External Defibrillator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

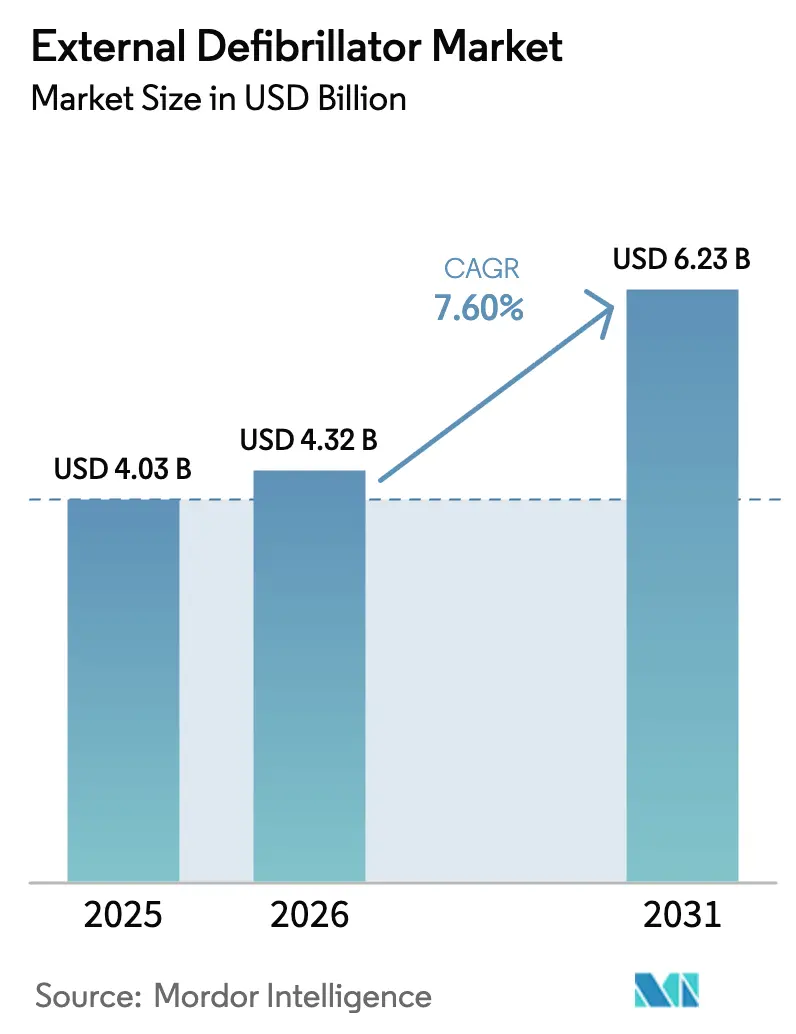

| Market Size (2026) | USD 4.32 Billion |

| Market Size (2031) | USD 6.23 Billion |

| Growth Rate (2026 - 2031) | 7.60% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

External Defibrillator Market Analysis by Mordor Intelligence

The External Defibrillator Market size was valued at USD 4.03 billion in 2025 and is estimated to grow from USD 4.32 billion in 2026 to reach USD 6.23 billion by 2031, at a CAGR of 7.60% during the forecast period (2026-2031).

The rising incidence of out-of-hospital cardiac arrest, stricter public-access mandates, and the rapid integration of artificial intelligence into automated external defibrillators are expanding the customer base beyond hospitals to schools, transportation hubs, and workplaces. North America leads in current revenue, while Asia-Pacific is gaining momentum due to regulatory reforms that have shortened device review timelines in China and incentive programs in India. Meanwhile, North America continues to generate high replacement demand as its installed fleets age. Product innovation is shifting value capture from hardware margins to subscription analytics and remote monitoring, favoring manufacturers that control both devices and software platforms. Tightening European trade rules and supply-chain volatility for semiconductor components are compelling firms to diversify production footprints and pursue component localization.

Key Report Takeaways

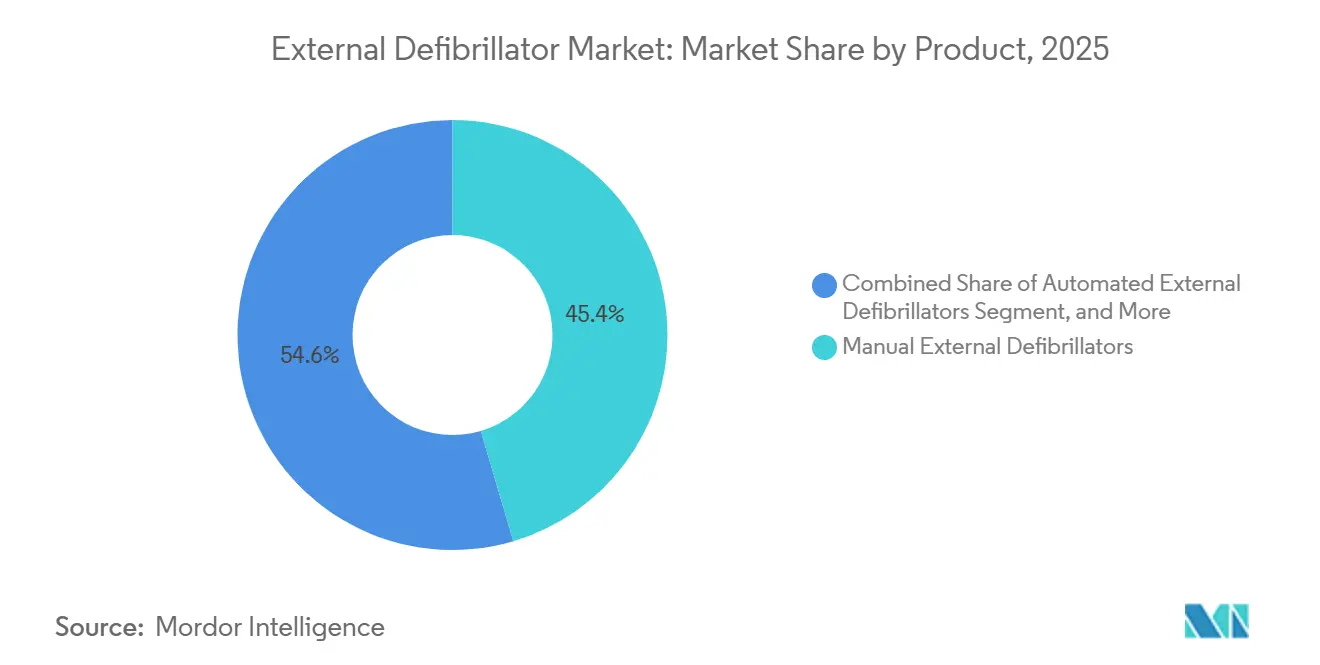

- By product category, manual devices led the external defibrillator market with 45.43% of the market share in 2025; automated external defibrillators are forecast to expand at a 9.54% CAGR through 2031.

- By end-user, hospitals and cardiac centers held 54.56% of the external defibrillator market size in 2025, while home healthcare is projected to advance at a 10.32% CAGR through 2031.

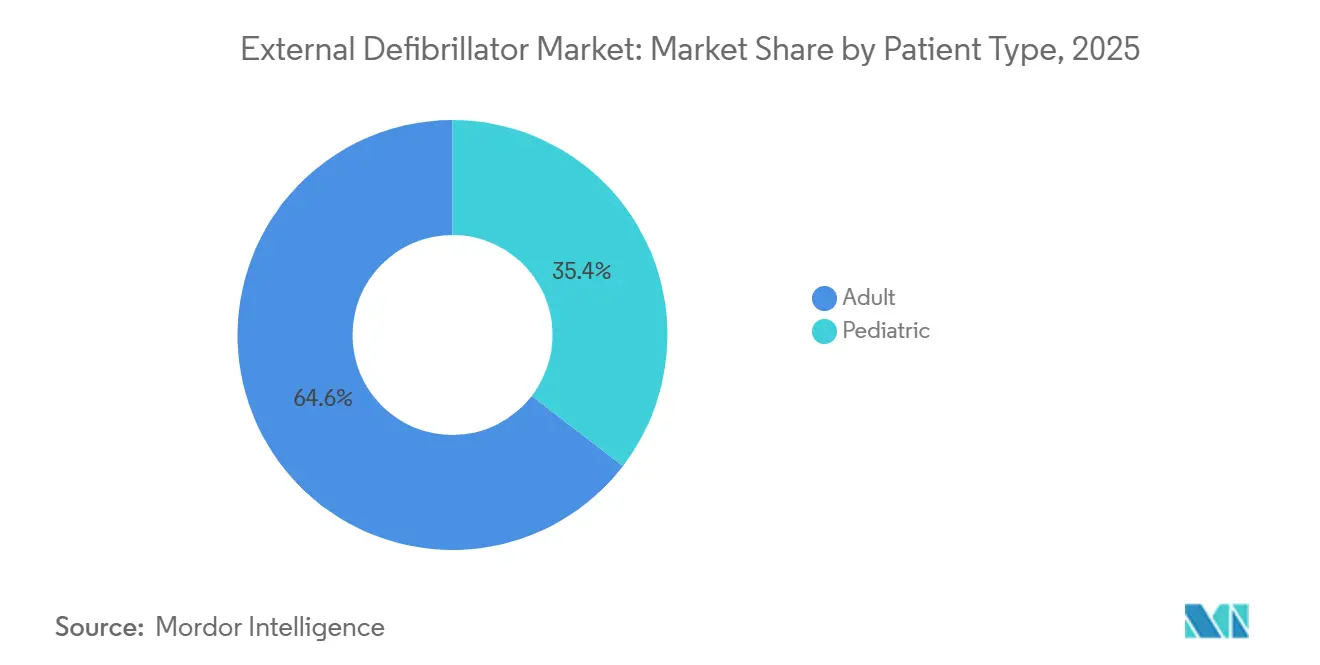

- By patient type, adults accounted for a 64.56% share of the external defibrillator market size in 2025, while pediatrics is projected to grow at a 9.66% CAGR through 2031.

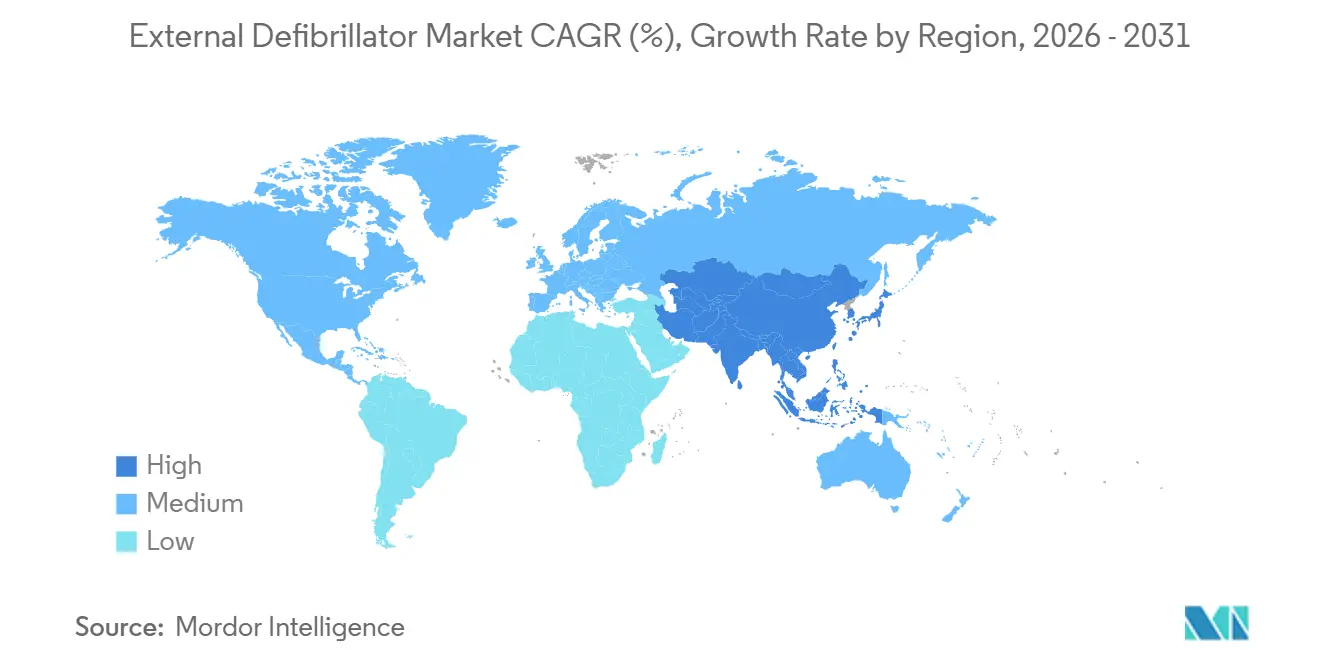

- By geography, North America captured 46.43% revenue in 2025, while Asia-Pacific is projected to sustain the fastest regional growth at an 8.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global External Defibrillator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden Of Sudden Cardiac Arrests Globally | +2.1% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Expanding Public-Access Defibrillation Programs And Mandates | +1.8% | North America, Europe, APAC urban centers | Medium term (2-4 years) |

| Technological Advancements In Smart And Connected AEDs | +1.5% | Global, early adoption in North America and Western Europe | Medium term (2-4 years) |

| Growing Adoption Of Wearable Cardioverter Defibrillators | +0.9% | North America, Europe | Medium term (2-4 years) |

| Supportive Reimbursement And Regulatory Frameworks | +0.7% | North America, select European markets | Long term (≥ 4 years) |

| Increasing Investments And Strategic Collaborations | +0.6% | APAC (China, India, Singapore), North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Sudden Cardiac Arrests Globally

Out-of-hospital cardiac arrest affects more than 350,000 people each year in the United States, yet survival-to-discharge remains below 12%, intensifying the need for rapid defibrillation. Aging populations and a higher prevalence of metabolic syndrome are amplifying case volumes across Europe and the Asia-Pacific region, thereby broadening the external defibrillator market. Every minute of defibrillation delay reduces the survival probability by 7% to 10%, prompting health authorities to prioritize the placement of devices in public venues. The 2025 American Heart Association guidelines extended perioperative defibrillation recommendations, prompting the procurement of defibrillators into surgical suites[1]American Heart Association, “2025 Guidelines Update,” heart.org. While epidemiological pressure is high, closing the survival gap also requires training initiatives, compelling manufacturers to bundle education with device sales.

Expanding Public-Access Defibrillation Programs and Mandates

State rules such as Maine’s health club AED requirement and New Jersey’s school deployment law have accelerated institutional purchases in the United States. In December 2025, PulsePoint and ZOLL Medical launched the National Emergency AED Registry to provide dispatch centers with real-time device location data, thereby shortening response times[2]. Europe’s 2022 peri-operative guidelines are driving National Health Service trusts to standardize equipment stocks, and China’s December 2024 policy reforms cut clinical review timelines to 30 days in pilot zones. Compliance remains uneven because few jurisdictions enforce penalties; however, the direction is firmly toward broader deployment, which supports demand growth in the external defibrillator market.

Technological Advancements in Smart and Connected AEDs

AliveCor received U.S. FDA clearance in June 2024 for a portable 12-lead AI-powered electrocardiogram, demonstrating that hospital-grade diagnostics can be integrated into field devices[3]. Stryker’s LIFEPAK 35 offers cloud dashboards that alert fleet managers when batteries or electrodes are nearing expiration, thereby reducing downtime and maintenance costs. Peer-reviewed studies in 2024 demonstrated that on-device deep-learning algorithms can effectively guide chest compressions, achieving area-under-the-curve scores above 0.90, thereby enhancing lay-rescuer performance. These capabilities differentiate premium products and open recurring-revenue models, elevating the strategic importance of software engineering resources within defibrillator firms.

Growing Adoption of Wearable Cardioverter Defibrillators

Wearable cardioverter defibrillators, such as ZOLL’s LifeVest, serve high-risk patients during the vulnerable post-discharge window, and expanded Medicare coverage after 2024 will reduce out-of-pocket costs. Clinical trials have documented the effectiveness of arrhythmia detection; however, adherence averages roughly 70% due to garment discomfort, which limits the absolute volumes. Companies are investing in lighter fabrics and wireless electrode arrays; however, the trade-off between continuous monitoring and patient convenience remains. Cardiologists increasingly favor hybrid platforms that combine wearables with cloud analytics, supporting individualized therapy titration and strengthening the external defibrillator industry’s service revenues.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost Of Ownership And Maintenance | -1.2% | Global, acute in price-sensitive emerging markets | Medium term (2-4 years) |

| Supply-Chain Constraints For Critical Components | -0.8% | Global, most evident in North America, Europe, and East Asia manufacturing hubs | Short term (≤ 2 years) |

| Stringent Regulatory Approval Timelines | -0.7% | Global, pronounced in the European Union and Japan | Medium term (2-4 years) |

| Insufficient Public Awareness And Training | -0.9% | Global, highest in rural and low-resource settings | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership and Maintenance

The retail price of an automated external defibrillator averages USD 2,338, but batteries and electrode pads require replacement every 2 to 5 years, pushing lifetime outlays above USD 4,000. Schools and community centers with limited budgets often defer the acquisition of refurbished units that lack software updates, creating a bifurcated installed base. Field audits in 2024 revealed 18% of public devices had expired electrodes and 12% had depleted batteries, undermining emergency readiness. The 2026 Durable Medical Equipment fee schedule raised allowable charges by only 2%, leaving most public-access deployments unfunded. Subscription models that bundle hardware, consumables, and monitoring are emerging to convert capital expenditure into predictable operating expenses.

Insufficient Public Awareness and Training

Bystander AED activation remains below 40% worldwide, reflecting limited knowledge about device locations and Good Samaritan legal protections. Only one-fifth of U.S. adults held a current CPR/AED certification in 2025, which limits the public health impact of the external defibrillator market. Virtual-reality training platforms can scale education, but their adoption tends to skew toward corporations rather than community programs. Regulators do not mandate end-user training, so manufacturers bear the burden of awareness campaigns, which erode their margins. To address underutilization, leading vendors partner with fire departments and emergency medical service agencies to embed device familiarization into CPR curricula, aligning commercial goals with public safety missions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Manual Devices Anchor Revenue, AEDs Propel Volume Growth

Manual external defibrillators captured 45.43% of the external defibrillator market share in 2025, reinforcing their role in critical-care environments that require invasive pressure monitoring and capnography. Average selling prices range between USD 15,000 and USD 25,000, and multi-parameter integrations justify hospital budget allocations despite lengthier replacement cycles. Automated external defibrillators, priced one-tenth as much, are set to expand at 9.54% CAGR, making them the key driver of unit shipments in the external defibrillator market. The external defibrillator market size for automated models is projected to increase by USD 1.25 billion between 2026 and 2031 as public venues update their fleets to comply with new registry-tracking standards. Wearable cardioverter defibrillators remain a niche, but robust clinical evidence and broader reimbursement could unlock incremental growth.

Feature roadmaps emphasize connectivity—Stryker’s LIFEPAK 35 uploads readiness data to cloud portals, allowing biomedical engineers to schedule maintenance proactively. AliveCor’s 12-lead device blurs lines between responder tools and diagnostic equipment, challenging incumbents to integrate high-resolution sensing without compromising lay-user simplicity. Manual defibrillator suppliers face price pressure as group purchasing organizations negotiate bulk contracts; however, premium software modules for post-event data analytics and protocol compliance help protect margins.

By Patient Type: Adults Dominate, Pediatrics Accelerates

Adults generated 64.56% of the revenue in 2025, reflecting the higher incidence of cardiac arrest in populations older than 50 years and well-established energy-dose protocols. The external defibrillator market size for adult indications is projected to reach USD 4.05 billion by 2031, as lifestyle-related cardiovascular risks continue to rise. Pediatric demand is advancing at a 9.66% CAGR, driven by state laws that require school campuses and youth sports facilities to stock child-capable AEDs. Pediatric-specific electrodes deliver 50-75 joules, minimizing myocardial injury while preserving shock efficacy. Dedicated pediatric units simplify operation but raise inventory costs because institutions must maintain separate fleets, prompting many buyers to favor dual-mode devices with switchable pads.

Regulators now require age-stratified clinical data for marketing claims, which extends development timelines but improves safety profiles. Manufacturers are introducing color-coded prompts and child-size illustrations to minimize cognitive load during high-stress scenarios. Continued guideline updates are likely to expand indications to neonatal resuscitation in surgical suites, creating additional, albeit small, revenue pockets within the external defibrillator industry.

By End-User: Institutional Core Faces Home-Care Disruption

Hospitals and cardiac centers accounted for 54.56% of revenue in 2025, valuing advanced monitoring that allows seamless integration with electronic medical records. However, payer pressure to prevent readmissions is steering providers toward remote monitoring platforms, which are migrating some therapies into the community. The external defibrillator market size in home-health settings is projected to increase from USD 0.28 billion in 2026 to USD 0.46 billion by 2031, driven by the adoption of wearable cardioverter defibrillators and tele-cardiology dashboards. Public-access locations continue to expand unit counts as liability insurers mandate on-site devices; nonetheless, field inspections reveal maintenance gaps that reduce functional availability during critical moments.

Emergency medical services rely on ruggedized devices capable of delivering shocks en route to hospitals, and many deploy automatic chest-compression adjuncts to maintain circulation. Subscription models that cover devices, batteries, pads, and cloud analytics are gaining popularity among schools and small businesses because they eliminate the need for large upfront purchases. Partnerships, such as the PulsePoint-ZOLL registry, reinforce ecosystem advantages by linking hardware fleets to public-safety workflows, thereby enhancing stickiness and driving recurring revenue.

Geography Analysis

Asia-Pacific is projected to be the fastest-growing region in the external defibrillator market, expanding at an 8.54% CAGR through 2031. China’s December 2024 regulatory reforms halved clinical-trial review timelines in pilot zones, accelerating approvals for automated models and encouraging local manufacturing. India’s Production Linked Incentive scheme selected BPL Medical Technologies and Allied Medical Limited for domestic production grants, reducing import reliance and improving price competitiveness. Japan’s super-aged demographics support institutional procurement, but cultural hesitation toward bystander intervention tempers public-access utilization rates. Localized production, exemplified by BIOTRONIK’s Singapore hub, shortens supply chains and sidesteps tariff volatility, positioning multinationals to respond swiftly to regional demand spikes.

North America exhibits mature deployment densities, with most public venues already equipped; growth, therefore, stems from technology refreshes and software upgrades. State mandates, such as Maine’s health-club rule, still generate incremental unit sales, but replacement cycles now stretch beyond seven years as hardware reliability improves. Europe is undergoing a supply-chain restructuring following the June 2025 International Procurement Instrument's restriction on Chinese devices in large public tenders, prompting hospitals to shift their orders to regional manufacturers. The change opens up opportunities for European mid-caps, but also presents component-sourcing challenges, as many sub-assemblies originate in China.

The Middle East and Africa remain nascent yet promising segments. Gulf Cooperation Council states are investing in national ambulance modernization, importing defibrillators with Arabic-language interfaces, whereas sub-Saharan markets rely on donor-funded public health projects. South America is expanding slowly; Brazil’s public-access initiative in São Paulo mandates AEDs in transport terminals, but high import tariffs hinder volume growth. Overall, geographic diversification necessitates multiple regulatory pathways, compelling manufacturers to tailor product documentation, language packs, and post-market surveillance procedures for each jurisdiction.

Competitive Landscape

The external defibrillator market is moderately consolidated, with ZOLL Medical (Asahi Kasei), Stryker, Medtronic, and Koninklijke Philips N.V. collectively controlling roughly 55-60% of the 2025 revenue. Philips’ decision in January 2025 to divest its Emergency Care business to Bridgefield Capital alters the hierarchy, removing a legacy brand and inviting second-tier players to vie for share. Incumbents differentiate through software; Stryker’s LIFEPAK 35 pushes readiness data to cloud dashboards, while ZOLL offers AI-driven CPR feedback loops. AliveCor’s FDA-cleared AI ECG signals new competition from digital-health specialists that can layer diagnostics onto consumer-style hardware.

Pricing pressure in hardware compels firms to monetize data. Subscription bundles covering device, consumables, fleet monitoring, and analytic insights provide predictable cash flow and deepen customer lock-in. European restrictions on Chinese tenders heighten interest in near-shore assembly, prompting Shenzhen Mindray to cultivate distributor networks in Latin America and Africa to offset lost European volume. Barriers to entry remain high because the FDA classifies new AEDs under the premarket approval process, which demands rigorous clinical evidence, and the EU MDR assigns a Class III designation for defibrillators, requiring third-party audits and post-market surveillance.

Strategic collaborations are increasing. The December 2025 PulsePoint-ZOLL registry integrates crowd-sourced AED mapping into emergency dispatch, providing ZOLL with a data advantage that its competitors must match. BIOTRONIK’s Singapore facility supports design-for-cost projects targeting ASEAN price points, while Asahi Kasei invests in semiconductor production to mitigate chip shortages. These moves show a sector balancing innovation with supply resiliency as it navigates variable trade policies and component availability.

External Defibrillator Industry Leaders

Koninklijke Philips N.V.

Stryker (Physio-Control)

GE Healthcare

Boston Scientific Corp.

Asahi Kasei (ZOLL Medical)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Philips announced the divestiture of its Emergency Care business, including the HeartStart AED portfolio, to Bridgefield Capital

- December 2025: PulsePoint and ZOLL Medical partnered to roll out a National Emergency AED Registry

- March 2024: Stryker, a global leader in medical technology, participated in the Criticare National Conference at the ITC Royal Bengal in Kolkata, India. During the event, the company launched and showcased two new products: the LIFEPAK CR2 AED for cardiac care and an Evacuation Chair for emergency patient evacuation. This highlights Stryker’s commitment to innovation in healthcare solutions.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the external defibrillator market as the worldwide sales value of new manual external defibrillators, automated external defibrillators (semi- and fully automatic), and wearable cardioverter defibrillators supplied to hospitals, emergency medical services, public-access programs, and home users during a calendar year.

Scope exclusion: Used or refurbished equipment, implantable devices, rental fleets, consumables, and post-sale services are not included.

Segmentation Overview

- By Product

- Manual External Defibrillators

- Automated External Defibrillators (AEDs)

- Semi-Automated AEDs

- Fully-Automated AEDs

- Wearable Cardioverter Defibrillators (WCDs)

- By Patient Type

- Adult

- Pediatric

- By End-User

- Hospitals & Cardiac Centers

- Pre-Hospital & EMS

- Public Access Settings

- Home Healthcare

- Alternate Care

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest Of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest Of Asia-Pacific

- Middle East And Africa

- GCC

- South Africa

- Rest Of Middle East And Africa

- South America

- Brazil

- Argentina

- Rest Of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Cardiologists, resuscitation instructors, EMS buyers, and senior commercial managers across North America, Europe, Asia-Pacific, and Latin America were interviewed. Their guidance on adoption barriers, channel discounts, and replacement cycles allowed us to refine desk assumptions and align the model with on-ground realities.

Desk Research

We began by gathering sudden cardiac arrest and cardiovascular mortality statistics from tier-one public sources such as the World Health Organization, American Heart Association, and European Resuscitation Council. Trade volumes from UN Comtrade, FDA and European Medicines Agency clearance logs, and national customs codes helped set shipment counts and average selling prices. Company 10-Ks, investor decks, and EMS procurement databases clarified unit costs and installed-base churn, while news and deal trackers from Dow Jones Factiva, plus distributor revenues from D&B Hoovers, rounded out competitive signals. The sources mentioned illustrate our approach; many other open datasets informed the analysis.

Market-Sizing & Forecasting

We applied a top-down demand pool that multiplies documented sudden cardiac arrest incidence by guideline-recommended penetration targets, then subtracts the working installed base to derive annual unit need. Sampled supplier roll-ups (shipment volumes × blended ASPs) served as a bottom-up check. Core variables include public-access mandate counts, hospital cath-lab expansion, EMS fleet growth, device replacement intervals, and ASP shifts toward connected models. Multivariate regression against demographic aging, cardiovascular mortality, and health-expenditure growth produced forecasts to 2030, with scenario ranges validated by our primary respondents.

Data Validation & Update Cycle

Draft outputs pass peer review, anomaly checks, and currency normalization before sign-off. Mordor refreshes each model annually and triggers mid-cycle updates whenever material regulatory or recall events alter the data landscape, so clients always receive the latest baseline.

Why Mordor's External Defibrillator Baseline Earns Stakeholder Confidence

Published estimates often diverge because firms mix device classes, apply different price deflators, or lock forecasts to outdated base years. By matching scope to real procurement patterns and updating faster, Mordor offers a balanced midpoint decision-makers can trust.

Key gap drivers include exclusion of wearables by some publishers, uniform global ASP assumptions, and the bundling of training contracts or implantables into external figures, all of which shift totals away from our 2025 view.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.01 B (2025) | Mordor Intelligence | NA |

| USD 3.85 B (2024) | Global Consultancy A | Earlier base year; limited tracking of public-access units |

| USD 4.40 B (2024) | Industry Association B | Uses list prices without channel discount adjustments |

| USD 4.81 B (2023) | Regional Consultancy C | Bundles training and maintenance revenue into device value |

The comparison shows that while figures vary, Mordor's disciplined scope selection, transparent variables, and timely refresh cycle create the most reproducible and decision-ready baseline for planners and investors.

Key Questions Answered in the Report

What is the projected revenue size for external defibrillators in 2031?

Global sales are forecast to reach USD 6.23 billion by 2031, rising from USD 4.32 billion in 2026 at a 7.60% CAGR.

Which region is expected to post the fastest growth through 2031?

Asia-Pacific is forecast to expand at an 8.54% CAGR on the back of quicker device approvals in China and incentive programs that encourage local production in India.

How quickly are automated external defibrillators (AEDs) growing compared with manual models?

AED revenue is projected to climb at a 9.54% CAGR to 2031, outpacing manual external defibrillators, which already hold the largest 2025 share at 45.43%.

What is the main cost concern that limits public-access deployments?

Total cost of ownership exceeds USD 4,000 over a seven-year life once batteries and electrode pad replacements are included, creating budget hurdles for schools and community venues.

Which patient segment is expanding the fastest?

Pediatric applications are growing at a 9.66% CAGR, driven by mandates for child-capable AEDs in schools and youth sports facilities.

Who are the current leaders in external defibrillator devices?

ZOLL Medical, Stryker, and Medtronic together account for roughly 55-60% of global revenue, with Philips' 2025 divestiture of its Emergency Care unit reshaping the competitive field.

Page last updated on: