Identity Governance And Administration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

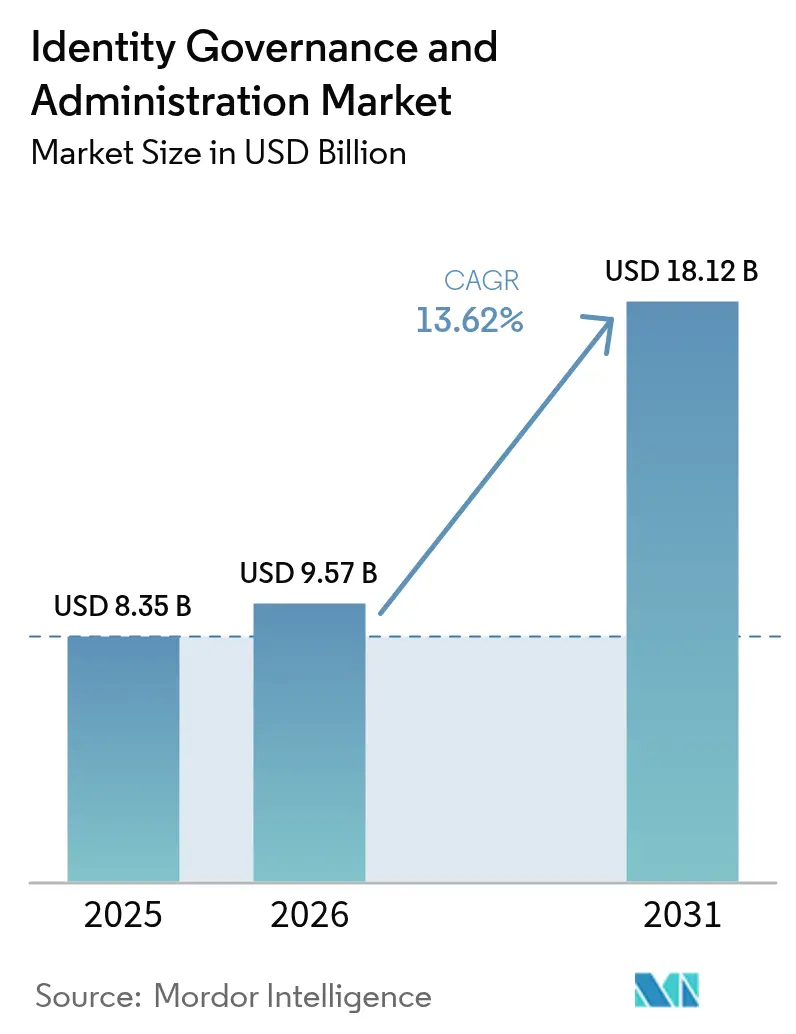

| Market Size (2026) | USD 9.57 Billion |

| Market Size (2031) | USD 18.12 Billion |

| Growth Rate (2026 - 2031) | 13.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Identity Governance And Administration Market Analysis by Mordor Intelligence

The Identity Governance And Administration market size is expected to increase from USD 8.35 billion in 2025 to USD 9.57 billion in 2026 and reach USD 18.12 billion by 2031, growing at a CAGR of 13.62% over 2026-2031. Rapid movement from periodic audits toward continuous access certification is widening adoption among banking and healthcare firms. Cloud deployment keeps momentum as Middle-East sovereign-cloud mandates demand domestic data residency without compromising global federation. Ongoing convergence of privileged access management with identity governance is lowering total cost of ownership for large European utilities, while zero-trust programs in the United States are accelerating demand for role-mining analytics. Skill shortages persist, so enterprises lean on managed services and low-code orchestration to fill implementation gaps.

Key Report Takeaways

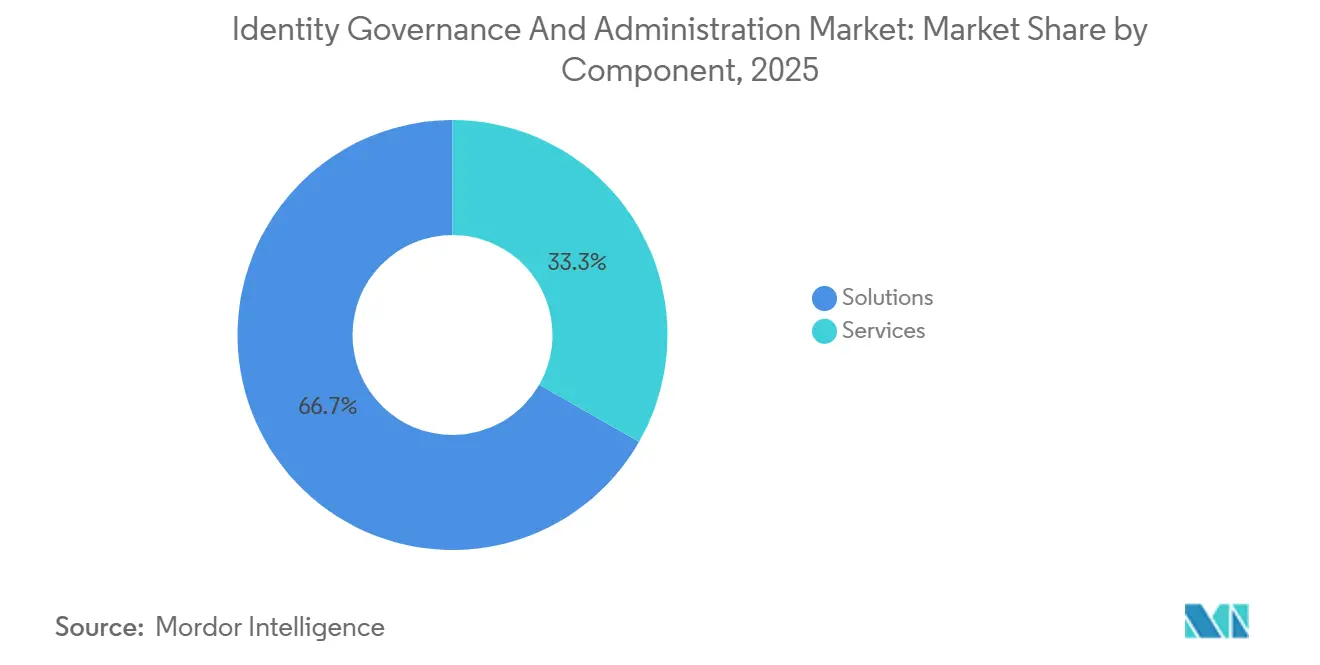

- By component, solutions held 66.73% of the Identity Governance And Administration market share in 2025 while services are expanding at a 13.71% CAGR through 2031.

- By deployment mode, cloud accounted for 57.91% revenue in 2025 and is advancing at a 13.77% CAGR over the forecast window.

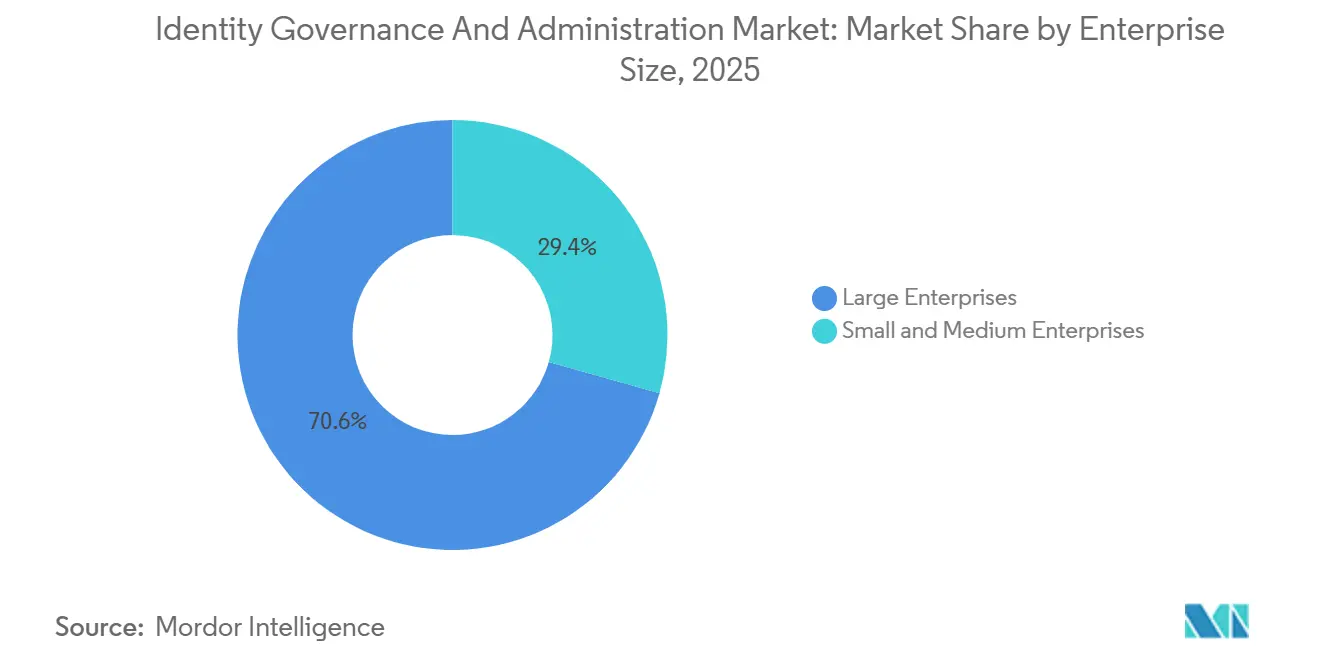

- By enterprise size, large enterprises commanded 70.63% spending in 2025 but small and medium enterprises are growing at a 13.83% CAGR to 2031.

- By end-user vertical, BFSI led with 29.26% revenue share in 2025, whereas retail and e-commerce is projected to grow at a 13.88% CAGR.

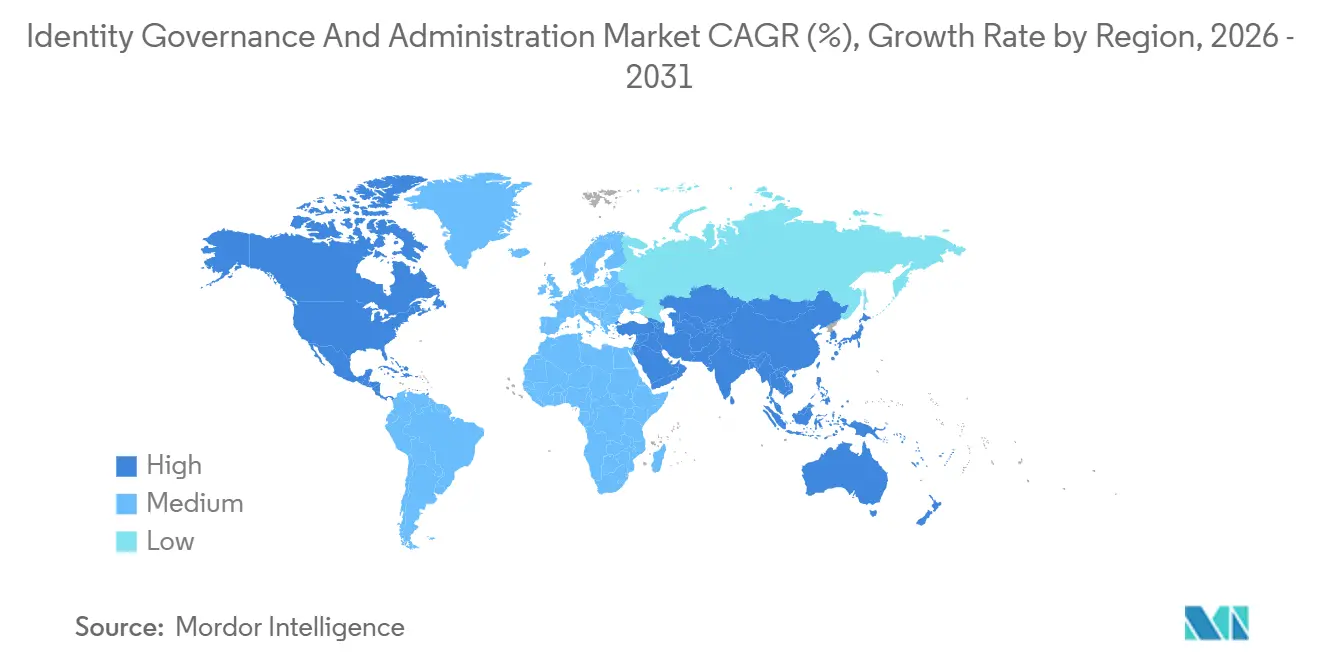

- By geography, North America captured 38.15% of global revenue in 2025, while Asia-Pacific is on track for a 13.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Identity Governance And Administration Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of AI-driven IGA for Continuous Access Certification | +2.8% | Global, with early traction in North America and Western Europe | Medium term (2-4 years) |

| Convergence of PAM and IGA Suites Among Highly Regulated Sectors in Europe | +2.1% | Europe, spillover to APAC financial hubs | Medium term (2-4 years) |

| Zero-Trust and Passwordless Initiatives Accelerating Role Mining Tools in North America | +2.5% | North America, expanding to APAC and Middle East | Short term (≤ 2 years) |

| M and A Activity Among Telcos Driving Telco-grade IGA Roll-outs in Asia-Pacific | +1.9% | Asia-Pacific core, emerging in Latin America | Medium term (2-4 years) |

| Sovereign-Cloud Mandates Fueling Domestic IGA Platforms in Middle East | +1.7% | Middle East, with policy influence in Africa and ASEAN | Long term (≥ 4 years) |

| ESG-Linked Vendor Assessment Requirements Pushing Audit-grade Identity Proof in Nordics | +1.4% | Nordic countries, expanding to broader EU under taxonomy regulations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of AI-Driven IGA for Continuous Access Certification

Organizations are embedding machine learning into access review workflows so anomalous entitlements are flagged in real time, replacing quarterly certification cycles with continuous evaluation. A 2025 survey covering 502 enterprises showed 68% plan AI-enabled access intelligence by 2027, yet just 22% have adequate data foundations, elevating demand for cleansing services.[1]Okta Inc, “State of Identity 2025,” OKTA.COM IBM incorporated natural-language processing to parse unstructured tickets, trimming manual triage by 40% in pilot programs.[2]IBM Corporation, “IBM Security Verify,” IBM.COM Vendors are positioning identity analytics platforms between traditional governance suites and security event tools to supply probabilistic risk scoring that improves remediation prioritization.

Convergence of PAM and IGA Suites Among Highly Regulated Sectors in Europe

European banks and utilities now favor unified architectures that link privileged session recording with upstream approval workflows, an approach codified in the European Banking Authority’s 2024 ICT risk guidelines.[3]European Banking Authority, “Guidelines on ICT Risk Management,” EBA.EUROPA.EU CyberArk and Saviynt launched converged modules in 2025, enabling just-in-time elevation and reducing duplicate directory costs by up to 20% in German insurance pilots. Spillover to Hong Kong and Singapore is visible as regulators adopt similar audit requirements.

Zero-Trust and Passwordless Initiatives Accelerating Role Mining Tools in North America

Federal zero-trust mandates compel agencies to map each entitlement to least-privilege roles before deploying phishing-resistant passkeys. The FIDO Alliance reported that 74% of enterprises rolling out FIDO2 credentials faced role-definition bottlenecks. Microsoft’s Entra suite introduced AI-assisted role recommendations in late 2025 that cluster historical usage data, helping merged entities reconcile conflicting catalogs within weeks rather than quarters.

M and A Activity Among Telcos Driving Telco-Grade IGA Roll-outs in Asia-Pacific

Consolidation across India, Indonesia, and the Philippines forces operators to reconcile subscriber identity stores that scale into the hundreds of millions. A 2024 Indonesian merger required harmonizing policies for 12,000 network engineers, exposing the limits of standard enterprise tools. Saviynt’s 2025 telecom edition introduced bulk-provisioning APIs processing millions of changes hourly. Similar patterns are emerging in Brazil and Mexico, where regulators tie merger approvals to robust lifecycle governance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skill Shortage in Identity Engineering Limiting Complex Deployments | -1.6% | Global, acute in North America and Western Europe | Short term (≤ 2 years) |

| API-Sprawl Elevating Integration Cost for Brownfield IT Environments | -1.3% | Global, pronounced in enterprises with legacy ERP | Medium term (2-4 years) |

| Fragmented Data-Residency Laws Slowing Global Rollouts for Multinationals | -1.1% | ASEAN, Latin America, Middle East, Africa | Long term (≥ 4 years) |

| Delayed ROI from Role-Based Access Clean-ups in Legacy ERP Estates | -0.9% | Global, concentrated in manufacturing and energy sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skill Shortage in Identity Engineering Limiting Complex Deployments

The cybersecurity workforce gap climbed to 4 million open positions in 2025, with identity engineering talent especially scarce. Sixty-two percent of surveyed organizations cited identity skill deficits as a top barrier to security maturity. Implementation timelines for multi-cloud IGA projects now stretch six to nine months, prompting vendors to release low-code configuration layers that still cannot fully replace specialized expertise.

API-Sprawl Elevating Integration Cost for Brownfield IT Environments

Heterogeneous estates often manage 187 applications and only 43% support standardized provisioning interfaces, forcing custom connectors that raise integration cost by 20%-30%. Legacy ERP authorization structures do not map neatly to attribute-based models, so enterprises maintain parallel governance streams that undermine the centralized promise of the Identity Governance And Administration market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as Complexity Outpaces Packaged Capabilities

The solutions segment dominated 2025 revenue yet enterprises increasingly realize that packaged functionality rarely covers bespoke brownfield scenarios. Services momentum stems from architecture redesign, connector development, and role-mining workshops that smooth migrations from on-premise directories to cloud-native platforms. Managed offerings appeal to mid-market buyers lacking deep identity skills, providing 24/7 campaign monitoring and quarterly rationalization reviews. Access certification software remains the largest sub-category because financial audits in BFSI demand demonstrable entitlement attestation.

Services growth at 13.71% annually underscores how mounting regulatory and operational complexity propels consultative spending. Providers now bundle licenses with outcome-based service level agreements that guarantee certification completion or automated remediation within fixed windows. This mix is expanding the Identity Governance And Administration market size for advisory firms while allowing software vendors to focus R and D on analytics and intelligent automation features.

By Deployment Mode: Cloud Leads While Hybrid Persists in Sensitive Sectors

Cloud captured 57.91% of 2025 spending and continues to climb thanks to elastic scalability and rapid onboarding benefits. Multi-tenant architectures from Microsoft and Okta shorten time-to-value, letting companies integrate thousands of SaaS applications through pre-built connectors. Sovereign-cloud mandates in the Middle East are reinforcing domestic data centers that still interoperate with global identity federations through privacy gateways.

Despite cloud enthusiasm, highly regulated operators maintain on-premise directories that store authentication secrets inside controlled facilities, producing hybrid blueprints where analytics engines run in the cloud. This design keeps sensitive attributes in country while enabling AI-driven anomaly detection services hosted remotely, sustaining diverse revenue streams inside the broader Identity Governance And Administration market.

By Enterprise Size: SMEs Accelerate Under Managed and Subscription Models

Large enterprises controlled 70.63% of 2025 revenue because of historical investments in complex developer workflows and compliance audits. However, small and medium enterprises are moving fastest, growing at a 13.83% CAGR as zero-trust frameworks become table stakes even for firms with fewer than 1,000 employees. Subscription pricing bundles licenses, deployment, and administration into predictable monthly costs that align with constrained capital budgets.

This democratization is reshaping vendor roadmaps toward intuitive interfaces, pre-configured policies, and automated update cadences that demand little internal oversight. Advanced analytics, session recording, and fine-grained attribute modeling remain hallmarks of enterprise editions. Still, the rising SME cohort widens the Identity Governance And Administration industry funnel by seeding future expansion opportunities when those customers scale.

By End-User Vertical: Retail Surges on Payment Security Pressures

BFSI retained 29.26% of 2025 spending by virtue of stringent segregation-of-duty mandates and heavy audit scrutiny. The most dynamic growth materializes in retail and e-commerce, which are advancing at a 13.88% CAGR after PCI DSS version 4.0 demanded just-in-time privileged access controls for cardholder data environments. Merchants embedding tokenization during checkout need automated role governance to protect payment APIs and satisfy quarterly attestations.

Telecommunications groups implement IGA to govern DevOps pipelines that deploy network functions as coded infrastructure, while healthcare providers adopt to comply with 21 CFR Part 11 electronic record rules. Energy utilities embrace governance to meet North American Electric Reliability Corporation standards for bulk power system integrity. These varied drivers together enlarge the Identity Governance And Administration market share of non-financial verticals, diversifying revenue bases for vendors.

Geography Analysis

North America’s revenue leadership in the Identity Governance And Administration market derives from mature regulatory frameworks, entrenched vendor ecosystems, and zero-trust mandates that keep federal agencies funding projects through late 2026. Canadian breach notification rules further motivate enterprises to harden entitlements and strengthen audit trails. Mexico’s banking sector incorporates role-based controls into payment systems, bolstering adoption beyond the United States and Canada. Skill shortages, particularly for hybrid Azure AD and on-premise directory synchronization, inflate professional service costs and occasionally defer go-lives.

Asia-Pacific delivers the fastest expansion as national identity projects intersect with private-sector modernization. India aligns consent-based data protection with policy engines baked into modern IGA suites. Indonesia and the Philippines require telecom operators to process subscriber modifications at country scale, driving demand for bulk-processing connectors. China’s Personal Information Protection Law forces multinational corporations to host identity instances domestically, prompting dual-platform architectures. Japan and Australia continue incremental growth under sector-specific security directives.

Europe shows consistent momentum, anchored by GDPR Article 32 and the Network and Information Security Directive 2. Converged PAM-IGA adoption reduces enterprise toolchains in banking and utilities while satisfying European Banking Authority guidelines. Germany’s updated cloud service rules and France’s threat-led penetration testing requirements deepen platform features around privileged session analytics. Nordic ESG procurement extends evaluation criteria to vendor sustainability disclosures, informing enterprise source-selection decisions and shaping product roadmaps.

Competitive Landscape

The Identity Governance and Administration market features moderate concentration because the top five suppliers collectively hold roughly 45%-50% of global revenue. Platform incumbents leverage pre-existing cloud and productivity footprints, embedding governance modules that raise switching costs and smooth cross-sell motions. Microsoft offers Entra functionality inside Microsoft 365 subscriptions, granting immediate reach into customer bases that already authenticate through Azure AD. SailPoint positions as a neutral orchestrator by emphasizing standards-based connectors into multi-cloud estates, limiting vendor lock-in for federated customers.

Mergers and acquisitions reshape portfolios as larger companies absorb niche players filling coverage gaps. Thales folded ForgeRock into hardware security module offerings that extend cryptographic roots-of-trust through governance workflows. Broadcom integrated Symantec assets, bundling endpoint protection with certification engines even though post-deal cultural differences have slowed synergy extraction. Startups such as Zilla Security and SecZetta differentiate by focusing on non-employee identities, a domain underserved by suites optimized for permanent staff.

Technology differentiation centers on artificial intelligence, graph databases, and natural-language interfaces. Saviynt and Omada embed AI role recommendations that compress attestation cycles, while IBM patents decentralize identity federation for zero-trust architectures. Emerging vendors adopt W3C Verifiable Credentials to future-proof against decentralized identity wallets. Consumption-based pricing models introduce revenue volatility yet lower purchase barriers for mid-market entrants, widening overall addressable demand while intensifying renewal competition among suppliers.

Identity Governance And Administration Industry Leaders

SAP SE

Microsoft Corporation

IBM Corporation

Oracle Corporation

Sailpoint Technologies Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Microsoft expanded Entra with AI-powered access recommendations and integration with Azure OpenAI Service to automate policy generation based on natural-language prompts.

- November 2025: SailPoint partnered with Amazon Web Services to embed Identity Security Cloud inside AWS Control Tower landing zones, trimming deployment time for regulated workloads by an estimated 40%.

- October 2025: CyberArk released Identity Security Platform 2.0, bringing just-in-time elevation policies that auto-revoke standing admin rights once tasks complete.

- September 2025: Okta published its State of Identity survey noting that 68% of enterprises plan AI-powered access intelligence by 2027 but only 22% have adequate data foundations.

Global Identity Governance And Administration Market Report Scope

Identity Governance and Administration is the centralized composition of access control and identity management practices often instituted to comply with government regulations and industry standards. For an organization, the main agenda for implementing Identity Governance and Administration (IGA) is to make sure that right people are getting the right access for the right reason at the right time. The report gives a detailed analysis of solutions and services offered on different deployment modes in various industries across the globe.

The Identity Governance And Administration Market Report is Segmented by Component (Solutions - Access Certification and Review, User Provisioning and De-provisioning, Privileged Governance, Password Management; Services - Professional Services, Managed Services), Deployment Mode (On-premise, Cloud), Enterprise Size (Large Enterprises, Small and Medium Enterprises), End-user Vertical (BFSI, IT and Telecom, Healthcare and Life Sciences, Energy and Utilities, Government and Public Defense, Manufacturing, Retail and e-Commerce), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Access Certification and Review |

| User Provisioning - De-provisioning | |

| Privileged Governance | |

| Password Management | |

| Services | Professional Services |

| Managed Services |

| On-premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| IT and Telecom |

| Healthcare and Life Sciences |

| Energy and Utilities |

| Government and Public Defense |

| Manufacturing |

| Retail and e-Commerce |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Solutions | Access Certification and Review |

| User Provisioning - De-provisioning | ||

| Privileged Governance | ||

| Password Management | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-premise | |

| Cloud | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By End-user Vertical | BFSI | |

| IT and Telecom | ||

| Healthcare and Life Sciences | ||

| Energy and Utilities | ||

| Government and Public Defense | ||

| Manufacturing | ||

| Retail and e-Commerce | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the Identity Governance And Administration market by 2031?

The market is forecast to reach USD 18.12 billion by 2031, driven by cloud deployment and continuous access certification demand.

How fast is the Identity Governance And Administration market expected to grow between 2026 and 2031?

It is set to expand at a 13.62% CAGR during the 2026-2031 period.

Which region will register the fastest growth through 2031?

Asia-Pacific is expected to post the quickest expansion with a 13.92% CAGR, propelled by national digital identity projects and telecom mergers.

Which component segment is rising the quickest?

Services are advancing at a 13.71% CAGR as enterprises seek consulting and managed assistance to tackle complex roll-outs.

Why are retail and e-commerce firms accelerating adoption?

Updated PCI DSS 4.0 payment-security rules require just-in-time privileged access governance, pushing merchants to deploy automated certification tools.

Page last updated on: