MEMS-Based IMU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.34 Billion |

| Market Size (2031) | USD 2.28 Billion |

| Growth Rate (2026 - 2031) | 11.12% CAGR |

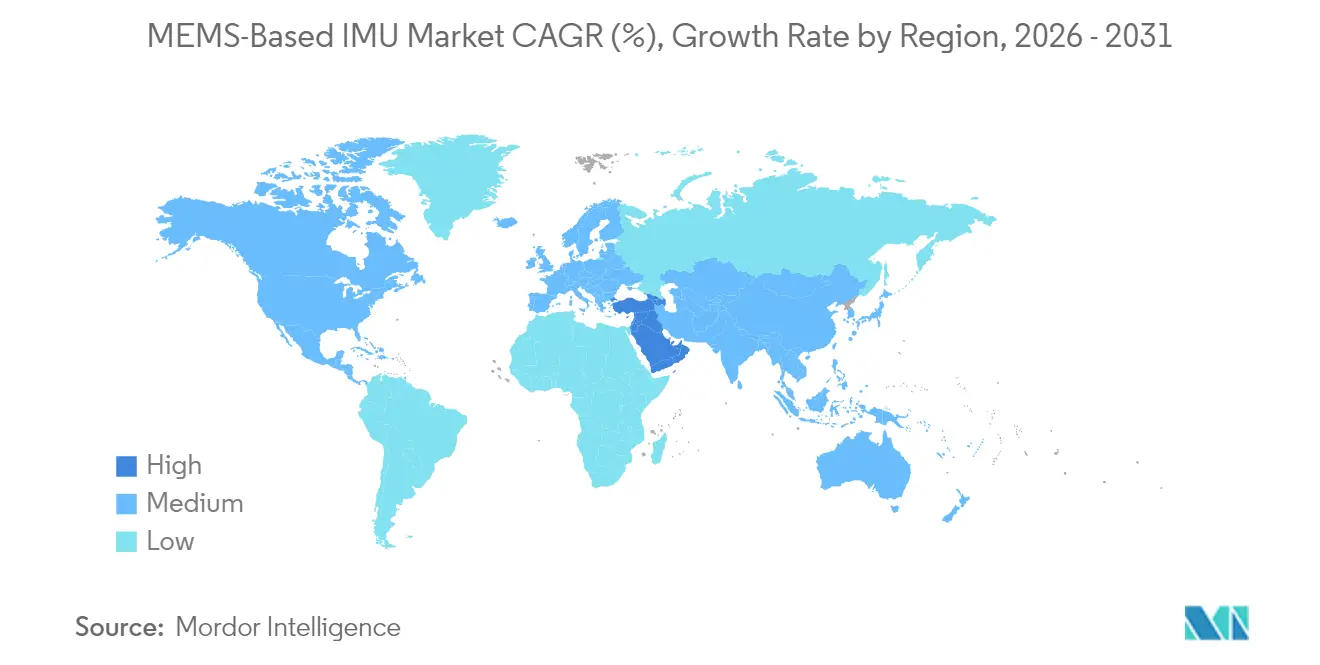

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MEMS-Based IMU Market Analysis by Mordor Intelligence

The MEMS-Based IMU market size is expected to grow from USD 1.21 billion in 2025 to USD 1.34 billion in 2026 and is forecast to reach USD 2.28 billion by 2031 at 11.12% CAGR over 2026-2031. The expansion centers on a rapid migration from fiber-optic and ring-laser gyroscopes to silicon MEMS designs that match tactical-grade performance while lowering bill-of-materials costs. Heightened demand for precise motion tracking in surgical robotics, autonomous vehicles, and augmented-reality devices is widening the customer base, even as smartphone commoditization compresses margins in consumer tiers. Government semiconductor stimulus in the United States, the European Union, and South Korea is reducing wafer lead times and promoting regional sourcing, which in turn enables original equipment manufacturers to accelerate product refresh cycles. Competitive pressure remains pronounced, with four consumer-grade suppliers holding roughly 60% of the shipment volume. However, the tactical and navigation segments remain fragmented, as export-control compliance and bespoke calibration protect incumbents.

Key Report Takeaways

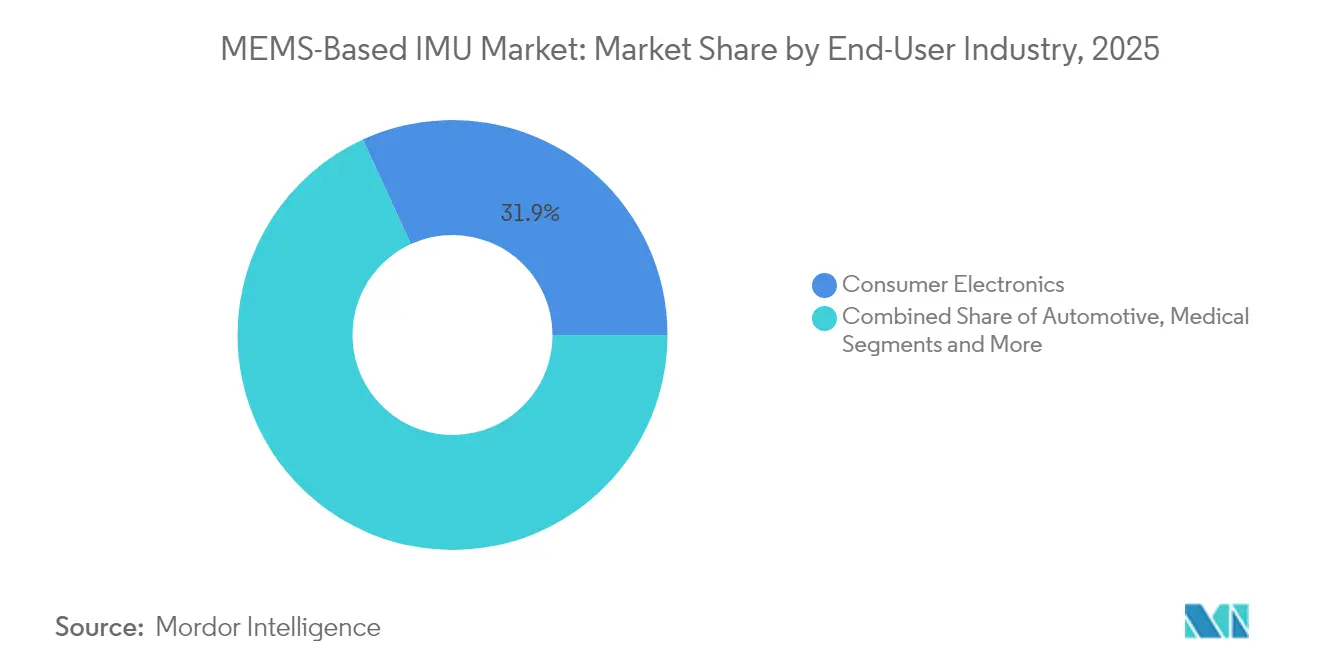

- By end user, consumer electronics retained 31.85% of the MEMS inertial measurement unit market share in 2025, while medical devices are projected to grow at a 12.43% CAGR through 2031.

- By component, integrated 6-axis modules led with 40.55% of the MEMS inertial measurement unit market share in 2025; integrated 9-axis modules are forecast to expand at an 12.74% CAGR to 2031.

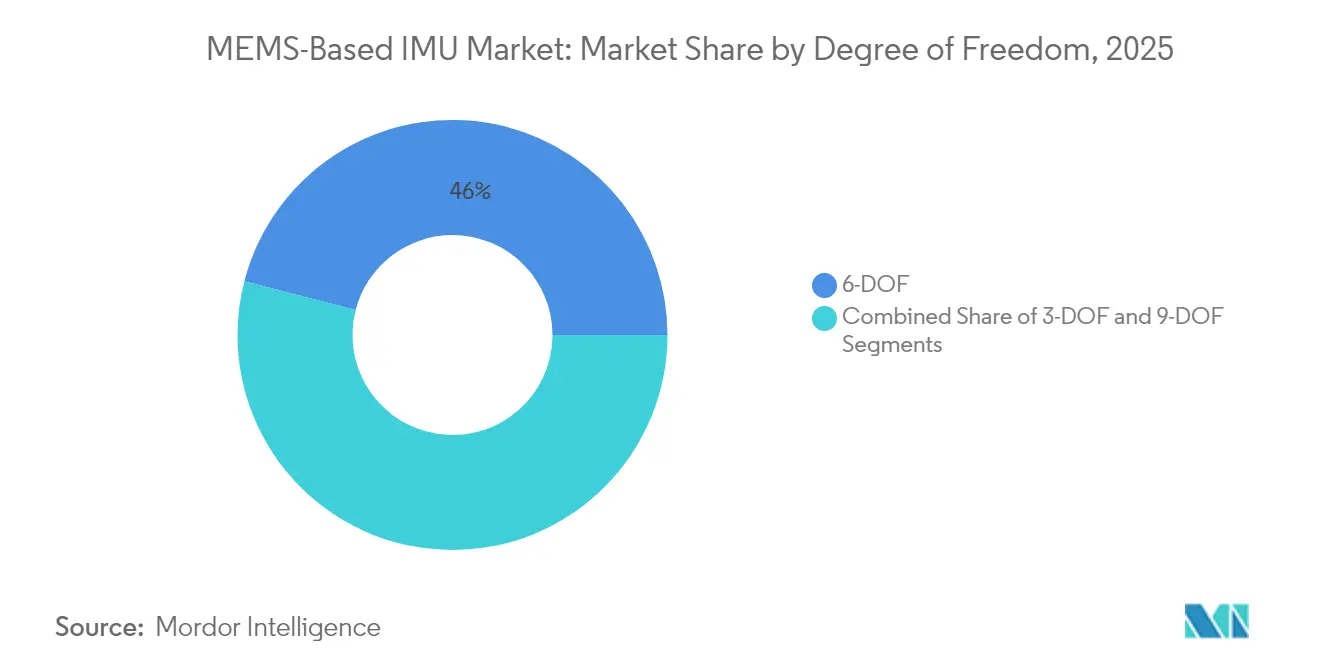

- By degree of freedom, 6-DOF devices accounted for 45.98% of the MEMS inertial measurement unit market share in 2025, whereas 9-DOF architectures are set to climb at a 12.55% CAGR during the forecast horizon.

- By platform grade, consumer-grade systems held 47.72% of the MEMS inertial measurement unit market share in 2025; tactical-grade units are poised for the fastest 13.86% CAGR through 2031.

- By geography, Asia Pacific commanded 44.10% of the MEMS inertial measurement unit market share in 2025, while the Middle East is expected to register a 11.75% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global MEMS-Based IMU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Autonomous Vehicles | +2.1% | Global (North America, China, Germany) | Medium term (2-4 years) |

| Surge in Consumer Wearables with 9-DOF Sensing | +1.8% | Global, led by Asia Pacific and North America | Short term (≤ 2 years) |

| Rising Defense Demand for Navigation-Grade MEMS IMUs | +2.4% | North America, Middle East, Europe, Asia Pacific | Long term (≥ 4 years) |

| Growth of IoT-Enabled Industrial Automation | +1.6% | Europe and North America, expanding to Asia Pacific | Medium term (2-4 years) |

| Miniaturization Trends in Aerospace CubeSats | +1.3% | North America and Europe, emerging in Asia Pacific | Long term (≥ 4 years) |

| Government Funding for Domestic Semiconductor Supply Chains | +2.2% | United States, European Union, South Korea, Japan, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Autonomous Vehicles

Automakers embedding Level 2+ autonomy platforms are installing between six and twelve MEMS IMUs per vehicle to ensure redundancy when satellite navigation degrades in tunnels or dense urban areas. Tesla’s Hardware 4 system brought Bosch SMI230 6-axis units into Model 3 and Model Y production lines in 2024, underscoring how IMUs have shifted from cost targets to safety-critical components.[1]Tesla, “Investor Day 2024 Presentation,” ir.tesla.com Waymo’s Generation 6 driver stack specifies tactical-grade gyroscopes with a resolution of below 5 degrees per hour, ensuring lane keeping even during ten-minute GPS outages. The Society of Automotive Engineers' J3016 Level 4 definition solidifies inertial sensing as a mandatory fallback, while China shipped 4.8 million Level 2+ vehicles in 2024, each carrying at least two IMUs, establishing a demand floor well above nine million units.

Surge in Consumer Wearables with 9-DOF Sensing

Smartwatches are transitioning from 6-axis tracking to 9-axis orientation sensing, allowing users to enjoy turn-by-turn navigation without requiring a phone tether. Samsung’s Galaxy Watch7 uses a 9-DOF suite to recognize wrist gestures that replace touchscreens during exercise. OPPO’s Watch X brought TDK InvenSense ICM-20948 into mainstream sports wearables for continuous compass heading. The architecture adds USD 0.80–1.20 to the bill of materials yet supports premium retail pricing, as illustrated by the USD 799 Apple Watch Ultra, which couples dual-frequency GPS with 9-axis inertial sensing. FDA-cleared devices, such as the Withings ScanWatch 2, pair motion sensors with photoplethysmography to filter noise from heart-rate signals.

Rising Defense Demand for Navigation-Grade MEMS IMUs

Defense ministries are replacing ring-laser gyroscopes with MEMS designs to reduce size, weight, and power without losing accuracy. DARPA funded chip-scale atomic clock pairings with sub-0.1-degree-per-hour IMUs for 72-hour GPS-denied missions. Safran Federal Systems will supply navigation-grade MEMS units for the U.S. Navy’s Next-Generation Jammer under a USD 47 million award that specifies an angular random walk of below 0.05 degrees per square root hour. Israel’s Rafael cut missile guidance weight by 30% using Northrop Grumman LITEF IMUs while maintaining meter-scale accuracy. Export-control rules tighten around devices with a temperature change of less than 0.01 degrees per hour, prolonging procurement yet elevating margins for compliant suppliers.

Growth of IoT-Enabled Industrial Automation

Factories switching from time-based maintenance to condition-based servicing integrate IMUs in robotic joints and rotating assets. STMicroelectronics’ ISM330BX withstands −40 °C to +105 °C and detects bearing wear three weeks before failure. TDK’s SmartIndustrial firmware classifies a dozen vibration signatures on-chip and dispatches alerts over industrial Ethernet, cutting unplanned downtime costs that averaged USD 260,000 per hour in automotive assembly during 2024. Beckhoff Automation embeds Murata inclinometers for crane boom angle measurement at 0.1-degree resolution to meet European Machinery Directive safety rules. The payback for installing IMU-enabled monitoring dropped from 24 months to 14 months in 2024.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Packaging-Induced Drift and Calibration Costs | -1.4% | Global, acute in aerospace and medical | Medium term (2-4 years) |

| Export Controls on High-Performance IMUs | -1.1% | North America and Europe producers; Middle East and Asia Pacific buyers | Long term (≥ 4 years) |

| Supply Shortages of Specialty MEMS Wafers | -0.9% | Global, Asia Pacific foundry networks | Short term (≤ 2 years) |

| Algorithmic Complexity in Multi-Sensor Fusion | -0.7% | Global, notably automotive and consumer sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Packaging-Induced Drift and Calibration Costs

Thermal-mismatch stress between silicon dies and ceramic packages shifts accelerometer bias by 10–50 milligravity across the temperature range of −40 °C to +85 °C, necessitating multi-point calibration that adds USD 2–8 per unit. The IEEE Sensors Journal quantified 15 MPa stress due to differing thermal-expansion coefficients, resulting in kilometer-scale navigation drift per operating hour.[2]IEEE Sensors Journal, “Packaging-Induced Stress in MEMS Devices,” ieeexplore.ieee.org Analog Devices countered with eight on-chip temperature sensors in the ADIS16577, although the die area increased by 18%. Automotive ISO 26262 ASIL-D qualification now requires 1,000 thermal cycles, extending test timelines to 14 months and increasing entry barriers. Calibration stands cost USD 400,000 each and require NIST recalibration every 90 days, limiting participation to well-capitalized vendors.

Export Controls on High-Performance IMUs

Devices below 0.01 degrees per hour fall under ITAR Category XII, imposing 6-12-month license delays and banning shipments to 28 nations. The U.S. Bureau of Industry and Security expanded EAR Category 7A103 in 2024 to include faster accelerometers, compelling suppliers to segregate production by performance tier. Honeywell spent USD 23 million on compliance in 2024, or 4.2% of the aerospace segment's income. The Wassenaar Arrangement added MEMS gyroscopes to its Munitions List, causing average eight-month contract delays for Middle Eastern buyers. Northrop Grumman indicated that 18% of its IMU backlog faced licensing uncertainty, complicating capacity planning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Medical Devices Outpace Consumer Electronics

Medical devices are expected to outpace all other sectors, with a projected 12.43% CAGR growth rate through 2031. This surge is largely driven by an increasing demand for pinpoint accuracy, particularly in surgical robotics and gait analysis monitors. Meanwhile, consumer electronics, which accounted for 31.85% of 2025's revenue, saw robust sales driven by smartphones and smartwatches. However, this segment is experiencing a slowdown as profit margins on handsets tighten.

In 2024, Stryker’s Mako SmartRobotics, a frontrunner in robotic surgery, secured a commanding 38% share of the U.S. knee-replacement market. This was achieved by incorporating 6-axis IMUs into their handheld cutters, enabling a precision of 0.5 degrees. Medtronic’s Hugo system, on the other hand, boasts tactical-grade gyros that counteract respiratory motion, leading to a notable 22% reduction in tissue trauma during laparoscopic procedures. The automotive sector has integrated 2–4 IMUs in each Level 2 vehicle, enhancing electronic stability control. However, due to supplier consolidation, growth is restrained to a 10.55% CAGR. In the aerospace and defense realm, MEMS are now the go-to replacements for ring-laser gyroscopes, especially in drones and compact missiles. Meanwhile, industrial machinery is leveraging IMUs for predictive maintenance, resulting in shortened payback cycles.

By Component: 9-Axis Modules Gain on Sensor-Fusion Demand

Integrated 6-axis modules dominated the revenue landscape, claiming a substantial 40.55% share in 2025. Meanwhile, integrated 9-axis devices are on a rapid ascent, boasting a notable 12.74% CAGR. This surge is largely driven by the increasing demands of augmented-reality headsets and drones, which now seek heading information sans the need for external magnetometers.

Bosch’s BMI323, measuring a compact 2.5 mm × 3.0 mm, operates at a mere 1.8 mA during continuous use, catering to spatial audio needs in earbuds. On the other hand, STMicroelectronics’ LSM6DSV16X stands out by combining a 9-axis sensor with an on-chip machine-learning core, capable of executing 16 decision trees. This innovation translates to a significant 40% reduction in system power. While stand-alone accelerometers are indispensable for airbag crash detection, where 100 G ranges are paramount, discrete gyros are essential for optical image stabilization. Notably, while magnetometers are transitioning into combo modules, they still find a niche in industrial compasses that demand precision of less than 1-degree heading.

By Degree of Freedom: 9-DOF Architectures Accelerate

6-DOF designs accounted for 45.98% of the revenue in 2025. Meanwhile, 9-DOF layouts surged, boasting a 12.55% CAGR. This growth is driven by the demands of AR and indoor navigation, which seek precise orientation without relying on satellite assistance.

TDK InvenSense's ICM-20948, a key player in the market, is featured in flagship devices like the Samsung Galaxy Watch7 and OPPO Watch X. This integration enables fitness tracking without relying on phone GPS. The elevated bill-of-materials cost justifies the premium pricing of these watches, evident in the USD 799 Apple Watch Ultra. While three-axis accelerometers dominate industrial vibration applications, they too are witnessing significant growth. This is largely attributed to designers' preference for integrated modules, which offer significant savings in board area.

By Platform Grade: Tactical Tier Gains Defense Share

Consumer-grade units commanded a substantial 47.72% share of the revenue in 2025, driven by the sale of over 1.5 billion smartphones and wearables. Meanwhile, tactical-grade modules surged, boasting a robust 13.86% CAGR, as military forces increasingly turned to MEMS, moving away from traditional ring-laser gyroscopes.

Analog Devices made waves in the market by pricing its ADIS16577 at a competitive USD 450. This move not only undercut fiber-optic competitors by a significant 40% but also ensured the module met the crucial 2-degree-per-hour stability standard, a key requirement for drone autopilots. Industrial-grade sensors, capable of operating in temperatures ranging from −40 °C to +105 °C, are utilized in factory robots and rail inspection systems. This versatility justifies the USD 15-40 premium they command. However, navigation-grade units face restrictions, as they are primarily utilized in commercial aviation and strategic platforms. This limitation stems from stringent export regulations and the units' need to meet the exacting standard of sub-0.01-degree-per-hour bias stability.

Geography Analysis

Asia Pacific led with 44.10% revenue in 2025, anchored by China’s USD 143 billion Integrated Circuit Fund and Japan’s dominance in volume MEMS foundry capacity. China’s subsidies to SMIC and Huahong trim reliance on foreign fabs, while Japanese leaders TDK and Murata captured 35% of consumer shipments through vertically integrated chains that compress lead times to eight weeks. South Korea’s KRW 622 trillion (USD 450 billion) semiconductor roadmap lifts Samsung’s System LSI MEMS capacity by 40% by 2027. Taiwan’s TSMC furnishes 8-inch foundry slots for Bosch, STMicroelectronics, and Analog Devices, though geopolitical risk is driving customers to diversify.

North America and Europe together accounted for nearly 37.60% of revenue in 2025, driven by demand from the aerospace, defense, and high-end automotive sectors. The United States CHIPS and Science Act dedicates USD 39 billion to fabrication incentives, with GlobalFoundries expanding its Malta, New York, output by 25% for automotive-grade IMUs. Germany offers EUR 10 billion for semiconductor facilities, enabling Bosch to enlarge Dresden MEMS lines by 30%. France’s Crolles advanced-packaging joint venture cuts module footprints 40% for wearable and medical clients. The United Kingdom’s Compound Semiconductor Applications Catapult channels GBP 150 million (USD 190 million) into gallium-nitride MEMS gyros for turbine engines.

The Middle East is projected to record the fastest 11.75% CAGR through 2031, as defense modernization and smart-city programs increasingly emphasize local content. Saudi Arabia’s SAMI is building a joint venture with Thales to achieve 60% indigenous tactical-grade output by 2028. The United Arab Emirates’ EDGE Group purchased 40% of Sensonor to secure gyro intellectual property for homegrown drones. Israel’s Rafael integrated LITEF IMUs into Spike missiles to save weight, while Turkey’s ASELSAN developed a navigation-grade MEMS unit for its KAAN fighter but faces nine-month export-license delays. Africa and South America each hold a share of under 5% because fabrication capacity is limited, and modules are imported with extended lead times.

Competitive Landscape

The MEMS-based inertial measurement unit market is experiencing moderate concentration among key players. Bosch Sensortec, STMicroelectronics, TDK InvenSense, and Murata have established a stronghold in consumer shipments. Their co-located fabs and assembly lines not only facilitate swift eight-week delivery windows but also significantly reduce customer inventory costs.

Meanwhile, in the aerospace and defense sectors, Honeywell and Northrop Grumman leverage their multi-decade platform qualifications. A testament to their dominance: the F-35 mission computer has a specified part number, Honeywell's HG1120, locked in until the next airframe refresh. Further shaking up the landscape, Analog Devices made waves with its USD 450 ADIS16577 launch, disrupting tactical pricing and compelling rivals to hasten their refreshes and extend warranties, all while squeezing their operating margins by as much as 300 basis points.[3]Analog Devices, “Investor Relations,” analog.com

While established players dominate, emerging opportunities abound, particularly in medical robotics and indoor positioning. Here, complexities in sensor fusion and regulatory pathways pose challenges for consumer incumbents. Movella’s Xsens unit has carved out a notable 28% share of the motion-capture revenue. A combination of 9-axis IMUs and proprietary fusion algorithms that maintain a 1-degree heading accuracy, even sans magnetometer calibration. VectorNav has made its mark in autonomous underwater vehicles, thanks to its innovative 6,000-meter pressure housings. Meanwhile, challenger brands like ACEINNA and SBG Systems are making waves by leveraging open-source libraries, slashing integration costs by half and drawing in robotics start-ups. Notably, patent filings for temperature-compensated packaging surged by 34% in 2024, with industry giants like Analog Devices, STMicroelectronics, and Bosch leading the charge. This uptick signals a heightened race to counter drift issues without resorting to costly calibrations.

MEMS-Based IMU Industry Leaders

Robert Bosch GmbH (Bosch Sensortec GmbH)

TDK Corporation

Analog Devices Inc.

STMicroelectronics N.V.

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Analog Devices unveiled the ADIS16545 and ADIS16547, two cutting-edge six degrees of freedom (6 DoF) inertial measurement units (IMUs). These units are engineered to provide tactical-grade performance, stepping in for applications that have conventionally relied on fiber optic gyros.

- September 2025: Safran Electronics & Defense has unveiled the latest ICONYX HP, setting a new standard as an advanced tactical Inertial Measurement Unit (IMU). This cutting-edge device promises unparalleled performance, resilience, and adaptability, catering to the most stringent guidance and control demands.

- June 2025: Honeywell has bolstered its navigation offerings by introducing the HG3900 Inertial Measurement Unit (IMU). This compact, lightweight, and energy-efficient device boasts tactical-grade capabilities, delivering accuracy and reliability on par with those of larger, near navigation-grade IMUs.

- April 2025: Thales has unveiled a groundbreaking Inertial Measurement Unit (IMU) in its TopAxyz product line, leveraging MEMS technology to revolutionize navigation solutions. Thales has unveiled a new unit, engineered for large-scale production, delivering performance on par with its top-tier TopAxyz IMU, but in a more compact, lightweight, and energy-efficient design.

Global MEMS-Based IMU Market Report Scope

MEMS Inertial Measurement Units (IMUs), compact and cost-effective, harness Micro-Electro-Mechanical Systems (MEMS) technology. By integrating accelerometers for linear motion and gyroscopes for rotational velocity, often alongside a magnetometer for directional sensing, these devices monitor motion and orientation. This capability facilitates navigation, stabilization, and motion sensing across a diverse range of applications, from smartphones to rockets.

The Global MEMS Based Inertial Measurement Unit Market Report is Segmented by End-User Industry (Consumer Electronics, Automotive, Medical, Aerospace and Defense, Industrial Machinery, and Other End-User Industries), Component (Accelerometers, Gyroscopes, Magnetometers, Integrated 6-Axis Modules, and Integrated 9-Axis Modules), Degree of Freedom (3-DOF, 6-DOF, and 9-DOF), Platform Grade (Consumer Grade, Industrial Grade, Tactical Grade, and Navigation Grade), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Consumer Electronics |

| Automotive |

| Medical |

| Aerospace and Defense |

| Industrial Machinery |

| Other End-User Industries |

| Accelerometers |

| Gyroscopes |

| Magnetometers |

| Integrated 6-Axis Modules |

| Integrated 9-Axis Modules |

| 3-DOF |

| 6-DOF |

| 9-DOF |

| Consumer Grade |

| Industrial Grade |

| Tactical Grade |

| Navigation Grade |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By End-User Industry | Consumer Electronics | ||

| Automotive | |||

| Medical | |||

| Aerospace and Defense | |||

| Industrial Machinery | |||

| Other End-User Industries | |||

| By Component | Accelerometers | ||

| Gyroscopes | |||

| Magnetometers | |||

| Integrated 6-Axis Modules | |||

| Integrated 9-Axis Modules | |||

| By Degree of Freedom | 3-DOF | ||

| 6-DOF | |||

| 9-DOF | |||

| By Platform Grade | Consumer Grade | ||

| Industrial Grade | |||

| Tactical Grade | |||

| Navigation Grade | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the MEMS based inertial measurement unit market in 2026?

The market size stands at USD 1.34 billion in 2026 and is forecast to reach USD 2.28 billion by 2031.

Which segment is growing fastest through 2031?

Medical devices lead with a 12.43% CAGR, reflecting demand for precise motion tracking in surgical robots and patient monitors.

Which region contributes the most revenue today?

Asia Pacific delivers 44.10% of global revenue, backed by strong consumer-electronics supply chains and national semiconductor programs.

Why are 9-axis modules gaining popularity?

They combine accelerometer, gyroscope, and magnetometer in one package, enabling absolute heading without external sensors and supporting AR, drones, and smartwatches.

What is the primary restraint on high-end IMU growth?

Export controls on devices with bias stability below 0.01 degrees per hour extend sales cycles by up to a year and limit the customer pool.

Who are the key incumbents in defense applications?

Honeywell and Northrop Grumman maintain long-term platform positions, while Analog Devices is challenging pricing norms with its ADIS16577 tactical-grade unit.

Page last updated on: