Home Care Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 202.34 Billion |

| Market Size (2031) | USD 262.45 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

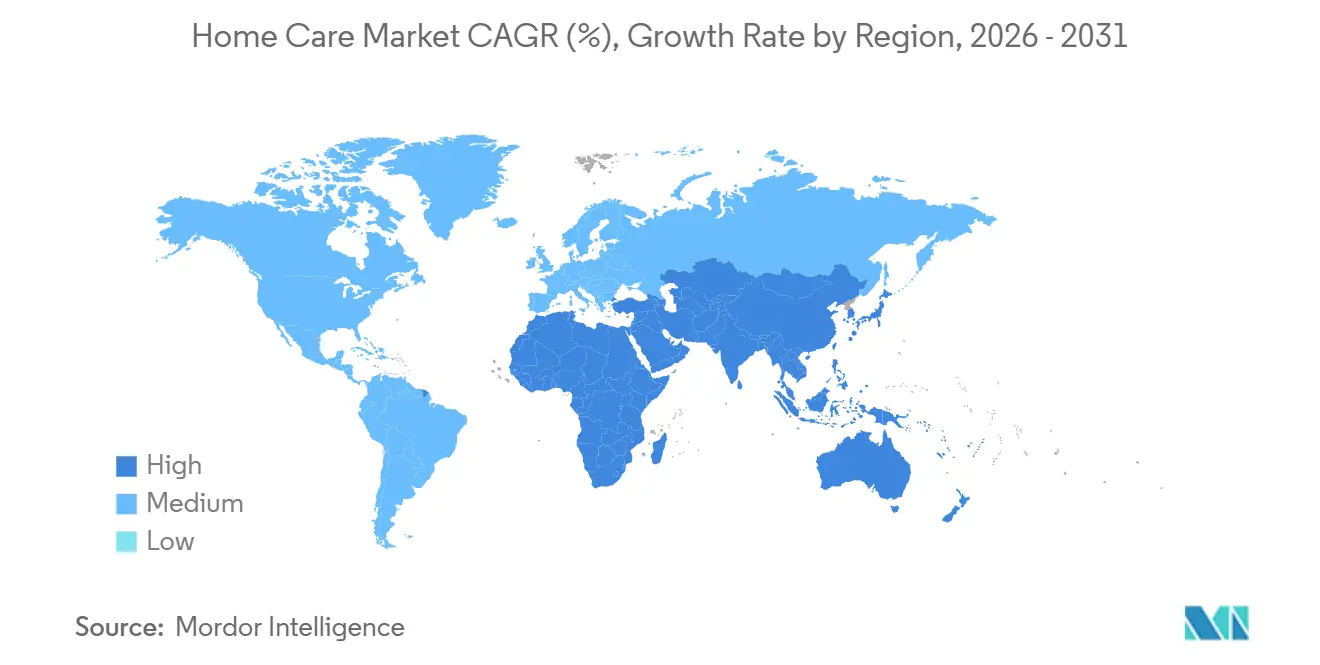

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

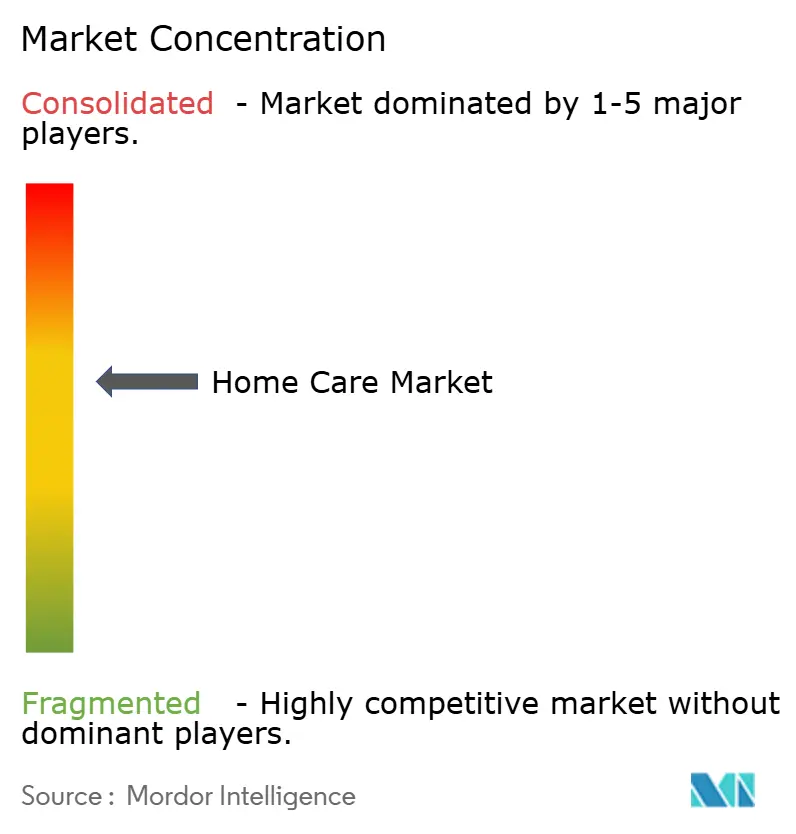

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Home Care Market Analysis by Mordor Intelligence

The home care market size is estimated at USD 202.34 billion in 2026, and is expected to reach USD 262.45 billion by 2031, at a CAGR of 5.34% during the forecast period (2026-2031). This trajectory reflects a structural shift from volume-led commodity sales toward premiumization anchored in wellness positioning, fragrance innovation, and digitally amplified brand narratives. Social media platforms generated 79 billion views under the #CleanTok hashtag by mid-2025, translating follower engagement into measurable revenue lifts. Unilever reported a 38% sales increase for Cif after partnering with micro-influencers, while Vileda's collaboration with cleaning content creators drove a 306% spike in mop sales. These dynamics underscore how household care incumbents now compete on cultural relevance as much as formulation efficacy. Regionally, Asia-Pacific leads absolute growth as China’s urbanization topped 67% in 2025 and India’s middle class added 50 million households yearly, expanding the addressable base for branded cleaners.

Key Report Takeaways

- By product type, laundry care captured 54.03% revenue in 2025, while air care is forecast to expand at a 6.76% CAGR through 2031.

- By packaging format, bottles retained a 43.88% share in 2025, but pouches are set to grow 6.88% annually on the strength of refill systems.

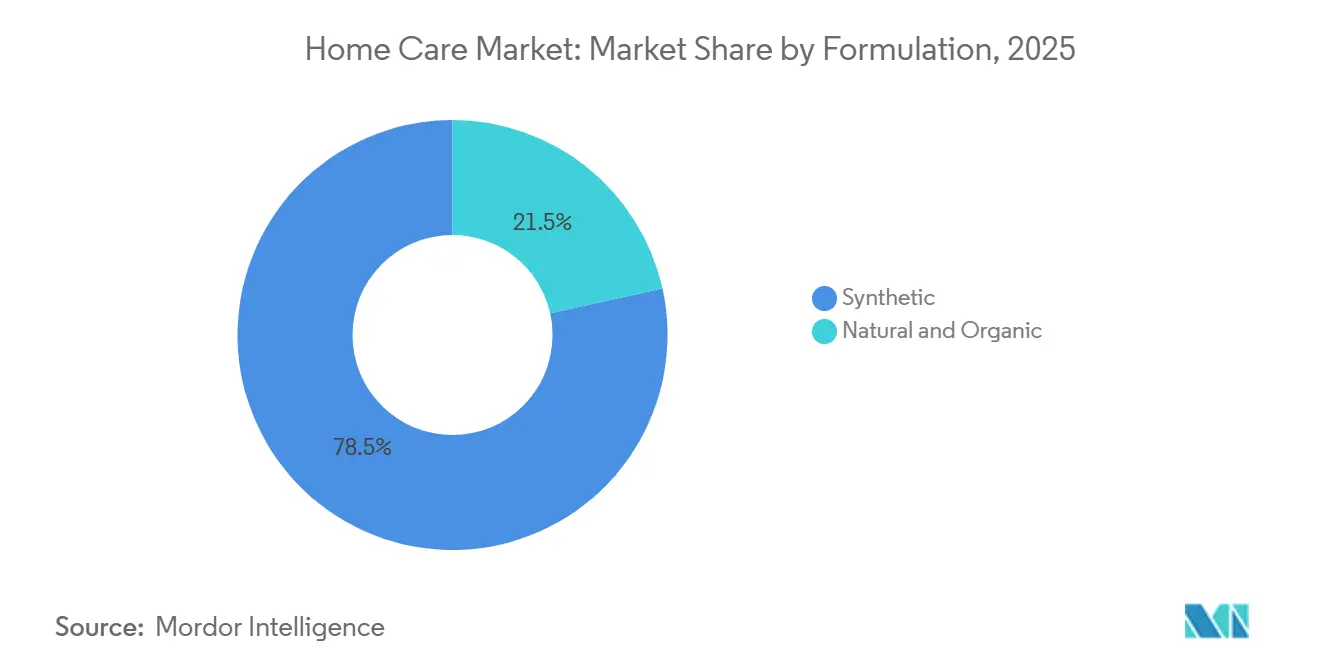

- By formulation, synthetic products held 78.47% of the household care products market share in 2025; natural and organic variants will rise at a 7.03% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets commanded 48.21% revenue in 2025, whereas online retail stores are projected to post a 6.04% CAGR through 2031.

- By geography, Asia-Pacific generated 28.95% of global sales in 2025 and is poised for a 6.33% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Home Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Influence of Social Media Platforms and Celebrity Endorsements | +0.8% | Global, with stronger impact in North America and Europe | Medium term (2-4 years) |

| Product Innovation in terms of Ingredients, Fragrance and Packaging Format | +1.2% | Global, led by developed markets | Long term (≥ 4 years) |

| Home Aesthetics and Wellness Trends | +0.6% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Sustainability Initiatives | +1.1% | Europe and North America leading, global adoption | Long term (≥ 4 years) |

| Consumer Preference for Natural and Eco-Friendly Products | +0.9% | Global, with premium segments in developed markets | Long term (≥ 4 years) |

| Increasing Awareness of Vector-Borne Diseases | +0.4% | Global, with higher impact in tropical regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Influence of Social Media Platforms and Celebrity Endorsements

Digital platforms transformed household care from a low-engagement category into a content-driven battleground where cleaning routines become viral entertainment. TikTok's #CleanTok hashtag accumulated 79 billion views by mid-2025, with creators demonstrating product efficacy in 15-second clips that bypass traditional advertising skepticism. Procter & Gamble's 2025 campaign for Mr. Clean leveraged Instagram Reels to showcase before-and-after transformations, achieving a 4.2% engagement rate triple the consumer packaged goods industry average. This channel rewards brands that master algorithmic distribution and authentic storytelling over polished production values. The shift also democratizes market entry for challenger brands that lack retail distribution but possess social media fluency, intensifying competition for shelf-stable incumbents. In Asia, where mobile device usage is high, these tactics show significant success. Western markets are seeing similar trends, with creators blending cleaning tips and entertainment. In 2024, Asia-Pacific averaged ~15 GB of mobile broadband traffic per subscription per month, the highest among all regions [1]Source: International Telecommunication Union, "Measuring Digital Development 2024", itu.int. This high data usage supports heavy social media engagement via videos and short-form content.

Product Innovation in Terms of Ingredients, Fragrance and Packaging Format

Formulation breakthroughs are redefining value propositions beyond cleaning efficacy to encompass sensory experience, environmental footprint, and convenience. Givaudan introduced PlanetCaps™ biodegradable fragrance microcapsules in 2025, replacing petroleum-based polymers with plant-derived alternatives that degrade within 28 days under composting conditions. Henkel opened a EUR 50 million (USD 54 million) fragrance innovation center in Düsseldorf in 2024, focusing on AI-driven scent profiling that matches consumer mood states to fragrance molecules. Novozymes launched a protease enzyme in 2025 that removes protein-based stains at 20°C, enabling cold-water laundry cycles that cut energy consumption by 60% per load. Packaging innovation accelerated with Procter & Gamble's 2025 rollout of Tide refill pouches containing 60% less plastic than equivalent bottles, while Unilever committed to 100% reusable, recyclable, or compostable packaging by 2025. Companies that integrate enzyme efficacy, sensory delight, and circular packaging will command premium pricing, while laggards face margin compression from private-label substitutes.

Home Aesthetics and Wellness Trends

Consumers increasingly frame household care as an extension of personal wellness and interior design, elevating cleaning from a chore to a ritual that signals self-care and status. This mindset shift correlates with the global wellness economy reaching significant revenue in 2024, with home environment optimization emerging as a distinct sub-segment. Air care products capitalized on this trend, with smart diffusers integrating IoT connectivity. Brands like Pura and Aera launched app-controlled devices in 2025 that schedule fragrance intensity based on circadian rhythms and air quality sensors. Essential oil-based formulations gained traction, with lavender and eucalyptus variants positioned as stress-reduction tools rather than mere odor neutralizers. This wellness framing justifies price premiums; products marketed with aromatherapy claims commanded 30-40% higher per-unit prices than conventional variants in 2025. The trend also drives cross-category bundling, with brands offering curated cleaning kits that mirror skincare routines in packaging aesthetics and ritual language.

Increasing Awareness of Vector-Borne Diseases

Persistent vector-borne disease burdens sustain structural demand for insect repellent formulations, particularly in tropical and subtropical geographies. The World Health Organization reported 249 million malaria cases and 608,000 deaths in 2024, with sub-Saharan Africa accounting for 95% of fatalities, while dengue incidence reached 96 million symptomatic cases globally, with 40,000 deaths. The U.S. Environmental Protection Agency registered 4 primary active ingredients for insect repellents: DEET, picaridin, IR3535, and oil of lemon eucalyptus (PMD), each offering distinct efficacy and safety profiles. Climate change amplifies risk zones. The CDC projected that warming temperatures would expand mosquito habitats into previously temperate regions, increasing U.S. populations at risk for dengue by 30% by 2030. This geographic expansion creates growth opportunities beyond traditional tropical markets, particularly for products combining repellent efficacy with skin-care benefits such as moisturization and UV protection.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Counterfeit Products | -0.7% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Health Concerns over Chemical Ingredients | -0.5% | Developed markets primarily, expanding globally | Long term (≥ 4 years) |

| High Cost of Eco-Friendly Products | -0.4% | Global, with stronger impact in price-sensitive markets | Medium term (2-4 years) |

| Stringent Regulatory Compliance For the Manufacturers | -0.3% | Europe and North America leading, global expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Counterfeit Products

Counterfeit household care products erode brand equity and consumer trust while posing safety risks through substandard formulations. The OECD estimated global counterfeit trade at USD 464 billion in 2024, with household care items frequently targeted due to high turnover rates and low detection risk. Online marketplaces amplified the problem. A 2025 investigation by the International Trademark Association found that 42% of household cleaning products purchased from third-party sellers on major e-commerce platforms failed authenticity verification. Counterfeit detergents often contain inadequate surfactant concentrations or substitute cheaper solvents that damage fabrics, while fake disinfectants may lack active antimicrobial agents, undermining hygiene efficacy. Enforcement challenges are significant in emerging markets, but developed markets also face issues due to online platforms with weak verification. In 2023, Amazon destroyed over 7 million counterfeit products globally and strengthened anti-counterfeiting efforts with brands and Chinese law enforcement, leading to 50+ raids and identifying 100+ suspects [2]Source: Amazon, "Brand Protection Report", amazon.com. Counterfeiting reduces market revenues and raises compliance costs, hindering home care market growth.

Health Concerns over Chemical Ingredients

Growing consumer awareness of chemical exposure risks drives reformulation demands and regulatory scrutiny, particularly for volatile organic compounds (VOCs), phthalates, and quaternary ammonium compounds (quats). The U.S. Environmental Protection Agency's Safer Choice program certified over 2,000 household cleaning products by 2025, requiring formulations to exclude ingredients linked to asthma, endocrine disruption, or aquatic toxicity. California's Safer Consumer Products regulation mandated disclosure of 5,000+ chemicals in cleaning formulations starting in 2025, with manufacturers facing penalties up to USD 10,000 per day for non-compliance. Academic research intensified concerns. A 2024 study published in Environmental Health Perspectives found that regular use of spray cleaners increased asthma risk by 30-50% due to aerosolized irritants. Phthalates, commonly used as fragrance carriers, face mounting restrictions. The European Chemicals Agency added 4 phthalate variants to the REACH authorization list in 2024, requiring sunset dates for phase-out. Brands reformulate toward plant-based surfactants and enzyme catalysts, but these alternatives often cost 40-60% more than synthetic equivalents, compressing margins or necessitating price increases that dampen volume growth. The challenge intensifies in emerging markets where regulatory frameworks lag, and price sensitivity limits the adoption of safer but costlier formulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Laundry Care Dominance Meets Air Care Acceleration

Laundry care captured 54.03% of market revenue in 2025, reflecting its status as a high-frequency, non-discretionary category with established brand loyalty and retail distribution. The segment will grow through 2031, driven by detergent pod adoption. Single-dose formats occupy a prominent share of North American laundry detergent sales in 2025, as consumers prioritize convenience and pre-measured dosing that reduces waste. Procter & Gamble's Tide Coldwater formula, launched in 2024, enables effective cleaning at 20°C, cutting energy consumption by 60% per load and aligning with European energy-efficiency mandates. Givaudan's biodegradable PlanetCaps™ fragrance microcapsules, introduced in 2025, address sustainability concerns while extending scent longevity by 40% compared to conventional encapsulation.

Dishwashing products maintained a stable share through enzyme innovation. Novozymes' 2025 lipase enzyme removes grease at lower temperatures, enabling formulations that cut water heating costs by 50%. Surface Care benefited from post-pandemic hygiene consciousness, though growth moderated to baseline levels as disinfectant stockpiling normalized. Toilet Care and Bleach segments face maturity, with innovation focused on eco-friendly oxidizers; oxygen bleach variants using hydrogen peroxide gained market share in Europe during 2025, displacing chlorine-based products restricted under the EU Biocidal Products Regulation. A notable shift in consumer perception has emerged: the air care segment, which is expected to grow at a 6.76% CAGR through 2031, is now closely associated with health, a change driven by concerns over airborne transmission and rising pollution levels. The Environmental Protection Agency reported that in 2024, the United States emitted 41 million tons of Carbon Monoxide (CO)[3]Source: Environmental Protection Agency, "Air pollutant emissions in the United States," epa.gov.

By Packaging Format: Refill Pouches Disrupt Bottle Incumbency

Bottles commanded 43.88% of packaging share in 2025, sustained by established supply chains, consumer familiarity, and compatibility with retail shelf fixtures. However, pouches are expanding at a 6.88% CAGR through 2031, driven by sustainability mandates and material cost advantages. Refill pouches use 60-80% less plastic than rigid bottles for equivalent volumes, reducing both carbon footprint and freight costs. Procter & Gamble's 2025 launch of Tide concentrated refill sachets exemplifies this shift, delivering 32 loads per 150-gram pouch versus 500 grams for a traditional bottle. Regulatory pressure amplifies the trend; the EU's Single-Use Plastics Directive and Extended Producer Responsibility schemes impose fees on non-recyclable packaging, making pouches economically attractive.

Aerosol cans retained niche applications in air care and insect repellent, though growth slowed due to propellant regulations. The EU's F-Gas Regulation phased down hydrofluorocarbons (HFCs) by 79% between 2015 and 2024, forcing reformulation to hydrocarbon or compressed-air propellants. Other Packaging Formats, including aluminum bottles and biodegradable films, captured early-adopter segments willing to pay 20-30% premiums for circular materials. Henkel piloted a closed-loop aluminium bottle for its Persil brand in Germany during 2025, achieving 95% recyclability versus 30% for mixed-material plastic bottles. The packaging landscape is fragmenting. Bottles will remain dominant in price-sensitive markets and categories requiring structural integrity (bleach, toilet cleaners), while pouches will gain share in laundry and dishwashing, where refill models align with consumer sustainability values and retailer space optimization goals.

By Formulation: Synthetic Scale Versus Natural Velocity

Synthetic formulations held 78.47% of the market share in 2025, reflecting cost efficiency, performance consistency, and incumbent manufacturing scale. Petroleum-derived surfactants like linear alkylbenzene sulfonate (LAS) cost USD 1.20-1.50 per kilogram versus USD 2.50-3.50 for plant-based alternatives such as alkyl polyglucosides, creating a structural price advantage that sustains volume leadership. However, Natural and Organic formulations are accelerating at a 7.03% CAGR through 2031, propelled by regulatory restrictions on synthetic chemicals and consumer willingness to pay premiums for plant-based ingredients. The U.S. EPA's Safer Choice program certified 2,000+ products by 2025, requiring exclusion of ingredients linked to asthma, endocrine disruption, or aquatic toxicity.

Enzyme technology bridges the performance gap. Novozymes' 2025 protease enzyme enables cold-water laundry cleaning, cutting energy use by 60% while maintaining stain-removal efficacy comparable to hot-water synthetic detergents. Plant-based surfactants derived from coconut and palm kernel oils gained traction, though sustainability concerns around palm cultivation prompted certification requirements. The Roundtable on Sustainable Palm Oil (RSPO) certified 19% of global palm oil production in 2024, with household care brands prioritizing RSPO-certified inputs to mitigate deforestation risks. The formulation divide will persist: synthetic products will dominate price-sensitive segments and institutional channels requiring bulk procurement, while natural variants will grow in premium retail and e-commerce, where brand storytelling and certification transparency drive purchase decisions.

By Distribution Channel: Digital Disruption Reshapes Retail Dynamics

Supermarkets and hypermarkets accounted for 48.21% of the distribution share in 2025, sustained by one-stop shopping convenience, promotional pricing, and impulse purchase opportunities. However, Online retail stores are expanding at a 6.04% CAGR through 2031, driven by subscription models, direct-to-consumer brands, and pandemic-accelerated digital adoption. Amazon captured a prominent share of U.S. household care sales in 2025, leveraging its Subscribe & Save program that offers 15% discounts for recurring deliveries, locking consumers into long-term purchase patterns. Direct-to-consumer brands like Grove Collaborative and Blueland bypassed traditional retail, offering concentrated refill tablets and reusable packaging systems that reduce shipping costs and environmental impact. Grove reported 1.2 million active subscribers in 2025, with 75% retention rates.

Convenience and grocery stores maintained relevance for top-up purchases and immediate needs, while other distribution channels, including dollar stores, pharmacies, and institutional suppliers, served niche segments. Online channels favor brands with strong digital fluency and supply chain agility, enabling rapid product iteration and targeted marketing. Subscription models generate predictable revenue streams but require sustained customer acquisition spending. Grove Collaborative's customer acquisition cost reached USD 45 in 2025, necessitating 18-month payback periods to achieve profitability. The distribution landscape will bifurcate: supermarkets will retain dominance for bulk purchases and price-driven shoppers, while online channels will capture premium, convenience-seeking, and sustainability-focused consumers willing to pay for curated assortments and delivery convenience.

Geography Analysis

Asia-Pacific captured 28.95% of global revenue in 2025 and will sustain the fastest regional CAGR of 6.33% through 2031, underpinned by urbanization, middle-class expansion, and rising hygiene awareness. China's urbanization rate reached 67% in 2025, with 250 million rural-to-urban migrants over the past decade driving demand for packaged household care products as traditional bulk-buying patterns shift toward branded, single-use formats, according to the National Bureau of Statistics of China. India's middle class expanded by 50 million households annually between 2020 and 2025, with disposable incomes rising 8% per year, enabling trade-up from unbranded detergents to premium laundry pods and specialty cleaners, according to the Reserve Bank of India. E-commerce penetration accelerated, and Alibaba's Tmall and JD.com accounted for a prominent share of China's household care sales in 2025, while India's Flipkart and Amazon India grew year-over-year, leveraging vernacular interfaces and cash-on-delivery options to reach tier-2 and tier-3 cities. Japan and South Korea exhibited mature market characteristics, with innovation focused on compact packaging for small living spaces and enzyme formulations for cold-water washing aligned with energy-efficiency norms.

North America and Europe's growth is shaped by regulatory stringency and sustainability mandates. The European Union's REACH regulation listed over 25,000 registered chemical substances by 2025, requiring extensive safety dossiers that cost USD 50,000-500,000 per substance, favoring multinational corporations with dedicated compliance teams over regional players, according to the European Chemicals Agency. The EU Ecolabel certified 450 household cleaning products in 2025, with certified items commanding 25-35% price premiums as consumers prioritized environmental credentials, according to the European Commission. The United States Environmental Protection Agency's Safer Choice program certified 2,000+ products by 2025, while California's Safer Consumer Products regulation mandated disclosure of 5,000+ chemicals, accelerating reformulation toward plant-based ingredients.

South America, the Middle East, and Africa are driven by population growth, urbanization, and hygiene infrastructure development. Brazil's household care market grew in 2025, supported by government initiatives to expand sewage treatment coverage from 55% to 70% by 2030, increasing demand for toilet cleaners and disinfectants, according to the Brazilian Ministry of Regional Development. Saudi Arabia and the United Arab Emirates exhibited high per-capita consumption due to elevated hygiene standards in hospitality and healthcare sectors, with insect repellent sales growing 18% annually as dengue cases rose in urban areas. Nigeria and South Africa faced challenges from counterfeit products and fragmented retail infrastructure, though mobile money penetration enabled e-commerce growth. Vector-borne disease burdens sustained insect repellent demand. Sub-Saharan Africa accounted for 95% of global malaria deaths in 2024, with 608,000 fatalities driving EPA-registered repellent adoption.

Regulatory Landscape

Regulation for home care products continues to tighten around chemical safety, product traceability, and packaging compliance, with Europe and North America setting many of the de facto requirements for global brands. In the European Union, Regulation (EU) 2026/405 on detergents and surfactants (adopted February 2026) replaces the long-standing Detergents Regulation (EC) No 648/2004 and introduces new compliance obligations, including digital product passports and clearer conformity assessment responsibilities for manufacturers placing detergents on the EU market.

Alongside detergents-specific rules, the EU General Product Safety Regulation (Regulation (EU) 2023/988, GPSR) is supported by updated harmonized standards following Commission Implementing Decision (EU) 2026/901, which entered into force on April 17, 2026. Outside government regulation, voluntary standards also shape formulation and claims substantiation in cleaning products, such as UL 2700 (Edition 2, published April 6, 2026), which updates sustainability and safety-related requirements relevant to hard-floor care and certain microbial-based cleaning products.

Competitive Landscape

The home care market shows moderate consolidation, with Unilever, Procter & Gamble, and Reckitt Benckiser dominating through established brand equity, multi-channel distribution, and global operations. Companies are focusing on product innovation to address consumer needs. In February 2025, Dawn launched PowerSuds liquid dish soap, with a formula that traps, locks, and removes up to 99% of grease. The product prevents grease transfer between dishes during washing, improving efficiency and reducing the need for repeated cleaning.

Emerging brands target market gaps through natural ingredients, cruelty-free certifications, and direct-to-consumer distribution models that enable quick product development. These companies implement subscription services to secure recurring revenue and gather customer data for targeted sales. Investment firms are increasing their funding for sustainable product initiatives, indicating market confidence in industry transformation. Companies continue to expand through mergers and acquisitions. Church & Dwight acquired its Japanese distributor Graphico for USD 19.9 million in June 2024, expanding its Asian visibility.

Digital technology adoption improves operational efficiency. Companies implementing AI-based demand forecasting, automated manufacturing, and machine learning product development report significant productivity improvements, reducing product development time and optimizing inventory management in the home care market. Technology deployment differentiates winners. Henkel's 2024 opening of a EUR 50 million (USD 54 million) fragrance innovation center in Düsseldorf employed AI-driven scent profiling to match consumer mood states to fragrance molecules, reducing time-to-market by 30%. These advances create additional resources for research and marketing investments. However, counterfeit products and increasing regulatory requirements present challenges, particularly for smaller companies, highlighting the importance of strategic partnerships in the home care industry.

Home Care Industry Leaders

-

Henkel AG & Co. KGaA

-

Unilever PLC

-

Procter & Gamble Company

-

Reckitt Benckiser Group PLC

-

Church & Dwight Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities in home care are increasingly concentrated in premium laundry care and format innovation that combines convenience with sustainability and traceability. The shift toward advanced capsule architectures and smart-home compatibility creates a clear whitespace for brands that can support performance claims with credible compliance documentation, especially in Europe where the detergents framework has been refreshed through Regulation (EU) 2026/405 and product-safety compliance is reinforced through the GPSR standards update effective April 2026. Unilever’s April to June 2026 push around four-chamber capsule technology (Persil/Dirt Is Good) and its collaboration with Samsung on auto-dose oriented products shows how incumbents are using appliance integrations and differentiated formats to defend price tiers.

Supply-chain and manufacturing upgrades also offer a route to compete on availability, cost-to-serve, and speed-to-shelf, while supporting refill and concentrated formats. Unilever completed a GBP 150 million investment at Port Sunlight in May 2026, including four-chamber capsule production capability and a new automated distribution center, reflecting continued capacity and logistics modernization for premium laundry formats. A parallel opportunity is emerging in compliant reformulation and labeled-safety positioning, supported by US EPA Safer Choice (2,000+ certified household cleaning products by 2025) and rising scrutiny on VOCs, phthalates, and quats, which together support higher-value safer-ingredient pipelines and more transparent product information systems.

Recent Industry Developments

- July 2026: Henkel relaunched the Purex laundry brand in North America with concentrated liquid formulas and packaging positioned around sustainability, including bottles made with 50% recycled plastic. The update refreshes a mass-market franchise while aligning with the broader shift toward concentrated formats and packaging claims that resonate with value and eco-aware shoppers.

- May 2026: Unilever completed a GBP 150 million investment at its Port Sunlight site, upgrading a Home Care factory to produce four-chamber laundry capsules and adding a 10,000 square-metre automated distribution center. The combination of production capability and automated logistics supports regional supply resilience for premium formats and supports faster replenishment for large retail channels.

- June 2024: Church & Dwight acquired its Japanese distributor Graphico for USD 19.9 million, expanding its commercial footprint and control of route-to-market in Japan. The deal increases local execution capability and supports broader Asia visibility for household and personal care portfolios.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the home care market covers packaged household cleaning and hygiene products used in residential settings, and it is measured as the annual value generated from these products across global markets.

Scope exclusions: Professional janitorial services, institutional cleaning programs, in-home care services, and home healthcare equipment are excluded from this market sizing.

Segmentation Overview

-

Product Type

- Air Care

- Dishwashing

- Bleach

- Insect Repellent

- Laundry Care

- Surface Care

- Toilet Care

-

Packaging Format

- Bottles

- Aerosol Cans

- Pouches

- Other Packaging Formats

-

Formulation

- Synthetic

- Natural and Organic

-

Distribution Channel

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Online Retail Stores

- Others Distribution Channel

-

Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map product boundaries, demand signals, and price movement patterns that influence retail value in home care. We used public sources such as national statistics portals for consumer spending and CPI series, UN Comtrade-style trade statistics for relevant chemical and packaged product flows, and government environment agencies for surfactant, disinfectant, and packaging related policy direction.

To make assumptions more realistic, we also reviewed sources such as trade association publications for detergents and cleaning products, peer-reviewed journals that cover formulation and efficacy trends, and company filings and investor presentations that explain category growth and channel mix. Where needed, paid subscriptions for company financials and news were used to cross-check revenue exposure and event impacts, and patent databases were referenced to track how fast new formats and formulations are being introduced. These are illustrative inputs only, and many other public sources were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was done through expert interviews and short surveys with participants across product manufacturing, distribution, and retail, along with select packaging and ingredient ecosystem contacts who see volume and pricing shifts early. Since the market is global, inputs were balanced across APAC, EMEA, and the Americas so assumptions on category growth, channel share, and price premiumization could be checked against local sourcing and shelf realities.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 13% | APAC: 39% |

| Mid tier: 43% | Functional/Unit leaders: 27% | EMEA: 34% |

| Smaller Players: 19% | Managers: 60% | Americas: 27% |

Market-Sizing & Forecasting

Market sizing was built using a top-down approach where country-level demand pools are reconstructed from household consumption signals, category penetration, and observed pricing ranges, which are then converted into value. We then corroborated the totals using selective bottom-up checks, such as sampled brand and private label price points multiplied by estimated category volumes, and channel checks on modern trade versus e-commerce splits.

Key inputs that shaped the model included household count and urbanization trends, product usage frequency for laundry and surface cleaning, category mix shifts (for example, liquid versus powder and unit-dose adoption), average selling price movement tied to input cost cycles, and the pace of premiumization in larger markets. Where data was thin for smaller countries, gaps were handled by using peer-market proxies with similar income bands and retail channel structures, followed by adjustments from primary feedback.

For forecasting, we relied mainly on scenario analysis supported by a simple multivariate regression layer for the larger countries, using variables such as disposable income growth, inflation-adjusted price trends, and channel expansion as the explanatory drivers. Assumptions were then stress-tested with interview feedback on promotions, pack-size changes, and downtrading behavior during high inflation periods.

Data Validation & Update Cycle

Outputs were validated by triangulating the modeled market totals against independent signals such as category growth commentary in filings, public trade and production indicators for key inputs, and visible pricing movement in major retail channels. When a country or category showed an unusual jump, the logic was reviewed step by step, and the assumption was either corrected or flagged for follow-up.

Before sign-off, results go through multi-step analyst reviews, with variance checks across regions and across product categories to make sure the story matches the numbers. The report is refreshed annually, and interim updates are made when material events occur, such as major regulatory actions, sharp raw material price swings, or channel disruptions. Right before delivery, a final pass is done so clients receive the most current view available.

Mordor Intelligence's Home Care Market Estimate Compared With Other Published Estimates

Published market sizes for home care do not always match because the underlying definition can shift between consumer packaged products and service-led care delivered at home, and because firms also vary on currency timing and inflation handling. Differences also show up when some studies mix household and institutional demand, or treat price premiumization assumptions in a more aggressive way.

By tracking constant-dollar conversion rules and category boundaries, Mordor Intelligence keeps the home care number tied to packaged household cleaning and hygiene products sold for residential use, which avoids pulling in adjacent service revenue or institutional spend that inflates the total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 202.34 B (2026) | |

| Global Consultancy A | USD 183.78 B (2026) | Uses a narrower category basket in its published scope and may blend household and commercial end-use differently, which can reduce the consumer-only value for the same year. It also does not clearly state a constant-dollar treatment, so inflation and currency timing can shift the reported level. |

| Industry Research Group B | USD 392.10 B (2025) | The scope is centered on home care services like personal and nursing care, which is a different revenue pool than packaged home care products. The base year is also different, and the higher growth path is driven by service utilization assumptions rather than retail category volumes and pricing. |

The comparison shows that the spread is mostly explained by scope, not just math, since one estimate sizes consumer packaged products while another sizes in-home services. When the same boundary and currency logic are applied consistently, the market total becomes easier to trace back to clear demand drivers and repeatable steps.

Key Questions Answered in the Report

What is the current value of the household care products market?

The household care products market size was USD 202.34 billion in 2026 and is forecast at USD 262.45 billion by 2031.

Which product type generates the highest revenue?

Laundry Care led with 54.03% of 2025 sales thanks to high-frequency use and strong brand loyalty.

Which segment is growing the fastest?

Air Care is projected to log the highest CAGR at 6.76% through 2031 as connected diffusers and premium fragrances gain favor.

How important is Asia-Pacific to future sales?

Asia-Pacific already delivers 28.95% of global turnover and is expected to grow at a 6.33% CAGR through 2031, the fastest of any region.

Page last updated on: