Household Composters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

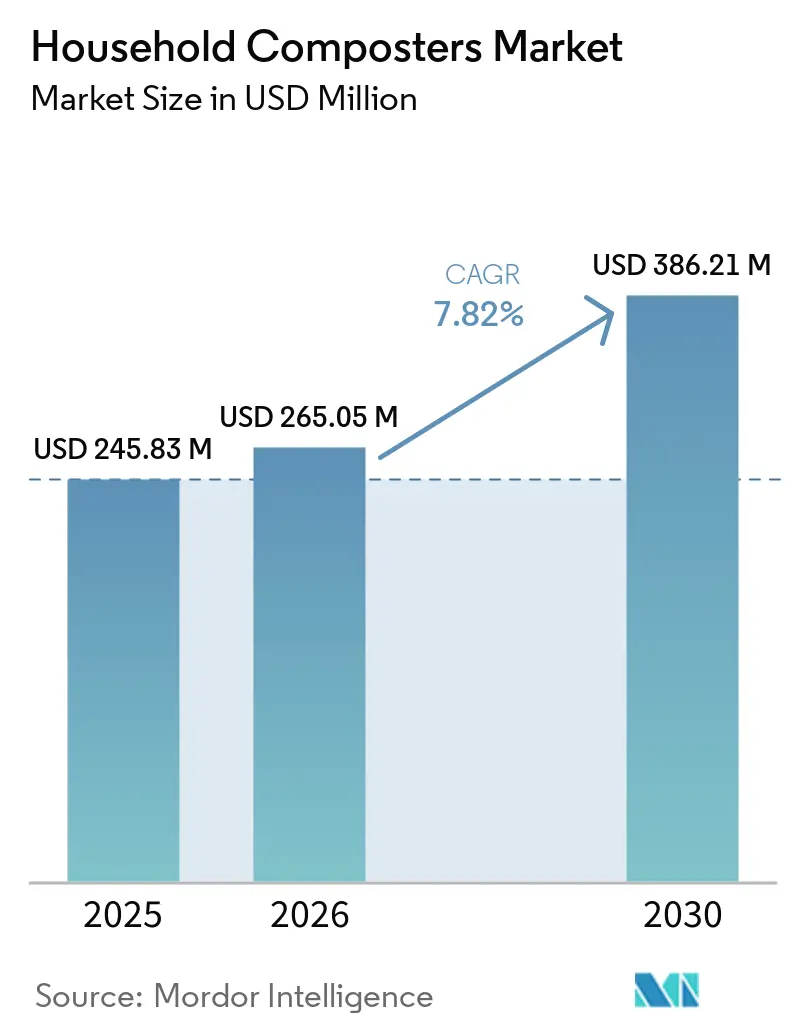

| Market Size (2026) | USD 265.05 Million |

| Market Size (2030) | USD 386.21 Million |

| Growth Rate (2025 - 2031) | 7.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Household Composters Market Analysis by Mordor Intelligence

The household composters market size is expected to grow from USD 245.83 million in 2025 to USD 256.05 million in 2026 and is projected to reach USD 386.21 million by 2031, at a CAGR of 7.82% over 2026-2031. State, national, and regional rules are shifting household practices toward source-separated organics, with California’s SB 1383 driving compliance activities and procurement requirements for recovered organics-derived products. Washington State will require year-round organics collection for all residential customers in designated ORCA zones by April 2027, clarifying obligations and timelines that strengthen curbside programs. The United States EPA’s Solid Waste Infrastructure for Recycling program will distribute up to USD 275 million to expand composting and related systems, with awards continuing into 2026. The European Union’s Regulation 2025/40 sets harmonized home-composting standards by February 2026 and mandates industrial composting compatibility for specific single-serve products and fruit labels by February 2028, signaling a step-change in packaging and at-home processing alignment. Technology improvements are addressing pain points that have held back the home composting solutions market, including sensor-driven maturity prediction with near-90% accuracy and permanent metal-ion odor filtration that eliminates the need for replacement cartridges [1]GEME, “GEME Terra 2: Fast, Odor-Free Kitchen Composter,” GEME, geme.bio.

Key Report Takeaways

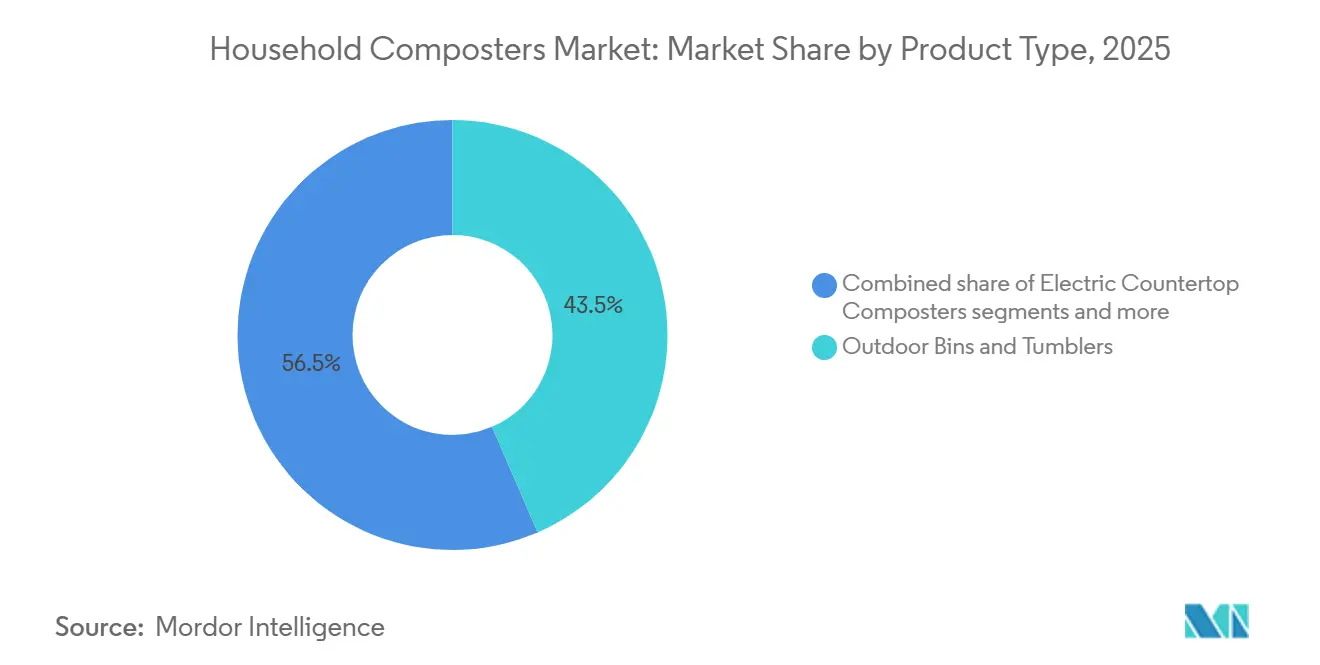

- By product type, Outdoor Bins & Tumblers led with 43.52% revenue share in 2025, while Electric Countertop Composters are forecast to expand at an 8.55% CAGR over 2026-2031.

- By capacity, the less than 20 L segment accounted for a 47.29% share in 2025, and the 20–50 L segment is projected to grow at a 9.62% CAGR through 2031.

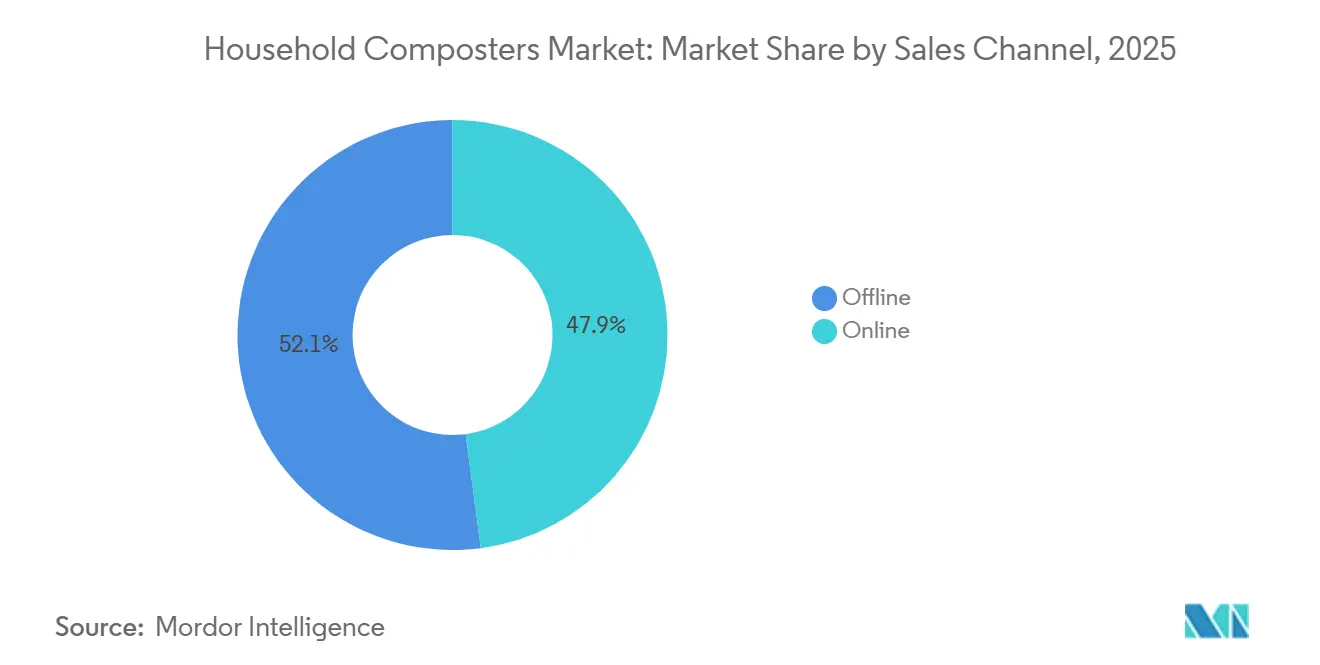

- By distribution channel, Offline held 52.09% of sales in 2025, and Online is set to advance at a 10.25% CAGR through 2031.

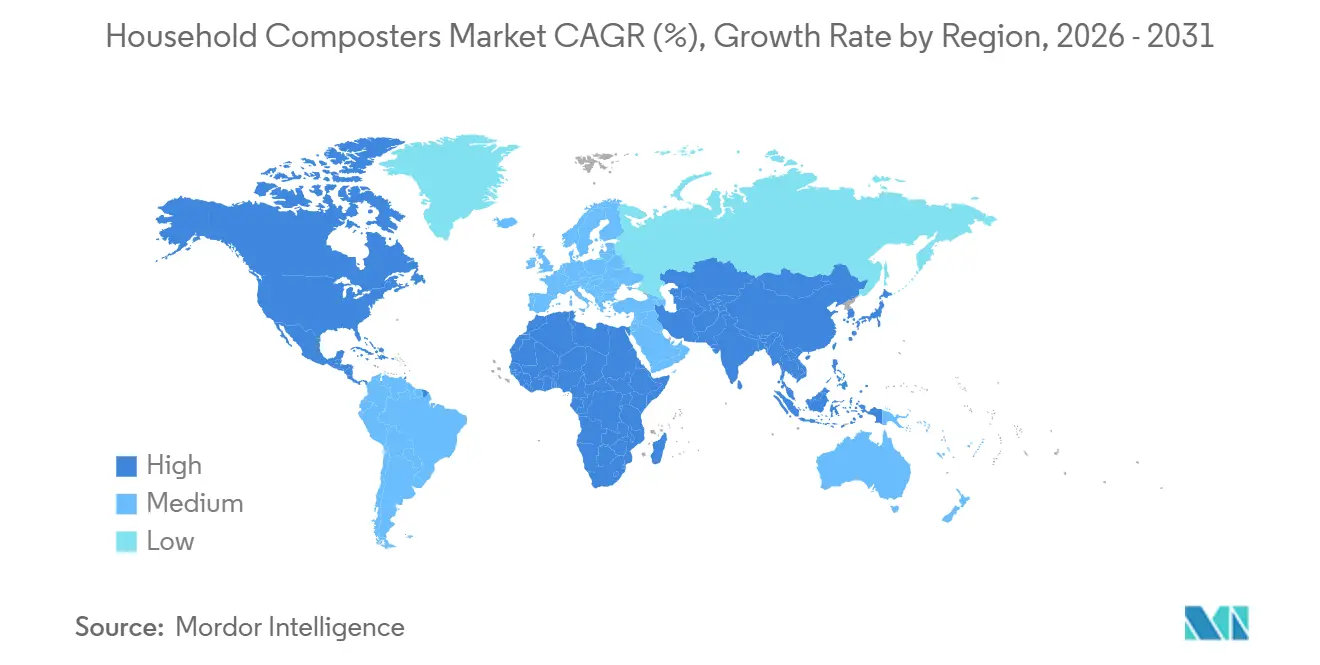

- By geography, North America captured 35.39% share in 2025, while Asia-Pacific is forecast to post the fastest growth at an 8.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Household Composters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Regulations and Organic Waste Diversion Mandates | +2.1% | Global, with early enforcement in California, Washington State, the EU-27, and South Korea | Short term (≤ 2 years) |

| Rising Environmental Awareness and Zero-Waste Initiatives | +1.8% | North America and the EU, spill-over to urban Asia-Pacific, including Japan and South Korea | Medium term (2-4 years) |

| Increasing Consumer Demand for Sustainable Living Practices | +1.5% | Global, strongest in high-income urban clusters | Medium term (2-4 years) |

| Growth Of Compact Electric and Countertop Composters for Urban Households | +1.4% | North America, Western Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Advancements In Odor Control, IoT, And Smart Composting Technologies | +1.0% | Global, led by North America and East Asia innovation hubs | Short term (≤ 2 years) |

| Municipal Subsidies and Incentives for Home Composting | +0.7% | National and local, with early gains in Japan, Washington State, and New York State | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Regulations and Organic Waste Diversion Mandates Accelerate Household Adoption

Mandates are moving home composting from an optional behavior to a routine part of household waste management within the home composting solutions market. California’s SB 1383 sets a 75% reduction target for organic waste by 2025 and compels local procurement of recovered organics-based products, helping normalize home composting alongside municipal programs. Washington State’s 2024 law requires year-round residential organics collection in designated zones by April 2027, with exemptions only for households that compost on-site or self-haul, reinforcing a preference for source separation at the household level. The EU’s Regulation 2025/40 will harmonize home-composting standards by February 2026 and require compostability labeling for select items by February 2028, thereby strengthening consumer confidence that home units can handle compliant materials. Japan’s national goal to cut food loss by 2030 aligns with city-level support, such as Inagi City’s reimbursement of up to 10,000 yen for electric composters, which reduces upfront cost barriers for households. South Korea’s RFID-based collection systems, which charge residents by weight, have supported very high food waste recycling rates while reinforcing household habits that also benefit at-home solutions. Together, these actions place the home composting solutions market closer to compliance-driven demand rather than discretionary purchasing.

Rising Environmental Awareness and Zero-Waste Initiatives Drive Consumer Behavior Shifts

United States federal priorities now frame food waste reduction as a climate strategy, which lifts the profile of home composting in household decision-making within the home composting solutions market. The United States EPA’s national strategy targets a 50% reduction in food loss and waste by 2030 and directs funding and guidance toward organics recycling, which strengthens local program economics and communications. Zero Waste Europe reports that community pilots with backyard composting have prevented substantial tonnage from landfills in participating areas, suggesting that structured local engagement can unlock high household participation and measurable diversion[2]European Parliament and Council, “Regulation (EU) 2025/40 on Packaging and Packaging Waste,” Official Journal of the European Union, valipac.academy. In Japan, a 2025 study found strong environmental values but limited at-home composting, indicating that convenience and social norms, rather than interest, explain the gap and that well-designed electric units can convert intent to action. Shenzhen’s experience in China shows that as infrastructure and communications improve, sorting and collection performance can rise sharply, complementing household-scale solutions when residents want faster or odor-free options at home. Community composting operations in the United States have also become more financially resilient, with sector surveys showing more sites achieving positive revenue, validating the overall ecosystem that households rely on to close nutrient loops. These factors align the home composting solutions market with broader waste prevention, climate, and circular economy priorities in 2026.

Increasing Consumer Demand for Sustainable Living Practices Elevates Home Composting to Lifestyle Category

Home composting is evolving into an accessible household routine, supported by design-forward devices that fit modern kitchens and daily schedules across the home composting solutions market. Devices such as the 12L Moreborn MB12 operate in always-on modes with WiFi diagnostics, keeping microbial systems active and allowing remote oversight for users familiar with other smart home devices. The willingness to pay for electric units has risen because these devices control odors and reduce processing time from weeks to hours, making composting achievable in small apartments as well as in detached homes. India’s Solid Waste Management Rules and municipal programs continue to push source separation and composting, helping normalize at-home solutions and increasing awareness of basic composting practices, even in large multifamily buildings. Subscription consumables for filters and microbial agents also help smooth the customer experience over time, much like other household devices that use refills to maintain performance. This consumer shift places the home composting solutions market at the intersection of sustainability, convenience, and connected living.

Growth of Compact Electric and Countertop Composters for Urban Households Addresses Space Constraints

Tight urban living spaces create strong product-market fit for compact electric units that can sit on counters or under cabinets, which is why this category is outpacing the broader home composting solutions market. The GEME Terra 2 demonstrates how premium models minimize footprint and noise while processing several kilograms of feedstock daily, supporting continuous use without odor between municipal pick-ups. FoodCycler’s Eco 3, launched in 2024 with a 3.5L chamber, targets renters and small households without outdoor bins or tumblers, easing adoption by reducing mess and time requirements. Countries with high urban density, like Japan, report low. Still, the growing adoption of home composting suggests that apartment dwellers need compact, low-odor, low-effort devices rather than traditional bins in shared or limited spaces. South Korea’s widespread RFID-based organics systems show that automation removes friction from handling food waste. This principle also supports interest in electric units that automate odor, temperature, and moisture. Home devices also address gaps in curbside programs that collect every other week, since households can process waste continuously rather than storing wet waste that can attract pests or create odors. This convenience advantage continues to expand the home composting solutions market in dense urban centers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of consumer awareness | -0.9% | Global, acute in rural areas and developing regions | Medium term (2-4 years) |

| High initial equipment costs and maintenance issues | -1.2% | Global, most pronounced in emerging markets | Short term (≤ 2 years) |

| Unpleasant odors, pest problems, and difficulty in composting food waste | -0.8% | North America, Europe, urban Asia | Short term (≤ 2 years) |

| Availability of alternative waste management solutions | -0.6% | North America, Europe, and commercial hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Consumer Awareness Limits Market Penetration in Untapped Demographics

Information gaps still limit the adoption of home composting solutions, especially in areas with uneven local communication or transient residents. In Japan, a national survey found that many households lacked prior composting experience, and awareness of support programs correlated with higher participation, suggesting untapped potential where outreach is minimal. Municipal planning documents often mention composting but do not provide a practical connection to end uses or household guidance, which leads to tactical confusion for residents and small businesses that want to participate. For households that would benefit from equipment rebates, information is sometimes siloed on city websites or in forms that are not widely promoted, which inhibits uptake by eligible residents. These dynamics narrow the addressable audience to early adopters and sustainability enthusiasts, rather than the broader population that would engage if programs, devices, and benefits were more widely communicated. Over time, sustained communication and school-based learning can normalize composting basics, so household interest converts into consistent buying in the home composting solutions market.

High Initial Equipment Costs and Maintenance Issues Create Affordability Barriers

Electric units in the home composting solutions market often cost several hundred dollars, which delays adoption for budget-conscious households or those uncertain about long-term use. There are quality differences across models, with lab tests indicating that some lower-cost machines fail after a few cycles. At the same time, mid-premium devices maintain performance, making low initial prices a risky proposition if early failures lead to replacements. Consumables can add to total cost if units rely on activated carbon filters or periodic microbe refills, which encourages households to compare these expenses to curbside collection fees or drop-off options. Sector guidance in India notes that multi-family buildings and housing societies can reach reasonable paybacks when municipalities co-fund pilots, although program access and application processes vary by city. When subsidies reduce capital costs and include training, households are more likely to adopt and continue using devices, indicating that structured support can mitigate affordability concerns in the home composting solutions market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Electric Countertop Composters Capture Premium Urban Demographics

Outdoor Bins & Tumblers held 43.52% of the home composting solutions market share in 2025, reflecting affordability and the fit for households with yards that can host passive bins and tumblers. The category remains popular among gardeners who value soil health and do not need rapid processing, and it aligns with community education programs that teach traditional composting methods. Electric Countertop Composters, projected to grow at 8.55% CAGR over 2026-2031, are rising faster because they address space, odor, and time barriers with cycle times measured in hours. Devices like GEME Terra 2 complete processing in 6-8 hours, feature permanent metal-ion odor filtration, and fit on the counter or under a cabinet. FoodCycler’s Eco 3, launched in 2024 with patented grinding that can handle bones and shells, broadens the acceptable input range beyond what many outdoor piles can handle. Worm and vermicompost bins have a stable niche, serving balcony users and those who want high-quality castings, and are now benefiting from selective technology upgrades such as smarter feeding and environmental monitoring. As packaging rules evolve and labeling tightens under EU Regulation 2025/40, certified electric units are likely to benefit from clearer compatibility claims that guide household buying in the home composting solutions market.

Against this backdrop, electric units position composting as a kitchen appliance rather than a yard activity, attracting urban residents who want cleaner counters and flexible schedules. The convenience premium and lower mess shift the audience from hobbyists to mainstream adopters who want control over odors and contamination. Established brands are emphasizing user experience through app-enabled notifications, easy loading and cleaning, and consistent outputs, while premium models pursue differentiation through permanent filtration and lower consumable costs. Traditional outdoor systems will continue to appeal to value-focused buyers who enjoy gardening and want soil volume at the lowest price. Still, the performance and convenience gains of electric models expand the total addressable market for home composting solutions. Innovation and design will drive the next leg of growth as households evaluate lifetime cost, time saved, and output quality. This progression underscores how the home composting solutions industry now competes on appliance attributes as much as on environmental outcomes.

By Capacity: Mid-Range 20–50 L Segment Captures Family Upgraders

The less than 20 L segment accounted for 47.29% of the home composting solutions market in 2025, reflecting early-stage adoption among singles and couples and the constraints of small apartments. Compact devices at this capacity focus on simplicity and price, lowering the barrier to first purchases and trial use. The 20–50 L segment, forecast to grow at 9.62% CAGR through 2031, captures families seeking fewer emptying cycles and more consistent throughput as composting becomes routine. GEME Terra 2’s 14L chamber is designed for daily inputs of up to 2 kg and infrequent emptying, which meet the needs of households that produce more food scraps. Larger-capacity units can also reduce perceived effort by lowering trips to outdoor carts or drop-off sites and by smoothing weekly waste management patterns. In markets with active municipal support or neighborhood-level initiatives, mid-capacity devices help families keep pace with program expectations while meeting home hygiene and storage standards. This balance of capacity and convenience is key to sustaining the home composting solutions market.

Capacity choice often reflects household size, available space, and budget. Entry models below 20L keep headline prices lower and fit tight kitchens, but require more frequent handling, which not all families want. Mid-capacity options trade at higher prices for lower friction and better alignment with 4-person households that produce steady volumes of organics. Local subsidies can influence decisions when fixed rebates cover a significant share of smaller devices. At the same time, larger units can still be cost-effective if they reduce consumable use or offer permanent filtration. In India, municipal programs and PPP facilities deepen public familiarity with composting, which, in turn, indirectly boosts the value households place on at-home capacity and throughput. As these preferences are sorted by household type and urban form, capacity segmentation will continue to evolve in the home composting solutions market. This clarity of use case is also broadening the appeal of the home composting solutions industry among family buyers.

By Distribution Channel: Online Dominates Through Direct-to-Consumer Models

Offline channels held a 52.09% share of the home composting solutions market in 2025, driven by the advantages of in-person evaluation for size, fit, and build quality. Retail showrooms support the discovery of traditional bins and tumblers, and staff can help new buyers choose models that align with household constraints and goals. However, Online is projected to grow faster at a 10.25% CAGR, led by direct-to-consumer models that bundle consumables, financing, and trial offers. FoodCycler’s Eco 3 launch leveraged e-commerce to provide pricing transparency and payment plans, reducing psychological hurdles for a USD 499.99 device. Premium brands also manage diagnostics and firmware updates through proprietary apps, which suit online-first selling and post-sale support. GEME’s Terra 2 launch demonstrates how pre-orders and phased delivery can be orchestrated digitally as batches sell out. These online strengths focus on models that make clear performance claims and service layers that reinforce satisfaction.

Government labeling and standards will further shape the mix, as e-commerce listings can be updated more quickly than retail packaging for compliance details mandated by rules such as EU Regulation 2025/40. Municipal programs often require digital applications for grants or pilot participation, which familiarize households with online processes tied to composting and nudge equipment purchases toward digital channels. Online reviews, tutorial videos, and influencer content also reduce uncertainty about daily use, maintenance, and output quality. Offline channels will continue serving DIY gardeners and price-sensitive buyers, while e-commerce will absorb premium and connected offerings supported by subscription plans. This integrated model positions the home composting solutions market to balance tactile retail discovery with the service depth and speed of direct online sales. The long-term trend favors digital, especially for devices embedded in smart-home ecosystems within the home composting solutions industry.

Geography Analysis

North America accounted for 35.39% of the home composting solutions market in 2025, supported by strong regulatory signals and federal program funding, while Europe contributed 28–30%, with EU-wide standardization shaping product design and labeling. U.S. rules at the state level, including California’s SB 1383, increased compliance and procurement activities tied to recovered organics-derived products. Washington State’s ORCA framework mandates year-round organics service to residential customers in designated areas by April 2027, accelerating access and awareness that complement at-home processing habits. The United States EPA and USDA are funding infrastructure and local partnerships to expand composting and reduce food waste, which strengthens the ecosystem that households rely on for education, drop-off, and program alignment. In Europe, Regulation 2025/40 harmonizes home-composting standards and tightens packaging compatibility timelines, which will influence buyer confidence and retail communications for at-home devices. These drivers put both regions on steady growth paths for the home composting solutions market, with online channels and premium devices particularly strong in dense urban centers that value odor control and speed.

Asia-Pacific is projected to grow at an 8.92% CAGR over 2026–2031, led by Japan and South Korea’s policy and behavioral frameworks, as well as China’s rapid infrastructure scale-up. Japan’s 2030 food loss targets and localized incentives, including Inagi City’s subsidy for electric composters, promote household participation and lower the cost of first-time device purchases. South Korea’s RFID-enabled systems, which charge residents by weight, have built consistent habits around source separation and food waste minimization that complement at-home solutions. In China, improvements in sorting rates and the scale of collection in cities such as Shenzhen show that public infrastructure can raise household awareness and expand the market for at-home appliances that reduce odor and shorten handling time. India’s regulatory architecture for solid waste management and PPP models for composting plants are making composting more visible and practical, which supports consumer understanding and willingness to adopt entry-level equipment. As consumer familiarity rises, the home composting solutions market in Asia-Pacific will benefit from a mix of incentives, infrastructure, and product fit for apartments and multifamily buildings.

Brazil, Chile, and Argentina are leading the way in South America, driven by urban environmental priorities and community pilots that build visibility and basic know-how. In the Middle East and Africa, higher-income Gulf countries lead small-scale adoption as part of national sustainability agendas, while South Africa grows slowly from municipal pilots. When cities launch organics programs or enable bulk procurement and local assembly, affordability improves, allowing households to adopt compact devices more readily. In both regions, steady gains will come from public campaigns that demonstrate odor control, cleanliness, and convenience, supported by online distribution that can reach early adopters. Sustained awareness and selective incentives will be necessary to expand the home composting solutions market in both regions over the forecast period.

Competitive Landscape

The home composting solutions market remains moderately fragmented, with the top five brands collectively capturing a major share in 2026, while more than 200 smaller players focus on worm bins, outdoor tumblers, and community systems. Established kitchen and home appliance makers are elevating expectations for design, noise levels, and cleanliness, which raises the bar for new entrants. Category leaders differentiate through odor control, ease of use, and smart features that reinforce daily convenience and help households adopt and sustain habits. Product introductions in 2024–2026 centered on faster cycles, permanent filtration, and fit for small kitchens, which play to urban buyers who prioritize clean, compact, and connected home composting solutions. Press releases and company announcements underscore this shift toward premium features and supportive service layers that justify higher upfront prices[3]GEME, “GEME Terra 2: Fast, Odor-Free Kitchen Composter,” GEME, geme.bio.

Technology and materials are active fronts for differentiation. Several brands are investing in real-time monitoring and predictive models that remove guesswork and ensure consistent outcomes across seasons and feedstocks. Research documents link gas emissions to compost maturity and provides practical sensor thresholds for avoiding anaerobic conditions, while materials such as biochar reduce ammonia and sulfur compounds that drive odors. Patents in odor-control films and grinding mechanisms point to an IP race that will support product differentiation and potential licensing. Permanent filtration and reduced reliance on consumables can shift lifetime costs and raise satisfaction, which influence device choice in multi-family homes. Premiumization is now a durable theme in the home composting solutions market, supported by advances that reduce maintenance and learning curves.

Distribution and service models also shape competition. Direct-to-consumer strategies combine online education, financing, and subscriptions that stabilize performance, while pilots and municipal collaborations broaden exposure. Community-scale services that bundle hardware with pickup of finished compost offer an alternative pathway for residents who want results without routine device maintenance[4]City of Somerville, “Mayor Ballantyne Announces Curbside Food Waste Collection Pilot,” City of Somerville, somervillema.gov. At the same time, curbside programs continue to grow, which validates source separation while also creating a substitute that households weigh against device purchases. The competitive set will keep tilting toward brands that can demonstrate odor-free operation, easy workflows, and visible cost control. These elements align with the learning curves of new adopters in the home composting solutions market. Continued investment in app features, consumable optimization, and durability will be central to winning share.

Household Composters Industry Leaders

Joseph Joseph

Pela Earth (Lomi)

Vitamix (FoodCycler)

Reencle

Envirocycle Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Wormingup secured USD 128,000 seed funding from 17 Malaysian and regional investors to scale IoT-enabled vermicomposting pods across Southeast Asia, targeting commercial launches in Indonesia and Thailand by late 2026. The company demonstrated 40% yield increases in local farm pilots through AI-optimized feeding schedules

- March 2026: Elea & Lili raised USD 2.94 million in seed funding led by Lifeline Ventures to commercialize cellulose-based superabsorbent materials (CSA™) that replace fossil-based polymers in composting and hygiene applications, with Isometric-certified carbon removal credits expected in Q1 2026. The biomaterial addresses microplastic contamination from traditional liners

- January 2026: RenX Enterprises completed the purchase of a Komptech Crambo 5000 shredder and Diamond Z 1463B horizontal grinder following strong operating performance, enhancing organic waste processing capacity and supporting expansion in the composting sector.

- January 2026: GEME launched the Terra 2 AI-powered composter at USD 549, featuring permanent metal-ion odor filtration and thermophilic microbes processing waste in 6-8 hours, with Batch 1 and 2 pre-orders selling out within weeks. This launch positions GEME as a premium alternative to consumable-dependent competitors by eliminating recurring filter costs

Global Household Composters Market Report Scope

| Outdoor Bins & Tumblers |

| Electric Countertop Composters |

| Worm/Vermicompost Bins |

| In-garden Digesters |

| Less than 20 L |

| 20–50 L |

| More than 50 L |

| Offline Retail (DIY Stores, Garden Centers) |

| Online Marketplaces |

| Direct-to-Consumer Brands |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway and Sweden) | |

| Rest of Europe | |

| Middle East And Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product Type | Outdoor Bins & Tumblers | |

| Electric Countertop Composters | ||

| Worm/Vermicompost Bins | ||

| In-garden Digesters | ||

| By Capacity | Less than 20 L | |

| 20–50 L | ||

| More than 50 L | ||

| By Sales Channel | Offline Retail (DIY Stores, Garden Centers) | |

| Online Marketplaces | ||

| Direct-to-Consumer Brands | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway and Sweden) | ||

| Rest of Europe | ||

| Middle East And Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the home composting solutions market?

The home composting solutions market size is USD 245.83 million in 2025 and is forecast to reach USD 386.21 million by 2031 at a 7.82% CAGR over 2026-2031.

Which product categories are leading and growing fastest in home composting?

Outdoor Bins & Tumblers led with 43.52% share in 2025, while Electric Countertop Composters are projected to grow fastest at 8.55% CAGR through 2031.

Which capacity range is most popular among households?

The less than 20 L segment led with 47.29% share in 2025 among compact buyers, while the 20–50 L segment is the fastest growing at a 9.62% CAGR as families upgrade.

How are regulations influencing adoption in North America and Europe?

California’s SB 1383, Washington’s ORCA, EU Regulation 2025/40, and national funding programs are expanding collection access, standardizing labels, and boosting confidence to adopt at-home systems.

What role do online channels play in adoption?

Online direct-to-consumer sales are growing at a 10.25% CAGR due to bundled subscriptions, financing, and app-enabled support, while offline retail remains important for discovery and traditional bins.

Are verified carbon credits influencing buyer decisions?

Yes; Pela Earth’s Lomi secured carbon-credit approval in 2024, demonstrating measurable environmental return that attracts eco-conscious consumers.

Page last updated on: