Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

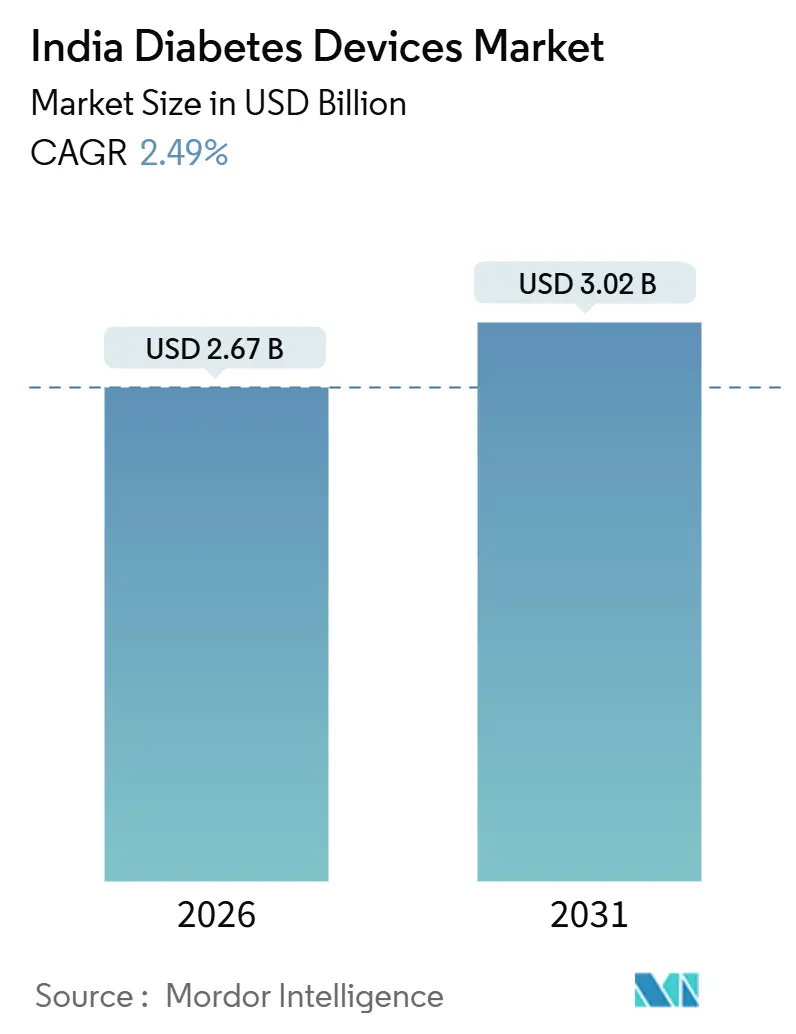

| Market Size (2026) | USD 2.67 Billion |

| Market Size (2031) | USD 3.02 Billion |

| Growth Rate (2026 - 2031) | 2.49% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Diabetes Devices Market Analysis by Mordor Intelligence

The India Diabetes Devices Market size is estimated at USD 2.67 billion in 2026, and is expected to reach USD 3.02 billion by 2031, at a CAGR of 2.49% during the forecast period (2026-2031).

Demand is shifting from high-volume self-monitoring blood glucose (SMBG) strips toward higher-value continuous glucose monitoring (CGM) sensors and advanced insulin-delivery solutions, driven by the earlier onset of Type 2 diabetes, wider adoption of telehealth, and the Production-Linked Incentive (PLI) scheme that is bolstering local manufacturing. Yet out-of-pocket costs, patchy reimbursement, and uneven cold-chain capacity keep the India diabetes devices market growth contained to low single digits. Multinational incumbents are responding with localized assembly. Roche now builds Accu-Chek Active meters in Chennai to protect share against indigenous challengers that target price-sensitive users with low-cost insulin pumps and cartridges. Telemedicine traction is another lever; eSanjeevani surpassed 318.6 million cumulative consultations in 2024, normalizing home-based glucose tracking and fueling the India diabetes devices market’s pivot to connected care.

Key Report Takeaways

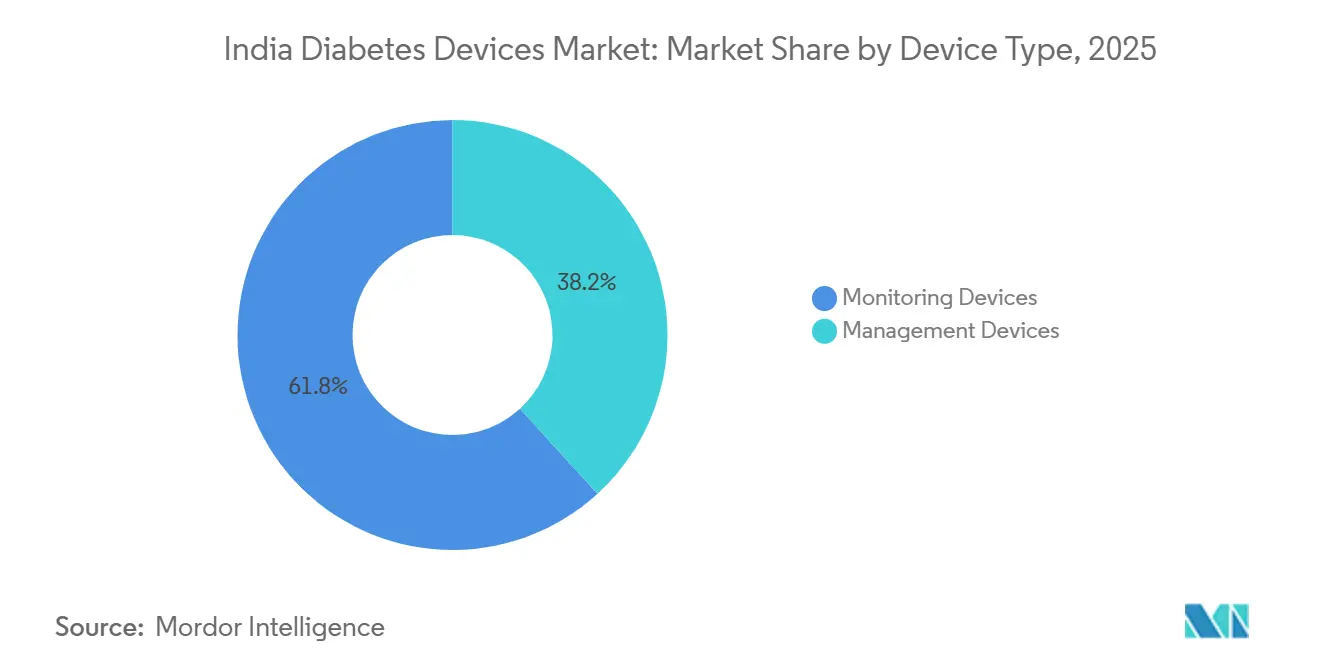

- By product type, monitoring devices commanded 61.78% revenue share in 2025; management devices are projected to expand at a 3.53% CAGR through 2031.

- By patient type, Type-2 diabetes accounted for 91.43% of the India diabetes devices market share in 2025, while Type-1 diabetes is forecast to advance at a 4.89% CAGR through 2031.

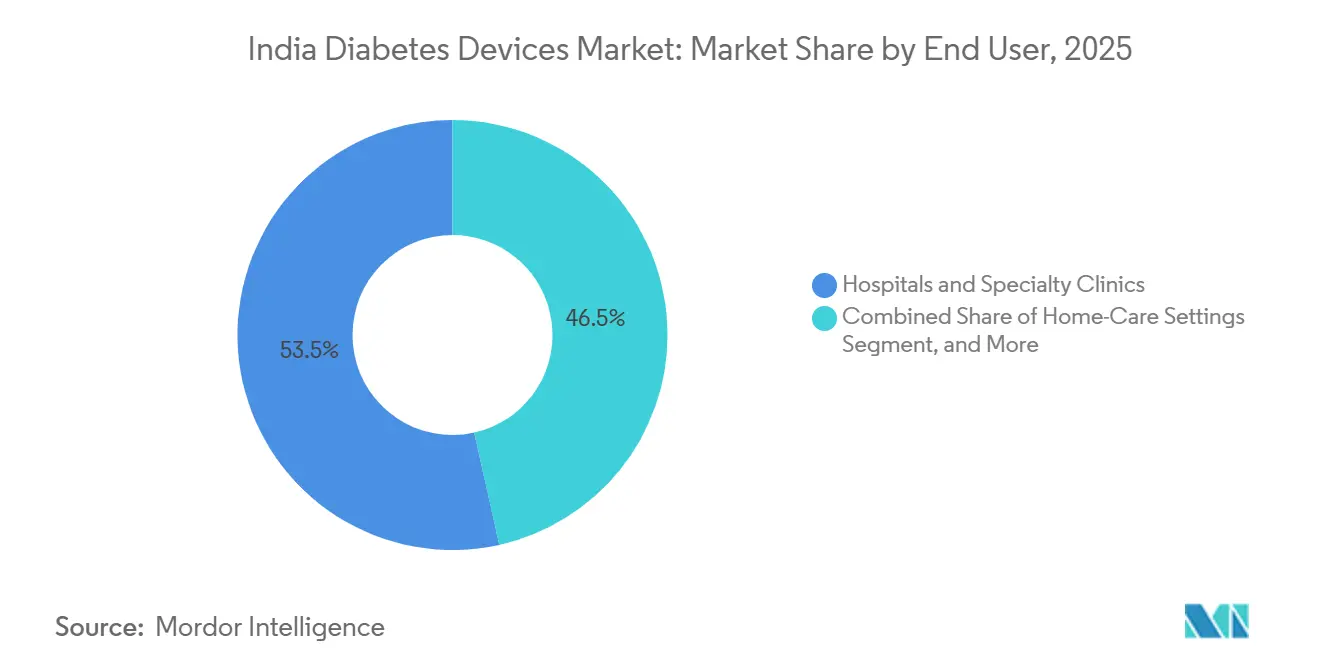

- By end user, hospitals and specialty clinics held 53.48% of the India diabetes devices market size in 2025, and home-care settings are set to grow at a 5.17% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Diabetes Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Obesity Among Youth Accelerating Earlier-Onset Diabetes | +0.6% | National, with concentration in urban metros | Medium term (2-4 years) |

| Expanding Public Reimbursement for CGM Sensors | +0.5% | National, early gains in CGHS/ECHS beneficiary clusters | Long term (≥ 4 years) |

| Rising Prevalence & Earlier Onset of Type-2 Diabetes | +0.4% | National, accelerating in tier-2 and tier-3 cities | Medium term (2-4 years) |

| Government PLI Scheme Spurring Local Diabetes-Device Manufacturing | +0.3% | National, greenfield projects in Gujarat, Tamil Nadu, Karnataka | Long term (≥ 4 years) |

| Pharmacy-Led Diabetes-Management Programs Boosting SMBG Adherence | +0.2% | Urban metros and tier-1 cities with organized retail pharmacy | Short term (≤ 2 years) |

| Employer-Funded Health-Tech Benefit Platforms Widening Device Access | +0.2% | Corporate hubs in Bengaluru, Mumbai, NCR, Hyderabad | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Obesity Among Youth Accelerating Earlier-Onset Diabetes

India’s adolescent obesity wave is pulling diabetes incidence into the under-35 cohort, creating multi-decade device demand. A 2024 Journal of the Endocrine Society study reported 17.9% diabetes prevalence among Indians below 35 years.[1]Journal of the Endocrine Society, “Prevalence of Diabetes and Pre-Diabetes in Adolescents in India,” oxfordacademic.com Device makers are repositioning: Dexcom launched ONE+ in 2024 at INR 4,000 per month, promoting smartphone-linked insights for young Type 2 users. Employer wellness plans follow suit, with MediBuddy data showing 24.40% pre-diabetes prevalence in employees aged 18-45, prompting group policies that bundle CGM rentals. Convergence of dyslipidemia and hypertension in obese youth strengthens the business case for integrated CGM platforms over stand-alone glucometers. The India diabetes devices market increasingly orients product roadmaps around this technology-savvy demographic.

Expanding Public Reimbursement for CGM Sensors

The Central Government Health Scheme raised the ceiling to INR 300,000 for sensor-augmented pumps and INR 4,000 for 14-day CGM use in its 2024 rate list.[2]Central Government Health Scheme, “CGHS Rate List 2024,” cghs.gov.in Although only 4 million beneficiaries currently qualify, the policy shift signals strategic support for continuous monitoring. Tamil Nadu’s state plan added annual CGM coverage for Type-1 patients, capping benefits at INR 50,000. Limited physician familiarity stalls uptake: the Indian Diabetes Federation found fewer than 30% of primary-care doctors were trained to interpret ambulatory glucose profiles. Still, the reimbursement tailwind is material to the India diabetes devices market trajectory as other states emulate early adopters.

Rising Prevalence and Earlier Onset of Type-2 Diabetes

The Indian Council of Medical Research counted 101 million diagnosed diabetics and 136 million people in pre-diabetes in 2024, with incidence cresting in the 30-45 bracket.[3]Indian Council of Medical Research, “ICMR-INDIAB Study,” icmr.gov.in Earlier insulin initiation drives demand for disposable pens and prefilled cartridges. Novo Nordisk introduced Ozempic in December 2025 at INR 2,200 per week, demonstrating pharmaceutical recognition that convenience trumps cost for upwardly mobile Type 2 cohorts. Real-world telemedicine data from Jothydev’s Diabetes & Research Centre showed that long-term complication rates fell to 9.8% under digital monitoring, underscoring the clinical value of connected SMBG and CGM programs.

Government PLI Scheme Spurring Local Diabetes-Device Manufacturing

The INR 3,420 crore PLI program has green-lighted 19 greenfield projects and generated cumulative device sales worth INR 8,039 crore by 2024. Schott’s 2025 commissioning of borosilicate cartridge tubing in Gujarat slashed insulin-device lead times from 12 weeks to 4 weeks. Roche’s Chennai assembly line cut landed meter costs by 15%, letting it underprice Chinese imports in tier-2 pharmacies. These milestones reduce import dependency, stabilize supply, and lift the India diabetes devices market toward higher local value added.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Out-of-Pocket Costs on Testing Consumables | -0.4% | National, acute in tier-2 and tier-3 cities | Medium term (2-4 years) |

| Low CGM-Prescription Awareness Among Primary-Care Physicians | -0.3% | Rural and semi-urban areas with limited specialist access | Long term (≥ 4 years) |

| Patchy Cold-Chain Capacity for Insulin Cartridges in Tier-3 Cities | -0.2% | Tier-3 cities and rural distribution networks | Medium term (2-4 years) |

| Data-Privacy Concerns Around Connected Pumps & Apps | -0.1% | Urban metros with higher digital-health adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Costs on Testing Consumables

SMBG strips cost INR 380-1,993 per pack, implying an annual spend of INR 13,860-19,930 for twice-daily testing. Abbott’s FreeStyle Libre 3 sensor at INR 5,000 every 14 days lifts annual CGM spend to INR 130,000. These figures exceed the median household income in many tier-3 cities, forcing patients to ration tests and slowing the transition to CGM. Private insurers cap diabetes consumable reimbursement at around INR 10,000 per year, covering less than 10% of CGM expenses. Affordability remains the sharpest brake on the India diabetes devices market.

Low CGM-Prescription Awareness Among Primary-Care Physicians

Primary-care doctors manage 70% of India’s diabetic patients, yet the Indian Diabetes Federation survey shows fewer than 30% have formal CGM training. Consultation slots average five minutes, inadequate for sensor education. Abbott’s Libre 2 Plus eliminates calibration to ease workflows, but concerns about data overload persist. Endocrinologists, mostly metro-based, prescribe CGM at quintuple the general-practice rate, leaving rural users underserved. Until tele-mentorship and CME credits are tied to CGM competence, physician inertia will continue to dampen the expansion of the India diabetes devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Management Devices Outpace Monitoring on Insulin-Delivery Innovation

Management devices are forecast to post a 3.53% CAGR through 2031, outstripping monitoring counterparts. Demand rides on rapid insulin-pump uptake among 1.2 million Type-1 patients and swelling disposable-pen use in urban Type-2 cohorts. Medtronic’s MiniMed 780G hybrid closed-loop system, launched in 2024, automatically adjusts basal insulin every five minutes and has widened time-in-range by 15% in Indian trials. AgVa Healthcare’s INSUL pump, locally priced at INR 24,999, undercuts imported pumps by 90% and integrates Bluetooth dosing logs, capturing value-conscious consumers. Schott’s domestic cartridge tubing reduced landed costs on insulin pens by 20%, encouraging Novo Nordisk to phase out vial formats in favor of FlexPen devices.

Monitoring devices still delivered a 61.78% revenue share in 2025, buoyed by 80 million glucometer users; however, their 1.9% CAGR lags behind the market pace. SMBG strips remain the default for price-sensitive buyers, but CGM is the fastest-growing sub-segment. Abbott’s Libre 3 sensor measures just 2.9 mm in diameter and beams one-minute readings via Bluetooth, while Dexcom’s ONE+ offers a 10-day sensor life at INR 4,000 per month. Combined, these launches have nudged the India diabetes devices market toward continuous data capture, although premium pricing keeps penetration below 7% of diagnosed diabetics.

By Patient Type: Type-1 Segment Accelerates on Pediatric-Onset Surge

Type-2 cases dominate volume at 91.43% in 2025, yet the Type-1 slice of the India diabetes devices market size is growing nearly twice as fast, posting a 4.89% CAGR to 2031. Earlier pediatric diagnoses and universal insulin dependency drive intensive device use. The MiniMed 780G capitalizes on this need with Guardian 4 sensor integration that cuts hypoglycemia events by 30%. School-based awareness programs in Bengaluru and Delhi have doubled the number of pediatric pump initiations since 2024, aided by CGHS coverage ceilings that now reimburse up to INR 300,000 for sensor-augmented pumps.

Type 2 patients are migrating from episodic finger sticks toward real-time tracking as employer wellness mandates expand. GLP-1 launches add momentum; Ozempic’s once-weekly dosing at INR 2,200 lowers daily injection burden and complements CGM dashboards for dose titration. As tele-diabetes clinics extend reach, Type-2 users will integrate SMBG and CGM data, sustaining the broader India diabetes devices market growth.

By End User: Home-Care Settings Surge on Telehealth Integration

Hospitals and specialty clinics retained 53.48% of 2025 revenue because initial CGM prescriptions and pump initiations require supervised titration. Nonetheless, home-care settings are projected to deliver the fastest growth at a 5.17% CAGR, lifting their share of the 318.6 million consultations provided by eSanjeevani, which offers a scalable physician interface for remote dose adjustments. The Ayushman Bharat Digital Mission has issued 568 million health IDs, enabling patients to share their CGM streams with doctors and insurers in real-time. Roche’s channel partnerships with Phable and PharmEasy bundle Accu-Chek meters with three-month digital coaching, demonstrating how pharmacy-integrated programs can reinforce adherence.

Primary-care and diabetes centers, though smaller by value, influence device adoption curves. BeatO’s pharmacy-linked SMBG service, covering 1.5 million users, triggers teleconsults based on strip refill data, resulting in a 10% glucose reduction within 90 days. Employer-funded platforms echo this trajectory; MediBuddy’s cohort analysis spurred corporations to include CGM rentals in benefits. Multinationals reinforce the digital pivot: Medtronic is investing USD 50 million in a Pune software hub to develop cloud analytics for closed-loop systems. As CDSCO guides tele-prescription of insulin analogs, routine dose titration will continue its migration from clinic to living room, strengthening home-care’s pull on the India diabetes devices market.

Geography Analysis

Regional dynamics frame the India diabetes devices industry’s expansion path. Metros such as Mumbai, Delhi-NCR, Bengaluru, and Hyderabad reflect higher disposable income and specialist density. CGM adoption in these hubs is three times the national average, helped by private-sector insurance that reimburses sensors and disposable pens.

Tier-2 cities, including Jaipur, Lucknow, Coimbatore, and Indore, are experiencing the fastest growth in incremental volume. Government PLI clusters in Gujarat and Tamil Nadu shorten supply chains, letting local distributors trim SMBG strip prices by 8-10%. Intensifying e-pharmacy penetration also improves last-mile access, narrowing the urban-rural gap. Still, cold-chain limitations curb the uptake of insulin cartridges, moderating the growth of management devices relative to monitoring kits in these regions.

Tier-3 cities and rural markets hold the largest patient pool. Limited endocrinologist availability and out-of-pocket payment requirements restrict the penetration of advanced devices. Government outreach, such as tele-specialist nodes under eSanjeevani and state subsidies, is a critical lever.

Regulatory Landscape

Diabetes devices in India are regulated by the Central Drugs Standard Control Organization (CDSCO) under the Drugs and Cosmetics Act, 1940, and the Medical Devices Rules (MDR), 2017. Oversight is led by the Drugs Controller General of India (DCGI). Under MDR, 2017, devices are risk-classified (Class A to Class D) and generally require licensing for manufacture and import through CDSCO processes, which determines the compliance pathway for glucose monitoring systems, insulin delivery devices, and key consumables.

For drug-device combinations, India does not run a standalone combination-product statute. Products containing both a drug and a device element are assessed as either a drug or a medical device based on the primary mode of action, and manufacturers can seek classification clarity from CDSCO. In April 2026, the Ministry of Health and Family Welfare issued draft Medical Devices (Amendment) Rules, 2026 for public comments, indicating active rulemaking under the MDR, 2017 framework that can affect technical documentation, labeling, and licensing expectations for diabetes-device manufacturers and importers.

Value Chain Analysis

The value chain covers upstream materials and components (sensor chips, enzymes and electrodes for monitoring systems, plastics and precision parts for pens and pumps, and primary packaging such as glass tubing for cartridges), then moves to device design, manufacturing or assembly, and quality and regulatory compliance under CDSCO. A recurring constraint is dependence on imported high-spec electronics and sensor inputs, which concentrates supply risk outside India even as domestic assembly grows. This has pushed companies toward localization where feasible, including Roche assembling Accu-Chek Active meters in Chennai and Schott commissioning borosilicate cartridge-tubing capacity in Gujarat in 2025 to reduce lead times for insulin-device components.

Downstream, hospitals and specialty clinics drive initial use for pumps and CGM starts, while retail and organized pharmacy channels support high-volume SMBG replenishment. E-pharmacy and digital-health platforms are also expanding through device-and-coaching bundles. Government manufacturing incentives, including the PLI program for medical devices, support local production economics, alongside an updated approved-applicant list released by the Department of Pharmaceuticals in November 2024. Still, affordability and infrastructure constraints, including patchy cold-chain capacity beyond metros, limit the reach of insulin cartridges and higher-end management devices in tier-2 and tier-3 markets.

Competitive Landscape

The India diabetes devices market is moderately fragmented, with the five largest multinationals controlling significant revenue share through branded CGM sensors, insulin pumps, and disposable pens. Abbott leads CGM, Roche dominates SMBG meters, Medtronic heads the premium pump niche, while Novo Nordisk and Eli Lilly anchor injectable portfolios. Localization mitigates currency swings; Roche’s Chennai line trims meter costs, and Schott’s Gujarat tubing offsets cartridge imports. Novo Nordisk’s decision to phase out vials pivots supply toward pen formats, creating ancillary demand for compatible needles and cartridges.

Domestic challengers exploit price elasticity. AgVa Healthcare’s INSUL pump at INR 24,999 widened pump affordability to middle-income families and captured double-digit share in new installations by mid-2025. Local strip assemblers leverage PLI incentives to match Chinese landed costs, pressuring incumbent gross margins. Start-ups like Ultrahuman bundle CGM sensors with lifestyle coaching, selling mainly through corporate wellness contracts and adding a subscription layer to the India diabetes devices market.

Strategic moves underscore competitive intensity. Schott’s USD 75 million glass-tubing plant secures critical feedstock for indigenous insulin hardware, while Medtronic’s Pune tech center focuses on closed-loop algorithms for global deployment. Roche has established data-sharing APIs with digital health platforms, streamlining physician workflows and enhancing brand stickiness. As ABDM data standards mature, interoperability will shape win-loss outcomes more than hardware specs, compelling players to invest in cloud security compliance and patient-facing analytics.

India Diabetes Devices Industry Leaders

Medtronics

Becton Dickinson

Roche

Dexcom

Abbott

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The strongest opportunity centers on reimbursement expansion combined with connected care. CGHS revised its 2024 rate list to raise ceilings to INR 300,000 for sensor-augmented pumps and INR 4,000 for 14-day CGM use, which provides clearer purchasing reference points for eligible beneficiaries and for provider systems. The public-sector digital backbone also creates room for device-plus-service models in home care. eSanjeevani surpassed 318.6 million cumulative consultations in 2024, and the Ayushman Bharat Digital Mission issued 568 million health IDs, supporting remote monitoring workflows and data sharing that can improve utilization of CGM, smart SMBG, and insulin-dose titration programs.

Local manufacturing depth remains a key lever for pricing and supply resilience, reinforced by the National Medical Devices Policy 2023 and the PLI program footprint. Developments in insulin-delivery ecosystems also point to investable demand for pens and cartridges: in July 2026, Shantha Biologics signed a manufacturing agreement with Novo Nordisk to perform cartridge fill-finish operations at its Hyderabad facility, and Shaily Engineering Plastics disclosed plans in May 2026 to scale GLP-1 pen capacity to over 150 million units by FY28. These moves align with the shift toward prefilled, patient-friendly delivery formats, supporting demand for compatible device components, sterile primary packaging, and India-focused distribution partnerships that can extend diabetes-device portfolios beyond metro specialist channels.

Recent Industry Developments

- July 2026: Abbott India formalized a distribution partnership with Novo Nordisk for Awiqli, positioning its 4,000+ member distribution network to broaden access to once-weekly basal insulin in India. The move strengthens the device-adjacent delivery ecosystem around pens and cartridges, supporting higher throughput for diabetes care consumables across non-metro channels.

- August 2025: Schott opened a large syringe and cartridge glass-tubing facility at Jambusar, Gujarat, aimed at expanding regional supply of borosilicate tubing used in insulin delivery systems. Greater local availability of this upstream input shortens lead times and reduces dependence on imports for cartridge-based formats, influencing the cost structure of insulin-device supply chains.

- December 2024: Lupin acquired Eli Lilly's branded human insulin portfolio in India, including Huminsulin, strengthening its presence in insulin vials and cartridges. The acquisition widened a domestic supplier's role in insulin delivery formats, with implications for demand planning and partnering across compatible injection and cartridge-related device components.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the India diabetes devices market is defined as the revenue generated from devices and related patient-use consumables that are used to monitor blood glucose and to deliver insulin for diabetes management in India.

Scope exclusions: The estimate excludes diabetes drugs, standalone mobile apps, and services that do not directly qualify as a device sale (or a paired device consumable).

Segmentation Overview

- By Product Type

- Monitoring Devices

- Self-Monitoring Blood Glucose Devices

- Continuous Glucose Monitoring

- Management Devices

- Insulin Pumps

- Insulin Syringes

- Insulin Cartridges

- Disposable Pens

- Other Management Devices

- Monitoring Devices

- By Patient Type

- Type-1 Diabetes

- Type-2 Diabetes

- By End User

- Hospitals & Specialty Clinics

- Primary Care & Diabetes Centres

- Home-Care Settings

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with mapping demand and access signals for diabetes care in India, and then translating those signals into device adoption and replacement patterns. We mainly relied on public sources such as Ministry of Health and Family Welfare publications, National Health Mission program documents, ICMR-linked epidemiology papers, and peer-reviewed clinical journals that report testing frequency and insulin use practices.

To keep assumptions realistic, pricing and channel context were also read from sources such as DCGI and CDSCO notifications (for device policy cues), Customs import-export statistics (for volume direction checks), and company annual reports and investor presentations for product mix and India exposure. In a few places, we used paid subscriptions for company financials and for patent databases to understand innovation intensity, and then these were used only as supporting checks. The desk research sources listed here are illustrative and not exhaustive, and many other references were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating how devices and consumables move through hospitals, clinics, pharmacies, and e-commerce, and how usage differs between insulin users and non-insulin users. We spoke with a mix of manufacturers, distributors, diabetologists, lab managers, and procurement teams so that gaps from desk inputs like pricing, refill cycles, and device switching could be closed with on-ground feedback across India.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | |

| Mid tier: 56% | Functional/Unit leaders: 36% | |

| Smaller Players: 16% | Managers: 50% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand pool approach, where diagnosed population signals and insulin-treated cohorts are converted into device users, and then into annualized units and value. The model then gets cross-checked using selective bottom-up approximations, such as sampled price points by channel and a roll-up of visible supplier and distributor revenue shares, which are then used to correct any over-counting.

Key inputs that shaped the India model include the estimated diabetes prevalence and diagnosis rate, the share of patients on insulin, SMBG testing frequency and strip consumption, CGM adoption and sensor change intervals, and average selling prices by device type and channel. When data was uneven across cities and care settings, we used interview-led ranges and applied conservative penetration logic so that the final totals stay reproducible.

Forecasting relied on scenario-based modeling supported by exponential smoothing for price and adoption curves, followed by expert checks on what could realistically change within a 5-year window. Variables that were stress-tested included patient affordability, tender-driven pricing shifts, and the pace of CGM and pen uptake in urban private care.

Data Validation & Update Cycle

Outputs were validated through triangulation across epidemiology signals, channel movement cues, and the internal consistency of unit-to-value conversions. Any sharp jumps in growth, pricing, or mix were flagged, reviewed by another analyst, and then rechecked with fresh primary outreach when a data point could materially shift the total.

Reports are refreshed on an annual cycle, and interim updates are done when major policy, reimbursement, or supply events change assumptions. Before delivery, we do a final review pass so the market size and near-term trend narrative reflect the latest available information.

Mordor Intelligence's India Diabetes Devices Market Size Versus Other Published Estimates

Published market sizes for India diabetes devices often differ because each study sets its own definition of what counts as a device market and how consumables, connected features, and adjacent diabetes care items are treated. Differences also show up when authors pick different base years, apply faster or slower adoption curves, or do not align pricing to the same currency timing.

Some external estimates combine diabetes devices with therapeutics and digital programs, which naturally pushes the total higher even if the device volumes are similar. In Mordor Intelligence, the market total is limited to patient-use monitoring and insulin delivery devices plus their paired consumables, and it excludes diabetes drugs and standalone app or service revenue, which keeps the number tied to an identifiable sales pool.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.67 B (2026) | |

| Industry Publisher A | USD 3.76 B (2025) | Uses a broader diabetes devices and therapeutics scope, and the year basis is earlier, which can blend drug revenue with device totals and lift the stated size. |

| Regional Consultancy B | USD 2.80 B (2026) | Includes digital and remote monitoring elements in the device definition, and applies a higher long-run growth assumption, which changes value capture even when core device volumes are comparable. |

Overall, the spread is mainly explained by what is included around the core device stack, followed by how pricing and adoption are projected year to year. By keeping inputs traceable to patient cohorts, usage rates, and channel pricing checks, the final figure stays easier to reconcile and update when new signals emerge.

Key Questions Answered in the Report

What is the 2026 value of the India diabetes devices market?

The market is valued at USD 2.67 billion in 2026.

What is the market's expected growth rate through 2031?

It is forecast to post a 2.49% CAGR, reaching USD 3.02 billion by 2031.

Which product category is expanding quickest?

Management devices, especially insulin pumps and disposable pens, are projected to grow at a 3.53% CAGR.

Why are home-care settings gaining traction for device use?

Telemedicine platforms and digital health IDs enable remote monitoring and dose adjustments, lifting home-care growth to a 5.17% CAGR.

How does the PLI scheme support domestic manufacturing?

It offers financial incentives that have spurred 19 greenfield projects, cutting import dependency for meters, cartridges, and pumps.

Page last updated on: