Floor Adhesives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.22 Billion |

| Market Size (2031) | USD 2.81 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Floor Adhesives Market Analysis by Mordor Intelligence

The Floor Adhesives Market size was valued at USD 2.12 billion in 2025 and estimated to grow from USD 2.22 billion in 2026 to reach USD 2.81 billion by 2031, at a CAGR of 4.78% during the forecast period (2026-2031). Infrastructure spending in Asia-Pacific, the commercial sector’s tilt toward resilient surfaces, and stricter indoor-air-quality regulations reinforce demand for high-performance bonding systems. Resin producers are investing in bio-based polyurethane lines that reduce carbon footprints and align with green-building criteria, while contractors in mature economies continue to drive replacement purchases through renovation projects. Meanwhile, supply-chain localization in North America and Europe lowers import dependence for luxury vinyl tile (LVT) adhesives, even as petrochemical feedstock volatility nudges manufacturers to optimize raw-material sourcing. Growing interest in modular flooring and releasable adhesive technologies is widening the addressable user base beyond traditional professional installers to include facility managers and Do-It-yourself (DIY) consumers.

Key Report Takeaways

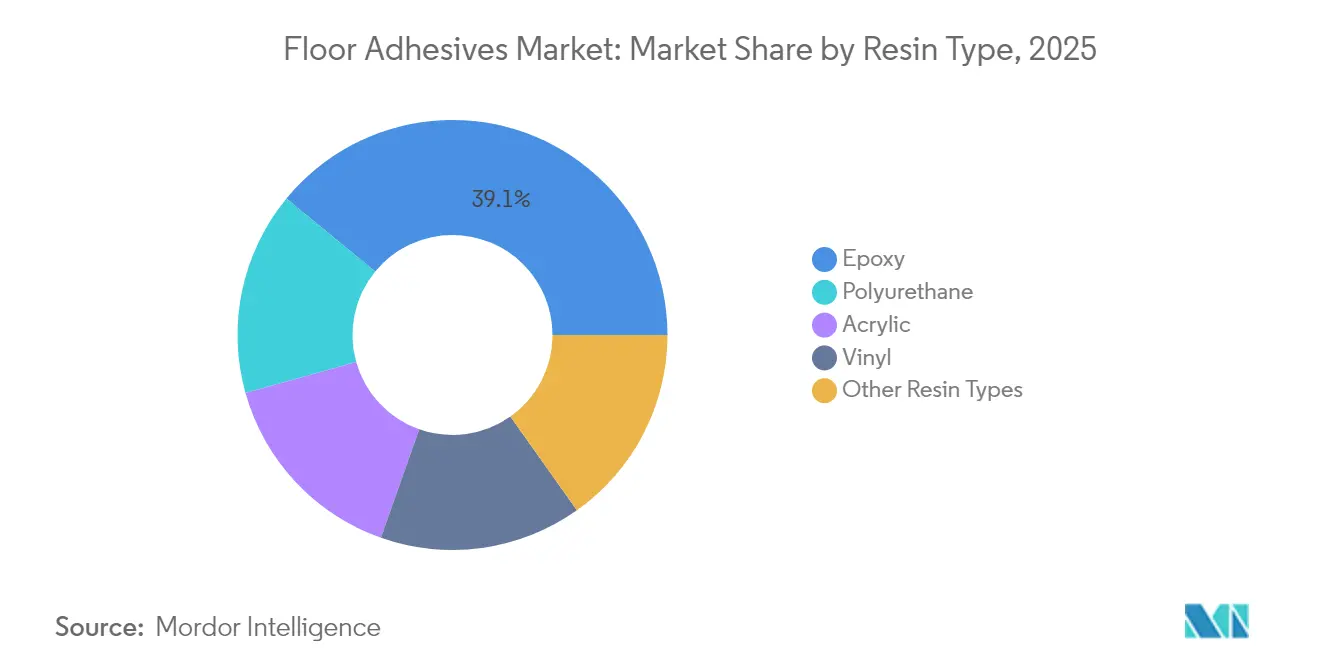

- By resin type, epoxy led with 39.05% revenue share in 2025; polyurethane is projected to expand at a 5.06% CAGR to 2031.

- By technology, solvent-borne systems held 44.20% of the Floor Adhesives market share in 2025, while water-borne variants are forecast to grow at 5.48% CAGR through 2031.

- By application, tile and stone accounted for 39.95% share of the Floor Adhesive market size in 2025 and is advancing at a 5.12% CAGR through 2031.

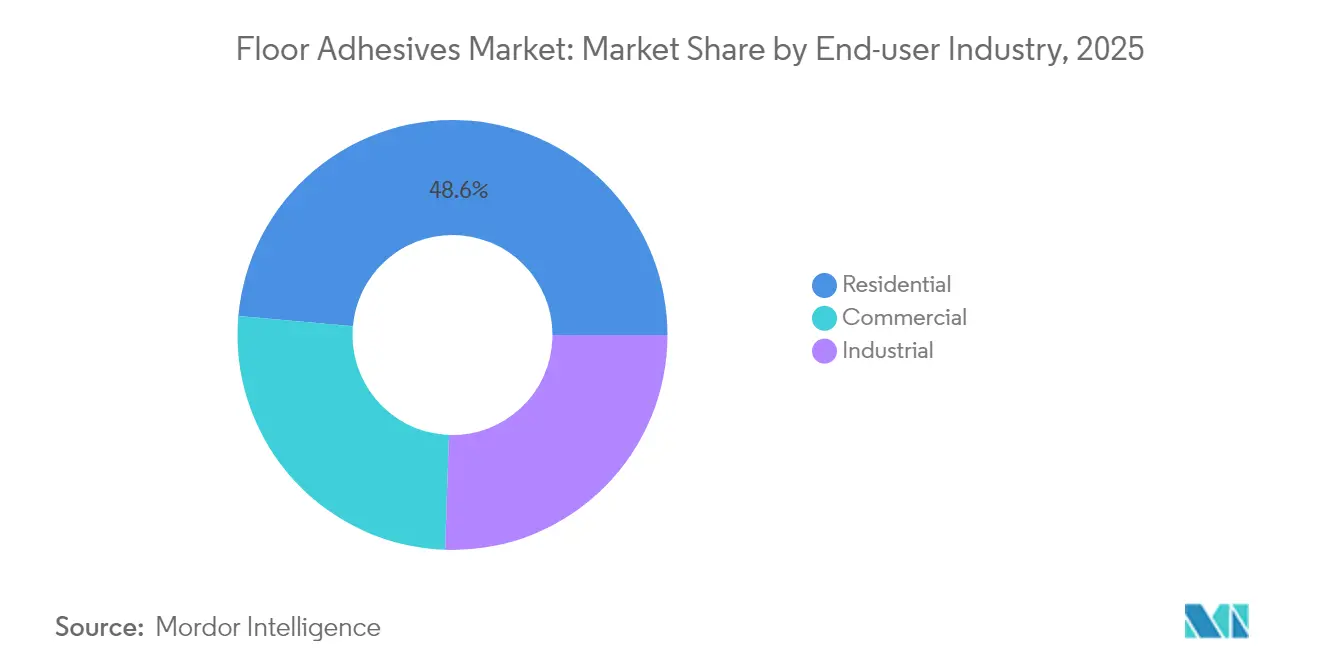

- By end-user industry, residential captured 48.60% share in 2025; commercial is the fastest-rising segment at 4.96% CAGR to 2031.

- By geography, Asia-Pacific dominated the floor adhesive market, holding a with a 43.40% share in 2025, and expanding at a 5.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Floor Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapidly Growing Global Construction Spending | +1.2% | Global, with strongest impact in APAC and Americas | Medium term (2-4 years) |

| Rising Renovation and Remodeling Demand in Mature Economies | +0.8% | North America & Europe, spillover to urban APAC | Short term (≤ 2 years) |

| Commercial Shift Toward Resilient and LVT Flooring Systems | +1.0% | Global, led by North America and Europe | Medium term (2-4 years) |

| Emergence of Modular Flooring Needing Releasable Adhesives | +0.6% | North America & Europe, early adoption in commercial sectors | Long term (≥ 4 years) |

| Bio-based Polyurethane Recipes Aligned with Green Buildings | +0.4% | Europe and North America, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapidly Growing Global Construction Spending

Construction outlays are increasing worldwide, giving the Floor Adhesive market a steady pipeline of projects that need durable bonding solutions. United States construction spending climbed 11.3% year over year in 2024, lifted by an 18% surge in non-residential work and single-family housing gains of 5.5%. India’s cement demand, a proxy for building activity, is expected to rise at 7.5% CAGR through 2026 under government housing programs that have delivered 25.64 Million rural units. The contractor backlog of 8.5 months signals consistent adhesive consumption, while semiconductor-plant construction incentivized by the Creating Helpful Incentives to Produce Semiconductors (CHIPS) and Science Act adds high-specification flooring needs. Legislative infrastructure packages in Brazil, Indonesia, and Saudi Arabia are creating parallel opportunities for suppliers offering moisture-resistant epoxy and quick-set polyurethane systems. Moderate raw-material inflation of 2% annually is allowing producers to pass through price increases without eroding demand, preserving margins across residential and commercial channels.

Rising Renovation and Remodeling Demand in Mature Economies

Deferred maintenance during 2024 created pent-up replacement activity that is now boosting adhesive sales in North America and Europe in the Floor Adhesive market. The United States flooring sector managed 3% growth in 2024 as commercial gains offset residential softness, but industry executives forecast a sharper recovery in 2025 once mortgage rates ease and secondary-home transactions rebound. European households are undertaking energy-efficiency upgrades that frequently involve installing new waterproof floor systems, which require low-volatile organic compound (VOC) adhesives to satisfy stricter indoor-air-quality codes. Retail home-improvement chains report higher demand for pressure-sensitive products that simplify Do-It-Yourself (DIY) installation, widening the customer base beyond professional contractors. Premium pricing for water-borne acrylics with fast tack times is improving retailer margins, while e-commerce channels are promoting small-pack offerings for consumers handling spot repairs. These trends collectively support recurring revenue streams for adhesive suppliers even when new-build volumes fluctuate.

Commercial Shift Toward Resilient and LVT Flooring Systems

Resilient products captured 27.6% of manufacturers’ flooring sales in 2024 in the Floor Adhesive market, with LVT revenue reaching USD 5.65 billion as facility owners pursue waterproof, easy-maintenance surfaces. Rigid-core LVT, particularly stone-plastic composite formats, displaces traditional materials and necessitates adhesives that tolerate substrate movement and moisture vapor. Commercial carpet tiles, representing 80% of the specified soft-surface market, increasingly rely on releasable adhesives that allow future module swaps without subfloor damage. Education and healthcare renovations funded by pandemic-related grants prioritize hygienic, chemical-resistant floors, accelerating demand for epoxy formulations with antimicrobial additives. Sustainability mandates such as Leadership in Energy and Environmental Design (LEED) steer specifiers toward bio-based or low-emission bonding agents, prompting suppliers to certify products under Indoor Advantage Gold and other programs. As a result, adhesive makers can balance green credentials with high bond strength are winning specifications in major commercial roll-outs.

Emergence of Modular Flooring Needing Releasable Adhesives

Circular-economy principles are encouraging designers in the Floor Adhesive market to choose flooring systems that can be removed and repurposed, spurring a niche for pressure-sensitive and peelable adhesives. Modular carpet specialists have unveiled backing constructions engineered for rapid uplift without substrate scraping, a feature valued in leased offices and pop-up retail [1]. European Union directives on product disassembly are setting precedents that could migrate into building codes, potentially making releasability a procurement requirement. Research into mycelium- and chitosan-based binders offers environmental advantages because the materials naturally break down, reducing end-of-life disposal concerns. Manufacturers like Henkel are adapting packaging wash-off adhesive chemistry to flooring, widening the palette of reversible solutions. Facility managers view these systems as cost-effective over multiple renovation cycles, reinforcing long-term demand for specialized formulations.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC and Indoor-air-quality Regulations | -0.7% | Global, strictest in Europe & North America | Short term (≤ 2 years) |

| Volatile Petrochemical Feedstock Prices | -0.5% | Global, acute in import-dependent regions | Short term (≤ 2 years) |

| Installer Skill Shortages for Advanced Adhesives | -0.3% | North America & Europe; emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC and Indoor-Air-Quality Regulations

Tougher emission limits are reshaping adhesive chemistry, compelling producers in the floor adhesives market to reformulate legacy solvent-borne lines. The United States Environmental Protection Agency imposed new reactivity-weighted VOC caps for aerosol coatings in January 2025, tightening permissible thresholds for carpet and fabric adhesives to 5% organic hazardous air-pollutants by weight. Europe’s REACH rules now restrict products containing over 0.1% diisocyanates, hastening adoption of two-part epoxies and acrylics in structural flooring applications. California’s South Coast Air Quality Management District (AQMD) maintains the world’s lowest VOC allowance at 4 g/L for certain carpet-pad glues, effectively setting a de-facto national benchmark. Compliance costs include sourcing low-odor propylene glycol ethers and installing closed-loop mixing lines, raising capital expenditure for small regional blenders. While these policies suppress short-term solvent demand, they also open differentiation avenues for suppliers offering certified zero-VOC water-borne or bio-based alternatives.

Volatile Petrochemical Feedstock Prices

Floor-adhesive margins in the floor adhesives market are vulnerable to swings in propylene oxide, polyether polyol, and epichlorohydrin prices that feed epoxy and polyurethane chains. During supply disruptions, polypropylene contract values rose 9% between Q1 and Q3 2024, while polyethylene climbed 7% on refinery turnarounds. Producers responded by introducing price-in-effect clauses tied to monomer indices and accelerating trials with recycled or bio-attributed feedstocks with more stable cost structures. End-users resisted frequent list-price changes, forcing manufacturers to amortize hikes across product portfolios. Volatility is most acute in import-reliant markets like South America, where currency depreciation compounds raw-material inflation. These conditions incentivize local sourcing agreements and long-term supply contracts, but can still trim demand when contractors delay projects awaiting price relief.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Polyurethane Innovation Drives Sustainable Growth

Epoxy systems retained a 39.05% share of the Floor Adhesive market in 2025, favored for chemical resistance and high compressive strength in logistics centers and healthcare corridors. Polyurethane volumes are rising fastest at a 5.06% CAGR, propelled by bio-based polyols that cut embodied carbon by up to 50% and qualify for green-building credits. The Floor Adhesives market size for polyurethane grades is projected to reach USD 1.07 billion by 2031, capturing incremental demand from resilient vinyl planks that flex with substrate movement. Acrylic dispersions continue to serve residential renovations where odor neutrality and quick tack are priorities, while hybrid moisture-cure chemistries tackle niche cold-storage and food-processing floors. Henkel’s LOCTITE HB S ECO platform uses more than 60% bio-attributed feedstock, demonstrating how sustainable claims can secure premium specifications in public-sector bids.

Adhesive manufacturers are scaling pilot plants for vegetable-oil-derived polyols in the floor adhesives market that maintain equivalent tensile properties to petroleum-based references, bridging performance gaps that once limited adoption. BASF reported a 30% product-carbon-footprint drop after shifting ethyl acrylate production to biomass-balanced feedstock, signaling broader industry migration. Demand for low-exotherm epoxies in thick-pour self-leveling floors is also climbing, and suppliers are adding latent-curing amines that extend pot life for large commercial pours. Collectively, these resin-level innovations position chemistry as the key differentiator in winning high-value projects.

By Technology: Water-borne Solutions Gain Regulatory Momentum

Solvent-borne lines still command 44.20% of 2025 revenues thanks to proven bond strength and broad installer familiarity, but tightening VOC limits are shifting share to water-borne products growing at 5.48% CAGR . The floor adhesives market size attributed to water-borne chemistries is forecast to surpass USD 1.12 billion by 2031 as builders and architects seek low-odor installations that minimize project downtime. VINNAPAS eco polymer dispersions substitute fossil n-butanol with bio-methanol inputs, reducing Scope 3 emissions without sacrificing shear strength, illustrating how water-borne platforms can compete head-to-head on performance. Hot-melt reactive urethanes find use in fast-track retail store rollouts where 1-hour walk-on time is essential, though their overall penetration remains niche due to equipment costs.

Regulatory compliance is the chief tailwind in the floor adhesive market: California’s upcoming 2026 Air Resources Board revision may ban certain aromatic solvents entirely, giving water-borne suppliers a head start on specification. Manufacturers are upgrading rheology modifiers to improve early-grab characteristics and adding crosslinkers that raise heat resistance, answering historical installer objections. As awareness grows, distributors are dedicating shelf space to two-part water dispersions packaged in dual-pouch sachets that lower mixing errors, further accelerating adoption.

By Application: Tile and Stone Dominance Reflects LVT Boom

The tile and stone application segment captures both the largest market share at 39.95% in 2025 for the floor adhesive market and the fastest growth rate at 5.12% CAGR through 2031, reflecting the luxury vinyl tile market's explosive expansion and commercial sector preference for hard surface flooring. Carpet applications maintain significant demand in commercial settings, particularly modular carpet tiles that require specialized pressure-sensitive adhesives for easy replacement and maintenance. Wood flooring applications benefit from moisture-blocking adhesive innovations that address substrate variability and seasonal movement, while laminate installations increasingly specify adhesives that accommodate floating floor systems.

Major manufacturers like Mohawk Industries are committing over USD 900 million to enhance domestic manufacturing capabilities in the floor adhesive market, reducing reliance on Asian imports while improving supply chain resilience. The shift toward polyvinyl chloride (PVC)-free hybrid alternatives to wood plastic composite and stone plastic composite is creating demand for adhesives compatible with new substrate chemistries and environmental requirements. Commercial flooring contractors are expanding services to include complex multi-surface projects, requiring adhesive systems that can bond dissimilar materials while meeting varying performance specifications across different flooring types.

By End-user Industry: Residential Segment Maintains Growth Leadership

Residential applications command 48.60% market share in 2025 and are expected to sustain growth at 4.87% CAGR through 2031 in the floor adhesives market, driven by renovation demand in mature markets and new construction activity in emerging economies. Commercial applications benefit from infrastructure investments and the shift toward resilient flooring systems that require advanced adhesive technologies for high-traffic environments. Industrial applications, while representing the smallest segment, demand specialized adhesive formulations that can withstand chemical exposure, temperature extremes, and mechanical stress in manufacturing and processing facilities.

The residential sector's dominance reflects both renovation activity in established markets and new construction in developing regions, with India's housing initiatives in the floor adhesive market creating substantial adhesive demand through programs like the Pradhan Mantri Awas Yojana. The United States residential market's recovery prospects for 2025, driven by anticipated mortgage rate declines and pent-up demand, position floor adhesives for accelerated growth as homeowners resume deferred improvement projects. Commercial applications are increasingly specifying sustainable adhesive systems that contribute to LEED certification and other green building standards, creating premium pricing opportunities for manufacturers offering bio-based and low-emission formulations. The education sector's strong demand, supported by pandemic-related funding, is driving commercial adhesive sales as schools prioritize durable and hygienic flooring solutions that require advanced bonding technologies.

Geography Analysis

Asia-Pacific led with 43.40% of 2025 revenue and is set to advance at a 5.92% CAGR through 2031 as megaproject pipelines in India and Indonesia accelerate tender activity. The floor adhesive market share of the region benefits from China’s urban-renewal budgets and railway expansions that specify vibration-dampening epoxy mortars. Foreign direct investment into Vietnam’s industrial parks is spawning demand for anti-static flooring bonded with conductive polyurethane. India’s INR 20,000 crore (USD 2.3 Billion) construction-chemicals sector is luring global entrants; Master Builders Solutions targets INR 500 crore (USD 58 Billion) turnover by 2028 via localized tile-adhesive lines compatible with high-humidity climates.

North America ranks second, underpinned by an 11.3% uptick in 2024 construction expenditure and federal incentives for semiconductor fabs that require dust-free, chemical-resistant floors. The United States commercial installations' floor adhesives market size is poised for mid-single-digit growth once deferred healthcare and education refurbishments restart in 2025. Canada’s infrastructure plan allocates CAD 33 Billion (USD 24.1 Billion) to public transit upgrades and channel orders to moisture-mitigating epoxies for station platforms. Europe’s trajectory is flatter, yet premium due to regulations; Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH)-compliant acrylics enjoy price premiums of 8-10% over legacy solvent lines, preserving supplier profitability even as volumes level off.

South America and the Middle East & Africa collectively represent less than 15% of 2025 demand floor adhesive market but offer upside in mega-events and tourism projects. Saudi Arabia’s NEOM smart-city development is tendering hospital and hotel flooring packages that mandate low-VOC adhesives, creating entry points for water-borne specialists. Brazil’s tax incentives for domestic petrochemical investments could stabilize local raw-material costs, moderating price swings that have historically dampened adhesive uptake.

Competitive Landscape

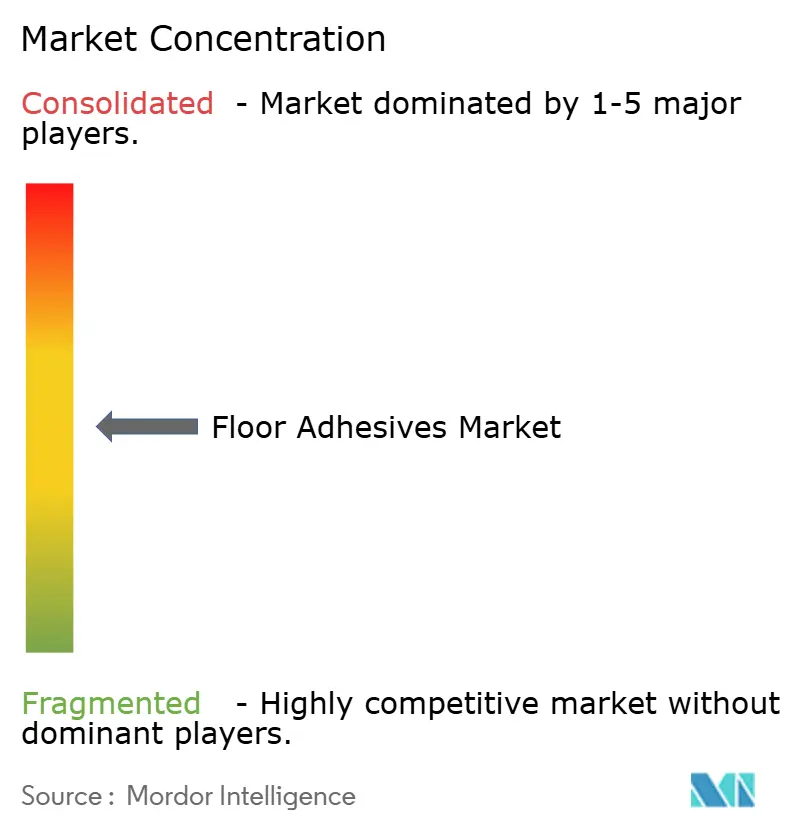

The Floor Adhesive Market is moderately consolidated with the presence of major players, such as Sika AG, MAPEI S.p.A., Henkel AG & Co. KGaA, H.B. Fuller Company, and Arkema. These players leverage multi-continent production footprints and patent portfolios exceeding 2,500 active filings to defend share in epoxy and polyurethane niches. Saint-Gobain’s USD 1.025 Billion purchase of FOSROC expanded its geographic reach to 73 countries, unlocking cross-selling of flooring adhesives through established grout distribution. H.B. Fuller Company divested its floor-covering unit to Pacific Avenue Capital for USD 80 Million, freeing capital to concentrate on high-margin electronics and hygiene segments. Pricing discipline has strengthened since 2024’s raw-material spike; leading suppliers issued 5-7% list hikes but cushioned contractors with extended payment terms.

Floor Adhesives Industry Leaders

Sika AG

H.B. Fuller Company

Henkel AG & Co. KGaA

Arkema

MAPEI S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Sika AG launched SikaBond-5900 and SikaBond-5800, two time-tested resilient flooring adhesives for the interior installation of luxury vinyl tile, luxury vinyl plank, vinyl sheet goods, fiberglass-backed sheet vinyl, carpet tile, rubber flooring, and more for residential and commercial applications.

- February 2024: Pidilite Industries Ltd. announced the inauguration of a new state-of-the-art manufacturing facility in Sandila, India, for its prominent tile adhesive (floor adhesive) brand, Roff. This facility is set to enhance Roff’s footprint in North India, catering to markets in Central and Eastern Uttar Pradesh, Madhya Pradesh, and certain areas of Bihar.

Global Floor Adhesives Market Report Scope

Floor adhesive is any strong, permanent glue for adhering flooring materials to a subfloor or underlayment. The floor adhesives market is segmented by resin type, technology, application, end-user industry, and geography. By resin type, the market is segmented into epoxy, polyurethane, acrylic, vinyl, and other resin types. By technology, the market is segmented into water-borne, solvent-borne, and other technologies. By application, the market is segmented into tile and stone, carpet, wood, laminate, resilient flooring, and other applications. By end-user industry, the market is segmented into residential, commercial, and industrial. The report also covers the size and forecasts for the floor adhesives market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD million).

| Epoxy |

| Polyurethane |

| Acrylic |

| Vinyl |

| Other Resin Types |

| Water-borne |

| Solvent-borne |

| Other Technologies |

| Tile and Stone |

| Carpet |

| Wood |

| Laminate |

| Resilient Flooring |

| Other Applications |

| Residential |

| Commercial |

| Industrial |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Resin Type | Epoxy | |

| Polyurethane | ||

| Acrylic | ||

| Vinyl | ||

| Other Resin Types | ||

| By Technology | Water-borne | |

| Solvent-borne | ||

| Other Technologies | ||

| By Application | Tile and Stone | |

| Carpet | ||

| Wood | ||

| Laminate | ||

| Resilient Flooring | ||

| Other Applications | ||

| By End-user Industry | Residential | |

| Commercial | ||

| Industrial | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Floor Adhesives market and how fast is it growing?

The Floor Adhesives Market size is expected to reach USD 2.22 Billion in 2026 and grow at a CAGR of 4.78% to reach USD 2.81 Billion by 2031.

Which resin type leads global demand?

Epoxy systems hold the largest 2025 share at 39.05%, owing to high chemical resistance and durability in heavy-traffic settings.

Why are water-borne adhesives gaining traction?

Tightening VOC regulations in North America and Europe favor low-emission products, enabling water-borne lines to grow at a 5.48% CAGR.

Which region offers the strongest growth outlook?

Asia-Pacific commands 43.40% of 2025 revenue and is expanding fastest at 5.92% CAGR, driven by large-scale infrastructure projects in China and India.

How are installer shortages affecting the industry?

A shrinking skilled-labor pool in the United States and Europe is slowing adoption of advanced moisture-mitigating systems, prompting suppliers to fund training programs.

Page last updated on: