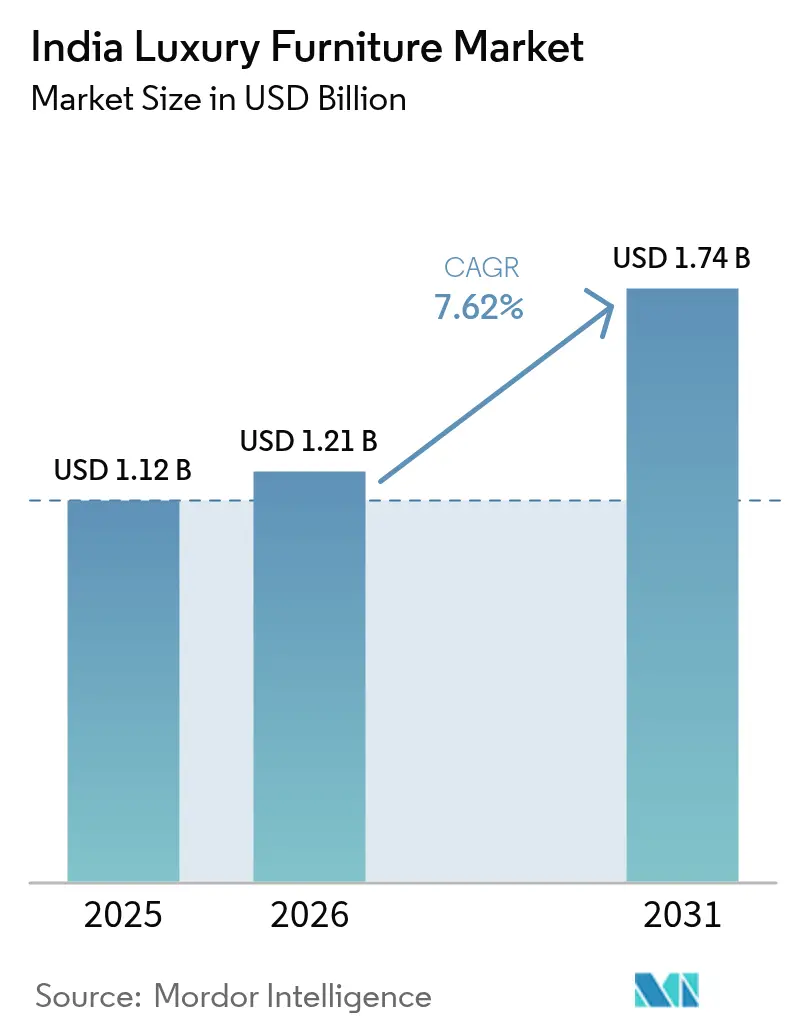

| Base Year Market Size (2025) | USD 1.12 Billion |

| Market Size (2026) | USD 1.21 Billion |

| Market Size (2031) | USD 1.74 Billion |

| Growth Rate (2026 - 2031) | 7.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Luxury Furniture Market Analysis by Mordor Intelligence

The India luxury furniture market size was valued at USD 1.12 billion in 2025 and estimated to grow from USD 1.21 billion in 2026 to reach USD 1.74 billion by 2031, at a CAGR of 7.62% during the forecast period (2026-2031). Robust wealth creation, expanding branded retail footprints, and a decisive shift toward premium living spaces underpin this trajectory. Rising discretionary income following the 2025-26 Union Budget tax relief is lifting demand for high-design furnishings, while omnichannel distribution upgrades widen geographic reach for aspirational consumers. Institutional procurement from hospitality chains and Grade-A offices is gaining momentum, accelerating supplier consolidation and deepening specification standards. ESG-driven sourcing, celebrity-backed interior trends, and rapid trend diffusion through social media are amplifying premiumization, prompting brands to invest in design partnerships, agile prototyping, and certified materials. Meanwhile, raw-material price volatility and BIS certification deadlines raise compliance costs, nudging the ecosystem toward organized, quality-oriented manufacturing.

Key Report Takeaways

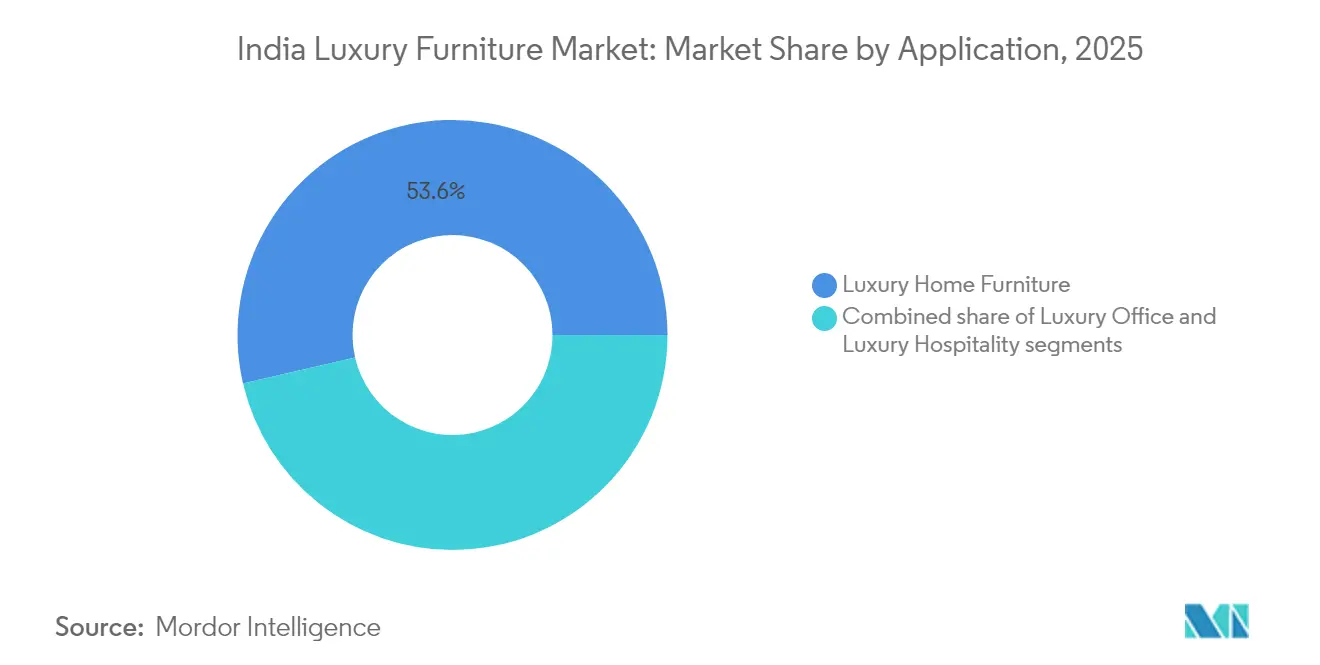

- By application, luxury home furniture commanded 53.62% of the India luxury furniture market share in 2025, whereas luxury hospitality furniture is advancing at an 8.48% CAGR to 2031.

- By material, wood accounted for a 58.72% share of the India luxury furniture market size in 2025 and is projected to grow at a 9.03% CAGR to 2031.

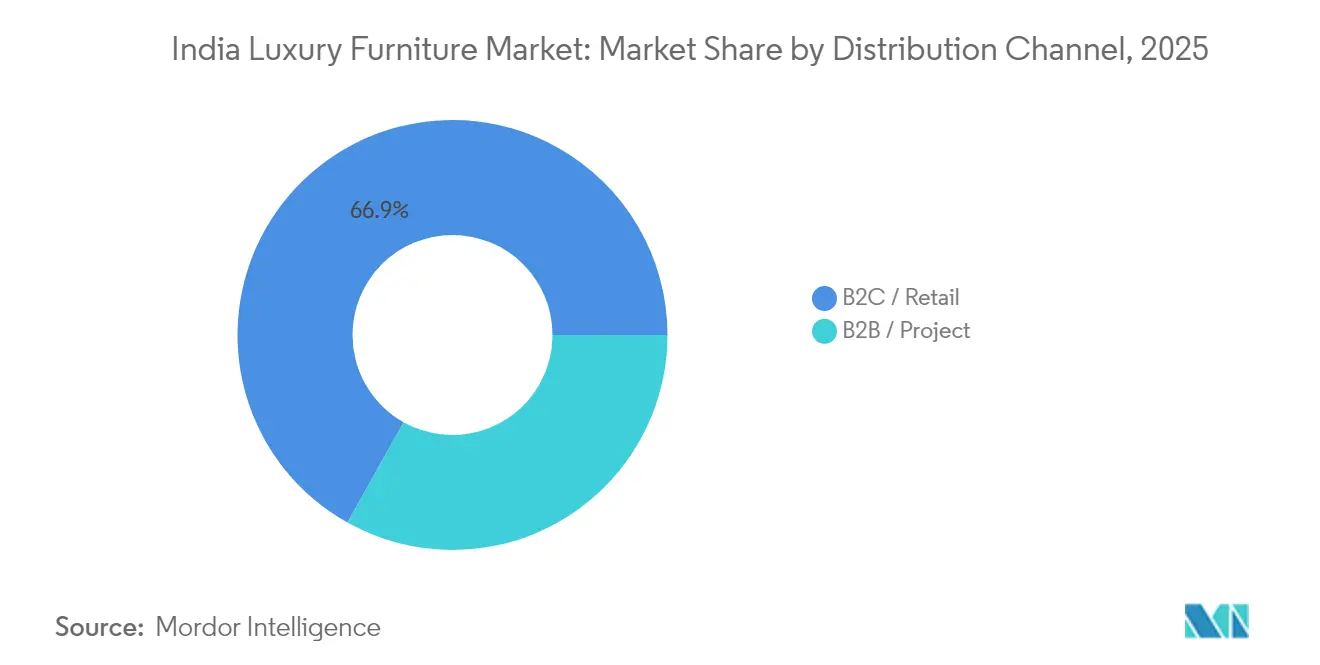

- By distribution channel, B2B project sales held a 33.12% share in 2025 while recording the highest projected CAGR at 7.91% through 2031.

- By geography, West India led with 31.05% revenue share in 2025; North-East India is forecast to expand at an 8.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Luxury Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing aspirational spending among the upper-middle class | +2.1% | National, metros & tier-1 cities | Medium term (2-4 years) |

| Expansion of branded retail chains & e-commerce | +1.8% | National; early gains in West & South India | Short term (≤ 2 years) |

| Premiumization of residential design via celebrity architects | +1.2% | West India, North India metros | Medium term (2-4 years) |

| Boom in Grade-A office stock & coworking spaces | +1.5% | National, spill-over to tier-2 cities | Short term (≤ 2 years) |

| Surge in branded hotel pipeline in tier-2/3 cities | +1.9% | National, tier-2/3 markets | Long term (≥ 4 years) |

| ESG mandates for sustainable/green materials | +0.8% | Global; export-linked clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Aspirational Spending among India’s Upper-Middle Class

Furniture purchases have evolved from need-based outlays to lifestyle statements that communicate social status. Disposable income increased following the 2025 tax restructuring that waived income tax on salaries up to INR 1.2 million, redirecting a share of household budgets toward premium home upgrades[1]Press Information Bureau, “NO INCOME TAX ON ANNUAL INCOME UPTO Rs. 12 LAKH UNDER NEW TAX REGIME,” pib.gov.in. Shorter renovation cycles now 10-12 years reflect a craving for contemporary aesthetics that align with global design narratives, encouraging recurring spend on the India luxury furniture market. Social platforms compress style diffusion from metros to tier-2 hubs within 18-24 months, compelling brands to launch micro-collections synced with trending palettes. Luxury showrooms in Mumbai, Delhi, and Bangalore report basket sizes rising 12-15% after adopting experience-center formats where curated vignettes trigger emotional buying. Aspirational buyers increasingly request provenance certificates for materials, blending conspicuous consumption with conscious living.

Rapid Expansion of Branded Retail Chains & E-Commerce Platforms

Omnichannel strategies are redrawing shopper journeys by merging tactile store experiences with digital convenience. IKEA’s compact 25,000–70,000 sq ft city stores complement 150,000 sq ft fulfillment hubs that promise 24-hour deliveries without diluting brand theater [2]Bailay Rasul, “Ikea plans 25,000 sq. ft ‘mini’ stores in India,” indiaretailing.com. Domestic players such as HomeLane, following its Design Café acquisition, integrate design consultation, manufacturing, and last-mile installation on a single tech stack, shrinking project lead times from 12 weeks to 6 weeks. Advanced 3D visualizers let customers overlay sofas or wardrobes onto room photos, boosting online conversion rates above 18% and reducing return rates through precise spatial matches. Unified inventories ensure online promotions map instantly to showroom stock, preserving price integrity. These innovations collectively democratize the India luxury furniture market by reaching affluent households in tier-3 towns without heavy real-estate outlay.

Premiumization of Residential Interior Design Driven by Celebrity Architects

High-profile architects have become design influencers who translate global trends into culturally resonant interiors, shaping consumer preferences downstream. The 2025 “Silent Opulence” theme favors muted luxe through tactile fabrics, intricate joinery, and understated metallic inlays, shifting demand toward artisanal limited editions [3]Sayoni Bhaduri, “India’s Interior Design Trends 2025,” luxe.outlookindia.com. Celebrity-designed model apartments inside new luxury towers accelerate design adoption, with furniture brands gaining instant credibility through co-branding. Bespoke requests smart coffee tables with concealed chargers or modular daybeds clad in hand-woven silk require agile factories capable of low-volume, high-mix production. Storytelling around craft provenance, such as Rajasthan hand-carved teak or Nagaland cane weave, allows brands to command premiums of 25-30% over mass alternatives. Collaborations also shorten concept-to-shelf timelines, keeping collections fresh and safeguarding relevance in the India luxury furniture market.

Boom in Grade-A Office Stock & Coworking Spaces

Office absorption forecasts of 65–70 million sq ft for 2025 translate into mass procurement of ergonomic, tech-enabled workstations. Coworking operators prioritize plug-and-play furniture that supports 24/7 usage, modular reconfiguration, and rapid sanitization requirements that elevate specification complexity and raise barriers to entry for unorganized suppliers. Manufacturers like Godrej Interio deploy Motion chairs with flexible lumbar modules that adapt to dynamic postures, integrating smart sensors for occupancy analytics. Hybrid work pushes crossover demand, with corporate employees buying compact sit-stand desks for home offices that retain professional aesthetics, thereby blurring B2B and B2C lines inside the India luxury furniture market. Tier-2 cities such as Jaipur and Coimbatore witness fresh Grade-A stock, extending institutional demand beyond traditional metros. The result is a virtuous cycle: rising office quality expectations spill into residential preferences, reinforcing the premium furniture narrative.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw material prices (wood, metal, leather) | -1.4% | National; import-dependent zones | Short term (≤ 2 years) |

| Fragmented, unorganized sector limits premium pricing | -0.9% | Nationwide; tier-2/3 concentration | Medium term (2-4 years) |

| Shortage of skilled carpenters & upholsterers | -0.7% | Manufacturing clusters | Long term (≥ 4 years) |

| Lengthy building-code and fire-safety clearances | -0.5% | Nationwide; state-level variance | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Material Prices

Soft-sawn wood averaged INR 27,500 per metric ton in April 2024, yet month-to-month gyrations exceed 15%, skewing cost forecasts for manufacturers that lock in project bids six months ahead [4]IndexMundi, “Soft Sawnwood – Monthly Price,” indexmundi.com. Imports soared from USD 630 million to USD 2.3 billion over two decades, exposing the India luxury furniture market to currency swings and freight surcharges. February 2026 BIS certification will require batch testing and factory audits, injecting compliance timetables into already tight project schedules. China’s stockpiling of tropical hardwoods has pushed up CIF rates for teak and merbau, forcing Indian buyers to explore alternative species and engineered panels. Manufacturers hedge by pre-buying logs when the rupee strengthens, but holding bulky inventories strains working capital. Price pass-through to consumers lags at least one quarter, compressing gross margins during spike periods.

Highly Fragmented Unorganized Sector Limiting Price Premium

Roughly 2,400 plywood units operate nationwide, yet fewer than 1,000 comply with mandatory Quality Control Orders, perpetuating a dual market where uncertified products undercut branded offerings by 25–35%. Informal workshops rely on familial labor networks and cash transactions, escaping tax nets and lowering cost structures, which dilutes consumer perception of the value difference between luxury and mass products. In tier-3 cities, buyers often prioritize visual similarity over material provenance, challenging organized brands to justify premiums without widespread design literacy. Government smart-city clusters promise INR 28,602 crore in infrastructure to nurture formal manufacturing, but project rollouts stagger across states, delaying consolidation. Unorganized dominance also hampers export prospects, as overseas buyers hesitate when domestic supply chains appear fragmented. To counter, leading brands invest in franchised dealer education programs that demonstrate durability tests in-store, slowly converting value-focused shoppers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Hospitality Drives Premium Growth

Luxury hospitality furniture held a 33.57% share of the India luxury furniture market in 2025 and is poised to cross USD 610 million by 2031 at an 8.48% CAGR. Chain operators mandate ASTM E84 fire-rating, moisture-sealed edges, and elevated abrasion scores, escalating technical requirements beyond residential norms. Vendors winning Marriott or ITC contracts often secure repeat orders for pipeline properties, stabilizing capacity utilization. Home furniture retains a 53.62% share in 2025, but its expansion moderates to 6.85% as repeat purchases dominate incremental volume. Buyers in metros demand hidden charging docks, velvet performance fabrics, and convertible storage beds, blending luxury with lifestyle pragmatism.

Office applications occupy a 12.81% share in 2025, catalyzed by coworking ventures requiring adaptable layouts that integrate privacy pods and plug-and-play conferencing tables. Ergonomic benchmarks such as BIFMA X5.1 now inform even SME procurements, nudging local suppliers to upgrade testing facilities. Education and healthcare segments, albeit smaller, display double-digit growth as administrators equate furniture quality to user well-being, procuring anti-bacterial laminates and rounded-edge desks for safety compliance. BIS norms effective 2026 are expected to prune non-certified vendors from institutional tenders, consolidating demand with established brands poised to scale the India luxury furniture market size in the coming years.

By Material: Wood Dominance Reinforces Sustainability Focus

Wood products commanded a 58.72% share in 2025 alongside the quickest 9.03% CAGR, reaffirming their cultural and aesthetic appeal in India. High-net-worth consumers prefer American white oak, black walnut, and Burmese teak for their grain character, leading U.S. wood exports to India to hit USD 84 million in 2023. ESG-aligned buyers request FSC or PEFC certificates, and hotel brands increasingly list these as non-negotiable in RFQs. Engineered veneers bonded with E0 low-formaldehyde resins provide a mid-premium alternative, widening material accessibility without compromising environmental credentials.

Metals, accounting for an 18.55% share in 2025, migrate from pure office settings to residential accent pieces such as matte-brass bar cabinets or gunmetal canopy beds. Demand for powder-coated steel bases in marble-top dining tables showcases cross-material harmony aimed at younger luxury buyers. Glass integration rises in niche smart-home products—transparent OLED panels embedded in coffee tables display news feeds or mood lighting presets. Leather maintains a loyal following in recliners and executive chairs, but vegan alternates such as cactus leather garner attention from eco-sensitive consumers. Sustainable composites—bamboo-resin boards, mycelium-grown panels—are nascent yet record 12-15% annual growth, suggesting a disruptive frontier for the India luxury furniture market.

By Distribution Channel: B2B Project Sales Accelerate

Although B2C retail dominated with a 66.88% share in 2025, B2B project sales demonstrate a superior 7.91% CAGR, propelled by multi-property hotel rollouts and Grade-A office fit-outs. Procurement cycles in B2B are consultant-driven, featuring detailed submittals, mock-ups, and factory audits that favor organized suppliers. Brands often secure furnishing packages worth USD 1–3 million per five-star hotel, translating to predictable production schedules. Value-added services—onsite installation, after-sales maintenance, strengthen long-term relationships, and justify premium pricing.

In retail, experiential flagship stores function as storytelling arenas, showcasing limited-edition collaborations and offering material libraries for bespoke orders. E-commerce growth leans on VR room planners that cut decision anxiety, elevating conversion rates and average order values. Click-and-collect formats allow customers in tier-3 towns to order online and pick up at franchise partners, mitigating last-mile breakage risks. Interior designers increasingly act as channel influencers, steering client budgets toward partner brands in exchange for specification fees, thereby softening the retail-project dichotomy inside the India luxury furniture market.

Geography Analysis

West India maintained leadership with a 31.05% share in 2025, anchored by Mumbai’s concentration of ultra-high-net-worth households and a steady influx of expatriate professionals. Maharashtra’s industrial corridors house specialized veneer factories and finishing plants that sync seamlessly with the JNPT port for timely imported wood clearances. Premium residential towers in South Mumbai and Pune’s IT hubs often include turnkey furnishing packages, enabling furniture brands to bundle products and services, raising per-unit revenue. The state government’s art-and-furniture cluster policy offers land rebates and power subsidies, stimulating capacity expansion among premium manufacturers.

South India contributed a 26.42% share in 2025, underpinned by Bangalore’s technology salaries and Chennai’s export-oriented manufacturing. Karnataka’s furniture parks leverage CNC machining and automated sanding lines to deliver precision consistent with global benchmarks. Hyderabad’s luxury villa projects, spurred by pharma and tech wealth, commission bespoke teak joinery fused with smart controls. Kerala’s design language, known for its minimalist coastal themes, inspires seaside resort orders, blending open-grain teak with brass inlay. The result is a rich tapestry where regional craftsmanship meets contemporary silhouettes, broadening appeal across the India luxury furniture market.

North India, led by Delhi-NCR, captured a 21.03% share in 2025. Proximity to political power and diplomatic missions drives demand for high-security, luxury fit-outs in chancery projects and government guest houses. IKEA’s INR 7,000 crore multi-format plan in Noida and Gurgaon signals confidence in the region’s purchasing power [BUSINESS-STANDARD.COM]. Furniture clusters in Yamuna Expressway Industrial Development Authority benefit from plug-and-play sheds and logistical proximity to retail showrooms. Meanwhile, Chandigarh’s modernist heritage rekindles interest in mid-century design revivals, influencing catalogue themes for brands looking to diversify style portfolios.

North-East, East, and Central India collectively hold a 21.50% share in 2025 yet display the highest aggregate growth momentum. Infrastructure upgrades, including the Bharatmala highway program, shorten transit times to Guwahati and Agartala, making project deliveries viable. Boutique eco-resorts in Assam and Meghalaya commission bamboo and rattan furniture with contemporary finishes, marrying sustainability with local identity. Bhubaneswar’s smart-city blueprint reserves dedicated zones for furniture and décor startups, incubating local design talent. Central India’s mining towns, such as Raipur, witness rising discretionary income among managerial cadres, translating into demand for branded furniture stores. As connectivity and incomes improve, brands are tailoring compact-form-factor collections to suit smaller urban homes, cementing future growth for the India luxury furniture market.

Competitive Landscape

The India luxury furniture market is characterized by an evolving equilibrium between legacy conglomerates, global entrants, and fast-scaling digital natives, making the market moderately fragmented. Traditional giants like Godrej Interio are recasting themselves as lifestyle labels, inaugurating concept studios that emphasize story-led displays and artisan collaborations rather than broad-spectrum catalogues. International retailers, notably IKEA, localize assortments by pairing Scandinavian minimalism with Indian craft accents, thereby balancing global identity with regional sensibilities. Direct-to-consumer disruptors such as Wakefit and Wooden Street exploit online configurators and data-driven inventory management to compress lead times and undercut showroom overheads.

Partnerships around sustainable sourcing and smart-home integration emerge as decisive differentiators. Domestic brands are signing long-term FSC-certified timber contracts, while multinationals set up joint ventures with finishing-chemical specialists to embed low-VOC processes. Technology collaboration is equally intense: sensor-embedded recliners and app-controlled lighting desks enter prototypes, expanding functional narratives beyond aesthetics. Acquisitions gain pace, Japan’s KOKUYO taking over HNI India’s assets illustrates how foreign firms view Indian manufacturing bases as springboards for wider Asian supply networks. Overall, competitive rivalry hinges more on design agility, omnichannel fluency, and compliance credentials than on price wars.

The middle tier of regional players faces strategic crossroads. Some embrace white-label manufacturing for global brands, leveraging process certifications to climb the value chain. Others specialize in heritage craft niches, bone inlay from Rajasthan, or mother-of-pearl marquetry from Tamil Nadu, and sell through online marketplaces targeting export customers. As BIS norms tighten, organized players with audit readiness are positioned to absorb market share vacated by non-compliant workshops, potentially accelerating the formalization of the India luxury furniture market.

India Luxury Furniture Industry Leaders

Godrej Interio

Durian

IKEA India

Urban Ladder

Pepperfry

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: IKEA announced plans to increase local sourcing to 50% for its global business. The move anchors multi-year contracts for Indian suppliers of certified hardwood frames, textiles, and metal fixtures, positioning the country as a strategic export hub. Industry observers expect ripple effects in capacity expansions across upholstery and surface-treatment clusters.

- May 2025: Japan’s KOKUYO completed the acquisition of HNI India’s office furniture operations. KOKUYO gains a ready manufacturing base in Nagpur along with an installed client roster across the IT and BFSI sectors, while HNI offloads a non-core asset to focus on modular system innovations. The deal underscores growing foreign confidence in India’s commercial furniture demand trajectory.

- February 2025: IKEA launched e-commerce operations in Delhi-NCR months before physical stores. Partnering with Rhenus Logistics, the 150,000 sq ft warehouse in Gurugram facilitates 24-hour delivery across 1,200 SKUs, many in the India luxury furniture market’s upper-mid price bands. The digital-first strategy allows the brand to gauge product resonance and optimize in-store assortments ahead of launch.

- September 2024: HomeLane acquired Design Café in a share-swap deal and raised INR 2.25 billion from Hero Enterprise and WestBridge Capital. The integration triples design-service capacity and merges back-end factories, streamlining costs by pooling procurement volumes. Analysts project the combined entity to exceed INR 10 billion in revenue in FY 25, solidifying its foothold in turnkey luxury interiors.

India Luxury Furniture Market Report Scope

Luxury furniture is something that makes it easier to live a luxurious life. It has elements that are elegant, lavish, and indulgent. A complete background analysis of the Indian luxury furniture market, which includes an assessment of the luxury furniture market in India, emerging trends by segments and regional markets, significant changes in market dynamics, and a market overview, is covered in the report. The report also features qualitative and quantitative assessments by analyzing the data gathered from industry analysts and market participants across key points in the industry's value chain.

The India Luxury Furniture Market Is Segmented By Product Type (Lighting, Tables, Chairs, And Sofas; Accessories; Bedrooms; Cabinets; And Other Products), End User (Residential And Commercial), And Distribution Channel (Home Centers, Flagship Stores, Specialty Stores, Online, And Other Distribution Channels). The Market Size And Forecasts For The India Luxury Furniture Market In Volume (Thousand Metric Tons) And Value (USD) For All The Above Segments.

By Application

| Luxury Home Furniture | Chairs and Sofas |

| Tables (Side, Coffee, Dressing, etc.) | |

| Beds | |

| Wardrobes | |

| Dining Tables / Dining Sets | |

| Kitchen Cabinets | |

| Other Home Furniture (Bathroom, Outdoor, etc.) | |

| Luxury Office Furniture | Chairs |

| Tables | |

| Storage Cabinets | |

| Desks | |

| Sofas and Other Soft Seating | |

| Other Office Furniture | |

| Luxury Hospitality Furniture | |

| Other Applications (Educational Furniture, Healthcare Furniture, Retail Malls, Government Offices, etc.) |

By Material

| Wood |

| Metal |

| Glass |

| Leather |

| Plastic and Other Synthetics |

| Sustainable / Green Materials |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Flagship Store | |

| Other Distribution Channels | |

| B2B / Project |

By Geography

| North India |

| South India |

| West India |

| East India |

| Central India |

| North-East India |

| By Application | Luxury Home Furniture | Chairs and Sofas |

| Tables (Side, Coffee, Dressing, etc.) | ||

| Beds | ||

| Wardrobes | ||

| Dining Tables / Dining Sets | ||

| Kitchen Cabinets | ||

| Other Home Furniture (Bathroom, Outdoor, etc.) | ||

| Luxury Office Furniture | Chairs | |

| Tables | ||

| Storage Cabinets | ||

| Desks | ||

| Sofas and Other Soft Seating | ||

| Other Office Furniture | ||

| Luxury Hospitality Furniture | ||

| Other Applications (Educational Furniture, Healthcare Furniture, Retail Malls, Government Offices, etc.) | ||

| By Material | Wood | |

| Metal | ||

| Glass | ||

| Leather | ||

| Plastic and Other Synthetics | ||

| Sustainable / Green Materials | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Flagship Store | ||

| Other Distribution Channels | ||

| B2B / Project | ||

| By Geography | North India | |

| South India | ||

| West India | ||

| East India | ||

| Central India | ||

| North-East India | ||

Key Questions Answered in the Report

What is the projected value of the India luxury furniture market by 2031?

It is expected to reach USD 1.74 billion.

Which application segment is growing fastest?

Luxury hospitality furniture is expanding at an 8.48% CAGR owing to a record hotel pipeline.

Why are B2B project sales gaining traction?

Institutional buyers demand specification-grade products, fueling an 7.91% CAGR in B2B project sales.

How does ESG influence material choices?

Corporate procurements increasingly require FSC timber and GREENGUARD finishes, encouraging sustainable material adoption.

Which region is witnessing the quickest growth?

North-East India shows the fastest 8.07% CAGR as infrastructure and tourism investments accelerate demand.

What challenges does the industry face regarding skilled labor?

A shortage of trained carpenters and upholsterers slows lead times and raises wage costs, prompting brands to set up training academies.

Page last updated on: