AIOps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

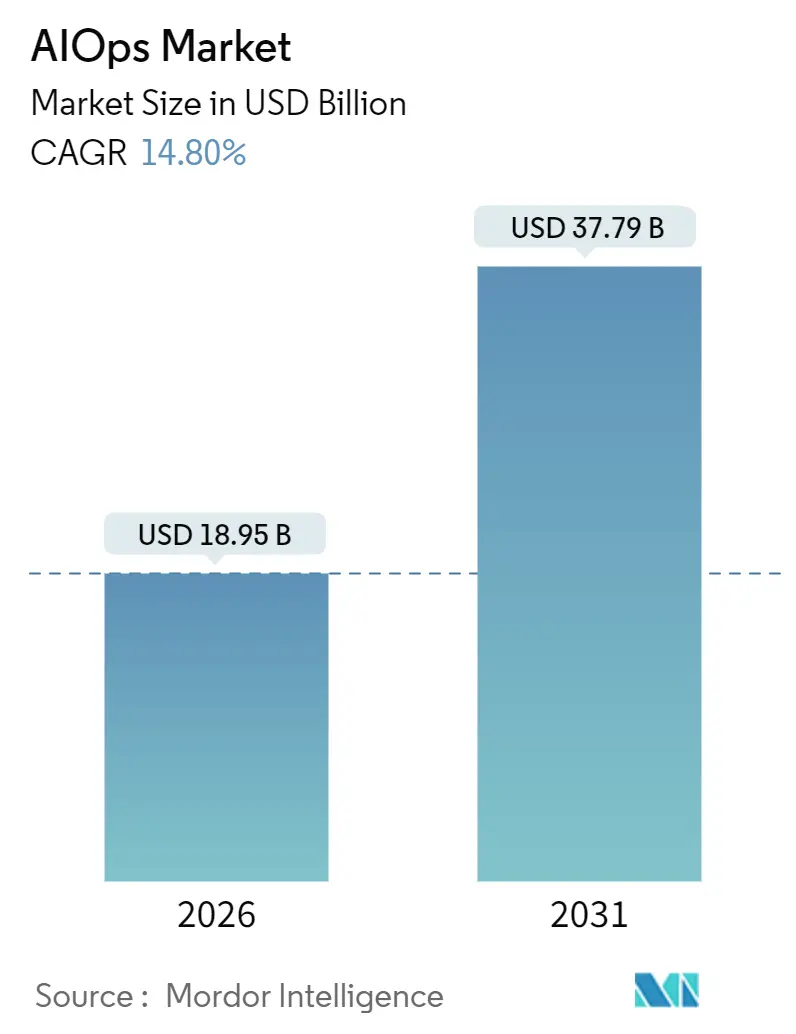

| Market Size (2026) | USD 18.95 Billion |

| Market Size (2031) | USD 37.79 Billion |

| Growth Rate (2026 - 2031) | 14.80% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AIOps Market Analysis by Mordor Intelligence

The AIOps market size stands at USD 18.95 billion in 2026 and is projected to reach USD 37.79 billion by 2031, reflecting a 14.8% CAGR. Rapid substitution of manual incident triage with machine-learning correlation engines is shortening mean time to resolution by as much as 60%, particularly across hybrid infrastructures where alert volumes have multiplied. Platform vendors currently dominate spending, yet rising integration complexity is steering future growth toward services that help customers operationalize algorithms. Cloud-first pricing models are lowering entry barriers for small and medium enterprises, while regulated industries continue to run mission-critical workloads on-premise to satisfy data-sovereignty mandates. Consolidation among platform providers and the arrival of generative AI copilots are reshaping competitive dynamics in the AIOps market.

Key Report Takeaways

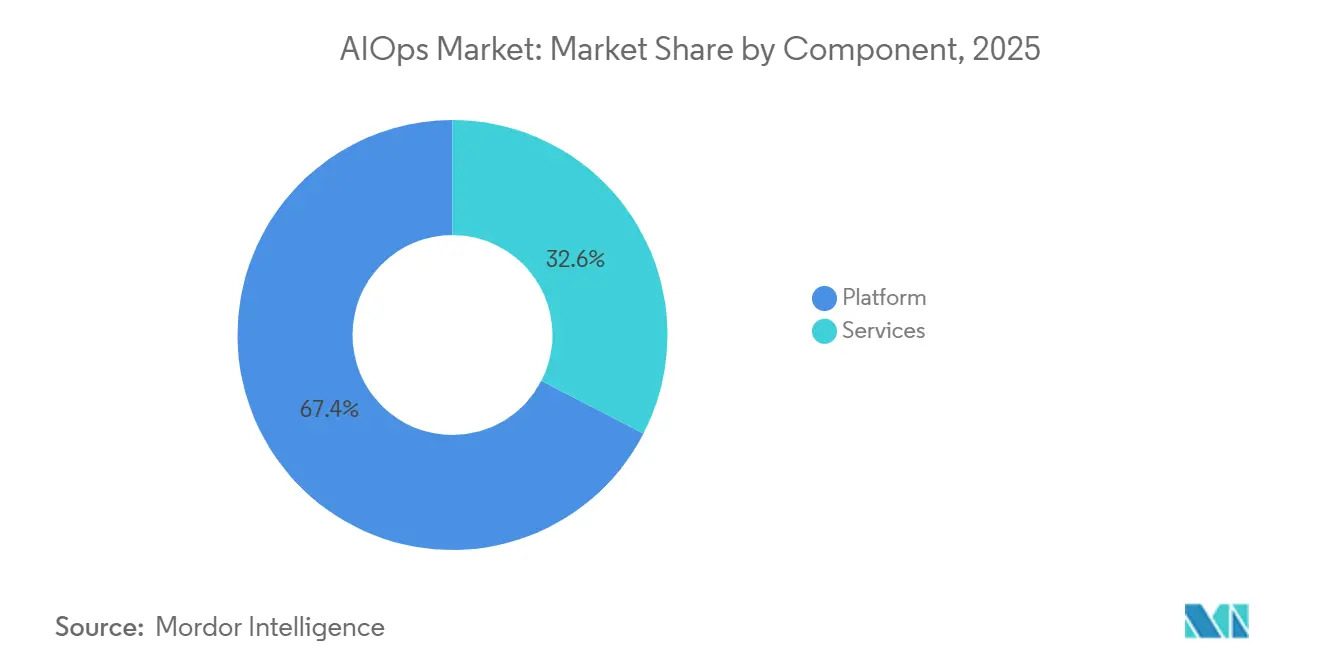

- By component, platform subscriptions led with 67.42% revenue in 2025, while services are forecast to deliver the fastest 16.04% CAGR through 2031.

- By deployment mode, on-premise installations held 56.66% share of spending in 2025, whereas cloud implementations are set to expand at a 15.66% CAGR to 2031.

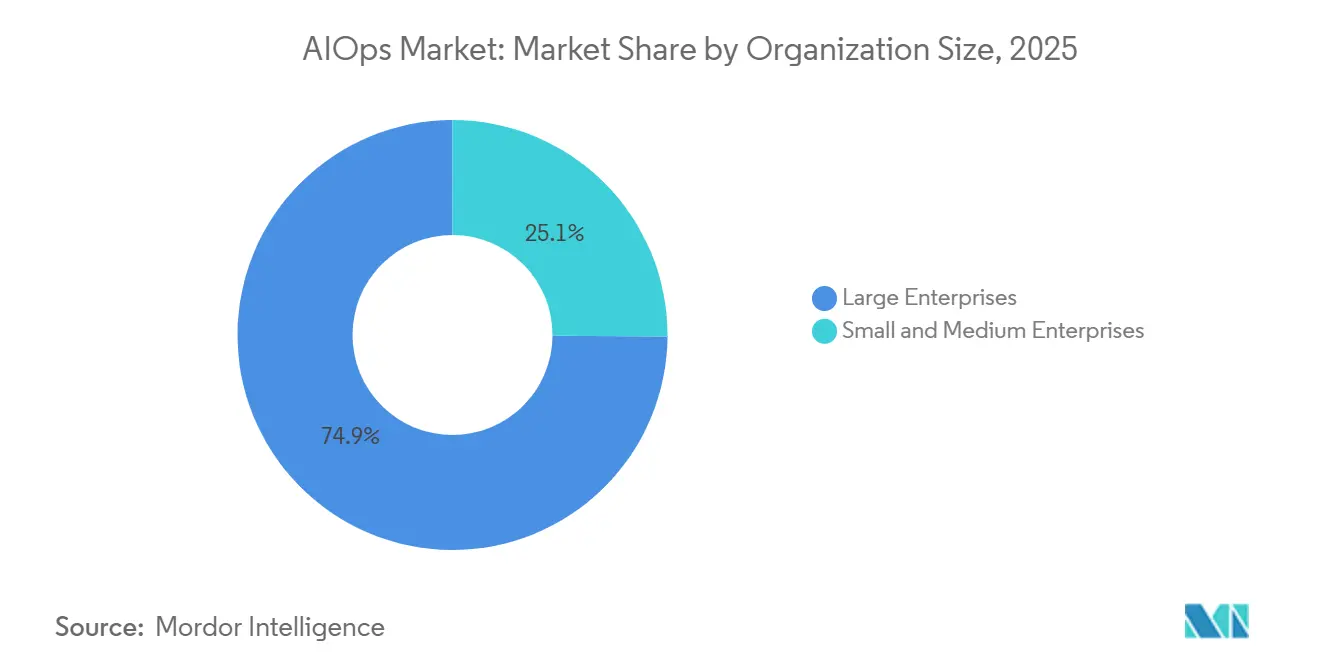

- By organization size, large enterprises commanded 74.89% purchasing power in 2025, yet small and medium enterprises represent the fastest-growing cohort at 15.44% CAGR.

- By end-user industry, IT and telecom captured 32.28% of 2025 demand, while healthcare is projected to advance at a 16.66% CAGR to 2031.

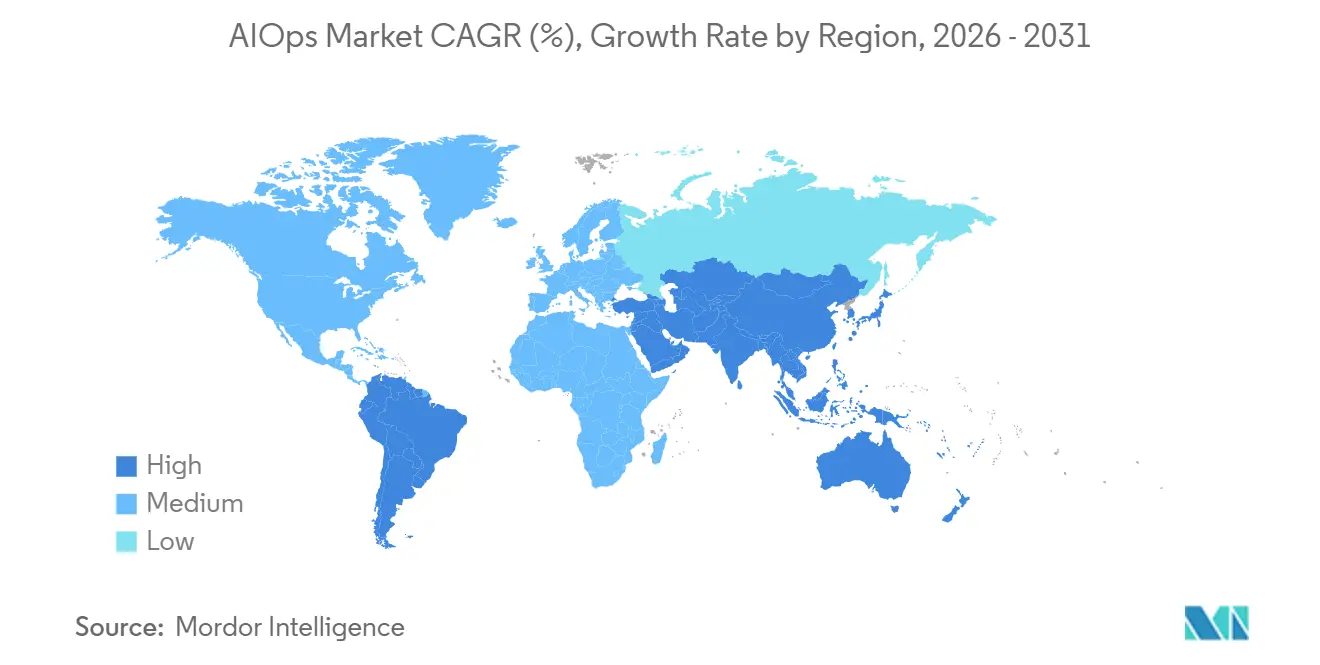

- By geography, North America accounted for 42.54% of 2025 revenue, but Asia Pacific is on track for the quickest 16.22% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AIOps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Driven Observability Demand Surge | +3.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Shift to Hybrid and Multi-Cloud Architectures | +2.8% | Global, particularly North America, Europe, and Asia Pacific | Long term (≥ 4 years) |

| Need for Faster MTTR and SRE Adoption | +2.4% | Global, led by IT and Telecom, BFSI sectors | Short term (≤ 2 years) |

| Gen-AI Copilots for Ops Automation | +2.1% | North America and Europe early adoption, Asia Pacific following | Medium term (2-4 years) |

| FPGA and DPU Acceleration at the Edge | +1.3% | Manufacturing hubs in Asia Pacific, industrial sectors in Europe and North America | Long term (≥ 4 years) |

| Rise of ESG-Linked "Green Ops" Compliance | +0.9% | Europe primary, North America secondary, expanding to Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Driven Observability Demand Surge

Enterprises moved from 42% to 54% adoption of AI-powered monitoring between 2024 and 2025 as microservices generated tenfold more telemetry than monolithic stacks. Traditional rule-based alerts could not cope, producing storms that desensitized on-call teams. Machine-learning baselines now filter infrastructure noise and surface user-impacting incidents, shrinking triage queues. Datadog’s LLM Observability, introduced in 2025, tracks token consumption and latency in generative AI workloads, a blind spot as customer-facing applications embed large language models. Finance leaders have doubled monitoring budgets because a single hour of downtime costs USD 2 million in lost transactions and compliance penalties. The magnitude of these losses explains why the AIOps market continues to accelerate.

Shift to Hybrid and Multi-Cloud Architectures

Hybrid and multi-cloud workloads climbed to 87% in 2025, up from 76% in 2023, as firms diversify suppliers and comply with data-residency rules.[1]Flexera, “2025 State of the Cloud Report,” flexera.com Every hyperscaler exposes a different telemetry model - AWS CloudWatch, Azure Monitor and Google Cloud Operations - forcing teams to normalize data before correlation. OpenTelemetry adoption reached 64% of cloud-native projects, but legacy systems still emit syslog and SNMP, prompting gateway translation. Cisco’s post-acquisition fusion of AppDynamics and Splunk created a single pane for on-premise and cloud visibility.[2]Cisco, “Cisco Observability Suite,” cisco.com Sovereign-cloud regulations in the European Union and India require region-locked AIOps instances, fragmenting oversight while driving demand for federated analytics.

Need for Faster MTTR and SRE Adoption

Site reliability engineering practices were observed at 48% of enterprises in 2025, compared with 34% in 2023, as organizations formalized error budgets and service-level objectives. Dynatrace customers reduced mean time to resolution by 60% through distributed-trace analytics that map anomalies to user sessions. PagerDuty’s generative AI escalates incidents using historical patterns and responder availability, eliminating lengthy manual routing. Minutes of downtime during Black Friday can erase an entire day’s margin. The European Union’s Digital Operational Resilience Act obliges banks to restore critical services within two hours, converting MTTR metrics into compliance mandates.

Gen-AI Copilots for Ops Automation

Generative AI copilots entered production at 38% of enterprises in 2025, automating runbook execution and incident summaries. Azure Copilot translates natural-language prompts into Kusto queries, lowering the knowledge bar for junior engineers. Splunk’s AI Assistant drafts search queries and correlation rules by mining past tickets. Despite enthusiasm, 68% of site reliability engineers say the scripts still need review because model training lacks context for proprietary middleware. Cisco’s conversational assistant now spans AppDynamics and ThousandEyes, blending application and network intelligence. Early adopters see productivity gains, yet unchecked copilots risk propagating errors at machine speed.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tool Sprawl and ROI Uncertainty | -1.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Shortage of AIOps-Savvy Talent | -1.5% | Global, particularly acute in Asia Pacific and emerging markets | Medium term (2-4 years) |

| Data-Sovereignty and AI-Governance Hurdles | -1.1% | Europe, Asia Pacific, Middle East with strict data localization | Long term (≥ 4 years) |

| Vendor Black-Box Algorithms and Lock-In Risk | -0.8% | Global, especially impacting large enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tool Sprawl and ROI Uncertainty

Most enterprises still juggle multiple monitoring tools, fragmenting telemetry and inflating licensing overhead. Consolidation efforts intensified in 2025, yet integration complexity can postpone payback beyond eighteen months. Only a small subset of organizations achieved triple-digit return on investment inside the first year, while a quarter reported negative returns due to underused features. Overlaps among application, log and network monitoring create redundant alerts that drown operators in noise. Small and medium enterprises face sharper friction because many AIOps platforms assume 24/7 site reliability teams that these firms do not staff. Managed service providers help close gaps but often add margin, diluting ROI.

Shortage of AIOps-Savvy Talent

The cybersecurity and IT operations workforce gap reached 3.5 million positions in 2025.[3]ISC2, “2025 Cybersecurity Workforce Study,” isc2.org Only 12% of practitioners hold credentials in machine-learning model governance, and universities have yet to scale relevant curricula. Hybrid skill sets combining infrastructure fluency, statistical modeling and software development remain rare. Regional shortages are most pronounced in Asia Pacific, where digital transformation outpaces talent pipelines. Enterprises respond by hiring consultants at premium rates or by sending staff to vendor academies such as Dynatrace University, yet 58% of firms say new certificate holders still require six months of mentoring before they can manage platforms independently.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Ground as Integration Demands Deepen

Platform subscriptions captured 67.42% of 2025 spending, the largest slice of the AIOps market share for that year. The services segment, however, is projected to grow at a 16.04% CAGR to 2031 as organizations rely on external expertise to connect heterogeneous data feeds, tune baselines and automate remediation. This drift toward services underscores how black-box algorithms need context-specific calibration before they deliver value.

Professional services firms are embedding site reliability engineers inside client teams to accelerate adoption, while managed service providers offer follow-the-sun incident response priced on retainer. Vendor certification programs have become a parallel revenue stream and a way to expand the talent pool. Platform development is turning toward generative AI interfaces and edge inference, with DPUs and FPGAs driving sub-millisecond anomaly detection in industrial IoT environments. Environmental, social and governance metrics are also being woven into dashboards so that operational and sustainability priorities appear side by side.

By Deployment Mode: Cloud Momentum Builds Despite On-Premise Stronghold

On-premise implementations represented 56.66% of installed environments in 2025 as banks, hospitals and government agencies guarded sensitive telemetry within their own data centers. Cloud deployments are forecast to expand at a 15.66% CAGR through 2031 as hyperscalers embed native AIOps and offer sovereign regions that satisfy residency laws. The gradual shift is notable because cloud subscriptions eliminate capital outlays and scale elastically with workload growth, aligning cost with usage.

Hybrid architectures are emerging as a pragmatic compromise, retaining sensitive logs on-premise while allowing less-restricted data to flow into cloud-based analytics. Cloud-native vendors such as Datadog and New Relic enjoy outsized share among digital-first companies; Datadog’s annual recurring revenue surpassed USD 2 billion in 2025. The European Union’s GDPR fines and new sovereign clouds demonstrate how regulatory frameworks directly influence deployment choices. Over a five-year horizon, operating self-hosted stacks often costs considerably more than subscription services due to patching, scaling and hardware refresh cycles.

By Organization Size: SMEs Accelerate on SaaS Accessibility

Large enterprises held 74.89% of the AIOps market in 2025, reflecting sprawling hybrid estates that generate terabytes of telemetry daily. Small and medium enterprises are expected to post a 15.44% CAGR to 2031 as consumption-based pricing and pre-configured dashboards lower adoption friction. Entry-level plans that monitor a handful of hosts for free and expand incrementally are bringing observability within reach of budget-conscious firms.

Large organizations are meanwhile trimming toolkits from six platforms to nearer four to reduce overlap and license duplication. Consolidation favors full-stack suites that bundle application, log and infrastructure insights under a single agreement. Cisco’s 2024 absorption of Splunk exemplifies this trajectory and signals a future where platform ecosystems carry more weight than point solution features. SMEs still prize simplicity over depth, opting for quick-start templates and managed services rather than heavy customization.

By End-User Industry: Healthcare Emerges as the Fastest Adopter

IT and telecom generated 32.28% of revenue in 2025 and remain the largest vertical because operators manage both their own infrastructure and that of customers. Healthcare is anticipated to grow the fastest at 16.66% CAGR to 2031, propelled by electronic health record complexity, strict audit requirements and the patient-safety implications of downtime. A single hour of EHR unavailability can delay treatments and cost hospitals hundreds of thousands of dollars.

Financial services continue to allocate premium budgets due to the existential cost of outages and the arrival of the Digital Operational Resilience Act. Retail, manufacturing and media each have workload patterns - flash sales, predictive maintenance, live streaming - that benefit from predictive analytics and automated scaling. Government agencies across several continents are embedding AIOps into modernization projects to ensure citizen portals remain available during tax and benefits windows. Collectively, these verticals demonstrate how sector-specific regulations and service-level expectations drive nuanced adoption curves within the larger AIOps market.

Geography Analysis

North America commanded 42.54% of 2025 revenue, driven by mature IT operations capabilities and early-stage adoption of generative AI copilots. Financial institutions in the United States experience median outage costs of USD 2 million per hour, a figure that reinforces investment urgency. Vendor consolidation is most visible here, where large enterprises are standardizing on full-stack suites to satisfy audit and resilience mandates.

Asia Pacific is forecast to register the fastest 16.22% CAGR to 2031 as public-sector digitization programs and data-localization laws compel multinational firms to deploy region-specific observability stacks. India’s Digital India initiative, China’s 14th Five-Year Plan and Japan’s Society 5.0 blueprint collectively pour billions into cloud infrastructure and IoT, generating new telemetry that requires automated correlation. Regional vendors such as Alibaba Cloud and Tencent Cloud embed AIOps in their services to cut reliance on Western software.

Europe remains a significant contributor, though growth is moderated by stringent privacy and AI governance regimes. The EU AI Act classifies AIOps applied to critical infrastructure as high risk, obliging transparency and human oversight. GDPR enforcement continues to impose hefty penalties when telemetry traverses borders without consent. Latin America, the Middle East and Africa are earlier in their adoption curve but are progressing through government modernization and telecom expansion projects that plant seeds for future uptake.

Regulatory Landscape

Regulation affecting AIOps centers on AI governance, privacy, and operational resilience, which in turn shapes model design and telemetry deployments. In the European Union, the EU AI Act (Regulation (EU) 2024/1689) sets mandatory obligations for high-risk AI systems, including risk management, data governance, technical documentation, record-keeping, and human oversight, with an August 2026 enforcement milestone for high-risk obligations. GDPR enforcement continues to influence where operational telemetry can be processed, reinforcing on-premise or region-locked deployments in regulated industries.

In the United States, governance is more fragmented, with multiple state AI laws taking effect in January 2026, while federal direction leans on voluntary and policy frameworks. NIST AI Risk Management Framework (AI RMF 1.0) remains a widely used baseline for operationalizing AI risk controls, including documentation and incident-response testing. In March 2026, the White House released the National Policy Framework for Artificial Intelligence: Legislative Recommendations, which calls for regulatory sandboxes and a more unified federal approach to reduce conflicting state requirements.

Value Chain Analysis

The AIOps value chain starts with telemetry generation and ingestion across applications, infrastructure, networks, and cloud control planes, then moves through normalization (logs, metrics, traces, events, topology), correlation and anomaly detection, and automated workflows integrated into ITSM, SOAR, and orchestration. Upstream inputs include OpenTelemetry standards and data platforms capable of handling high-volume machine data, with AI/ML capabilities that convert operational information into incident insights and remediation actions. Downstream delivery includes platform subscriptions plus professional and managed services that implement connectors, tune baselines, and operationalize runbooks, reflecting the market shift toward services when customers face tool sprawl and heterogeneous environments.

Ecosystem partnerships and integrated suites increasingly determine time-to-value, especially for hybrid and multi-cloud operations and telecom network operations. Examples of value chain coordination include Cisco and Splunk positioning a combined observability and analytics stack, and the wider partner-led integrations seen in Google Cloud and Amdocs for AI-driven 5G operations, and Juniper Networks with ServiceNow for automation of managed services. As a concrete 2026 proof point, TPG Telecoms announced in March 2026 that it will transition its Service Operations Centre to an AIOps-driven model using Cisco and Splunk, illustrating how operators combine platform capabilities, integration expertise, and automation tooling. Bottlenecks remain data quality, interoperability across multi-vendor estates, and governance requirements that force ModelOps-style controls and regional deployment constraints.

Competitive Landscape

The top five vendors - Dynatrace, Splunk, Datadog, IBM and ServiceNow - controlled roughly 38% of global revenue in 2025, giving the AIOps market a moderately fragmented profile. Cisco’s USD 28 billion acquisition of Splunk in 2024 and IBM’s USD 6.4 billion purchase of HashiCorp exemplify strategic moves to build full-stack portfolios that blend infrastructure-as-code, observability and security analytics into unified workflows. Hyperscalers exert competitive pressure by embedding native AIOps into their control planes, often at marginal cost, entrenching themselves among cloud-native firms.

Smaller specialists such as BigPanda and Moogsoft differentiate through advanced event correlation that cuts alert noise by up to 90%. Open-source ecosystems - Grafana, Prometheus, OpenTelemetry - continue to gain mindshare among budget-conscious teams seeking transparency and vendor agnosticism, although regulated sectors still favor commercial support contracts. Hardware makers NVIDIA and AMD extend the battlefield to the edge, embedding inference engines in DPUs and FPGAs that enable sub-millisecond detection for industrial IoT.

Competitive strategies increasingly revolve around three vectors: embedding generative AI assistants, supporting edge inference and offering clear exit paths to mitigate lock-in concerns. Vendors are launching pre-built templates for healthcare, manufacturing and finance, a move that shortens time to value and aligns with sector compliance checklists. Managed service partners add another layer of differentiation by wrapping 24/7 incident response around core platforms, a model that resonates with resource-constrained SMEs.

AIOps Industry Leaders

International Business Machines Corporation

Cisco Systems, Inc. (AppDynamics, LLC)

Splunk LLC

Dynatrace, Inc.

Broadcom Inc. (VMware, Inc.; CA, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary whitespace is AI operations for AI agents, where traditional AIOps correlation expands into monitoring agent decision loops, tool calls, and automated execution. Investment is concentrating around this layer, including Coralogix raising USD 200 million (June 2026) to accelerate monitoring and troubleshooting for autonomous AI agents, and vendor moves toward autonomous remediation, such as Elastic acquiring DeductiveAI (June 2026) to add autonomous incident resolution into its observability direction.

Infrastructure efficiency and heterogeneous compute management are also active opportunity areas as organizations operationalize GPU-heavy AI workloads alongside conventional IT estates. ScaleOps raising USD 130 million (March 2026) to expand autonomous cloud and AI infrastructure management, plus Spectro Cloud raising USD 100 million (July 2026) around GPU and distributed inference operations, point to shifting spend toward tooling that reduces waste and stabilizes performance across multi-cluster and multi-cloud environments. On the enterprise services side, large transformation programs that pair infrastructure build-out with managed AI services expand the addressable services layer for AIOps, illustrated by HCL Technologies committing an initial INR 3,500 crore (July 2026) toward an AI-native data center ecosystem. In regulated industries and the public sector, governance mandates such as the US federal M-24-10 requirement for agency AI leadership and annual AI use-case inventories increase demand for operational transparency, model governance, and incident reporting that AIOps platforms can package as compliance-ready workflows.

Recent Industry Developments

- June 2026: Splunk introduced GenAI-driven time series anomaly detection powered by the Cisco Deep Time Series Model (CDTSM) through its AI Toolkit (v5.7.4). The release expands Splunk's AIOps capabilities for machine-data anomaly work without requiring extensive custom model building, and it reinforces the Cisco-Splunk stack as a combined platform for observability and operations automation.

- July 2025: Splunk and Red Hat detailed collaboration to integrate Splunk's observability portfolio with Red Hat Ansible Automation Platform using Event-Driven Ansible to automate incident response. The integration connects detection and correlation to repeatable infrastructure actions, supporting the shift from insight to execution in hybrid environments.

- June 2025: IBM announced general availability of IBM Cloud Pak for AIOps 4.10 with added script-based migration capabilities for Netcool WebGUI filters. The update targets faster modernization for existing IBM operations customers, helping preserve legacy monitoring investments while moving toward more automated incident management workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The AIOps market is defined as software and related services that use AI and analytics to monitor IT environments, detect anomalies, correlate alerts, and support faster incident resolution across hybrid and cloud operations.

Scope exclusions: Stand-alone monitoring or observability tools are excluded when they do not include automated correlation, root-cause assistance, or response workflow capabilities.

Segmentation Overview

- By Component

- Platform

- Services

- By Deployment Mode

- On-Premise

- Cloud

- By Organization Size

- Small and Medium Enterprises

- Large Enterprises

- By End-User Industry

- IT and Telecom

- BFSI

- Healthcare

- Retail and E-Commerce

- Media and Entertainment

- Manufacturing

- Government and Public Sector

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the outer rails of the model and to keep assumptions realistic as the market shifts quickly. We mainly relied on public sources such as US SEC filings and annual reports, NIST publications on AI and risk, FCC broadband and infrastructure indicators, US Bureau of Labor Statistics data for IT occupations, and OECD digital economy statistics.

To connect demand signals to spend, we also reviewed cloud adoption and outage or resilience guidance published by regulators and industry bodies, along with product documentation and reputable press coverage of major releases. Patent databases were checked to understand where automation and event-correlation innovation is concentrated, and a paid subscription for company financials and news was used to validate revenue mixes where disclosures were available. The sources listed here are illustrative only, and many other public references were used for cross-checks and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and surveys with IT operations leaders, SRE and NOC managers, platform engineering teams, and solution implementers who see buying decisions and renewal behavior. For a global view, inputs were balanced across mature and fast-growing adoption regions, and we used these conversations to test deployment mix, pricing direction, and the share of spending that is truly AIOps rather than general monitoring.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 14% | APAC: 45% |

| Mid tier: 48% | Functional/Unit leaders: 41% | EMEA: 30% |

| Smaller Players: 17% | Managers: 45% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where IT operations software and services spend is reconstructed by region, and then filtered using adoption and usage rates for AIOps-style capabilities inside monitoring, incident management, and automation programs. Where the story becomes clearer only after the parts are checked, we corroborate totals with selective bottom-up approximations such as sampled price points by deployment, channel feedback on deal sizes, and supplier revenue disclosures mapped to AIOps workloads.

Key inputs that shaped the model included growth in cloud and hybrid footprints, telemetry volumes and alert noise trends, automation penetration in incident workflows, typical contract structures (subscription versus services attach), and the shift toward platform consolidation in enterprises. For forecasting, scenario analysis was used and then anchored using multivariate regression on a small set of drivers that interviews repeatedly pointed to, including cloud workload growth, IT headcount tightness, and resilience priorities. When bottom-up signals were missing for smaller geographies, we applied proxy ratios from similar IT spend profiles and then re-checked them with local expert feedback.

Data Validation & Update Cycle

Outputs are validated through multiple checks, starting with currency normalization and consistency tests across regions and years, followed by variance review against adjacent markets such as IT operations management and monitoring. We also re-check unusual jumps by tracing them back to a concrete driver like a services mix change, a pricing reset, or a deployment shift.

Before sign-off, assumptions and calculations go through a multi-step analyst review, and experts are re-contacted when a key variable moves outside the expected range. Reports are refreshed annually, and interim updates are triggered when material events occur such as major platform shifts, regulation changes affecting data handling, or step changes in enterprise IT spending. Right before delivery, a fresh review pass is completed so clients receive the most current view.

Mordor Intelligence's Aiops Market Size Compared With Other Published Estimates

Published market values for AIOps can look far apart because each publisher draws the scope line differently and also uses different ways to treat services, deployment mix, and multi-year price changes. We also see timing effects, where some estimates are anchored to an earlier base year or use different currency conversion points.

The biggest gap drivers in AIOps are usually whether the number includes broader observability and monitoring spend, how managed services and implementation are counted, and whether the demand pool is built from IT ops budgets or from supplier revenues. When stand-alone monitoring tools are excluded unless automated correlation and response workflow value is present, and when pricing is refreshed using interview-led renewal and expansion patterns, the size stays closer to the true AIOps spend captured by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 18.95 B (2026) | |

| Global Research Publisher A | USD 14.60 B (2024) | Uses an AIOps platform-only scope with limited visibility on services attach, and the earlier base year can understate later pricing and expansion in large enterprise renewals. |

| Industry Research Publisher B | USD 2.23 B (2025) | Applies a narrower interpretation that can exclude parts of the IT ops automation and analytics stack, which can materially compress the spend pool versus broader AIOps capability-based definitions. |

The comparison shows that most variance comes from scope choices and base-year timing rather than a disagreement on demand direction. By keeping inclusions tied to specific capabilities, and then checking totals against real-world buying behavior and IT ops budget signals, the final number remains traceable and repeatable for planning.

Key Questions Answered in the Report

What is the current value of the AIOps market?

The AIOps market size is USD 18.95 billion in 2026 and is forecast to reach USD 37.79 billion by 2031.

Which segment is growing faster, platforms or services?

Services are expanding at a 16.04% CAGR through 2031, outpacing platform subscriptions.

Why are healthcare organizations adopting AIOps so rapidly?

Healthcare faces strict audit trails and patient-safety imperatives, driving a 16.66% CAGR for the segment through 2031.

How does tool consolidation affect AIOps ROI?

Reducing overlapping monitoring tools cuts licensing costs and alert noise, although integration complexity can delay ROI.

Which region offers the highest growth potential for AIOps vendors?

Asia Pacific is projected to record a 16.22% CAGR through 2031, the fastest regional expansion.

What impact do generative AI copilots have on incident response?

Copilots automate query writing and remediation suggestions, shortening triage times, but still require human validation for legacy and proprietary systems.

Page last updated on: