Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Home Security System Market is Segmented by Component (Hardware, Software, and More), Connectivity (Wired and More), Type of System (Video Surveillance System, and More), Distribution Channel (Online Direct-To-Consumer, E-Commerce and Marketplaces and More), Home Type (Single-Family Homes, Multi-Family Units and Apartments and More) and Geography

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

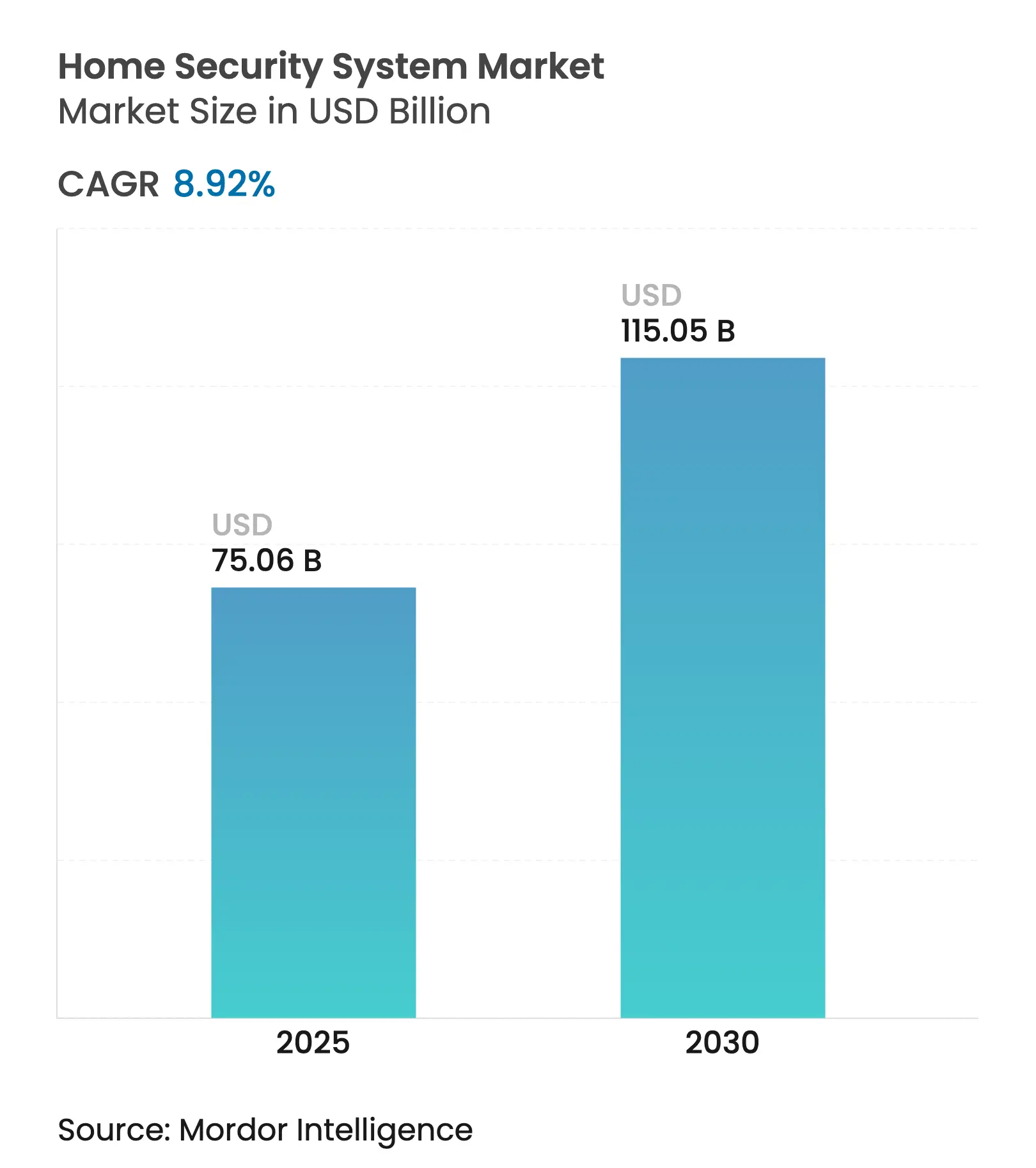

| Market Size (2025) | USD 75.06 Billion |

| Market Size (2030) | USD 115.05 Billion |

| Growth Rate (2025 - 2030) | 8.92 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Robust expansion is shaped by rapid IoT adoption, insurer incentives, and rising DIY installation that lower upfront costs while supporting profitable subscriptions. Hardware innovation, edge-AI processing, and open standards such as Matter now enable seamless device orchestration inside connected dwellings. Online direct-to-consumer sales and wireless connectivity accelerate penetration by giving consumers flexible purchase and installation choices. At the same time, insurers collaborate with security vendors to craft risk-based pricing that rewards connected homes, further reinforcing demand.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

IoT & wireless-enabled smart-home adoption IoT & wireless-enabled smart-home adoption | +2.1% | Global, with concentration in North America & Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast :+2.1% | Geographic Relevance :Global, with concentration in North America & Europe | Impact Timeline :Medium term (2-4 years) |

Rising penetration of DIY/contract-free systems Rising penetration of DIY/contract-free systems | +1.8% | North America & Europe, expanding to APAC | Short term (≤ 2 years) | |||

Declining device costs and subscription bundling Declining device costs and subscription bundling | +1.4% | Global | Short term (≤ 2 years) | |||

Insurance-premium discounts for connected homes Insurance-premium discounts for connected homes | +1.2% | North America & Europe | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

IoT & Wireless-Enabled Smart-Home Adoption

Interoperability advances led by the Matter protocol let cameras, locks, and sensors communicate fluidly across brands, converting isolated devices into predictive safety networks. Edge AI chipsets from Qualcomm allow on-device video analytics that reduce latency and preserve privacy. [1]Qualcomm Technologies, “Edge AI for Smart Security Devices,” qualcomm.com State Farm’s partnership with ADT exemplifies insurer alignment, using device data to refine risk models and offer policy discounts. As each incremental sensor boosts network efficacy, households perceive higher value, raising retention and subscription upgrades.

Rising Penetration of DIY/Contract-Free Systems

Self-install kits costing USD 200–2,000 undercut professional packages once priced at USD 2,500–5,000, shrinking acquisition friction and opening the home security system market to price-sensitive buyers. Brands such as SimpliSafe and Ring achieved user satisfaction above 90%, proving that smartphone-guided setup can rival pro standards. Shorter onboarding times let vendors scale quickly while capturing lifetime subscription value.

Declining Device Costs and Subscription Bundlin

Semiconductor scale economics cut hardware prices 15%–20% annually. Smart locks now install for USD 93–221 each, making advanced access control mainstream. Providers offset slimmer hardware margins with premium cloud video tiers and AI features that lift average revenue per user, while bundling raises switching costs, lowering churn.

Insurance-Premium Discounts for Connected Homes

Nationwide offers 4% policy savings to smart-home participants, and State Farm subsidizes ADT equipment, illustrating how insurers monetize real-time risk data. Homes with monitored security post 60% fewer successful burglaries, validating the economics of discount programs

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Cyber-attack and data-privacy vulnerabilities Cyber-attack and data-privacy vulnerabilities | -1.6% | Global; heightened concern in Europe under GDPR | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast :-1.6% | Geographic Relevance :Global; heightened concern in Europe under GDPR | Impact Timeline :Short term (≤ 2 years) |

High initial purchase & professional installation cost High initial purchase & professional installation cost | -1.1% | Global; greater impact in emerging markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Cyber-Attack and Data-Privacy Vulnerabilities

The European Cyber Resilience Act obliges manufacturers to publish software bills of materials and remediate vulnerabilities across a product’s lifespan, raising compliance costs and security. Research in Frontiers in Computer Science shows spoofing and DDoS attempts escalating with the USD 4 trillion IoT economy. India’s 2025 CCTV certification rule likewise elevates entry barriers. [2]Business Today Bureau, “India’s Mandatory CCTV Certification from April 2025,” businesstoday.in Sustained breaches could spark consumer pullback, tempering growth.

High Initial Purchase & Professional Installation Cost

Fully featured systems still demand USD 700–2,500 for equipment plus labor, limiting adoption among lower-income households. Financing plans ease sticker shock, yet multi-family property managers balance capital budgets against rent yield, occasionally postponing upgrades.

By Component: Services Drive Revenue Transformation

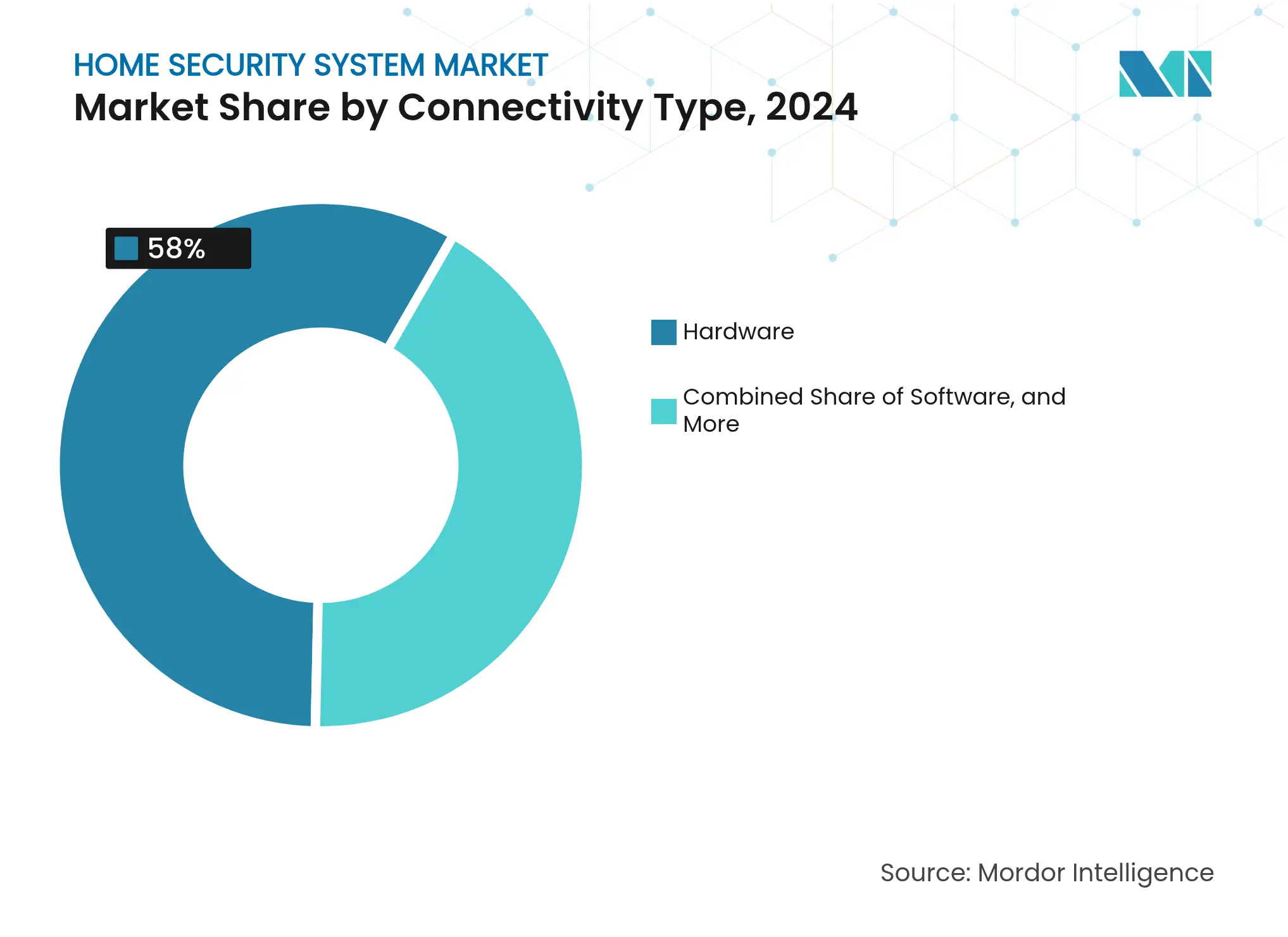

Services are projected to outpace hardware with a 10.20% CAGR as customers favor managed monitoring, cloud video storage, and AI analytics delivered under monthly plans. Professional monitoring layers predictive maintenance and smart-home orchestration, reinforcing loyalty. Hardware remains crucial at 58% of 2024 turnover, yet commoditization shifts differentiation to software platforms that bind devices into cohesive ecosystems. Installation and integration services gain sophistication as mixed wireless protocols demand expert configuration.

Service-centric economics foster longer customer relationships and predictable cash flows. Providers use tiered subscriptions to fund R&D that continually enrich feature sets, sustaining a virtuous cycle. In parallel, hardware design focuses on low-power chips and modular form factors that streamline self-installation, expanding the addressable base of the home security system market.

Note: Segment shares of all individual segments available upon report purchase

By Connectivity: Wireless Dominance Accelerates

Wireless options held 72% revenue in 2024 while rising at 12.98% CAGR, underscoring consumer appetite for cable-free retrofits. Wi-Fi 6 and 5G reduce latency and support high-resolution video, while battery advances stretch maintenance intervals. Hybrid wired-wireless bundles remain relevant for new builds demanding redundancy. Matter certification eliminates vendor lock-in and simplifies device enrollment.[3]MDPI Electronics, “Wireless Standards and Matter Integration,” mdpi.com

Ultra-wideband adds fine-grained location awareness, evident in Schlage’s 2025 smart lock lineup.

The scaling wireless footprint benefits telecom carriers by bundling broadband with security, pulling new entrants into the home security system market. Competition thus pivots toward service quality, AI capabilities, and integration breadth rather than mere connectivity type.

By Type of System: AI Transforms Video Surveillance

Video surveillance controlled 46% of 2024 sales and is expanding at 11.05% CAGR as edge AI converts footage into actionable insights. Alarm and intrusion panels integrate voice assistants and geofencing to arm automatically, while connected fire sensors deliver early smoke and CO warnings. Biometric access control shifts credential management from keys to fingerprints and mobile IDs, improving convenience.

Generative AI lets users query archives in natural language, as Ring’s 2024 software upgrade illustrates. These capabilities transform stored video from passive liability into valuable data, encouraging higher cloud storage tiers and boosting average revenue per user. The momentum cements video analytics as a linchpin of the broader home security system market.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Distribution Channel: Digital Transformation Accelerate

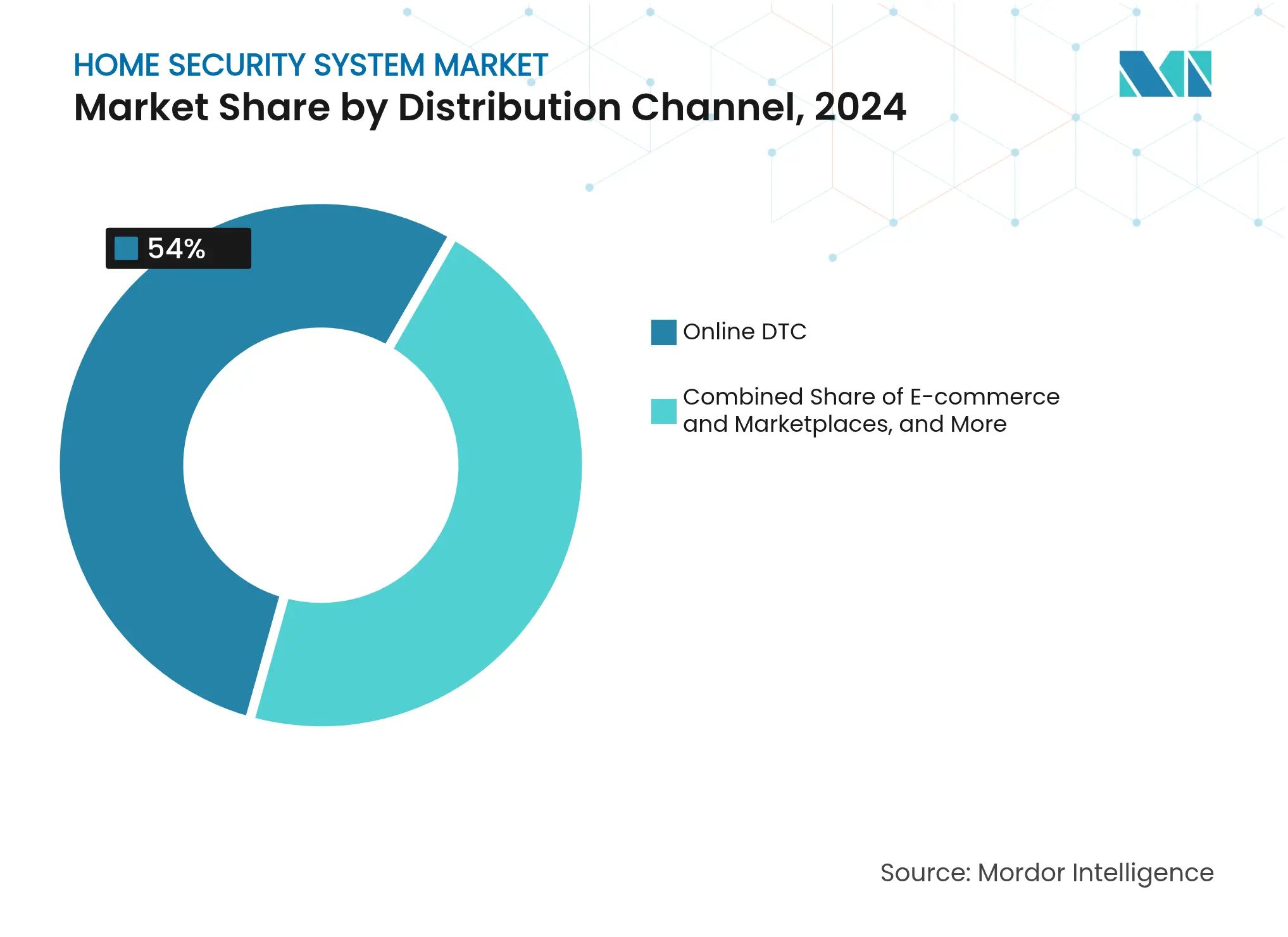

E-commerce and manufacturer web stores owned 54% of 2024 shipments and are climbing at 13.50% CAGR, propelled by transparent pricing, doorstep delivery, and extensive peer reviews. Brick-and-mortar retailers cater to shoppers wanting tactile demos or immediate pickup, yet their share declines as consumers grow comfortable ordering complex kits online. Installer networks focus on large estates and mixed-use developments where system design complexity merits professional involvement.

Direct sales empower brands to collect usage telemetry, guiding product iteration and upsell campaigns. Subscription onboarding becomes frictionless when hardware ships pre-provisioned to user accounts, illustrating why online channels will remain pivotal to the home security system market.

Note: Segment shares of all individual segments available upon report purchase

By Home Type: Multi-Family Growth Opportunities

Single-family dwellings represented 61% of ships in 2024, benefiting from owner autonomy to invest in safety upgrades. Multi-family buildings, however, register a stronger 9.30% CAGR to 2030 as property managers deploy centralized video walls and smart locks to attract tenants and trim insurance premiums. Vacation rentals adopt transient-guest-aware solutions that balance protection with privacy, riding growth in the short-term lodging sector.

For multi-family sites, cloud platforms deliver per-unit credential provisioning and common-area analytics, reducing on-site staff workload. Vendors that tailor dashboards to property management workflows are poised to gain share in this segment of the home security system market.

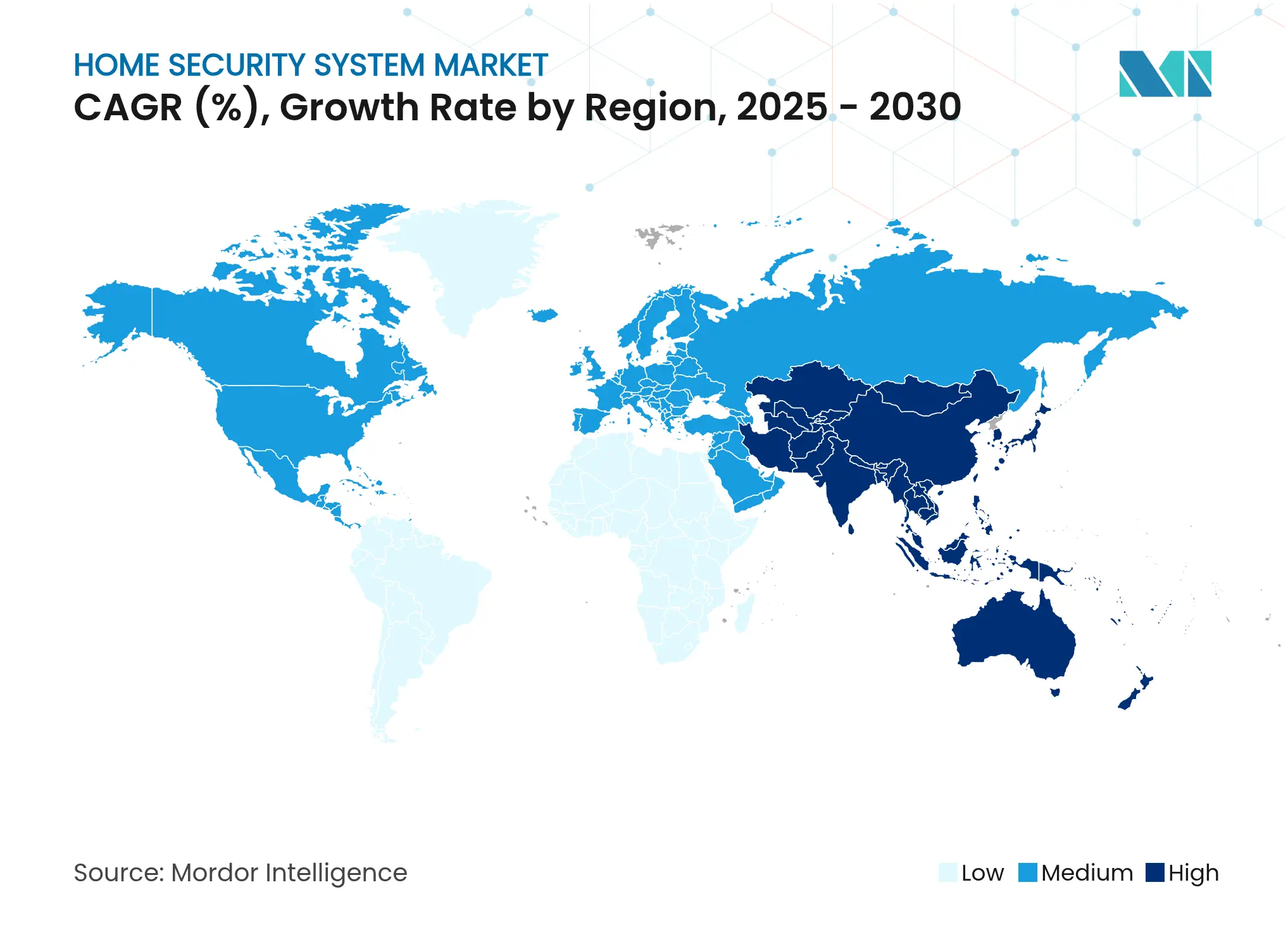

Asia Pacific led the home security system market with 39% revenue in 2024 and exhibits the fastest 8.98% CAGR to 2030. Government smart-city mandates in China, India, and Singapore integrate cameras, alarms, and traffic sensors into unified municipal dashboards, stimulating residential adoption through ecosystem familiarity. China benefits from vertical supply-chain control, though export restrictions spur alternative sourcing in India, which doubled local production capacity following its 2025 CCTV certification ruling. Japan and South Korea spearhead premium AI-enabled systems, leveraging domestic giants Samsung and LG to bundle robotics and security.

North America maintains high penetration, supported by 55 million professionally monitored installations in 2024. Insurer partnerships, robust broadband, and early smart-home culture underpin steady upgrades toward service-heavy models. Canada mirrors U.S. trends on a smaller scale, while Mexico’s urban centers adopt wireless kits to circumvent wiring constraints in aging housing stock.

Europe grows steadily amid stringent privacy laws. Revenues reached EUR 29.7 billion in 2021 and are projected to more than double by 2026. GDPR and the Cyber Resilience Act raise compliance thresholds, favoring vendors with certified secure development life cycles. Germany, the United Kingdom, and France drive high-tier demand; Eastern Europe offers catch-up potential as EU structural funds modernize housing infrastructure.

Market Concentration

The home security system market remains moderately fragmented. ADT and Vivint leverage installed bases and 24/7 monitoring centers, while Amazon Ring, Google Nest, and Apple HomePod align with broader smart-home ecosystems. Price-aggressive entrants from Asia offer hardware “good enough” for DIY buyers, forcing incumbents to differentiate via AI software, warranty extensions, and insurer tie-ins.

M&A continues: GardaWorld acquired Stealth Monitoring in November 2024, amassing 100,000 active cameras to build a global AI-enabled surveillance footprint. ASSA ABLOY bought InVue for USD 165 million in January 2025 to enhance connected asset protection. Amazon secured a patent for customizable intrusion zones, ensuring future UX refinements. Competitive advantage tilts to players integrating devices, cloud, and analytics with transparent privacy controls across jurisdictions.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

A home security system is a group of physical and electronic components that all work together to protect a home. The scope of the study has been segmented based on the components - hardware, software, and services. Hardware has been further segmented into electronic locks, security cameras, fire sprinklers, window sensors, door sensors, and other hardware products. These components are used in various systems, such as video surveillance, alarm, access control, and fire protection systems.

The Home Security System Market is segmented by Component (Hardware (Electronic Locks, Security Cameras, Fire Sprinklers, Window Sensors, Door Sensors), Software, Services), Type of System (Video Surveillance System, Alarm System, Access Control System, Fire Protection System), Distribution Channel (Online, Offline) and Geography. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.