Down and Feather Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

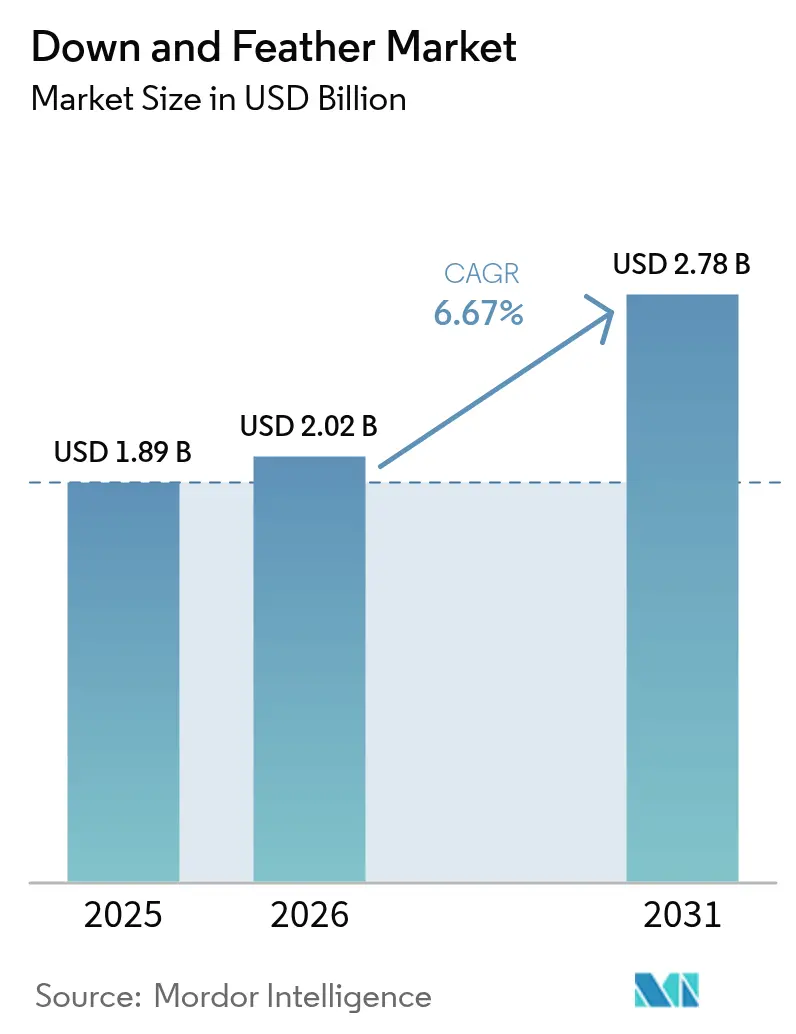

| Market Size (2026) | USD 2.02 Billion |

| Market Size (2031) | USD 2.78 Billion |

| Growth Rate (2026 - 2031) | 6.67% CAGR |

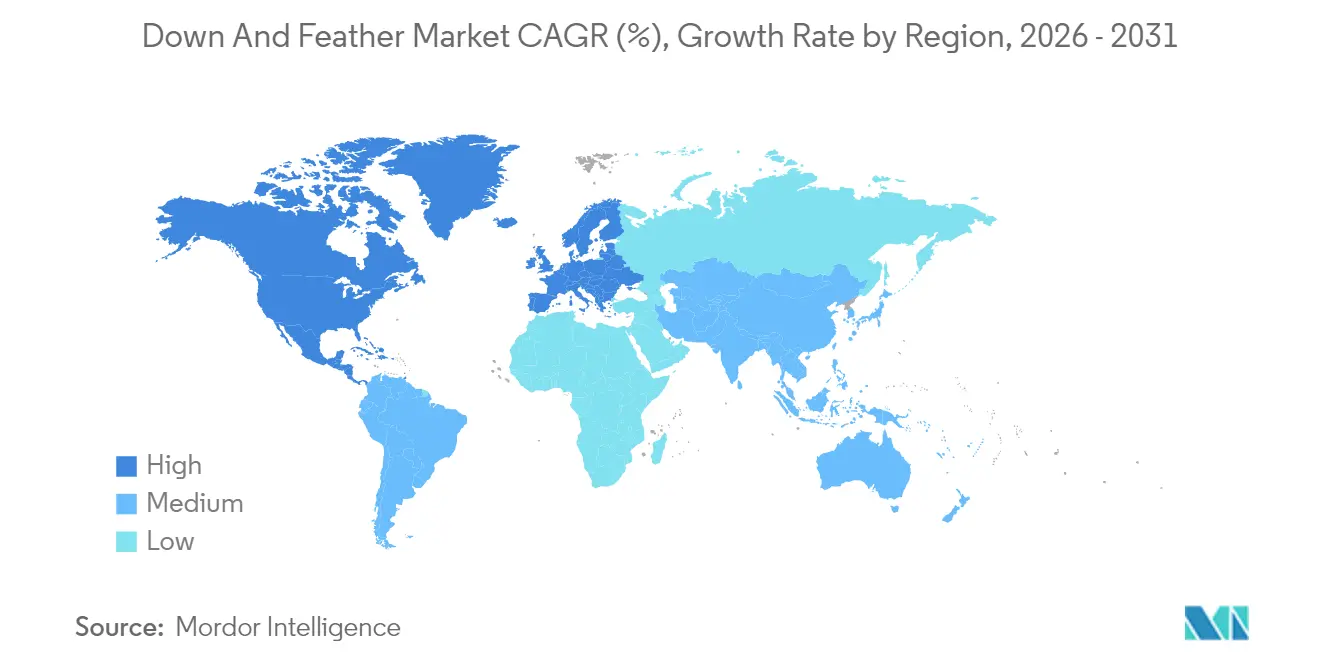

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Down and Feather Market Analysis by Mordor Intelligence

Down and feather market size in 2026 is estimated at USD 2.02 billion, growing from 2025 value of USD 1.89 billion with 2031 projections showing USD 2.78 billion, growing at 6.67% CAGR over 2026-2031. This growth underscores a global shift towards premium natural insulation, as consumers increasingly prioritize both sustainability and performance. Factors such as rising disposable incomes in emerging markets, a surge in outdoor recreational activities, and tightening ecological regulations bolster this demand. Furthermore, initiatives like ethical sourcing and the incorporation of recycled materials are unveiling new revenue avenues for suppliers. While duck-origin fills dominate the mass market, there's a noticeable shift towards goose down and high-fill-power recycled alternatives. Consumers are willing to invest more for benefits like reduced weight, enhanced loft, and assured sourcing transparency. Manufacturers prioritizing traceability and adopting PFC-free water-repellent treatments are safeguarding their margins, even as synthetic insulations close the performance gap. Despite facing challenges from avian influenza outbreaks and escalating feed costs, the industry is countering with measures like enhanced biosecurity funding and diversifying geographically. Highlighting the industry's vigilance, the National Institutes of Health (NIH) reported 743 detections of HPAI A(H5) in Europe across 31 countries between December 2024 and March 2025, predominantly in waterfowl like mute swans and barnacle geese[1]Source: National Institutes of Health (NIH), "Avian influenza overview December 2024–March 2025", www.pmc.ncbi.nlm.nih.gov.

Key Report Takeaways

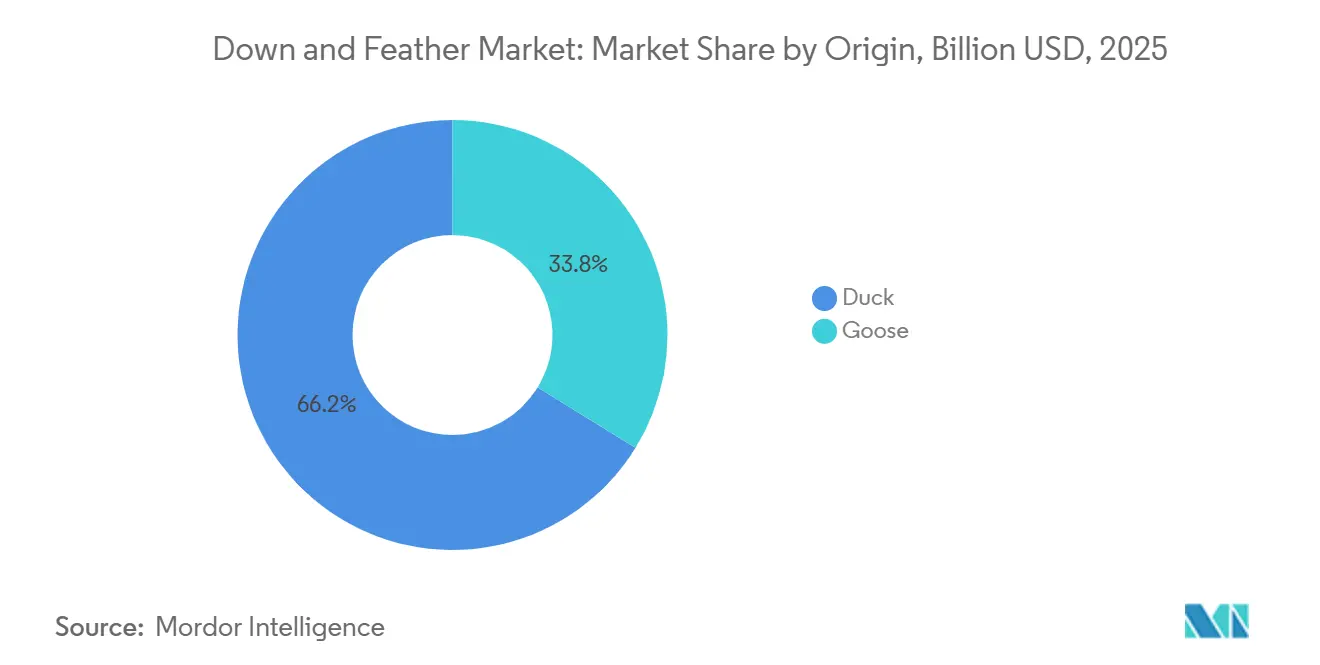

- By origin, duck down led with 66.21% of down and feather market share in 2025, while goose down is projected to expand at a 7.55% CAGR through 2031.

- By type, virgin down commanded 47.12% of the down and feather market size in 2025, whereas recycled down is advancing at a 7.62% CAGR for the same period.

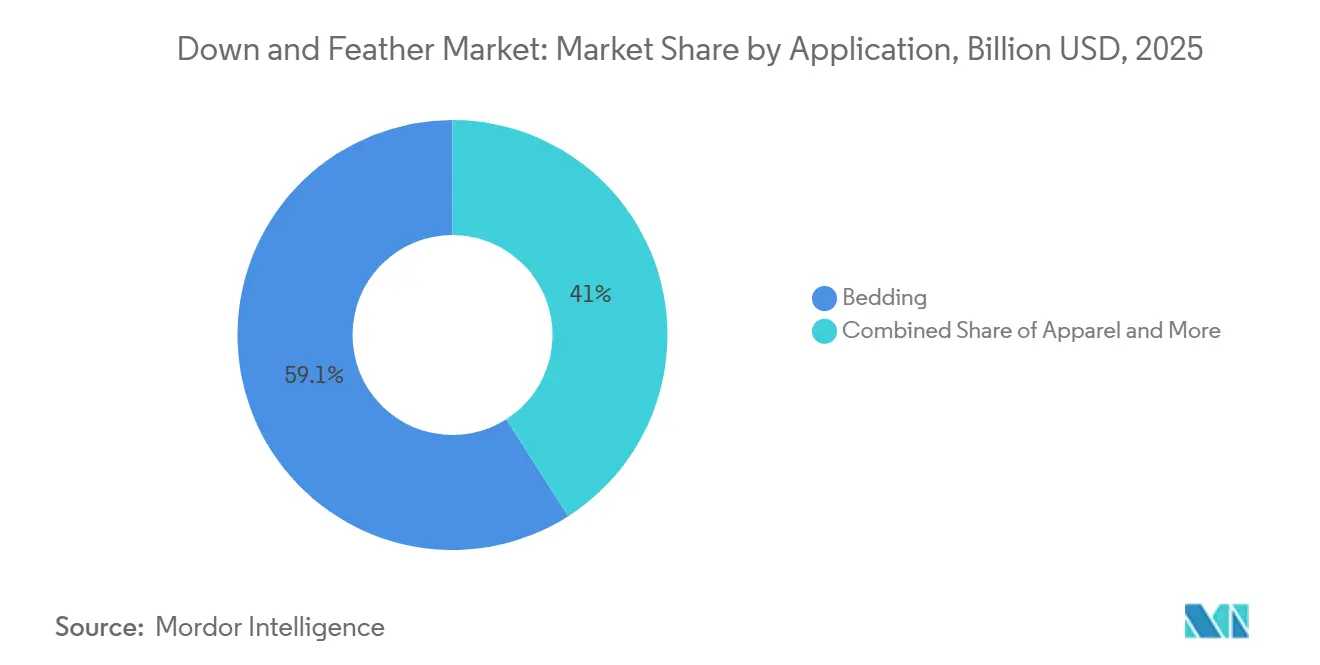

- By application, bedding accounted for 59.05% revenue share in 2025; apparel is set to grow at an 8.12% CAGR to 2031.

- By geography, North America represented 41.98% of the down and feather market in 2025, and Asia-Pacific is forecast to post an 8.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Down and Feather Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for premium, natural, and luxury products | +1.8% | Global, with a premium focus in North America and Europe | Medium term (2-4 years) |

| Growth of the outdoor recreation and adventure tourism industry | +1.5% | North America and Europe core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Increasing focus on sustainability and ethical sourcing | +1.2% | Global, led by the European regulatory framework | Medium term (2-4 years) |

| Technological innovations in processing and treatments | +0.9% | Global, with innovation centers in North America and Europe | Long term (≥ 4 years) |

| Increased demand from the hospitality sector | +0.7% | The Asia-Pacific and North America, expanding to emerging markets | Short term (≤ 2 years) |

| Demand for lightweight and high-performance products | +0.6% | Global, concentrated in the outdoor apparel segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Preference for Premium, Natural, and Luxury Products

As consumers increasingly link natural down with luxury and authentic performance, premium product positioning emerges as the primary growth driver. In 2023, Consumer Reports highlighted that about 43% of U.S. participants spent between USD 50 to 100 on new queen-sized bedsheets. The same survey revealed that fabric feel was a crucial factor for at least half of the U.S. participants when purchasing bedsheets[2]Source: Consumer Reports, "American Experiences Survey: A Nationally Representative Multi-Mode Survey, January 2023", www.article.images.consumerreports.org. This trend goes beyond traditional price sensitivity. For instance, Hungarian white goose down, despite facing supply constraints, commands a premium price, with prices surging over 50% in the last five years. This premiumization isn't limited to raw materials; it extends to finished products. Brands are now using certifications like RDS and GOTS not only to meet consumer demands for transparency and quality but also to justify higher margins. The luxury bedding segment reaps significant benefits from this trend. Companies like Down & Feather Company are marketing 750-800 fill power Hungarian goose down as premium offerings, paired with GOTS-certified organic cotton shells. The hospitality industry further amplifies this trend. Hotels are investing in premium down bedding, enhancing guest experiences and justifying higher room rates, thus fueling a growing demand for high-quality natural fills.

Growth of the Outdoor Recreation and Adventure Tourism Industry

As outdoor recreation expands, there's a growing preference for natural down's superior warmth-to-weight ratio over synthetic alternatives. This sector's growth fuels demand for specialized products, such as ultralight down gear. A prime example is Stellar Equipment's Ultralight Down 2.0 program, which boasts 850 fill-power European goose down in garments weighing a mere 282 grams, yet ensuring comfort in temperatures as low as -9°C. With the rise of adventure tourism, the apparel segment stands to gain the most. Consumers are on the lookout for gear that not only performs in varied climates but is also travel-friendly. Highlighting this trend, the Outdoor Foundation reports that in 2024, over 63.4 million Americans engaged in hiking, marking the highest participation since 2010 and a notable 31% point increase over 15 years[3]Source: Outdoor Foundation, "2025 Sports, Fitness, and Leisure Activities Topline Participation Report", www.sfia.users.membersuite.com. The trend isn't limited to traditional mountaineering; urban outdoor activities are on the rise, presenting opportunities where fashion meets technical performance. This blend of outdoor gear with everyday wear is a key reason the apparel segment is witnessing the fastest growth rate at an impressive 8.47% CAGR.

Increasing Focus on Sustainability and Ethical Sourcing

With only 4% of the world's down and feathers meeting animal welfare certification standards, the push for sustainability is reshaping supply chains and opening doors for ethically compliant suppliers. The Responsible Down Standard (RDS) has become the gold standard in the industry. Textile Exchange highlights a swift adoption by major brands, aiming to distance themselves from the negative spotlight of live-plucking allegations. Companies like Re: Down, with facilities in Hungary and China, are at the forefront, turning post-consumer bedding and apparel into certified recycled fills, embodying the principles of a circular economy. The European Union's animal welfare frameworks are setting global benchmarks, steering sourcing choices even outside EU borders. This trend underscores the competitive edge for suppliers who proactively embrace traceability and ethical sourcing.

Technological Innovations in Processing and Treatments

Innovations in processing are not only creating new product categories but also broadening market applications and overcoming traditional limitations. For instance, DownTek's PFC-free water-repellent technology, which is bluesign-approved, showcases this trend. It allows down insulation to perform in wet conditions while ensuring environmental compliance. Similarly, Allied Feather + Down's ExpeDRY technology is a notable advancement. By harnessing gold nanoparticles, it speeds up water evaporation without resorting to chemical treatments, thus tackling both performance and sustainability issues. The processing of recycled down has seen significant strides. Advanced washing and sterilization techniques now yield over 750 fill power from post-consumer materials, all while preserving hypoallergenic traits. Such innovations not only broaden down's market reach but also address historical concerns related to moisture sensitivity and ethics. This convergence of technologies is forging new competitive advantages for companies that invest in proprietary processing methods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ethical concerns and consumer backlash regarding animal welfare | -1.4% | Global, most pronounced in Europe and North America | Medium term (2-4 years) |

| Increased competition from advanced synthetic alternatives | -1.1% | Global, with premium synthetic adoption in outdoor markets | Long term (≥ 4 years) |

| Risk of bird disease outbreaks | -0.8% | Global, concentrated in major production regions | Short term (≤ 2 years) |

| Higher production costs and consumer price sensitivity | -0.6% | Global, with emerging market price sensitivity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ethical Concerns and Consumer Backlash Regarding Animal Welfare

Ongoing investigations continue to document live-plucking practices, highlighting the persistent reputational risks tied to animal welfare controversies, despite industry assurances. This challenge is intensified by the fact that many ducks and geese endure inadequate welfare standards, with only 4% of global production achieving animal welfare certifications. This issue is further underscored by a notable decline in the production of down and feather quilts. For instance, data from Japan's Ministry of Economy, Trade, and Industry reveals that the production volume of down and feather quilts in Japan's textile industry fell to 1.08 million sheets in 2023, marking the industry's lowest output in a decade. Major brands, such as Canada Goose, face heightened scrutiny from activist organizations. Even after securing RDS certification, Canada Goose remains under the spotlight, underscoring the lasting impact of historical practices. The fallout from this scrutiny extends beyond just consumer sentiment; it influences institutional procurement policies as well. In a move to reinforce their sustainability commitments, companies like H&M are gradually eliminating virgin down from their offerings. This transition has created a bifurcated market: certified ethical suppliers are now able to command premium prices, while their uncertified counterparts face dwindling margins and limited market access.

Increased Competition from Advanced Synthetic Alternatives

Synthetic insulation technologies are now matching the performance of natural down, boasting enhanced wet-weather capabilities and ensuring full compliance with animal welfare standards. PrimaLoft's ThermoPlume+ technology stands out in this evolution, ingeniously blending sail-shaped fibers with fiber spheres. This creates a loft effect akin to down, all while using 20% less material than earlier synthetic versions. Meanwhile, The North Face's Heatseeker Eco technology underscores the push for sustainability, utilizing 70-85% post-consumer recycled materials. It also boasts breathability and durability benefits that outshine those of natural down. Advanced synthetic materials pose a significant challenge to down's supremacy, especially in technical outdoor settings where managing moisture is paramount. As synthetic options gain a foothold, they also benefit from cost efficiencies due to larger-scale production. They sidestep the intricate supply chain challenges tied to ethically sourcing down. Consequently, natural down suppliers are pivoting, honing in on premium segments where their product's performance edge is still pronounced.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Origin: Duck Dominance Faces Goose Premium Shift

In 2025, duck-origin materials dominate the market with a 66.21% share, thanks to their cost advantage and the concentrated poultry industry's abundant supply in Asia. Meanwhile, goose-origin products are witnessing a robust expansion, boasting a 7.55% CAGR through 2031, as consumers increasingly acknowledge their superior performance characteristics. China's vast production infrastructure, responsible for about 90% of the world's duck down, allows the duck segment to leverage economies of scale, resulting in competitive pricing for mass-market applications. Goose down, on the other hand, commands a premium due to its larger cluster sizes, which offer higher fill power ratings. These ratings typically range from 600-900 for goose down, compared to 300-700 for duck down, justifying a 50-100% price premium in luxury bedding and high-performance apparel. The swift growth of goose-origin materials underscores a premiumization trend, with consumers valuing performance over price, especially in outdoor apparel where benefits like weight savings and compressibility are paramount.

Goose down from Europe, especially that sourced from Hungary and Poland, fetches the highest premiums. This is attributed to stringent animal welfare regulations and a traditional processing expertise that ensures superior cluster integrity and cleanliness. The market dynamics showcase a clear divide: while duck-origin materials see volume growth in mass-market applications, the value growth is increasingly leaning towards goose-origin products in premium segments. Eiderdown, the ultra-premium offering, is hand-collected from wild Common Eiders in Iceland and Canada. Here, conservation programs facilitate sustainable harvesting, benefiting both habitat protection and local economies.

By Type: Recycled Down Disrupts Traditional Hierarchy

In 2025, down materials command a dominant 47.12% market share, while recycled down is the fastest-growing segment, boasting a 7.62% CAGR. This shift underscores a move towards circular economy principles, hinting at potential changes in competitive dynamics. Traditional down remains favored for its superior thermal performance and natural appeal, especially in premium bedding. Here, its loft and breathability offer a sleep comfort that's hard to match, especially when compared to feather-heavy alternatives. Feather materials, on the other hand, find their niche in cost-sensitive applications. They provide essential structural support in products like pillows, where the quill's stiffness delivers a firmness that pure down can't match. The brisk growth of the recycled down segment underscores the market's response to sustainability mandates. Companies like Patagonia are leading the charge, utilizing 190,000 pounds of recycled down in Fall 2024 and boasting a 33% reduction in CO2 emissions per kilogram when compared to virgin alternatives.

Thanks to processing innovations, recycled down now achieves fill power ratings exceeding 750, rivaling virgin materials and dispelling previous quality concerns. A testament to this progress is Allied Feather + Down's RENU program, which annually recycles over 1 million pounds of textile waste into high-performance recycled down, achieving turbidity ratings beyond 1000mm. The segment's growth is driven by regulatory pressures and corporate sustainability pledges. Brands are increasingly focused on shrinking their environmental footprints without compromising on performance. Yet, there's a significant gap: data from Textile Exchange reveals that in 2023, a mere 0.9% of global down and feathers received certification to the Global Recycled Standard. This statistic not only underscores the segment's growth potential but also highlights the scaling of processing capabilities and the increasing acceptance among consumers.

By Application: Apparel Acceleration Challenges Bedding Dominance

In 2025, bedding applications command a dominant 59.05% market share, underscoring their pivotal role in ensuring sleep comfort and elevating home luxury. Meanwhile, apparel applications are witnessing the swiftest growth, boasting an impressive 8.12% CAGR. This surge is largely attributed to the expanding realms of outdoor recreation and the premiumization of fashion. The bedding segment's consistent performance can be traced to cyclical replacements and a buoyant housing market. As awareness of wellness rises and disposable incomes allow for luxury purchases, consumers are increasingly gravitating towards premium sleep products. The hospitality sector further fuels this bedding boom. Hotels, in a bid to enhance guest experiences and justify premium room rates, are turning to upscale products. A case in point is Pacific Coast Feather Co.'s FeatherBest pillows, commanding a price of USD 120.96 in the hotel market. Beyond bedding, other sectors like automotive insulation and technical textiles are emerging as lucrative avenues, leveraging down's unique thermal properties.

The apparel segment's rapid ascent is driven by a blend of burgeoning outdoor recreation, urban fashion trends, and the demand for technical performance. These factors collectively highlight down's unmatched warmth-to-weight ratio. The segment is reaping rewards from crossover designs that seamlessly merge outdoor functionality with everyday fashion, allowing for premium pricing across diverse consumer demographics. A testament to this trend is Stellar Equipment's ultralight 282-gram jackets, designed for comfort in temperatures as low as -9°C, all while exuding a chic aesthetic. However, the apparel domain is grappling with heightened competition from advanced synthetic materials, which boast advantages in wet conditions. Yet, natural down continues to lead in performance during dry scenarios, where attributes like weight and packability are paramount. Furthermore, the regulatory landscape, particularly RDS certification mandates, is playing an increasingly influential role in apparel sourcing. Brands are keenly aware of the reputational risks tied to animal welfare debates, making these certifications all the more crucial.

Geography Analysis

In 2025, North America accounted for 41.98% of the revenue, driven by its technological leadership and high per-capita spending on outdoor gear and home textiles. Upper-tier bedding benefits from traceable Hutterite goose down sourced from Western Canada. Meanwhile, a broader reshoring initiative is evident with U.S. capital projects, including a USD 6 million Thindown facility inaugurated in New York in May 2024. However, the region isn't immune to production shocks; a recent bird-disease outbreak in 2024–2025 led to the loss of over 28 million layer hens. In response, the federal government allocated USD 1 billion towards biosecurity measures, a move anticipated to stabilize raw material costs in the long run.

Asia-Pacific is on track to achieve an 8.21% CAGR through 2031, positioning it as both the primary engine and growth catalyst for the down and feather market. With China holding a dominant 80% share of the global raw-material supply, it enjoys cost leadership. However, this dominance comes with risks, as evidenced by the recent avian influenza outbreak that led to the culling of over 50 million birds. To mitigate such risks, brand sourcing teams are increasingly turning to Vietnam and Indonesia. These countries, with their new processing plants, offer competitive wages and an expanding port capacity.

While Europe may contribute a smaller volume to the market, it undeniably sets the benchmark for quality standards, commanding premium unit prices. Goose farms in Hungary and Poland often produce clusters exceeding 800 fill-power, making them a perfect fit for luxury bedding and expedition apparel. Europe's push towards a circular economy has birthed a thriving recycled down infrastructure, further enhancing its premium reputation. Moreover, EU regulations on animal welfare and chemical usage have become global benchmarks, influencing sourcing choices for multinational retailers in the down and feather market.

Competitive Landscape

Market concentration remains moderate, with fragmented regional players dominating local supply chains. However, consolidation pressures are intensifying. Ethical sourcing requirements and technological investments are creating barriers to entry, favoring larger, better-capitalized operations. The competitive landscape is bifurcated: volume production is concentrated in Asia, driven by cost-efficient processors, while premium segments are gravitating toward European and North American suppliers. These suppliers offer certified ethical sourcing and advanced processing capabilities. Companies are increasingly centering their strategic differentiation on sustainability credentials. For instance, Allied Feather + Down has launched TrackMyDown.com, the industry's first comprehensive traceability platform, which serves over 100 partner brands.

Technology adoption is creating new competitive moats. This is especially evident in areas like PFC-free water-repellent treatments and recycled down processing. Here, proprietary capabilities are enabling premium positioning and margin expansion. White-space opportunities are emerging at the intersection of sustainability and performance. Companies developing circular economy solutions and advanced processing technologies stand to capture disproportionate value. The competitive dynamics are favoring suppliers who invest early in RDS certification infrastructure and traceability systems. This is crucial as regulatory compliance is evolving from a mere differentiator to a prerequisite for market access.

Emerging disruptors, such as recycled down specialists Re: Down, are making waves. With facilities in Hungary and China, they're processing post-consumer materials into certified fills that directly compete with virgin alternatives. The landscape is increasingly rewarding companies adept at navigating complex ethical sourcing requirements while remaining cost-competitive. This creates sustainable competitive advantages for integrated suppliers who maintain end-to-end control over their value chains.

Down and Feather Industry Leaders

-

Allied Feather & Down Corp.

-

Down-Lite International, Inc.

-

Feather Industries

-

Prauden

-

United Feather & Down

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Hollander Sleep Products, a major player in the bedding industry, acquired the down processing facilities of Feather Industries. This acquisition enables Hollander to vertically integrate its supply chain, speeding up the development of its premium down bedding products.

- May 2024: Duckworth, a company focused on premium wool and down products, introduced its "DownPure" product line. This was a significant development at the raw material level. The line featured a traceable, responsibly sourced goose down and involved a redesigned packaging strategy, which highlighted the focus on supply chain transparency and premium insulation materials.

- March 2024: Chinese processor Chunli International entered a strategic partnership with Ohio Feather Co. to strengthen its global presence. This alliance focused on expanding supply chain efficiency, particularly in providing traceable, premium down products to North American and European markets.

- January 2024: In a major strategic move, raw material processor Allied Feather & Down announced a partnership with the Chinese conglomerate Nanshan Group. The joint venture aimed to develop a regional down-processing and distribution hub in the Asia-Pacific. This collaboration was designed to secure a sustainable and consistent supply chain for down and expand Allied's footprint in a key manufacturing region.

Global Down and Feather Market Report Scope

The down of birds is a layer of fine feathers found under the more rigid exterior feathers. Very young birds are clad only in down. The global down and feather market is segmented by origin into duck and goose and by application into pillows, comforters, bedding, and others. The market covers North America, Europe, Asia-Pacific, and the Rest of the World. The report offers market size and forecasts for the down and feather market in value (USD million) for all the above segments.

| Duck |

| Goose |

| Down |

| Feather |

| Recycled Down |

| Bedding |

| Apparel |

| Other Applications |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Origin | Duck | |

| Goose | ||

| By Type | Down | |

| Feather | ||

| Recycled Down | ||

| By Application | Bedding | |

| Apparel | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the down and feather market?

The global down and feather market size stands at USD 2.02 billion in 2026.

How fast is the sector expanding?

Industry revenue is projected to grow at a 6.67% CAGR from 2026 to 2031.

Which region contributes the most demand?

North America accounts for 41.98% of global revenue and Asia-Pacific also posts the fastest 8.21% CAGR.

Why is recycled down gaining traction?

Brands leverage recycled down to meet net-zero goals, reduce CO₂ by roughly one-third, and secure RDS-compliant supply without sacrificing loft.

What segment shows the highest growth?

Apparel applications are rising at an 8.12% CAGR as outdoor recreation and fashion convergence boost demand for lightweight, high-performance garments.

How are companies addressing animal-welfare concerns?

Leading suppliers obtain Responsible Down Standard certification and deploy traceability tools like TrackMyDown to provide farm-level transparency.

Page last updated on: