Aeroengine Composites Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

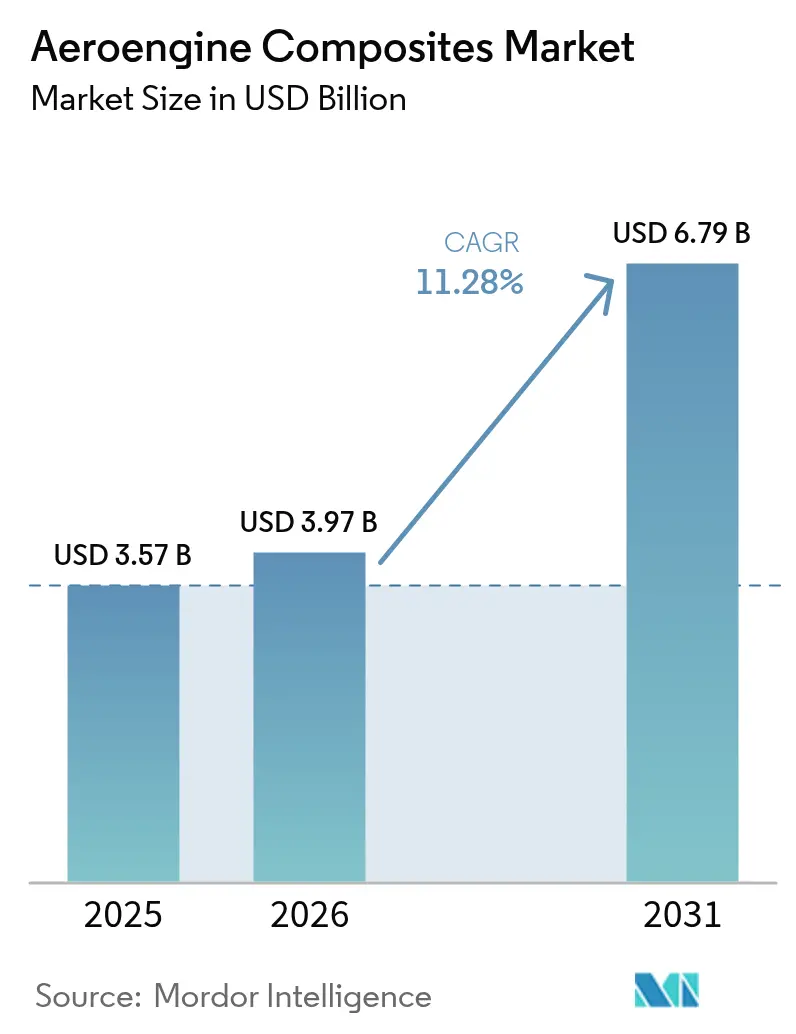

| Market Size (2026) | USD 3.97 Billion |

| Market Size (2031) | USD 6.79 Billion |

| Growth Rate (2026 - 2031) | 11.28% CAGR |

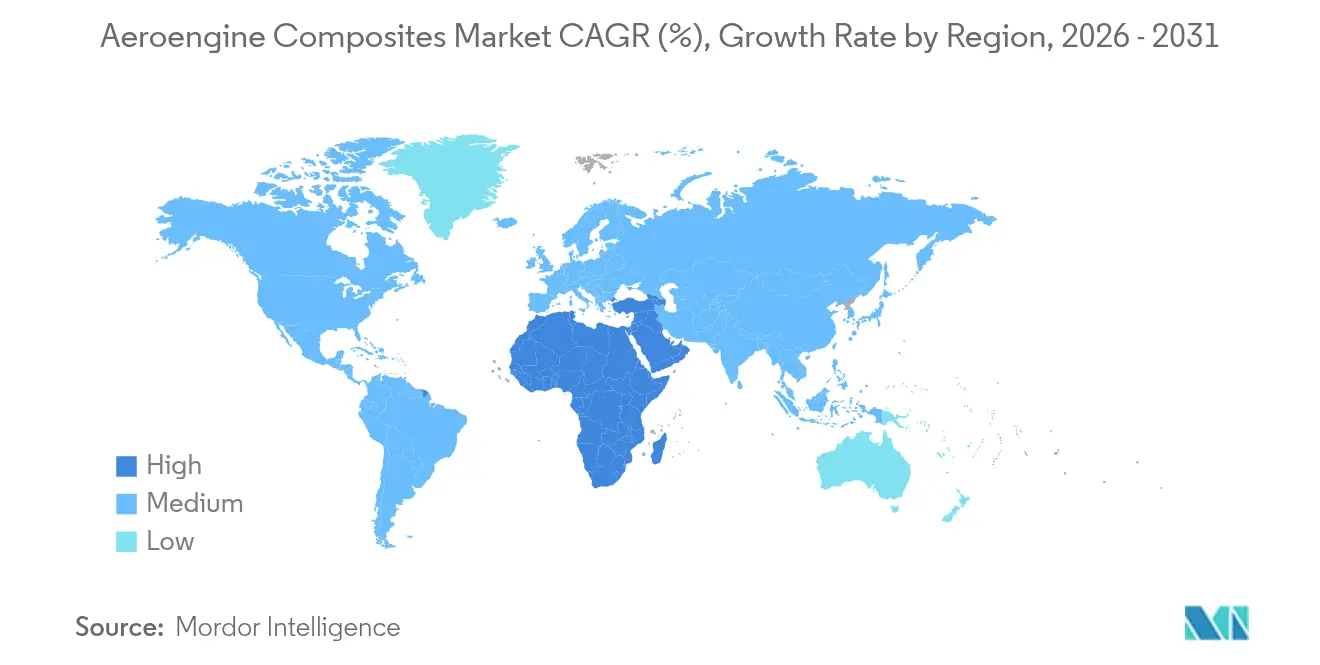

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aeroengine Composites Market Analysis by Mordor Intelligence

Aeroengine composites market size in 2026 is estimated at USD 3.97 billion, growing from 2025 value of USD 3.57 billion with 2031 projections showing USD 6.79 billion, growing at 11.28% CAGR over 2026-2031. Growing fleet renewal, decarbonization mandates, and rising fuel prices push airlines and engine makers toward lighter propulsion systems that cut fuel burn by up to 20% while meeting stricter emission limits. Ceramic matrix composites (CMC) now withstand 1,300°C, allowing higher core temperatures and improved thermal efficiency. Automated fiber-placement and out-of-autoclave curing are lowering the cost per pound by nearly 30%, making composites economically viable for narrowbody programs. Supply-chain resilience remains critical after GE Aerospace’s 10% delivery shortfall in 2024 exposed bottlenecks in high-pressure turbine blade sourcing.

Key Report Takeaways

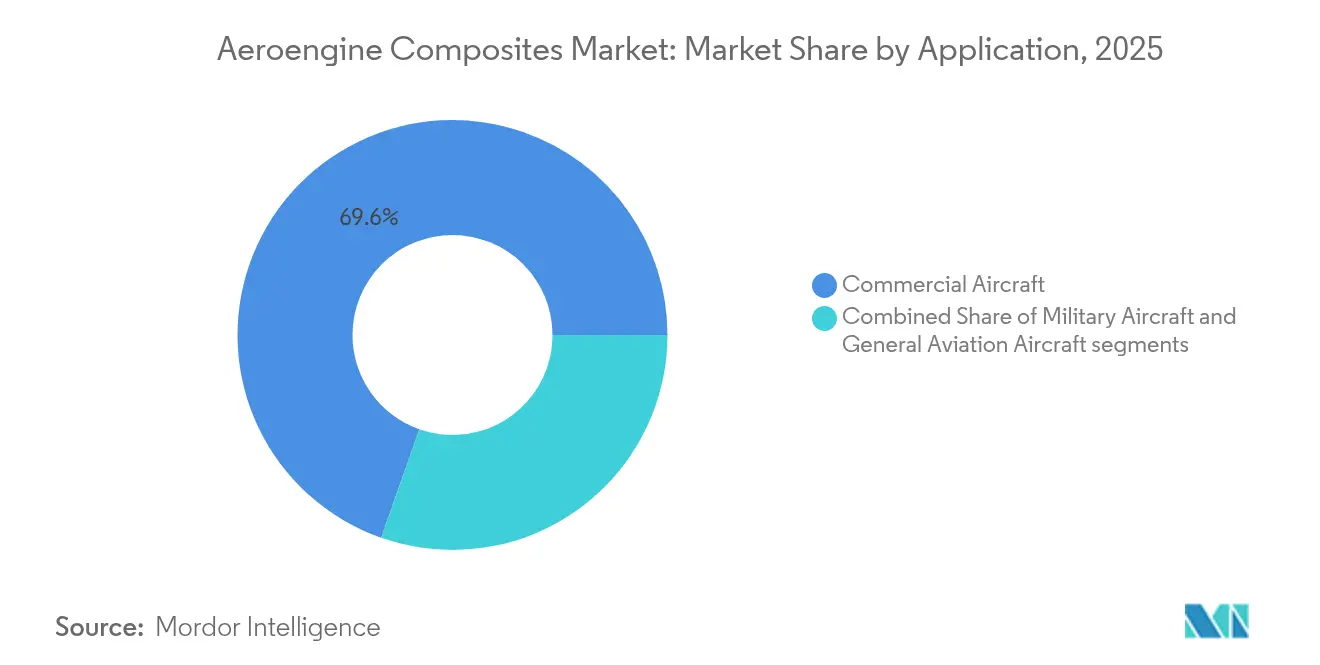

- By application, commercial aviation held 69.62% of the aeroengine composites market share in 2025, while the military segment is expected to grow the fastest at a 12.55% CAGR to 2031.

- By component, fan blades accounted for 37.42% of the aeroengine composites market size in 2025; fan cases are projected to expand at a 13.21% CAGR through 2031.

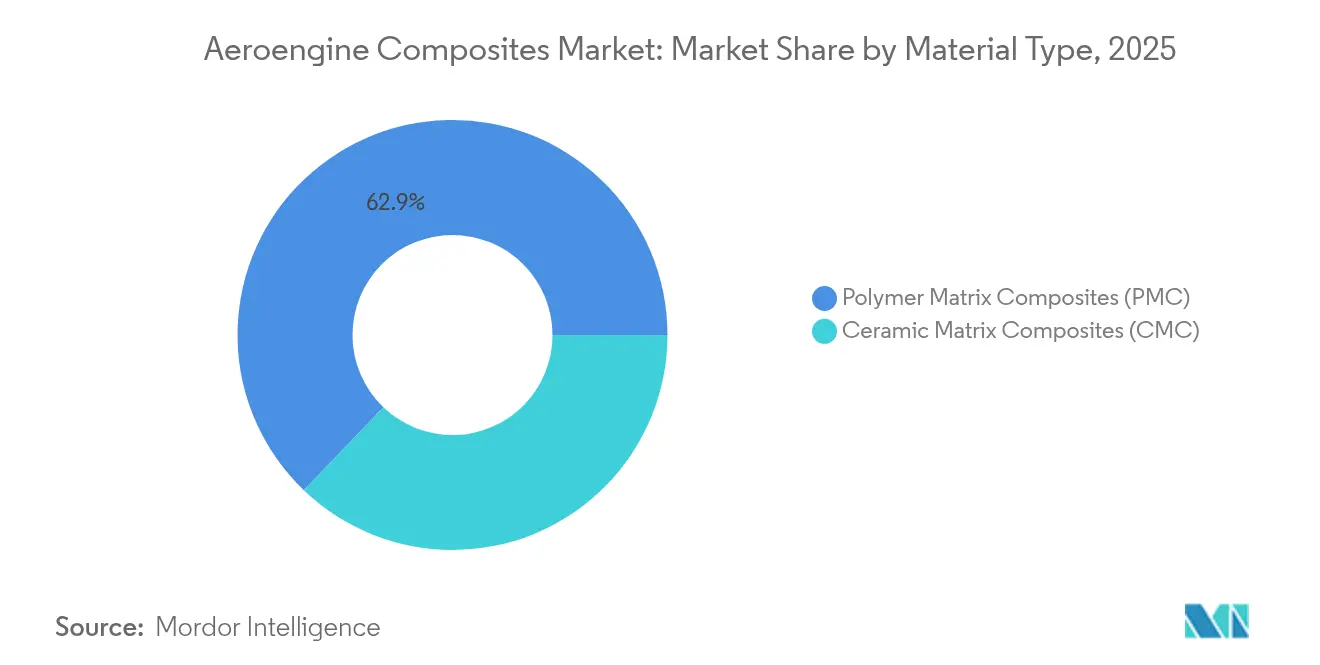

- By material, polymer matrix composites retained 62.85% share in 2025, whereas ceramic matrix composites are set to record a 14.72% CAGR to 2031.

- By end-user, OEMs dominated with 86.05% revenue share in 2025; the aftermarket is forecast to rise at an 11.63% CAGR through 2031.

- By geography, Asia-Pacific led with a 31.92% share in 2025, while the Middle East and Africa region is anticipated to grow at a 12.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aeroengine Composites Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward lightweight, fuel-efficient propulsion systems | +2.8% | Global | Medium term (2-4 years) |

| Ramp-up of LEAP and GEnx engine production volumes | +3.2% | North America and Europe | Short term (≤2 years) |

| Decarbonization roadmaps driving high-temperature CMC demand | +2.1% | EU and North America | Long term (≥4 years) |

| Shifting aftermarket spend toward composite replacement parts | +1.4% | Asia-Pacific | Medium term (2-4 years) |

| Cost reductions from automated manufacturing processes | +1.7% | North America and Europe | Short term (≤2 years) |

| Increasing funding for hypersonic and 6th-gen fighter manufacturing | +0.9% | North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Shift toward lightweight, fuel-efficient propulsion systems

Airlines need 15-20% fuel savings to offset volatile fuel prices, driving a rapid pivot toward composites that cut nacelle weight and boost bypass ratios. GE Aerospace’s RISE open-fan demonstrator targets 20% CO₂ reductions using carbon-fiber fan blades with bypass ratios up to 60.[1]GE Aerospace, “RISE Program Fact Sheet,” geaerospace.com Airbus is flight-testing carbon-fiber reinforced thermoplastic structures that pair with 100% sustainable aviation fuel and promise 20% fuel burn cuts. Narrowbody output above 100 aircraft per month heightens the urgency for scalable, automated composite production.

Ramp-up of LEAP and next generation aircraft engine production volumes

Over 4,000 aircraft fly with LEAP engines, prompting Safran to invest EUR 1 billion (USD 1.16 billion) in new MRO facilities in Brussels, Hyderabad, Querétaro, and Casablanca to handle 1,200 annual shop visits by 2028.[2]Safran Aircraft Engines, “Safran Invests in Global LEAP MRO Network,” safran-aircraft-engines.com GE earmarked EUR 64 million (USD 74.05 million) for European test cells and tooling that support the LEAP and GE9X programs. Component shortages, chiefly high-pressure turbine blades, trimmed 2024 engine deliveries by 10% despite USD 26.9 billion in commercial revenue, underscoring the need for diversified composite supply chains.

Decarbonization roadmaps driving high-temperature CMC demand

CMCs enable turbine inlet temperatures 500°F hotter than metal parts, raising thermal efficiency. Using rotating CMC components, GE’s XA100 adaptive-cycle engine shows 25% fuel savings and 30% range gains. More than 100,000 GE CMC shrouds have logged 10 million flight hours, demonstrating durability at scale. Mitsubishi Chemical’s 1,500°C carbon-fiber-based CMC for space applications illustrates widening performance envelopes in pursuit of net-zero flight.

Shifting aftermarket spend toward composite replacement parts

Airlines are shifting from price-focused spares to total-cost-of-ownership strategies that leverage composites’ longer on-wing life. Safran’s purchase of Component Repair Technologies positions it to capture demand for composite part refurbishment as LEAP shop visits accelerate. Asia-Pacific carriers with high utilization hours are early adopters of composite repairs that slice fuel burn and extend maintenance intervals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Brittleness and inspection complexity of CMCs | −1.8% | North America and Europe | Medium term (2-4 years) |

| Limited high-temperature resin supply base | −1.2% | North America and Europe | Short term (≤2 years) |

| Volatile build-rates deferring CAPEX on new lines | −1.6% | North America | Short term (≤2 years) |

| Protracted qualification cycles under FAA/EASA Part 21 rules | −2.1% | US and Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Brittleness and inspection complexity of CMCs

CMC fan blades risk foreign object damage because their ceramic microstructure can crack under impact loads. Traditional ultrasonic or X-ray methods struggle to detect microcracks, forcing OEMs to invest in computed-tomography scanning and specialist training. New machining methods using polycrystalline diamond tools cut processing time by 70%, raising capital costs and making adoption harder for smaller suppliers.

Protracted qualification cycles under FAA/EASA Part 21 rules

Novel materials can take 5-7 years to qualify. Each resin tweak requires retesting for fatigue, thermal cycling, and environmental durability, stalling the entry of promising CMC grades. Digital twin certification is being explored, but regulators have yet to accept simulation-only evidence, so engine makers stick with proven composites to avoid delays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Commercial Aviation Drives Volume Growth

Commercial engines captured 69.62% of the aeroengine composites market share in 2025 because thousands of LEAP and GEnx units integrate composite fan blades and cases that deliver up to 20% fuel savings. The aeroengine composites market size tied to military programs will expand the fastest at a 12.55% CAGR through 2031 as XA100-class propulsion and hypersonic demonstrators adopt CMC shrouds.

Business jets and regional aircraft operators are beginning to retrofit composite-rich engines as technology migrates downstream. Partnerships like GE Aerospace and Kratos Defense plan small-class engines that marry CMC turbines with affordable production methods, widening the customer base. This diffuses risk across civil and defense budgets, improving supplier order stability.

By Component: Fan Blades Lead, Fan Cases Accelerate

Fan blades retained 37.42% of 2025 revenue because carbon-fiber construction delivers high stiffness-to-weight and reduces inertia for better thrust response. Fan cases are projected to grow at 13.21% CAGR, lifting the aeroengine composites market size for containment hardware as regulatory containment tests favor composite shells.

Integrating shrouds, guide vanes, and O-ring seals into monolithic composite structures will keep margins healthy by reducing part count and assembly hours. Suppliers with AFP capability can machine complex aerofoils in a single pass, enhancing performance consistency.

By Material Type: PMC Dominance, CMC Acceleration

Polymer matrix composites held a 62.85% share in 2025 owing to entrenched supply chains and proven process repeatability. Ceramic matrix composites will outpace at a 14.72% CAGR, lifting the aeroengine composites market size for high-temperature sections, such as shrouds, liners, and exhaust plugs migrate to CMC.

Hybrid lay-ups that bond PMC fan blades to CMC leading edges are under evaluation to balance cost with heat resistance. The global resin shortage remains a near-term risk because only a handful of suppliers produce aerospace-qualified phenolics.

By End-User: OEM Dominance, Aftermarket Momentum

OEMs controlled 86.05% of 2025 revenue because composites are embedded at the design stage and purchased with new engines. The aftermarket is forecast at an 11.63% CAGR; airlines now pay premiums for composite spares that cut fuel costs and extend on-wing time.

Safran’s EUR 1 billion (USD 1.16 billion) MRO expansion aims to capture this spending shift through regional repair hubs that process composite fan blades and cases, reducing shipping time for Asia-Pacific operators. Predictive health-monitoring tools further boost aftermarket adoption by quantifying real-time fuel savings.

Geography Analysis

Asia-Pacific held a 31.92% share in 2025 as China accelerated Indigenous programs like the CJ-1000 for the C919 and the 35-ton-thrust CJ-2000, which are rich in composite hot-section parts. China’s turbine blades now tolerate 1,700 °C through single-crystal casting and 3D-printed cooling channels. Japan and South Korea supply high-strength fibers and prepregs, while India’s widebody orders boost regional demand.

North America remains a technology leader. GE Aerospace’s USD 26.9 billion commercial engines revenue in 2024 stemmed from composite-laden LEAP and GEnx programs, though material shortages cut deliveries by 10%. NASA’s HyTEC initiative is coating CMC airfoils to raise single-aisle efficiency, sustaining R&D pipelines.

The Middle East and Africa is projected to witness the fastest growth at 12.98% CAGR as the Gulf carriers add composite-rich engines and regional forces invest in next-generation fighters. Safran-MTU’s EURA engine will anchor European helicopter upgrades, while EU Clean Aviation’s open-fan demonstrator supports 20% CO₂ cuts via large-diameter composite fans.

Regulatory Landscape

Certification for composite-containing propulsion hardware continues to be governed by FAA and EASA engine and materials acceptance pathways, with qualification burden anchored in Part 21 approval processes and the building-block approach used for composite design allowables (commonly aligned with CMH-17 practices and FAA-recognized material data approaches such as NCAMP). In Europe, EASA adopted CS-E Amendment 8 in January 2025, updating engine certification specifications with provisions that influence how durability, maintenance program definition, and endurance demonstrations are substantiated for modern turbofans that incorporate composite structures and high-temperature materials.

Standards activity is also shaping procurement and sustainability compliance for composite engine parts and repairs. CEN published EN 4913:2026 in April 2026, setting requirements for regrinds and recycled materials in thermoplastic aerospace parts, including conditions around recycled content and validation. SAE International released AMS3970/3B in July 2026, a purchasing specification for carbon fiber fabric repair prepreg used in vacuum-cured repairs. Alongside airworthiness requirements, chemical compliance under EU REACH influences resin systems and consumables used across the composite value chain, pushing documentation, traceability, and substitution planning into early material selection and process qualification.

Value Chain Analysis

The aeroengine composites value chain begins with specialty inputs, including carbon fibers and ceramic fibers, high-temperature matrix resins, and prepregs, which are controlled through tightly specified procurement and process requirements (for example, aerospace process specifications used for bonded composite fabrication and repair). These materials feed Tier suppliers and specialist fabricators that convert fibers and resins into qualified subcomponents such as fan blades, fan cases, guide vanes, and hot-section hardware (liners, shrouds). Processes span automated fiber placement and resin transfer molding to high-temperature CMC processing and advanced inspection.

Downstream, engine OEMs and major integrators (GE Aerospace, CFM International, Pratt & Whitney, Rolls-Royce, Safran) incorporate composite parts into certified engine configurations and extend demand into aftermarket repair networks as shop visits rise. Capacity security and risk mitigation increasingly depend on long-term agreements and industrial partnerships with composite specialists. This includes Albany Engineered Composites securing a long-term Pratt & Whitney contract in April 2026 for structural composite engine components, and GKN Aerospace scaling additive production for engine parts after full-rate production of a fan case mount ring in 2025. Bottlenecks still concentrate around constrained high-temperature component supply and qualification lead times, while trade frictions and tariffs can add cost and complexity to cross-border flows of composite raw materials and production equipment.

Competitive Landscape

Market concentration is moderate. GE Aerospace, CFM International, Pratt & Whitney, and Rolls-Royce plc dictate engine architectures. Still, composite part supply is fragmented across Hexcel, Solvay, Toray, and a growing field of specialist fabricators. GE’s partnership with Kratos Defense aims to leverage small-engine expertise for unmanned systems, signaling intent to diversify revenue streams.

Safran’s acquisition of Component Repair Technologies underscores consolidation in the MRO space, where control of composite repair know-how secures recurring income. Patent filings emphasize process innovation, such as magnetic advanced jet turbines that embed CMC for extreme heat tolerance. Disruptors such as iCOMAT target double-digit weight savings through rapid tape shearing, enticing airframers seeking faster cycle times.

Supply-chain resilience is now a key differentiator. Firms with vertically integrated fiber, resin, and part production can better buffer raw-material shocks than traders who rely on spot markets. Long-term agreements with airframers and Tier-1 suppliers are becoming prerequisites for investment in new AFP lines.

Aeroengine Composites Industry Leaders

CFM International

Rolls-Royce plc

Pratt & Whitney (RTX Corporation)

Safran SA

GE Aerospace (General Electric Company)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A whitespace is emerging around localized, high-rate composite capacity that reduces exposure to constrained supply nodes and long logistics chains for fan system hardware and structural engine composites. Concrete investments and contracts show how the industry is addressing this: Safran announced a EUR 125 million investment in March 2026 to build a new aircraft engine compressor components plant in Welkenraedt, Belgium, tied to production ramp-ups for major engine families. Albany Engineered Composites received a long-term Pratt & Whitney award in April 2026 to produce structural composite engine components for GTF engines through 2036. These moves reinforce opportunities for qualified tier suppliers that can combine certified materials, automated production, and robust nondestructive inspection to support stable deliveries.

Technology roadmap activity also creates near-term openings for materials and process providers that can shorten cycle times while meeting stringent qualification requirements for next-generation architectures. Program work on open-fan concepts is directly linked to composite-intensive designs, and GE Aerospace highlighted the integration of Dowty expertise into the CFM RISE open-fan demonstrator, underscoring demand for advanced composite blade design and production methods such as automated resin transfer molding. Regional manufacturing hubs are being expanded as well, including Safran activity in Mexico and India-linked industrial partnerships, which broadens the supplier base for composite-adjacent components and increases the need for standardized, auditable material and process control across multiple geographies.

Recent Industry Developments

- July 2026: GE Aerospace highlighted the integration of its UK subsidiary Dowty’s composite blade design and automated resin transfer molding know-how into the CFM RISE open-fan demonstrator work. The emphasis on manufacturable composite blade technology supports higher-rate pathways for large composite rotating parts and strengthens the supplier ecosystem around open-fan architectures.

- April 2026: Albany Engineered Composites received a long-term Pratt & Whitney contract, extending through 2036, to manufacture structural composite engine components for the GTF engine family. The duration and scope improve production visibility for composite fabrication capacity and can accelerate supplier investments in automation, tooling, and qualified inspection capability.

- March 2024: GE Aerospace announced plans to invest EUR 64 million in European manufacturing facilities to enhance commercial and military engine production using advanced techniques and materials. The investment supports lighter, more efficient engine hardware and reinforces Europe’s role in qualified production and testing infrastructure for composite-rich engine programs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the annual value of composite parts that are installed in fixed-wing aircraft gas-turbine engines, counted at the point of factory installation. It includes polymer-matrix and ceramic-matrix composite components used across key engine sections where weight and temperature performance are design drivers.

Scope exclusions: It excludes helicopter turboshaft engines and composite structures that sit outside the propulsion system, such as wings, fuselage structures, and cabin interiors.

Segmentation Overview

- By Application

- Commercial Aircraft

- Narrow-Body

- Wide-Body

- Regional Jet

- Military Aircraft

- General Aviation Aircraft

- Business Jet

- Others

- Commercial Aircraft

- By Component

- Fan Blades

- Fan Case

- Guide Vanes

- Shrouds

- Other Components

- By Material Type

- Polymer Matrix Composites (PMC)

- Ceramic Matrix Composites (CMC)

- By End-User

- OEM

- Aftermarket

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base model structure and set clear boundaries for what is counted as an aeroengine composite part. We relied on public aviation and trade statistics, such as ICAO air transport indicators and FAA fleet and certification updates, to track aircraft activity levels and engine build momentum.

We also referenced sources including EASA airworthiness and certification publications, UN Comtrade trade codes for composite materials and aerospace parts (used as directional signals rather than a direct proxy for market value), and peer-reviewed journals covering ceramic-matrix composites and high-temperature polymer systems. Company annual reports, investor presentations, and reputable aerospace press were used to confirm program milestones and material adoption statements. When needed, we used paid subscriptions for company financials and patent databases to cross-check revenue exposure and innovation intensity. These examples are not exhaustive, and we consulted many other public sources to collect, validate, and clarify specific data points.

Primary Interviews and Surveys

Primary interviews focused on confirming which composite parts are being installed, how adoption differs by engine platform, and how pricing shifts with volume ramps and qualification stages. We spoke with material suppliers, component manufacturers, and aerospace procurement and engineering roles across APAC, EMEA, and the Americas, so gaps from desk research could be closed and the key assumptions could be sanity-checked against practical adoption patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 20% | APAC: 38% |

| Mid tier: 43% | Functional/Unit leaders: 22% | EMEA: 37% |

| Smaller Players: 22% | Managers: 58% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs demand using aircraft production and in-service fleet signals, and then converts that into composite content typically installed per engine family and module. After defining the demand pool, we apply blended pricing logic that reflects part type, for example hot-section versus cold-section use, and the qualification curve that shapes achievable yields.

To keep the model operational each year, we focus on a short list of inputs that can be refreshed, such as commercial and defense aircraft deliveries, engine production ramp indicators, composite penetration by component category, scrap and rework factors linked to manufacturing maturity, and high-temperature material adoption markers for CMC parts. Forecasting uses scenario analysis, since platform ramps and supply constraints do not always follow smooth historical patterns. Interview feedback is used to keep assumptions grounded, and results are cross-checked with selective bottom-up approximations, including supplier roll-ups based on publicly discussed program exposures and sampled ASP-time volume checks for a few high-value component groups. Totals are adjusted if these checks point to a mismatch. Where bottom-up detail is missing for niche components, we apply conservative gap-fill using adjacent part benchmarks, then re-validate through follow-up calls.

Data Validation & Update Cycle

Outputs are checked against independent signals, including aircraft delivery trends, known engine ramp plans, and documented technology adoption events that should show up in composite content. When an outlier appears, we reopen the drivers, re-test the assumptions, and run follow-up outreach to confirm whether the change is real or the result of a scope definition mismatch.

Before sign-off, the model and write-up go through multi-step analyst reviews focused on scope alignment, arithmetic accuracy, and year-to-year variance logic. Reports are refreshed annually, and interim updates are made when material events occur, such as major production disruptions, regulatory shifts, or program schedule changes. A final review is done right before delivery so clients receive the most current view available.

Mordor Intelligence's Aeroengine Composites Market Sizing Compared With Other Published Estimates

Published market sizes for aeroengine composites can vary because the boundary of what counts as an engine composite part is not always consistent, and the year used for the stated value can differ across reports. Differences also show up when firms blend factory-installed demand with aftermarket replacement, or when metal-matrix materials and non-engine structures are included in the same pool.

Aircraft and engine production signals, along with component-level adoption checkpoints for polymer and ceramic composites, are the evidence used to keep Mordor Intelligence's estimate anchored to factory-installed content in fixed-wing gas-turbine engines. That anchoring shifts the total versus studies that use broader aircraft composite definitions or apply factory-gate revenue conventions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.97 B (2026) | |

| Industry Research Publisher A | USD 3.50 B (2025) | Uses a different stated year and a wider component and material scope that explicitly includes metal-matrix composites, which can raise or shift totals depending on what is counted as an aeroengine part versus adjacent aerospace hardware. |

| Global Market Publisher B | USD 2.97 B (2025) | Reports factory-gate revenues and applies its own geography and supply-chain boundary rules, which can understate totals versus an installation-linked demand model when channel pass-through and program mix are treated differently. |

The spread across the three figures mostly comes down to scope edges and the reference year, not simple math differences. When the market is anchored to installed engine content and then cross-checked with production ramps and adoption milestones, the resulting number is easier to replicate and explain on a program-by-program basis.

Key Questions Answered in the Report

Why are composites increasingly used in commercial aero-engines?

Composites cut engine weight, allow higher temperatures, and enable 15-20% fuel savings, helping airlines meet cost and emission goals.

How large is the aeroengine composites market in 2026?

The aeroengine composites market size stands at USD 3.97 billion in 2026 and is projected to reach USD 6.79 billion by 2031 at an 11.28% CAGR.

Which segment grows fastest within the market?

The military application segment posts the highest growth, with a 12.55% CAGR through 2031 as adaptive-cycle and hypersonic programs scale.

What challenges hinder wider adoption of CMCs?

Key barriers include brittleness, complex nondestructive inspection, limited high-temperature resin supply, and lengthy FAA/EASA qualification cycles.

Which region leads demand for aeroengine composites?

Asia-Pacific leads with 31.92% market share, driven by China’s indigenous engine programs and rising commercial jet deliveries.

How are cost reductions achieved in composite manufacturing?

Automated fiber-placement, rapid tape shearing, and snap-cure prepregs cut lead times by up to one-third and reduce cost per pound by about 30%.

Page last updated on: