Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 38.79 Billion |

| Market Size (2031) | USD 63.22 Billion |

| Growth Rate (2026 - 2031) | 10.25% CAGR |

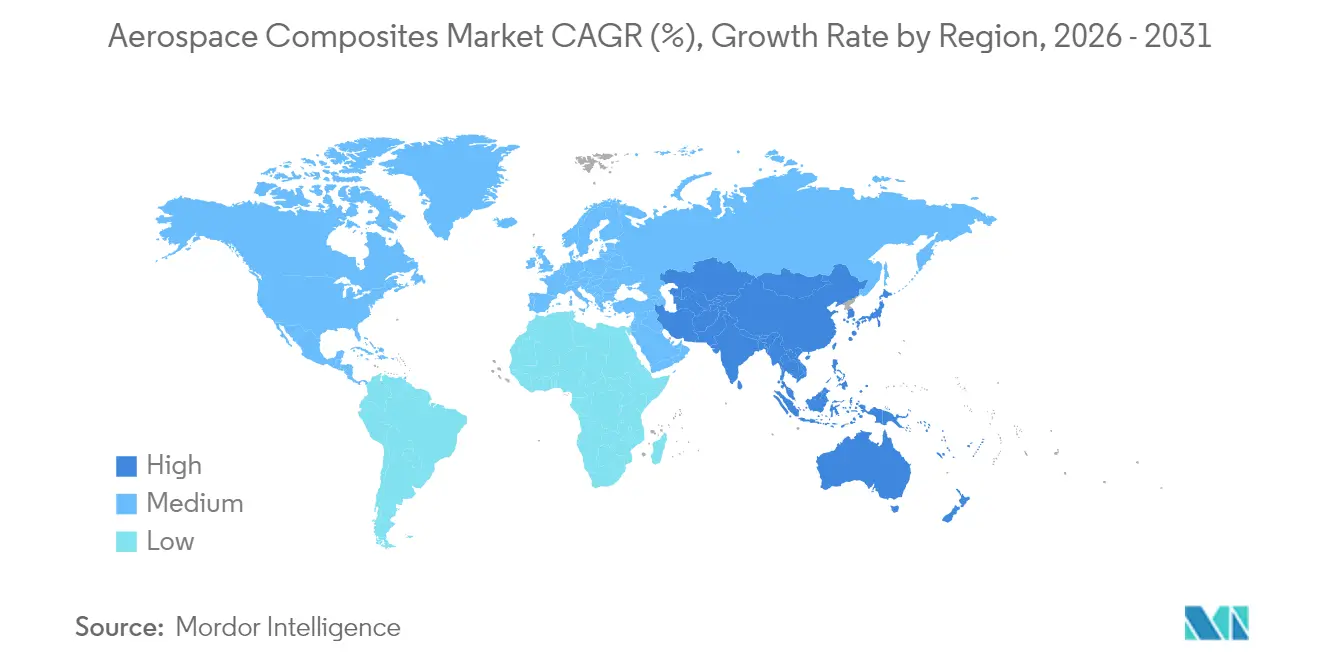

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

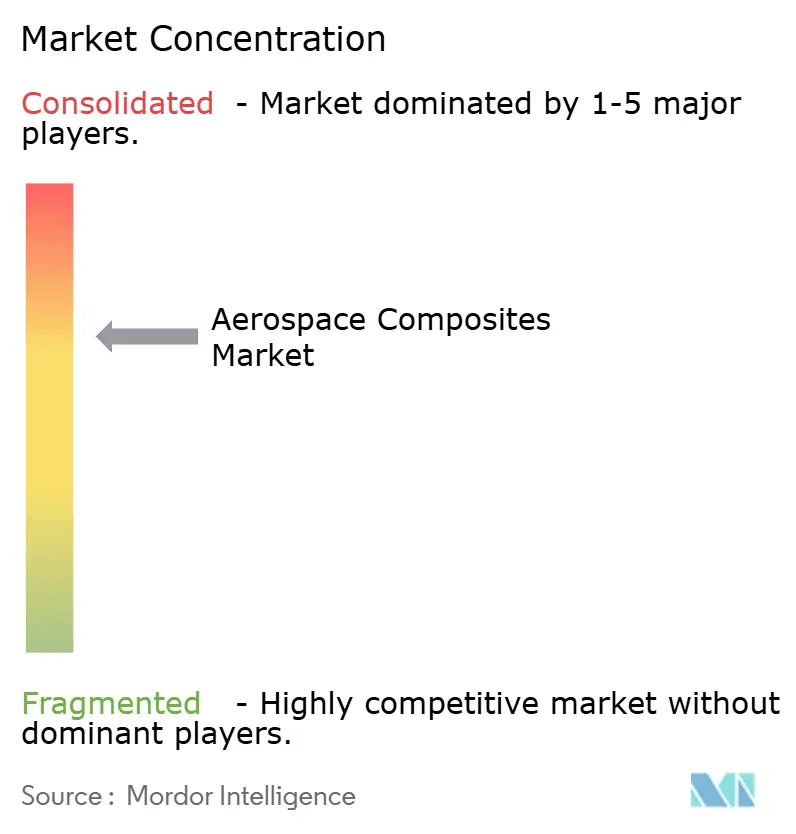

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerospace Composites Market Analysis by Mordor Intelligence

The aerospace composites market size is expected to grow from USD 35.18 billion in 2025 to USD 38.79 billion in 2026 and is forecast to reach USD 63.22 billion by 2031 at 10.25% CAGR over 2026-2031. Strong demand for lightweight structures that enhance fuel efficiency, expanding hypersonic programs, and the growing need for recyclable materials are the central forces shaping the market. Automated fiber placement (AFP) systems delivering 4–8 times higher throughput than legacy lay-up lines, the rapid uptake of thermoplastics in single-aisle backlogs, and fleet electrification requirements for high-temperature parts are among the most influential growth drivers. Major aircraft OEMs vertically integrate composite production to control quality and cost, intensifying supplier competition and accelerating qualification cycles for novel resins. Asia’s expanding manufacturing base and rising investments in electric propulsion are turning the region into the fastest-growing hub in the market.

Key Report Takeaways

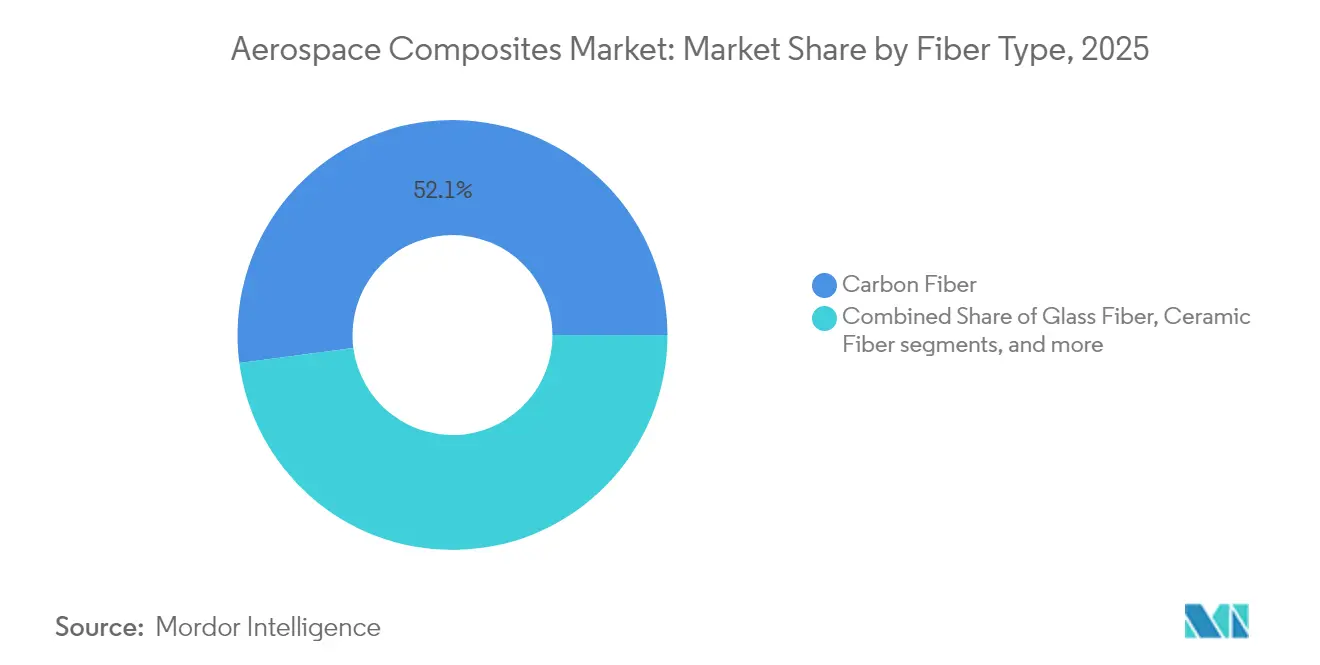

- By fiber type, carbon fiber held 52.08% of the aerospace composites market share in 2025, while ceramic fiber is forecast to expand at a 10.74% CAGR through 2031.

- By resin type, thermosets led with 45.73% revenue share in 2025, but thermoplastics are advancing at a 13.22% CAGR to 2031.

- By manufacturing process, prepreg lay-up accounted for a 44.25% share in 2025; AFP registered the fastest growth at a 12.76% CAGR.

- By aircraft type, commercial narrow-body aircraft captured 38.02% of the market size in 2025, whereas spacecraft/launch vehicles are expected to grow at a 14.41% CAGR.

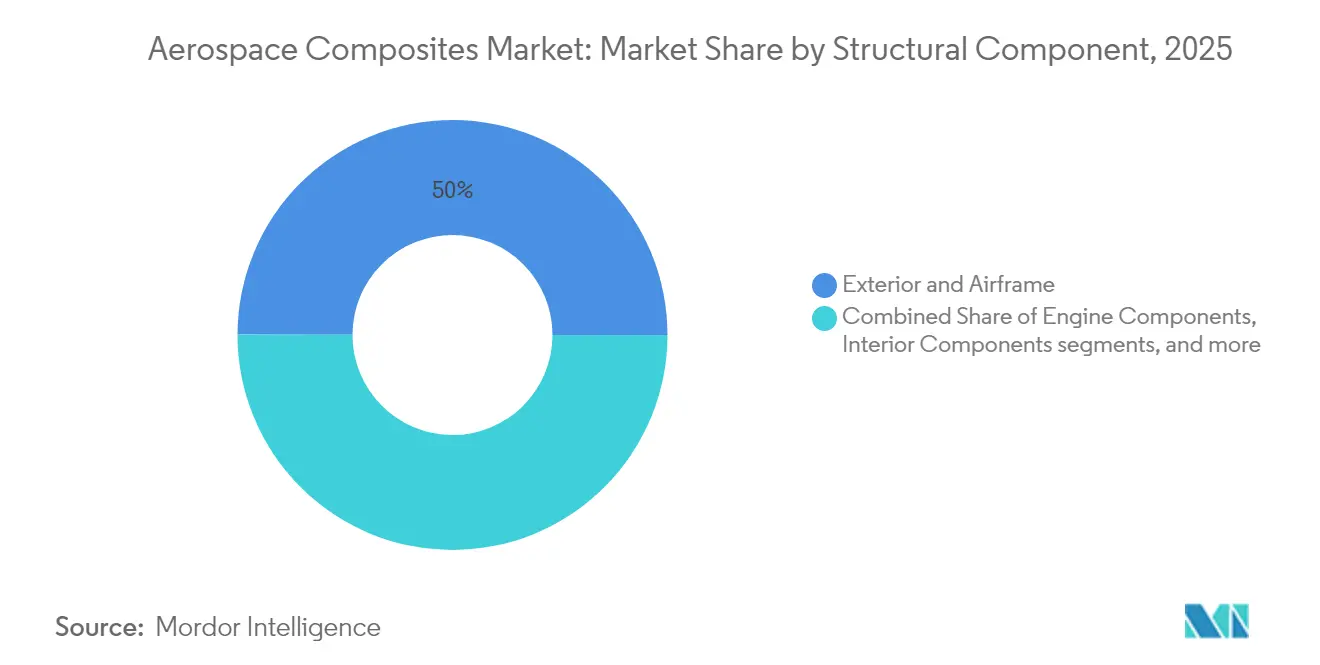

- By structural component, exterior and airframe parts represented a 49.96% share of the market in 2025; engine parts are growing the quickest at a 17.12% CAGR.

- By end-user, OEMs dominated with an 79.88% share in 2025, while the aftermarket/MRO segment is projected to rise at 8.74% CAGR.

- By region, North America held 29.71% of global revenue in 2025; the Asia-Pacific region is poised for a 10.30% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aerospace Composites Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of thermoplastic composites to accelerte production rates of single-aisle programs (Europe-led) | +2.5% | Europe-led global | Medium term (2-4 years) |

| Increasing penetration of carbon fiber in next-gen narrow-body wings in North America | +1.8% | North America, Europe | Medium term (2-4 years) |

| Fleet eletrification and more-electric aircraft (MEA) driving high-temperature composite demand in Asia | +1.2% | Asia, global | Medium term (2-4 years) |

| Space-launch commercialization boosing demand for lightweight composite structures | +2.0% | US, China, global | Short term (≤2 years) |

| Military stealth programs propelling ceramic-matrix composite uptake in hypersonic applications | +1.5% | US, China, Russia | Medium term (2-4 years) |

| OEM sustainability targets pushing recyclable composite solutions | +1.0% | Europe-led global | Long term (≥5 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Thermoplastic Composites

Collins Aerospace demonstrates that thermoplastic aerostructures cut production cycles by 80%, eliminate autoclave curing, and are nearly 100% recyclable.[1]Collins Aerospace, “Thermoplastic Composites for High-Rate Aircraft Production,” collinsaerospace.comEuropean single-aisle programs have embraced the material to reduce delivery backlogs. At the same time, an Arkema-Hexcel partnership produced the first fully thermoplastic commercial aircraft structure, validating large-scale out-of-autoclave fabrication. High recyclability aligns with emerging sustainability mandates, positioning thermoplastics as a cornerstone of future market expansion.

Increasing Penetration of Carbon Fiber in Next-Gen Narrow-Body Wings

Airbus’s eXtra Performance Wing testbed incorporates extensive CFRP skins to lower drag and cut CO₂, showcasing the build feasibility of 32 m-long carbon-fiber wingskins.[2]Airbus, “Extra Performance Wing and Bio-Fiber Panels Advance Sustainable Aviation,” airbus.com North American programs perform parallel studies, aiming to match or exceed European CFRP usage. Weight savings of up to 50% versus aluminum and AFP throughput gains directly address the backlog challenge.

Fleet Electrification and More-Electric Aircraft

Electric propulsion subsystems require composite housings that endure 450°F operating environments; Hexcel’s high-temperature Flex-Core HRH-302 honeycomb meets this need. Asian manufacturers leverage electronics experience to integrate thermal management layers into composite skins, driving regional demand. The evolution of battery and fuel-cell architectures is expected to stimulate orders for hybrid polymer-ceramic laminates across the market.

Space Launch Commercialization

Reusable launchers depend on lightweight fairings; Chinese supplier Monks Aviation delivered composite fairings 30% lighter than metal designs for the Ceres-1 program. Parallel European initiatives are developing all-composite LH₂ tanks to TRL 5, underscoring strong market pull from private launch ventures. The spacecraft segment’s 14.90% CAGR positions it as the most dynamic pocket of the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High preform and autoclave capital costs limiting adoption in tier-2 suppliers | -1.8% | Global, emerging markets | Short term (≤2 years) |

| Supply-chain volatility for aerospace-grade precursors for PAN-based carbon fiber | -2.0% | Global | Short term (≤2 years) |

| Qualification and certification delays for novel resin systems with FAA/EASA | -1.5% | Regulated markets | Medium term (2-4 years) |

| Limited repairability expertise for advanced thermoplastics in MRO sector | -0.8% | Global | Long term (≥5 years) |

| Source: Mordor Intelligence | |||

High Preform and Autoclave Capital Costs

Aerospace-grade autoclaves cost USD 5–10 million and require extensive infrastructure, deterring Tier-2 entrants. Out-of-autoclave thermoplastic welding and resin infusion are emerging as lower-investment alternatives that can broaden supplier participation across the aerospace composites market.

Supply-Chain Volatility of Aerospace-Grade Precursors

Major OEMs formed the Aviation Supply Chain Integrity Coalition to harden vendor accreditation and part traceability after recurring precursor shortages disrupted deliveries. Efforts include stricter non-conformance audits and digital tracking, but raw-material lead times remain an ongoing risk within the aerospace composites market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fiber Type: Ceramic Fibers Expand Heat-Resistant Envelope

Carbon fiber retained 52.08% of the aerospace composites market share in 2025, thanks to mature supply chains and superior stiffness-to-weight ratios. Ceramic fibers, however, are pacing the segment with a 10.74% CAGR, propelled by hypersonic and space vehicle demand for 1,500 °C capability. Hybrid laminates combining carbon and ceramic plies are gaining favor among engine OEMs aiming to cut cooling air draw by 25%. Graphene-enhanced rovings under evaluation show 20–30% modulus boosts while embedding strain-sensing pathways, a step toward self-monitoring wingskins.

The cost-effective positioning of glass fiber maintains relevance in radome and fairing skins, while aramid fibers sustain a share in ballistic-resistant helicopter floors. Continued material innovation supports diversification, yet carbon and ceramic remain the backbone of the market size throughout the forecast horizon.

By Resin Type: Thermoplastics Challenge Thermoset Dominance

Thermoset epoxy and BMI systems commanded 45.73% of 2025 revenue because of an extensive qualification pedigree. Thermoplastic PEKK and PEI families are surging at a 13.22% CAGR, driven by 80% cycle-time reductions cited by Collins Aerospace. The aerospace composites market size for thermoplastics is projected to exceed USD 19.38 billion by 2031 as AFP lines pivot to in-situ consolidation. Bio-based resins pioneered by SHD Composites offer near-100% renewable content and withstand 200 °C service, aligning environmental targets with mechanical integrity.

Qualification momentum is accelerating: the FAA has already cleared welded thermoplastic control surfaces for business jets, signaling an imminent broadening of use cases across the industry.

By Manufacturing Process: AFP Transforms High-Rate Production

Prepreg lay-up delivered 44.25% of the 2025 value, yet AFP and automated tape laying are expanding at 12.76% CAGR as Electroimpact’s AFP 4.0 attains 99% quality compliance while quadrupling throughput on identical capital. The market size linked to AFP equipment installations is expected to outpace all other processes through 2031. RTM adoption is climbing for complex engine nacelles; additive composite printing remains nascent but offers topology-optimized brackets that cut buy-to-fly ratios by 80%. Under FAA assessment, the resin infusion for transport fuselages promises to shave operating costs in thin-walled shells, widening market accessibility.

By Aircraft Type: Spacecraft Lead Growth amid Commercial Recovery

As Airbus and Boeing cleared pandemic order backlogs, commercial narrow-bodies contributed the largest slice, 38.02% in 2025. The spacecraft and launc h-vehicle category will grow at a 14.41% CAGR, reflecting private-launch proliferation and satellite constellation demand. Military fleets remain a resilient buffer, with stealth fighters integrating radar-absorbing CFRP skins. Business jets and rotorcraft incrementally raise composite content for range and payload gains. Emerging eVTOL craft call for high-rate thermoplastic fuselages, adding a fresh volume stream to the aerospace composites market.

By Structural Component: Engines Drive Advanced-Material Uptake

Exterior skins and primary airframe members occupied 49.96% of 2025 revenue, yet engine components will climb fastest at 17.12% CAGR as CMC shrouds enable 200°F higher turbine entries. The aerospace composites market size attached to engines could nearly triple by 2031 as geared turbofan and open-rotor concepts seek mass and thermal advantages. Multifunctional laminates combining energy storage layers with load paths are under lab trials, pointing to future integration leaps.

By End-User: MRO Opportunities Rise in Composite Fleet

OEMs controlled 79.88% of 2025 spend, but MRO is accelerating at 8.74% CAGR. Collins Aerospace operates eight global autoclave sites to service growing shop visits for composite airframes. GE Aerospace’s USD 1 billion injection into its repair network targets engine composite fan-case throughput to contain airline downtime. As the installed base ages, demand for bonded-patch and scarf-repair expertise will enlarge the aerospace composites market.

Geography Analysis

North America remains the largest regional contributor with a market share of 29.71%, anchored by The Boeing Company, GE Aerospace, and Lockheed Martin Corporation. The region accounts for roughly 75% of North American sales, with Canada’s Montréal cluster supplying high-end nacelles. NASA’s HiCAM program underpins thermoplastic welding certification, reinforcing domestic supply chains.

Europe follows, propelled by Airbus and a robust tier network in Germany, France, and the United Kingdom. Aggressive sustainability mandates, such as the EU’s Fit for 55 package, are catalyzing the adoption of bio-based composites. Thermoplastic wineskins under production in Wales exemplify Europe’s commitment to high-rate, low-carbon manufacturing.

Asia-Pacific is the fastest-growing territory with a CAGR of 10.30%, driven by China’s COMAC fleet ramp-up and electric-propulsion R&D hubs in Japan and South Korea. HRC’s new Chinese plant supplies AFP stringers for aerospace and high-speed rail, underscoring manufacturing scale advantages. India is nurturing a composites corridor around Bengaluru, supplying ISRO launch vehicles and HAL fighters, further enlarging regional aerospace composites market activity.

Latin America, led by Brazil’s Embraer, integrates composites in E2 jet families, while Mexico’s Querétaro cluster fabricates nacelle doors for North American primes. In the Middle East and Africa, the United Arab Emirates’ Strata composites facility and South Africa’s Denel Aerostructures are emerging contributors, aided by offset agreements and skills transfer.

Competitive Landscape

The aerospace composites market shows moderate concentration. Toray dominates intermediate-modulus carbon fiber supply, while Hexcel and Solvay leverage integrated prepreg and honeycomb offerings. Hexcel’s 2024 sales of USD 1.903 billion marked an 11.8% rise in commercial aerospace revenue.

OEM vertical integration is intensifying. Airbus is co-developing thermoplastic ribs with Stelia, and Boeing’s Charleston out-of-autoclave center fabricates B787 skin panels in-house. To maintain share, material firms are forming alliances—Arkema-Hexcel for PEKK tapes and Solvay-Safran for resin transfer-molded fan blades.

Strategic mergers and acquisitions are accelerating. Kineco’s full acquisition of Kineco Kaman Composites India boosts its defense footprint, while Daikin’s stake in Advanced Composite Corporation enhances resin chemistries for thermoplastic fuselages. Investment in AFP, CMC capacity, and recycling plants remains a priority as companies target differentiated positions within the aerospace composites industry.

Aerospace Composites Industry Leaders

Hexcel Corporation

Solvay

SGL Carbon

Mitsubishi Chemical Carbon Fiber and Composites, Inc. (Mitsubishi Chemical Group Corporation)

Toray Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Airbus flight-tested a bio-fiber nose panel on the H145 PioneerLab, confirming performance parity with conventional carbon fiber.

- April 2024: MIT researchers unveiled “nanostitching” using carbon nanotubes to boost interlaminar toughness by 62%.

- March 2024: Arkema-Hexcel produced the first fully thermoplastic aircraft structure consolidated out-of-autoclave.

- February 2024: Mitsubishi Chemical Group introduced a 1,500 °C-capable ceramic matrix composite for space launch customers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the aerospace composites market as the annual value of newly manufactured structural and interior components made from carbon, glass, ceramic, or hybrid fibers that are combined with polymer, metal, or ceramic matrices and installed on civil or military fixed-wing aircraft, rotorcraft, and space launch vehicles. We include prepreg, filament-wound, lay-up, resin-infused, and automated fiber-placed parts that leave tier-1 suppliers' facilities and enter the aerospace supply chain; repair kits and scrap are excluded. According to Mordor Intelligence, this scope places 2025 demand at USD 35.18 billion.

(Scope exclusion) Items produced for automotive, marine, or wind applications, even if made from identical materials, sit outside our coverage.

Segmentation Overview

- By Fiber Type

- Glass Fiber

- Carbon Fiber

- Ceramic Fiber

- Aramid Fiber

- Other Fiber Types

- By Resin Type

- Thermoset Composites

- Thermoplastic Composites

- By Manufacturing Process

- Lay-Up (Hand and Automated)

- Resin Transfer Molding (RTM)

- Filament Winding

- Injection/Compression Molding

- Automated Fiber Placement and Tape Laying

- Additive Manufacturing of Composites

- By Aircraft Type

- Commercial Aircraft

- Narrow-Body

- Wide-Body

- Regional Jets

- Freighters

- Business Jets

- Military Aircraft

- Fighter Jets

- Transport and Tanker

- Rotorcraft

- Helicopters

- Spacecraft and Launch Vehicles

- Commercial Aircraft

- By Structural Component

- Interior Components

- Exterior and Airframe

- Engine Components

- Auxiliary Structures

- By End-User

- OEM

- Aftermarket/MRO

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed air-framer engineers, material formulators, MRO managers, and civil-aviation regulators across North America, Europe, and Asia-Pacific. These conversations tested weight-per-aircraft assumptions, adoption curves for thermoplastic wings, and price-move expectations, letting us close gaps left by desk research and cross-check early model outputs.

Desk Research

We began by mapping the fleet backlog, recent aircraft delivery data, and spacecraft launch manifests from sources such as the International Air Transport Association, Airbus and Boeing orders and deliveries files, NASA and ESA launch logs, and defense budget papers. Trade statistics from UN Comtrade, carbon-fiber export reports curated through Volza, and production indices from the U.S. Bureau of Labor Statistics helped us size material flows. Our team also mined peer-reviewed journals that track resin uptake rates and weight-saving benchmarks, while D&B Hoovers fed company-level financials to ground pricing bands. Additional inputs came from investor transcripts, patent families retrieved via Questel that hint at processing shifts, and Aviation Week program databases that flag composite-rich variants entering service. This list is indicative; many other public and paid sources supported validation.

Market-Sizing & Forecasting

We applied a top-down build that reconstructs composite content from production and trade data, then confirms totals with sampled average selling price multiplied by volume roll-ups at key suppliers. Variables such as annual narrow-body deliveries, average composite shipset weight, carbon-fiber price indices, defense aircraft procurement outlays, and reusable launch demand inform the model. Multivariate regression with scenario analysis projects 2026-2030 values; primary research consensus guides variable trend lines. Bottom-up estimates are used where supplier data are strong, and any gap is proportionally distributed before final sign-off.

Data Validation & Update Cycle

Outputs pass anomaly checks against historical ratios, external benchmarks, and margin profiles. Senior reviewers re-run variance scans, and we refresh numbers each year, with interim updates when program cancellations, supply shocks, or currency swings exceed preset thresholds.

Why Mordor's Aerospace Composites Baseline Earns Trust

Published estimates differ because firms choose distinct material mixes, inflation adjustments, and fleet outlooks.

Our disciplined scope, yearly refresh, and dual-track validation keep users anchored to the most current, explained baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 35.18 B | Mordor Intelligence | - |

| USD 30.30 B | Global Consultancy A | Excludes spacecraft parts and applies constant 2024 prices without exchange-rate updates |

| USD 36.40 B | Trade Journal B | Uses aggressive aircraft build forecast and omits aftermarket weight attrition factors |

The comparison shows how divergent inputs tilt results; our approach balances realistic build rates, updated pricing, and full aerospace scope, giving decision-makers a dependable, transparent starting point.

Key Questions Answered in the Report

What is the projected size of the aerospace composites market by 2031?

The aerospace composites market is forecast to reach USD 63.22 billion by 2031, growing at a 10.25% CAGR.

Which composite material is growing the fastest in aerospace applications?

Thermoplastic composites are expanding at a 13.22% CAGR due to 80% cycle-time reductions and near-100% recyclability.

Why are ceramic matrix composites important for future engines?

CMCs withstand temperatures above 1,200°C, enabling hotter, more efficient turbines that cut fuel burn and emissions.

Which aircraft segment offers the highest growth for composites?

Spacecraft and launch vehicles lead with a 14.41% CAGR as reusable rockets and satellite constellations drive lightweight-structure demand.

How are OEM sustainability goals influencing material choices?

Targets to reduce life-cycle emissions are accelerating adoption of bio-derived fibers, recyclable thermoplastics and closed-loop carbon-fiber recycling.

What role does AFP technology play in meeting production backlogs?

Automated fiber placement boosts throughput by up to 8-times and reduces labor, enabling OEMs to clear single-aisle order backlogs efficiently.

Page last updated on: