Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

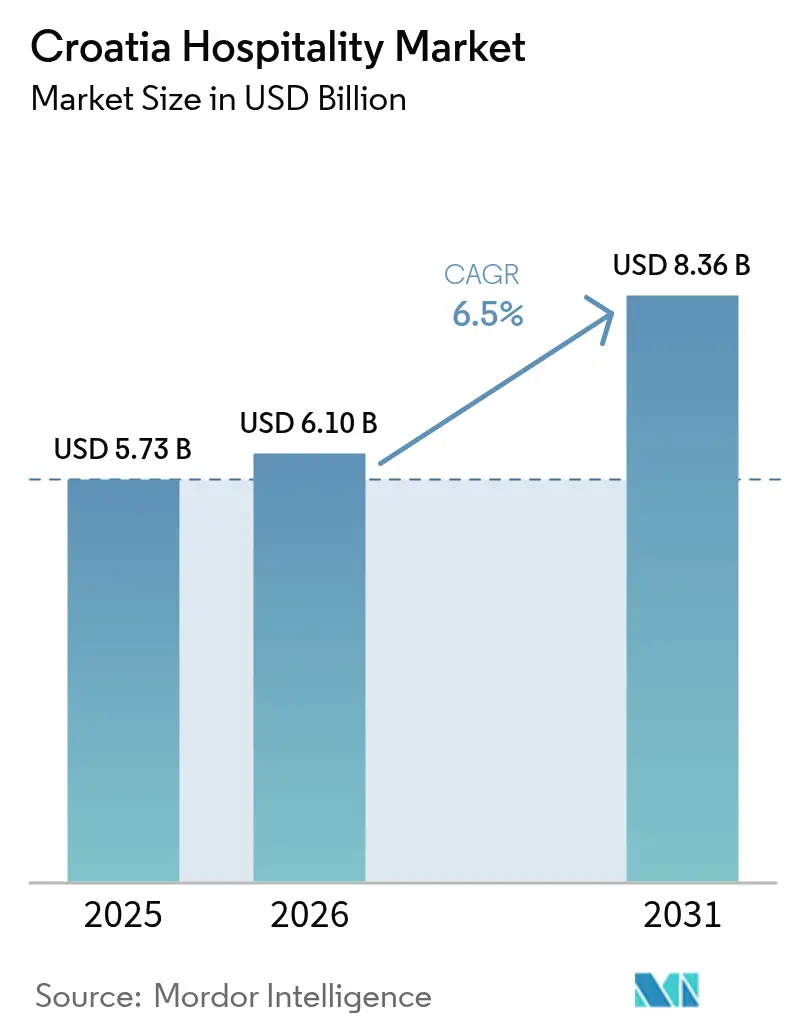

| Base Year Market Size (2025) | USD 5.73 Billion |

| Market Size (2026) | USD 6.1 Billion |

| Market Size (2031) | USD 8.36 Billion |

| Growth Rate (2026 - 2031) | 6.50% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Croatia Hospitality Market Analysis by Mordor Intelligence

The Croatia Hospitality Market size was valued at USD 5.73 billion in 2025 and estimated to grow from USD 6.1 billion in 2026 to reach USD 8.36 billion by 2031, at a CAGR of 6.5% during the forecast period (2026-2031).

Croatia’s simultaneous entry into the Schengen Area and the Eurozone in 2023 removed border checks and currency-exchange costs, widening the demand funnel for European travelers and directly accelerating the Croatia hospitality market expansion[1] BNP Paribas, “Euro Adoption Strengthens Croatia's Economy,” economic-research.bnpparibas.com.. Infrastructure investments led by cruise-port upgrades, marina expansions, and airport modernizations continue to unlock capacity during peak months, while government incentives for wellness tourism temper seasonality. Labor shortages remain acute, yet rising wages have supported disposable income among hospitality workers, spurring domestic spending that partially offsets recruitment costs. Digital transformation is redefining booking behavior, as hotel operators leverage direct platforms to claw back margin from online travel agencies. The Croatia hospitality market enjoys regulatory tailwinds that reward upgraded, energy-efficient properties, signaling durable value creation for operators with scale and capital discipline.

Key Report Takeaways

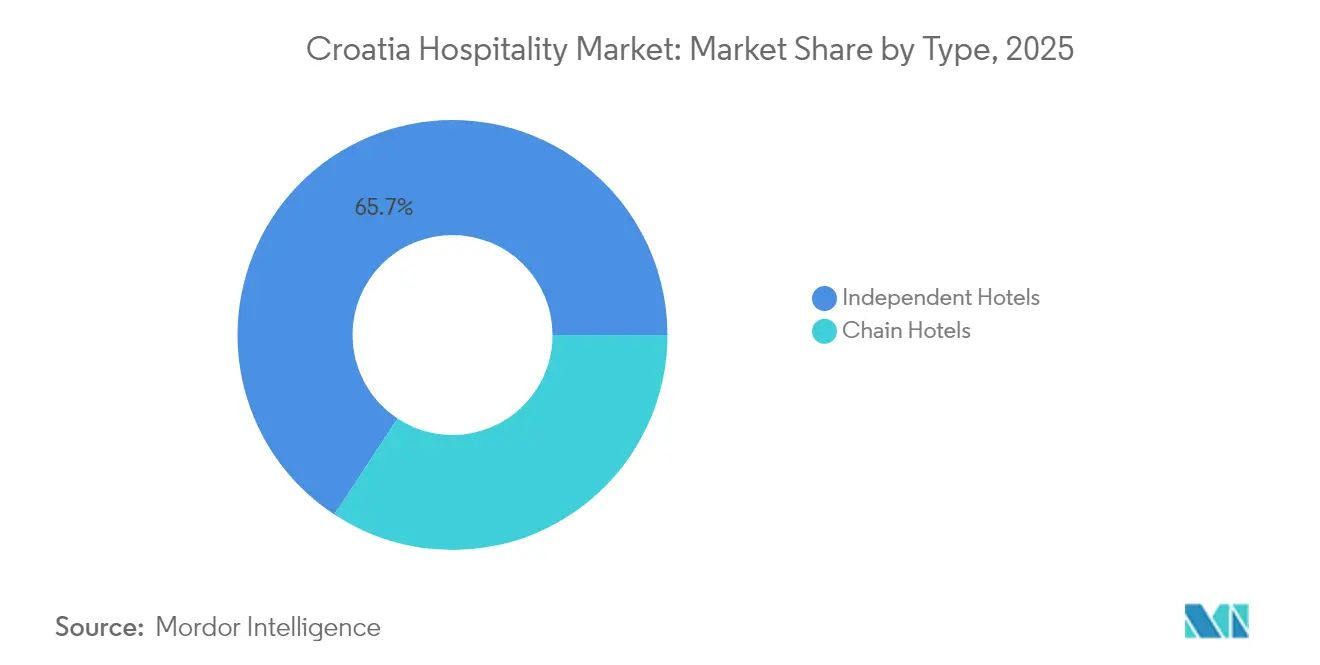

- By type, independent hotels commanded 65.74% of the Croatia hospitality market share in 2025; Chain Hotels are projected to grow at a 7.48% CAGR between 2026-2031.

- By accommodation class, mid & upper-mid-scale captured 48.95% share of the Croatia hospitality market size in 2025, while Luxury is advancing at an 8.07% CAGR between 2026-2031.

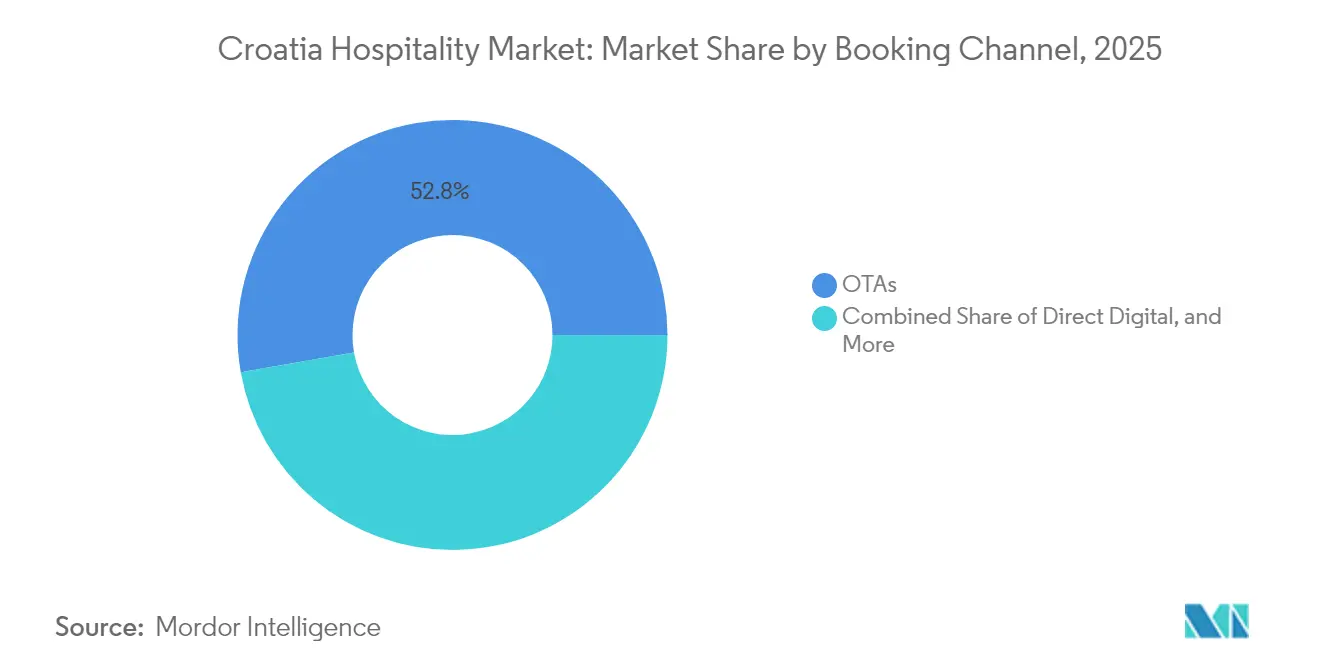

- By booking channel, OTAs held a 52.78% share of the Croatia hospitality market; direct digital bookings are forecast to expand at a 10.45% CAGR between 2026-2031.

- By geography, Dalmatia accounted for 38.75% of the Croatia hospitality market size in 2025, whereas the Adriatic Islands are progressing at an 7.92% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Croatia Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Schengen & Eurozone entry easing arrivals | +1.2% | Global with EU concentration | Short term (≤ 2 years) |

| Adriatic air- & cruise-port capacity expansion | +0.8% | Coastal Croatia | Medium term (2-4 years) |

| Digital-nomad visa lengthening average stays | +0.4% | Continental & coastal cities | Medium term (2-4 years) |

| Ultra-luxury yacht tourism fuelling marina demand | +0.6% | Dalmatia, Istria, Kvarner | Long term (≥ 4 years) |

| Government incentives for year-round wellness resorts | +0.3% | Continental thermal regions | Long term (≥ 4 years) |

| Smart-hotel energy-retrofit cost savings | +0.2% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Schengen & Eurozone Entry Easing Arrivals

Croatia’s adoption of Schengen and the Euro in 2023 removed two structural frictions—border queues and currency conversion fees—that historically discouraged spontaneous cross-border travel. Border crossings now process 15–20 minutes faster per vehicle, which meaningfully improves road-trip itineraries popular among German and Austrian visitors[2]Croatian Bureau of Statistics, “Tourist Arrivals and Nights in Commercial Accommodation, 2024,” podaci.dzs.hr.. Euro adoption erased the 2–3% exchange cost on consumer outlays, allowing hotels to advertise comparable rates to Italy or Slovenia without hidden fees. The reform further enables seamless multi-country vacations; travelers can start in Venice, transit the Istrian coast, and finish in Split without added paperwork. Although a stronger Euro price perception creates competitive pressure versus neighboring Balkan destinations, operators are countering through bundled packages and dynamic pricing. The overall effect has been a measurable uplift in visitor nights and higher-value ancillary spending, bolstering the Croatia hospitality market.

Adriatic Air- & Cruise-Port Capacity Expansion

Between 2024 and 2026, Croatia is committing USD 218 million to expand maritime gateways, led by Split’s EBRD-financed terminal upgrade and Šibenik’s new berths[3]European Bank for Reconstruction and Development, “More Cruise Ships Will Head to Port of Split in Croatia,” ebrd.com.. Dubrovnik expects 345 cruise ship calls delivering 511,000 passengers in 2025, a pivot that required scheduling caps to avoid Old Town congestion. By diverting large vessels to secondary ports, authorities are spreading economic gains to lesser-known coastal towns while relieving Dubrovnik’s infrastructure. In aviation, Zadar and Rijeka airports are extending runways to receive trans-European narrow-body jets, pushing dire ct seat capacity beyond pre-pandemic peaks. These bottleneck solutions add resilience and broaden the Croatia hospitality market catchment beyond high-season weekend peaks. Integrated transport planning, including upgraded road links, assures last-mile connectivity between terminals and hotels, converting arrivals into longer average stays.

Digital-Nomad Visa Lengthening Average Stays

The digital-nomad visa, permitting up to 18-month residencies, has approved more than 1,000 applicants since launch, with most arrivals concentrating in Zagreb, Split, and Zadar[4] Ministry of the Interior of the Republic of Croatia, “Temporary Stay of Digital Nomads,” mup.gov.hr.. Remote workers spend like residents rather than transient tourists, channeling expenditures to grocery, coworking, and long-term rentals. Their presence flattens Croatia’s extreme seasonality curve, lifting shoulder-season hotel occupancy by low-single-digit points. Municipalities are repurposing under-utilized municipal buildings into coworking hubs, anchoring local ecosystems designed to retain nomads beyond their first visa cycle. Constraints remain around rural broadband speeds, which currently limit dispersion into Continental Croatia villages. Nonetheless, the program supplies a template for diversifying source markets and elevating the Croatia hospitality market quality mix away from purely sun-and-sea demand.

Ultra-Luxury Yacht Tourism Fuelling Marina Demand

With 72 marinas and an average USD 137.34 daily spend per guest, nautical tourism outperforms beach tourism on per-capita metrics. ACI Marina Dubrovnik invested USD 5.12 million in longer berths, while ACI Marina Rijeka is positioning to become the Adriatic’s largest superyacht hub at 260 berths. Charter arrivals are projected at 480,000 annually, catalyzing demand for premium provisioning, concierge, and maintenance services. Hotel operators in Istria and Kvarner are integrating marina access into resort master plans, capturing cross-selling opportunities between rooms, spas, and yacht services. Regulatory ambiguity on concession extensions remains a risk, potentially delaying investment horizons beyond 2026. Even so, the high-margin nature of yacht tourism is solidifying Croatia’s positioning among Mediterranean elite destinations, adding depth to the Croatia hospitality market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Coastal over-tourism zoning caps | -0.7% | Dubrovnik, Split | Short term (≤ 2 years) |

| Post-pandemic labor shortages & wage inflation | -0.9% | National, coastal regions | Medium term (2-4 years) |

| Infrastructure strain during peak season | -0.6% | Dalmatian Coast, Istria | Short term (≤ 2 years) |

| Delays in sustainable hotel certification adoption | -0.5% | National, eco-sensitive zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Coastal Over-Tourism Zoning Caps

Dubrovnik imposed a freeze on new private rental permits within the Old Town and limits simultaneous cruise arrivals to two vessels, constraining bed-stock expansion. UNESCO compliance further restricts façade modifications, slowing hotel renovations that seek to add rooms. These caps create scarcity, driving daily ADR higher yet also displacing demand toward Šibenik and Makarska, where infrastructure may lag visitor expectations. The policy aims to protect cultural heritage but risks diverting capital to destinations outside Croatia if returns compress. Operators holding grandfathered licenses enjoy quasi-moat advantages, underpinning premium valuations within the Croatia hospitality market. Secondary cities gain a window to capture displaced development, provided they scale utilities and transport links swiftly.

Post-Pandemic Labor Shortages & Wage Inflation

Tourism faces the highest job-vacancy rate in Croatia, with open roles outstripping local supply despite the employment rate rising to 66.5%. Domestic out-migration to higher-paying EU states has forced dependence on workers from Nepal, India, and the Philippines. Recruitment costs, visa processing, and cultural integration programs inflate pre-opening budgets, while wage bills climbed 40–50% versus 2019 levels for certain culinary roles. Some operators cut restaurant hours or scale back amenities during shoulder seasons to manage payroll pressures. Automation—from self-check-in kiosks to AI-driven housekeeping schedules—provides partial relief but requires upfront capex that smaller independents struggle to finance. Sustained wage inflation squeezes EBITDA margins and could delay refurbishment cycles, tempering growth within the Croatia hospitality market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Independent Hotels Retain Scale as Chains Accelerate

Independent hotels controlled 65.74% of the Croatia hospitality market size in 2025, a legacy of family ownership structures and historic villas converted into boutique properties. Their deep local knowledge, flexible rate strategies, and emphasis on authentic experiences resonate with European leisure travelers seeking cultural immersion. Nevertheless, brand-affiliated Chain Hotels grew at a 7.48% CAGR and are slated to add flagged rooms across coastal resorts and inland conference hubs. International chains import standardized operating manuals, robust loyalty networks, and capital access, which enhance resilience in downturns. Franchise and management-contract models lower entry hurdles, enabling Marriott, Hilton, and Accor to leverage Croatian partners’ landholdings. Independent operators confront rising distribution-cost headwinds, pushing many toward soft-branding affiliations that retain identity while tapping global systems. This duality is likely to persist, with niche independents thriving on uniqueness and chains consolidating mid-scale and upscale supply in the Croatia hospitality market.

Chain growth also reflects investor appetite for asset-light returns and transparent performance metrics. Portfolio transactions, such as TUI’s stake in Karisma Hotels Adriatic, illustrate that scale brings bargaining power with suppliers and talent pools. Meanwhile, independents differentiate through culinary provenance, heritage architecture, and community engagement programs that attract premium rates despite smaller key counts. Technology adoption remains the competitive equalizer; boutique hotels are partnering with cloud-based PMS providers to match chain efficiencies. As both groups modernize, the Croatia hospitality market will likely settle into a barbell structure—densely branded properties in high-traffic nodes and curated independents in experience-centric locales.

By Accommodation Class: Mid-Scale Holds Volume as Luxury Surges

Mid & upper-mid-scale properties accounted for 48.95% of the Croatia hospitality market share in 2025, reflecting the core demand from price-sensitive European families and couples. These hotels balance amenity depth with affordability, often clustering around Blue Flag beaches and national parks. The Luxury tier—though smaller registered an 8.07% CAGR on the back of superyacht arrivals, exclusive wellness retreats, and heritage conversions such as the EUR 85 million (USD 92.65 million) Monumenti Resort in Pula. Investors pivot to five-star assets given their superior RevPAR and insulation from OTA discount wars. Budget & economy accommodation still thrives in coastal campsites and apartment rentals, especially among road-trippers from Central Europe. Service Apartments are the emergent niche, capturing extended-stay nomads seeking kitchenettes and workspace in one unit.

Rising labor and energy costs are squeezing margins across classes, but luxury properties deploy pricing power to absorb cost shocks, whereas mid-scale operators resort to tech-enabled efficiency gains. Sustainability certifications such as Green Key are now prerequisites for bank financing, benefiting upscale resorts that can amortize capex over higher nightly rates. As wealth disparities widen within source markets, Croatia is poised to host parallel accommodation ladders: value-driven mass beach resorts and bespoke high-end enclaves, both integral to the broader Croatia hospitality market.

By Booking Channel: OTA Supremacy Faces Direct-Digital Push

OTAs controlled 52.78% of bookings in 2025, owing to marketing muscle and user-generated content that drives trust among first-time visitors. However, Direct Digital channels, notably mobile apps and brand websites, are projected to grow at a 10.45% CAGR as hotels invest in CRM suites to personalize offers and circumvent commission fees. Dynamic packaging, advanced loyalty tiers, and price-match guarantees help chains lure repeat travelers to direct portals. Independents, historically reliant on OTA visibility, are adopting meta-search advertising and cooperative marketing via regional tourism boards. Corporate/MICE itineraries remain largely agent-led, though self-service booking tools are gaining share within multinationals.

Wholesale and traditional agents cater to niche segments such as pilgrimage tours and luxury bespoke trips, maintaining relevance through high-touch service. Across all channels, data capture and AI-driven segmentation are the new competitive edges, enabling upsells that lift per-guest revenue. The balancing act between reach and margin will define distribution strategies in the Croatia hospitality market over the next decade.

Geography Analysis

Dalmatia topped regional rankings with 38.75% of the Croatia hospitality market size in 2025, buoyed by Split’s expanding cruise terminal and Dubrovnik’s global brand equity anchored in UNESCO World Heritage status. Average daily rates rose as capacity constraints in Dubrovnik pushed visitors toward Split, Šibenik, and the Makarska Riviera, prompting investors to scout secondary coastal towns for next-wave development. Port diversification is easing pressure on Dubrovnik’s walled city, but zoning caps continue to limit new supply, granting established hotels strong pricing power. The region has also begun leveraging cultural festivals, gastronomic trails, and film tourism to extend shoulder-season occupancy, smoothing revenue curves in the Croatia hospitality market.

Istria & Kvarner captured 34.67% share, thriving on drive-to proximity from Italy, Austria, and Slovenia. The peninsula blends wine tourism, cycling routes, and wellness retreats, creating multi-segment appeal that stretches beyond the summer peak. Investments such as Valamar’s EUR 139 million (USD 151.51 million) Pical Resort will add five-star capacity and reinforce eco-label credentials through solar arrays and wastewater recycling systems. Kvarner’s marina network dovetails with yacht tourism, enabling bundled land-and-sea itineraries. Sustainability leadership gives the region an edge with EU funding channels, ensuring continued product differentiation within the Croatia hospitality market.

Continental Croatia, home to Zagreb and spa destinations like Varaždinske Toplice, represented 26.58% of 2025 revenue yet shows the highest untapped potential. EU-backed broadband upgrades now support conference and remote-work sub-segments, while thermal waters underpin medical-wellness positioning that draws year-round guests. Rural villages are experimenting with agritourism homestays, though brand awareness remains modest compared with coastal staples. Government grants covering up to 55% of rural accommodation refurbishments aim to lift quality standards. The interior’s relative affordability, coupled with authentic cultural assets, positions it as Croatia’s strategic hedge against coastal over-dependence, promising to elevate the Croatia hospitality market beyond its maritime origins.

Regulatory Landscape

Croatia’s hospitality sector is primarily governed by the Hospitality Act (Zakon o ugostiteljskoj djelatnosti), with a significant amendment published in the Official Gazette in December 2024 (NN 152/2024). Oversight spans multiple public bodies, including the Ministry of Tourism and Sport, the State Inspectorate, and local authorities, with rising coordination aimed at compliance gaps in private accommodation and coastal over-tourism constraints (notably in destinations such as Dubrovnik that manage permits and cruise-arrival intensity).

In June 2026, the Government approved a proposal for a new Hospitality Act targeting unregistered short-term rentals and aligning sector controls with EU Regulation 2024/1028. The proposal introduces a single registration system and mandatory registration numbers for rooms, apartments, and holiday homes advertised on digital platforms, supported by further digitalization of categorization and administrative workflows through eTurizam. On the tax side, flat-rate taxation for tourist accommodation (pausalni porez) continues to be structured through local self-government decisions under the Ministry of Finance and Tax Administration, alongside national rules for tourist tax (touristicka pristojba), creating a dual compliance burden across licensing and fiscal reporting.

Value Chain Analysis

Croatia’s hospitality value chain runs from upstream inputs (construction and refurbishment contractors, energy and utilities, laundry and consumables, and a mix of domestic and imported agri-food) through property owners and operators (independent hotels, branded chains, camps, and private accommodation), and into demand and distribution (OTAs, direct digital, tour operators/wholesalers, and corporate/MICE intermediaries). Government programs under the National Plan for Sustainable Tourism Development to 2027 and the associated Action Plan to 2025 shape investment and operating priorities across this chain by pushing green and digital upgrades, higher value-added products, and initiatives that reduce seasonality.

Two operational bottlenecks are shaping value capture. First, cost inflation and labor availability have become binding constraints: the Croatian Tourism Association (HUT) reported labor costs rising 11.7% year-on-year in the first half of 2025, while industry feedback via the Croatian Chamber of Economy (HGK) highlighted work-permit processing as a bottleneck for foreign labor in the Dubrovnik area. Second, profitability pressure is flowing through procurement and operating lines, with HUT noting EBITDA margin compression from 28.2% (2024) to an estimated 26.6% (2025) as costs grew faster than revenues, and food procurement costs increasing faster than the EU average in 2025. This is pushing operators to tighten sourcing, standardize multi-property operations, and deepen integration with domestic producers to reduce import leakage during peak season.

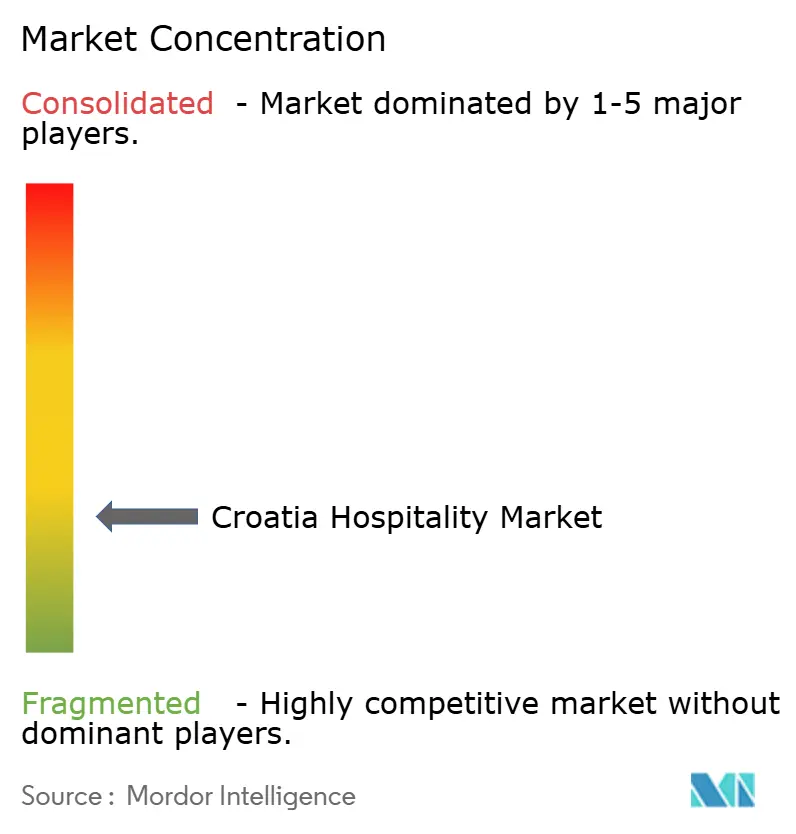

Competitive Landscape

The Croatia hospitality market is fragmented. Market leader Valamar Riviera maintains its lead by advancing a substantial investment pipeline aimed at upgrading flagship resorts and driving sustainable operations. Maistra Hospitality Group follows closely, emphasizing premium offerings in Rovinj and Zagreb, particularly in the conference segment. Arena Hospitality Group ranks third, with a diversified portfolio spanning Istria, Zagreb, and select properties in Germany. International brands are intensifying footholds: Marriott debuted The Isolano, Cres under Autograph Collection, and Accor will open its first Handwritten Collection in Rijeka in 2026. These moves underscore Croatia’s ascent as a core Mediterranean growth node for global chains.

Consolidation is speeding up as asset-light operators seek scale; TUI’s acquisition of a 33.3% stake in Karisma Hotels Adriatic injects distribution prowess, whereas Brown Hotels’ purchase of the Jadran hotel portfolio signals Israeli capital’s confidence. Technology is the battleground: Plava Laguna’s rollout of IDeaS G3 RMS across 16,376 units exemplifies data-driven yield management. Sustainability investments—from solar carports to desalination plants—are now standard in competitive tenders for coastal concessions. Regulation shapes strategy; operators navigating zoning limits and concession renewals secure long-run asset security. Fragmentation persists below the top tier, offering acquisition targets for funds seeking entry into the Croatia hospitality market.

Overall, competitive intensity revolves around balancing aggressive expansion with heritage conservation, operational excellence, and regulatory compliance. Those able to integrate digital capabilities with authentic Croatian storytelling will command premium RevPAR and capture disproportionate wallet share in the evolving Croatia hospitality market.

Croatia Hospitality Industry Leaders

Amadria Park

Liburnia Riviera Hoteli

Plava Laguna

Valamar Riviera

Hotel Dubrovnik d.d.

Sunce Hotels (Bluesun)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory and program-led digitization creates whitespace for compliant, data-integrated operating models across hotels and private accommodation. The Government’s enactment of an Action Plan on April 9, 2026 for implementing the National Plan for Sustainable Tourism Development until 2027, together with the Ministry’s presentation of a draft new Hospitality Act on April 17, 2026 to curb unregistered rentals and modernize categorization, supports investment in registration, reporting, and property-upgrade workflows. For operators with scale, this environment strengthens standardized processes, improves inventory visibility, and supports better coordination with platforms and authorities. It also increases the compliance burden for fragmented, informal supply.

Technology modernization is also opening product and margin opportunities tied to multi-property standardization, guest-experience digitization, and unified data layers. In 2026, Suncani Hvar completed an island-wide IT infrastructure deployment with m3connect (Wi-Fi 6 and IoT-ready data centers) across eight hotels and went live with Shiji Infrasys POS on April 25, 2026 across nine properties and more than 40 outlets, showing a shift toward enterprise-grade, cloud-enabled operations in Croatian resort portfolios. On the vendor and consolidation side, SWEN Hospitality’s February 2026 acquisition of Diventa (ITI Computers) points to centralized hotel information systems gaining traction, while releases from local providers such as Istra Tech, including AI sentiment analysis modules and digital self check-in/out tools in 2026, indicate expanding adoption pathways for independents seeking chain-like efficiency without full brand affiliation.

Recent Industry Developments

- June 2026: Valamar Riviera announced preapproved investments for 2027, extending visibility into its multi-year development pipeline beyond the report’s base year. This reinforced the role of large domestic operators in driving product upgrades and influencing supplier demand across construction, fit-out, and sustainability-related services.

- May 2026: Plava Laguna reopened Hotel Garden Istra after a complete renovation, adding new family-focused facilities such as the Aquapark Splash Zone and upgraded Pepi Clubs. The upgrade supports differentiation in the mid-to-upper segment and increases competitive pressure on nearby coastal properties to refresh amenities and raise on-site spend per guest.

- November 2024: Accor signed its first Handwritten Collection deal in Croatia for Hotel Continental Rijeka, planned to open in 2026 with 75 rooms. The signing marked a new brand-entry route into Croatia via conversion and soft-branding, expanding the toolkit for owners seeking international distribution while retaining local identity.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues generated from paid stays and related guest services delivered by organized accommodation providers across Croatia, tracked in value terms and expressed in USD for consistency across years.

Scope exclusions: Informal or unregistered stays, private peer to peer rentals that do not report as hospitality businesses, and non tourism real estate income are not counted.

Segmentation Overview

- By Type

- Chain Hotels

- Independent Hotels

- By Accommodation Class

- Luxury

- Mid & Upper-Mid-scale

- Budget & Economy

- Service Apartments

- By Booking Channel

- Direct Digital

- OTAs

- Corporate / MICE

- Wholesale & Traditional Agents

- By Geographic Region

- Istria & Kvarner

- Dalmatia (Split & Dubrovnik)

- Adriatic Islands

- Continental Croatia (Zagreb & Central)

- Slavonia & Eastern Croatia

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the factual base for demand, supply, and pricing signals in Croatia. We reviewed official tourism arrivals and overnight stays, and then cross checked seasonality and source markets using publications such as the Croatian Bureau of Statistics, the Croatian National Tourist Board, and Eurostat.

To avoid overcounting, the secondary review also considered macro and operating context that influences spend per stay, such as inflation series and household spend indicators from sources such as the World Bank and IMF, along with VAT and tourism related policy notes published by government portals. Company annual reports, investor decks, and reputable press were used to understand capacity additions, refurbishment cycles, and positioning shifts. Paid subscriptions supporting company financials and intelligence, plus news and financials, were referenced selectively for consistency checks. This list is illustrative rather than exhaustive, and we also used other public documents and references to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on validating how the revenue pools split between direct bookings, OTAs, and corporate demand, and how ADR and occupancy moved across peak and shoulder seasons. We spoke with a mix of accommodation operators, local travel intermediaries, and industry advisors across the coast and inland areas so that regional differences in stay length, pricing, and capacity utilization could be reflected in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 16% | APAC: 44% |

| Mid tier: 51% | Functional/Unit leaders: 40% | EMEA: 35% |

| Smaller Players: 16% | Managers: 44% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where tourism arrivals and overnight stays are translated into demand pools, which are then converted into revenue using occupancy patterns, ADR ranges, and mix shifts between chain and independent properties. Where the public time series has gaps by region or class, the missing pieces are filled using proportional splits observed in adjacent years and then checked with interview feedback.

To keep totals realistic, outputs are corroborated with selective bottom-up approximations, such as sampled room inventory by region multiplied by observed occupancy and ADR bands, plus channel checks on booking commissions and corporate share. Key inputs used in the model include accommodation capacity additions and closures, seasonality of nights stayed, ADR movement by class, share of direct digital bookings, and inflation adjusted operating price pressure.

Forecasting uses scenario analysis anchored on expected visitor growth, air connectivity and cruise scheduling signals, and the pace of new hotel openings and renovations. Assumptions on ADR progression and occupancy normalization were aligned to what operators and advisors expect for peak season pricing power and shoulder season demand depth, and then the curve was adjusted so it stays consistent with macro indicators and recent performance.

Data Validation & Update Cycle

Model outputs are cross checked against independent signals like total nights, capacity utilization ranges, and observable price movements, and then variance outliers are reviewed before the numbers are finalized. When the model shows a sudden jump that is not supported by supply additions or demand indicators, we recheck the inputs and, if needed, recontact sources to confirm what changed.

Each report goes through a multi step analyst review where assumptions, calculations, and year to year bridges are inspected for consistency. The study is refreshed annually, and interim updates are made when material events occur, such as major tax changes, demand shocks, or large capacity announcements. Before delivery, a final update pass is completed so clients receive the most current view based on the latest available information.

Mordor Intelligence's Croatia Hospitality Market Size Compared Against Other Published Estimates

Published market values for Croatia hospitality can look far apart because different studies choose different definitions of what counts as hospitality, and they also use different base years and currency timing. The spread usually becomes larger when a forecast window is long and when the model relies on a single driver that does not fully capture seasonality.

In practice, gaps often come from whether the scope is limited to hotels only or expanded to include a wider set of lodging formats, and from how ADR and occupancy are projected across peak and shoulder months. Some estimates lean on headline industry turnover conversions, while others model a demand pool from nights stayed and then apply pricing and channel mix, with peer checks on 2025 as the base year and on class and booking channel splits used to keep hotel only revenues separate from wider accommodation pools, which is how the Croatia total is set up in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.73 B (2025) | |

| Global Consultancy A | USD 4.25 B (2024) | Uses a different base year and a broader hospitality definition that blends lodging types and service lines, which can shift the counted revenue pool even before growth is applied. |

| Industry Publisher B | USD 4.80 B (2026) | Starts the series at a later year and appears to apply a single growth curve over a longer horizon, with limited visibility on how occupancy seasonality and ADR by class were reconciled. |

Looking at the three figures together, the difference is mainly explained by what is counted, which year anchors the calculation, and how pricing and utilization are carried forward. Our approach stays traceable because each step ties back to visible tourism demand signals and practical pricing checks, which makes the final number easier to reproduce and stress test.

Key Questions Answered in the Report

How large is the Croatia hospitality market in 2026?

The Croatia hospitality market size reached USD 6.1 billion in 2026 and is forecast to grow at a 6.5% CAGR to 2031.

Which region generates the highest revenue?

Dalmatia contributes the largest share at 38.75% of 2025 revenue, driven by Split and Dubrovnik’s global appeal.

What segment is expanding fastest?

Luxury accommodation posts the strongest growth, advancing at an 8.07% CAGR on the back of yacht tourism and heritage hotel investments.

How are booking habits changing?

While OTAs remain dominant, direct digital bookings are climbing at a 10.45% CAGR as hotels enhance CRM and loyalty programs.

What is the main challenge facing operators?

Persistent labor shortages and wage inflation are compressing margins, given vacancies that exceed domestic talent supply.

Which companies lead the competitive landscape?

Valamar Riviera, Maistra Hospitality Group, and Arena Hospitality Group collectively hold roughly one-third of the market’s revenue.

Page last updated on: