In Situ Hybridization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

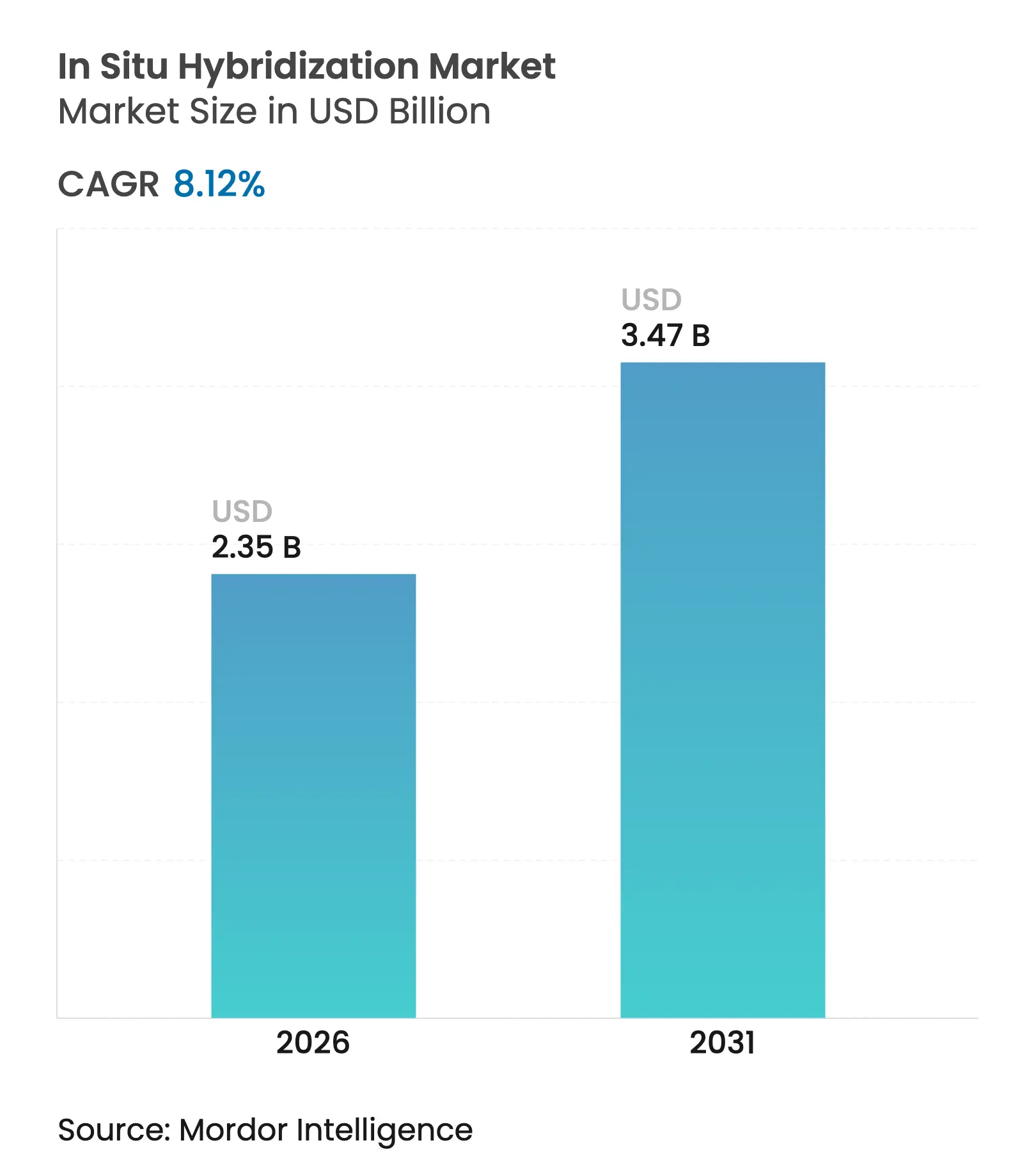

| Market Size (2026) | USD 2.35 Billion |

| Market Size (2031) | USD 3.47 Billion |

| Growth Rate (2026 - 2031) | 8.12 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

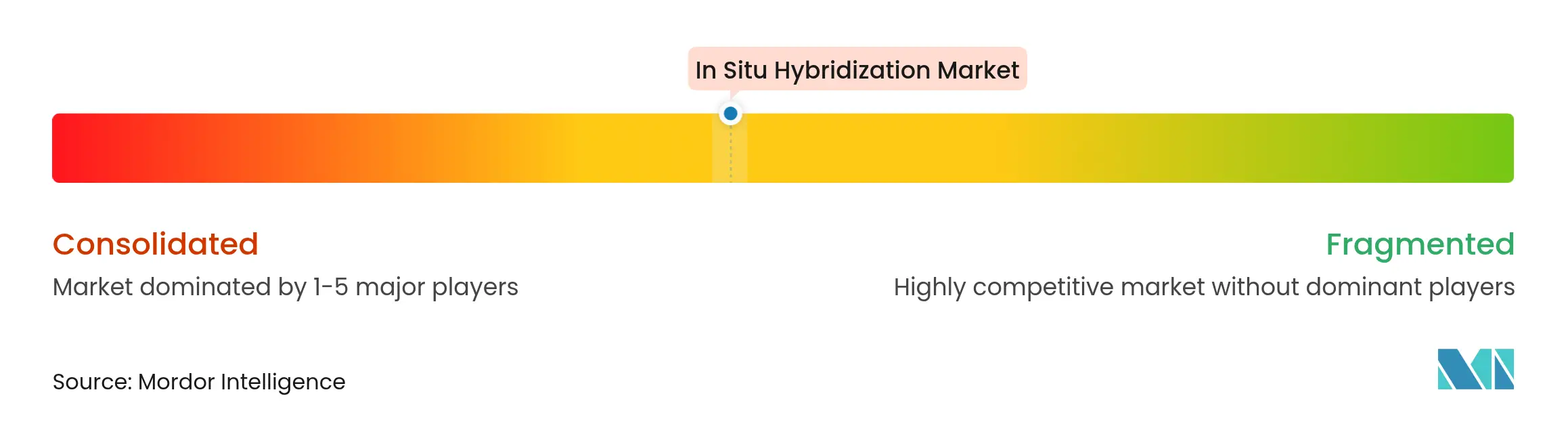

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

In Situ Hybridization Market Analysis by Mordor Intelligence

The acceleration stems from precision-medicine programs that rely on spatial genomics to guide oncology, infectious-disease and neuroscience diagnostics. Regulatory support is growing; the 2025 FDA decision to shift ISH test systems from Class III to Class II removes a costly pre-market hurdle, allowing faster product launches. High disease prevalence, especially cancer, keeps testing volumes high, while AI-driven image analysis cuts turnaround times and labor costs. Rising investments in spatial transcriptomics platforms and automated slide processors reinforce adoption, and consumable demand rises in parallel as new RNA-ISH probe chemistries routinely replace legacy reagents. Asia-Pacific is expanding fastest as national genomics plans reshape reimbursement policy and boost test uptake.

Key Report Takeaways

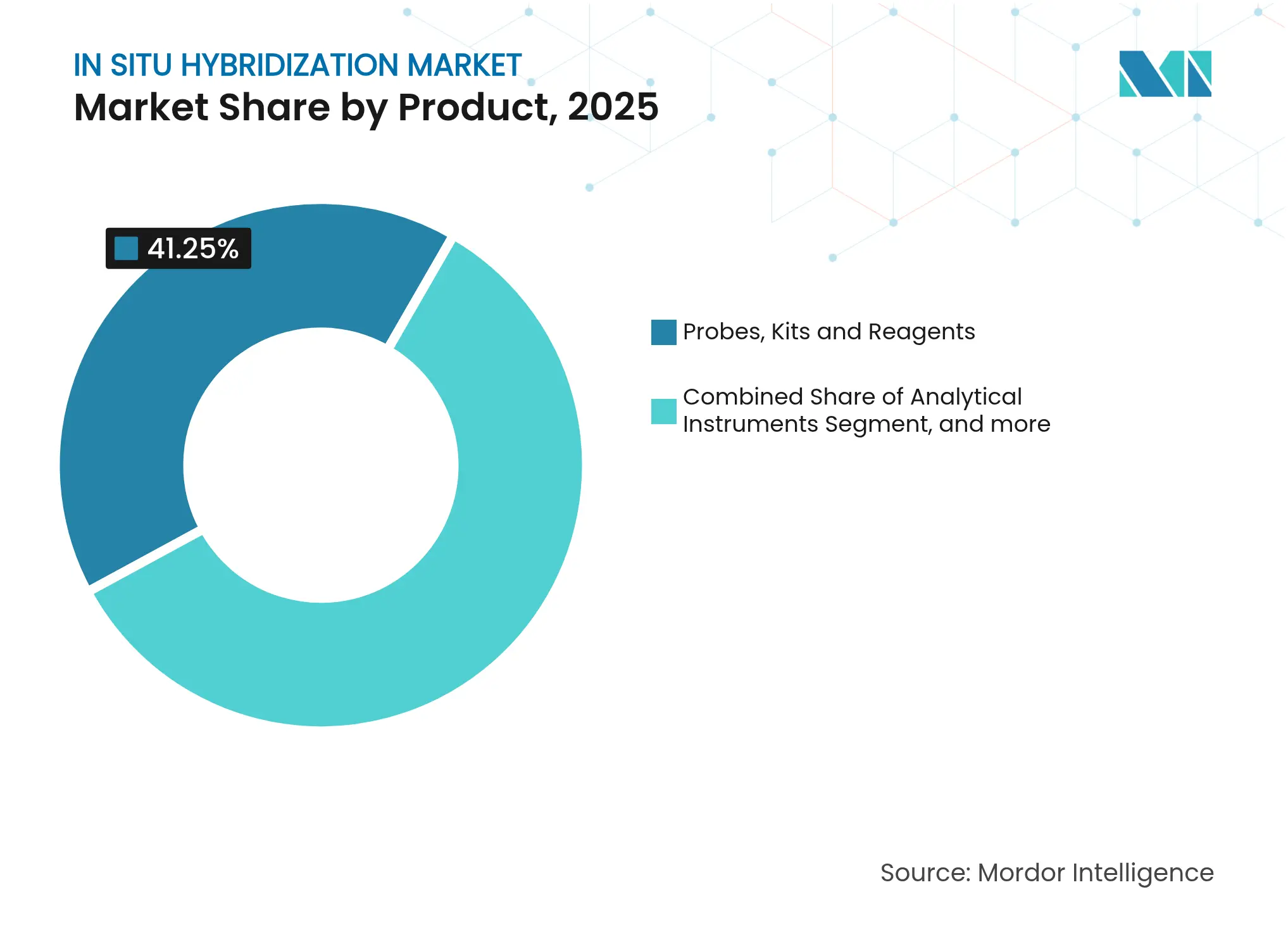

- By product type, probes, kits, and reagents led with 41.25% revenue share in 2025; this consumables segment is forecast to expand at a 10.29% CAGR through 2031.

- By technique, fluorescence ISH commanded 60.45% of the in situ hybridization market share in 2025, while amplified RNA-ISH platforms are projected to grow at 12.95% CAGR to 2031.

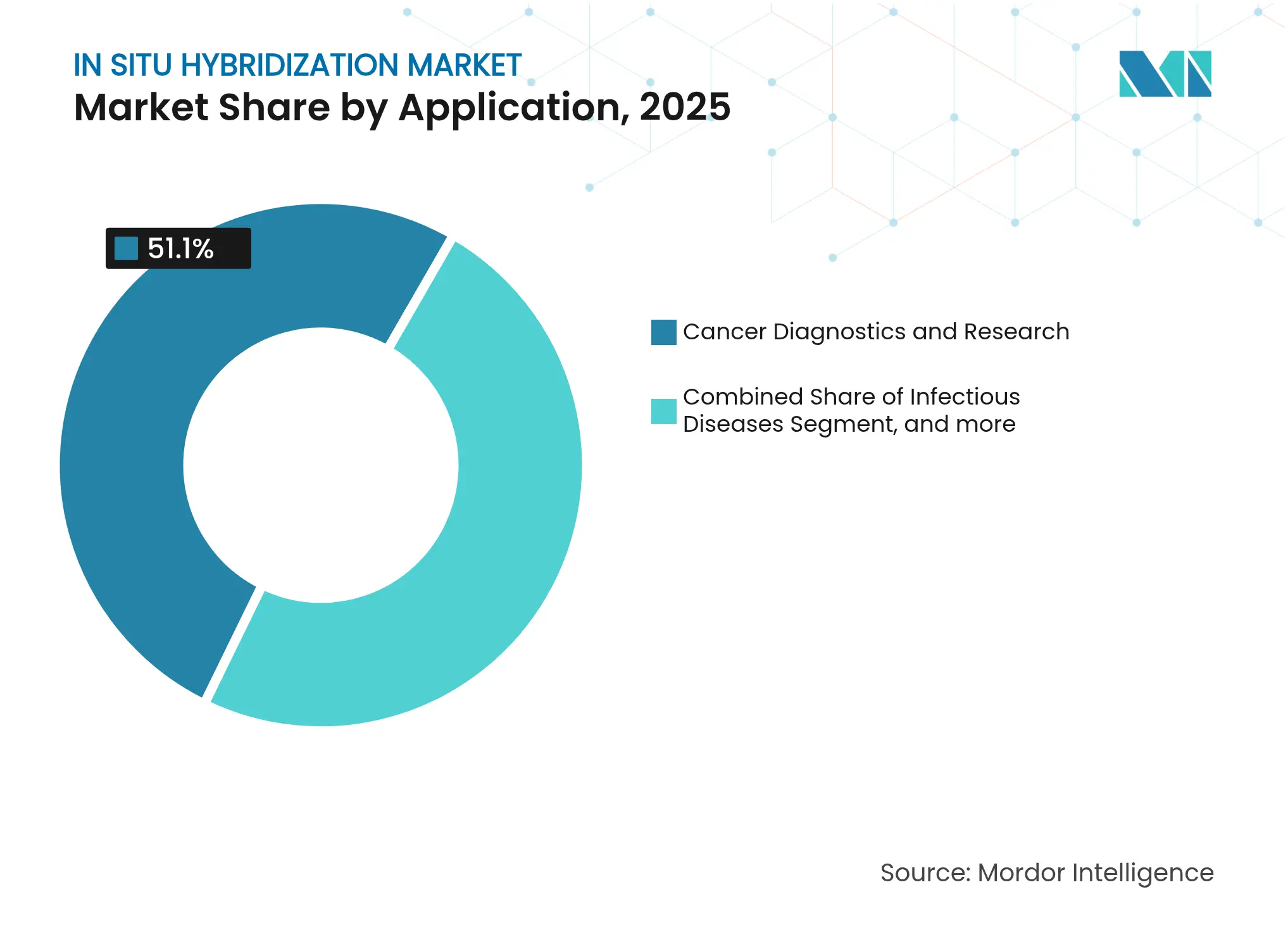

- By application, cancer diagnostics captured 51.10% of the in situ hybridization market size in 2025; neuroscience applications are projected to rise at 13.20% CAGR between 2026-2031.

- By end user, diagnostic laboratories held 44.05% of revenue in 2025, while academic and research institutes post the quickest expansion at 11.05% CAGR to 2031.

- By geography, North America accounted for 36.35% of global revenue in 2025; Asia-Pacific is expected to register a 12.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global In Situ Hybridization Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising burden

of cancer, infectious & genetic diseases

Rising burden

of cancer, infectious & genetic diseases

| +2.1% | Global, higher in North America & Europe | Long term (≥ 4 years) |

(~) %

Impact on CAGR Forecast

:

+2.1%

|

Geographic

Relevance

:

Global,

higher in North America & Europe

|

Impact

Timeline

:

Long term (≥

4 years)

|

Growing

adoption of companion diagnostics & precision oncology

Growing

adoption of companion diagnostics & precision oncology

| +1.8% | North America & EU, expanding to APAC | Medium term (2-4 years) | |||

Technological

advances in automated, multiplex RNA-ISH platforms

Technological

advances in automated, multiplex RNA-ISH platforms

| +1.5% | Global, led by developed markets | Short term (≤ 2 years) | |||

Investment

boom in spatial genomics & transcriptomics workflows

Investment

boom in spatial genomics & transcriptomics workflows

| +1.2% | North America & EU, emerging in APAC | Medium term (2-4 years) | |||

AI-driven

image analysis accelerating ISH throughput

AI-driven

image analysis accelerating ISH throughput

| +0.9% | Global, concentrated in high-tech systems | Short term (≤ 2 years) | |||

Emergence of

point-of-care ISH kits for decentralised testing

Emergence of

point-of-care ISH kits for decentralised testing

| +0.6% | Global, impactful in emerging markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Burden of Cancer, Infectious & Genetic Diseases

Global cancer incidence now tops 20 million new cases annually, intensifying demand for spatially resolved biomarker tests that guide targeted therapy. Large-scale genome programs, such as the UK 100,000 Genomes Project and Japan’s Action Plan for Whole-Genome Analysis, embed tissue-based RNA localization into clinical workflows, confirming ISH as a frontline diagnostic tool.[1]Hui Han, “National Actions on Cancer Genomics,” Cancer Biology & Medicine, cancerbiomed.org WHO pandemic-preparedness frameworks for mpox likewise identify tissue ISH as a critical detection method, underlining its infectious-disease relevance.[2]Seema Lakdawala, “Advances in Mpox Detection,” Nature Communications, nature.com Genetic-disease programs increasingly mandate tissue-specific RNA mapping to understand phenotypic variation, further lifting test volumes. Longer lifespans and widespread screening initiatives bring more early-stage lesions to pathology labs, driving routine adoption of highly sensitive probes. These overlapping dynamics ensure the in situ hybridization market maintains a robust trajectory through the decade.

Growing Adoption of Companion Diagnostics & Precision Oncology

The pivot toward precision oncology is evident as payors require biomarker confirmation before reimbursing many targeted drugs. Dual ISH-IHC workflows that co-detect RNA and protein markers are gaining traction, enabling same-slide confirmation of gene expression and pathway activation. FDA green-lights for combined whole-exome and transcriptome assays reinforce the clinical expectation that a single test deliver comprehensive genomic insight.[3]Food and Drug Administration, “Reclassification of In Situ Hybridization Device Systems,” fda.gov Commercial alliances, such as QIAGEN’s QIAstat-Dx partnerships with AstraZeneca, embed ISH probes inside multiplex cartridges so oncologists can act on results during the initial consultation. Net effect: the in situ hybridization market benefits from growing per-test value as laboratories shift from single-gene FISH panels to multi-target RNA-ISH kits.

Technological Advances in Automated, Multiplex RNA-ISH Platforms

Automation is transforming bench workflows. Roche’s BenchMark ULTRA processes up to 120 slides overnight and allows continuous loading, collapsing turnaround from days to hours. Bio-Techne’s protease-free RNAscope preserves morphology while enabling dual RNA-protein reads, eliminating artifacts common in harsh pre-treatment steps. Next-generation chemistries such as FISHnCHIPs boost signal-to-noise 20-fold, exposing transcripts once below the detection thresholds. DART-FISH, capable of profiling thousands of genes in a day, moves spatial transcriptomics into everyday lab routines. By lowering hands-on time and elevating multiplexing, these devices fuel recurring probe sales and widen clinical indications, underpinning the expansion of the in situ hybridization market.

Investment Boom in Spatial Genomics & Transcriptomics Workflows

Investors see spatial biology edging from discovery to clinical necessity. 10X Genomics alone has deployed over USD 1 billion in R&D to commercialize its Xenium in-tissue sequencing platform, building a large installed base only three years after launch. Leica Biosystems’ stake in Indica Labs merges whole-slide scanners with AI analytics, demonstrating the push to integrate hardware, consumables, and software in one ecosystem. Agilent’s USD 925 million BIOVECTRA acquisition strengthens its oligonucleotide manufacturing, ensuring probe supply security for high-growth users. Bruker’s takeover of NanoString folds nCounter and CosMx assets into a broader life-science franchise, giving customers a single vendor for sample prep, hybridization, and imaging. These capital flows legitimize spatial-omics as core diagnostic infrastructure and channel new users toward the in situ hybridization market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Shortage of

skilled molecular pathologists & cytogeneticists

Shortage of

skilled molecular pathologists & cytogeneticists

| -1.4% | Global, most severe in rural & developing regions | Long term (≥ 4 years) |

(~) %

Impact on CAGR Forecast

:

-1.4%

|

Geographic

Relevance

:

Global, most

severe in rural & developing regions

|

Impact

Timeline

:

Long term (≥

4 years)

|

High cost of

advanced ISH instruments & probes

High cost of

advanced ISH instruments & probes

| -1.1% | Global, impactful in emerging markets | Medium term (2-4 years) | |||

Regulatory

uncertainty around multiplex clinical ISH assays

Regulatory

uncertainty around multiplex clinical ISH assays

| -0.8% | Varies by jurisdiction | Short term (≤ 2 years) | |||

Competition

from sequencing-based spatial omics platforms

Competition

from sequencing-based spatial omics platforms

| -0.7% | Developed markets with advanced sequencing infrastructure | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Shortage of Skilled Molecular Pathologists & Cytogeneticists

Fewer than 14 pathologists per million population serve the global patient base, and retirements outpace trainee numbers in every region. The ASCP survey logged vacancy rates above 8% in cytology and molecular labs, jeopardizing throughput for high-complexity tests. ISH interpretation relies on fine-grained pattern recognition and knowledge of signal amplification artifacts, competencies seldom covered in general pathology residencies. While automation trims staining time, final case sign-out still requires credentialed experts. Staffing gaps slow lab onboarding of new ISH panels, tempering growth even as instrument capability rises across the in situ hybridization market.

High Cost of Advanced ISH Instruments & Probes

Fully automated slide processors carry price tags above USD 500,000, and multiplex probe sets can exceed USD 200 per slide, creating steep entry barriers for mid-volume labs. Reimbursement lags product innovation; US molecular labs report 90-day payment cycles and frequent claim denials for complex panels. NIH guidance now urges developers to align regulatory and payment strategies early, highlighting financial risk as much as technical feasibility nih.gov. Emerging point-of-care systems lower capex but trade off multiplex capacity, limiting revenue per test. Without cost-containment measures, the price hurdle will continue to weigh on the in situ hybridization market.

Segment Analysis

By Product: Consumables Sustain Market Leadership

Recurring reagent demand anchors growth. Probes, kits, and reagents held 41.25% of 2025 revenue and are expected to post a 10.29% CAGR, reflecting continuous redesign cycles that refresh catalogs every 18-24 months. The in situ hybridization market relies on these consumables for annuity-like sales, as each new oncology guideline typically spawns an updated panel requiring novel probe sets. Bio-Techne’s RNAscope series, cited in more than 12,000 papers, demonstrates the magnet effect of validated probe chemistry on laboratory purchasing decisions.

Instrument sales follow but at a steadier pace. Automated stainers, hybridization ovens, and fluorescent microscopes reflect replacement cycles of five to seven years, capping unit volume. Yet software and analytics services are expanding fastest inside the equipment bundle, as labs subscribe to cloud image-analysis suites rather than buying perpetual licenses. These subscription fees diversify vendor revenues and partially buffer the price erosion facing older hardware lines in the in situ hybridization market.

Note: Segment shares of all individual segments available upon report purchase

By Technique: FISH Remains Anchor as RNA-ISH Surges

Fluorescence ISH retained 60.45% of the in situ hybridization market share in 2025 due to entrenched lab protocols and decades of proficiency-testing data. It remains the go-to assay for HER2 and ALK rearrangements in breast and lung cancer, securing a stable baseline of oncology volume. However, amplified RNA-ISH formats grow at 12.95% CAGR because they map expression rather than purely structural changes, matching the biomarker shift toward transcriptomic signatures. FISHnCHIPs and HCR chemistries deliver 20-fold sensitivity gains, prompting more labs to adopt RNA panels for tumors with low transcript abundance. As multiplex capacities climb into the hundreds, RNA-ISH platforms move beyond research use to clinical decision support, strengthening their share in the in situ hybridization market.

Chromogenic ISH holds niche roles where bright-field microscopes dominate, notably in community hospitals without fluorescence scanners. In-situ sequencing, though still early, lures high-budget centers that value open-ended gene discovery. Vendors now bundle microfluidics and barcoding kits, lowering experimental friction and preparing the ground for future clinical reimbursement.

By Application: Cancer Diagnostics Dominate, Neuroscience Accelerates

Cancer testing generated 51.10% of revenue in 2025 and shows steady volume growth as more tumor types gain biomarker-linked therapies. Roche’s VENTANA Kappa/Lambda dual RNA-ISH assay, FDA-cleared in 2025, streamlined B-cell lymphoma typing on one slide, cutting biopsy repeats and reinforcing laboratory dependence on multi-target panels. Companion-diagnostic partnerships funnel pharma marketing dollars into testing outreach, lifting utilization, and bolstering the in situ hybridization market size attached to oncology.

Neuroscience owns the fastest-growing slice at a 13.20% CAGR. Whole-brain mapping studies now rely on multiplex ISH combined with tissue clearing to pinpoint cell-type-specific expression across cortical layers. Techniques such as MERFISH unravel developmental gradients and disease-linked circuit disruptions at single-cell scale. Funding agencies increasingly earmark grants for spatial brain atlases, compelling core facilities to invest in high-plex RNA-ISH instruments. Infectious-disease and inherited-disorder panels hold steady demand, but their growth tilts toward regions pursuing newborn-screening mandates rather than blockbuster volume shifts.

Note: Segment shares of all individual segments available upon report purchase

By End User: Diagnostic Labs Lead, Academia Scales Quickly

Diagnostic laboratories captured 44.05% of 2025 spending on reagents and instruments, as community hospitals integrate ISH into routine service lines. High test throughput rewards automation, with multi-slide loaders trimming turnarounds to less than eight hours. Yet workforce shortages force labs to lean on AI software that pre-classifies images and flags borderline cases for human review, enhancing consistency while stretching staffing budgets.

Academic and research institutes grow at 11.05% CAGR as spatial transcriptomics joins the essential-equipment list for core facilities. Grant agencies now view multiplex ISH as complementary to single-cell RNA-seq, encouraging labs to cross-validate expression patterns. These purchases often precede technology diffusion to nearby diagnostics labs, effectively seeding future demand across the in situ hybridization market. Pharma and biotech firms, meanwhile, deploy platform instruments in translational programs to validate drug targets and develop companion biomarker assays, broadening vendor pipelines for service contracts and custom probe design.

Geography Analysis

North America retained the top regional position with 36.35% of global revenue in 2025. Widespread insurance coverage for molecular oncology, extensive biopharma pipelines and the FDA’s class-downlisting of ISH systems ensure steady instrument turnover. Academic-industry clusters in Boston and the Bay Area foster continual probe innovation, while NIH grants finance method development. Yet reimbursement audits by Medicare Administrative Contractors slow cashflow for smaller labs, pushing some to outsource high-plex panels rather than invest in onsite capability.

Europe ranks second, anchored by Germany, the United Kingdom, and France. National cancer plans tie drug access to validated biomarker status, increasing probe usage. The EU In Vitro Diagnostic Regulation harmonizes market clearance, and hospital tenders increasingly specify AI-enabled scanners, amplifying the service side of the in situ hybridization market. Budget ceilings nonetheless squeeze mid-tier hospitals; many rely on regional reference labs for multiplex RNA-ISH while retaining single-plex FISH locally.

Asia-Pacific is the fastest-growing territory with a projected 12.05% CAGR. China scales nationwide genomic screening for lung, gastric and colorectal cancers and invests in local probe manufacturing, lowering unit costs and stimulating domestic instrument sales. Japan’s Action Plan for Whole-Genome Analysis earmarks funding for transcriptomics diagnostics, catalyzing clinical deployment of automated RNA-ISH systems. India’s biotechnology clusters in Bengaluru and Hyderabad attract venture funding for point-of-care ISH kits aimed at tuberculosis and HPV screening. However, the shortage of pathologists outside tier-one cities and fragmented reimbursement programs temper the absolute uptake rate.

Competitive Landscape

Market Concentration

The in situ hybridization market is moderately consolidated. The major players operating globally in the In Situ Hybridization Market are Abnova Corporation, Agilent Technologies Inc., F. Hoffmann-La Roche Ltd, Biocare Medical LLC., Genemed Biotechnologies Inc., Thermo Fisher Scientific Inc., Biogenex Laboratories, Zytomed Systems GmbH, Creative Bioarray, and Bio SB Inc. Thermo Fisher Scientific, Roche, and Abbott leverage broad life-science portfolios to bundle sample prep, hybridization, and imaging with data analytics. Roche cross-markets the BenchMark instrument family with its NAVIFY Digital Pathology suite, embedding AI calls inside the LIS to widen customer lock-in.

Disruptive entrants focus on high-plex spatial biology. Bio-Techne’s Advanced Cell Diagnostics defends its RNAscope IP aggressively and collaborates with Leica Biosystems to integrate slide scanners. 10X Genomics channels more than USD 300 million annually into Xenium roadmap updates, adding whole-exome expansion panels that threaten conventional multiplex FISH. Bruker’s 2024 acquisition of NanoString aggregates nCounter expression profiling with CosMx spatial imaging, pressing incumbents to accelerate pipeline refresh cycles.

White-space opportunities sit in cost-sensitive markets. Several Chinese vendors ship compact bench-top stainers under USD 60,000 and partner with reagent OEMs to keep consumable margins competitive. European start-ups pursue fully-closed microfluidic cartridges that reduce biosafety-level requirements, courting regional clinics that lack complex lab infrastructure. Strategic alliances, technology-license swaps and litigation over amplification chemistries signal an active IP battlefield that will shape competitive dynamics through 2030.

In Situ Hybridization Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Molecular Instruments (MI), a trailblazer in bioimaging technology, is proud to announce a landmark achievement in precision dermatology. In partnership with the Department of Dermatology at Yale School of Medicine, MI has successfully developed and implemented novel laboratory-developed tests (LDTs) utilizing its proprietary HCR™ Pro RNA in situ hybridization (RNA-ISH) platform.

- January 2025: Roche received FDA clearance for the VENTANA Kappa and Lambda Dual ISH mRNA Probe Cocktail, the first clinically approved in-situ hybridization test for assessing B-cell lymphoma subtypes. The test can evaluate over 60 B-cell lymphoma subtypes on a single tissue slide, reducing the need for multiple biopsies and enhancing diagnostic accuracy for hematopathology applications.

Table of Contents for In Situ Hybridization Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Burden of Cancer, Infectious & Genetic Diseases

- 4.2.2Growing Adoption of Companion Diagnostics & Precision Oncology

- 4.2.3Technological Advances in Automated, Multiplex RNA-ISH Platforms

- 4.2.4Investment Boom in Spatial Genomics & Transcriptomics Workflows

- 4.2.5AI-Driven Image Analysis Accelerating Ish Throughput

- 4.2.6Emergence of Point-Of-Care ISH Kits for Decentralised Testing

- 4.3Market Restraints

- 4.3.1Shortage of Skilled Molecular Pathologists & Cytogeneticists

- 4.3.2High Cost of Advanced Ish Instruments & Probes

- 4.3.3Regulatory Uncertainty Around Multiplex Clinical ISH Assays

- 4.3.4Competition from Sequencing-Based Spatial Omics Platforms

- 4.4Porter’s Five Forces Analysis

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitutes

- 4.4.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value in USD)

- 5.1By Product

- 5.1.1Analytical Instruments

- 5.1.2Probes, Kits & Reagents

- 5.1.3Software & Services

- 5.1.4Other Products

- 5.2By Technique

- 5.2.1Fluorescence ISH (FISH)

- 5.2.2Chromogenic ISH (CISH)

- 5.2.3Amplified RNA-ISH (HCR, RNAscope)

- 5.2.4In-situ Sequencing (ISS)

- 5.3By Application

- 5.3.1Cancer Diagnostics & Research

- 5.3.2Infectious Diseases

- 5.3.3Genetic & Rare Disorders

- 5.3.4Neurological & Developmental Biology

- 5.3.5Other Applications

- 5.4By End User

- 5.4.1Diagnostic Laboratories

- 5.4.2Academic & Research Institutes

- 5.4.3Pharma-Biotech & CROs

- 5.4.4Veterinary & Environmental Labs

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East & Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East & Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Abnova Corporation

- 6.3.2Agilent Technologies Inc.

- 6.3.3F. Hoffmann-La Roche Ltd

- 6.3.4Abbott Laboratories

- 6.3.5Thermo Fisher Scientific Inc.

- 6.3.6Qiagen N V

- 6.3.7Merck KGaA

- 6.3.8PerkinElmer Inc.

- 6.3.9Bio-Techne (Advanced Cell Diagnostics)

- 6.3.10Biocare Medical LLC

- 6.3.11Genemed Biotechnologies Inc.

- 6.3.12BioGenex Laboratories

- 6.3.13Zytomed Systems GmbH

- 6.3.14Oxford Gene Technology

- 6.3.15NanoString Technologies Inc.

- 6.3.1610x Genomics Inc.

- 6.3.17Leica Biosystems Nussloch GmbH

- 6.3.18Molecular Instruments Inc.

- 6.3.19Creative Diagnostics

- 6.3.20Enzo Life Sciences Inc.

- 6.3.21IncellDx Inc.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global In Situ Hybridization Market Report Scope

As per the scope of the report, it is a technique that allows precise localization of a specific segment of nucleic acid within a histologic section. It is a laboratory technique to localize a sequence of DNA or RNA in a biological sample.

The In Situ Hybridization Market is segmented by Product (Analytical Instruments, Kits and Reagents, Software and Services, and Other Products), Technique (Fluorescence In Situ Hybridization(FISH), and Chromogenic In Situ Hybridization(CISH)), Application (Cancer, Infectious Diseases, and Other Applications), End User (Diagnostics Laboratories, Academic and Research Institutions, and Contract Research Organizations (CROs)), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.