IMSI Catcher Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 207.68 Million |

| Market Size (2031) | USD 306.47 Million |

| Growth Rate (2025 - 2031) | 8.08% CAGR |

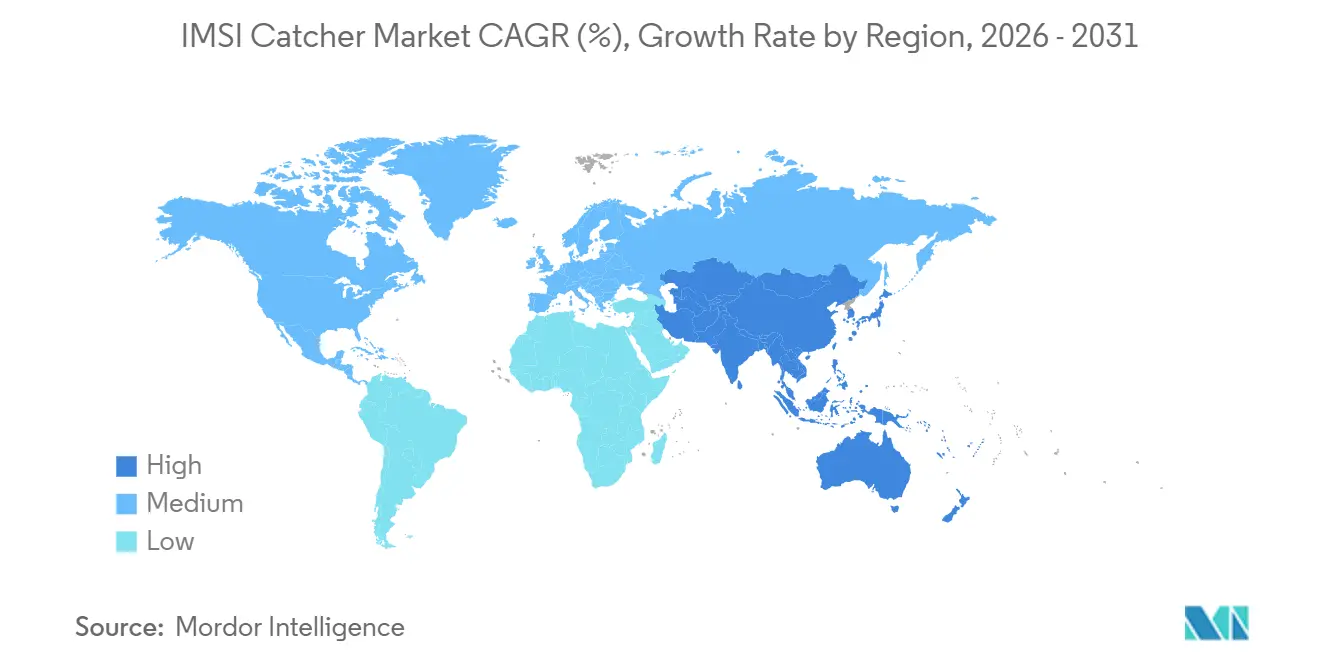

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

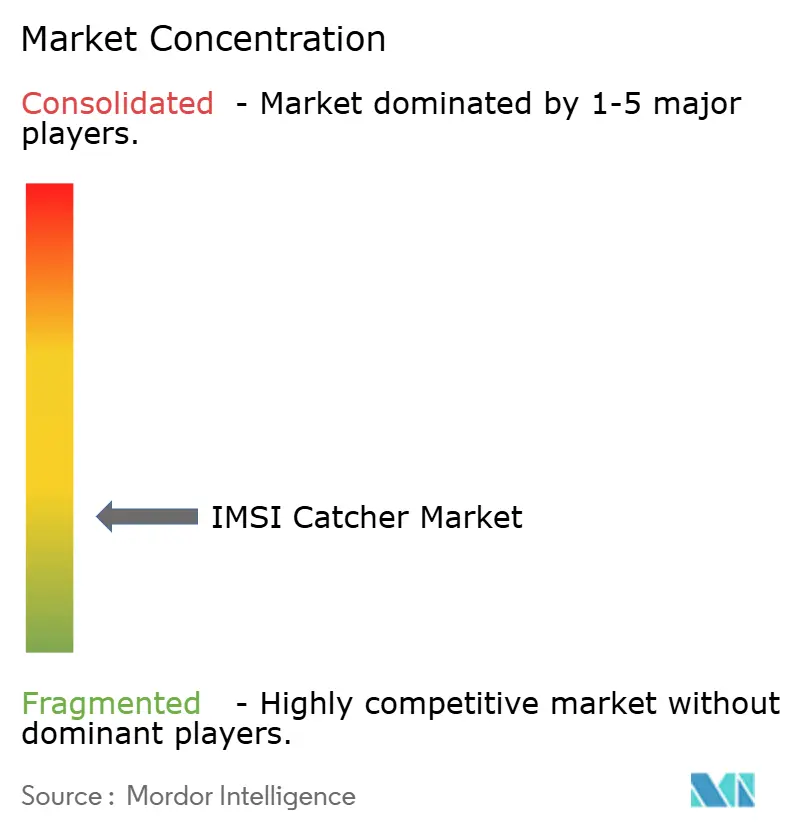

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IMSI Catcher Market Analysis by Mordor Intelligence

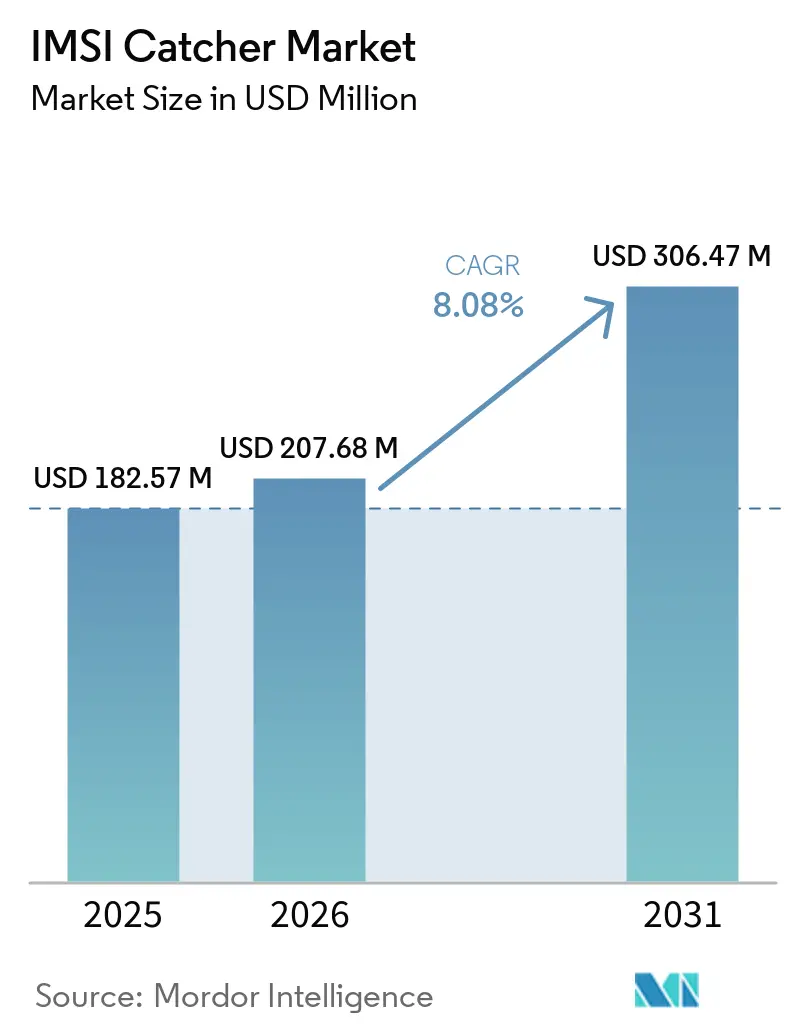

The IMSI catcher market size is expected to increase from USD 182.57 million in 2025 to USD 207.68 million in 2026 and reach USD 306.47 million by 2031, growing at a CAGR of 8.08% over 2026-2031. The IMSI catcher market continues to draw support from steady procurement by law enforcement agencies, intelligence services, and defense establishments that still operate across mixed legacy and next-generation cellular environments. Demand remains split between mature procurement cycles in North America and Western Europe, where annual budgets and established usage frameworks support repeat purchases, and newer national security programs in Asia-Pacific, the Middle East, and parts of South America that are building interception capability for the first time. The IMSI catcher market also benefits from the global dominance of 5G non-standalone deployments, because these networks still depend on 4G-era architecture and preserve identifier exposure pathways that keep existing LTE-capable systems commercially relevant. Competitive conditions remain moderate, with larger defense electronics vendors facing pressure to add software-defined and backward-compatible 5G functionality while smaller specialists stay relevant through faster development cycles, customizable platforms, and pricing flexibility in export-authorized tenders. Legal oversight and the gradual spread of 5G standalone networks are reshaping the IMSI catcher market, which means near-term demand remains healthy, but medium-term vendor positioning now depends on credible solutions for environments where legacy interception methods lose effectiveness.

Key Report Takeaways

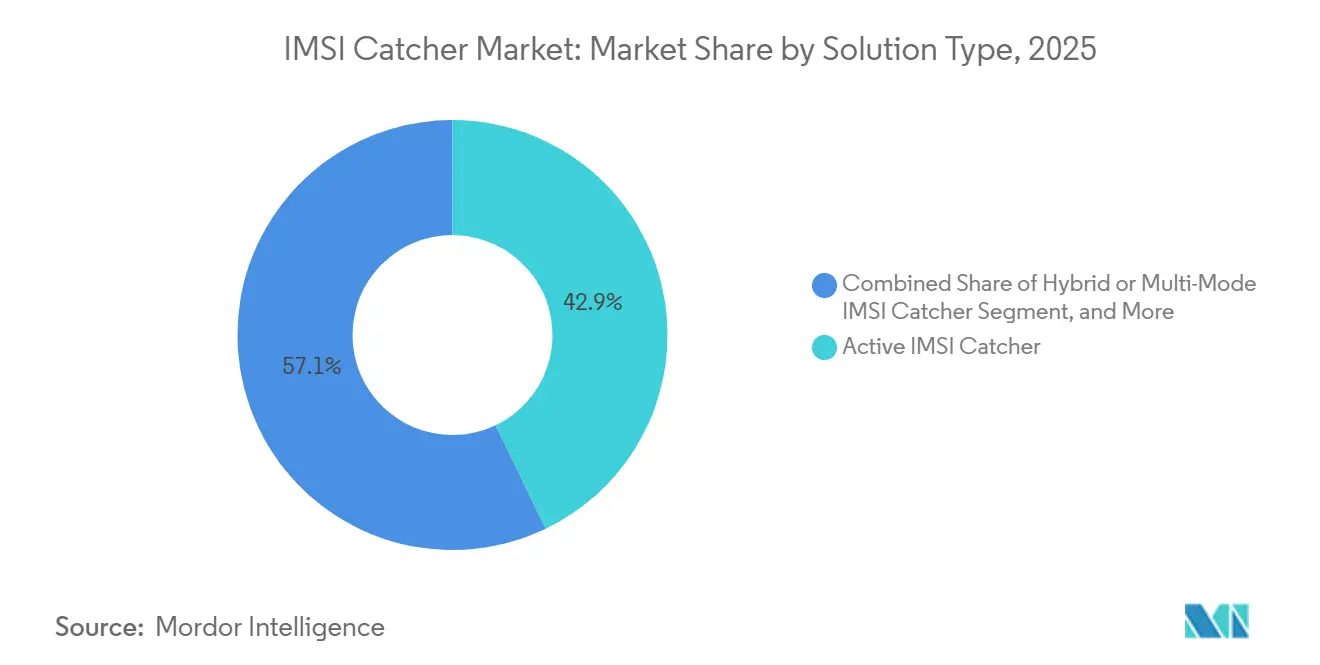

- By solution type, active IMSI catcher led with 42.87% of revenue in the IMSI catcher market 2025, while hybrid and multi-mode units are projected to record the fastest growth at a 9.67% CAGR through 2031.

- By form factor, portable briefcase configurations held 38.23% of revenue in the international mobile subscriber identity (IMSI) catcher market in 2025, while drone-mounted platforms are forecast to expand at a 11.38% CAGR through 2031.

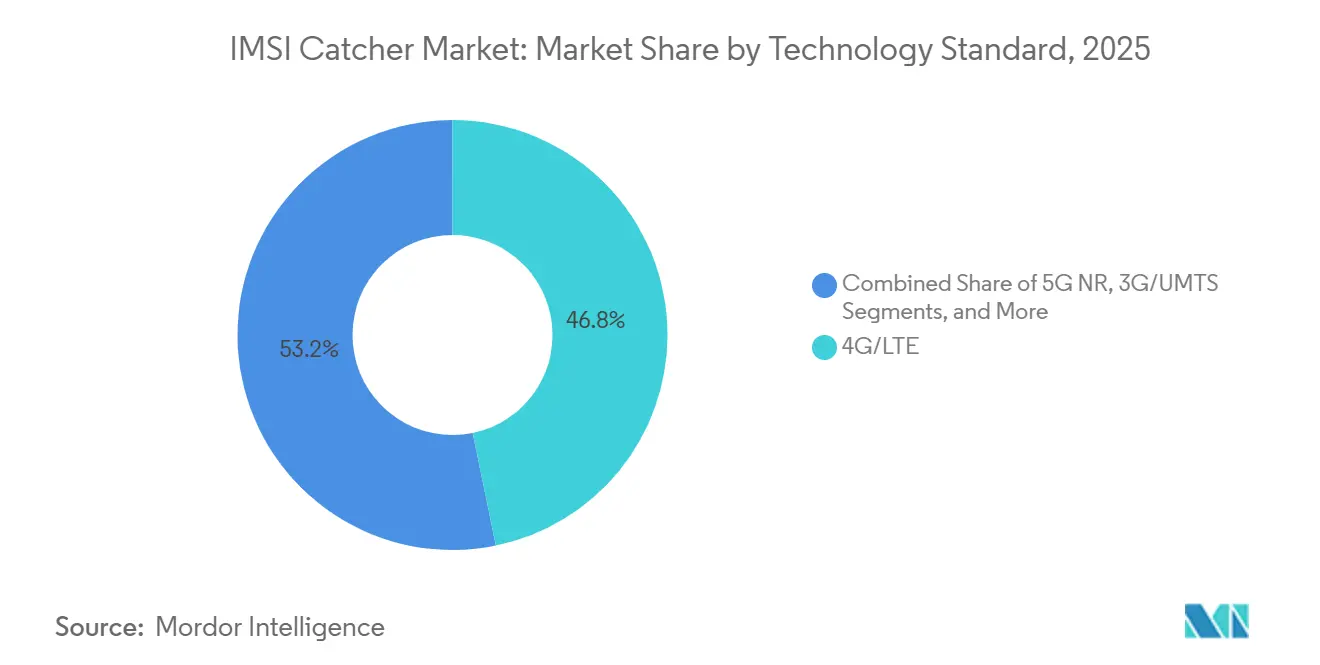

- By technology standard, 4G/LTE solutions accounted for 46.77% of revenue in the IMSI catcher market in 2025, while 5G NR solutions are expected to advance at a 11.44% CAGR through 2031.

- By end user, law enforcement agencies held 51.68% of revenue in the international mobile subscriber identity (IMSI) catcher market in 2025, while military and defense forces are projected to post the fastest growth at a 10.63% CAGR through 2031.

- By geography, North America captured 35.66% of global revenue in the IMSI catcher market in 2025, while Asia-Pacific is forecast to grow at the fastest regional CAGR of 10.98% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global IMSI Catcher Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Demand From Law Enforcement And Intelligence Agencies | +3.2% | Global, with concentrated volumes in North America and Western Europe | Short term (≤ 2 years) |

| Rising Border Security And Counterterror Modernization Budgets | +2.5% | APAC, Middle East, North America, Eastern Europe | Medium term (2-4 years) |

| 4G/LTE And 5G Migration Driving Multi-Band Upgrade Cycles | +2.1% | Global, led by APAC and North America 5G rollout zones | Medium term (2-4 years) |

| Growing Adoption Of Portable, Vehicular, And Airborne Platforms | +1.4% | Global, with early gains in Middle East, APAC, and North America | Short to medium term (≤ 4 years) |

| Expansion Of Prison Contraband-Phone And Sensitive-Facility Missions | +0.6% | North America and Europe | Long term (≥ 4 years) |

| Convergence Of Tactical SIGINT, Counter-UAS, And Cross-Border Tracking Workflows | +0.4% | Middle East, APAC, Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Demand From Law Enforcement And Intelligence Agencies

The IMSI catcher market continues to benefit from direct spending by agencies that are still refreshing or expanding operational fleets rather than treating interception hardware as a one-time purchase. In the United States, ICE executed vehicle-related cell-site simulator contracts across September 2024 and May 2025, which showed that procurement had moved beyond older handheld deployments and into purpose-built mobile platforms for homeland security operations. Demand is also broadening across local and regional agencies, as shown by the San Francisco Police Department's December 2025 exigent deployment of a borrowed device under court authorization, which points to a shared-use model that can still support fresh purchases across multiple jurisdictions.[1]Derrick J. Lew, “Exigency Report to Board of Supervisors Re. Cellular Communications Interception Technology on December 31, 2025,” San Francisco Police Department, sanfranciscopolice.org The NYPD's February 2026 policy revision kept judicial oversight in place while clarifying how the tool may be used, which suggests that oversight has not stopped usage but has made contract structure and operating rules more formal. Cognyte's March 2026 expansion with a Tier-1 EMEA national security agency further shows that the international mobile subscriber identity (IMSI) catcher market now includes multi-year renewals and analytics scale-ups in addition to first-time hardware acquisition.[2]Cognyte Software Ltd., “Cognyte Secures Approximately USD 5 Million Follow-on Order as Top NATO-Member Military Organization Advances Intelligence Modernization,” Cognyte, cognyte.com

Rising Border Security And Counterterror Modernization Budgets

The IMSI catcher market is also gaining from defense and interior ministry spending that now links cellular interception with aerial surveillance, direction finding, and cross-border monitoring missions. The US Army's December 2025 sources-sought notice for an airborne anti-terrorism and border security SIGINT system under Foreign Military Sales to Egypt showed clear demand for 2G, 3G, and 4G interception with IMSI and IMEI extraction from aircraft operating at high altitude. Cognyte's military and national security contract wins across late 2025 and early 2026 also indicate that buyers are choosing scalable tactical SIGINT systems that can replace incumbent platforms across several mission environments. This demand is widening the addressable geography of the international mobile subscriber identity (IMSI) catcher market because Eastern European and North African contracts are no longer reserved for a narrow group of Anglo-American suppliers. At the same time, export access remains controlled, and vendors still need to navigate dual-use licensing rules under Wassenaar and national regulations before they can convert these modernization budgets into delivered systems.

4G/LTE And 5G Migration Driving Multi-Band Upgrade Cycles

The IMSI catcher market remains closely tied to the fact that most active 5G infrastructure still uses non-standalone architecture built on a 4G core. This matters because NSA deployments preserve the 4G downgrade pathway, which keeps legacy LTE-capable interception hardware useful even as operators expand 5G radio coverage.[3]Stavros Eleftherakis, Domenico Giustiniano, and Nicolas Kourtellis, “SoK, Evaluating 5G Protocols Against Legacy and Emerging Privacy and Security Attacks,” arXiv, arxiv.orgAgencies with single-generation inventories are now facing a clearer replacement case, since operational environments increasingly include a mix of 2G, 3G, 4G, and 5G access layers that cannot be covered efficiently by older single-band devices. The April 2025 release of ETSI TS 33.127 V18.11.0 reinforced this shift by formalizing lawful interception architecture across 2G through 5G under 3GPP Release 18, which raises the importance of multi-generation capability in government procurement.[4]European Telecommunications Standards Institute, “Digital Cellular Telecommunications System (Phase 2+) (GSM), Universal Mobile Telecommunications System (UMTS), LTE, 5G, Lawful Interception (LI) Architecture and Functions (3GPP TS 33.127 Version 18.11.0 Release 18),” ETSI, etsi.org As a result, the international mobile subscriber identity (IMSI) catcher market is moving toward backward-compatible, software-defined, multi-band platforms that can operate across today's mixed networks while giving agencies a path into more advanced 5G environments.

Growing Adoption Of Portable, Vehicular, And Airborne Platforms

The IMSI catcher market is also being shaped by a shift in platform preference rather than by radio capability alone. Drone-mounted systems have gained attention because they can cover difficult terrain, scan from altitude, and reach areas that are inefficient for fixed or vehicle-based sweeps. Spain's Military Emergency Unit received 6 drone-deployable IMSI catcher units from Amper through ETRA Group in May 2025, which confirmed that this form factor had already moved from concept into formal government delivery. Portable and briefcase units remain important because they can be used in transit hubs, large buildings, and urban operations where a vehicle cannot be positioned effectively. Vehicular units still matter for persistent border surveillance and inter-agency operations, so the international mobile subscriber identity (IMSI) catcher market is not shifting toward one dominant platform but toward a broader portfolio of task-specific configurations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tighter Privacy, Warrant, And Export-Control Oversight | -1.5% | North America and Europe, spill-over to APAC through Wassenaar-aligned states | Medium term (2-4 years) |

| 5G Identifier Concealment And Stronger Authentication | -0.9% | Global, sharpest where 5G SA penetration is highest, US, South Korea, Japan | Long term (≥ 4 years) |

| Open-Source Detection Tools And 2G Disablement Reducing Covert Effectiveness | -0.6% | North America and Europe | Medium term (2-4 years) |

| Shift Toward Lower-Cost Alternative Location And Device-Forensics Tools | -0.4% | North America and Western Europe | Short to medium term (≤ 4 years) |

| Source: Mordor Intelligence | |||

Tighter Privacy, Warrant, And Export-Control Oversight

The IMSI catcher market faces a slower sales cycle in major procurement regions because legal authorization rules are becoming more explicit and more restrictive. In the Netherlands, a joint interpretation from TIB and CTIVD in November 2024 stated that Article 47(4) of the Wiv 2017 is the valid basis for state international mobile subscriber identity (IMSI) catcher deployment, which means operations require ministerial approval and regulatory review rather than a broader reading of existing authority. Germany's Federal Constitutional Court added another constraint in June 2025 by narrowing the legal scope for source telecommunications surveillance in lower-penalty criminal cases, which may influence how proportionality is interpreted across other European jurisdictions. The 2025 Wassenaar dual-use control list also placed mobile telecommunications interception equipment under code 5.A.1.f., which tightened export licensing expectations across 42 participating states. In the United Kingdom, the June 2025 Equipment Interference Code of Practice revision reinforced judicial commissioner approval and proportionality assessment requirements, which adds another compliance layer for agencies and vendors serving sensitive operations.

5G Identifier Concealment And Stronger Authentication

The IMSI catcher market also faces a structural technical challenge as 5G standalone networks spread and reduce the value of legacy interception methods. NIST documented that 5G SA uses the Subscription Concealed Identifier with ECIES-based protection, so the permanent subscriber identity is not exposed in cleartext over the air, which removes the direct identifier path that active catchers historically relied on. T-Mobile US reported zero SUPI exposures on its 5G SA network since launch, while still recording monthly IMSI exposure events on its 4G network, which shows both the strength of SA protection and the continued relevance of NSA and LTE-linked vulnerabilities. NIST's later work on temporary identity reallocation further showed that 3GPP protections are reducing another path for passive tracking in 5G environments. The international mobile subscriber identity (IMSI) catcher market, therefore, remains viable in near-term mixed-network environments, but vendors increasingly need lawful-intercept-linked approaches or technically credible 5G SA workarounds such as SS8's February 2026 identity resolution patent if they want to defend medium-term relevance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Active Devices Dominate Revenue, Hybrid Configurations Accelerate

Active IMSI catcher held 42.87% of the IMSI catcher market share in 2025, which kept them as the leading revenue segment because they can trigger registration quickly and return IMSI, IMEI, and TMSI data in the same operating cycle. Their position in the IMSI catcher market remains tied to time-sensitive law enforcement work, where operators often need immediate device identification and cannot wait for slower passive collection windows. This functional advantage has kept active systems central to tactical deployments even as oversight has become stricter in several major procurement markets. Law enforcement demand reinforces that pattern because agencies that buy at scale still prioritize operational certainty, rapid response, and standardized workflows over purely covert collection features. Vendors serving this part of the IMSI catcher market, therefore, continue to compete on speed, multi-band support, and integration with command-and-control environments rather than on concealment alone.

Passive devices still occupy a durable role because they collect without transmitting radio signals, which makes them better suited to long-duration covert work in settings where any active RF signature would create operational risk. Intelligence agencies remain the main fit for these systems because their missions more often favor persistence, discretion, and selective collection over forced network interaction. Hybrid and multi-mode units are forecast to grow at a 9.67% CAGR through 2031, which reflects procurement demand for platforms that can switch between active identification, passive monitoring, and selective-access control without hardware replacement. This shift is also changing revenue mix inside the IMSI catcher market because software-defined hybrid systems usually carry higher selling prices and support longer platform life than single-mode devices. Amper's SICIDG-R24-2, which supports simultaneous 16-carrier processing across 2G through 5G NR with SDR and SoC architecture, shows how vendors are designing active and hybrid platforms for mobility, auto-configuration, and operational continuity across complex environments.

By Form Factor: Portable Briefcase Configurations Lead, Drone-Mounted Platforms Redefine Area Coverage

Portable briefcase configurations accounted for 38.23% of the IMSI catcher market size in 2025, which kept them as the leading form factor because they balance coverage, concealment, and deployment ease across dense urban settings. Their appeal comes from practical use in transit hubs, event venues, office towers, and other locations where a vehicle cannot be positioned close enough and fixed infrastructure is unavailable. The IMSI catcher market still relies heavily on these briefcase units because they fit standard law enforcement workflows and support rapid movement between locations during live operations. Compact SDR processing and directional antenna designs have improved the range and accuracy of these systems while keeping them fully portable. That combination has allowed the briefcase category to hold a leading revenue position even as more specialized formats gain attention.

Fixed and vehicular platforms remain important for persistent surveillance, perimeter missions, and inter-agency field operations that need a stable onboard power and control environment. ICE's cell-site simulator vehicle procurement across 2024 and 2025 showed continued demand for integrated mobile platforms that support federal tactical use and longer operating windows. Handheld devices continue to serve close-access missions where covert carriage matters more than broad-area collection. Drone-mounted platforms are projected to expand at a 11.38% CAGR through 2031, and the Hocell IMSIX02 illustrates why, since it supports 4 simultaneous SDR channels, detection of up to 800 terminals per minute, and positioning within 10 meters from heights up to 400 meters GNSS.AE. The airborne segment is becoming a distinct engineering niche in the IMSI catcher industry because weight, power efficiency, vibration tolerance, and 5G NSA compatibility must all be optimized for UAV deployment rather than for ground-based use alone.

By Technology Standard: 4G/LTE Anchors Revenue, 5G NR Solutions Lead Growth

4G/LTE solutions represented 46.77% of the IMSI catcher market size in 2025, which kept them as the anchor technology because LTE remains widespread, and 5G NSA still preserves 4G-linked interception vectors. This has given the IMSI catcher market a useful transition period in which buyers can continue operating LTE-capable systems without facing immediate obsolescence. In many mid-income and emerging markets, LTE is still the main cellular layer, so 4G-capable hardware remains operationally relevant across several procurement cycles. At the same time, 2G/GSM and 3G/UMTS are losing standalone importance as network operators continue legacy shutdown programs. That decline is not removing older generations from procurement logic, but it is pushing the IMSI catcher market toward multi-band systems that can handle any active network layer encountered in the field.

Multi-band platforms are gaining popularity because agencies increasingly operate across jurisdictions where cellular architecture is uneven and where a single mission may still encounter several active standards. ETSI TS 33.127 V18.11.0 strengthened that direction by formalizing lawful interception architecture from 2G through 5G, which makes pan-generation capability more relevant in procurement and compliance discussions. 5G NR solutions are forecast to grow at a 11.44% CAGR through 2031, which makes them the fastest-growing technology segment in the IMSI catcher market as agencies seek future-proof hardware. Peer-reviewed security work still identifies residual pathways such as downgrade induction and newer tracking methods, which is why buyers have not treated 5G SA as a complete barrier to collection capability. SS8's February 2026 patent for non-downgrade 5G SA user equipment identity resolution shows that the IMSI catcher industry is moving from research-stage debate toward early commercial attempts to solve the 5G SA challenge.

By End User: Law Enforcement Anchors Volume, Military Segment Records Fastest Growth

Law enforcement agencies held 51.68% of revenue in 2025, which made them the structural base of the IMSI catcher market because procurement is supported by repeat budgeting, established operational rules, and inter-agency sharing frameworks. Their purchasing behavior is more regular than that of many other buyer groups, which helps stabilize annual demand even when legal oversight becomes tighter. This part of the IMSI catcher market is also supported by a mature vendor ecosystem that already provides portable, vehicular, fixed, and analytics-linked systems tailored to municipal, state, and federal workflows. Intelligence agencies remain the second-largest buyer group and usually favor passive or hybrid configurations that suit longer collection windows and lower-signature missions. Private security companies stay smaller in scale and are concentrated in correctional institutions, government campuses, and secure facilities where communications control and geofencing are becoming more relevant than traditional interception in some jurisdictions.

Telecom operators and regulators are still a small buyer category, but they are appearing more often in the IMSI catcher market as passive rogue-cell detection and network integrity tools gain relevance under lawful interception and security compliance frameworks. ETSI's April 2025 update to TS 33.127 reinforced the technical importance of multi-generation lawful interception functions, which supports this small but emerging demand pool. Military and defense forces are forecast to grow at a 10.63% CAGR through 2031, which makes them the fastest-growing end-user segment in the IMSI catcher market as modernization programs embed cellular SIGINT into multi-domain electronic warfare packages. Cognyte's sequential wins with Tier-1 military organizations in late 2025 and early 2026, including an initial deal and a follow-on expansion, show how defense buyers are extending tactical SIGINT across land, air, and maritime missions rather than treating it as a narrow niche tool. The pull from counter-UAS and cross-domain targeting is reinforcing that trend because military users increasingly want tools that can tie a cellular signature to a wider operational threat picture.

Geography Analysis

North America held 35.66% of the IMSI catcher market share in 2025, which kept the region in the lead because of broad federal procurement, established operating policies, and a dense base of domestic suppliers. The United States remains the main anchor of regional demand, and ICE's CSS vehicle contracts across 2024 and 2025 showed that federal use still supports purpose-built mobile interception platforms rather than only legacy handheld tools. The NYPD's February 2026 policy update also showed that major urban agencies continue to maintain formal operating frameworks for cell-site simulators under tighter public accountability rules. The SFPD's December 2025 exigent deployment, supported through inter-jurisdictional borrowing under court authorization, pointed to a layered operating model that can preserve use even when every agency does not own a full system. Canada and Mexico add regional demand through organized crime interdiction, border coordination, and immigration-related security programs tied to North American cross-border enforcement.

Europe remains the second-largest regional block in the IMSI catcher market, with demand centered in Germany, the United Kingdom, France, Israel, and a growing group of Central European NATO members. Procurement in the region is still active, but oversight changes are making purchasing timelines more formal and more document-heavy. Germany's June 2025 Constitutional Court order narrowed the legal setting for some surveillance use cases, which adds proportionality pressure to future deployments. The United Kingdom's revised Equipment Interference Code of Practice in June 2025 added another layer of judicial and proportionality review for targeted operations.

Asia-Pacific is projected to grow at a 10.98% CAGR through 2031, which makes it the fastest-growing regional part of the IMSI catcher market as defense and public security modernization programs continue to expand. China adds pricing pressure through its domestic interception ecosystem, while India supports demand through border security and counterinsurgency needs that favor portable and drone-mounted systems. South Korea and Japan matter because faster 5G SA rollout makes them natural early-adoption markets for newer 5G-compatible hardware as vendors close the technical gap. South America remains an emerging growth area led by Brazil and Argentina, although fiscal volatility and import licensing can delay procurement cycles. The Middle East has one of the strongest per-capita security spending profiles and supports both procurement and manufacturing, especially through Israel, Saudi Arabia, the UAE, and Turkey, while Africa remains the least-penetrated region and depends more heavily on bilateral assistance and capacity-building channels than on large direct sovereign purchases.

Competitive Landscape

The IMSI catcher market remains moderately fragmented, with a small group of vertically integrated defense and intelligence vendors operating alongside a broader set of specialist suppliers, regional integrators, and SDR-focused companies. Rohde and Schwarz, L3Harris Technologies, and Cognyte sit in the upper tier because they can address more of the workflow from signal capture through analytics and lawful-intercept-aligned delivery. Their position is supported by compliance readiness, longer service relationships, and the ability to participate in larger institutional procurement cycles rather than only in one-off tactical tenders. The broader field still matters because smaller vendors from Israel, Spain, and Central Europe compete effectively on price, customization, and faster iteration cycles. This combination keeps the IMSI catcher market from becoming highly concentrated, even though a few larger players have stronger visibility and deeper government relationships.

Strategic moves in 2025 and 2026 show that software-defined capability is becoming a more important basis of competition. Rohde and Schwarz completed the acquisition of Software Radio Systems in March 2026, which strengthened its access to 5G SDR engineering and improved its position for future software-updatable cellular intelligence platforms. SS8's February 2026 patent publication for 5G standalone user equipment identity resolution showed that intellectual property around non-downgrade identification is becoming a real differentiator in the IMSI catcher market. Cognyte's March 2026 expansion with a Tier-1 national security agency also showed that vendors with analytics depth can capture multi-year renewals rather than compete only on box-level hardware replacement.

The most important white space remains 5G SA-compatible interception, where no vendor has yet established a clearly dominant globally deployed commercial solution. A second opening sits in prison and secure-facility communications control, where geofencing, passive monitoring, and managed-access approaches are becoming more relevant under changing telecom rules and where SS8's Quiet Zone framework points to broader product expansion beyond tactical interception. A third opening is the integration of counter-UAS and cellular SIGINT into a single deployable system that can associate a drone threat with its related cellular command path. Across all 3 areas, the IMSI catcher market is being filtered more strongly by export compliance, lawful-intercept alignment, and standards-readiness, which means technical capability alone is no longer enough to secure institutional demand.

IMSI Catcher Industry Leaders

Rohde and Schwarz GmbH and Co KG

Septier Communication Ltd.

L3Harris Technologies, Inc.

Rayzone Group Ltd.

PKI Electronic Intelligence GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: SS8 Networks published its Quiet Zone capability framework for private mobile network compliance in critical infrastructure, detailing geofencing-based cellular control for prisons and sensitive facilities using passive location, heuristic analysis, and active device monitoring to identify and disable unauthorized SIM-enabled devices. The solution addresses a growing market segment where managed-access control is replacing traditional jamming under evolving national telecommunications regulatory frameworks, positioning SS8 as a contender in the facility-level communications control niche beyond conventional tactical interception.

- March 2026: Rohde and Schwarz completed the acquisition of Software Radio Systems, an Irish specialist in 5G SDR systems with operations in Ireland, Spain, and the United States, effective March 5, 2026. The transaction expands Rohde and Schwarz's cellular and wireless communications software portfolio, accelerates AI-based test and non-terrestrial network roadmap development, and positions the combined entity to offer 5G SA-capable intelligence platforms ahead of its next hardware generation.

- March 2026: Cognyte Software Ltd. announced a USD 10+ million expansion with a Tier-1 EMEA national security agency, scaling the agency's deployment of Cognyte's investigative analytics platform, extending coverage to additional organizational units, and embedding AI-powered predictive analytics for cyber threat intelligence. The agency has relied on Cognyte as core counterterrorism infrastructure for over a decade, making this a multi-year platform renewal that sustains recurring revenue rather than a new customer acquisition.

- February 2026: Cognyte secured an approximately USD 5 million follow-on contract from a top NATO-member military organization, extending tactical SIGINT capabilities across additional land, air, and maritime mission environments and bringing total engagement value with that customer to approximately USD 20 million. The expansion leverages AI for real-time data analysis to accelerate operational decision-making in complex multi-domain defense environments.

Global IMSI Catcher Market Report Scope

The International Mobile Subscriber Identity (IMSI) Catcher Market covers surveillance and security devices that imitate mobile base stations to identify, intercept, and track mobile phones within a defined area. These systems are used mainly by law enforcement, intelligence agencies, and security organizations for location tracking, threat detection, and communications monitoring.

The IMSI Catcher Market Is Segmented By Solution Type (Active, Passive, Hybrid And Multi-Mode), Form Factor (Fixed And Vehicular, Briefcase, Handheld, Drone-Mounted), Technology Standard (2G/GSM, 3G/UMTS, 4G/LTE, 5G NR, Multi-Band), End User (Law Enforcement Agencies, Intelligence Agencies, Military and Defense Forces, Private Security Companies, Telecom Operators and Regulators), And Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). Market Forecasts Are Provided In Terms Of Value, USD.

| Active IMSI Catcher |

| Passive IMSI Catcher |

| Hybrid and Multi-Mode IMSI Catcher |

| Fixed and Vehicular |

| Portable Briefcase |

| Handheld |

| Drone-Mounted |

| 2G/GSM |

| 3G/UMTS |

| 4G/LTE |

| 5G NR |

| Multi-Band (2G-5G) |

| Law Enforcement Agencies |

| Intelligence Agencies |

| Military and Defense Forces |

| Private Security Companies |

| Telecom Operators and Regulators |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| Turkey | |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Solution Type | Active IMSI Catcher | |

| Passive IMSI Catcher | ||

| Hybrid and Multi-Mode IMSI Catcher | ||

| By Form Factor | Fixed and Vehicular | |

| Portable Briefcase | ||

| Handheld | ||

| Drone-Mounted | ||

| By Technology Standard | 2G/GSM | |

| 3G/UMTS | ||

| 4G/LTE | ||

| 5G NR | ||

| Multi-Band (2G-5G) | ||

| By End User | Law Enforcement Agencies | |

| Intelligence Agencies | ||

| Military and Defense Forces | ||

| Private Security Companies | ||

| Telecom Operators and Regulators | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| Turkey | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the IMSI catcher market and where is it headed?

The IMSI catcher market stood at USD 182.57 million in 2025, reaches USD 207.68 million in 2026, and is forecast to reach USD 306.47 million by 2031 at an 8.08% CAGR.

Which buyer group accounts for the largest share of demand?

Law enforcement agencies led demand with 51.68% of revenue in 2025, supported by recurring procurement cycles, replacement budgets, and established operating frameworks.

Why do 4G/LTE systems still matter in a 5G environment?

4G/LTE solutions held 46.77% of revenue in 2025 because most 5G deployments still use non-standalone architecture that preserves 4G-linked identifier exposure pathways.

Which form factor is growing the fastest and why?

Drone-mounted platforms are projected to grow at a 11.38% CAGR through 2031 because they offer wider area coverage, better terrain access, and faster collection in difficult field conditions.

Which region is expanding the fastest?

Asia-Pacific is expected to record the fastest regional growth at a 10.98% CAGR through 2031, driven by defense modernization, border security spending, and rising public security investment.

What is the main long-term technical challenge for vendors?

The biggest long-term challenge is 5G standalone architecture, where SUCI and stronger authentication reduce the utility of legacy active interception methods and push vendors toward new approaches.

Page last updated on: