Hong Kong Used Car Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

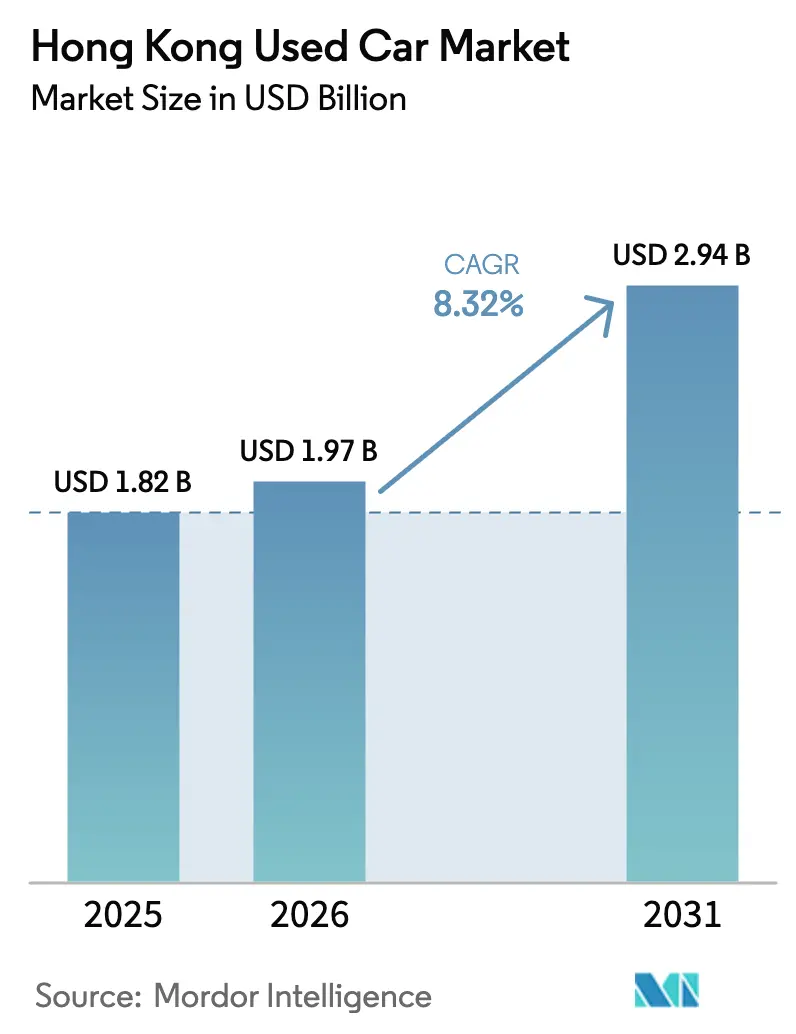

| Base Year Market Size (2025) | USD 1.82 Billion |

| Market Size (2026) | USD 1.97 Billion |

| Market Size (2031) | USD 2.94 Billion |

| Growth Rate (2026 - 2031) | 8.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hong Kong Used Car Market Analysis by Mordor Intelligence

The Hong Kong used car market size was valued at USD 1.82 billion in 2025 and estimated to grow from USD 1.97 billion in 2026 to reach USD 2.94 billion by 2031, at a CAGR of 8.32% during the forecast period (2026-2031). Robust income levels, rapid electrification, and an increasingly digital retail environment position the Hong Kong used car market for sustained growth. City-wide EV incentives accelerate replacement cycles, while cross-border inventory flows under the Greater Bay Area framework increase vehicle variety and price competition. Organized dealers strengthen their footprint as consumers favor professional warranties and transparent vehicle-history checks. However, residual-value uncertainty for electric vehicles, scarce parking, and high tunnel tolls continue to cap demand elasticity.

Key Report Takeaways

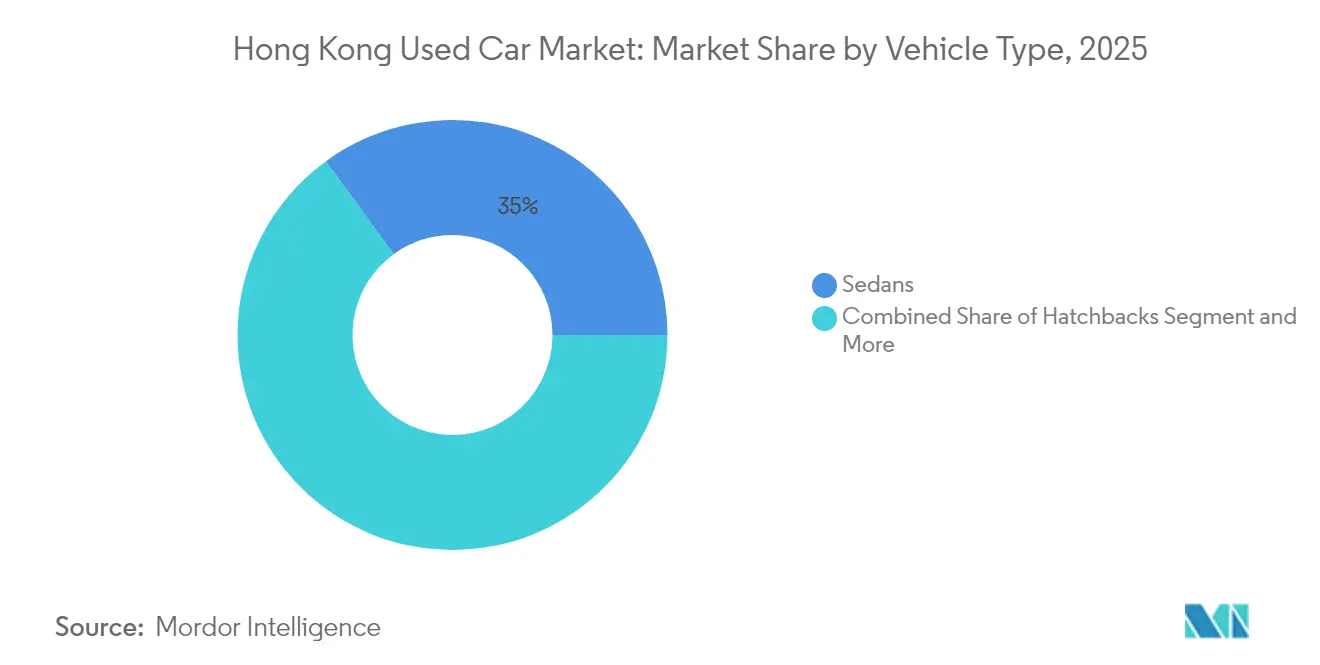

- By vehicle type, sedans led with 35.02% of Hong Kong used car market share in 2025, while sport-utility vehicles are projected to advance at a 7.05% CAGR to 2031.

- By vendor type, organized vendors held 57.05% share of the Hong Kong used car market size in 2025 and are set to grow at 6.55% annually through 2031.

- By fuel type, petrol cars retained 62.58% share of the Hong Kong used car market size in 2025; battery-electric units are expanding at a 13.25% CAGR.

- By vehicle age, 3-5 years cohort captured 38.74% of Hong Kong used car market share in 2025, whereas the the 0-2 years bracket is rising fastest at a 9.85% CAGR.

- By price segment, cars priced above USD 30,000 commanded 28.55% of the Hong Kong used car market size in 2025 and are growing at 9.42% CAGR.

- By sales channel, offline segment accounts for 49.88% of the Hong Kong used car market size in 2025, online platforms are climbing at a 10.10% CAGR, confirming omnichannel uptake.

- By ownership, multi-owner units accounted for 65.72% of the Hong Kong used car marke share in 2025; first-owner resales are growing at 9.25% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Hong kong contributes to a system defined not by any single country or region but by the interaction of many. The global used car market data by Mordor Intelligence represents that combined structure.

Hong Kong Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prices of New Vehicles | +2.8% | Hong Kong Island, Kowloon, New Territories | Medium term (2-4 years) |

| Online Used-Car Platforms' Penetration | +2.1% | Central, Tsim Sha Tsui, Sha Tin | Short term (≤ 2 years) |

| EV-Related Tax Incentives | +1.9% | New Territories, Kowloon | Medium term (2-4 years) |

| Cross-Border Inventory Flows | +1.2% | Shenzhen Bay, Lok Ma Chau border areas | Long term (≥ 4 years) |

| Digital Financing and E-Payment | +0.8% | Central, Admiralty, Causeway Bay | Short term (≤ 2 years) |

| Corporate-Fleet Downsizing | +0.6% | Central Business District, Kwun Tong | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prices of New Vehicles

Higher first-registration tax brackets escalate new-car prices, steering value-minded buyers toward pre-owned alternatives. Scrappage-linked EV incentives of up to HKD 287,500 increase list prices for new electric models, widening the price gulf vis-à-vis used petrol sedans[1]Martin Choi, “Which are the top EV brands and bestselling models in Hong Kong?” South China Morning Post, scmp.com. Extended delivery lead-times caused by semiconductor shortages further redirect demand, especially within the USD 30,000-plus bracket that already holds 28.83% share. Currency swings affecting import costs heighten new-car sticker prices, reinforcing the appeal of the Hong Kong used car market.

Growing Penetration of Online Used-Car Platforms

Investor-backed platforms roll out AI-driven inspections, instant loan approvals, and home-delivery services, propelling online transactions at a double-digit pace. Smartphone ubiquity allows buyers to browse inventory and secure digital financing in minutes, compressing the purchase journey. Offline dealers respond with hybrid models, adding live-chat and virtual showrooms to preserve reach. The convenience and perceived transparency of e-commerce drive the Hong Kong used car market toward a digitally dominated future.

EV-Related Tax Incentives Stimulating Trade-ins

First-registration tax concessions valid to March 2026 accelerate trade-ups as early adopters chase newer battery technology. Used BEV listings grow at 14.03% CAGR, supported by the government target of 100% electric new-car sales by 2030. Conventional cars trade at steeper discounts, enabling budget buyers to enter the Hong Kong used car market, while lightly-used EVs command premium pricing due to supply scarcity and incentive spill-overs.

Cross-Border Inventory Flows Within Greater Bay Area

Tariff-free movement of vehicles between Hong Kong and Guangdong fosters arbitrage on luxury models and diversifies stock pools. Dealers exploit price differentials and currency spreads, although regulatory alignment on southbound driving quotas remains unfinished[1]. Long-run harmonization promises deeper inventory and leaner logistics costs, further globalizing the Hong Kong used car market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Trust and Transparency Concerns | -1.8% | Kowloon, New Territories | Short term (≤ 2 years) |

| Scarce Parking and High Ownership Costs | -1.4% | Hong Kong Island, Central, Tsim Sha Tsui | Long term (≥ 4 years) |

| EV Residual-Value Uncertainty | -0.9% | New Territories, Tseung Kwan O | Medium term (2-4 years) |

| Stricter Inspection and Compliance Cost | -0.7% | All regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Trust and Transparency Concerns

Limited vehicle-history databases and inconsistent inspection standards fuel buyer skepticism. Although certified programs and return policies emerge, reputation-building requires time. Multi-owner cars dominate at 66.03%, but each additional handoff complicates valuation and negotiation. Strengthened consumer-protection statutes are still evolving, restraining shorter-term momentum in the Hong Kong used car market.

Scarce Parking and High Ownership Costs

Peak-hour tunnel tolls hit HKD 60 and core-district parking exceeds HKD 3,000 per month, inflating total cost of ownership. High fixed outlays dissuade marginal buyers, concentrating demand among households with secured parking or employer subsidies. While the Hong Kong used car market gains from affluent patrons, overall penetration stalls under these structural headwinds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Sedans Lead Despite SUV Momentum

Sedans retained a 35.02% slice of the Hong Kong used car market in 2025, thanks to intuitive maneuverability in dense urban grids. Compact footprints support ease of parking, sustaining demand among commuter households. Sport-utility vehicles, however, are pacing ahead at 7.05% CAGR through 2031 as families seek taller seating, advanced safety suites, and upmarket styling. Hybrid mini-SUVs and emerging electric seven-seaters broaden appeal beyond luxury buyers. Hatchbacks stay relevant for novice drivers valuing low running costs. MPVs satisfy niche multi-generational travel, while convertibles and coupes populate prestige lanes at premium price points.

Modern SUVs integrate fold-flat seating, panoramic roofs, and Level 2 driver assists, narrowing the practicality gap with sedans. Expanded lane-keeping and park-assist systems lower accident risk, enhancing insurer appetite and buyer confidence. Dealers leverage augmented-reality showrooms to demonstrate cabin flexibility, nudging upgrades. Sedans nonetheless retain executive-fleet loyalty, aiding steady turnover in corporate off-lease channels. The dual-play of practicality and incentive-loaded EV SUVs ensures both body styles coexist and power total volume growth in the Hong Kong used car market.

By Vendor Type: Organized Channels Gain Market Share

Organized vendors controlled 57.05% of the Hong Kong used car market size in 2025, charting 6.55% annual growth. Branded showrooms deploy standardized 160-point inspections and offer one-year power-train coverage, fortifying trust. Transparent, algorithm-driven pricing shields buyers from negotiation fatigue, drawing digitally savvy millennials. Scale advantages deliver wider vehicle selection and integrated financing, reinforcing repeat patronage. Unorganized players lose ground as compliance costs rise and reputation metrics amplify competitive gaps.

Franchise alliances with OEMs inject certified-pre-owned badges that promise factory-grade refurbishment. Cross-selling of maintenance plans and insurance elevates margins, funding further network expansion. Social-media marketing funnels high-intent leads directly into booking engines, trimming acquisition costs. Although corner-lot dealers persist in value segments, rising consumer expectations tilt share toward structured players, cementing organized dominance in the Hong Kong used car market.

By Fuel Type: Petrol Dominance Faces Electric Disruption

Petrol vehicles still held 62.58% share of the Hong Kong used car market size in 2025, yet BEVs are outrunning at a 13.25% CAGR. Diesel demand slips amid clean-air directives and urban low-emission zones. Hybrids bridge the tech confidence gap for hesitant adopters, though their relative tax-benefit erosion tempers acceleration.

Battery replacement warranties and falling kilowatt-hour costs cushion resale-value fears, nudging cautious shoppers over the line. Petrol models remain favoured by long-distance chauffeurs due to broader refuelling infrastructure, sustaining baseline throughput. Nevertheless, electric disruption will continue siphoning share as battery swap stations edge into the New Territories, steering fuel mix transformation within the Hong Kong used car market.

By Vehicle Age: Premium on Newer Models

Cars aged 3-5 years attracted 38.74% of Hong Kong used car market share in 2025, offering factory warranty overlap alongside steep initial depreciation savings. Meanwhile, the 0-2 years cohort is accelerating at 9.85% CAGR as affluent drivers upgrade to fresh EV platforms and over-the-air software feature packs. Dealers lease back nearly-new units, enhancing affordability while maintaining inventory churn.

Six-to-eight-year cars garner attention from price-sensitive households but must clear stringent annual inspections. Units older than 12 years wrestle with parts scarcity and higher failure rates, prompting many owners to export or scrap instead of reselling locally. The up-trend toward newer vintages elevates average transaction value and compresses warranty claim exposure, ultimately boosting profitability across the Hong Kong used car market.

By Price Segment: Premium Vehicles Drive Growth

Cars priced above USD 30,000 delivered 28.55% of the Hong Kong used car market size in 2025 and outpaced all brackets at 9.42% CAGR. The affluent landscape, dominated by finance and professional-services executives, underpins the appetite for near-luxury badges. Buyers capture high-spec trims at 30-40% discounts to new-car MSRP, while dealers enjoy healthier gross margins.

The USD 20,000-29,999 range remains the mainstream battleground, blending residual warranty with family-friendly features. Sub-USD 5,000 units appeal primarily to commercial couriers or entry-level learners willing to shoulder maintenance uncertainties. Elevated ownership expenses encourage rationalization toward higher-quality stock, channeling dollars into vehicles that justify parking and toll outlays, thus shaping price-led stratification inside the Hong Kong used car market.

By Sales Channel: Digital Transformation Accelerates

Offline dealerships still hold 49.88% of the Hong Kong used car market in 2025, yet online transactions are rising at a 10.10% CAGR as mobile-first consumers pursue frictionless experiences. Virtual walkarounds, 360-degree imaging, and doorstep test drives defuse distrust, while embedded fintech approvals collapse loan processing from days to minutes.

Hybrid models merge tactile reassurance of physical lots with digital discovery, offering click-to-collect services. Auction platforms capture wholesale liquidity, helping dealers trim aging inventory. OEM-backed e-stores surface certified stock, tightening brand-loyalty loops. End-to-end digitization cements scale for the Hong Kong used car market, particularly as young buyers treat smartphones as the default showroom.

By Ownership: Multi-Owner Vehicles Dominate

Two-plus-owner cars represented 65.72% of the Hong Kong used car market in 2025, attesting to long-life-cycle utilization. Competitive insurance packages and improved build quality have stretched functional life, legitimizing higher hand transfer volumes. While perceived risk rises with each change, inspection tech and transparent service logs mitigate concerns.

First-owner resales, expanding at 9.25% CAGR, capture premium positioning by advertising known history and lower wear. Corporations cycling fleets every three years feed this supply, enabling predictable maintenance patterns for secondary buyers. Ownership history emerges as a decisive filter within digital listings, elevating confidence and shortening decision windows in the Hong Kong used car market.

Geography Analysis

Central districts on Hong Kong Island concentrate premium demand. Finance professionals earning high disposable incomes gravitate toward luxury sedans and compact electric SUVs despite HKD 60 peak tunnel charges. Parking scarcity compels investment in smaller footprints or private bays bundled with upmarket residences, sustaining elevated average deal sizes for the Hong Kong used car market.

Kowloon serves a mixed demographic, with families prioritizing practicality and affordability. Organized dealerships cluster in Mong Kok and Tsim Sha Tsui, leveraging dense footfall and MTR connectivity. The area’s role as a logistics node eases cross-border transfers, supporting inventory diversity. Digitally adept millennials embrace e-commerce, reinforcing a 6.55% organized-vendor CAGR. Trust-building initiatives, including video inspections and seven-day return windows, resonate strongly, further integrating Kowloon into the Hong Kong used car market.

The new territories register the highest growth arc, spurred by expanding satellite towns and easier on-street parking. Proximity to Shenzhen Bay and Lok Ma Chau encourages bilateral trade, enriching stock, especially of right-hand-drive EVs. Government charging grants for housing estates reduce range anxiety and lift BEV turnover. Family-centric buyers opt for SUVs and MPVs for weekend outings, strengthening the region’s influence on volume growth within the Hong Kong used car market.

The used car market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Africa. This is complemented by country-specific insights for Myanmar, Sri Lanka, Kenya, New Zealand, Norway, Switzerland, Belgium, and Nigeria, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Market concentration remains moderate, with DCH Motors, Zung Fu, and VINS Motors collectively holding a subtle market share. Digital disruptors scale swiftly by blending AI diagnostics, seamless financing, and post-sale guarantees, pressuring traditional dealer economics. Strategic acquisitions, such as a leading platform integrating a local classified portal in 2024, signal accelerating consolidation.

Top dealers hedge residual-value risk by offering battery-health certificates on used EVs, enhancing pricing power. Cross-border sourcing teams exploit arbitrage in Guangdong, importing late-model luxury SUVs to satisfy domestic margin targets. Franchise dealers leverage parent-brand tooling to refurbish and remarket trade-ins under certified umbrellas, lifting trust metrics among risk-averse customers.

Smaller independents carve niches in kei cars, collector classics, or budget vans, where personalized service trumps scale. Technology adoption gaps widen cost curves; AI-enabled dynamic pricing confers an edge to larger platforms. Over the medium term, partnership ventures with ride-hailing companies and subscription fleets promise fresh downstream demand, sustaining momentum in the Hong Kong used car market.

Hong Kong Used Car Industry Leaders

VIN’S MOTORS COMPANY LTD

Kam Lung Motor Group

Zung Fu Limited

Hong Kong Motor City

DCH Motors Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Singapore-based marketplace Carro introduced its 160-point AI-driven “Carro Certified” program in Hong Kong, including a five-day return option and 12-month gearbox and engine warranty.

- March 2024: Carro acquired Beyond Cars, bolstering its regional scale and reflecting accelerating consolidation among digital automotive retailers.

Hong Kong Used Car Market Report Scope

A used car, a pre-owned vehicle, or a secondhand car is a vehicle that has previously had one or more retail owners. A certified pre-owned (CPO) vehicle, on the other hand, is a pre-owned vehicle that has been extensively inspected (pre-purchase inspection) and expertly reconditioned.

Hong Kong's used car market is segmented into vehicle type, vendor type, and fuel type. Based on the vehicle type, the market is segmented into hatchbacks, sedans, sports utility vehicles, and multi-purpose vehicles. Based on the vendor type, the market is segmented into organized and unorganized. Based on the fuel type, the market is segmented into gasoline, diesel, electric, and alternative fuel vehicles.

For each segment, the market sizing and forecast have been done based on the value (USD).

| Hatchbacks |

| Sedans |

| Sport-Utility Vehicles (SUVs) |

| Multi-Purpose Vehicles (MPVs) |

| Others (convertibles, coupes, crossovers, sports cars) |

| Organised |

| Unorganised |

| Petrol |

| Diesel |

| Hybrid (HEV and PHEV) |

| Battery-Electric (BEV) |

| LPG / CNG / Others |

| 0 to 2 Years |

| 3 to 5 Years |

| 6 to 8 Years |

| 9 to 12 Years |

| Above 12 Years |

| Below USD 5,000 |

| USD 5,000 to USD 9,999 |

| USD 10,000 to USD 14,999 |

| USD 15,000 to USD 19,999 |

| USD 20,000 to USD 29,999 |

| USD 30,000 and Above |

| Online | Digital Classified Portals |

| Pure-play e-Retailers | |

| OEM-Certified Online Stores | |

| Offline | OEM-Franchised Dealers |

| Multi-brand Independent Dealers | |

| Physical Auction Houses |

| First-owner Resale |

| Multi-owner |

| By Vehicle Type | Hatchbacks | |

| Sedans | ||

| Sport-Utility Vehicles (SUVs) | ||

| Multi-Purpose Vehicles (MPVs) | ||

| Others (convertibles, coupes, crossovers, sports cars) | ||

| By Vendor Type | Organised | |

| Unorganised | ||

| By Fuel Type | Petrol | |

| Diesel | ||

| Hybrid (HEV and PHEV) | ||

| Battery-Electric (BEV) | ||

| LPG / CNG / Others | ||

| By Vehicle Age | 0 to 2 Years | |

| 3 to 5 Years | ||

| 6 to 8 Years | ||

| 9 to 12 Years | ||

| Above 12 Years | ||

| By Price Segment | Below USD 5,000 | |

| USD 5,000 to USD 9,999 | ||

| USD 10,000 to USD 14,999 | ||

| USD 15,000 to USD 19,999 | ||

| USD 20,000 to USD 29,999 | ||

| USD 30,000 and Above | ||

| By Sales Channel | Online | Digital Classified Portals |

| Pure-play e-Retailers | ||

| OEM-Certified Online Stores | ||

| Offline | OEM-Franchised Dealers | |

| Multi-brand Independent Dealers | ||

| Physical Auction Houses | ||

| By Ownership | First-owner Resale | |

| Multi-owner | ||

Key Questions Answered in the Report

What is the current size of the Hong Kong used car market?

The market is valued at USD 1.97 billion in 2026 and is projected to reach USD 2.94 billion by 2031.

Which vehicle type leads sales in the Hong Kong used car market?

Sedans led with 35.02% share, while SUVs are the fastest growing at a 7.05% CAGR.

How quickly are online sales channels growing?

Online transactions are expanding at a 10.10% CAGR, reflecting rapid digital adoption.

What impact do EV incentives have on the Hong Kong used car market?

Tax concessions valid until 2026 spur trade-ins and push battery-electric vehicle listings to a 13.25% CAGR.

Which vendor segment is gaining ground?

Organized dealers hold 57.05% share and are growing at 6.55% annually, aided by warranties and transparent pricing.

Page last updated on: