India Fleet Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

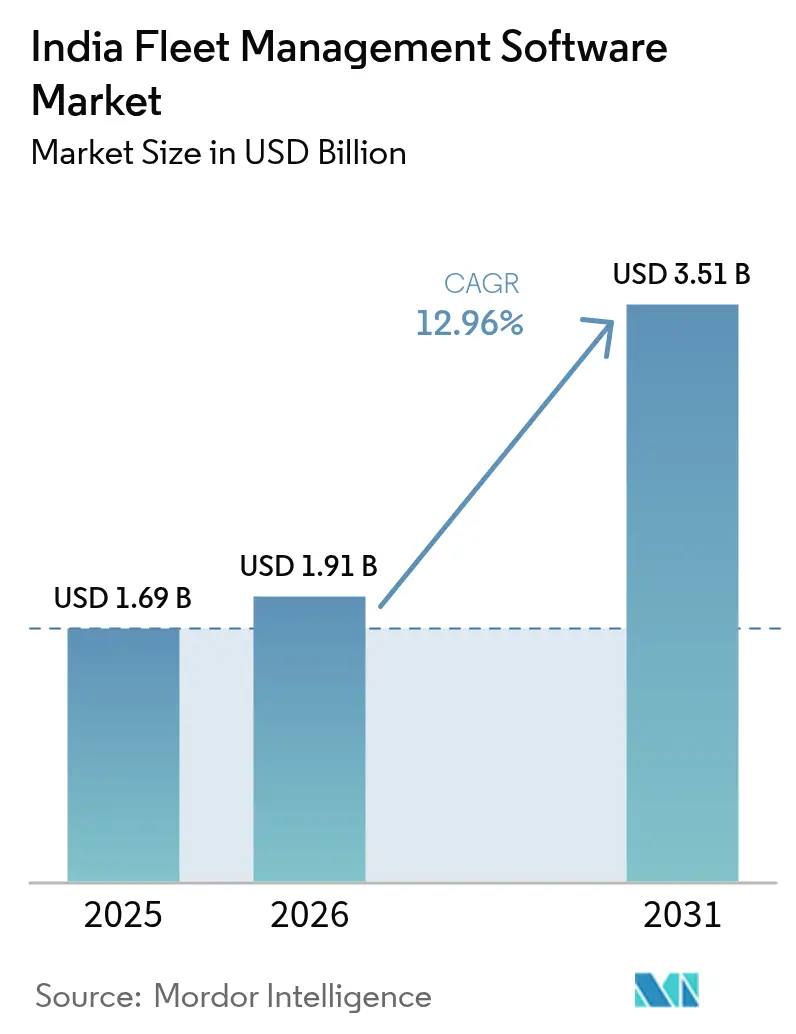

| Base Year Market Size (2025) | USD 1.69 Billion |

| Market Size (2026) | USD 1.91 Billion |

| Market Size (2031) | USD 3.51 Billion |

| Growth Rate (2026 - 2031) | 12.96% CAGR |

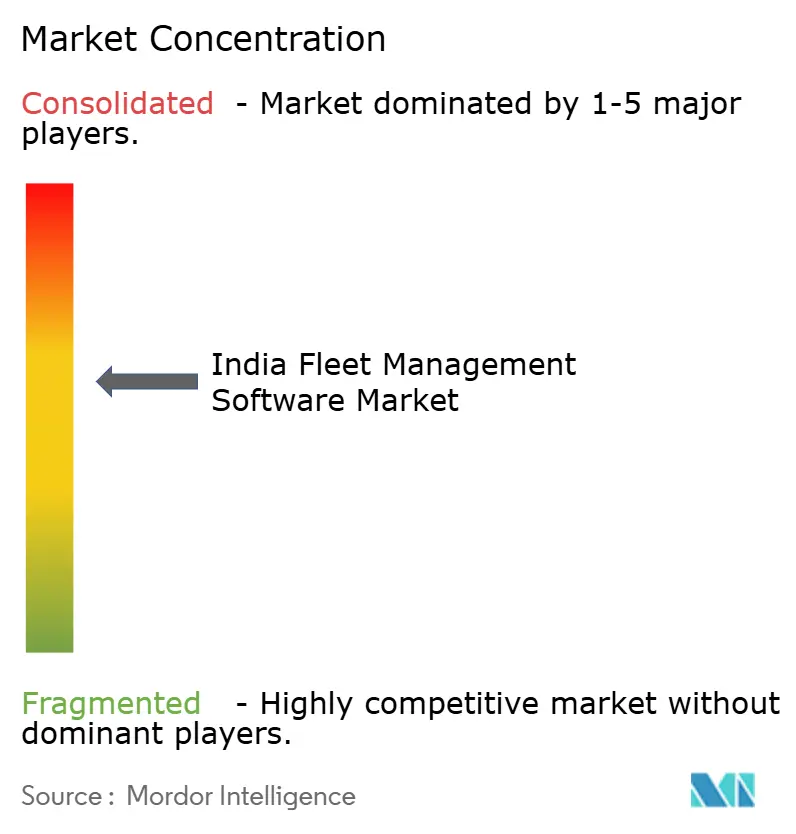

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Fleet Management Software Market Analysis by Mordor Intelligence

The India fleet management software market size in 2026 is estimated at USD 1.91 billion, growing from 2025 value of USD 1.69 billion with 2031 projections showing USD 3.51 billion, growing at 12.96% CAGR over 2026-2031. Robust expansion is underpinned by mandatory AIS-140 and IS-16833 compliance, volatile fuel economics that elevate total-cost-of-ownership pressure, and the digital push embedded in the National Logistics Policy 2022.[1]MarkLines Co., Ltd., “Government of India BS-VII, ADAS, and Safety Roadmap 2025,” marklines.com Cloud deployment dominates because pay-as-you-go pricing suits highly fragmented trucking ownership, while medium fleets anchor current volume even as large enterprise fleets log the fastest growth. Light commercial vehicles remain the backbone of goods movement, yet two-wheelers are reshaping last-mile economics amid India’s gig-economy surge. Competitive intensity is moderate, with roughly 250 connected-vehicle start-ups complementing global telematics leaders and legacy Indian providers.

Key Report Takeaways

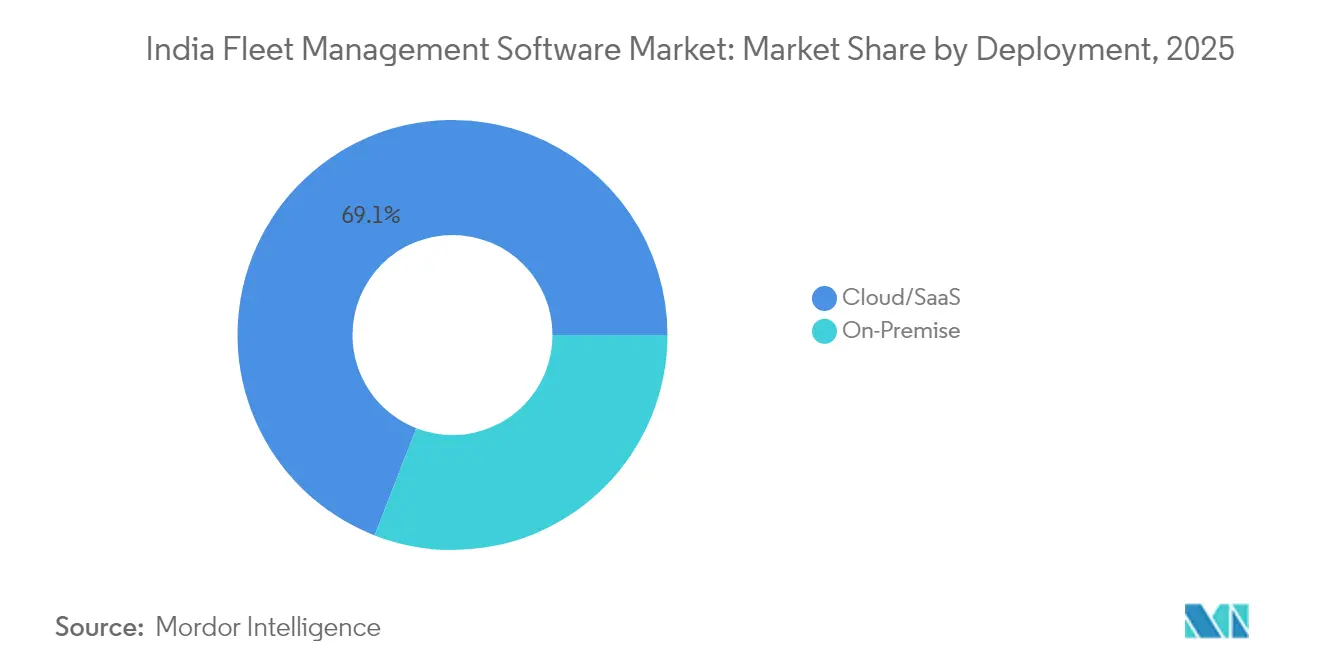

- By deployment, cloud/SaaS captured 69.10% of the India fleet management software market share in 2025 and is expanding at a 13.55% CAGR to 2031.

- By fleet size, medium fleets held 51.10% share of the India fleet management software market size in 2025, while large fleets are projected to grow at 13.78% CAGR through 2031.

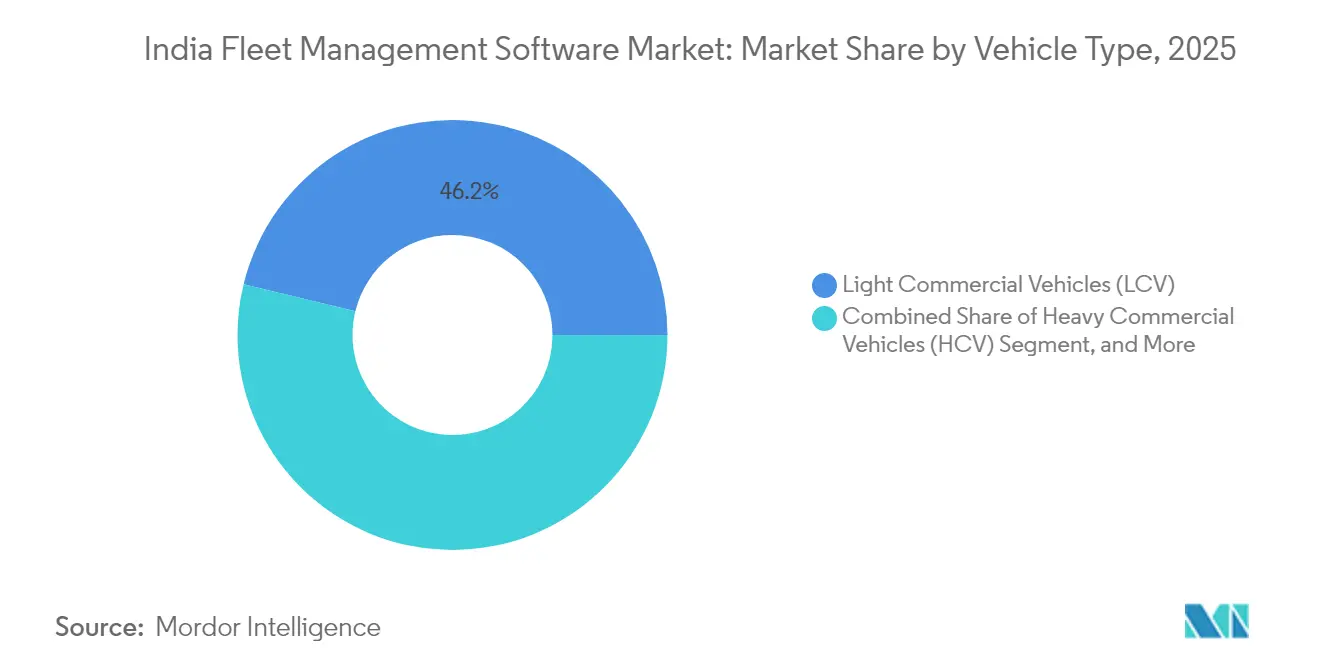

- By vehicle type, light commercial vehicles led with 46.20% share of the India fleet management software market in 2025, and two-wheelers are advancing at a 13.92% CAGR to 2031.

- By end-user industry, logistics and transportation accounted for 41.85% of the 2025 revenue of the India fleet management software market; passenger transport is registering the highest 13.84% CAGR to 2031.

- By functionality, tracking and telematics retained 34.35% share of the India fleet management software market in 2025; analytics and reporting is forecast to rise at 14.12% CAGR through 2031.

- By region, South India commanded 36.05% of the 2025 revenue of the India fleet management software market, while West India is on track to post a 14.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Fleet Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AIS-140 and IS-16833 compliance mandates | +2.8% | National, with early gains in Delhi, Mumbai, Bangalore | Short term (≤ 2 years) |

| Volatile fuel prices driving Total-Cost-of-Ownership (TCO) reduction | +2.2% | Global, spill-over to rural transport corridors | Medium term (2-4 years) |

| E-commerce and on-demand logistics boom | +2.5% | Urban centers, expanding to Tier-2/3 cities | Medium term (2-4 years) |

| Declining IoT hardware costs and GNSS accuracy gains | +1.8% | National, with stronger adoption in tech-forward regions | Long term (≥ 4 years) |

| OEM data-monetization partnerships with FMS vendors | +1.4% | Manufacturing hubs in Tamil Nadu, Maharashtra, Gujarat | Long term (≥ 4 years) |

| EV fleet electrification and energy-aware routing demand | +1.9% | Metro cities, government fleet corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AIS-140 and IS-16833 Compliance Mandates Drive Market Acceleration

Government directives compel every commercial vehicle to install GPS-enabled tracking devices that transmit real-time data to state transport servers. The mandates extend to panic buttons and driver-behavior monitoring, transforming fleet software from optional optimization to compulsory safety infrastructure. Small and medium operators that historically deferred tech spending now face time-bound compliance, triggering rapid adoption across the India fleet management software market. Vendors that embed over-the-air rule updates gain an edge because regulatory specifications evolve quickly. The compliance surge is also generating retrofit demand among used-truck dealers, broadening the addressable base beyond new-vehicle sales.

Volatile Fuel Prices Catalyze TCO-Focused Digitization

Fuel accounts for 40%–50% of trucking operating costs; recent price swings have eroded razor-thin margins and hastened technology uptake to rein in idling, speeding, and route detours.[2]Eicher Trucks & Buses, “AC Cabins Mandatory for Indian Trucks by 2025,” eichertrucksandbuses.com Fleet software now couples fuel sensors with predictive analytics that benchmark consumption across similar duty cycles, empowering operators to negotiate with drivers and shippers using objective data. Cloud dashboards that aggregate diesel invoices, driver scorecards, and route heatmaps deliver quick ROI, a persuasive narrative for cost-sensitive fleets evaluating subscription outlays.

E-Commerce and On-Demand Logistics Boom Reshapes Fleet Requirements

Same-day delivery expectations oblige fleets to manage unpredictable volumes, multivehicle mixes, and late-night dispatches. Modern platforms, therefore, integrate routing engines that recalculate ETAs every few seconds, chatbots that update customers, and APIs that feed delivery status to e-commerce storefronts.[3]CarDekho, “Charging Infrastructure in India,” cardekho.com Tier-2 and Tier-3 city penetration of online retail magnifies demand for hyperlocal route optimization and two-wheeler fleet orchestration. Driver performance analytics gain prominence because consumer-facing delivery times directly influence seller ratings and repeat sales. Platform scalability becomes a non-negotiable checklist item for procurement heads at large marketplaces.

Declining IoT Hardware Costs Democratize Advanced Telematics

Telematics unit prices have fallen even as sensor payloads expand to include accelerometers, engine diagnostics, and video feeds. Entry-level GPS devices now retail at about INR 175 per month, placing digital tracking within reach of fleets with fewer than five vehicles. The cost curve also unlocks large-scale pilot programs for camera-based driver monitoring that were financially prohibitive two years ago. As IoT affordability converges with rising cellular coverage, software vendors package predictive maintenance alerts and vehicle-health dashboards as standard features, quickening penetration into rural transport corridors and specialized haulage segments such as reefer or tanker fleets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Traditional fleet-operator and driver-union technology resistance | -1.8% | National, stronger in traditional transport hubs | Short term (≤ 2 years) |

| High capex for multi-sensor telematics in SME fleets | -2.1% | Rural and semi-urban fleet operators | Medium term (2-4 years) |

| Rural data-connectivity gaps hindering always-on tracking | -1.4% | Rural transport corridors, North-East regions | Medium term (2-4 years) |

| 2G/3G sunset forcing legacy-device retrofit costs | -0.9% | Pan-India, gradual phase-out timeline | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Traditional Operator and Union Resistance Limits Early Uptake

Long-haul drivers often equate telematics with surveillance, and small-fleet owners view app-based freight platforms as threats to decades-old broker ties.[4]Intugine Technologies, “Leveraging Tracking Data in Supply Chain,” intugine.com The skepticism is amplified by an acute driver shortage that pushes employers to prioritize retention over strict monitoring. Successful vendors reframe software as a welfare enabler offering SOS alerts, salary advances, and in-cab infotainment to shift the narrative from control to empowerment. State-level awareness campaigns by transport departments are gradually softening resistance, but cultural change remains a multi-year journey.

High Capex for Multi-Sensor Telematics Constrains SMEs

While basic tracking is affordable, full-stack telematics covering video, tire pressure, and ADAS can cost upwards of INR 12,000 per vehicle, a hurdle for fleets running fewer than twenty trucks. Financing schemes tied to OEMs and non-bank lenders have begun to gain traction, yet penetration remains uneven. Temperature-controlled trucking and hazardous goods transport suffer the most because regulations mandate extra sensors, inflating capital outlays further. Vendor innovation in plug-and-play hardware and per-trip billing models is critical to closing the affordability gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Dominance Accelerates Digital Adoption

Cloud solutions claimed 69.10% of 2025 revenue, translating to the largest India fleet management software market share within the deployment spectrum. Cloud platforms minimize upfront investment, a decisive factor for India’s 80% small-operator landscape. Pay-per-vehicle subscriptions, automatic over-the-air updates, and API-based integrations allow fleets to scale features without new servers. Over the next five years, this flexibility fuels a 13.55% CAGR, the fastest of any deployment mode.

On-premise installations remain relevant for large enterprises and public agencies requiring data residency or custom workflow logic. However, they lag in innovation velocity because each regulatory or feature update demands on-site patches. Amid the surge in electric vehicles and driver-scorecard analytics, cloud vendors push weekly releases, widening the functionality gap. Combined with India’s improving 4G and 5G coverage, cloud subscription is expected to maintain its commanding India fleet management software market size leadership.

By Fleet Size: Medium Fleets Lead While Large Enterprises Drive Growth

Medium fleets accounted for 51.10% of 2025 spending, reflecting the abundance of carriers that own 20–100 vehicles. Their operational complexity is high enough to warrant digitization but still agile enough to experiment with new vendors. These operators typically begin with tracking and upgrade to route optimization and maintenance modules within twelve months, driving sticky monthly recurring revenue.

Large fleets above 100 vehicles posted the highest 13.78% CAGR and are pivotal to forecasts of the India fleet management software market. Consolidation in e-commerce logistics and organized 3PLs produces mega-fleets that require real-time dashboards, driver engagement apps, and enterprise resource planning integration. Small fleets under twenty vehicles trail in adoption because owners tend to calculate payback in weeks, not months. Freemium mobile-first offerings remain the entry gateway for this cohort.

By Vehicle Type: LCV Dominance Meets Two-Wheeler Disruption

Light commercial vehicles held 46.20% revenue in 2025, reinforcing their centrality to intercity and regional freight movement. Aggregators favor LCVs because they balance payload and maneuverability along India’s diverse road network. Heavy commercial vehicles dominate long haul, but upgrade cycles are slower, dampening software wallet share.

Two-wheelers achieved the fastest 13.92% CAGR thanks to food delivery, quick commerce, and hyperlocal courier services that thrive on motorcycles and e-scooters. Telematics hardware for motorcycles is inexpensive, and installation takes minutes, enabling fleet roll-outs of thousands of riders in a single week. Electric variants further boost telematics demand because operators crave battery state-of-charge and swap-station location intelligence.

By End-User Industry: Logistics Leadership with Passenger Transport Acceleration

Logistics and transportation companies generated 41.85% of 2025 revenue, cementing their status as the anchor vertical within the India fleet management software industry. Route density, stringent service-level agreements, and fuel cost volatility force continuous optimization, sustaining software investment pipelines.

Passenger transport covering school buses, state road transport corporations, and ride-hailing fleets is growing at a 13.84% CAGR. AIS-140 mandates and rising consumer safety expectations propel real-time monitoring, panic-button integration, and driver-attendance logging. Manufacturing, utilities, and waste management collectively form a steady mid-tier that values compliance reporting and uptime analytics for specialized equipment.

By Functionality: Tracking Foundation Enables Analytics Innovation

Tracking and telematics occupied 34.35% of 2025 spend, reaffirming that “know-where-my-vehicle-is” remains the baseline pain point in the India fleet management software market. Once tracking is installed, fleets typically add maintenance, compliance, and fuel modules within a year, but analytics and reporting already show a brisk 14.12% CAGR.

Analytics dashboards mine historical trip data to forecast part failures, benchmark driver behavior, and optimize load scheduling. A surge in EV adoption further inflates demand for energy-management layers that harmonize battery usage with route length and charger availability. As enterprise customers demand single-pane-of-glass visibility, vendors bundle business-intelligence widgets and no-code report builders to outflank rivals.

Geography Analysis

South India contributed 36.05% of 2025 revenue, reflecting its dense concentration of technology adopters in Bengaluru, Chennai, and Hyderabad. Automotive OEM plants and supply clusters in Tamil Nadu and Karnataka amplify demand for real-time transport visibility, making the region an early test bed for ADAS-ready telematics.

West India, anchored by Mumbai’s finance hub and Gujarat’s industrial corridors, is projected to record the highest 14.02% CAGR through 2031. State EV incentives and the Western Dedicated Freight Corridor strengthen the business case for cloud-connected fleets equipped with energy-aware routing. Tier-2 cities such as Pune and Surat are emerging pockets of software pilots aimed at factory-to-port logistics. North India, led by Delhi NCR, sustains sizable procurement volumes driven by government fleet upgrades and interstate warehousing networks. Central India benefits from its crossroads geography and mining activity, adopting telematics for asset security along remote haul roads. East and North-East India remain nascent but receive a tailwind from the BharatNet broadband rollout and public-sector bus modernizations. Gradual 5G expansion is expected to narrow regional penetration gaps across the India fleet management software market.

Competitive Landscape

The India fleet management software market features a moderately concentrated field where the top five providers account for roughly 45% of 2024 revenue. Global brands such as Trimble, Samsara, and Geotab leverage enterprise relationships and hardware ecosystems to win large multi-state contracts. Indigenous players LocoNav, FleetX, TrackoBit, Uffizio, and Axestrack compete aggressively on localization, vernacular mobile-app interfaces, and sub-USD 3 per-vehicle monthly pricing tiers.

Differentiation is increasingly vertical. FleetX offers cold-chain compliance dashboards, whereas TrackoBit caters to on-demand delivery fleets with two-wheeler-specific telematics devices. Hardware-agnostic SaaS models coexist with end-to-end packages bundling sensors and SIMs, enabling customers to mix and match based on capex appetite. OEM tie-ups are pivotal: Tata Motors’ Fleet Edge now connects half a million vehicles, and VE Commercial Vehicles embeds IoT gateways on AC-ready truck cabins scheduled for production in late 2025.

Pricing flexibility and rapid regulatory updates decide tender outcomes in government bus, school transport, and mining concessions, where AIS-140 audit trails are scrutinized monthly. As fleets electrify, vendors scramble to add charger-management APIs and battery-health analytics, opening a white-space arena where start-ups like Griden Technologies integrate chargers, telematics, and payment gateways.

India Fleet Management Software Industry Leaders

Trimble Mobility Solutions India Private Limited

BT TechLabs Private Limited (LocoNav)

fleetx Technologies Private Limited

Uffizio India Software Consultants Private Limited

Web World Digital Solutions Private Limited (TrackoBit)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Axestrack gained recognition in Gartner’s fleet-telematics guide, validating Indian providers globally.

- February 2025: SMEStreet reported rapid EV-charging build-out, spurring integration demand for charger management.

- February 2025: TrackoBit emphasized telematics’ role in road safety improvement amid high accident rates.

- January 2025: Griden Technologies showcased cloud-based charger-management software targeting electric fleets.

- January 2025: The government issued a 2025 roadmap covering BS-VII emission norms, e-rickshaw safety, and truck ADAS, escalating compliance requirements.

- January 2025: Intangles highlighted predictive maintenance and AI demand forecasting, reshaping fleet operations.

India Fleet Management Software Market Report Scope

Fleet Management Software is software that allows people to perform a number of separate tasks in the management of any or all aspects related to an organization's vehicle fleet, and they can do this on their own. The India Fleet Management Software Market offers an in-depth stakeholder analysis that includes Fleet management solution providers, fleet leasing companies, fleet management companies, etc. The market is segmented based on deployment mode and end-users, including Logistics, manufacturing, and others such as Corporate, Education, etc.

The India Fleet Management Software Market is segmented by Deployment (On-Premise, Cloud) and End-User (Logistics, Manufacturing). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| On-Premise |

| Cloud/SaaS |

| Small (<20 vehicles) |

| Medium (20–100) |

| Large (>100) |

| Light Commercial Vehicles (LCV) |

| Heavy Commercial Vehicles (HCV) |

| Passenger Cars |

| Two-Wheelers |

| Logistics and Transportation |

| Manufacturing and Industrial |

| Passenger Transport (Bus, Taxi, School) |

| Other End-User Industries (Corporate, Utilities, Waste Management) |

| Tracking and Telematics |

| Route Optimisation and Navigation |

| Maintenance and Diagnostics |

| Compliance and Safety |

| Fuel and Energy Management |

| Analytics and Reporting |

| North India |

| West India |

| South India |

| East and North-East India |

| Central India |

| By Deployment | On-Premise |

| Cloud/SaaS | |

| By Fleet Size | Small (<20 vehicles) |

| Medium (20–100) | |

| Large (>100) | |

| By Vehicle Type | Light Commercial Vehicles (LCV) |

| Heavy Commercial Vehicles (HCV) | |

| Passenger Cars | |

| Two-Wheelers | |

| By End-User Industry | Logistics and Transportation |

| Manufacturing and Industrial | |

| Passenger Transport (Bus, Taxi, School) | |

| Other End-User Industries (Corporate, Utilities, Waste Management) | |

| By Functionality / Module | Tracking and Telematics |

| Route Optimisation and Navigation | |

| Maintenance and Diagnostics | |

| Compliance and Safety | |

| Fuel and Energy Management | |

| Analytics and Reporting | |

| By Region | North India |

| West India | |

| South India | |

| East and North-East India | |

| Central India |

Key Questions Answered in the Report

What is the 2026 value of the India fleet management software market?

It stands at USD 1.91 billion, with a forecast to reach USD 3.51 billion by 2031.

Which deployment mode shows the strongest growth?

Cloud/SaaS, expanding at a 13.55% CAGR as fleets favor low-capex, scalable solutions.

How fast is the two-wheeler telematics segment expanding?

It is registering a 13.92% CAGR through 2031, the fastest among all vehicle categories.

Which region outpaces others in growth?

West India leads with a projected 14.02% CAGR thanks to industrialization and EV incentives.

Why are compliance mandates crucial for adoption?

AIS-140 and IS-16833 make GPS tracking and safety features compulsory, accelerating technology uptake across all fleet sizes.

What functionality is growing quickest beyond basic tracking?

Analytics and reporting, forecast to rise at 14.12% CAGR as fleets seek data-driven optimization.

Page last updated on: