Automotive Secondary Wiring Harness Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

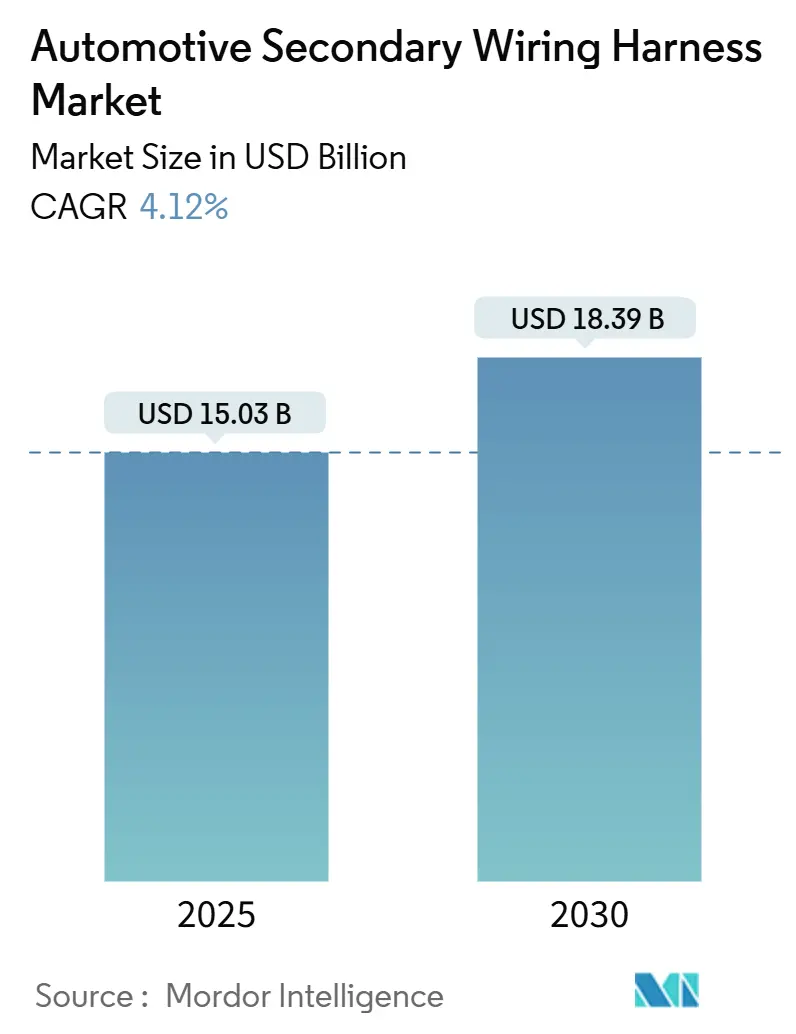

| Market Size (2025) | USD 15.03 Billion |

| Market Size (2030) | USD 18.39 Billion |

| Growth Rate (2025 - 2030) | 4.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Secondary Wiring Harness Market Analysis by Mordor Intelligence

The automotive secondary wiring harness market size stands at USD 15.03 billion in 2025 and is forecast to reach USD 18.39 billion by 2030, translating into a 4.12% CAGR. Rising electrification content per vehicle, modular zonal E/E architectures, and the rapid ramp-up of APAC production volumes continue to push harness complexity and unit demand upward. Dual-voltage 48 V architectures, growing ADAS sensor density, and heightened thermal-cycle requirements in EV battery packs further enlarge secondary loom content while opening opportunities for smart, sensor-rich harnesses. OEM cost-down targets and tighter sustainability regulations accelerate material substitution toward aluminum and composites, yet copper’s entrenched supply chain keeps it dominant in the near term. Capacity additions in Morocco, Egypt, and Thailand illustrate suppliers’ drive to balance labor availability with proximity to regional OEM hubs. Meanwhile, aftermarket retrofits for infotainment and telematics help offset OEM margin pressure and sustain value growth for the automotive secondary wiring harness market.

Key Report Takeaways

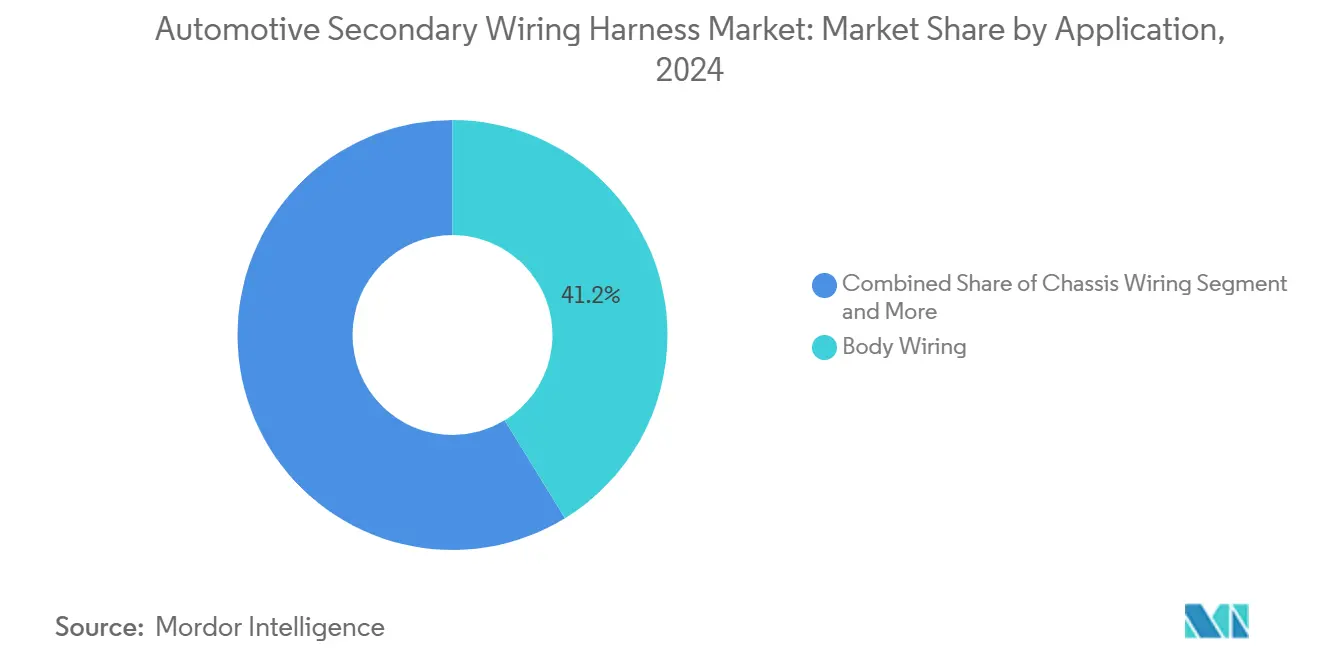

- By application, body wiring held 41.23% of the automotive secondary wiring harness market share in 2024, while power distribution is projected to expand at a 5.48% CAGR to 2030.

- By vehicle type, passenger cars captured 52.82% of the automotive secondary wiring harness market share in 2024; commercial vehicles exhibit the fastest 6.12% CAGR through 2030.

- By material, copper commanded 72.29% of the automotive secondary wiring harness market share in 2024, whereas composites are forecast to rise at a 6.28% CAGR to 2030.

- By connector type, sealed connectors led with 38.31% of the automotive secondary wiring harness market share in 2024; multi-connector systems are climbing at a 5.96% CAGR through 2030.

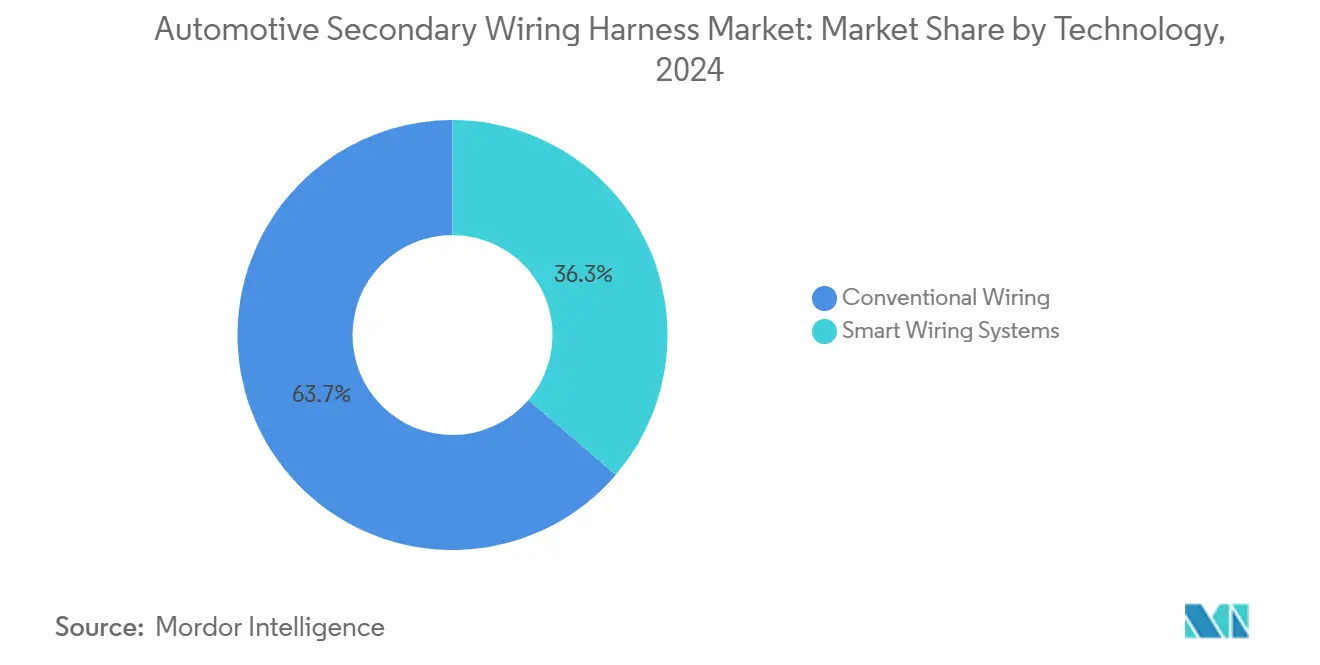

- By technology, conventional systems accounted for 63.73% of the automotive secondary wiring harness market share in 2024, and smart wiring is advancing at a 6.78% CAGR toward 2030.

- By end user, OEM channels retained 78.28% of the automotive secondary wiring harness market share in 2024, while the aftermarket is moving ahead at a 5.37% CAGR across the forecast window.

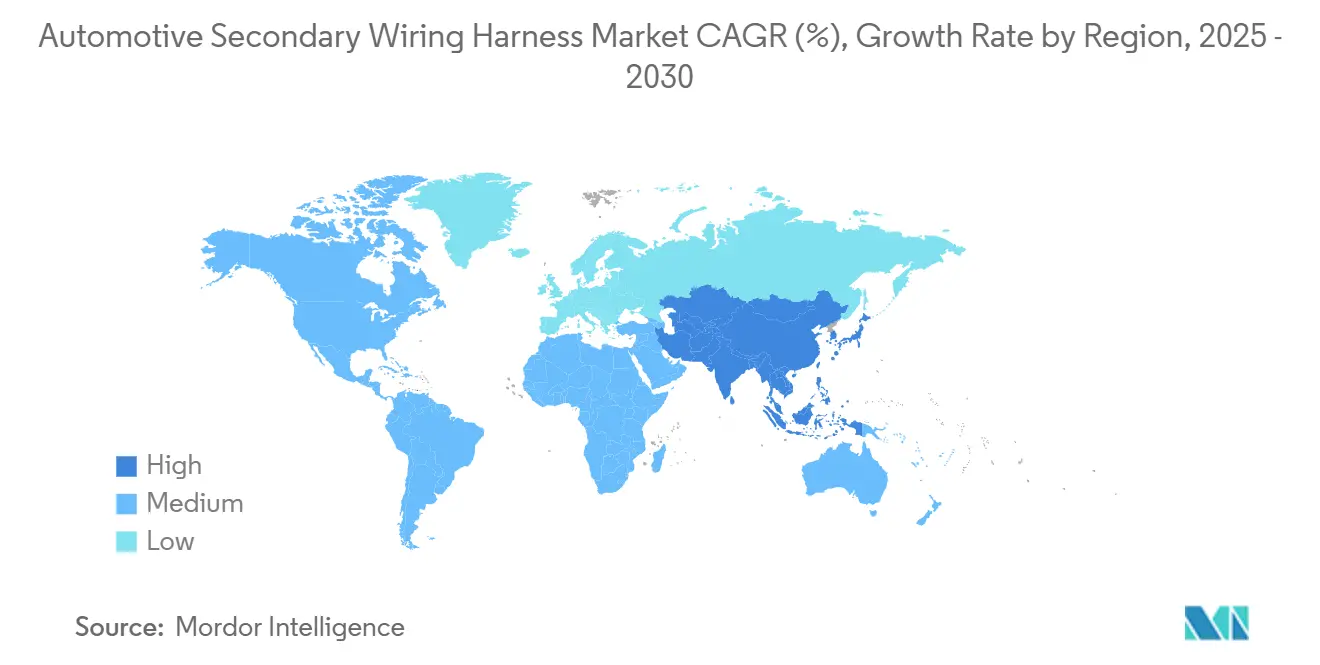

- By region, Asia-Pacific dominated, with 47.43% of the automotive secondary wiring harness market share in 2024. On the back of surging NEV production, the market is set to grow at a 5.86% CAGR to 2030.

Global Automotive Secondary Wiring Harness Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Vehicle Electrification and ADAS Adoption | +1.2% | Global, with Asia Pacific and Europe leading | Medium term (2-4 years) |

| Rapid Asia Pacific Vehicle Production Expansion | +1.0% | Asia Pacific core, spill-over to Middle East and Africa | Short term (≤ 2 years) |

| Zonal E/E Architectures Driving Modular Secondary Looms | +0.9% | Global, led by premium OEMs | Long term (≥ 4 years) |

| Lightweighting Push—Shift from Copper to Al/Composites | +0.8% | Global, strongest in Europe and North America | Long term (≥ 4 years) |

| Aftermarket Demand for Retrofit Electronics | +0.6% | North America and Europe, emerging in Asia Pacific | Medium term (2-4 years) |

| 48V Auxiliary Systems Creating New Low-Voltage Harness Needs | +0.7% | Global, concentrated in premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Vehicle Electrification and ADAS Adoption

Battery electric vehicles (BEVs) are transforming automotive wiring architecture. Unlike internal combustion engine (ICE) vehicles, BEVs require more low-voltage circuits due to added isolation layers, redundant safety paths, and sensors. Advanced driver-assistance systems (ADAS), especially Level 2+, further increase wiring needs with radar, lidar, and camera looms meeting strict electromagnetic compatibility standards.

Dual-voltage systems (12V/48V) are standard in premium EVs to support high-performance components like electric superchargers and active chassis systems. These require branch harnesses capable of handling high current loads. Battery pack looms integrate temperature sensors for extreme duty cycles and durability[1]“Thermal Management Sensors for EV Battery Applications,”, Amphenol Sensors, amphenol-sensors.com.

Zonal E/E Architectures Driving Modular Secondary Looms

OEMs migrating to zonal structures consolidate up to 100 ECUs into a handful of high-performance zone controllers, cutting wire length, yet concentrating complexity at zone hubs[2]“LIMEVERSE Circular Cable Portfolio,”, Leoni AG, leoni.com. Automotive Ethernet (1000BASE-T1) dictates single-pair shielded twisted pair designs capable of 1 Gbps alongside 60 W power delivery. Pre-assembled modular looms enable automated insertion and variant simplification, letting OEMs swap options without holistic redesign. Thermal and vibrational loads rise near controller mounts, so secondary looms now specify aluminum heat sinks and silicone encapsulation. Suppliers with simulation-driven design and flexible manufacturing lines gain a competitive advantage as zonal programs scale across premium and eventually volume segments of the automotive secondary wiring harness market.

Aftermarket Demand for Retrofit Electronics (Infotainment, Telematics)

North American vehicle age reached 12.5 years in 2025, fueling retrofit appetite for connectivity upgrades that rely on plug-and-play secondary kits. Fleet operators retrofit ADAS packages for collision avoidance, demanding CAN-FD and Ethernet-ready looms that integrate cameras and radar without voiding OEM warranties. E-commerce platforms are transforming the automotive secondary wiring harness market by offering vehicle-specific bundles with QR-code installation guides. This reduces installation time and promotes DIY adoption, expanding the customer base beyond traditional service channels. Regulatory pressures from European CE-mark standards tighten electromagnetic compatibility (EMC) requirements. Suppliers pre-test retrofit looms to ensure compliance, enhancing product reliability and market trust.

48 V Auxiliary Systems Creating New Low-Voltage Harness Needs

Mild hybrids deploy 48 V belt-starter-generators, electric turbos, and active roll bars that demand compact looms certified for 200 A continuous load while maintaining isolation from 12 V circuits[3]“48 V Mild Hybrid Power Architectures,”, Infineon Technologies, infineon.com. DC-DC converters introduce noise, so braided shields and ferrite rings become standard. In commercial vans, 48 V steering and brake boosters slash engine parasitics, making dual-voltage harness families a default spec for fleets aiming at fuel savings. Connector makers roll out color-coded terminals to avoid voltage cross-mate errors, and suppliers develop standardized loom families that serve passenger and light-duty truck platforms alike. The surge of 48 V adoption anchors a new product tier inside the automotive secondary wiring harness market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Copper and Polymer Prices | -0.9% | Global, strongest impact in cost-sensitive segments | Short term (≤ 2 years) |

| Migration To Wireless/Data-Bus Architectures: Reducing Wire Count | -0.7% | Global, led by premium OEMs | Long term (≥ 4 years) |

| Thermal-Cycle Failures in EV Battery Pack Harnesses | -0.4% | Global EV markets, concentrated in fast-charging applications | Medium term (2-4 years) |

| Labor-Intensive Manufacturing Causing Capacity Bottlenecks | -0.6% | Global, most acute in high-labor-cost regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Copper and Polymer Prices

In the automotive secondary wiring harness market, tightening supplies of polymer resin and volatile copper prices are reshaping cost structures. Annual price-down pressures from OEMs, coupled with sharp swings in copper prices, have compressed profit margins. Simultaneously, fluctuations in petrochemicals and mandates for green chemistry have rendered high-temperature insulation materials both pricier and less predictable. While larger Tier-1 suppliers mitigate risks through long-term contracts, smaller firms find it challenging to absorb these cost spikes, jeopardizing their expansion plans. Furthermore, the protracted qualification cycles for alternative metals hinder swift substitutions, leaving the market susceptible to shocks in raw material prices. Collectively, these challenges have tempered growth projections, trimming nearly a percentage point from the sector's anticipated compound annual growth rate.

Migration to Wireless/Data-Bus Architectures: Reducing Wire Count

Single-pair Ethernet 10BASE-T1S chains up to eight nodes over one twisted pair, displacing legacy point-to-point sensor looms. A2B audio buses remove multi-core harnesses, and over-the-air diagnostics lessen physical service connectors. Non-critical sensors migrate to BLE or UWB links, especially in cabin comfort roles. Yet ISO 26262-classified functions retain hardwired redundancy, anchoring a baseline of copper even as convenience wiring contracts. Wire-count erosion trims revenue growth potential by 0.7 percentage points yet spurs demand for higher-value, data-capable harnesses in the automotive secondary wiring harness market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Body Wiring Maintains Volume Lead While Power Distribution Rises

Body wiring captured 41.23% of the automotive secondary wiring harness market share in 2024 as modern lighting, seat, and HVAC modules rely on dense interconnects across doors and dashboards. Although smaller today, power distribution looms are projected to outpace all other applications at 5.48% CAGR as EVs demand redundant battery-to-battery, battery-to-converter, and high-current junction routes. This shift raises average copper weight per vehicle despite lightweighting efforts and keeps secure sealing, EMI shielding, and heat-resistant jackets in focus.

Power distribution’s ascent transforms harness design toward flat-braid busbars and over-molded fuses that blend electrical and mechanical roles. Integration supports zonal architectures because centralized power units feed nearby loads, reducing long branch runs. Suppliers that master high-voltage insulation testing and in-house fuse stamping position themselves as solution partners for OEMs seeking to rationalize component counts, thereby adding value and resilience to the automotive secondary wiring harness market size at subsystem level.

By Vehicle Type: Commercial Fleets Accelerate Electrification Uptake

Passenger cars retained a 52.82% share of the automotive secondary wiring harness market in 2024 through sheer production volume. Commercial vehicles, however, post the fastest 6.12% CAGR as last-mile vans, heavy trucks, and municipal buses electrify under TCO and emissions mandates. These platforms require high-power looms for traction batteries and data-rich harnesses for telematics and advanced fleet-management systems.

Long-haul e-trucks demand liquid-cooled battery harnesses with a continuous rating above 500 A, and transit buses adopt modular rooftop battery strings linked by ultra-flexible silicone cables for serviceability. Fleet retrofits such as video-telematics add incremental secondary harnesses that tap existing CAN buses. High uptime expectations push suppliers to engineer abrasion-resistant sleeves and quick-swap connectors, creating premium niches that lift revenue mix inside the automotive secondary wiring harness market.

By Material Type: Copper Dominance Holds but Aluminum Momentum Builds

Copper comprised 72.29% of the automotive secondary wiring harness market size in 2024 because of mature crimp technology and global recycling networks. Composite and aluminum alternatives grow at a 6.28% CAGR under OEM CO₂ targets and spike pricing risks. Sumitomo’s Al-Fe-Mg conductors meet 110 MPa tensile strength and 58% IACS, permitting one-gauge-up swaps that net 2.6 g per meter saved without loss of conductivity. Hybrid solutions splice aluminum leads into copper terminations, easing corrosion and tooling hurdles while cutting weight.

Carbon fiber-reinforced thermoplastics appear in battery undertrays where EMI shielding and crash energy absorption converge. Cost parity with copper remains distant, but regulatory tailwinds and potential circular-economy credits encourage pilot deployments. Suppliers optimizing tin-zinc coatings and multi-stage crimp barrels aim to unlock broader aluminum adoption, diversifying sourcing options for the automotive secondary wiring harness industry.

By Connector Type: Multi-Connector Platforms Enable Modular Electronics

Sealed connectors commanded a 38.31% share through 2024 in response to underhood temperature cycles and road-spray exposure. Multi-connector systems grow 5.96% CAGR because zonal architectures and variant management drive plug-and-play demands. Integrated power-plus-data couplers carry 50 A and 100 Mbps over single interfaces, trimming assembly time and repair complexity.

ISO 11452 EMC validation extends to connectors, leading to metalized shells and 360-degree braid terminations for GHz-range signal integrity. Tool-less lever-lock mechanisms shorten line takt time and cut rework rates. Suppliers integrating connector and cable design capture higher margins and safeguard intellectual property, reinforcing their foothold in the automotive secondary wiring harness market.

By Technology: Smart Wiring Systems Pioneer Vehicle Intelligence

Conventional looms still represent 63.73% of installations, yet smart wiring grows at a 6.78% CAGR as ECUs integrate diagnostics into the harness itself. Printed temperature and strain sensors on flat flex cables enable real-time health monitoring, while embedded microcontrollers support predictive maintenance and OTA parameter tuning.

Vehicle-to-everything (V2X) harnesses embed phased-array antenna tracks and PoE lines, cutting discrete modules and simplifying roof installations. Cyber-secure gateways safeguard in-house data with hardware encryption blocks. Suppliers capable of firmware delivery and cybersecurity certification differentiate themselves, migrating the revenue mix from commodities toward intelligent subsystems, a key evolutionary step for the automotive secondary wiring harness market.

By End User: Aftermarket Retrofits Broaden Revenue Horizons

OEM programs generated 78.28% of revenue in 2024, but the aftermarket advanced at a 5.37% CAGR due to vehicle longevity and demand for connectivity upgrades. Plug-and-play kits leverage vehicle-specific connectors to preserve warranties and reduce install times, appealing to DIY owners and professional shops.

Fleet retrofits add dash cameras, ADAS sensor pods, and telematics gateways, each requiring auxiliary looms that tap CAN-FD backbones without splicing. Regulatory differences between EU CE marking and North American self-certification create compliance services as an additional value stream for mature suppliers. This dual-channel strategy buffers cyclical OEM production swings and enlarges the customer base within the automotive secondary wiring harness industry.

Geography Analysis

Asia-Pacific commanded 47.43% share of the automotive secondary wiring harness market in 2024 and is projected to post a 5.86% CAGR through 2030 as China’s NEV penetration hits 41% and ASEAN plants ramp up volume. Regional players pioneer 800V charging looms and cybersecurity-ready smart harnesses while leveraging labor-cost advantages and vertically integrated copper smelting capacity.

North America remains a mature yet evolving arena where cybersecurity rules and reshoring initiatives reshape supply chains. Commercial vehicle electrification lifts demand for high-current, data-rich looms, and aftermarket retrofits flourish on 12.5-year vehicle age. Domestic assembly investments in Mexico and the U.S. mitigate tariff exposure and shorten lead times, strengthening resilience across the region's automotive secondary wiring harness market size.

Europe drives stringent EMC and circular-economy requirements, pushing aluminum and recyclable polymers while pioneering zonal Ethernet topologies. German Tier-1s invest in R&D for 2.5 Gbps single-pair Ethernet harnesses, and Brexit-related logistics realignments encourage multi-plant strategies spanning the EU and the UK. Premium OEM focus on luxury EVs elevates per-vehicle harness value, sustaining Europe’s role as a technology bellwether within the automotive secondary wiring harness market.

Competitive Landscape

The automotive secondary wiring harness market exhibits moderate concentration, with the top five vendors collectively accounting for a significant global revenue share, balancing long-standing Japanese leaders Yazaki and Sumitomo Electric with diversified multinationals Aptiv, Leoni, and Draexlmaier. Japanese firms exploit vertical integration from copper rod to final assembly, enabling a stable supply and rapid material innovation. European peers pursue automation; Aptiv’s USD 45 million Tangier plant deploys robotic over-molding and inline optical inspection, trimming labor cost and warranty claims.

Chinese entrants accelerate globalization: Luxshare’s 50.1% stake in Leoni injects capital and opens European OEM doors, while establishing a beachhead for cost-competitive harnesses that meet ISO 11452-4 standards. Technology strategies converge on modular loom platforms that support zonal architectures and innovative diagnostics. Barriers to entry arise from capital-intensive validation labs and OEM qualification cycles exceeding 24 months, constraining smaller firms yet protecting incumbents’ share inside the automotive secondary wiring harness market.

Automotive Secondary Wiring Harness Industry Leaders

Yazaki Corporation

Aptiv PLC

Leoni AG

Samvardhana Motherson

Sumitomo Electric Industries, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Smiths Interconnect has expanded its cable harness production capacity at its Tunisia facility. This strategic expansion addresses the rising demand for premium cable harness solutions across multiple industries and bolsters Smiths Interconnect's product lineup, underscoring its commitment to growth across all EMEA production sites.

- January 2025: Leoni AG has inaugurated a state-of-the-art plant in Agadir, Morocco, dedicated to producing wiring systems tailored for trucks, powertrains, and off-road vehicles. This new facility emphasizes digitalization, efficiency, and sustainability. This significant investment highlights Leoni AG's aspirations in the burgeoning global market for commercial vehicles and underscores Morocco's pivotal role in the automotive industry.

Global Automotive Secondary Wiring Harness Market Report Scope

| Body Wiring |

| Chassis Wiring |

| Power Distribution |

| Lighting Systems |

| Two-Wheelers |

| Three-Wheelers |

| Passenger Cars |

| Commercial Vehicles |

| Copper |

| Aluminum |

| Composite Materials |

| Sealed Connectors |

| Unsealed Connectors |

| Terminal Blocks |

| Multi-Connector Systems |

| Conventional Wiring | |

| Smart Wiring Systems | IoT-Enabled Harnesses |

| V2X Integration Harnesses |

| OEMs |

| Aftermarket Suppliers |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Body Wiring | |

| Chassis Wiring | ||

| Power Distribution | ||

| Lighting Systems | ||

| By Vehicle Type | Two-Wheelers | |

| Three-Wheelers | ||

| Passenger Cars | ||

| Commercial Vehicles | ||

| By Material Type | Copper | |

| Aluminum | ||

| Composite Materials | ||

| By Connector Type | Sealed Connectors | |

| Unsealed Connectors | ||

| Terminal Blocks | ||

| Multi-Connector Systems | ||

| By Technology | Conventional Wiring | |

| Smart Wiring Systems | IoT-Enabled Harnesses | |

| V2X Integration Harnesses | ||

| By End User | OEMs | |

| Aftermarket Suppliers | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the automotive secondary wiring harness market in 2025 and what growth is expected?

It is valued at USD 15.03 billion in 2025 and is projected to reach USD 18.39 billion by 2030, registering a 4.12% CAGR.

Which application segment adds the greatest value to vehicle programs?

Body wiring remains the largest at 41.23% share because it integrates lighting, comfort, and door modules, making it indispensable across all vehicle types.

What drives the shift toward aluminum conductors?

Aluminum offers up to 67% weight reduction versus copper, helping OEMs meet CO₂ targets and mitigate copper price volatility while new alloys solve strength and corrosion challenges.

How does aftermarket demand influence growth?

Vehicle lifespans of 12.5 years spur retrofits for telematics and ADAS, pushing aftermarket looms to a 5.37% CAGR and diversifying revenue beyond OEM production cycles.

Which region will generate the fastest harness demand through 2030?

Asia-Pacific, led by China and ASEAN expansions, is forecast to grow at 5.86% CAGR thanks to high NEV penetration and new manufacturing footprints.

Page last updated on: