Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

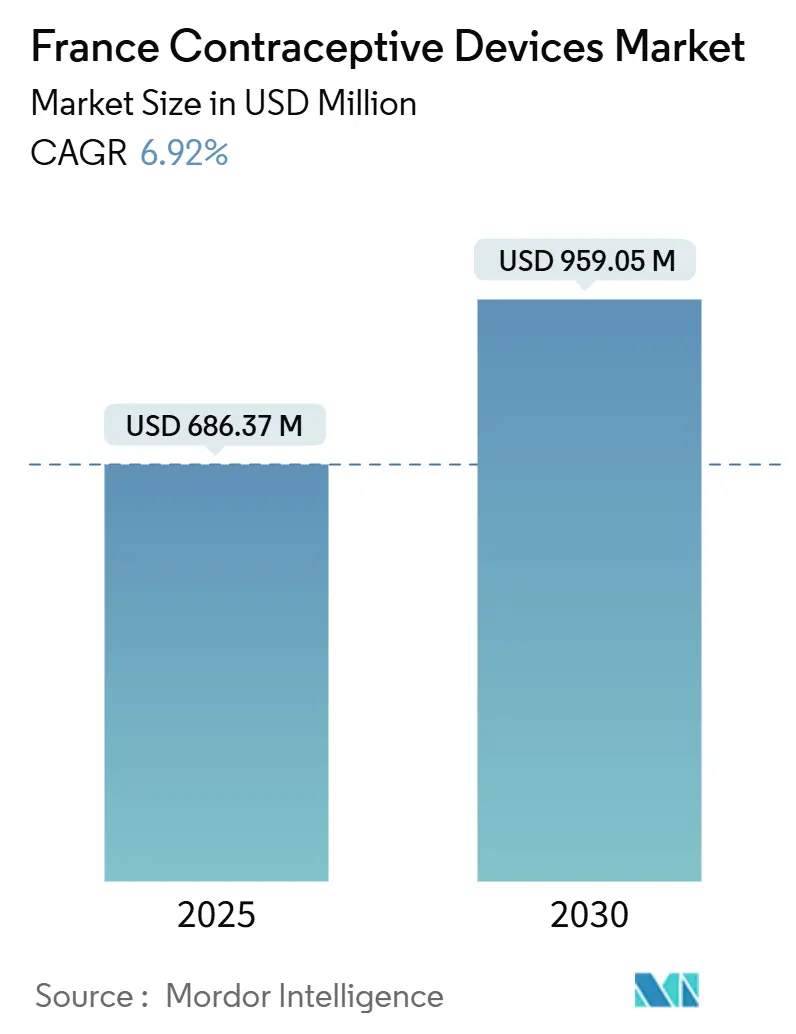

| Market Size (2025) | USD 686.37 Million |

| Market Size (2030) | USD 959.05 Million |

| Growth Rate (2025 - 2030) | 6.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Contraceptive Devices Market Analysis by Mordor Intelligence

The France contraceptive devices market is valued at USD 686.37 million in 2025 and is forecast to reach USD 959.05 million in 2030, advancing at a 6.92% CAGR. Momentum is shifting as male-focused products expand at a 9.01% CAGR while female-oriented devices hold steady share gains. Free condom distribution for residents under 26 years, AI-enabled fertility platforms, and tighter European Medical Device Regulation (MDR) oversight combine to reshape purchasing behavior and product design. Latex supply disruptions since the pandemic spur non-latex research, and digital pharmacies accelerate device availability by bypassing traditional retail bottlenecks. Companies with hormone-free portfolios and strong regulatory compliance capabilities are positioned to capture demand created by safety concerns surrounding hormonal pills and implants.

Key Report Takeaways

- By product type, condoms held 41.62% revenue share of the France contraceptive devices market in 2024, whereas subdermal implants are forecast to expand at a 7.91% CAGR through 2030.

- By gender, female-oriented devices accounted for 72.22% of the France contraceptive devices market share in 2024 while male devices are projected to grow at a 9.01% CAGR between 2025 and 2030.

- By material, latex products captured 83.78% of the France contraceptive devices market size in 2024; non-latex variants are poised to grow at an 8.97% CAGR over the same period.

- By distribution channel, retail pharmacies comprised 57.68% of the France contraceptive devices market size in 2024 and online pharmacies are forecast to rise at an 11.33% CAGR from 2025 to 2030.

France Contraceptive Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High burden of STIs coupled with increased awareness | +1.2% | National with urban concentration | Medium term (2-4 years) |

| High number of unintended pregnancies and delayed family planning | +1.5% | National, 25-34 age group | Short term (≤2 years) |

| Growing popularity of LARC | +1.1% | National with regional adoption gaps | Medium term (2-4 years) |

| E-pharmacy and tele-consult prescription surge | +1.8% | Metropolitan hubs | Short term (≤2 years) |

| Men’s thermal contraception R&D momentum | +0.7% | Progressive regions | Long term (≥4 years) |

| AI-enabled fertility tracking integrated with devices | +0.9% | Tech-savvy demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High burden of STIs coupled with increased awareness

France records rising syphilis and gonorrhea notifications that galvanize demand for dual-protection barrier devices. A 2024 survey showed 60% of clinicians felt under-trained on STI counselling, leaving a knowledge gap that condom brands fill with education initiatives. The government’s January 2023 policy of free condoms for people under 26 immediately broadens reach to cost-sensitive users.[1]Gouvernement français, “Gratuité des préservatifs en pharmacie pour les moins de 26 ans,” info.gouv.fr Brands integrating educational content into packaging and digital apps tap into an evidence-based narrative that condoms prevent both infection and pregnancy. Social marketing around World AIDS Day 2024 further normalised condom use on university campuses. The combination of policy incentives and public campaigns positions barrier devices as essential public-health tools within the France contraceptive devices market.

High number of unintended pregnancies and delayed family planning

France registered 243,623 abortions in 2023, equal to 1 procedure for every 3 live births.[2]Vie Publique, “Interruption volontaire de grossesse : 243 623 IVG en 2023,” vie-publique.fr Abortions are most common among women aged 25-34, who increasingly delay childbirth due to career planning and economic caution. This demographic trend accelerates uptake of long-acting reversible contraceptives that reduce user error. Health insurers reimburse 65% of IUD and implant costs, making them financially attractive for women seeking set-and-forget protection. Manufacturers emphasise real-world effectiveness data to convince sceptical users after several high-profile product recalls. Delayed family planning thus pushes innovation toward user-independent devices with robust clinical backing.

Growing popularity of LARC

IUDs represent 17.7% of prescribed contraceptives, underscoring a shift toward products that require minimal daily attention.[3]Congy et al., “Contraceptive Use Measured in a National Population–Based Approach,” publichealth.jmir.org The EURAS-LCS12 cohort enrolled 7,974 French women and found 96.3% selected IUDs, with lower-dose LNG variants popular among adolescents. The France contraceptive devices market benefits from a 65% reimbursement policy that lowers out-of-pocket cost barriers. Manufacturers must still navigate ANSM audits that scrutinise adverse events, potentially delaying launches but assuring long-term credibility. LARC appeal aligns with lifestyle preferences among dual-income households who value convenience over daily administration.

E-pharmacy and tele-consult prescription surge

Online platforms such as ZAVA recorded nearly 2.3 million European consultations in 2024, reflecting demand for discreet reproductive health services. Digital channels shorten prescription cycles and enable same-day shipping for condoms and emergency contraception, driving an 11.33% CAGR in online sales. AI chatbots embedded within e-pharmacies recommend appropriate devices based on questionnaire logic, increasing conversion rates. Policymakers are drafting guidance to ensure remote prescriptions meet MDR obligations, and compliant firms will gain first-mover advantages. The digital shift expands geographic reach to rural areas where specialist clinics are scarce.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Side-effects and litigation around hormonal devices | -1.3% | National, heightened since 2012 pill scare | Medium term (2-4 years) |

| Cultural resistance among migrant sub-populations | -0.8% | Diverse metropolitan areas | Long term (≥4 years) |

| Supply chain shocks for latex and nitrile | -0.9% | National, latex-dependent products | Short term (≤2 years) |

| Slow CE-mark update pathway for next-gen male devices | -0.6% | EU-wide innovation timeline | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Side-effects and litigation around hormonal devices

Legal action by Androcur users alleging meningiomas underscores safety anxieties that dampen hormonal category growth. June 2024 guidance restricts 3rd and 4th generation pills due to thrombotic risk, and ANSM intensifies pharmacovigilance for related implants. These measures lengthen approval cycles and inflate compliance costs, prompting manufacturers to pivot toward hormone-free platforms. Insurers also reassess reimbursement thresholds, potentially raising patient costs. Such dynamics curb the France contraceptive devices market expansion of hormonal sub-segments.

Cultural resistance among migrant sub-populations

Immigrant women average 2.8 children compared with the national norm of 1.8, indicating lower contraceptive uptake. Research in Seine-Saint-Denis shows 27% of patients at Family Planning Centres experienced intimate partner violence, complicating counselling effectiveness. Language, religious norms, and trust deficits hinder device adoption even when products are reimbursed. Brands must collaborate with community leaders and multilingual NGOs to design culturally sensitive outreach. Without such engagement, demand growth in diverse districts may remain subdued.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type – Condoms retain lead while implants outpace growth

Condoms command 41.62% of the France contraceptive devices market share in 2024 due to policy-backed free distribution and dual-protection messaging, reflecting strong demand in the condom market. The France contraceptive devices market size for subdermal implants is projected to climb at a 7.91% CAGR as women seek hassle-free long-term efficacy. Condoms benefit from cost efficiency and widespread retail reach, yet user error and breakage concerns spur interest in LARC solutions. Diaphragms and cervical caps serve niche hormone-free demand but lack large-scale promotions. Vaginal sponges show modest sales because of lower effectiveness, whereas vaginal rings maintain stable growth through Organon’s NuvaRing portfolio, which generated USD 1.7 billion global women’s health revenue in 2024.

Innovation pipelines target user comfort and eco-friendly packaging. ANSM requires pre-market notification and post-market incident reporting that lengthen go-to-market timelines but raise consumer confidence. Implants tout three-year protection with a single clinical insertion, drawing busy professionals. Spermicidal films integrate with barrier methods for enhanced efficacy but remain secondary purchases. Permanent contraception trends pivot toward male procedures as vasectomies now outnumber female sterilisation since 2021, challenging tubal-clip sales trajectories.

By Gender – Male product acceleration challenges historic female dominance

Female devices hold 72.22% share but male solutions are set for a 9.01% CAGR through 2030, redefining responsibility expectations. Vasectomy procedures scaled from 1,940 in 2010 to 30,288 in 2022 following broader insurance coverage and better surgical training. The France contraceptive devices market size for male products is therefore expanding from a low base yet capturing headlines through start-ups such as Thoreme’s Andro-Switch ring that achieved 99.5% efficacy in trials. Hormonal gel NES/T nears late-phase data readout with 200 volunteers enrolled, underpinning investor confidence.

Female segment growth continues due to reimbursement and medicalisation traditions dating back to the 1975 Veil Law. Safety vigilance remains high, illustrated by 2024 retrieval of a migrated Nexplanon implant via endovascular technique that underscored surveillance needs. Emergency contraception became free for women under 26 in 2025, reinforcing public-funded access. The immigrant fertility differential highlights untapped opportunities for culturally adapted messaging to bolster female device penetration.

By Material – Non-latex innovation challenges natural rubber leadership

Latex accounted for 83.78% of the France contraceptive devices market in 2024, yet allergy awareness stimulates an 8.97% CAGR for synthetic substitutes. Polyurethane and polyisoprene condoms match tensile strength standards and eliminate protein allergens. OEMs gradually retrofit lines to accommodate dual-material production, but capital spend pressures smaller firms. The France contraceptive devices market size for non-latex products rises in hospitals where latex-free guidelines protect staff with sensitivities.

Supply chain risk management drives diversification strategies. The OECD’s 2024 report on medical supply chains flagged latex as a vulnerability, prompting European sourcing initiatives. MDR harmonised standard updates published in March 2024 clarify biocompatibility tests for new polymers, smoothing approval paths. Brand marketing emphasises comfort, odour-less profiles, and vegan certification to differentiate from traditional rubber.

By Distribution Channel – Digital transformation accelerates purchasing

Retail pharmacies still represent 57.68% of the France contraceptive devices market size thanks to walk-in convenience and pharmacist counselling. Online pharmacies, however, grow at 11.33% CAGR as tele-consult scripts integrate with doorstep delivery. Hims & Hers’ plan to acquire ZAVA underscores the strategic value of established digital patient relationships. Platforms leverage AI symptom checkers to triage contraception queries and generate prescriptions inside 10 minutes.

Hospitals and specialist clinics cater to IUD insertion and vasectomy surgeries, ensuring clinical-grade device adoption. Mandatory labelling changes effective January 2025 require clearer ingredient disclosure across all channels, raising compliance workloads but improving consumer trust. Direct-to-consumer startups experiment with subscription models bundling condoms, ovulation tests, and educational content, boosting monthly recurring revenue.

Geography Analysis

Regional patterns in the France contraceptive devices market stem from demographic diversity, cultural norms, and infrastructure disparities. Mainland urban centres such as Paris, Lyon, and Marseille offer dense pharmacy networks and early uptake of e-pharmacy solutions. These cities benefit from high STI campaign visibility and university-driven sexual health programmes that drive condom and LARC volumes. Vasectomy adoption is strongest in Pays de la Loire and Brittany where progressive GP training programmes normalised the procedure.

Overseas departments register abortion rates almost double mainland averages, signalling pronounced contraceptive gaps. Logistics hurdles complicate timely device delivery, prompting authorities to deploy mobile clinics stocked with LARC kits and emergency contraception. Manufacturers that partner with regional health agencies can embed training modules for nurses authorised to insert implants, thereby expanding reach without large hospital footprints.

Cultural heterogeneity shapes market nuance. Districts with high immigrant populations demonstrate elevated fertility and lower device adoption because of language and trust issues. Community health workers recruited from within diaspora networks help translate product instructions and dispel myths. The French equality ministry’s 2025 expansion of EVARS centres places multi-disciplinary teams in underserved suburbs, distributing free condoms and educational brochures. Such initiatives collectively raise baseline demand and support long-term volume growth within the France contraceptive devices market.

Competitive Landscape

The France contraceptive devices market shows moderate fragmentation as multinationals like Bayer, CooperCompanies, and Church & Dwight leverage scale, while niche innovators focus on hormone-free and male-centric breakthroughs. Thoreme exemplifies French engineering strength with its silicone Andro-Switch ring handcrafted in Nouvelle-Aquitaine and currently awaiting ANSM clearance after a 2022 suspension. The product pipeline includes heat-regulated boxers and smartphone-linked temperature trackers that promise discreet male contraception.

Large incumbents hedge risk by investing in diversified portfolios. Bayer announced EUR 400 million to expand its LARC manufacturing campus in Turku, intending to supply European demand for next-generation levonorgestrel IUDs. CooperCompanies reported double-digit European fertility segment growth in Q2 2024, crediting French sales of its Paragard copper IUD. Church & Dwight boosts brand differentiation through eco-friendly condom wrappers and latex-free SKUs.

Digital health convergence becomes a key battleground. Hims & Hers gains immediate pharmaceutical dispensing rights and local medical licences through its ZAVA acquisition, streamlining entry for US-originated contraceptive brands. Local firms integrate AI chatbots that flag contraindications, enhancing clinical decision support and meeting MDR software classification rules. Competitive rivalry therefore spans hardware innovation, regulatory mastery, and digital user engagement, underpinning a dynamic yet moderately concentrated marketplace.

France Contraceptive Devices Industry Leaders

Reckitt Benckiser

Bayer AG

Cooper Surgical Inc.

Church & Dwight Co.

LifeStyles Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Hims & Hers Health announced plans to buy ZAVA, a digital health platform with 2.3 million 2024 consultations, aiming to deepen presence in France, Germany, the UK, and Ireland.

- January 2025: The French health ministry marked the 50th anniversary of the Veil Law by expanding EVARS centres to improve contraception outreach in underserved regions

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the France contraceptive devices market as the annual revenue generated by barrier and long-acting reversible devices, condoms, diaphragms, cervical caps, vaginal sponges or rings, intra-uterine devices, sub-dermal implants, spermicidal inserts, and tubal clips sold through retail, hospital, clinic, and online channels to prevent pregnancy or curtail sexually transmitted infections.

Scope exclusion: Hormonal pills, patches, injectables, permanent surgical sterilization, and digital fertility apps are outside our device-only boundary.

Segmentation Overview

- By Product Type

- Condoms

- Diaphragms and Cervical Caps

- Vaginal Sponges

- Vaginal Rings

- Intra-Uterine Devices (IUD)

- Subdermal Implants

- Spermicidal Devices

- Tubal Sterilization Clips

- By Gender

- Male

- Female

- By Material

- Latex

- Non-Latex

- By Distribution Channel

- Retail Pharmacies & Drug Stores

- Hospital & Specialty Clinics

- Online Pharmacies & D2C Platforms

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with French gynecologists, midwives, retail-chain buyers, and health-insurance officials helped us validate typical replacement cycles, patient preferences, and net of reimbursement price realization across Ile-de-France, Auvergne-Rhone-Alpes, and Occitanie. Follow-up surveys with contraception NGO counselors confirmed uptake accelerators for free, condom schemes and age-band eligibility shifts.

Desk Research

Our analysts started with French Ministry of Health reimbursement schedules, INSEE demographic tables, Eurostat birth-rate files, WITS import data for sheath contraceptives, and WHO reproductive health dashboards, which together anchor usage volumes and price corridors. Trade association notes from SFLS on STI incidence, patent families extracted via Questel showing next-gen copper IUD designs, and Dow Jones Factiva news on retail pharmacy sales seasons sharpened trend signals. Company 10-Ks and D&B Hoovers filings supplied branded ASP clues. The sources above are illustrative; many additional public and proprietary references were consulted.

Market-Sizing & Forecasting

We first reconstructed the national demand pool top-down using the female population of reproductive age, weighted modern-method prevalence, and device-specific switching ratios; results were then cross-checked with bottom-up roll-ups of sampled import volumes and producer revenue disclosures to fine-tune totals. Key variables in our model include the youth LARC adoption rate, latex unit import prices, retail e-pharmacy penetration, and public reimbursement caps. Multivariate regression with scenario analysis projects 2025-2030 sales, while ARIMA smooths short-term seasonality linked to back-to-school campaigns. Gap cells where brand sales were opaque were bridged by channel-level ASP-times-volume proxies derived from primary interviews.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance scans, peer analyst audits, and final research-lead sign-off. Annual refreshes are standard; interim revisions trigger when material events, price controls, safety recalls, or new reimbursement laws shift volumes materially. A last-minute fact-check is completed before report delivery.

Why Our France Contraceptive Devices Baseline Commands Reliability

Published figures often diverge because firms mix drugs with devices, apply different reimbursement netting, or freeze exchange rates at distinct quarters.

Key gap drivers include: (1) our device-only scope versus others' blended drug-device view, (2) model inputs that reflect France's free-under-26 policy from 2023 while some models still rely on pre-2022 uptake, and (3) our yearly refresh cadence, whereas some estimates roll over multi-year without mid-term checks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 686.4 M (2025) | Mordor Intelligence | - |

| USD 7.14 B (2024) | Global Consultancy A | Bundles oral drugs, uses global ASPs, no reimbursement adjustments |

| USD 943.0 M (2024) | Regional Consultancy B | Combines drugs and devices; applies static 2021 FX rates |

| USD 458.2 M (2023) | Trade Journal C | Older base year, omits online pharmacy flows |

In short, by isolating devices, capturing the latest policy shocks, and reconciling top-down demand with bottom-up channel evidence, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace back to clear public metrics and repeatable steps.

Key Questions Answered in the Report

1. What is the current size of the France contraceptive devices market?

The France contraceptive devices market is worth USD 686.37 million in 2025 and is projected to reach USD 959.05 million by 2030.

2. Which product category leads the market?

Condoms lead with 41.62% revenue share in 2024, supported by a national free distribution policy for young adults.

3. Are male contraceptive devices growing faster than female devices in France?

Yes, male devices are forecast to grow at a 9.01% CAGR from 2025 to 2030, outpacing the overall market as thermal and hormonal innovations progress

4. How important are online pharmacies for future sales?

Online pharmacies and direct-to-consumer platforms are expected to grow at 11.33% CAGR, making them the fastest-growing distribution channel.

5. What regulatory body oversees contraceptive devices in France?

The National Agency for the Safety of Medicines and Health Products (ANSM) supervises pre-market notification, CE marking compliance, and post-market surveillance for all contraceptive devices.

6. Why are long-acting reversible contraceptives gaining popularity?

LARCs offer multi-year effectiveness with minimal user intervention, and they benefit from 65% reimbursement by France’s health insurance system, making them attractive for women who prefer convenience and reliability.

Page last updated on: