Vyndaqel Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

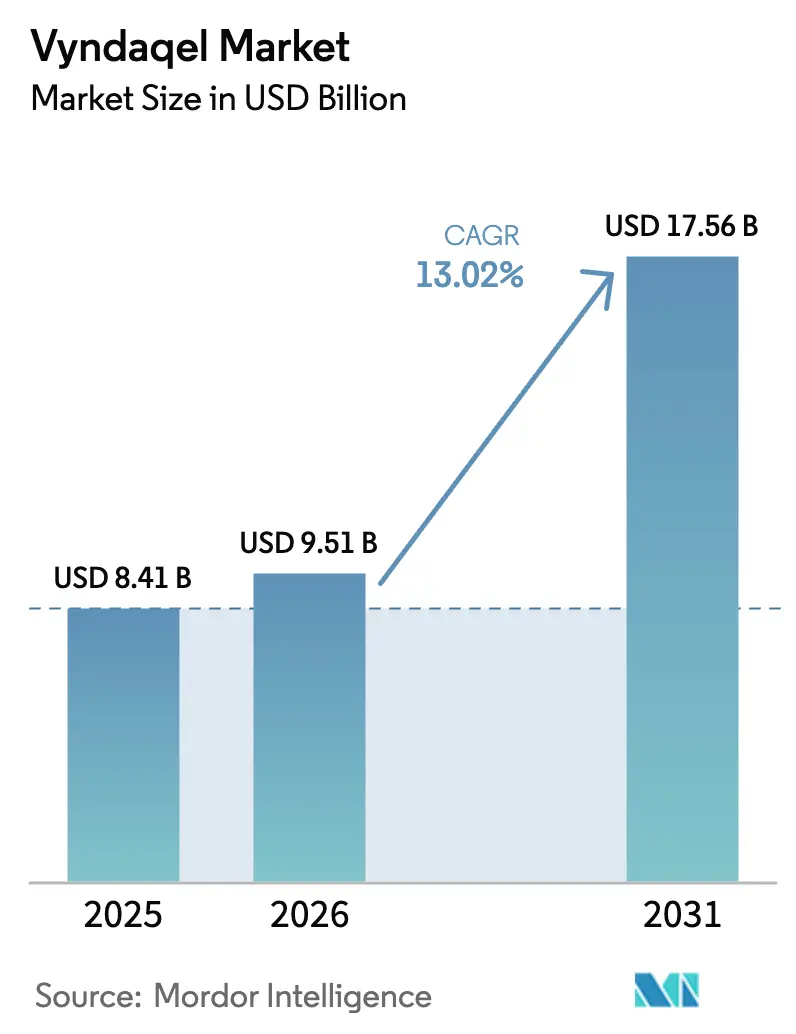

| Market Size (2026) | USD 9.51 Billion |

| Market Size (2031) | USD 17.56 Billion |

| Growth Rate (2026 - 2031) | 13.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vyndaqel Market Analysis by Mordor Intelligence

The vyndaqel market size is expected to grow from USD 8.41 billion in 2025 to USD 9.51 billion in 2026 and is forecast to reach USD 17.56 billion by 2031 at 13.02% CAGR over 2026-2031. Growing diagnosis rates, broader reimbursement and a sustained pivot from palliative management to disease-modifying therapy continue to widen the treated population. Pfizer’s tafamidis shows durable reductions in cardiovascular death and hospitalization, anchoring first-line use while encouraging earlier referral to specialized amyloidosis centres. Breakthrough designations for next-generation competitors, artificial-intelligence screening that now shortens the diagnostic journey to mere hours and rapid centre-of-excellence roll-outs collectively accelerate addressable demand. Competitive pressure is mounting as RNA-interference, gene-silencing and single-dose CRISPR candidates progress through late-stage pipelines, but these entrants also deepen market awareness and expand therapeutic choice. Payer acceptance is gradually improving; Medicare spending quadrupled between 2019 and 2021, and private insurers are adopting value-based frameworks that balance high list prices with measurable outcome gains.

Key Report Takeaways

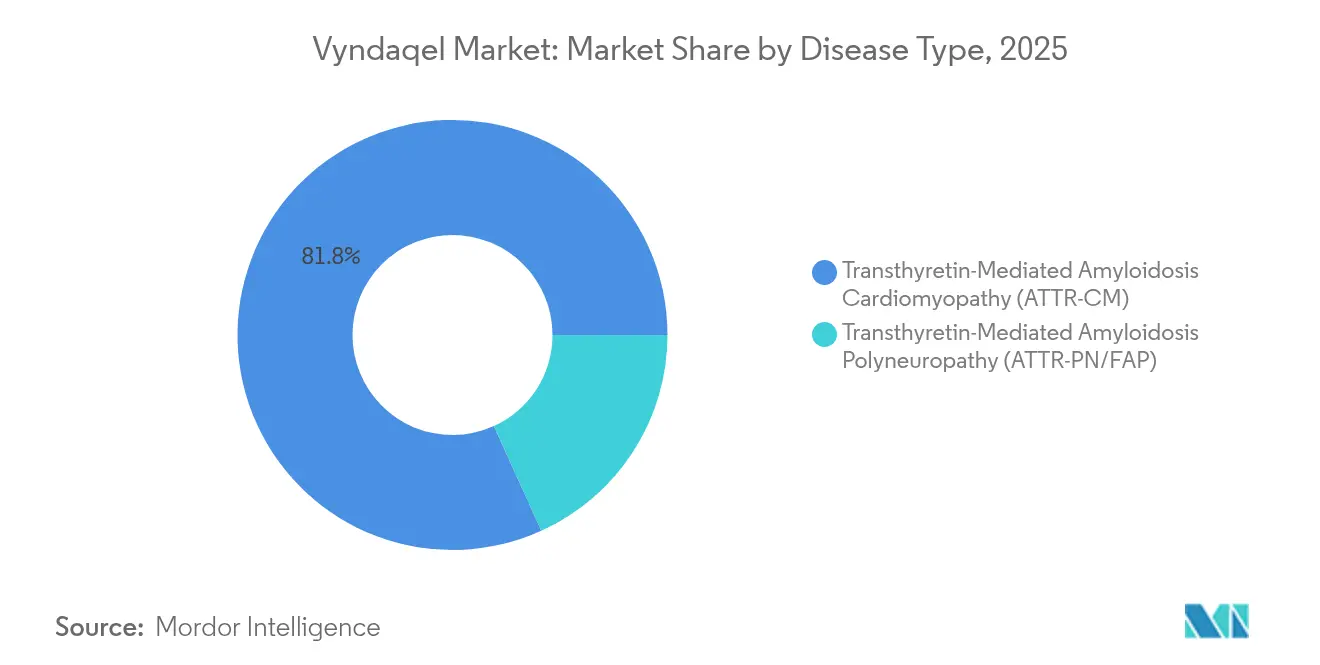

- By disease type, ATTR-CM held 81.78% of vyndaqel market share in 2025. ATTR-PN/FAP is projected to advance at a 15.12% CAGR between 2026-2031.

- By patient setting, inpatient care accounted for 67.95% of the vyndaqel market size in 2025. Outpatient treatment is expanding at a 15.05% CAGR through 2031.

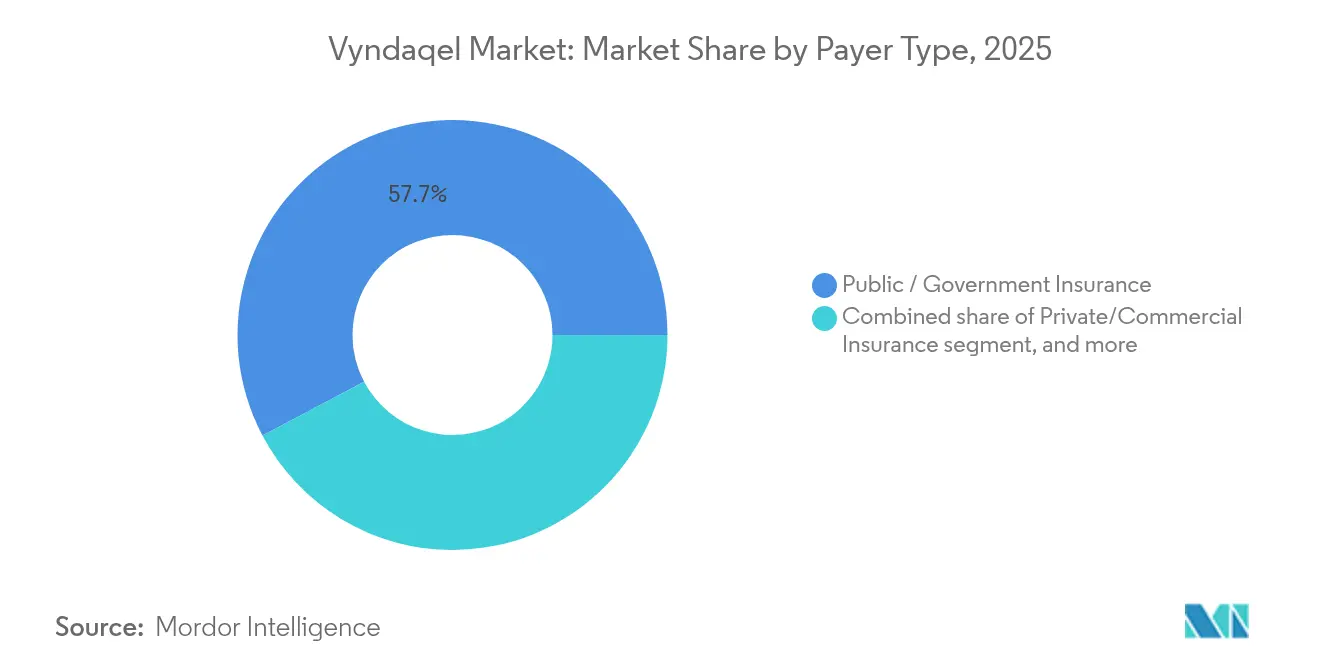

- By payer type, public and government programmes made up 57.74% of 2025 revenue. Private insurance shows the fastest growth at 15.33% CAGR to 2031.

- By distribution channel, hospital pharmacies led with 60.82% share in 2025. Online and specialty pharmacies are rising at a 16.02% CAGR over the forecast window.

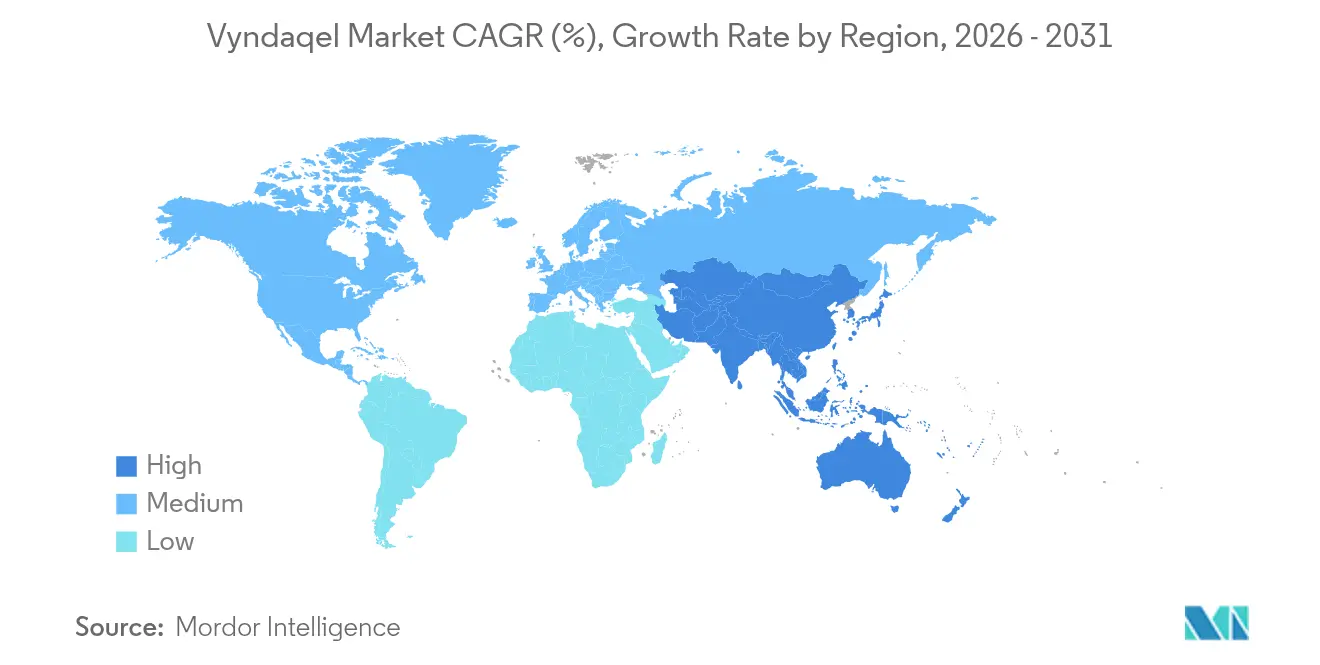

- By geography, North America commanded 41.95% revenue share in 2025. Asia-Pacific is the quickest-growing region at a 14.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vyndaqel Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing disease awareness and diagnosis rates | +2.8% | Global, strongest in North America & Europe | Medium term (2-4 years) |

| Regulatory approvals and orphan-drug incentives | +2.1% | United States & European Union | Short term (≤2 years) |

| Favorable reimbursement and cost-sharing policies | +1.9% | North America, Europe, selective Asia-Pacific markets | Medium term (2-4 years) |

| Expansion of specialized amyloidosis treatment centers | +1.6% | Global, rapid build-out in Asia-Pacific | Long term (≥4 years) |

| Emerging non-invasive diagnostic technologies | +1.4% | Early adoption in developed markets | Medium term (2-4 years) |

| Growing aging population and cardiac disease burden | +1.2% | Developed economies worldwide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Increasing Disease Awareness and Diagnosis Rates

Machine-learning algorithms embedded in electronic-health-record systems now identify high-risk patients within 12 hours, a striking acceleration compared with the historical 8.6-year diagnostic delay. Pfizer and academic collaborators have reported 93% sensitivity when screening heart-failure records, a performance mirrored by Mayo Clinic’s ATTR-CM score that gives non-specialists a practical triage tool. Genetic testing campaigns uncover hereditary variants, broadening the treatable pool beyond previously recognised cohorts. Continuous medical-education initiatives for cardiologists and neurologists cut misdiagnosis rates that once exceeded one-third of cases. Advocacy groups reinforce outreach in regions where amyloidosis awareness is still nascent, ensuring that improved tools translate into real-world identification.

Regulatory Approvals and Orphan Drug Incentives

Seven-year market exclusivity in the United States and 10-year protection in Europe remain powerful catalysts for innovation. Intellia’s CRISPR candidate nexiguran ziclumeran received Regenerative Medicine Advanced Therapy status in 2025, accelerating review timelines. In parallel, Europe cleared BridgeBio’s acoramidis, the first near-complete stabiliser, setting a new efficacy benchmark. Breakthrough Therapy designations now extend to diagnostics such as Attralus’ PET agent, underscoring regulator commitment across the care continuum. Nevertheless, looming patent expiry for tafamidis between 2025-2026 foreshadows generic entry, injecting cost competition into a premium-priced arena.

Favorable Reimbursement and Cost-Sharing Policies

Patient-assistance initiatives mitigate affordability gaps: 35% of Medicare tafamidis users rely exclusively on such programmes, and a further 14% blend them with public coverage. Australia’s Pharmaceutical Benefits Scheme recently listed therapy for hereditary polyneuropathy, strengthening Asia-Pacific precedent. Out-of-pocket spend per Medicare patient has fallen from USD 738.34 in 2019 to USD 505.59 in 2021, yet absolute burden remains high relative to beneficiary income. Private-payer uptake is rising alongside outcomes-based contracts that link reimbursement to functional gains. As total US public spending nears USD 1 billion annually, value-based negotiations are intensifying.

Expansion of Specialized Amyloidosis Treatment Centres

Mayo Clinic now manages more than 2,500 cases per year, while Heidelberg University Hospital treats 1,500, illustrating global scaling of expert hubs. International Cardio-Oncology Society standards promote multidisciplinary teams and shared protocols, curbing regional variance in outcomes. Cleveland Clinic’s centre-of-excellence designation fosters trial access and standardised care, and Royal Free London’s National Amyloidosis Centre aligns prescribing with NICE guidance. Rapid centre expansion in Asia-Pacific mirrors rising diagnosis; newly accredited units in Japan, South Korea and Australia bridge historical access gaps.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy cost and cost-effectiveness concerns | -3.2% | Global, most acute in price-sensitive markets | Medium term (2-4 years) |

| Competitive pipeline of alternative therapies | -2.1% | Developed markets with advanced healthcare systems | Short term (≤2 years) |

| Limited diagnosis infrastructure in developing regions | -1.5% | Latin America, Africa, parts of South & Southeast Asia | Long term (≥4 years) |

| Potential drug price negotiations and policy pressures | -1.3% | Global, led by US and EU payers | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Therapy Cost and Cost-Effectiveness Concerns

ICER calculations indicate tafamidis would need a 96% price cut from its USD 268,000 list price to hit traditional cost-effectiveness thresholds. Medicare expenditure escalated from USD 141.8 million in 2019 to USD 655.9 million by 2021, a trajectory policymakers view as unsustainable. The US Department of Veterans Affairs is piloting dose-optimisation protocols that could lower spending without compromising efficacy. Health-economic evaluation is complicated by limited quality-of-life metrics for rare diseases, but payers are demanding clearer evidence of value for money. These dynamics fuel pressure for risk-sharing contracts and prompt consideration of reference pricing in many countries.

Competitive Pipeline of Alternative Therapies

Acoramidis reached ≥90% transthyretin stabilisation and cut mortality plus hospitalisation by 42% in Phase 3 studies, raising physician expectations. Alnylam’s RNA-interference agent Amvuttra gained FDA approval in March 2025 with a 36% overall mortality benefit, while Intellia’s single-dose CRISPR therapy posts 90% serum TTR knock-down and moves into Phase 3 megatrials[1]New England Journal of Medicine, “CRISPR-Cas9 for Transthyretin Amyloidosis,” nejm.org. Each modality promises differentiated profiles—less frequent dosing, deeper biomarker response or curative intent—that could erode tafamidis volumes. Conversely, broader therapeutic choice might expand the treated base, partially offsetting share dilution for incumbent brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: ATTR-CM Dominance Drives Market Leadership

ATTR-CM generated 81.78% of 2025 revenue, underpinned by its high prevalence among ageing populations and well-established cardiology referral pathways. The Vyndaqel market size for this segment is projected to rise steadily through 2031 as earlier diagnosis enlarges the eligible pool. Wild-type ATTR-CM alone affects roughly 400,000 individuals worldwide and carries a median untreated survival of 2–3.5 years, underscoring the urgency for therapy. Hereditary phenotypes present at younger ages, creating lifelong treatment trajectories that support long-run revenue stability.

ATTR-PN/FAP expands at a 15.12% CAGR thanks to RNA-interference launches such as Amvuttra and Wainua, both of which address neural impairment. Genetic screening now routinely identifies mutations like V30M and V122I, broadening detection beyond historical clusters. Non-invasive cardiac scintigraphy also differentiates cardiac from mixed phenotypes, guiding therapy selection. As a result, physicians are adopting a more segmented approach: stabilisers remain core for pure cardiomyopathy, while gene-silencing agents gain traction in neuropathic cases. Commercial uptake in ATTR-PN therefore complements, rather than cannibalises, the ATTR-CM-centric Vyndaqel market.

By Patient Setting: Outpatient Shift Accelerates Care Delivery

Inpatient settings still accounted for 67.95% of 2025 administrations, reflecting the need for baseline monitoring at therapy initiation. However, the outpatient share of the Vyndaqel market is expanding rapidly on the back of oral dosing convenience and standardised protocols that enable community follow-up. Amyloidosis centres are reconfiguring infusion suites to support routine vutrisiran delivery, while reserving beds for acute decompensation or complex comorbidity management.

Telemedicine and home-based monitoring devices further tilt the balance toward outpatient care. Patients value reduced travel and shorter wait times, while providers benefit from lower overheads within value-based payment models. Health-system data show that proactive outpatient management cuts emergency-department visits, reinforcing payer support. As these efficiencies accumulate, the Vyndaqel market share of inpatient care is expected to contract gradually despite overall demand growth.

By Payer Type: Private Insurance Adoption Accelerates

Public coverage—principally Medicare and Medicaid—delivered 57.74% of 2025 revenue as ATTR-CM skews toward older adults. The absolute Vyndaqel market size funded by government programmes will keep rising because of demographic ageing, yet commercial payers are the faster-growing slice. Employer plans recognise productivity gains from symptom control and are incorporating rare-disease carve-outs that streamline authorisation.

Outcomes-based contracts are emerging in the United States and Germany, aligning reimbursement with six-minute-walk improvements and NT-proBNP reduction. Patient-assistance schemes remain vital, cushioning high co-pays and keeping discontinuation rates low. In low-to-middle-income markets, hybrid funding that blends charitable foundations with limited government subsidy is becoming more common, gradually lifting treatment penetration.

By Distribution Channel: Specialty Pharmacies Transform Access Models

Hospital pharmacies retained 60.82% share in 2025 because many centres initiate and dispense therapy on-site to manage complex logistics. Nonetheless, specialty pharmacies are the fastest-expanding conduit, capturing patients who prefer doorstep delivery and 24/7 support. This shift lifts adherence and gives manufacturers richer real-world data through dedicated hubs, advantages that resonate in a competitive landscape.

Cold-chain integrity and REMS-aligned counselling protocols pose barriers for standard retail outlets but align well with specialty-pharmacy infrastructure. Digital apps integrated into these channels remind patients to take tafamidis, schedule lab tests and connect with nurse educators. Consequently, the relative Vyndaqel market share of specialty pharmacies is poised to climb throughout the forecast horizon.

Geography Analysis

North America led with 41.95% revenue in 2025, supported by advanced diagnostic infrastructure, strong academic-medical-centre networks and broad reimbursement coverage. US Medicare spend on tafamidis surged from USD 141.8 million in 2019 to USD 655.9 million in 2021, underscoring steep volume uptake. Canada offers nationalised coverage via provincial formularies, while Mexico is building new amyloidosis clinics albeit constrained by budgetary limits. Leading North American sites such as Mayo and Cleveland Clinic treat thousands annually, run pivotal trials and pioneer AI-based screening that other regions emulate.

Europe contributes a sizeable portion of the Vyndaqel market, anchored by specialist hubs in Germany and the United Kingdom. Heidelberg University Hospital treats the continent’s largest cohort, whereas the UK’s National Amyloidosis Centre follows NICE guidelines that place tafamidis on formulary for eligible cardiomyopathy cases. BridgeBio’s partnership with Bayer accelerates acoramidis launch, harnessing Europe’s cross-border regulatory alignment under the EMA. Reimbursement is generally comprehensive, but budget caps in Italy and Spain may temper uptake growth relative to Germany or France.

Asia-Pacific is the fastest-growing territory at a 14.32% CAGR, adding meaningful volume to the Vyndaqel market size. Japan’s PMDA has cleared multiple agents, giving clinicians broad choice, while Australia’s Pharmaceutical Benefits Scheme listing for hereditary polyneuropathy creates an important precedent. China is mapping ATTR mutation prevalence and expanding nuclear-medicine capacity, yet high out-of-pocket costs limit immediate penetration. India, South Korea and Taiwan are rolling out dedicated amyloidosis clinics and public-private diagnostic projects. As population ageing accelerates, APAC’s contribution to global revenue will expand despite heterogeneous reimbursement environments.

Competitive Landscape

Pfizer generated USD 3 billion from tafamidis in 2023, but exclusivity wears thin from May 2026, inviting generic competition. Meanwhile, Alnylam secured FDA clearance for Amvuttra in March 2025, becoming the first RNA-interference therapy for both cardiomyopathic and neuropathic manifestations. Its 36% mortality benefit positions it as a formidable rival. BridgeBio’s Attruby reached market late-2024 and reported USD 36.7 million first-quarter sales, outpacing analyst forecasts. New entrants do not merely split demand; they magnify attention on transthyretin amyloidosis and grow the total addressable market.

Mechanistic diversity is now a defining trait. Stabilizers such as tafamidis and acoramidis compete against gene-silencing and gene-editing modalities. Intellia’s CRISPR programme offers single-dose potential, challenging the chronic-dosing premise that underpins stabilizer economics. Diagnostics are part of the arms race: Attralus’ PET imaging agent received Breakthrough Therapy Designation, giving it an expedited path to market and strengthening the combined treatment-diagnosis value proposition.

Strategic alliances are proliferating. BridgeBio licensed European rights to Bayer, widening its commercial footprint without incurring full infrastructure cost. Pfizer is integrating AI screening partnerships with academic health systems to defend share by speeding diagnosis and treatment initiation. Alnylam is investing in real-world evidence to demonstrate long-term functional gains, a critical differentiator in cost-effectiveness debates. The competitive scene, therefore, is intensifying but also expanding overall opportunity.

Vyndaqel Industry Leaders

Pfizer Inc.

Alnylam Pharmaceuticals

Ionis Pharmaceuticals / AstraZeneca

BridgeBio Pharma (Eidos)

Intellia Therapeutics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Alnylam Pharmaceuticals received FDA approval for AMVUTTRA (vutrisiran), the first RNAi therapy approved for both cardiac and polyneuropathy ATTR manifestations.

- March 2025: Intellia Therapeutics gained FDA Regenerative Medicine Advanced Therapy designation for nexiguran ziclumeran, expediting a CRISPR-based single-dose treatment.

- November 2024: BridgeBio Pharma secured FDA approval for Attruby (acoramidis) after Phase 3 trials showed a 42% reduction in all-cause mortality and cardiovascular hospitalization.

- November 2024: The European Commission approved acoramidis (Beyonttra) and triggered a USD 75 million milestone payment to BridgeBio from Bayer.

- August 2024: Attralus received FDA Breakthrough Therapy Designation for 124I-evuzamitide, a pan-amyloid PET imaging agent.

- August 2024: Australia’s Pharmaceutical Benefits Scheme listed therapies for hereditary ATTR-PN, expanding access across the country.

Global Vyndaqel Market Report Scope

As per the scope of the report, Vyndaqel (Tafamidis meglumine) stabilizes the transthyretin protein to combat transthyretin amyloid cardiomyopathy (ATTR-CM). By preventing the breakdown of this protein, Vyndaqel curbs the formation of harmful amyloid deposits in the heart. As a result, it significantly lowers the chances of death and hospitalization for adults grappling with either wild-type or hereditary ATTR-CM. The Vyndaqel market is segmented by disease type, distribution channel, and geography. By disease type, the market is segmented into transthyretin-mediated amyloidosis cardiomyopathy, and familial amyloid polyneuropathy. By distribution channel, the market is segmented into hospital pharmacies, online pharmacies, and retail pharmacies. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Transthyretin-Mediated Amyloidosis Cardiomyopathy (ATTR-CM) |

| Transthyretin-Mediated Amyloidosis Polyneuropathy (ATTR-PN/FAP) |

| Inpatient Use |

| Outpatient Use |

| Public / Government Insurance |

| Private / Commercial Insurance |

| Self-Pay / Out-Of-Pocket |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online / Specialty Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease Type | Transthyretin-Mediated Amyloidosis Cardiomyopathy (ATTR-CM) | |

| Transthyretin-Mediated Amyloidosis Polyneuropathy (ATTR-PN/FAP) | ||

| By Patient Setting | Inpatient Use | |

| Outpatient Use | ||

| By Payer Type | Public / Government Insurance | |

| Private / Commercial Insurance | ||

| Self-Pay / Out-Of-Pocket | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online / Specialty Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Vyndaqel market in 2026 and how fast will it grow to 2031?

The market totals USD 9.51 billion in 2026 and is projected to reach USD 17.56 billion by 2031, reflecting a 13.02% CAGR over 2026-2031.

Which disease segment dominates current sales?

ATTR-CM accounts for 81.78% of 2025 revenue, making it the largest contributor to overall demand.

What region is expanding fastest?

Asia-Pacific posts the quickest growth, with a 14.32% CAGR driven by new approvals and centre-of-excellence expansion.

How is the competitive landscape evolving?

New entrants including RNA-interference and CRISPR-based therapies are gaining approvals, creating mechanism diversity and intensifying competition.

What is the primary barrier to wider therapy adoption?

Therapy cost remains the key hurdle; traditional cost-effectiveness metrics suggest tafamidis pricing must fall considerably to meet payer thresholds.

Are outpatient settings becoming more important?

Yes. Outpatient care is growing at 15.05% CAGR as oral dosing and telemedicine enable community management, shifting treatment away from inpatient wards.

Page last updated on: