Hosiery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 71.21 Billion |

| Market Size (2031) | USD 92.87 Billion |

| Growth Rate (2026 - 2031) | 5.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hosiery Market Analysis by Mordor Intelligence

The hosiery market size is projected to be USD 68.12 billion in 2025, USD 71.21 billion in 2026, and reach USD 92.87 billion by 2031, growing at a CAGR of 5.45% from 2026 to 2031. Investments in environmentally friendly fibers, the increasing penetration of online platforms, and the growing demand for versatile legwear options are reshaping competitive priorities within the market. Body stockings accounted for two-thirds of the projected turnover in 2025; however, tights and pantyhose are witnessing faster growth due to the adoption of technical fabrics that combine the polished appearance required for workplaces with the comfort associated with athletic wear. Premium brands are focusing on advanced features such as moisture-wicking yarns and seamless knitting techniques to justify higher price points, while mass-market channels are prioritizing maintaining sales volumes through extensive and accessible distribution networks. Europe continues to hold the largest share of revenue generation, while the Asia-Pacific region is driving most of the incremental demand. This growth in Asia-Pacific is supported by factors such as increasing urbanization, changes in professional dress codes, and the rising influence of Western fashion trends.

Key Report Takeaways

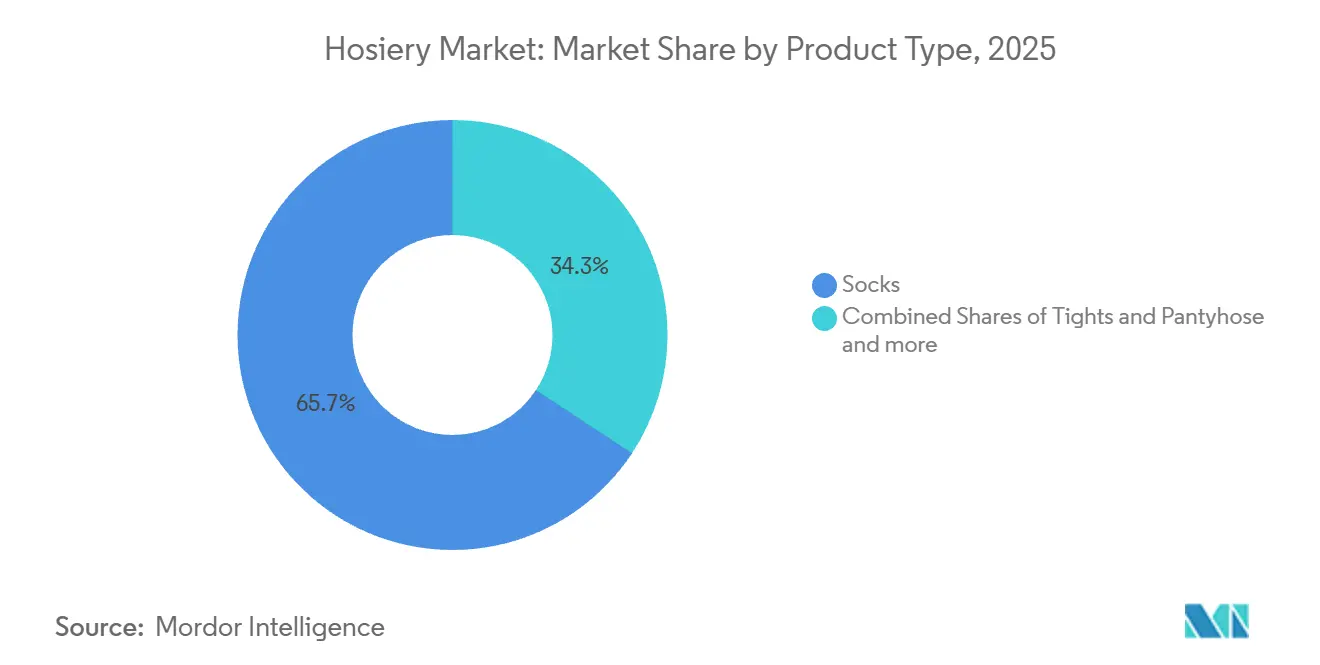

- By product type, socks led with 65.73% revenue share in 2025, whereas tights and pantyhose are forecast to expand at a 6.83% CAGR through 2031.

- By end-user, women held 68.32% of 2025 sales, while men’s hosiery is projected to grow at a 6.97% CAGR to 2031.

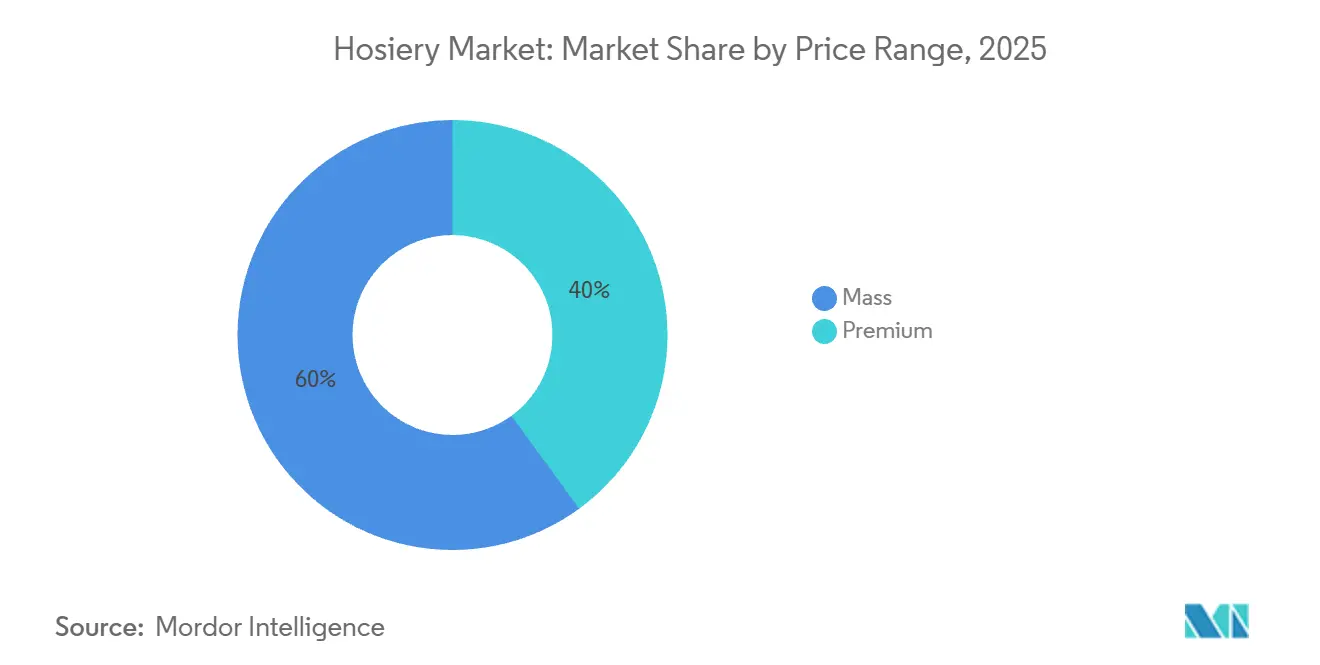

- By price range, the mass tier accounted for 60.03% of 2025 revenue, yet premium lines are set to rise at a 7.26% CAGR during 2026-2031.

- By distribution channel, supermarkets and hypermarkets generated 46.89% of 2025 turnover, whereas online retail is poised for a 7.68% CAGR to 2031.

- By geography, Europe supplied 39.88% of 2025 revenue, while Asia-Pacific is expected to log a 7.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hosiery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for fashionable hosiery like patterned and designer stockings | +1.2% | Global, with concentration in Europe and North America | Medium term (2-4 years) |

| Increasing women's workforce participation requiring professional attire | +1.0% | North America, Europe, Asia-Pacific urban centers | Long term (≥ 4 years) |

| Global fitness movement boosting performance hosiery for workouts and athletics | +0.9% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Product innovations like moisture-wicking, anti-bacterial, and temperature-specific tights | +0.8% | Global, premium segments in developed markets | Medium term (2-4 years) |

| Adoption of Western fashion trends in emerging markets | +0.7% | Asia-Pacific, South America, Middle East and Africa | Long term (≥ 4 years) |

| Sustainability initiatives using eco-friendly fibers and biodegradable yarns | +0.6% | Europe, North America, select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for fashionable hosiery like patterned and designer stockings

Hosiery has transitioned from being a purely functional necessity to becoming a significant fashion statement, with retailers in the United Kingdom reporting notable sales growth in 2024. Marks and Spencer recorded a 50% increase in sales of patterned and designer stockings, while John Lewis experienced a 55% rise. Additionally, the direct-to-consumer brand Heist Studios successfully doubled its revenue. This change highlights how younger consumers now view legwear as an accessory rather than a basic commodity. As a result, brands are introducing seasonal collections that feature intricate designs, bold colors, and collaborations with fashion influencers. This trend has proven advantageous for premium-tier brands, which are able to achieve higher profit margins through limited-edition products and compelling storytelling. At the same time, it has led to fragmented shelf space as mass-market retailers expand their stock-keeping unit (SKU) offerings to meet the demands of variety-seeking shoppers. Social commerce is playing a critical role in amplifying this trend, with TikTok hashtags related to hosiery content attracting billions of views and live-stream shopping in China converting impulse browsing into immediate purchases. Brands that focus on investments in visual merchandising, partnerships with influencers, and rapid product development cycles are capturing a larger share of the market, while those relying on static catalog assortments risk losing relevance in this dynamic and competitive environment.

Increasing women's workforce participation requiring professional attire

In 2024, women's labor-force participation stabilized at 58.9% in the United States and 65.6% in the European Union, sustaining the demand for professional hosiery as hybrid work arrangements became the standard and selective dress codes returned [1]. This trend has reinforced the popularity of sheer tights, control-top pantyhose, and seamless styles that pair well with tailored trousers and skirts, ensuring a stable revenue base for established brands. Additionally, there is a growing need for hosiery among women employed in service sectors, healthcare, and hospitality, where durable and comfortable options are essential for enduring long work shifts. This has created opportunities for the development of technical fabrics that incorporate features such as compression for improved circulation and moisture management for enhanced comfort. Brands that strategically segment their product offerings based on specific professions and practical use cases, rather than relying on generic work categories, can capture a larger share of customer spending and reduce product returns caused by mismatched performance expectations.

Global fitness movement boosting performance hosiery for workouts and athletics

The athleisure market is anticipated to experience consistent growth in the coming years, with hosiery emerging as a key category as consumers increasingly opt for socks and compression tights for activities such as running, yoga, and gym workouts. Performance features such as moisture-wicking, anti-bacterial treatments, and graduated compression, which were once exclusive to niche athletic brands, have now become widely available in mainstream collections. This shift has effectively blurred the lines between activewear and everyday legwear. Technological advancements like LYCRA DRY fiber technology, which is designed to enhance sweat evaporation, and Fulgar Q-SKIN yarns, which are specifically engineered to inhibit bacterial growth, directly address common consumer concerns such as odor and chafing during prolonged use. Younger consumers, particularly those from Generation Z, place a high value on functional benefits and are willing to invest in premium products that deliver noticeable improvements in comfort. This trend presents significant opportunities for brands to combine technical performance with fashionable designs, positioning hosiery as a versatile option suitable for multiple occasions rather than being restricted to specific uses. However, a critical challenge remains in educating consumers about these advanced features through clear product labeling and trial programs. This is especially important as the apparel industry continues to face elevated return rates, with issues related to size and fit being a major factor contributing to these returns.

Product innovations like moisture-wicking, anti-bacterial, and temperature-specific tights

Advancements in fiber science and knitting technology are enabling hosiery manufacturers to differentiate their products by offering more than just competitive pricing and attractive designs. For instance, Hong Kong Polytechnic University developed iActive moisture-wicking fabric, which is specifically designed to lower skin temperature during physical activity, while X-Bionic introduced HeatLoop thermal regulation technology, which helps retain body heat in colder conditions without adding unnecessary bulk [2]Source: The Hong Kong Polytechnic University, “iActive: Intelligent Active-Perspiration Activewear,” polyu.edu.hk. These innovations cater to diverse consumer needs, including athletes striving for enhanced performance, commuters looking for consistent comfort throughout the day, and individuals in colder regions who prefer warmth without the inconvenience of excessive layering. These advanced features allow brands to position their products at a premium price point compared to standard nylon-spandex blends. Additionally, seamless knitting technology adds further value by reducing fabric waste and eliminating irritation caused by seams, making it particularly appealing to environmentally conscious consumers and those with sensitive skin. From a business perspective, companies that invest in research and development and secure exclusive fiber partnerships can establish significant competitive advantages over private-label competitors, which often lack the financial resources and technical expertise to replicate such innovations. However, educating consumers remains a key priority, as many shoppers find it difficult to distinguish between genuine technological advancements and marketing claims. Transparent labeling and third-party certifications play a vital role in building trust and credibility with consumers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer concerns over chemicals in dyes and preservatives used in production | -0.5% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Shift to sustainable alternatives limiting synthetic hosiery demand | -0.4% | Europe, North America, select Asia-Pacific markets | Medium term (2-4 years) |

| Volatility in raw material prices disrupting production schedules | -0.6% | Global, especially Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Supply chain disruptions affecting availability and consistency | -0.7% | Global, with acute impact on Asia-Europe and Asia-North America routes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer concerns over chemicals in dyes and preservatives used in production

Heightened awareness of the environmental and health impacts of textile chemicals has driven significant regulatory actions and consumer backlash. The European Union's Registration, Evaluation, Authorisation, and Restriction of Chemicals (REACH) framework has restricted a large number of substances, while the OEKO-TEX Standard 100 has banned a wide range of chemicals used in dyes and preservatives, with full implementation expected in the coming years. In the United States, California's Proposition 65 has introduced specific warnings for textiles containing certain azo dyes and formaldehyde-based finishes. This has compelled brands to reformulate their products to avoid labeling requirements that could deter consumers from making purchases. Additionally, the Zero Discharge of Hazardous Chemicals (ZDHC) Manufacturing Restricted Substances List version 3.2 has become a widely recognized industry standard. Major retailers now require suppliers to comply with these guidelines and conduct random audits to ensure adherence. Reformulating products has introduced additional costs for brands using traditional dye systems, along with extended lead times as suppliers validate new chemical formulations. Smaller producers, often lacking the resources for research and development, face increasing pressure to exit the market. In contrast, vertically integrated companies that manage their own dyeing and finishing processes are better equipped to adapt quickly, enabling them to gain a competitive advantage and capture market share from non-compliant competitors.

Shift to sustainable alternatives limiting synthetic hosiery demand

Consumer preference for environmentally friendly materials often conflicts with the cost and performance benefits offered by synthetic hosiery. Materials such as nylon and spandex blends provide essential qualities like stretch, durability, and affordability, which natural fibers frequently struggle to match. For instance, Swedish Stockings has introduced recycled polyamide tights made with a significant proportion of post-consumer waste, while AMNI SOUL ECO biodegradable fiber represents another promising alternative. However, these innovative materials come with higher production costs and limited manufacturing capacity, making them less accessible for widespread adoption. While many consumers express a willingness to pay a premium for sustainably produced clothing, actual purchasing behavior often falls short of these stated intentions. This discrepancy places financial pressure on brands that choose to absorb the additional costs associated with sustainable materials. The European Union's Textile Strategy for the year 2024 has implemented mandatory requirements for minimum recycled-content thresholds, forcing brands to either reformulate their products or withdraw from specific markets. In contrast, regulations in North America remain voluntary, creating opportunities for brands to leverage differences in regulatory environments. Companies that successfully position sustainable materials as offering tangible performance benefits, such as enhanced durability and a reduced environmental impact, can justify higher price points. However, brands that lack credible certifications may face growing skepticism from increasingly informed and discerning consumers. The primary strategic challenge for the industry lies in scaling up the production of alternative fibers to achieve cost competitiveness with traditional synthetic materials. Addressing this challenge will require significant investments across the industry in recycling infrastructure and the development of bio-based feedstocks to support sustainable manufacturing practices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Socks Dominate Casual and Athletic Wear, Tights and Pantyhose Surge

Socks accounted for 65.73% of the projected 2025 revenue, reflecting their widespread use across casual, athletic, and professional settings. This dominance highlights their versatility and essential role in everyday wear. However, tights and pantyhose are expected to grow at a compound annual growth rate (CAGR) of 6.83% through 2031. This growth is driven by increasing workplace formality and advancements in sheer fabric technologies, which enhance both functionality and aesthetics. The sock category benefits from two primary demand drivers. First, performance socks designed for athletics incorporate features such as moisture-wicking and anti-bacterial properties, catering to active consumers. Second, fashion socks with bold designs and premium materials appeal to style-conscious buyers and yield higher profit margins. For example, Bombas has built a business exceeding USD 300 million by focusing on comfort features such as reinforced heels and seamless toes. This success demonstrates that consumers are willing to pay premium prices for products that combine functionality and comfort.

Body stockings cater to niche markets in fashion and intimate apparel, offering unique options for specific consumer preferences. Meanwhile, knee-highs and hold-ups attract individuals seeking comfort without the need for full-leg coverage. Hosiery accessories, including garters, clips, and storage solutions, remain a low-margin and low-growth segment with limited potential for innovation. The faster growth of tights and pantyhose highlights a shift toward products that effectively blend fashion and functionality. Features such as seamless construction, control-top designs, and moisture-wicking fabrics address consumer concerns related to comfort and durability. Additionally, innovations like bonded panels and laser-cut edges help eliminate visible panty lines, which is a significant factor influencing purchases for professional and evening wear. Graduated compression variants further appeal to travelers and healthcare workers by offering circulation benefits, addressing both health and comfort needs.

By End-User: Women Lead, Men's Segment Surges on Athleisure and Workplace Shifts

Women accounted for 68.32% of the 2025 revenue, driven by demand for professional attire, fashion hosiery, and shapewear. However, the men's hosiery market is projected to grow at a compound annual growth rate (CAGR) of 6.97% through 2031, as the blending of workplace formality and athleisure trends reduces traditional gender distinctions. SKIMS reported that men's products contributed significantly to its sales, while the French brand Les Belles noted that half of the customers purchasing men's tights identified as male. This indicates a growing acceptance of men's hosiery beyond niche markets. The growth of the men's hosiery market is primarily attributed to three key categories: formal dress socks for professional use, performance socks for athletic activities, and compression tights for travel and recovery purposes. In contrast, kids' hosiery remains stable, supported by school uniform requirements and seasonal gifting, though it continues to lag behind adult segments in terms of innovation and profit margins.

The potential for growth in men's hosiery extends beyond product development to include marketing strategies and retail positioning. Historically, legacy brands have marketed men's socks as purely functional items, with limited emphasis on their fashion appeal. Bombas, a direct-to-consumer brand, has achieved notable revenue by focusing on comfort-oriented features such as reinforced heels and seamless toes. This demonstrates that men are willing to invest in products that provide functional benefits and enhanced comfort.

By Price Range: Mass Segment Holds Share, Premium Tier Grows on Innovation

The mass segment accounted for 60.03% of the revenue in 2025, highlighting hosiery's traditional role as a consumable commodity. However, the premium segment is projected to grow at a compound annual growth rate (CAGR) of 7.26% through 2031, driven by the adoption of technical fabrics, designer collaborations, and sustainability-focused offerings. Mass-market players focus on competitive pricing and extensive distribution networks, utilizing supermarket and hypermarket placements to capture impulse purchases. On the other hand, premium brands emphasize durability, comfort, and compelling brand narratives to justify price premiums ranging from 50% to 100% over standard nylon-spandex blends.

This segmentation reflects a broader trend of consumer polarization. Value-conscious buyers are increasingly drawn to private-label and fast-fashion options, while affluent consumers prefer brands that deliver measurable performance benefits or adhere to ethical sourcing practices. Calvin Klein's shapewear launch in 2025, priced between USD 34 and USD 104, serves as a clear example of premium positioning. The brand leverages its equity and incorporates technical innovations, such as targeted compression zones, to appeal to this segment of consumers.

By Distribution Channel: Supermarkets Dominate, Online Retail Accelerates

Supermarkets and hypermarkets are projected to account for 46.89% of the revenue in 2025, benefiting from high foot traffic and the influence of impulse purchases. In contrast, online retail stores are anticipated to grow at a compound annual growth rate (CAGR) of 7.68% through 2031. This growth is attributed to the rising prominence of direct-to-consumer brands, the dominance of online marketplaces, and the adoption of personalized sizing tools. Specialty stores maintain a niche position by offering curated product assortments and fitting services, which support premium pricing. Other channels, such as vending machines and airport kiosks, address the needs of consumers seeking emergency replacements. Brands that invest in artificial intelligence (AI)-powered sizing recommendations, virtual try-on tools, and detailed product imagery are effectively reducing return rates and improving unit economics. Social commerce has emerged as an important discovery channel, with a significant percentage of consumers inclined to purchase items featured in live-streams. This trend is particularly pronounced among younger generations, such as Generation Z, presenting opportunities for hosiery brands to showcase fit and styling in real-time. By leveraging these tools, brands can better align with consumer expectations and enhance the overall shopping experience.

Specialty stores continue to play a critical role in premium and shapewear categories, where in-person fittings and expert advice justify higher price points. However, these stores must adopt omnichannel strategies to remain competitive and align with the majority of purchase journeys that begin with online research. By integrating physical and digital touchpoints, specialty stores can deliver a seamless shopping experience that caters to modern consumer behavior while preserving their unique value proposition.

Geography Analysis

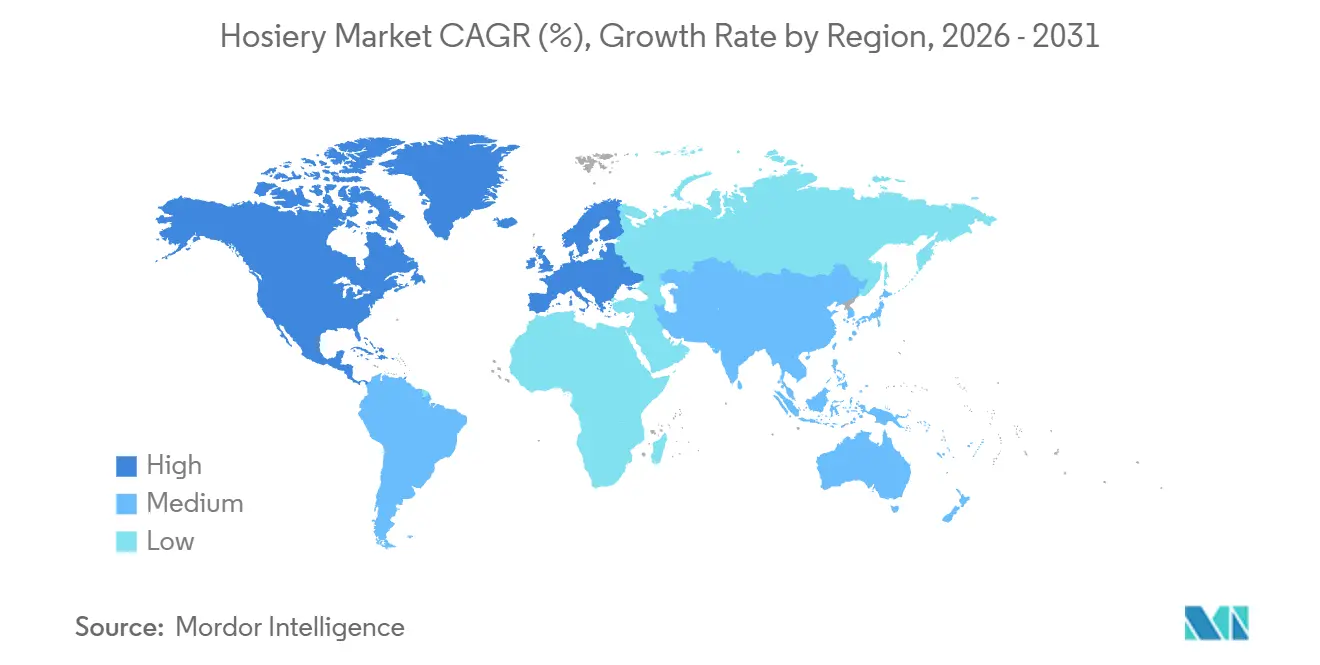

Europe continues to lead the global hosiery market, contributing 39.88% of the projected revenue for 2025. This leadership is supported by its renowned fashion capitals, a well-established retail infrastructure, and strict textile regulations that favor brands with strong compliance capabilities. Key markets such as Germany, the United Kingdom, Italy, and France drive demand due to professional attire requirements and high per-capita hosiery consumption. Additionally, Eastern European markets offer growth potential as disposable incomes increase and Western fashion trends gain popularity. The European Union's Textile Strategy 2024, which enforces extended producer responsibility and minimum recycled-content thresholds, is encouraging the use of eco-friendly fibers while creating challenges for non-compliant imports. Despite revenue challenges, such as Wolford's fiscal 2024 sales decline by 30% to EUR 126.9 million, brands like Wolford and Falke maintain loyal customer bases due to their heritage and technical expertise [3]Source: European Commission, “EU Ecolabel,” environment.ec.europa.eu. However, European companies must carefully balance sustainability investments with profit margins, as consumers remain hesitant to pay higher prices despite their stated environmental concerns.

The Asia-Pacific region is the fastest-growing segment in the global hosiery market, with a projected compound annual growth rate (CAGR) of 7.43% through 2031. This growth is fueled by urbanization, rising middle-class incomes, and the increasing adoption of Western fashion in countries such as China, India, and Southeast Asia. According to McKinsey's State of Fashion 2025 report, China's share of United States apparel imports declined by approximately 6 percentage points between 2019 and 2023, as production shifted to India, Vietnam, and Bangladesh, where labor costs are 50% lower than in China. India has emerged as a significant sourcing hub for hosiery manufacturers, supported by approximately USD 2.5 billion in Production-Linked Incentives for textiles and a threefold increase in foreign direct investment since 2019. These developments position the region as a cost-effective and nearshoring alternative for global manufacturers.

Other regions, including North America, South America, and the Middle East and Africa, collectively hold smaller shares of the global hosiery market but exhibit distinct characteristics. North America benefits from the growing popularity of athleisure and the rise of direct-to-consumer innovations, with brands such as Bombas gaining traction. South America is experiencing steady growth driven by urbanization and the modernization of retail infrastructure. In contrast, the Middle East and Africa remain emerging markets, limited by lower per-capita incomes and underdeveloped retail infrastructure outside major urban areas. Companies entering these regions need to adopt standardized product platforms while customizing sizing, pricing, and distribution strategies to align with local market conditions and achieve profitability.

Competitive Landscape

The hosiery market is characterized by fragmentation, with established players, new entrants focused on athleisure, and disruptors emphasizing sustainability competing for market share. Legacy brands such as HanesBrands, Golden Lady, Wolford, and Falke benefit from strong brand equity and extensive distribution networks. However, they face increasing margin pressures due to the expansion of private-label products and competition from direct-to-consumer brands. HanesBrands reported fourth-quarter 2024 sales of USD 1.3 billion, reflecting a 12% decline compared to the previous year. In response, the company launched the Hanes Moves activewear line in 2024 and 2025 to address the growing demand for athleisure products. Calzedonia Group, which achieved over EUR 3.5 billion in revenue in fiscal 2024 with a 13.5% growth rate, demonstrates the benefits of vertical integration and geographic diversification. The company operates retail stores across Europe, Asia, and the Americas while maintaining control over its manufacturing and design processes.

Growth opportunities in the hosiery market are centered on technical innovation, sustainability, and addressing underserved demographics. Brands that focus on advanced features such as moisture-wicking fibers, anti-bacterial treatments, and seamless construction can differentiate themselves beyond price competition. Additionally, adopting biodegradable yarns and recycled materials appeals to environmentally conscious consumers who are willing to pay a premium for sustainable products. Men's hosiery is emerging as a high-growth niche, with brands like SKIMS and Les Belles demonstrating that mainstream acceptance can extend beyond early adopters when products prioritize comfort and performance. These developments highlight the potential for brands to capture new customer segments by aligning with evolving consumer preferences.

Emerging disruptors are redefining the hosiery market. For instance, Heist Studios doubled its revenue in 2024 by positioning tights as fashion accessories, while Swedish Stockings, which uses 82% recycled polyamide, challenges established players by reshaping category norms. Technology adoption also varies significantly across the market. Leading brands are utilizing artificial intelligence (AI)-powered sizing tools and virtual try-on features to reduce return rates and improve customer satisfaction. In contrast, competitors relying on static size charts and generic product imagery face higher return-related costs, which negatively impact their profit margins. Regulatory compliance is another critical factor in the market. Adherence to standards such as OEKO-TEX Standard 100 and Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH) restrictions is essential in Europe and North America. However, smaller producers with limited research and development resources face increasing pressure to exit the market as reformulation costs continue to rise.

Hosiery Industry Leaders

Hanesbrands Inc

Jockey International, Inc.

Wolford AG

Falke KGaA

Golden Lady Company S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Swedish Stockings collaborated with influencer Camille Charrière to create a collection of fashionable, responsibly produced tights. This partnership leveraged influencer marketing to promote the brand's core message of sustainability and stylish, durable legwear.

- November 2024: Windsong Global, the new owner of L'eggs, relaunched the brand to appeal to a younger, Gen Z audience. The new line of shapewear tights, including the "360 Contour" collection, was made from recycled yarns and featured innovative knitting techniques to provide modern shaping and comfort in various colors and patterns.

- May 2024: PUMA collaborated with luxury retailer Coperni as part of their full Spring/Summer 2024 collection and launched a range that included fashion-forward tights and bodysuits. The collection fused athletic influences with high fashion and targeted consumers seeking performance and style in their legwear.

Global Hosiery Market Report Scope

The global hosiery market includes knitted legwear products such as socks, stockings, tights, pantyhose, and leggings. These products are made from materials like cotton, nylon, and spandex, catering to fashion, comfort, and performance needs worldwide. The market is segmented based on product type, end-user, price range, distribution channel, and geography. The product type segment includes body stockings, socks, knee-highs and hold-ups, tights and pantyhose, and hosiery accessories. The end-user segment is categorized into women, men, and kids. The price range is divided into mass and premium categories. The distribution channel includes supermarkets and hypermarkets, specialty stores, online retail stores, and other distribution channels. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Body Stockings |

| Socks |

| Knee-highs and Hold-ups |

| Tights and Pantyhose |

| Hosiery accessories |

| Women |

| Men |

| Kids |

| Mass |

| Premium |

| Supermarkets and Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Body Stockings | |

| Socks | ||

| Knee-highs and Hold-ups | ||

| Tights and Pantyhose | ||

| Hosiery accessories | ||

| By End-User | Women | |

| Men | ||

| Kids | ||

| By Price Range | Mass | |

| Premium | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the hosiery market be by 2031?

It is projected to reach USD 92.87 billion by 2031, rising at a 5.45% CAGR from 2026 through 2031.

Which product group is growing the fastest within global legwear?

Tights and pantyhose are forecast to expand at 6.83% CAGR due to workplace dress code revival and fabric innovations that merge comfort with style.

What drives premium pricing in women’s legwear?

Seamless knitting, moisture-wicking fibers such as LYCRA DRY, and sustainability credentials like recycled polyamide justify 20-30% premiums over mass nylon blends.

Why is Asia-Pacific pivotal for future hosiery demand?

Urbanization, rising middle-class incomes, and Western fashion adoption push Asia-Pacific growth to 7.43% CAGR, outpacing all other regions.

How are brands addressing high e-commerce return rates?

AI-based sizing tools, detailed imagery, and virtual try-on apps cut fit-related returns, improving profitability as online sales gain share.

Page last updated on: