Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

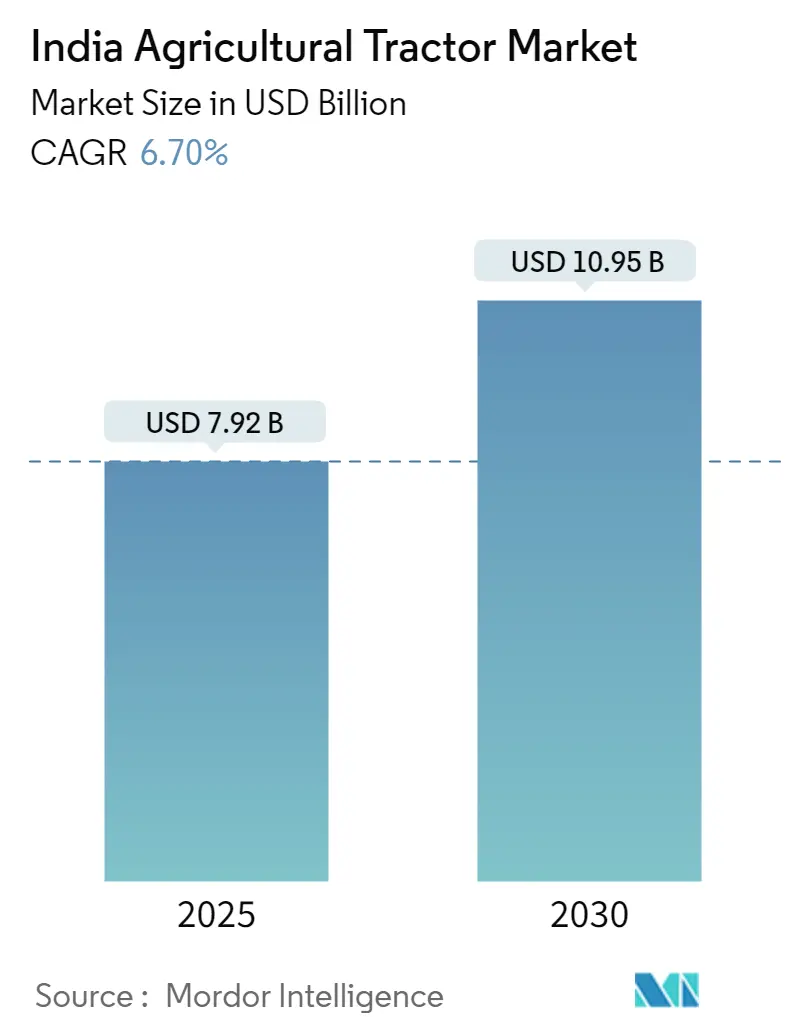

| Market Size (2025) | USD 7.92 Billion |

| Market Size (2030) | USD 10.95 Billion |

| Growth Rate (2025 - 2030) | 6.70% CAGR |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Agricultural Tractor Market Analysis

The India Agricultural Tractor Market size is estimated at USD 7.92 billion in 2025, and is expected to reach USD 10.95 billion by 2030, at a CAGR of 6.7% during the forecast period (2025-2030).

The Indian agricultural landscape continues to undergo significant transformation, with approximately 51.09% of the country's land dedicated to agriculture. However, the sector is experiencing a gradual shift in its workforce dynamics, as evidenced by World Bank data showing a decline in agricultural employment from 44% in 2021 to 43.4% in 2022. This structural change has catalyzed the adoption of advanced agricultural machinery and farm equipment, particularly in regions with diverse agro-climatic conditions. The evolving agricultural landscape has prompted manufacturers to develop more sophisticated and efficient tractor solutions that address the specific needs of different farming operations.

The industry is witnessing a remarkable technological revolution, particularly in the realm of sustainable and smart farming solutions. In January 2024, Tractors and Farm Equipment Limited (TAFE) marked a significant milestone by introducing electric tractors equipped with auto-steer and advanced farm management systems. This innovation reflects the industry's commitment to environmental sustainability and technological advancement. Similarly, in February 2024, Sonalika Tractors launched a new range of 10 advanced heavy-duty tractors under the "Tiger" series, featuring cutting-edge technologies like CRDS and HDM+ engines, demonstrating the industry's focus on innovation and efficiency.

The horticulture sector has emerged as a significant driver of tractor demand, with the area under horticulture production expanding from 28.04 million hectares in 2021-2022 to 28.44 million hectares in 2022-2023. This growth has led to increased demand for specialized agricultural equipment designed for orchard and vineyard operations. Manufacturing companies are responding to this trend by establishing strategic partnerships and expanding their production capabilities. For instance, in October 2023, VST Tillers Tractors and HTC Investments (owners of the ZETOR brand) formed a strategic alliance to deliver high-quality tractors specifically designed for Indian farmers' needs.

The industry is experiencing significant capital investments in manufacturing infrastructure, reflecting confidence in the market's growth potential. Major manufacturers are expanding their production facilities to meet the growing demand and incorporate advanced manufacturing technologies. In March 2024, Sonalika Tractors invested in two new plants in Hoshiarpur, Punjab, including a tractor assembly facility and a high-pressure foundry plant. Similarly, Escorts Kubota Ltd announced plans to invest approximately Rs 4,500 crore in a new manufacturing plant in Rajasthan, aiming to double their domestic tractor production capacity to 3.4 lakh units annually. These investments underscore the industry's commitment to enhancing production capabilities and maintaining technological leadership in the global market.

India Agricultural Tractor Market Trends

Increasing Farm Mechanization Rates

Farm mechanization in India has been experiencing significant growth due to several interconnected factors, including shrinking land and water resources, a decreasing agricultural labor force, increasing power availability, and supportive government policies. According to World Bank data, employment in agriculture decreased from 44% in 2021 to 43% in 2022, indicating a continuing shift away from traditional farming practices. This decline in the agricultural workforce is driving farmers to adopt mechanized solutions, particularly farm machinery like tractors, to maintain and enhance productivity levels while compensating for labor shortages.

The penetration of farm machinery in India remains relatively low compared to other major agricultural nations, with the United States at 95% and Brazil at 75% mechanization rates. This presents a significant opportunity for growth, especially considering that approximately 80% of Indian farmers are small and marginal landholders with less than five hectares. To address this, the Indian government has implemented the Sub-Mission on Agricultural Mechanization (SMAM), focusing on increasing mechanization through various support mechanisms and technological advancement initiatives. The program particularly emphasizes 'balanced farm mechanization' by providing subsidies on various equipment and supporting bulk buying through front-end agencies to increase mechanization levels across different farming operations.

Understand The Key Trends Shaping This Market

Download PDF

Rising Trend of Custom Hiring of Tractors

The custom hiring model has emerged as a revolutionary concept in Indian agriculture, making modern agricultural machinery accessible to small and marginal farmers through a pay-per-use system. As of 2023, major agricultural states have established extensive networks of custom hiring centers, with Punjab leading at 11,133 centers, followed by Andhra Pradesh with 8,471 centers, and Haryana with 8,253 centers. This widespread availability of custom hiring facilities has significantly reduced the financial burden on farmers while ensuring access to modern agricultural machinery.

The state governments are actively expanding their custom hiring infrastructure to support farmers. For instance, in March 2024, the Madhya Pradesh government announced the establishment of 3,000 new custom hiring centers, offering a 40% credit-linked back-ended subsidy up to a maximum of INR 10 lakh for setting up these centers. These centers not only provide access to tractors but also offer skilled operator services at affordable rates, making it a more cost-effective solution compared to separate labor hiring. The success of this model has encouraged both government agencies and private players to invest in custom hiring services, creating a sustainable ecosystem for farm mechanization.

Growing Government Support to Enhance Farm Mechanization

The Indian government has demonstrated a strong commitment to agricultural mechanization through various targeted initiatives and subsidy programs. In 2024, the Bihar government implemented the "Bihar Agricultural Machinery Scheme" under the Bihar Krishi Yantra Yojana, offering substantial subsidies to farmers for purchasing agricultural implements, including tractors. Similarly, the Madhya Pradesh government launched the Kisan Anudhan Yojana in 2023, providing subsidies ranging from 30%-50% to support farmers in acquiring modern farming equipment and enhancing their operational efficiency.

The support extends beyond direct subsidies to include comprehensive agricultural development programs. For instance, the Assam government's Tractor Distribution Scheme under the Chief Minister Samagra Gramya Unnayan Yojna (CMSGUY) has made significant progress in revitalizing the agricultural sector. The scheme has successfully distributed approximately 10,109 tractors in its first phase, with plans to cover all 26,000 villages across the state. These initiatives, combined with credit programs and other support measures, are creating a favorable environment for increased farm mechanization and technological adoption in Indian agriculture, including the integration of precision farming equipment.

Segment Analysis: Engine Power

30-50 HP Segment in India Agricultural Tractors Market

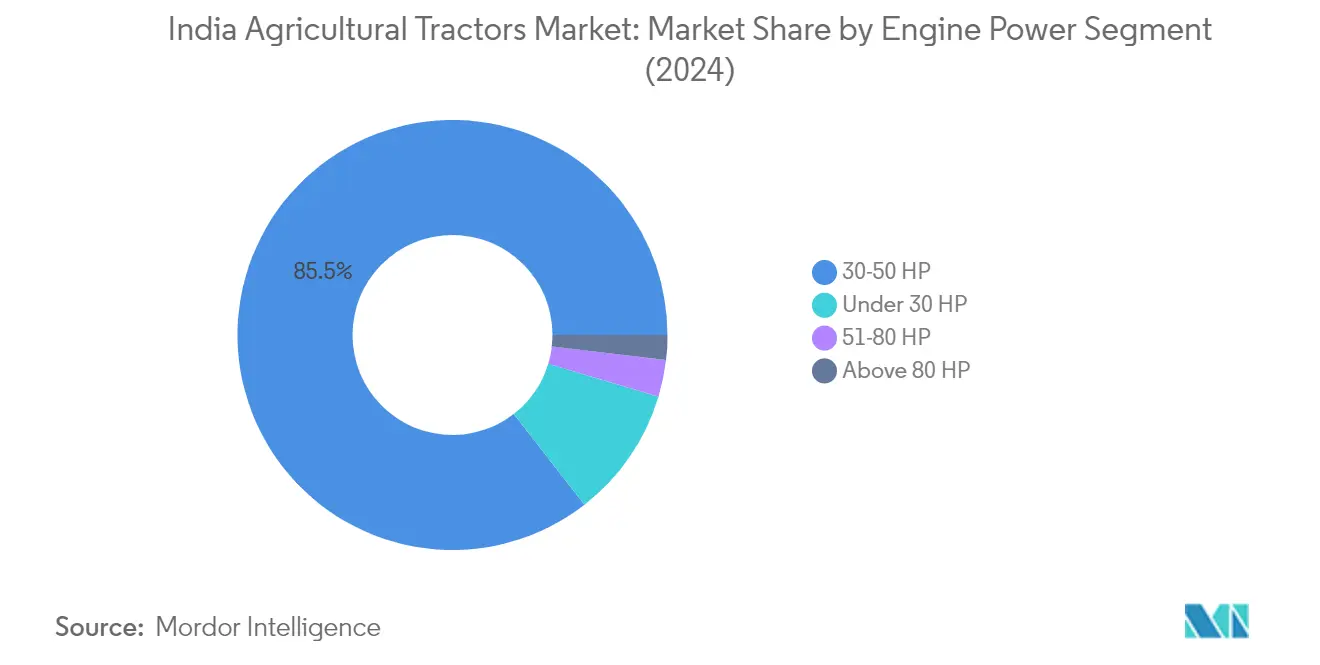

The 30-50 HP segment dominates the India Agricultural Tractors market, commanding approximately 86% market share in 2024, while also being the fastest-growing segment with a projected growth rate of around 7% during 2024-2029. This segment's prominence can be attributed to its optimal balance of power and cost-effectiveness for Indian farming conditions. With the average size of household ownership decreasing and farm holdings seeing a downward trend, these compact tractors prove viable and efficient for small farm holdings while being key to increasing productivity. The segment's growth is further supported by continuous product innovations from major manufacturers. For instance, in November 2022, VST Tillers Tractors Ltd and Zetor Tractors launched new tractor models with 40 & 50 HP engine capacities, addressing the specific needs of Indian farmers. The low cost of these tractors compared to higher horsepower variants, coupled with their fuel efficiency and versatility in handling various agricultural tasks, makes them particularly attractive to small and marginal farmers who constitute the majority of India's farming community.

Remaining Segments in Engine Power Segmentation

The other segments in the market include Under 30 HP, 51-80 HP, and Above 80 HP tractors, each serving specific agricultural needs. The Under 30 HP segment caters to small-scale farming operations and specialized applications like horticulture and gardening, offering compact and maneuverable solutions for smaller land holdings. The 51-80 HP segment serves medium to large-scale farming operations, providing enhanced power for heavy-duty agricultural tasks and specialized farming applications. The Above 80 HP segment, while representing a smaller portion of the market, plays a crucial role in large-scale commercial farming operations and specialized agricultural applications requiring significant power output. These segments complement each other by addressing diverse farming requirements across different land holding sizes and agricultural applications throughout India.

Segment Analysis: Drive Type

Two Wheel Drive Segment in India Agricultural Tractors Market

The Two Wheel Drive segment dominates the India Agricultural Tractors market, holding approximately 86% market share in 2024. These tractors are predominantly used in dry farming conditions where fields are not excessively muddy, sloped, or wet, making them ideal for operations like sowing seeds, spraying fertilizers and pesticides, and topping pastures. Two-wheel drive tractors have gained significant popularity among small and marginal farmers due to their cost-effectiveness, affordability, and improved maneuverability. These tractors are particularly efficient in fuel consumption, typically using between 2 to 5 liters per hour depending on engine size and working conditions. Major manufacturers like Sonalika, Mahindra and Mahindra, John Deere, Swaraj, and Eicher have strengthened their market position by offering innovative two-wheel drive tractors that cater specifically to the Indian agricultural landscape. The segment's dominance is further reinforced by these tractors' ability to handle basic farming activities effectively while maintaining lower operational costs compared to their four-wheel counterparts.

Four Wheel Drive Segment in India Agricultural Tractors Market

The Four Wheel Drive segment is emerging as the fastest-growing category in the India Agricultural Tractors market, projected to grow at approximately 7% CAGR from 2024 to 2029. These tractors are specifically engineered for challenging terrains and demonstrate superior performance in harsh, wet, and muddy farmland conditions. The segment's growth is driven by their versatility in performing multiple agricultural tasks beyond basic farming activities, including crop protection, loading, and construction work, thereby reducing the need for additional equipment purchases. Four-wheel drive tractors are particularly valued for their ability to efficiently operate several heavy-duty implements like cultivators and loaders, contributing to increased overall productivity while maintaining quality standards. Major manufacturers are actively investing in research and development to enhance these tractors' capabilities, as evidenced by John Deere's launch of the 5045 D PowerPro 4WD in 2023, which specifically addresses the needs of Indian farmers by improving agricultural efficiency and reducing labor requirements.

Segment Analysis: Application

Row Crop Tractor Segment in India Agricultural Tractors Market

The Row Crop Tractor segment dominates the India Agricultural Tractors Market, holding approximately 34% market share in 2024. These agricultural tractor machinery are specifically tailored to grow crops that meet all agricultural demands, such as plowing, harrowing, leveling, pulling seed drills, weed control, and running various machines like water pumps and belt pulley threshers. The segment's prominence is driven by the increasing unavailability of farm laborers and growing mechanization of agriculture. Row-crop tractors are provided with replaceable driving wheels of different tread widths and have high ground clearance to prevent crop damage. The increasing demand for power, precision, handling, and efficiency has shaped the development of the row crop tractor segment in India. Major players in the market are investing heavily in R&D work to develop innovative equipment and maintain a strong market foothold, with several new models being introduced featuring advanced technologies like integrated car-like headlamps, compact packaging with underhood mufflers, stylish SMC bonnets, and digital clusters. Additionally, the segment is projected to grow at the fastest rate of approximately 7% during 2024-2029, driven by these tractors' versatility as all-rounders and their effectiveness as substitutes for manual labor.

Remaining Segments in Application Segmentation

The other segments in the India Agricultural Tractors market include Orchard Tractors and Other Applications. Orchard tractors are specifically designed for creating and maintaining lawns, gardens, fruit crops, vines, and specialized agricultural operations. These utility tractors are light and compact, with a small turning radius drive that provides better traction for operation across terrains. The Other Applications segment encompasses utility tractors, which are general-purpose machines used for various agricultural operations, including small- and medium-sized farms and specialty agricultural industries such as dairy and livestock. These tractors are designed for tasks such as plowing and driving other types of equipment through their drives, offering features like compact design, user-friendly interfaces, and limited space requirements. Both segments contribute significantly to the market's diversity by catering to specific agricultural needs and operational requirements across different farming applications.

India Agricultural Tractor Industry Overview

Top Companies in India Agricultural Tractors Market

The Indian agricultural equipment tractors market features prominent players like Mahindra & Mahindra, Tractors and Farm Equipment Limited, International Tractors Limited, and Escorts Kubota Limited leading the industry. These companies are actively pursuing product innovation through the introduction of advanced tractor models incorporating new technologies like electric powertrains, automated guidance systems, and precision farming capabilities. Operational agility is demonstrated through rapid responses to changing market demands, with manufacturers developing region-specific models and customized solutions for different farming applications. Strategic moves in the industry are characterized by partnerships with financial institutions to provide easier financing options and collaborations with technology companies to enhance digital capabilities. Companies are also focusing on expanding their manufacturing footprint, with several players announcing new production facilities and capacity expansions to meet growing demand and strengthen their market presence.

Domestic Players Dominate Consolidated Market Structure

The Indian agricultural tractors market exhibits a highly consolidated structure dominated by domestic manufacturers who have built strong brand equity and extensive distribution networks over decades of operation. These local players have successfully competed against global agricultural equipment manufacturers through their deep understanding of Indian farming conditions and ability to offer cost-effective solutions tailored to local needs. The market features a mix of pure-play tractor manufacturers and diversified conglomerates, with the latter leveraging their broader industrial expertise and financial resources to maintain competitive advantages.

The industry has witnessed strategic consolidations through mergers and acquisitions, particularly involving international players seeking to establish or strengthen their presence in the Indian market. These M&A activities have primarily focused on technology transfer, manufacturing capability enhancement, and distribution network expansion. The partnerships between domestic and global players have resulted in knowledge sharing and product development synergies, contributing to the overall advancement of the industry while maintaining its predominantly Indian character.

Innovation and Distribution Drive Market Success

Success in the Indian agricultural tractors market increasingly depends on manufacturers' ability to balance technological innovation with affordability while maintaining strong distribution and after-sales support networks. Incumbent players can strengthen their market position by investing in research and development to introduce advanced features that improve productivity and reduce operating costs for farmers. Companies must also focus on developing comprehensive product portfolios that address various farming applications and power requirements while maintaining strong relationships with dealers and financial institutions to ensure product accessibility.

For contenders looking to gain market share, the key lies in identifying and serving underserved segments through specialized products and innovative business models. This includes developing application-specific tractors for niche farming operations and introducing flexible ownership models to address affordability concerns. While the risk of substitution remains low due to tractors' essential role in agricultural automation, manufacturers must stay attuned to evolving regulatory requirements, particularly regarding emissions and safety standards. The concentrated nature of the end-user base, primarily comprising small and medium-sized farmers, necessitates a deep understanding of local farming practices and economic conditions for successful market penetration.

India Agricultural Tractor Market Leaders

-

Mahindra & Mahindra Limited

-

John Deere India Private Limited

-

TAFE Limited

-

Escorts Group

-

International Tractors Ltd (Sonalika)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

India Agricultural Tractor Market News

- October 2024: Mahindra & Mahindra launched the Mahindra Arjun 605 DI 4WD tractor to address the increasing demand for higher horsepower tractors during farming seasons. The company introduced the new tractor model in Punjab, Haryana, Madhya Pradesh, Rajasthan, and Uttar Pradesh.

- April 2024: Swaraj Tractors introduced five variants in a limited edition on its 50th anniversary. This edition, available for two months, has MS Dhoni's signature as a symbol of gratitude to the customers.

- March 2024: Sonalika Tractors invested USD 157.4 million for two new plants in Punjab. The company invested USD 121.1 million in a new tractor assembly plant and USD 36.3 million in a high-pressure foundry.

India Agricultural Tractor Industry Segmentation

A tractor is an engineered vehicle designed to provide high tractive effort at low speeds, primarily used to pull agricultural machinery or trailers. This report focuses exclusively on tractors used in agricultural operations. It does not include other agricultural machinery or tractor attachments. Tractors designed for industrial and construction purposes are excluded from the study's scope.

The Indian agricultural tractor market is segmented by engine power (less than 30 HP, 31-50 HP, 51-80 HP, and above 80 HP), drive type (two-wheel drive and four-wheel drive), application (row crop tractors, orchard tractors, and other applications), and geography (Uttar Pradesh, Madhya Pradesh, Maharashtra, Rajasthan, Gujarat, and other regions).

The report provides market estimation and forecast in value terms (USD) for each segment.

| Engine Power | Less than 30 HP |

| 31-50 HP | |

| 51-80 HP | |

| Above 80 HP | |

| Drive Type | Two-wheel Drive |

| Four-wheel Drive | |

| Application | Row Crop Tractors |

| Orchard Tractors | |

| Other Applications | |

| Geography | Uttar Pradesh |

| Madhya Pradesh | |

| Maharashtra | |

| Rajasthan | |

| Gujarat | |

| Others |

Engine Power

| Less than 30 HP |

| 31-50 HP |

| 51-80 HP |

| Above 80 HP |

Drive Type

| Two-wheel Drive |

| Four-wheel Drive |

Application

| Row Crop Tractors |

| Orchard Tractors |

| Other Applications |

Geography

| Uttar Pradesh |

| Madhya Pradesh |

| Maharashtra |

| Rajasthan |

| Gujarat |

| Others |

Need A Different Region or Segment?

Customize Now

India Agricultural Tractor Market Research FAQs

How big is the India Agricultural Tractor Market?

The India Agricultural Tractor Market size is expected to reach USD 7.92 billion in 2025 and grow at a CAGR of 6.70% to reach USD 10.95 billion by 2030.

What is the current India Agricultural Tractor Market size?

In 2025, the India Agricultural Tractor Market size is expected to reach USD 7.92 billion.

Who are the key players in India Agricultural Tractor Market?

Mahindra & Mahindra Limited, John Deere India Private Limited, TAFE Limited, Escorts Group and International Tractors Ltd (Sonalika) are the major companies operating in the India Agricultural Tractor Market.

What years does this India Agricultural Tractor Market cover, and what was the market size in 2024?

In 2024, the India Agricultural Tractor Market size was estimated at USD 7.39 billion. The report covers the India Agricultural Tractor Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the India Agricultural Tractor Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: December 10, 2024