Wheat Flour Market Size and Share

Market Overview

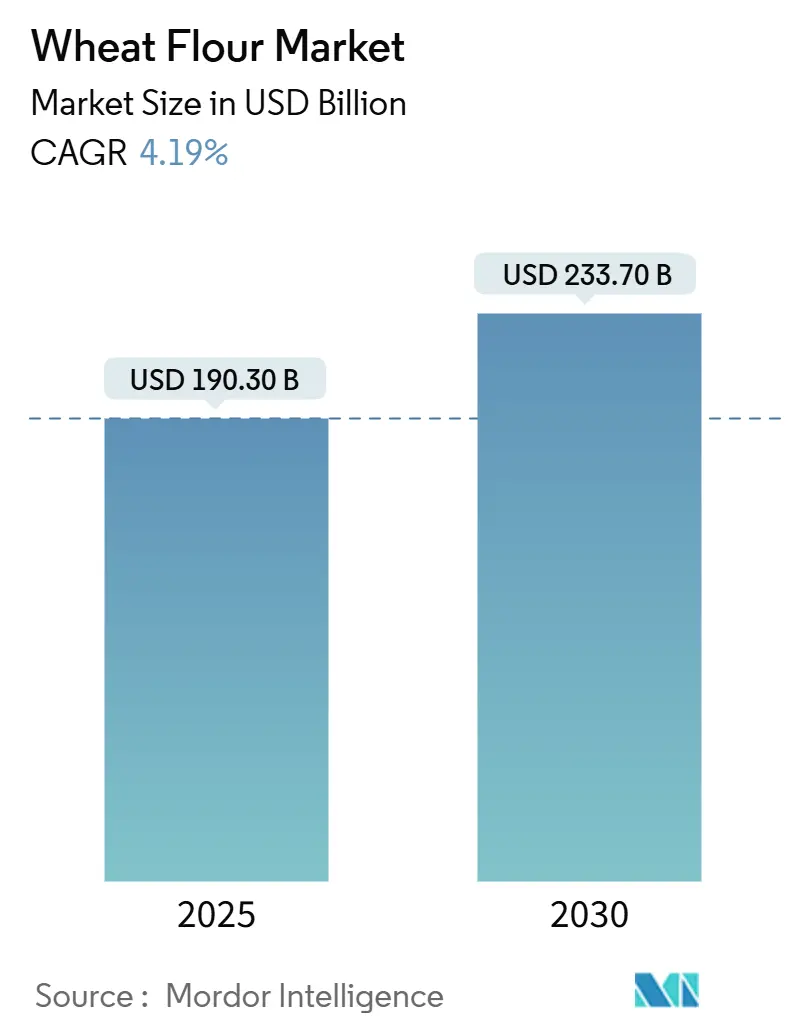

| Study Period | 2020 - 2030 |

| Market Size (2025) | USD 190.30 Billion |

| Market Size (2030) | USD 233.70 Billion |

| Growth Rate (2025 - 2030) | 4.19% CAGR |

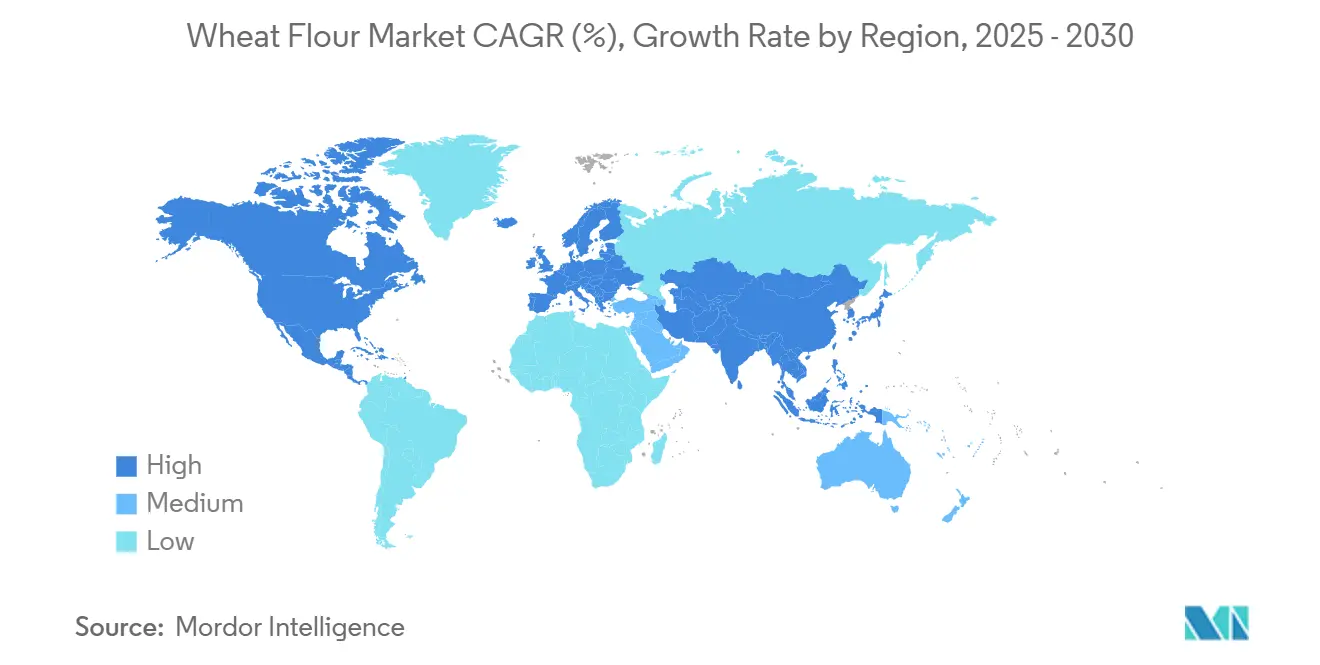

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Wheat Flour Market Analysis by Mordor Intelligence

The wheat flour market, valued at USD 190.3 billion in 2025, is set to climb to USD 233.7 billion by 2030, marking a steady 4.19% CAGR. Growth is bolstered by ongoing urbanization, a steadfast demand for staple foods, and consistent investments in cutting-edge milling technologies, spanning both developed and emerging regions. Industrial processors are enhancing capacities with energy-efficient roller mills and inline fortification systems. These advancements not only boost extraction rates and nutrient retention but also elevate profitability, all while adhering to evolving regulatory standards. As climate-related production risks loom, geographic diversification is reshaping procurement strategies. Millers are broadening their multi-origin sourcing networks and crafting blended-grain formulations to ensure flour consistency, even in unpredictable crop years. Concurrently, a surge in consumer health consciousness is steering innovation funds towards whole-grain, organic, and micronutrient-rich products, which enjoy premium margins across retail, foodservice, and institutional sectors.

Key Report Takeaways

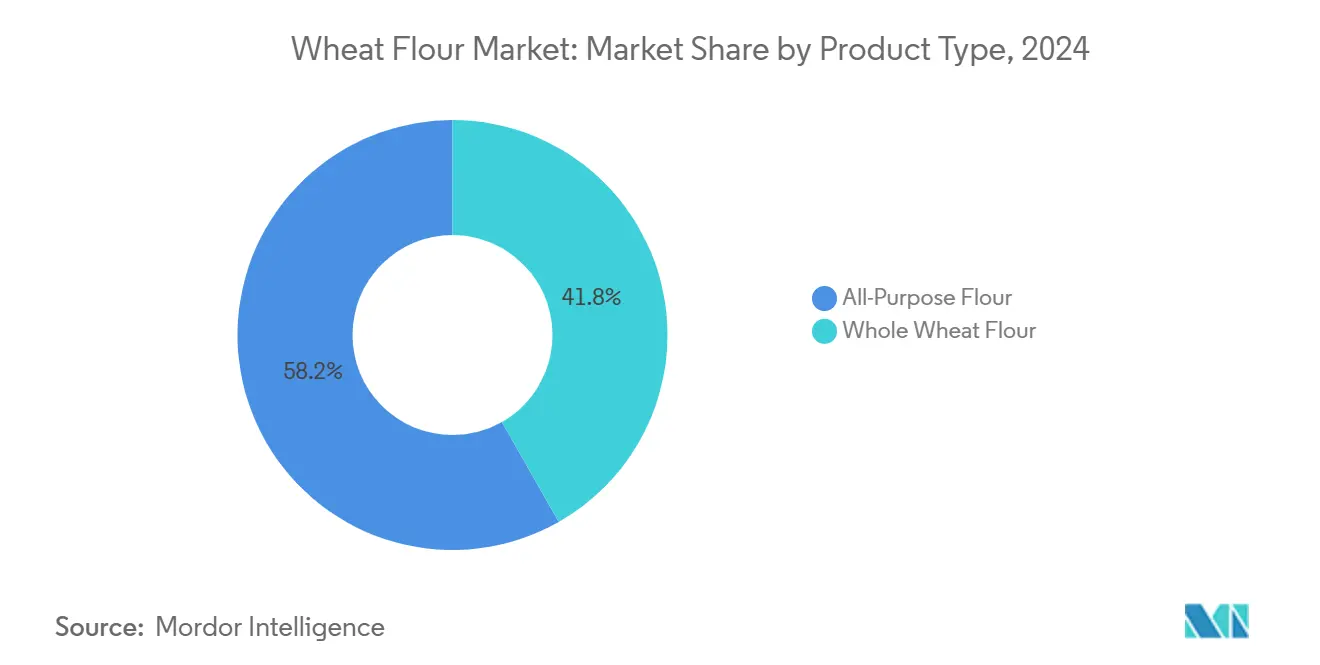

By product type, all-purpose flour accounted for 58.22% of the wheat flour market share in 2024; whole wheat flour registers the fastest 5.28% CAGR to 2030.

By category, conventional flour held 91.25% of the wheat flour market size in 2024; organic flour is projected to grow at a 7.53% CAGR through 2030.

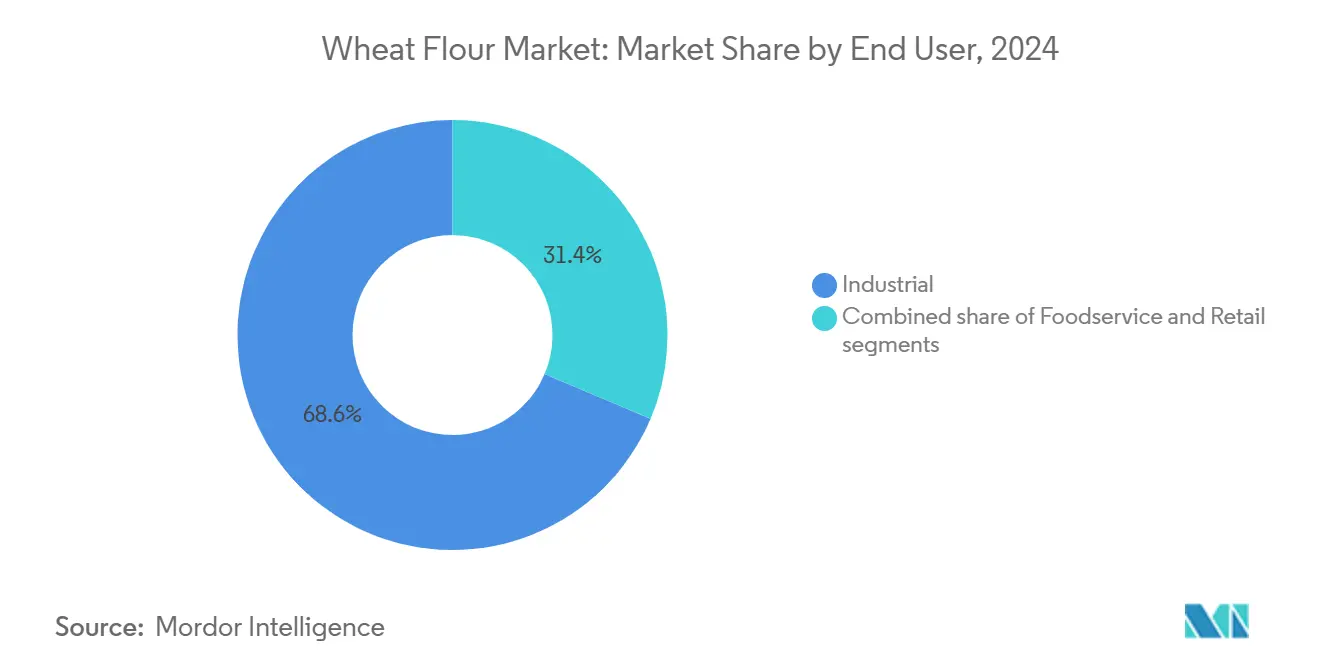

By end user, industrial processing led with 68.63% of wheat flour market share in 2024, while the foodservice & HoReCa segment is forecast to expand at a 6.12% CAGR to 2030.

By geography, Asia-Pacific represented 43.86% of the wheat flour market in 2024, whereas the Middle East & Africa region leads growth at a 7.16% CAGR.

Global Wheat Flour Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for bakery and ready-to-eat foods | +0.8% | Global, with strongest impact in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Growing consumption of wheat-based snacks and convenience products | +0.6% | North America and Europe core, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Increasing adoption of fortified wheat flour for nutritional benefits | +0.5% | Middle East and Africa and South Asia primary, with regulatory support in developed markets | Long term (≥ 4 years) |

| Surging interest in home baking among consumers | +0.4% | North America and Europe, post-pandemic sustainability | Short term (≤ 2 years) |

| Technological advancements in flour milling and processing | +0.3% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Expansion of foodservice, HORECA, and institutional catering sectors | +0.5% | Asia-Pacific and Middle East and Africa growth corridors | Medium term (2-4 years) |

Source: Mordor Intelligence

Rising demand for bakery and ready-to-eat foods

The bakery sector's transformation, driven by premiumization rather than mere volume expansion, is significantly increasing wheat flour demand. In 2024, U.S. per capita flour consumption accounted to 128.9 pounds [1]Source: Baking Business, "Per capita flour consumption up modestly in 2024", www.bakingbusiness.com, highlighting how consumers are shifting their preferences toward convenience foods, which require efficient, large-scale industrial flour processing. The ready-to-eat segment is experiencing notable growth, particularly in emerging markets. Urbanization and rising incomes in these regions are reshaping consumption patterns, with more consumers opting for shelf-stable products over traditional fresh preparations due to their longer shelf life and convenience. As this demand grows, manufacturers are adapting flour specifications to meet evolving requirements. They are focusing on ensuring consistent protein content and functional properties, which support extended shelf life, maintain product quality, and align with automated production processes to enhance scalability and efficiency.

Growing consumption of wheat-based snacks and convenience products

The increasing consumption of wheat-based snacks and convenience products is a significant driver of the wheat flour market. The growing preference for ready-to-eat and easy-to-prepare food items, particularly among urban populations, has fueled the demand for wheat flour as a primary ingredient. According to the United States Wheat Associated Report, global wheat consumption reached approximately 800 million metric tons in 2024 [2]Source: U.S. Wheat Associates, "Global wheat consumption to total", www.uswheat.org , driven by the rising popularity of wheat-based products such as biscuits, noodles, and bakery items. Additionally, government initiatives promoting wheat production and consumption, such as subsidies for wheat farmers in countries like India and China, further support market growth. For instance, the Indian government, under its Minimum Support Price (MSP) scheme, ensures fair pricing for wheat farmers, thereby encouraging higher production and availability of wheat flour for various applications. This trend is expected to continue during the forecast period, bolstering the wheat flour market's expansion.

Increasing adoption of fortified wheat flour for nutritional benefits

The increasing adoption of fortified wheat flour is a significant driver in the wheat flour market, as consumers prioritize nutritional benefits. Fortified wheat flour, enriched with essential vitamins and minerals such as iron, folic acid, and zinc, addresses widespread nutritional deficiencies, particularly in developing regions. Governments worldwide are implementing policies to promote the use of fortified wheat flour. In India, the Food Safety and Standards Authority of India (FSSAI) mandates fortification standards for wheat flour under its Food Fortification Resource Centre (FFRC) initiative [3]Source: Food Safety and Standards Authority of India, "Food Safety and Standards (Fortification of Foods) Regulations, 2018", www.fssai.gov.in. Similarly, in Africa, countries like Nigeria have adopted mandatory wheat flour fortification programs to combat malnutrition. These initiatives are expected to drive the demand for fortified wheat flour during the forecast period. Furthermore, the growing awareness among consumers about the health benefits of fortified foods, coupled with government-backed campaigns, is likely to sustain the growth of this segment in the wheat flour market.

Technological advancements in flour milling and processing

Flour milling and processing embrace cutting-edge technologies, driving significant advancements in the wheat flour market. Innovations such as automation, artificial intelligence, and advanced milling equipment have enhanced efficiency, reduced production costs, and improved product quality. These technological developments enable manufacturers to meet the growing demand for high-quality wheat flour while adhering to stringent safety and quality standards. Additionally, the integration of smart technologies in milling processes allows for real-time monitoring and optimization, further boosting productivity and ensuring consistency in output. Such advancements are pivotal in addressing the evolving consumer preferences and supporting the market's growth during the forecast period. Furthermore, the adoption of energy-efficient milling technologies has contributed to reducing the environmental impact of production processes, aligning with global sustainability goals.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility and climate impact on wheat production | -0.9% | Global, with severe impact in major wheat-producing regions | Medium term (2-4 years) |

| Growing consumer preference for gluten-free alternatives | -0.6% | North America & Europe primary, expanding globally | Long term (≥ 4 years) |

| Rising competition from substitute flours | -0.5% | Europe, North America, and regulated Asia-Pacific markets | Long term (≥ 4 years) |

| Storage challenges and limited shelf life of wheat flour | -0.4% | North America, Europe, and affluent urban centers | Medium term (2-4 years) |

Source: Mordor Intelligence

Price volatility and climate impact on wheat production

Climate-induced production volatility is fundamentally altering wheat flour market dynamics, creating supply chain disruptions that extend far beyond traditional seasonal patterns. Price volatility, driven by fluctuating demand, supply chain disruptions, geopolitical tensions, and currency fluctuations, creates uncertainty for producers and impacts market stability. The unpredictability of wheat prices makes it difficult for manufacturers to plan production and manage costs effectively, thereby affecting profit margins. Additionally, climate change exacerbates these challenges by altering weather patterns, leading to extreme conditions such as droughts, floods, and heatwaves. These adverse climatic conditions result in unpredictable yields, reduced crop quality, and increased susceptibility to pests and diseases, further straining the supply chain. The combined impact of these factors disrupts the availability of raw materials, increases production costs, and limits the ability of market players to meet consumer demand consistently.

Growing consumer preference for gluten-free alternatives

Consumers increasingly favor gluten-free alternatives, which poses a significant restraint on the wheat flour market. The rising awareness of gluten-related health issues, such as celiac disease and gluten intolerance, has driven a shift in consumer preferences toward gluten-free products. Additionally, the growing trend of adopting healthier lifestyles has further amplified the demand for gluten-free alternatives. This shift challenges the wheat flour market, as manufacturers face the need to innovate and diversify their product offerings to cater to changing consumer demands. The increasing availability of gluten-free substitutes, such as almond flour, coconut flour, and rice flour, further intensifies the competition, impacting the growth potential of the wheat flour market. Furthermore, the perception of gluten-free products as healthier options, even among individuals without gluten-related health conditions, has contributed to the growing popularity of these alternatives. This trend has led to a decline in the consumption of traditional wheat flour-based products, such as bread, pasta, and baked goods, as consumers explore gluten-free options.

Segment Analysis

By Product Type: Whole Wheat Gains Despite All-Purpose Dominance

In 2024, all-purpose flour commanded a dominant 58.22% share of the wheat flour market, underscoring its trusted status in both industrial bakeries and home kitchens. Its versatility and consistent performance make it a staple ingredient for a wide range of baked goods, including bread, cakes, and pastries. The widespread availability and affordability of all-purpose flour further contribute to its strong market presence, catering to the needs of both large-scale food manufacturers and individual consumers. Its ability to deliver reliable results across various culinary applications ensures its continued preference in the market. Additionally, the product's adaptability to different recipes and its long shelf life make it a convenient choice for households and commercial establishments alike, solidifying its position as a key segment in the wheat flour market.

Meanwhile, whole wheat flour is on the rise, boasting a 5.28% CAGR, poised to reshape the wheat flour landscape as health-conscious consumers increasingly prioritize fiber and nutrient density. The growing demand for healthier food options has driven the adoption of whole wheat flour, which is rich in essential nutrients and dietary fiber. This trend is particularly evident among wellness-oriented consumers who are shifting away from refined flours in favor of more wholesome alternatives. Additionally, the increasing popularity of clean-label and organic products has further propelled the growth of whole wheat flour, making it a key driver in the evolving wheat flour market. The product's association with health benefits, such as improved digestion and better heart health, has also contributed to its rising demand.

Note: Segment shares of all individual segments available upon report purchase

By Category: Organic Acceleration Challenges Conventional Scale

In 2024, conventional variants dominate the wheat flour market, accounting for 91.25% of the market share. This dominance is driven by entrenched distribution networks, cost advantages, and consistent global harvests that ensure a steady supply. Conventional wheat flour remains the preferred choice for consumers and manufacturers due to its affordability and widespread availability. Its established presence in both developed and emerging markets further solidifies its position as the volume leader in the market, leaving little room for competition in this segment.

On the other hand, organic wheat flour is rapidly gaining traction, reflected in its impressive 7.53% CAGR during the forecast period. The growing consumer preference for healthier and sustainably sourced products is fueling the demand for organic flour. Additionally, increasing awareness about the environmental and health benefits of organic farming practices is encouraging producers to expand their organic product portfolios. Although organic flour currently holds a smaller market share, its rapid growth indicates a significant shift in consumer behavior, posing a potential challenge to conventional variants in the long term.

By End User: Industrial Dominance Faces Foodservice Disruption

In 2024, industrial processors dominate the wheat flour market, holding a significant 68.63% share. This dominance is driven by their ability to leverage economies of scale, which allows for cost-efficient production. Additionally, the use of automated production lines ensures consistent quality and high output, meeting the demands of large-scale operations. Long-term supply agreements further contribute to the stability of this segment, enabling processors to secure raw materials at predictable costs and maintain uninterrupted production. These factors collectively position industrial processors as key players in the wheat flour market.

On the other hand, the foodservice and HoReCa segment is experiencing notable growth, with a compound annual growth rate (CAGR) of 6.12%. This growth is fueled by the increasing demand for tailored wheat flour blends that cater to specific culinary needs. These blends are designed to enhance crumb softness, improve freeze-thaw stability, and support the creation of premium artisanal bread, which is gaining popularity among consumers. The focus on customization and quality in this segment highlights its role in addressing evolving consumer preferences and expanding the market for specialized wheat flour products.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

In 2024, Asia-Pacific dominates the wheat flour market, holding a 43.86% share, driven by its dense population, shifting dietary preferences, and established industrial hubs. China's flour consumption is on the rise, bolstered by government-led fortification initiatives, heightening the demand for nutrient-rich grades. Meanwhile, India's public distribution system is fast-tracking the use of fortified whole-grain flours, underscoring the country's commitment to food security. In Japan, a seasoned market with a penchant for premium quality, there's a growing emphasis on precise milling. This trend is pushing suppliers towards near-infrared protein mapping to ensure consistency in every batch.

The Middle East and Africa are poised for growth, boasting a 7.16% CAGR through 2030. Many countries in the region grapple with climatic challenges, leading to a reliance on wheat imports. Egypt stands out as the globe's top wheat importer, directing subsidised flour into its expansive baladi bread initiative, ensuring steady demand. Data from ITC Trade Map reveals that Egypt's wheat flour imports rose to 12,282 tons in 2023, a notable increase from 8,796 tons in 2021. This growth highlights a rising demand for wheat flour in the country over the past two years[4]Source: ITC Trade Map, "Import Volume of Wheat Flour", www.trademap.org. Meanwhile, in the Gulf states, there's a burgeoning appetite for organic and premium flour, paving the way for niche markets and specialty millers.

North America's wheat flour landscape is marked by cutting-edge automation, a commitment to sustainability, and stable consumption rates. Retail flour sales in the United States are bouncing back, thanks to a surge in home baking. In Canada, laws mandating flour enrichment bolster the demand for fortified products. Europe is on a similar trajectory, balancing strict contaminant regulations with a rising trend in artisanal baking. South America, buoyed by wheat harvests in Argentina and Brazil, is not only processing locally but also exporting blends to its Andean and Caribbean neighbors. Despite facing challenges like infrastructure gaps and currency fluctuations, the region's long-term demand for flour as a staple remains robust.

Competitive Landscape

The wheat flour market, characterized by a moderate fragmentation level of 4 out of 10, offers significant opportunities for strategic consolidation. The competitive landscape is shaped by the presence of numerous regional and global players, each striving to capture market share through various strategies. Key players in the market include companies such as Archer Daniels Midland Company, General Mills Inc., and Wudeli Flour Mill Group which have established strong brand recognition and extensive distribution networks. These companies are leveraging their resources to introduce innovative products, such as fortified wheat flour and gluten-free alternatives, to cater to evolving consumer preferences.

In recent years, investments in research and development and partnerships have become prominent strategies for companies aiming to strengthen their foothold in the market. For instance, General Mills Inc. has been actively investing in research and development to introduce healthier wheat flour options, such as whole grain and organic variants, to meet the growing demand for nutritious food products. These strategic initiatives not only help companies expand their market presence but also enable them to address the increasing competition from private-label brands and local manufacturers.

The competitive environment is further influenced by advancements in milling technologies and the rising demand for wheat flour in emerging economies. For example, countries in Asia-Pacific, such as India and China, are witnessing a surge in demand due to population growth and changing dietary habits. This has prompted companies to invest in expanding their production facilities and enhancing their distribution networks in these regions. Additionally, the growing trend of health-conscious consumers opting for fortified and specialty wheat flour products has created new growth avenues for market players. As the market continues to evolve, companies that can effectively adapt to these trends and implement strategic initiatives are likely to gain a competitive edge and achieve sustainable growth.

Wheat Flour Industry Leaders

-

Ardent Mills LLC

-

General Mills Inc.

-

Cargill, Incorporated

-

Archer Daniels Midland Company

-

Conagra Brands, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Michigan's largest flour miller, King Milling Co., unveiled a new six-floor, 35,000-square-foot concrete mill at its flour milling complex. This state-of-the-art facility significantly enhances the company's production capabilities, with a daily production capacity of 8,000 cwts of flour, further solidifying its position as a leader in the regional flour milling market.

- August 2024: Ardent Mills announced plans to update and expand its flour mill in Commerce City, Colorado. This initiative underscores Ardent Mills' commitment to the Mountain West market, focusing on improving efficiency and capacity to better serve its expanding customer base. With the expansion, the Commerce City mill's daily milling capacity will rise by 9,500 hundredweights (cwts) or 475 tons, elevating the total capacity to 28,000 cwts (1,400 tons) per day.

- March 2024: Farmer Direct Foods completed a USD 2 million facility expansion in Salina, Kansas, adding new warehouse space and automated packaging lines for 25-pound and 50-pound flour bags. The expansion enhances operational flexibility and production capacity for stone ground grain products made from Kansas and Colorado wheat.

- January 2024: Bratney, in collaboration with Omas, Cimbria, and PHM Brands, inaugurated a cutting-edge flour mill in Richmond, Utah. This facility stands out as Omas's most significant mill installation in North America, tailored for on-demand flour production catering to the snack food industry.

Global Wheat Flour Market Report Scope

Wheat flour is made by grinding or milling the wheat grain and contains all the constituents of the wheat kernels. The global wheat market (henceforth referred to as the market studied) is segmented by type, category, distribution channel, and geography. By type, the market is segmented into whole wheat flour, all-purpose flour, and others. By category, the market is segmented into organic and conventional. By end user, the market is segmented into hotels, restaurants, catering (HoReCa); retail; and industrial manufacturing. Retail is further sub-segmented into supermarkets/hypermarkets, convenience stores, online stores, and other distribution channels. It provides an analysis of emerging and established economies across the world, comprising North America, Europe, South America, Asia-Pacific, and Middle-East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| By Type | All-Purpose Flour | |||

| Whole Wheat Flour | ||||

| By Category | Organic | |||

| Conventional | ||||

| By End User | Industrial Applications | Food and Beverage Processors | Bakery and Confectionery | |

| Pasta and Noodles | ||||

| Snacks and RTE Foods | ||||

| Other Food Manufacturers | ||||

| Animal Feed | ||||

| Other Industrial Applications | ||||

| Foodservice / HoReCa | ||||

| Household / Retail | ||||

| Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Rest of North America | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Spain | ||||

| Italy | ||||

| Netherlands | ||||

| Sweden | ||||

| Poland | ||||

| Belgium | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| India | ||||

| Japan | ||||

| Australia | ||||

| South Korea | ||||

| Indonesia | ||||

| Thailand | ||||

| Singapore | ||||

| Rest of Asia-Pacific | ||||

| South America | Brazil | |||

| Argentina | ||||

| Chile | ||||

| Peru | ||||

| Columbia | ||||

| Rest of South America | ||||

| Middle East and Africa | Saudi Arabia | |||

| United Arab Emirates | ||||

| South Africa | ||||

| Nigeria | ||||

| Egypt | ||||

| Morocco | ||||

| Turkey | ||||

| Rest of Middle East and Africa | ||||

| All-Purpose Flour |

| Whole Wheat Flour |

| Organic |

| Conventional |

| Industrial Applications | Food and Beverage Processors | Bakery and Confectionery |

| Pasta and Noodles | ||

| Snacks and RTE Foods | ||

| Other Food Manufacturers | ||

| Animal Feed | ||

| Other Industrial Applications | ||

| Foodservice / HoReCa | ||

| Household / Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Columbia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current size of the wheat flour market?

The wheat flour market size stands at USD 190.3 billion in 2025 and is forecast to reach USD 233.7 billion by 2030.

Which region leads the wheat flour market?

Asia-Pacific leads with 43.86% market share in 2024, driven by large populations and mature processing industries.

Which end use segment is growing fastest in the wheat flour market?

The foodservice & HoReCa segment posts the highest CAGR, advancing 6.12% through 2030 as dining-out rebounds.

How is climate change affecting wheat flour supply chains?

Increasing droughts and heat waves have already caused production losses, raising price volatility and forcing millers to diversify sourcing.

Page last updated on: July 2, 2025