Automated Parcel Delivery Terminals Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

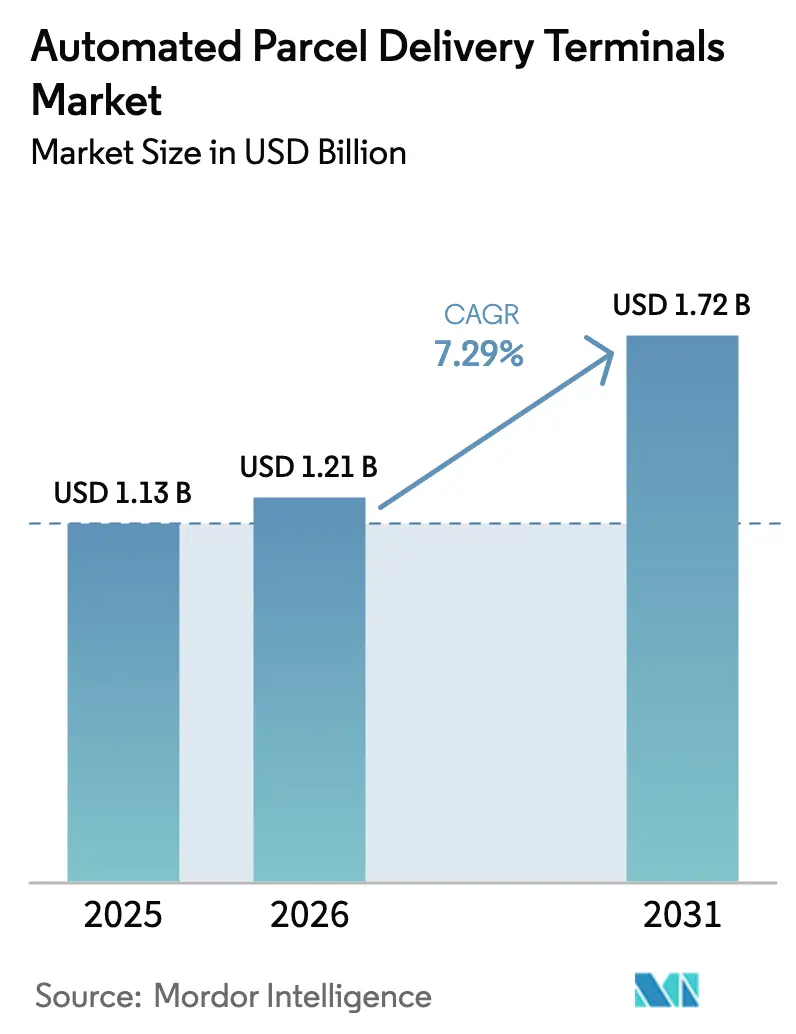

| Market Size (2026) | USD 1.21 Billion |

| Market Size (2031) | USD 1.72 Billion |

| Growth Rate (2026 - 2031) | 7.29% CAGR |

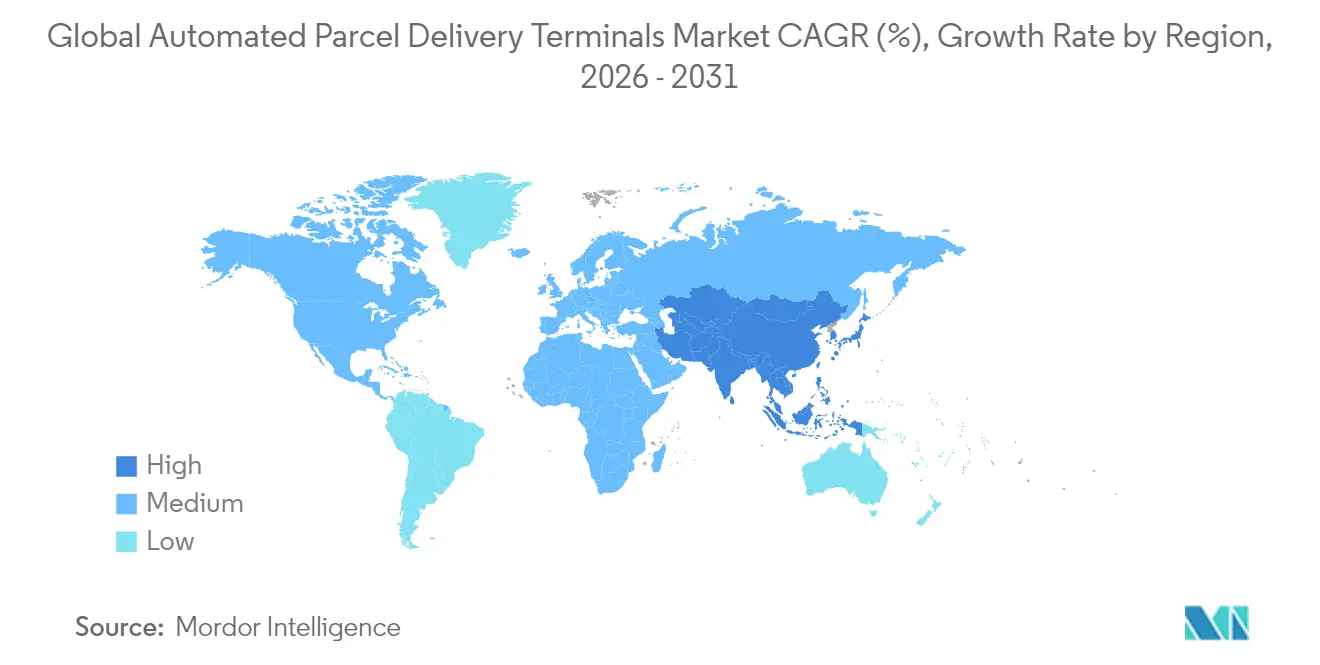

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automated Parcel Delivery Terminals Market Analysis by Mordor Intelligence

automated parcel delivery terminals market size in 2026 is estimated at USD 1.21 billion, growing from 2025 value of USD 1.13 billion with 2031 projections showing USD 1.72 billion, growing at 7.29% CAGR over 2026-2031. Rising urban density, e-commerce scale, and postal operators’ shift to carrier-agnostic infrastructure underpin the expansion, while AI-enabled routing reduces costly failed first-attempt deliveries, strengthening the business case[1]International Transport Forum, “The Cost of Failed First-Attempt Deliveries,” itf-oecd.org . Regulatory pressure for carbon-neutral last-mile services, hardware innovations that allow off-grid outdoor units, and retail investments in click-and-collect banks further accelerate network roll-outs. At the same time, security threats and fragmented U.S. permitting rules temper growth, prompting operators to prioritize indoor deployment and advanced surveillance. Competitive intensity is heightening as logistics firms, e-commerce giants, and hardware specialists all race to control customer touchpoints and delivery data.

Key Report Takeaways

- By deployment, indoor installations commanded 64.28% share of the automated parcel delivery terminals market size in 2025; outdoor banks are growing at 8.41% CAGR between 2026-2031.

- By business model, the business-to-consumer (B2C) segment held 87.55% of the automated parcel delivery terminals market share in 2025; consumer-to-consumer (C2C) transactions are poised for an 8.70% CAGR between 2026-2031.

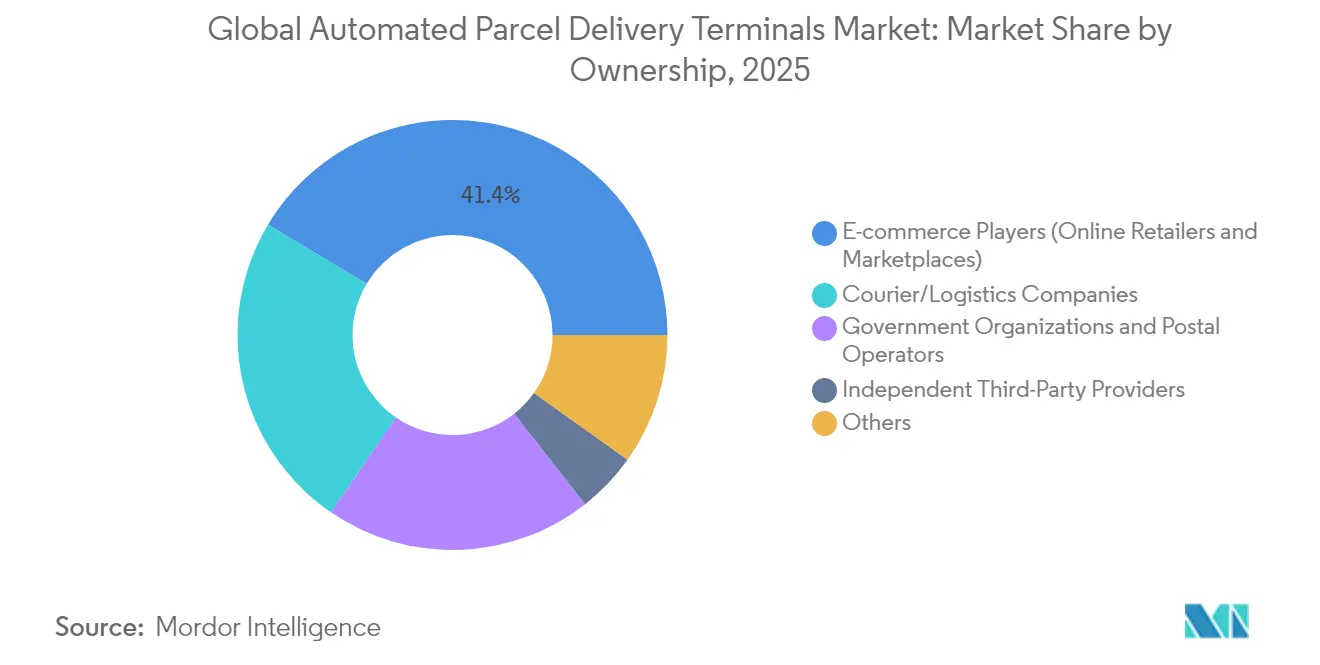

- By ownership, e-commerce platforms controlled 41.42% of installed units in 2025, while courier/ logistics companies-owned lockers represent the fastest-growing ownership group at 8.19% CAGR between 2026-2031.

- By configuration, modular parcel lockers captured 50.35% revenue share in 2025; cooling (fresh-food) lockers are advancing at a 8.94% CAGR between 2026-2031.

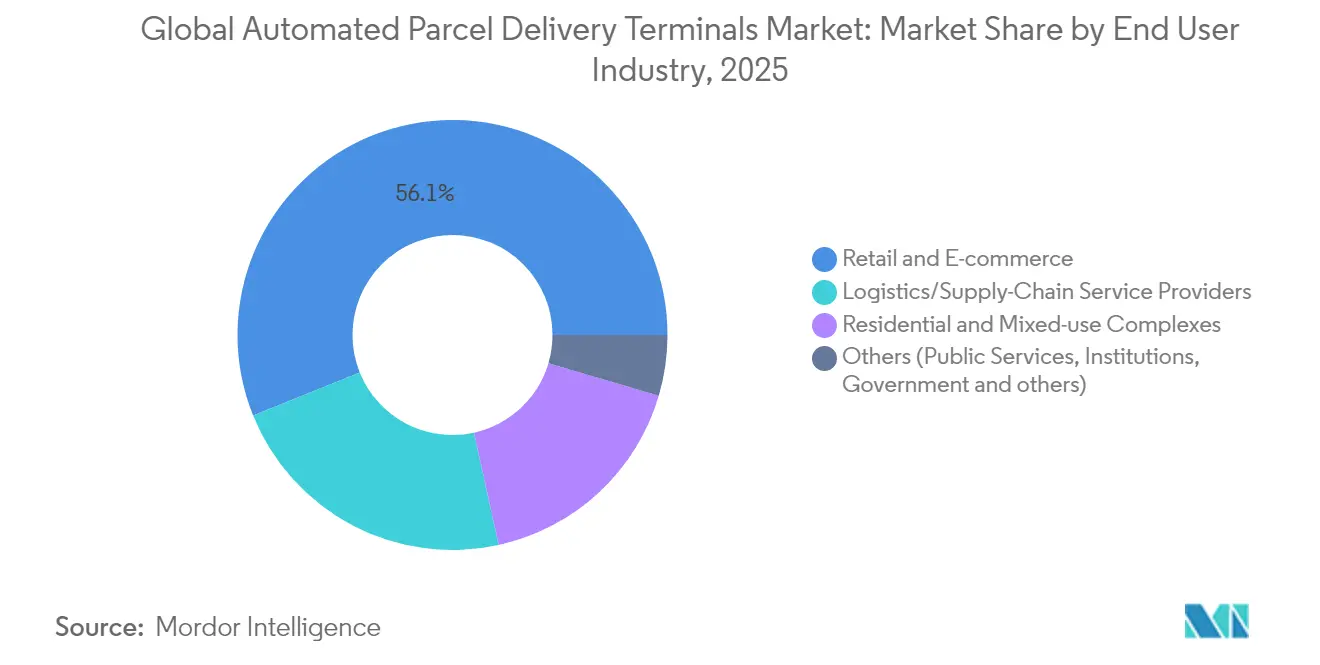

- By end user industry, the retail and e-commerce segment accounted for 56.10% share in 2025, whereas residential and mixed-use complexes are rising at an 8.79% CAGR between 2026-2031.

- By speed of delivery, non-express deliveries led with 68.75% of the automated parcel delivery terminals market share in 2025, while express parcels are projected to grow at an 8.29% CAGR between 2026-2031.

- By geography, Europe led with 33.07% of the automated parcel delivery terminals market share in 2025, while Asia-Pacific is forecast to expand at an 7.98% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automated Parcel Delivery Terminals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urban e-commerce fulfilment needs in densely populated Asian cities | +1.8% | Asia-Pacific core, MEA spill-over | Medium term (2-4 years) |

| Consolidation of carrier-agnostic locker networks by European postal operators | +1.2% | Europe, early North America | Long term (≥ 4 years) |

| Retailer investments in store-front click-and-collect banks across North America | +0.9% | North America, selective EU | Short term (≤ 2 years) |

| Carbon-neutral last-mile mandates accelerating locker roll-outs in the Nordics | +0.7% | Nordic region, broader EU | Medium term (2-4 years) |

| AI-enabled dynamic locker routing reducing failed first-attempt deliveries | +1.1% | Global, tech-advanced markets | Short term (≤ 2 years) |

| Temperature-controlled grocery locker pilots driving fresh-food use cases | +0.6% | Global urban grocery hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Urban E-commerce Fulfilment Needs

China processed more than 130 billion parcels in 2024, and megacities such as Shanghai see densities topping 50 parcels /km² daily, a scale that makes door-to-door models unsustainable[2]China.org.cn, “China Express Delivery Statistics 2024,” china.org.cn. Smart lockers in residential towers cut last-mile costs by up to 40%, while SingPost’s USD 22.72 million capacity upgrade quadruples parcel throughput and signals how operators are scaling to meet volume spikes. High utilization rates improve payback periods, reinforcing the automated parcel delivery terminals market as core urban infrastructure rather than a convenience feature.

Consolidation of Carrier-Agnostic Locker Networks

Deutsche Post DHL plans to double German Pack stations to 30,000 by 2030, investing EUR 500 million (USD 551.82 million) to harvest multi-carrier flows and lower per-parcel costs. Royal Mail, bpost, and Poste Italiane are following suit through joint ventures and retailer partnerships that densify networks without proportionate capex outlays. Consolidation erects entry barriers and positions incumbents as platform orchestrators, shifting competitive dynamics in the automated parcel delivery terminals market.

AI-Enabled Dynamic Locker Routing

Amazon’s locker-capacity algorithm cut unjustified rejections by 60%, proving how machine learning elevates compartment utilization and customer experience[3]INFORMS Journal on Applied Analytics, “Locker Capacity Optimization at Amazon,” pubsonline.informs.org. Autonomous delivery pilots in China integrate V2X communication with real-time traffic data to synchronize routes and locker availability, trimming failed first-attempt deliveries that otherwise inflate costs by 40-50%[4]MDPI Sustainability, “AI-Driven Urban Logistics Frameworks,” mdpi.com. AI, therefore, unlocks margin gains that accelerate global adoption.

Temperature-Controlled Grocery Lockers

Albertsons, Kroger, and European grocers deploy multi-temperature lockers that store ambient, chilled, and frozen items, enabling same-day pickup without staff intervention. Cleveron’s 501 unit holds 120 totes and shortens in-store handling time by up to 70%, highlighting how specialty hardware opens new revenue streams for operators and grocers alike. Rising online grocery demand is set to double by 2027, creating fertile ground for this niche within the automated parcel delivery terminals market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ongoing vandalism and security breach incidents in public-access locker sites | -1.4% | Global urban centers | Short term (≤ 2 years) |

| Fragmented regulatory approvals for curb-side installations in US cities | -1.1% | United States | Short term (≤ 2 years) |

| Limited grid-power access for rural and suburban outdoor banks | -0.8% | Rural North America, developing Asia-Pacific | Medium term (2-4 years) |

| High retrofit costs to integrate legacy postal infrastructure | -0.9% | Global mature postal markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ongoing Vandalism and Security Breaches

Package theft in the UK totals GBP 376 million (USD 478.65 million) annually, and USPS recorded over 1,200 mail theft arrests in 2024, forcing operators to invest in hardened enclosures and video analytics that add 15-20% to operating costs. Elevated risk weighs on deployment economics, particularly for outdoor banks situated in high-crime districts.

Fragmented Regulatory Approvals in U.S. Cities

New York City’s LockerNYC program requires four-to six-month consent processes and long-term fee agreements, delaying scale-up and skewing the automated parcel delivery terminals market toward operators with established municipal ties. A patchwork of state rules governing delivery robots and sidewalk use further complicates nationwide roll-outs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Retail First, Residential Next

Retail and e-commerce sectors commanded a 56.10% share in 2025, leveraging lockers to cut in-store handling and attract omnichannel shopper footfall. Residential and mixed-use complexes deliver the fastest growth at 8.79% CAGR (2026-2031), with developers installing lobby banks that eliminate concierge burden and differentiate property amenities. Case studies show 52% CO₂ savings and 60-hour monthly labor reductions per building after smart-box adoption Citibox.

For logistics providers, residential deployments unlock consolidated drop-off routes that shrink stop counts. The automated parcel delivery terminals market, therefore, straddles commercial and living spaces, embedding itself in daily routines and urban design codes.

By Deployment: Indoor Installations, Anchor Network Economics

Indoor sites accounted for 64.28% of 2025 revenue, a dominance underpinned by lower vandalism exposure and climate control that extends hardware life. This share equals USD 0.78 billion of the automated parcel delivery terminals market size in 2026, with retail foyers and mixed-use lobbies offering constant footfall and minimal permitting friction. Insurance premiums fall as much as 30% compared with outdoor banks, reinforcing indoor preference. On the flip side, the outdoor sites' growth of 8.41% CAGR (2026-2031) reflects battery- and solar-powered designs that bypass grid constraints. CTT’s solar lockers in Lisbon and Cleveron’s battery modules allow operators to fill suburban and rural coverage gaps. As security technology matures, outdoor nodes will form the mesh that complements dense indoor clusters, expanding geographic reach without duplicating legacy branch networks.

Second-order effects include data monetization: indoor units provide anonymized shopper traffic insights that retailers leverage for in-aisle promotions. Outdoor units gather environmental telemetry valuable to municipal planners optimizing curbside use. Consequently, deployment decisions now balance direct parcel revenue with adjacent data-service potential, broadening the return profile for investors in the automated parcel delivery terminals market.

By Speed of Delivery: Non-Express Parcels Dominate but Express Usage Climbs

Standard/ non-express parcels represented 68.75% of 2025 revenue, reflecting consumers’ willingness to exchange speed for flexible pickup windows. Express parcels grew 8.29% CAGR (2026-2031) and now tap lockers to guarantee time-definite retrieval without surcharge for failed delivery. AI-backed slot reservation tools allocate compartments dynamically between service levels, improving occupancy and revenue per cubic foot. Carriers trial predictive rerouting that diverts overflow express parcels to nearby banks in real time, minimizing throttle during peak seasons. These innovations keep capacity elastic, protecting service quality as e-commerce order cycles shorten.

Rising express share also changes site economics: higher-value goods justify premium locker fees, accelerating payback in central business districts where real estate costs are steep. The automated parcel delivery terminals market can therefore capture incremental margin by tiering compartment pricing based on dwell time and service urgency.

By Ownership: Platform Control Versus Shared Ecosystems

E-commerce (online retailers and marketplaces) owned 41.42% of installed lockers in 2025, motivated by brand stickiness and last-mile data capture. Courier/logistics companies owned estates, expanding at 8.19% CAGR (2026-2031), indicate rising carrier appetite to internalize locker costs rather than pay per-parcel access fees. Postal operators hold sizable footprints enabled by public-service mandates and municipal real-estate rights.

Independent specialists operate multi-carrier hubs that monetize access across all players, creating neutral infrastructure critical to parcel-dense city centers. Debates over open versus closed networks will shape investment allocation, but the automated parcel delivery terminals market increasingly rewards owners that blend scale with interoperability to maximize slot utilization.

By Model: B2C Still Reigns as C2C Momentum Builds

The business-to-consumer (B2C) channel held 87.55% share in 2025, fueled by omnichannel retailers and marketplaces that embed locker pickup at checkout. Consumer-to-consumer (C2C) activity, however, is the fastest climber at 8.70% CAGR (2026-2031), propelled by resale platforms and social-commerce communities that need neutral hand-off points. InPost’s Send service exemplifies how operators tailor user journeys with QR-code label generation and app-based locker booking.

Business-to-business (B2B) flows remain modest but strategic for spare-parts supply chains that require predictable, unattended pickup outside standard hours. As sellers diversify into re-commerce and repair services, mixed-flow sites will blur traditional segment lines yet keep B2C as the anchor tenant of the automated parcel delivery terminals market.

By Locker Configuration: Modular Builds Enable Rapid Scaling

Modular parcel lockers represented 50.35% of 2025 deployments, their flexible bays supporting incremental additions as parcel volumes climb. Configurable chassis shorten installation to less than four hours, limiting business-day disruption at host sites. Cooling (fresh-food lockers) designs, growing 8.94% CAGR (2026-2031), satisfy perishable-goods demand and uphold food-safety compliance. Advanced units integrate ozone sanitization for grocery applications, preserving shelf life during warmer months.

Specialty formats such as high-capacity mailroom towers and secure returns kiosks diversify revenue while leveraging the same cloud platform, cementing modular design as the foundation of the automated parcel delivery terminals market.

Geography Analysis

Europe accounts for 33.07% of global revenue in 2025, reaching USD 0.4 billion of the automated parcel delivery terminals market size in 2026. Dense postal networks, stringent emission targets, and widespread consumer familiarity drive high utilization. Investments such as Deutsche Post DHL’s Packstation expansion and the DHL-Poste Italiane joint venture mark a decisive push toward 100% carrier-agnostic coverage, reinforcing Europe’s structural lead.

Asia-Pacific is the growth pacesetter at an 7.98% CAGR between 2026-2031, supported by unparalleled parcel volumes and government backing for smart-city logistics. Cainiao’s infrastructure build-out in Southeast Asia and sustained locker infill in Tier 1 Chinese cities exemplify the region’s scale potential. Local hardware makers tailor ruggedized units for monsoon climates, and municipal authorities fast-track approvals to mitigate traffic congestion linked to doorstep deliveries. These factors create a virtuous cycle that solidifies the region’s long-term contribution to the automated parcel delivery terminals market.

North America maintains steady double-digit locker additions, though fragmented zoning rules prolong rollout timelines. Retailers spearhead uptake via click-and-collect hubs that merge parcel pick-up with curb-side grocery, while USPS pilots indicate federal momentum toward nationwide coverage. Emerging Latin American and Middle-East markets show nascent but accelerating adoption, often through public-private partnerships that leverage postal real estate to bridge infrastructural gaps.

Regulatory Landscape

Regulation for automated parcel delivery terminals is shaped by postal engineering specifications, national standards for smart parcel boxes, and interoperability and security standards for digital access. In the United States, USPS engineering standard STD 4C sets design requirements for centralized mail receptacles that include parcel locker compartments, anchoring minimum compartment sizing and installation expectations where USPS delivery is involved. In China, GB/T 24295-2021 defines structural and safety requirements for smart letter and parcel boxes, while postal-industry guidance such as YZ/T 0173-2020 covers data-exchange expectations between terminal systems and postal authorities, including protocol and encryption requirements that influence software architecture and vendor compliance work.

In Europe, CEN standardization supports interoperability and security for digital opening systems and parcel box technical features, including CEN/TS 17457:2020 for digital opening frameworks (aligned with the European Commission standardization request M/548) and CEN/TS 16819:2015 for ergonomics, corrosion resistance, and security features. More recently, CEN/TR 18085:2024 provided guidance on safe and contactless last-mile delivery and proof-of-delivery approaches, reinforcing the role of lockers in compliant unattended delivery workflows even when hardware mandates differ by municipality. Across regions, these standards push operators toward auditable access control, secure data handling, and consistent physical performance for public-access deployments.

Value Chain Analysis

The value chain starts with locker hardware OEMs and component suppliers (steel enclosures, locks, sensors, barcode/RFID readers, displays, and power systems such as battery or solar modules), alongside embedded software and connectivity providers. These inputs support system integrators and platform vendors that provide control software, cloud hosting, monitoring, and APIs to connect lockers with carrier networks, e-commerce checkout, and tracking systems. Network operators (postal operators, courier/express/logistics companies, independent third-party providers, and e-commerce platforms) then procure and deploy terminals, secure sites (retailers, residential complexes, transit hubs, and municipal locations), and run field operations such as installation, maintenance, customer support, and security hardening.

Downstream, carriers and merchants generate parcel volumes, while property owners monetize footfall and amenity value through hosting agreements. Revenue increasingly depends on software-enabled utilization (slot reservation, dynamic routing, and compartment mix optimization) and multi-carrier access, since misconfigured compartment sizing can create throughput bottlenecks even in high-demand locations. Reverse logistics is also becoming standard, with lockers used for returns drop-off and C2C exchanges, expanding the operator revenue stack beyond first-attempt delivery avoidance.

Competitive Landscape

Competition remains moderately consolidated, with the top five operators controlling roughly 45% of installed bays worldwide. Postal incumbents exploit regulatory relationships to lock in prime curbside sites, while specialist operators pursue asset-light models that aggregate carrier demand. Hardware suppliers such as Cleveron and Quadient differentiate through rapid-install modular kits and temperature-controlled innovations, securing OEM alliances with retailers and grocers. E-commerce majors like Amazon integrate proprietary software stacks, achieving 60% fewer capacity rejections and using data insights to refine route orchestration.

Strategic moves in 2025 underscore consolidation and vertical integration. Deutsche Post DHL allocated EUR 500 million (USD 551.82 million) to network doubling, Cainiao opened cross-border facilities to cement presence in emerging trade lanes, and CTT unveiled solar-powered lockers that slash energy costs by up to 30%. Venture funding is flowing into AI-driven fleet-locker optimization startups, signaling that software capability is becoming the next competitive frontier within the automated parcel delivery terminals market.

Regulatory trends add another dimension: the EU’s incoming zero-emission zones favor operators able to validate carbon savings, whereas U.S. state-level robot-delivery statutes may soon encourage hybrid locker-bot ecosystems. Participants that harmonize hardware, software, and sustainability credentials will enjoy heightened bargaining power with retailers and carriers alike.

Automated Parcel Delivery Terminals Industry Leaders

Cainiao Network (Alibaba - Cainiao Smart Lockers)

InPost S.A. (InPost Parcel Lockers)

Amazon (Amazon Lockers)

Deutsche Post DHL Group (DHL Packstation)

SF Express (SF Lockers)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Open, carrier-agnostic out-of-home networks and transit or community-based sites create whitespace where operators can lift utilization without duplicating infrastructure. Europe provides near-term evidence of densification strategies: bpost installed a 244-compartment parcel locker in Ghent in February 2026 as part of its expansion agenda, and the broader European out-of-home delivery network surpassed 646,000 active points (including PUDO and automated lockers) by end-2025. These actions support opportunities for shared-access lockers at retail, residential, and transit nodes, particularly where incumbents and third-party operators can aggregate multi-carrier volumes and reduce the per-parcel cost of capacity.

Technology-led opportunities concentrate in three areas. First is integration and data exchange, where operators prioritize real-time capacity APIs and secure access control to interoperate with multiple carriers and merchant platforms. Second is automation around feeding and sorting, supported by SingPost unveiling a S$30 million automated sortation facility in June 2026 that tripled small and medium parcel processing capacity to 300,000 parcels per day, strengthening the hub-to-locker supply chain for dense networks. Third is expanding use cases beyond B2C delivery, including C2C and returns. The USPS launch of Local XChange in July 2026, enabling buy-and-sell exchanges via USPS Smart Lockers at Post Offices, shows how lockers can function as trusted exchange infrastructure and offers a template for postal and carrier operators to monetize locker estates through higher-frequency, community-based transactions.

Recent Industry Developments

- July 2026: Amazon entered a strategic cooperation to integrate MyFlexBox smart lockers in Germany into its delivery infrastructure. The move expanded Amazon-accessible out-of-home capacity via an existing locker ecosystem rather than a purely owned build-out, reinforcing partnerships as a faster path to dense coverage. It also raised competitive pressure on other networks to offer interoperable access and a consistent customer experience across third-party locker estates.

- May 2026: InPost reported in its Q1 2026 update that its network expanded to 64,680 automated parcel machines globally, up year-on-year. The added density strengthened InPost's ability to steer more parcels to automated delivery and returns, supporting higher utilization and lower last-mile delivery costs per parcel. The scale also increased its leverage with merchants and carriers seeking broad, standardized locker access across European markets.

- May 2025: CTT Expresso introduced a solar-powered Locky parcel locker at a Lisbon Lidl store. The launch targeted deployments where grid access is constrained and energy costs are a key barrier, improving the feasibility of outdoor expansion beyond dense urban cores. It also highlighted hardware innovation as a competitive lever for operators pursuing wider geographic coverage with fewer site constraints.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the automated parcel delivery terminals market covers revenues from self-service parcel locker terminals and related software support that let users drop off and pick up parcels without staff help, usually with 24/7 access in indoor or outdoor locations.

Scope exclusions: This scope leaves out staffed pickup counters, standard post boxes, and large warehouse sortation systems.

Segmentation Overview

- Deployment

- Indoor

- Outdoor

- Shipment Speed

- Express

- Non-Express

- Model

- Business-to-Business (B2B)

- Business-to-Consumer (B2C)

- Consumer-to-Consumer (C2C)

- Ownership

- E-commerce (Online Retailers and Marketplaces)

- Courier/Logistics Companies

- Government Organizations

- Postal Operators

- Independent Third-Party Providers

- Others

- Locker Configuration

- Modular Parcel Lockers

- Cooling (Fresh-Food Lockers)

- Postal (Mailroom Lockers )

- Laundry and Service-Based Lockers

- Others

- End-User Industry

- Retail and E-commerce

- Logistics/Supply-Chain Service Providers

- Residential and Mixed-Use Complexes

- Others (Public Services, Institutions, Government and Public Sector Among Others)

- Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Netherlands

- Nordics

- Central and Eastern Europe (CEE)

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- ASEAN

- Rest of Asia-Pacific

- Middle East And Africa

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with building a clean view of demand signals that indirectly explain locker rollout, and then mapping the supply side that can serve that demand. We referred to public sources such as postal and parcel traffic statistics from national postal regulators, trade and customs releases for electronic enclosures and access control components, and logistics and transport indicators from agencies such as the World Bank.

To sharpen assumptions, we also reviewed sources like patent databases for locker access and authentication themes, building and property publications that track multifamily and retail footprint changes, and company filings and investor presentations that describe network expansion and operating metrics. In a few places, a paid subscription focused on shipment-level trade flows and another one used for company financials and news helped cross-check where manufacturing and deployment momentum was shifting. The desk sources named here are illustrative only, and many other public and paid references were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what gets installed, how pricing is formed, and how rollout plans change by location type. We spoke with a mix of terminal suppliers, last-mile operators, site owners, and integrators, and then pressure-tested our assumptions on average selling prices, software attachment, replacement cycles, and utilization trends across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 22% | APAC: 49% |

| Mid tier: 49% | Functional/Unit leaders: 24% | EMEA: 30% |

| Smaller Players: 22% | Managers: 54% | Americas: 21% |

Market-Sizing & Forecasting

Sizing followed a top-down approach where parcel volume growth, out-of-home delivery adoption, and pickup point density were used to reconstruct the addressable demand for unattended pickup and drop-off. Once the demand pool was formed, assumptions on terminal placements by site type and average compartments per installation were applied, and then converted to revenue using an ASP curve that separates hardware, installation, and recurring software support.

To keep totals realistic, results were corroborated with selective bottom-up checks such as sampled ASP quotes from interviews, channel checks on typical installation bundles, and a limited roll-up of reported network expansion announcements where available. Key inputs that moved the model included e-commerce shipment growth by region, urbanization and multifamily housing additions, last-mile labor cost pressure, share of parcels routed to lockers versus home delivery, and replacement or upgrade cycles as terminals age.

For forecasting, scenario analysis was used because deployments can shift quickly with regulation changes, carrier strategy, and property owner approvals. In each region, we used conservative, base, and faster rollout cases, and then aligned the base case to what primary respondents indicated as most likely for capacity additions and price progression over the next few years.

Data Validation & Update Cycle

Outputs were tested through several checks so obvious overstatements do not pass through. We compared modeled revenue against independent signals like parcel volume trends, observed rollout intensity by geography, and plausible installation counts implied by site density. When a variance looked large, assumptions were revisited, and the team re-contacted sources to confirm what changed and whether the change was temporary.

Before sign-off, the numbers and assumptions go through multi-step analyst review, including spot checks on currency conversion, timing alignment, and price ladders. Reports are refreshed annually, and interim updates are made when material events occur, followed by a final pre-delivery review so clients receive the latest updated view.

Mordor Intelligence's Automated Parcel Delivery Terminals Market Size Compared Against Other Published Estimates

Published market values for automated parcel delivery terminals do not always line up because the timing and pricing choices vary between sources, even when the category name looks the same. In practice, differences come from the year used for currency conversion, whether hardware and software are bundled into one number, and how quickly ASPs are assumed to fall as deployments scale.

A refresh-led gap also shows up when older models keep early-year prices and rollout plans in place for too long, or when recent installation pauses and budget shifts are not reflected. The table below illustrates how these modeling choices move the current-year number, where a recent currency timing pass, an updated ASP ladder, and re-checked deployment assumptions were applied by Mordor Intelligence.

Overall, the spread is mainly explained by the year chosen for the starting point and how pricing and scope boundaries are updated over time. When the inputs are tied back to observed parcel trends and realistic rollout pacing, the resulting market size becomes easier to trace and repeat in future updates.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.21 B (2026) | |

| Global Research Publisher A | USD 0.82 B (2023) | Uses an earlier base year and may understate later rollout acceleration, and the price curve can look lower if newer software and service attachments are not consistently included. |

| Industry Research Publisher B | USD 1.00 B (2026) | Often applies a flatter ASP progression and a broader definition of terminal types, which can shift the total depending on what is counted as a full terminal versus adjacent locker formats. |

Overall, the spread is mainly explained by the year chosen for the starting point and how pricing and scope boundaries are updated over time. When the inputs are tied back to observed parcel trends and realistic rollout pacing, the resulting market size becomes easier to trace and repeat in future updates.

Key Questions Answered in the Report

How big is the automated parcel delivery terminals market in 2026?

The market is valued at USD 1.21 billion in 2026 and is forecast to reach USD 1.72 billion by 2031 at a 7.29% CAGR (2026-2031).

Which region is growing the fastest?

Asia-Pacific registers the highest growth, advancing at an 7.98% CAGR (2026-2031) on the back of soaring e-commerce volumes and supportive logistics investments.

Why are indoor lockers still preferred?

Indoor installations account for 64.28% of 2025 deployments because controlled environments reduce vandalism, cut insurance costs, and extend equipment life by 3-5 years.

What share do express parcels hold in locker traffic?

Express parcels remain a minority but are the fastest-growing category, expanding at 8.29% CAGR (2026-2031) as carriers leverage lockers to guarantee time-definite pickup without failed delivery risk.

Who owns most locker networks today?

E-commerce platforms lead with 41.42% ownership in 2025, but courier-controlled estates are the fastest-rising group, growing at 8.19% CAGR (2026-2031) as carriers pursue direct infrastructure control.

What technologies are shaping future growth?

AI-driven capacity management, battery- and solar-powered outdoor units, and temperature-controlled compartments for perishable goods are the key innovations enhancing locker economics and user adoption.

Page last updated on: