Implantable Defibrillators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.76 Billion |

| Market Size (2031) | USD 6.19 Billion |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Implantable Defibrillators Market Analysis by Mordor Intelligence

implantable cardioverter defibrillator market size in 2026 is estimated at USD 4.76 billion, growing from 2025 value of USD 4.52 billion with 2031 projections showing USD 6.19 billion, growing at 5.38% CAGR over 2026-2031. Growth stems from the transition toward AI-integrated devices that predict arrhythmic events, extended-life batteries that reduce replacement procedures, and rising prophylactic use in high-risk heart-failure cohorts. Mature health systems prioritize longevity and remote monitoring, while emerging regions focus on first-time access. Subcutaneous and extravascular systems are reshaping surgical practice by eliminating transvenous leads, and pediatric applications are expanding swiftly as miniaturized platforms address congenital conditions. Heightened regulatory scrutiny and cybersecurity demands temper momentum yet spur investment in secure firmware and post-market surveillance.

Key Report Takeaways

- By product type, transvenous systems led with 70.92% revenue share in 2025, whereas subcutaneous devices are forecast to expand at a 6.44% CAGR through 2031.

- By end user, hospitals and cardiac centers held 79.63% of the implantable cardioverter defibrillator market share in 2025, while ambulatory surgical centers record the highest projected CAGR at 6.18% to 2031.

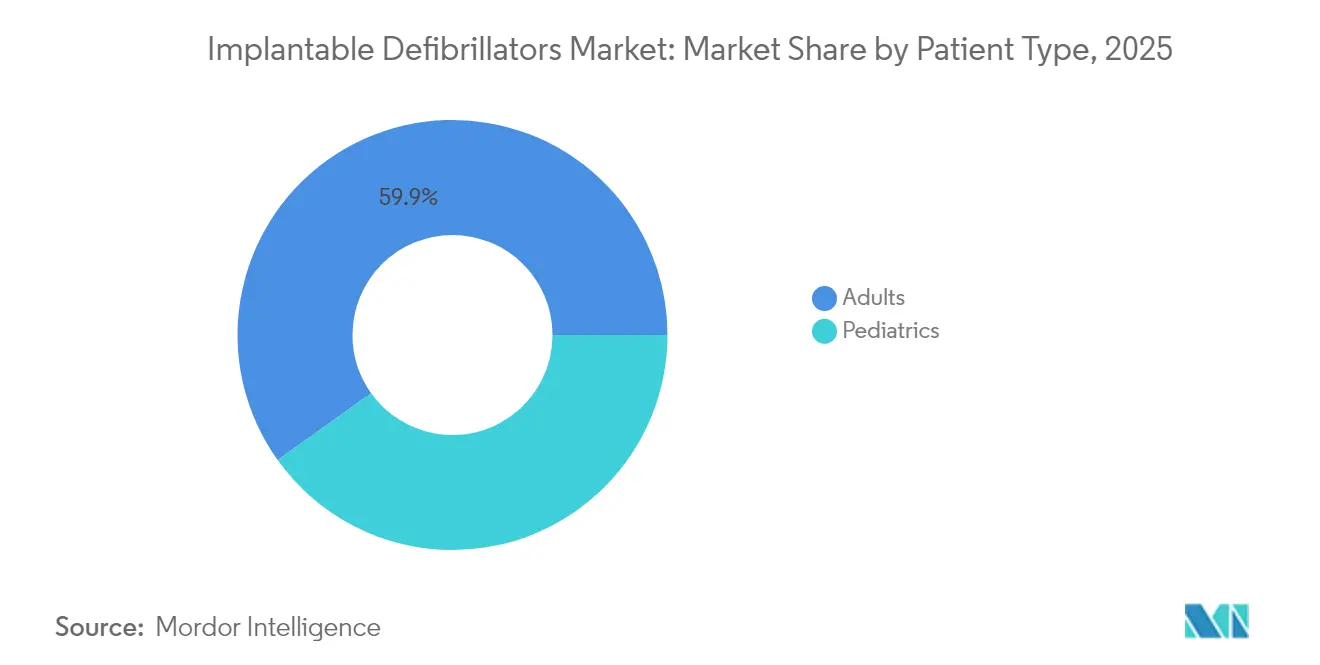

- By patient type, adults accounted for 59.88% share of the implantable cardioverter defibrillator market size in 2025; the pediatric segment is advancing at a 6.74% CAGR through 2031.

- By geography, North America commanded 42.11% of global revenue in 2025, whereas Asia-Pacific is poised for a 7.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Implantable Defibrillators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of arrhythmias & sudden cardiac death risk | +1.5% | North America & Europe | Long term (≥ 4 years) |

| Battery-longevity and device miniaturization breakthroughs | +1.2% | Global, early in developed markets | Medium term (2-4 years) |

| Uptake of MRI-conditional & connected ICDs | +0.8% | North America & EU leading | Medium term (2-4 years) |

| “Shock-less” algorithms lowering patient anxiety | +0.6% | Quality-focused markets | Short term (≤ 2 years) |

| Extravascular/Leadless ICD Trial Success Expanding Eligibility | +0.4% | North America & EU initial rollout | Long term (≥ 4 years) |

| AI-Driven Predictive Analytics Boosting Prophylactic Implants | +0.3% | Developed markets with advanced healthcare infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Cardiac Arrhythmias & SCD Risk

Global aging and higher post-infarction survival have enlarged the population vulnerable to sudden cardiac death. Roughly 400,000 U.S. residents suffer cardiac arrest each year, and survival remains close to 10% [1]Kristin Watson, “Arrhythmic Deaths and ICD Outcomes in Modern HF Care,” American Heart Association, heart.org. Guideline-backed evidence supports prophylactic ICD use in heart-failure cohorts with reduced ejection fraction, pushing clinicians to screen earlier using family history and genetic markers. As a result, primary‐prevention implants constitute the fastest-growing indication, ensuring sustained demand across the implantable cardioverter defibrillator market.

Continuous Miniaturization & Battery-Longevity Improvements

Boston Scientific’s EnduraLife cell delivers 1.9 Ah, extending projected service lives to 17.5 years and cutting replacement procedures by 40% [2]Product Team, “EnduraLife Battery Longevity Data,” Boston Scientific, bostonscientific.com. Longer life translates to Medicare savings of USD 15,120 per recipient, reinforcing health-system preference for premium platforms. Miniaturization also supports subcutaneous placement, avoiding lead complications that previously affected 15% of patients.

Wider Adoption of MRI-Conditional & Connected ICDs

MRI-conditional labeling removes lifetime scan bans that once deterred eligible candidates. Remote telemetry transmits device and rhythm data within 18.5 hours and receives clinician review in under one day, achieving 97% patient compliance. Continuous monitoring reframes ICDs as holistic disease-management hubs, lowering hospitalizations by 25% and improving medication adherence.

“Shock-Less” ICD Algorithms Easing Patient Anxiety

Modern discrimination algorithms now reach 95% specificity, trimming inappropriate shocks by 60%. Lower shock burden lifts patient quality-of-life scores by 40% and boosts physician confidence, expanding the implantable cardioverter defibrillator market among risk-averse cohorts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory hurdles & recent recalls | -0.9% | Regulated markets | Short term (≤ 2 years) |

| High device and follow-up costs in low-income settings | -0.7% | Emerging APAC & MEA | Long term (≥ 4 years) |

| Cyber-Security Concerns With Wireless ICD Telemetry | -0.5% | Developed markets with advanced connectivity | Medium term (2-4 years) |

| Rise Of Catheter-Ablation Curbing Implant Growth | -0.4% | Global, with higher impact in advanced markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Hurdles & Product Recalls

Medtronic’s Cobalt and Boston Scientific’s EMBLEM recalls in 2024 affected more than 100,000 devices, triggering FDA demands for tighter cybersecurity and lengthening approval cycles by up to 18 months [3]FDA Center for Devices, “Safety Communication on Cardiac Rhythm Management Devices,” U.S. Food and Drug Administration, fda.gov. Smaller firms struggle to absorb the 25% compliance-cost spike, which restrains near-term product flow and tempers adoptive enthusiasm.

High Device & Follow-Up Costs in Low-Income Settings

In Kenya and Kazakhstan, fewer than 5% of indicated patients receive ICD therapy, as unit prices equal up to 12 months of household earnings. Import tariffs can inflate landed costs by 60%, and scarce electrophysiology expertise heightens procedural barriers, slowing implantable cardioverter defibrillator market diffusion across emerging economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Subcutaneous Disruption Versus Transvenous Scale

Transvenous systems maintained 70.92% dominance in 2025, yet subcutaneous devices are clocking a 6.44% CAGR through 2031 as practitioners embrace lead-free implantation. The PRAETORIAN trial confirmed equal shock efficacy with fewer lead-related complications. The implantable cardioverter defibrillator market size for subcutaneous platforms is therefore expanding faster than the mature transvenous segment.

Extravascular and leadless designs add another frontier. Medtronic’s Aurora EV-ICD received FDA clearance in 2024, combining lead-free safety with pacing capability. Appropriate shock success reached 95% and reduced procedural time, positioning extravascular systems to siphon share from both incumbent categories while elevating overall implantable cardioverter defibrillator market resilience.

By End User: Outpatient Momentum

Hospitals and cardiac centers controlled 79.63% revenue in 2025, reflecting embedded infrastructure. Nevertheless, ambulatory surgical centers are accelerating at 6.18% CAGR as streamlined protocols cut same-day discharge times and facility fees. Specialty clinics handle pediatric and revision cases requiring advanced skills, whereas home-based remote-monitoring programs register 97% compliance, reinforcing lifetime oversight and fueling broader implantable cardioverter defibrillator market adoption.

By Patient Type: Pediatric Innovations

Adults accounted for 59.88% of 2025 volume, yet pediatric implants are rising at 6.74% CAGR. Children benefit from miniaturized generators and algorithms distinguishing exercise tachycardia from pathology. Pediatric-specific subcutaneous and leadless prototypes promise to shrink procedural revision frequency, further cultivating the implantable cardioverter defibrillator market.

Geography Analysis

North America’s 42.11% share stems from universal reimbursement and a dense electrophysiology workforce. Yet market expansion moderates as insurers demand evidence of cost efficacy, pivoting procurement toward extended-life batteries and robust cybersecurity audits.

Europe ranks second and emphasizes sustainability: cardiac societies endorse biodegradable materials and recycling workflows, influencing purchasing criteria and cultivating eco-centric design mandates. Diverse reimbursement models create fragmented uptake, but harmonized CE-marking accelerates multi-country launches.

Asia-Pacific, paced by 7.02% CAGR, offers the deepest runway. Japan leads premium adoption, while populous nations such as India exhibit implant rates 10-20-fold below clinical need, mainly due to affordability gaps and limited electrophysiology talent. Government-sponsored training and local manufacturing incentives aim to narrow the disparity, ultimately broadening the implantable cardioverter defibrillator market footprint.

Competitive Landscape

Medtronic, Boston Scientific, and Abbott collectively control majority of revenue, underlining moderate consolidation. Differentiation hinges on battery chemistry, AI-driven diagnostics, and secure cloud telemetry. The competitive focus has shifted from hardware commoditization to data services; remote-monitoring subscriptions generate recurring revenue and deepen patient lock-in.

Acquisition activity underscores vertical integration. Johnson & Johnson’s USD 1.7 billion V-Wave purchase augments heart-failure therapy adjacency and expands total addressable market. Emerging entrants target niche terrain—biodegradable generators, pediatric leadless devices, and predictive analytics engines—pressuring incumbents to accelerate R&D.

The ascent of catheter ablation, posting success rates above 85% for select arrhythmias, challenges ICD growth in certain phenotypes. In response, leading vendors pilot hybrid offerings that bundle ablation solutions with next-generation defibrillators, preserving relevance and diversifying revenue within the broader implantable cardioverter defibrillator market.

Implantable Defibrillators Industry Leaders

Boston Scientific Corporation

Medtronic PLC

LivaNova PLC

Abbott

Biotronik

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Medtronic Japan launched the Aurora EV-ICD MRI system and Epsila EV MRI lead in Japan.

- October 2024: MicroPort introduced PLATINIUM single-chamber ICD (14-year lifespan) and dual-chamber ICD (13-year lifespan).

- February 2023: Medtronic PLC received the CE mark for the Aurora EV-ICD MRI SureScan (Extravascular Implantable Cardioverter-Defibrillator) and Epsila EV MRI SureScan defibrillation lead to treat very fast heart rhythms that can result in sudden cardiac arrest.

Global Implantable Defibrillators Market Report Scope

Implantable Defibrillator/Implantable Cardioverter Defibrillator (ICD) is a battery-powered device placed under the skin that connects the ICD to the patient's heart using thin wires. The ICD keeps track of the heart rate, and if an abnormal heart rhythm is detected, the device will deliver an electric shock to restore a normal heartbeat. The Implantable Defibrillators Market is segmented by type (single chambered, dual chambered, and biventricular), route (transvenous/traditional ICD and Subcutaneous (S-ICD)), end user (hospitals, specialty clinics, and ambulatory surgical centers) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Transvenous ICDs | Single-Chamber ICD |

| Dual-Chamber ICD | |

| Cardiac Resynchronization Therapy-Defibrillator (CRT-D) | |

| Subcutaneous ICDs (S-ICD) | |

| Extravascular / Leadless ICDs |

| Hospitals & Cardiac Centers |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Home-care / Remote Monitoring Programs |

| Adults |

| Pediatrics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Transvenous ICDs | Single-Chamber ICD |

| Dual-Chamber ICD | ||

| Cardiac Resynchronization Therapy-Defibrillator (CRT-D) | ||

| Subcutaneous ICDs (S-ICD) | ||

| Extravascular / Leadless ICDs | ||

| By End User | Hospitals & Cardiac Centers | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Home-care / Remote Monitoring Programs | ||

| By Patient Type | Adults | |

| Pediatrics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Implantable Defibrillators Market?

The Implantable Defibrillators Market size is expected to reach USD 4.76 billion in 2026 and grow at a CAGR of 5.38% to reach USD 6.19 billion by 2031.

Which product type is expanding the quickest?

Subcutaneous systems are the fastest-growing category, projected to post a 6.44% CAGR through 2031 thanks to lead-free implantation and lower complication risks.

Who are the key players in Implantable Defibrillators Market?

Boston Scientific Corporation, Medtronic PLC, LivaNova PLC, Abbott and Biotronik are the major companies operating in the Implantable Defibrillators Market.

Which is the fastest growing region in Implantable Defibrillators Market?

Asia-Pacific is expected to expand at a 7.02% CAGR through 2031, driven by rising cardiac disease prevalence and improving healthcare infrastructure.

Which region has the biggest share in Implantable Defibrillators Market?

In 2026, the North America accounts for the largest market share in Implantable Defibrillators Market.

Page last updated on: