High-Performance Data Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

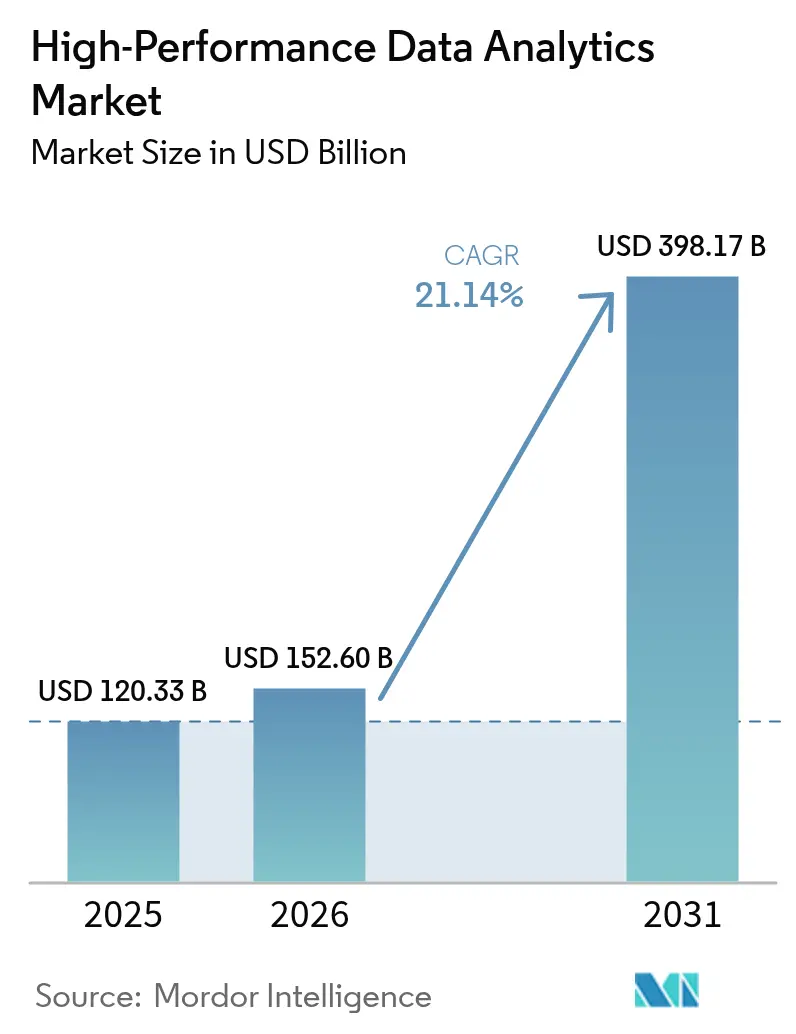

| Market Size (2026) | USD 152.60 Billion |

| Market Size (2031) | USD 398.17 Billion |

| Growth Rate (2026 - 2031) | 21.14% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High-Performance Data Analytics Market Analysis by Mordor Intelligence

The high-performance data analytics market size is expected to increase from USD 120.33 billion in 2025 to USD 152.60 billion in 2026 and reach USD 398.17 billion by 2031, growing at a CAGR of 21.14% over 2026-2031. Surging AI and machine-learning model training, real-time fraud detection in banking, and renewable-energy grid optimization are forcing enterprises to replace legacy clusters with parallel GPU architectures. Cloud and hybrid deployments dominate because hyperscalers rent accelerators on demand, removing capital barriers for small and medium enterprises. Hardware still captures the largest revenue, yet accelerators GPUs, FPGAs, and ASICs are the fastest-growing component as workloads shift toward tensor-optimized chips. Regionally, North America leads on spending, but Asia-Pacific is the growth engine as sovereign-AI mandates in China, Japan, and India expand petascale capacity.

Key Report Takeaways

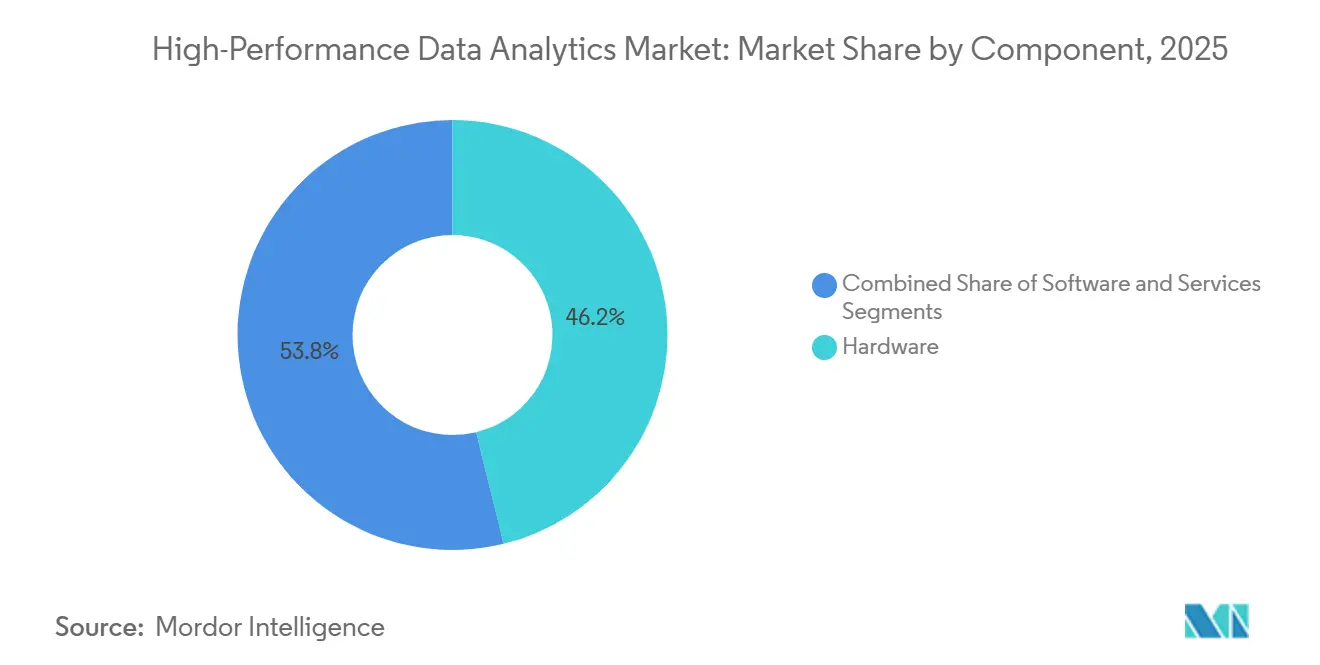

- By component, hardware led with 46.19% revenue share in 2025, while accelerators are forecast to expand at a 21.97% CAGR through 2031.

- By deployment model, cloud and hybrid captured 71.84% of the high-performance data analytics market share in 2025, whereas the same segment is projected to grow at a 21.56% CAGR to 2031.

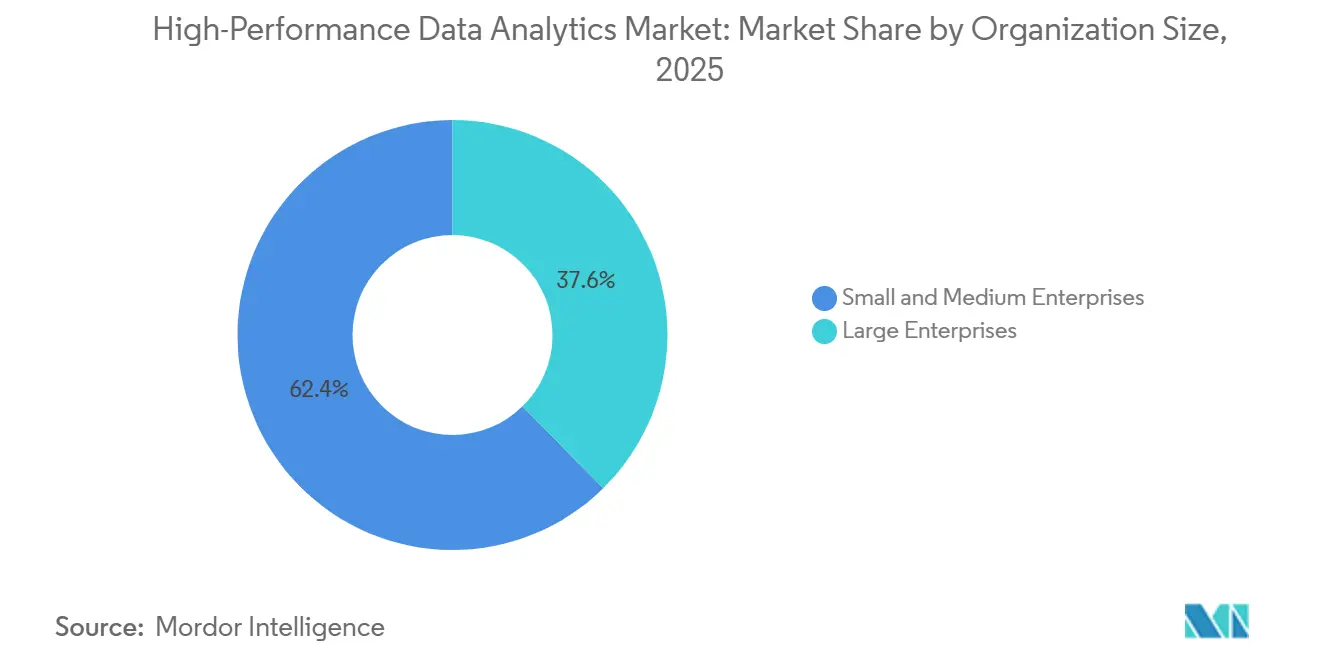

- By organization size, large enterprises held 62.36% of spending in 2025, but small and medium enterprises are advancing at a 21.67% CAGR during 2026-2031.

- By end-user industry, banking, financial services, and insurance contributed 24.53% of revenue in 2025, yet retail and e-commerce is set to grow at a 21.88% CAGR to 2031.

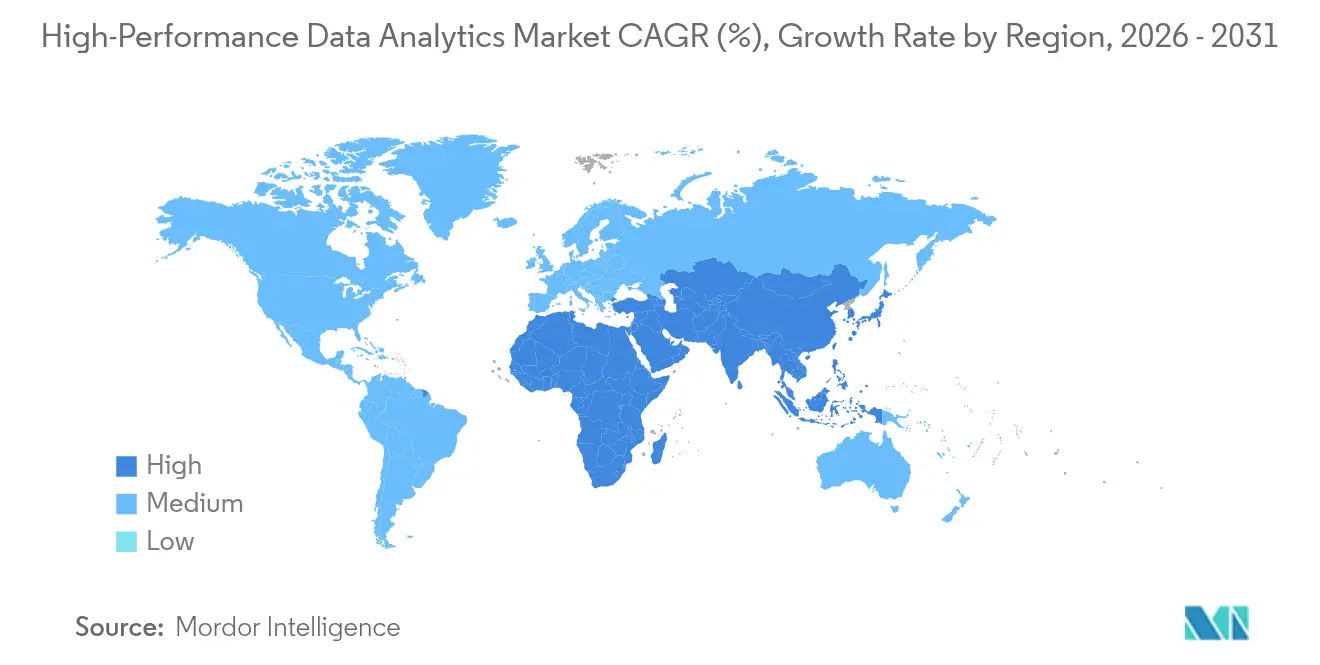

- By geography, North America commanded 41.29% share in 2025, while Asia-Pacific is on track for a 22.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global High-Performance Data Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in AI and ML Model Training Requiring Petabyte-Scale Data Processing | +4.20% | Global, with concentration in North America, China, and Europe | Medium term (2-4 years) |

| Growth of Edge-to-Cloud HPC for Smart Manufacturing | +3.80% | APAC core (China, Japan, South Korea), spill-over to North America and Europe | Medium term (2-4 years) |

| Accelerating Adoption of Real-Time Analytics in BFSI for Fraud Detection | +3.50% | Global, led by North America and Europe, expanding in APAC | Short term (≤ 2 years) |

| Falling Cost-per-Core for GPU and CPU Clusters Enabling Affordable HPC for SMEs | +3.10% | Global, with early gains in North America, Europe, and India | Long term (≥ 4 years) |

| National Defense Big-Data Modernization Programs | +2.90% | North America, Europe, Australia, and Middle East | Long term (≥ 4 years) |

| Renewable-Energy Grid Optimization Initiatives Driving HPC Analytics | +2.60% | Europe, North America, with emerging adoption in China and India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in AI and ML Model Training Requiring Petabyte-Scale Data Processing

Large language-model and generative-AI workloads regularly draw on training sets above 10 petabytes, forcing enterprises to abandon disk-bound Hadoop clusters for GPU-accelerated frameworks that cut time-to-convergence by a factor of ten.[1]Nvidia Corporation, “Nvidia NeMo Framework Accelerates Large Language Model Training,” nvidia.com Hyperscalers in North America and China logged a 340% year-over-year jump in GPU instance hours during 2025 as companies fine-tuned foundation models for legal discovery, drug-target finding, and automated driving.[2]Bloomberg News, “AWS, Microsoft Slash GPU Pricing to Capture AI Workloads,” bloomberg.com The Cerebras WSE-3 single-chip system delivered 52 petaflops at Argonne National Laboratory in 2026, demonstrating that wafer-scale designs can remove network bottlenecks.[3]Microsoft Azure, “Hybrid HPC Architecture for Enterprise Workloads,” azure.microsoft.com Cloud providers now bundle automated orchestration tools that manage checkpointing and fault tolerance, letting data scientists focus on model logic without deep MPI knowledge. Once a training job exceeds 72 hours, GPU clusters become the lowest-cost option, a threshold already crossed by 60% of enterprise AI projects in 2025.[4]McKinsey and Company, “AI Training Infrastructure: Economic and Technical Considerations,” mckinsey.com

Growth of Edge-to-Cloud HPC for Smart Manufacturing

Industrial plants now stream more than 1 terabyte of sensor data per day, prompting deployment of compact edge servers that flag anomalies within milliseconds before shipping summaries to cloud warehouses. Intel and Foxconn equipped 500 assembly lines in Shenzhen with OpenVINO edge devices in 2025, cutting defect-detection latency from 8 seconds to 120 milliseconds and lowering scrap by 18%. Automakers mirror the pattern: BMW’s Regensburg plant uses HPE Edgeline gear to inspect 3D weld data in real time. Japan’s Ministry of Economy, Trade and Industry set aside JPY 45 billion (USD 310 million) in 2025 to subsidize similar edge installations, targeting a 12% productivity lift by 2028. International standards such as ISO 23247 are locking in interoperability, allowing mixed fleets of Nvidia Jetson inference modules and AMD EPYC preprocessing nodes.

Accelerating Adoption of Real-Time Analytics in BFSI for Fraud Detection

Global payment networks require sub-second fraud scoring, pushing banks toward GPU-accelerated graph analytics that map billions of transaction nodes. JPMorgan Chase processed 12 billion transactions in 2025 on IBM Power10 servers with Nvidia A100 GPUs, flagging 4.2 million high-risk events while cutting false positives by 30%. Europe’s PSD3 rule, effective January 2026, mandates real-time monitoring, catalysing upgrades across the region. Oracle’s Exadata X10M, released mid-2025, retains fraud-model state in persistent memory, trimming cold-start latency by 80%. In Asia-Pacific, banks blend public-cloud front ends with on-premises analytics engines to stay within sovereignty rules, following implementations by DBS Bank and ICICI Bank.

Falling Cost-per-Core for GPU and CPU Clusters Enabling Affordable HPC for SMEs

Accelerator prices fell 35% year-over-year in 2025 as hyperscalers introduced home-grown chips such as AWS Trainium2, widening access for cash-constrained firms. Consumption-based billing removes capital outlays, letting SMEs scale clusters by the hour instead of buying equipment outright. Dell’s APEX service converts on-premises deployments into monthly subscriptions, giving predictable costs and automatic three-year hardware refreshes. Public-sector incentives reinforce the trend: India’s Digital India program reimburses up to 50% of eligible cloud expenses for qualifying SMEs. As accelerator-to-CPU price ratios drop, the payback period for bursting to cloud slips below six months for seasonal workloads, accelerating adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership for Dedicated HPC Clusters | -2.80% | Global, particularly acute for mid-tier enterprises in North America and Europe | Short term (≤ 2 years) |

| Shortage of Skilled HPC and Parallel Programming Professionals | -2.20% | Global, with severe gaps in APAC and emerging markets | Long term (≥ 4 years) |

| Data-Sovereignty Regulations Limiting Cross-Border Cloud Analytics | -1.90% | Europe (GDPR), China, India, with emerging restrictions in Middle East | Medium term (2-4 years) |

| Infrastructure Reliability Issues in Emerging Markets Hampering Continuous Data Streams | -1.60% | Sub-Saharan Africa, Southeast Asia, parts of South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership for Dedicated HPC Clusters

On-premises clusters cost roughly USD 15,000 per GPU node, and annual power, cooling, and maintenance add another 40%-60% of the initial spend, discouraging mid-tier enterprises. A 2025 Deloitte survey found 58% of European manufacturers cited unpredictable egress fees as a major cloud drawback, eroding projected savings. Power draw is formidable: a 1,024-node Nvidia H100 cluster can consume 2.5 megawatts, comparable to 1,800 homes, forcing operators to secure dedicated utility contracts. Liquid-cooling adds USD 1.2 million per megawatt of heat removed, according to an Uptime Institute report. These economics disadvantage firms with intermittent workloads like quarterly forecasts, prompting a migration to pay-per-use models.

Shortage of Skilled HPC and Parallel Programming Professionals

Sixty-eight percent of global HPC centers reported open CUDA, OpenMP, or MPI roles in 2025, and time-to-hire for senior staff averaged nine months. Universities graduate fewer than 2,000 parallel-computing specialists annually against 18,000 openings, inflating salaries and slowing deployments. Asia-Pacific faces the toughest gap as China’s new AI institutes and India’s expanded supercomputing mission chase the same talent, producing attrition rates above 25% at tier-2 labs. Enterprises invest in internal academies IBM certified 1,200 developers in 2025 yet producing job-ready staff can take a year. Rapid hardware churn complicates the issue because code optimized for one GPU generation may underperform on the next, requiring continuous upskilling.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Accelerators Drive Next-Generation Workloads

The hardware segment accounted for 46.19% of revenue in 2025, cementing its role as the backbone of the high-performance data analytics market. Within hardware, accelerators are expanding at a 21.97% CAGR because GPUs, FPGAs, and ASICs execute matrix operations far faster than CPUs. Nvidia Blackwell B200 GPUs deliver 20 petaflops of FP4 inference while consuming less power than earlier A100 units, enabling real-time language-model serving. AMD MI300X provides 192 GB of HBM3 memory, addressing bandwidth limits that previously constrained large-model training. High-speed NVMe-over-Fabrics storage trims I/O bottlenecks, pushing sustained throughput to petabyte-scale levels.

Software components flourish in parallel as vendors bundle Kubernetes-based orchestration that hides cluster complexity, lifting average utilization from 40% to above 70%. Services revenue rises because firms lacking HPC skills outsource tuning and monitoring. Together, this ecosystem positions accelerators as the pivotal growth lever, and their proliferation underpins future expansion of the high-performance data analytics market size at both cloud and on-premises sites.

By Deployment Model: Cloud and Hybrid Architectures Dominate

Cloud and hybrid models held 71.84% of revenue in 2025, illustrating how consumption pricing and near-instant scalability align with data-intensive workloads. AWS Trainium2 instances, priced 40% below comparable H100 offerings, triggered wide adoption among start-ups fine-tuning language models. Google’s Cross-Cloud Interconnect launched in 2026, moving petabyte-scale data between on-premises clusters and Google Compute Engine with sub-10 millisecond latency.

Regulated sectors still run sensitive workloads in private data centers, but most now adopt hybrid frameworks that burst seasonal peaks to public cloud. Egress fees average USD 0.09 per GB, making it impractical to repatriate large datasets, which effectively anchors analytics pipelines to the originating provider. Sovereign-cloud zones AWS Local Zones in Saudi Arabia and Azure Stack Hub in India attempt to reconcile data-residency rules with hyperscale economics. These developments ensure cloud and hybrid deployments will continue to propel the high-performance data analytics market through the forecast horizon.

By Organization Size: SMEs Accelerate Adoption

Large enterprises commanded 62.36% of spending in 2025 because multi-year contracts and global support requirements favour hyperscaler volume pricing. Yet SMEs are the fastest-growing cohort at a 21.67% CAGR, aided by low-entry SaaS platforms such as Databricks Unity Catalog, which automates governance for lakehouse environments. Snowflake Cortex AI lets business analysts trigger sentiment analysis with a single SQL call, bypassing Python coding.

Government grants accelerate uptake: Singapore’s SME Go Digital scheme subsidizes cloud pilot projects, while India offers tax credits under Digital India. Financing programs like Dell APEX spread payments, letting firms treat infrastructure as an operating expense. As these mechanisms converge, SMEs enlarge their slice of the high-performance data analytics market share without shouldering deep in-house technical teams.

By End-User Industry: Retail Leads Growth

Banking, financial services, and insurance contributed 24.53% of revenue in 2025, anchored by fraud analytics and capital modelling, but growth is levelling as core systems mature. Retail and e-commerce, by contrast, is projected to grow at a 21.88% CAGR, driven by sub-100-millisecond personalization that upsells before shopper attention fades. Walmart’s Item 360 engine analysed 2.5 billion daily transactions in 2025 and reduced out-of-stock events by 22%.

Healthcare and life sciences show strong momentum because genomic pipelines push compute demand up 40% year on year. Government and defense, energy and utilities, and telecommunications collectively hold mid-single-digit shares but use cases grid optimization, 5G network slicing, quality control are widening. These vertical dynamics collectively sustain expansion of the high-performance data analytics market.

Geography Analysis

North America retained 41.29% of 2025 spending thanks to hyperscaler capital outlays above USD 200 billion and federal exascale programs such as the Frontier system that breached the one-exaflop barrier. Canada invested CAD 400 million (USD 295 million) in 2025 to lift national capacity to 100 petaflops by 2027. Mexico is emerging as a near-shoring data-center hub with combined hyperscaler investment of USD 3.2 billion in 2025.

Asia-Pacific is forecast for the fastest growth at a 22.07% CAGR, driven by China’s plan for 1,000 exaflops by 2030 and Japan’s quantum-classical hybrid roadmap. India expanded its National Supercomputing Mission to 18 centers in 2025 with INR 4,500 crore (USD 540 million) allocated for phase-three upgrades. Australia’s new Canberra supercomputer targets 50 petaflops for climate research. Data-sovereignty laws in China and India insist on local processing, steering investment toward in-country cloud zones.

Europe holds a mid-20% share, supported by the EuroHPC Joint Undertaking that funded pre-exascale systems across Spain, Italy, and Germany with budgets above EUR 8 billion (USD 9 billion). Germany’s JUPITER reached 500 petaflops in 2025, showcasing energy-efficient liquid cooling. The United Kingdom earmarked GBP 900 million (USD 1.15 billion) for an AI Research Resource, although talent outflow after Brexit slows progress. South America and the Middle East and Africa remain nascent but not idle; Saudi Arabia’s sovereign wealth fund opened a national HPC center in 2025.

Competitive Landscape

The market shows moderate concentration: the top five vendors Amazon Web Services, Microsoft, Google, Hewlett Packard Enterprise, and Nvidia captured about 55% of global revenue in 2025. Hyperscalers are integrating vertically by designing custom silicon such as AWS Trainium2, Google TPU v5, and Microsoft Maia to cut reliance on third-party chips. Traditional hardware firms pivot toward software-defined orchestration and managed services, bundling Kubernetes clusters with infrastructure sales to mask complexity.

Emerging players like Cerebras Systems use wafer-scale silicon to eliminate inter-node latency, and Graphcore targets sparse inference with intelligence processing units, yet both lack hyperscaler distribution reach.

Open-source frameworks Apache Spark, Dask, Ray commoditize middleware, pushing proprietary vendors to differentiate through security certifications and enterprise support. Mergers reshape the field: Broadcom acquired VMware in 2024 to tighten virtualization links, and AMD’s earlier purchase of Xilinx strengthens its FPGA stack. Overall rivalry centers on lowering cost-per-flop while embedding analytics directly into vertical SaaS platforms.

High-Performance Data Analytics Industry Leaders

SAS Institute, Inc.

Oracle Corporation

ATOS SE

Microsoft Corporation

NVIDIA Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: NVIDIA unveiled Blackwell Ultra architecture with the NVL576 rack that houses 576 Rubin Ultra GPUs, enabling exascale-class AI computing while cutting energy draw via co-packaged optics.

- May 2025: One Stop Systems signed a Cooperative Research and Development Agreement with USSOCOM to co-develop rugged edge HPC units for field AI workloads.

- May 2025: Seer released Proteograph ONE plus SP200 automation, raising weekly proteomics throughput above 1,000 samples.

- April 2025: Google Cloud debuted autonomous data-foundation services and workflow agents that lift campaign productivity for partners such as Radisson Hotel Group by 50%.

- March 2025: IonOpticks appointed new global sales leaders to prepare for expanded proteomics and clinical launches.

Global High-Performance Data Analytics Market Report Scope

The High-Performance Data Analytics Market Report is Segmented by Component (Hardware, Software, Services), Deployment Model (On-Premise, Cloud and Hybrid), Organization Size (Small and Medium Enterprises, Large Enterprises), End-User Industry (Banking Financial Services and Insurance, Government and Defense, Energy and Utilities, Retail and E-Commerce, Healthcare and Life Sciences, Telecommunication and IT Services, Manufacturing), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware | Servers |

| Accelerators (GPU, FPGA, ASIC) | |

| High-Speed Storage | |

| Interconnect And Networking | |

| Software | Distributed File Systems And Databases |

| Analytics Frameworks And Libraries | |

| Orchestration And Cluster Management | |

| Services | Professional Services |

| Managed Services |

| On-Premise |

| Cloud And Hybrid |

| Small and Medium Enterprises |

| Large Enterprises |

| Banking, Financial Services and Insurance |

| Government and Defense |

| Energy and Utilities |

| Retail and E-Commerce |

| Healthcare and Life Sciences |

| Telecommunication and IT Services |

| Manufacturing |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Component | Hardware | Servers |

| Accelerators (GPU, FPGA, ASIC) | ||

| High-Speed Storage | ||

| Interconnect And Networking | ||

| Software | Distributed File Systems And Databases | |

| Analytics Frameworks And Libraries | ||

| Orchestration And Cluster Management | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Model | On-Premise | |

| Cloud And Hybrid | ||

| By Organization Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By End-User Industry | Banking, Financial Services and Insurance | |

| Government and Defense | ||

| Energy and Utilities | ||

| Retail and E-Commerce | ||

| Healthcare and Life Sciences | ||

| Telecommunication and IT Services | ||

| Manufacturing | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is spending on high-performance data analytics expected to grow?

Between 2026 and 2031 spending is projected to rise at a 21.14% CAGR, taking the market from USD 152.60 billion in 2026 to USD 398.17 billion by 2031.

Which deployment model drives the largest share of current revenue?

Cloud and hybrid deployments generated 71.84% of global revenue in 2025, reflecting broad preference for consumption pricing and elastic capacity.

Why are accelerators so important for analytics workloads?

GPUs, FPGAs, and ASICs execute tensor and matrix operations far faster than CPUs, enabling real-time AI inference and cutting model-training time, which propels their 21.97% CAGR.

Which region is set to post the highest growth through 2031?

Asia-Pacific is forecast to grow at a 22.07% CAGR because sovereign-AI mandates in China, Japan, and India continue to add petascale capacity.

What limits on-premise adoption for mid-tier enterprises?

High total cost of ownership, including USD 15,000 per GPU node plus steep power and cooling bills, makes dedicated clusters hard to justify for intermittent workloads.

How severe is the talent shortage in parallel programming?

In 2025, 68% of HPC centers reported unfilled CUDA or MPI roles, and global demand outpaced university supply by roughly ninefold, extending hiring cycles to nine months.

Page last updated on: