Hedgehog Pathway Inhibitors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.88 Billion |

| Market Size (2031) | USD 1.52 Billion |

| Growth Rate (2026 - 2031) | 11.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hedgehog Pathway Inhibitors Market Analysis by Mordor Intelligence

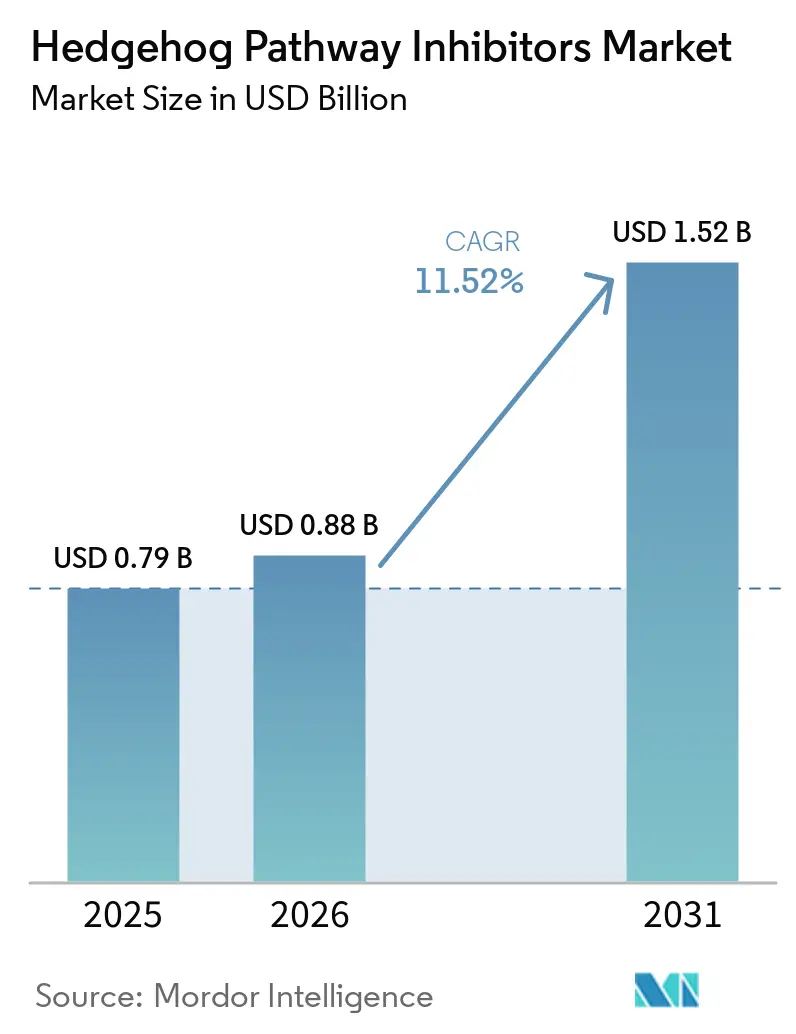

The Hedgehog Pathway Inhibitors Market size is expected to grow from USD 0.79 billion in 2025 to USD 0.88 billion in 2026 and is forecast to reach USD 1.52 billion by 2031 at 11.52% CAGR over 2026-2031.

Demand in the hedgehog pathway inhibitors market remains closely tied to the heavy burden of basal cell carcinoma in older adults. The demand base is broader than standard incidence counts suggest because patients with recurrent high-frequency BCC and patients with Gorlin syndrome often require sustained lesion suppression rather than short treatment cycles, which gives the hedgehog pathway inhibitors market a more stable treatment pool over time. Growth in the hedgehog pathway inhibitors market is also being shaped by topical reformulations and digitally enabled specialty dispensing, both of which directly address treatment drop-off linked to systemic toxicity and refill complexity. Combination use and biomarker-guided patient selection are widening the clinical logic for the hedgehog pathway inhibitors market beyond the narrowest use settings, particularly where pathway activation or resistance management can be identified more clearly before treatment starts. The market remains moderately concentrated because a small set of approved products still controls most current revenue, but resistance, toxicity, and tightly managed reimbursement in secondary markets continue to limit the upside implied by disease prevalence alone.

Key Report Takeaways

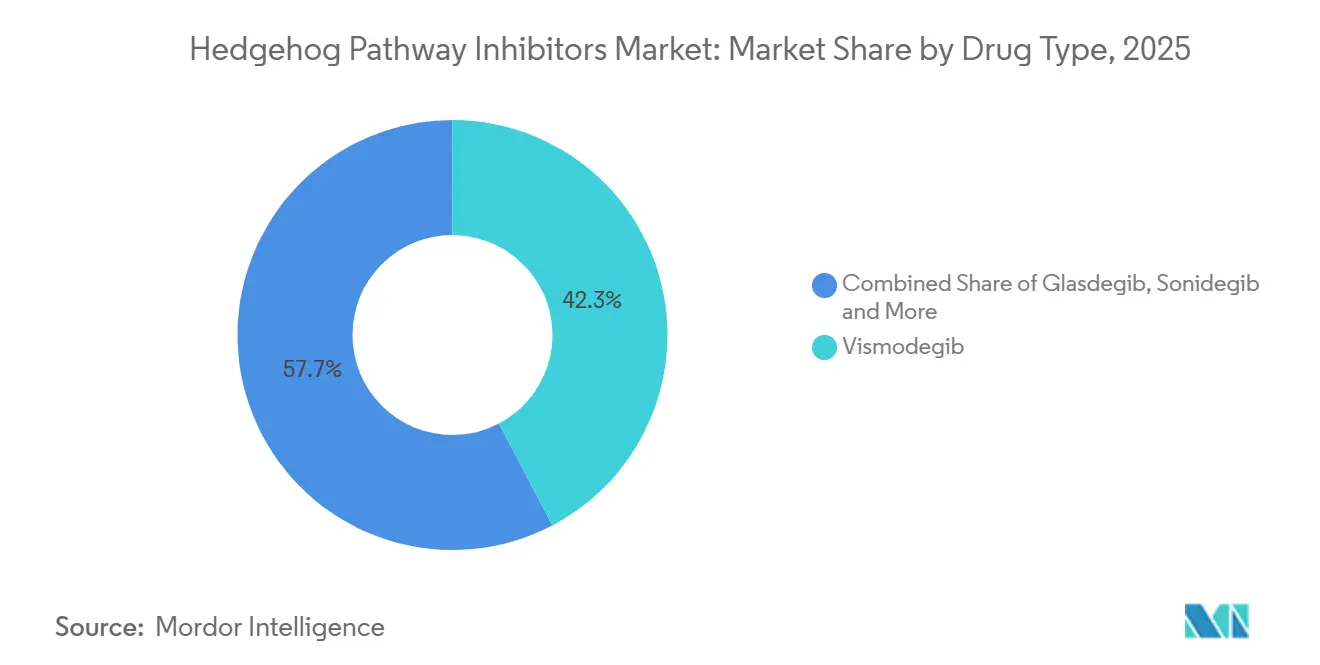

- By drug type, vismodegib held 42.31% revenue share in 2025, while glasdegib is projected to record the highest CAGR at 12.38% through 2031.

- By application, basal cell carcinoma accounted for 76.24% share in 2025, while Gorlin syndrome is forecast to expand at a 13.52% CAGR through 2031.

- By route of administration, oral formulations held 54.52% share in 2025, while topical reformulations are projected to advance at a 13.25% CAGR through 2031.

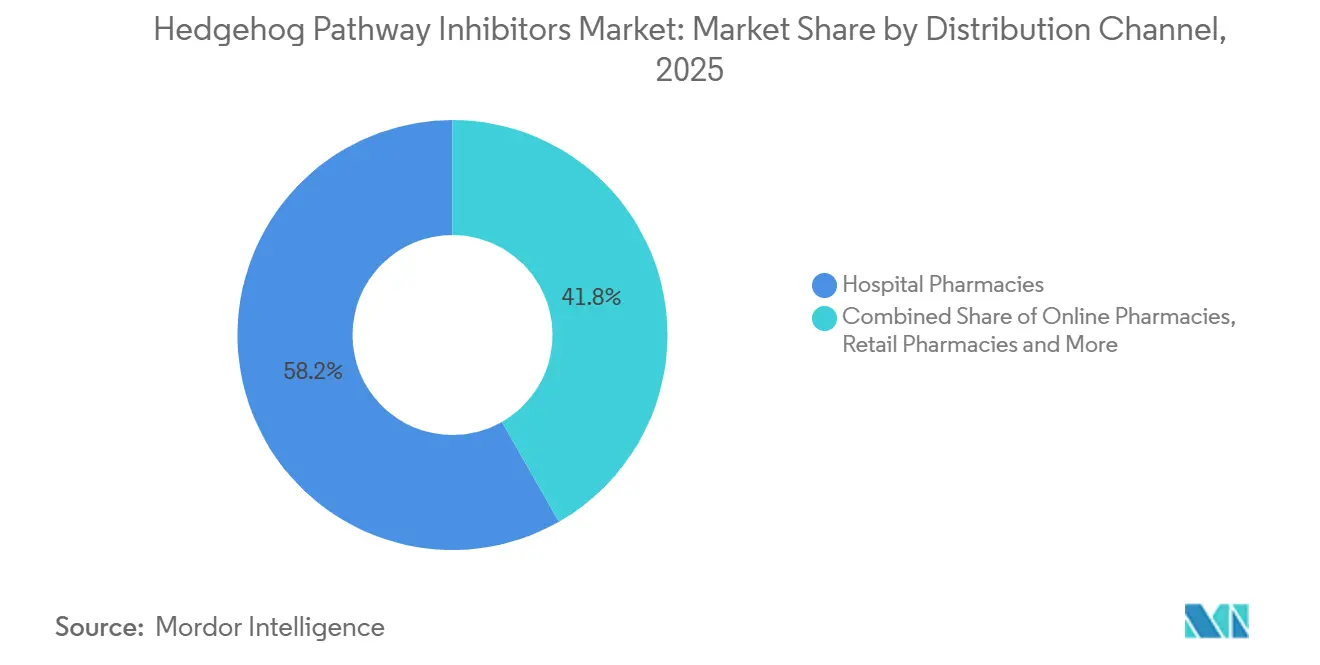

- By distribution channel, hospital pharmacies captured 58.24% share in 2025, while online pharmacies are expected to grow at a 14.52% CAGR through 2031.

- By end user, hospitals represented 60.44% share in 2025, while research institutes are projected to grow at a 12.68% CAGR through 2031.

- By geography, North America led with 41.52% share in 2025, while Asia-Pacific is forecast to expand at a 13.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hedgehog Pathway Inhibitors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising BCC and AML burden in aging and UV-exposed populations | +2.8% | Global, with steepest gains in high-income North America and East Asia | Long term (≥ 4 years) |

| Biomarker-guided patient stratification | +1.5% | North America and Europe, with early spill-over to APAC | Medium term (2-4 years) |

| Combination regimens beyond monotherapy | +1.3% | North America and Europe | Medium term (2-4 years) |

| Topical and locally delivered reformulations | +1.0% | North America, Europe, and APAC | Medium term (2-4 years) |

| Orphan and accelerated pathways | +1.2% | United States and EU | Short term (≤ 2 years) |

| Real-world evidence and persistence gains | +0.9% | Global, with early gains in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Basal Cell Carcinoma and AML in Aging and UV-Exposed Populations

The basic demand engine for the hedgehog pathway inhibitors market is demographic, because the treated population sits heavily in older age groups where both skin cancer burden and treatment complexity are rising. Global new BCC cases among adults aged 55 and above are increasing, and projections show sharper increases ahead in the oldest age bands, with the United States, Brazil, and China carrying the largest absolute caseloads. The hedgehog pathway inhibitors market also benefits from a less visible but important expansion in immunosuppressed patients, since transplant recipients and people on long-term biologics develop BCC at materially higher rates than immunocompetent populations, which widens the locally advanced pool that can move toward drug therapy.

On the leukemia side, glasdegib is positioned for adults aged 75 years or older or for adults with comorbidities that preclude intensive chemotherapy, which aligns the product with the oldest and fastest-growing AML treatment cohort[1]“Label, DAURISMO (Glasdegib) Tablet, Film Coated,” DailyMed, National Library of Medicine, dailymed.nlm.nih.gov. Real-world practice has reinforced that logic, with a 50% combined remission rate reported in first-line community oncology use of glasdegib-based care, which supports a durable clinical and commercial role for the hedgehog pathway inhibitors market in frail AML patients. As these older and medically complex populations expand, the hedgehog pathway inhibitors market gains not just more patients, but more patients who fit current label and care-setting requirements.

Biomarker-Guided Patient Stratification Expands Addressable Cohorts

Patient selection is becoming more precise, and that precision can materially improve conversion from diagnosis to treatment within the hedgehog pathway inhibitors market. In PTCH1-mutated tumors, vismodegib produced a 100% response rate in Gorlin syndrome patients, compared with a 43% response rate in unselected advanced BCC cohorts, which shows how strongly molecular context can change treatment value. That gap matters because broader genomic screening in dermatology and oncology practice can bring high-response patients into therapy earlier, rather than leaving hedgehog inhibitors for the latest refractory settings.

The hedgehog pathway inhibitors market also stands to benefit from the gradual normalization of pathway-level testing, since clinicians gain more confidence when target activation and likely response can be tied to a defined mutation pattern. Liquid biopsy platforms detecting circulating PTCH1 and SMO variants reached an 87.5% concordance rate with tissue-based testing, which lowers sampling friction and could increase screening rates in both skin cancer and leukemia programs[2]“Phase II Study of Vismodegib in Patients With SMO- or PTCH1-Mutated Tumors,” JCO Precision Oncology, ascopubs.org. As noninvasive testing improves and becomes easier to use at scale, the hedgehog pathway inhibitors market can add patients through better selection rather than through label expansion alone.

Combination Regimens Extend Clinical Utility Beyond Monotherapy

Combination treatment is giving the hedgehog pathway inhibitors market a wider clinical role than monotherapy alone was able to establish in earlier development cycles. The most credible current signal comes from glioblastoma, where the GEINOGLAS Phase Ib/II study showed that glasdegib combined with the Stupp regimen delivered a 15-month overall survival rate of 52.1% and a median overall survival of 15.3 months. That result matters because it shows hedgehog pathway inhibition working alongside standard radiochemotherapy, rather than trying to replace backbone treatment in a difficult tumor setting.

The hedgehog pathway inhibitors market is therefore gaining value as a platform that can reshape tumor behavior or treatment sensitivity, which is a broader role than direct pathway blockade in BCC or AML alone. This approach also diversifies the revenue base because positive combination data can support use across additional solid tumor contexts without reducing the importance of current labeled oncology segments. If more studies confirm this pattern, the hedgehog pathway inhibitors market will rely less on a narrow set of monotherapy indications and more on a larger treatment architecture built around combination logic.

Topical and Locally Delivered Reformulations Reduce Systemic Toxicity

Local delivery has become one of the clearest growth levers in the hedgehog pathway inhibitors market because it directly addresses the tolerability limits that have constrained long-course oral therapy. In preclinical work, pH-sensitive sonidegib invasome hydrogel delivered intratumorally produced a 99.05% reduction in tumor volume in DMBA-induced skin cancer models while keeping systemic exposure low. That matters because the commercial issue is not only patient comfort, it is also treatment persistence, since lower systemic exposure can keep more patients on therapy for longer periods.

The hedgehog pathway inhibitors market may also gain a distinct prevention layer through local delivery, especially in Gorlin syndrome where chronic suppression of new lesions is a different need from treatment of existing advanced disease. Sol-Gel Technologies completed enrollment in its pivotal Phase 3 study of SGT-610 and expects top-line data in Q4 2026, while its method-of-use patent allowance extends protection to 2044. Company communication places the prevention opportunity at more than USD 300 million in annual peak revenue, which would add a non-overlapping pool to the hedgehog pathway inhibitors market rather than shifting value within the existing treatment base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Musculoskeletal and taste-related toxicity | -1.8% | Global | Long term (≥ 4 years) |

| SMO mutation-mediated resistance | -1.5% | Global | Long term (≥ 4 years) |

| Narrow reimbursable label and surgery or radiation substitution limits | -1.3% | Europe and North America | Medium term (2-4 years) |

| Limited late-stage pipeline depth and high attrition in niche indications | -0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Musculoskeletal and Taste-Related Toxicity Drives Discontinuation

Toxicity remains one of the strongest limits on the hedgehog pathway inhibitors market because it reduces treatment duration even when eligible patient numbers continue to rise. In a multicenter real-world study, treatment interruption due to adverse events occurred in 47.4% of vismodegib recipients and in 13.2% of sonidegib recipients, which highlights a very large persistence gap within the same therapeutic class. That gap is commercially meaningful because sonidegib’s longer half-life allows more flexibility through intermittent dosing, while vismodegib often forces a harder trade-off between continuous disease control and tolerability. The adverse event burden is not limited to controlled studies, and real-world pharmacovigilance work continues to show a strong signal for muscle spasms and dysgeusia in oral hedgehog inhibitor exposure.

The hedgehog pathway inhibitors market loses value whenever patients stop before complete response, because the treated population is large enough to create demand, but each patient contributes fewer therapy months than expected. Until lower-toxicity formats or better management protocols become routine, the hedgehog pathway inhibitors market will keep facing a structural persistence problem rather than a simple awareness problem.

SMO Mutation-Mediated Resistance Limits Duration of Response

Resistance continues to cap the durability of the hedgehog pathway inhibitors market because it directly weakens the benefit of all therapies that rely on binding the Smoothened receptor. Advanced genomic analyses identified SMO variants such as D473Y, G497W, and W535L in 50% of progressing BCC lesions, showing that resistance is not a rare edge case in advanced disease. These variants either obstruct the ligand-binding pocket or trigger downstream pathway activity that makes continued SMO blockade less effective, which shortens useful treatment duration even when the initial response is favorable.

Glasdegib’s binding geometry is different enough to attract interest for sequencing after vismodegib or sonidegib exposure, and no documented SMO mutation-mediated resistance in BCC has been reported for glasdegib to date. Even so, the hedgehog pathway inhibitors market still lacks approved downstream GLI inhibitors or resistance-specific combinations that could turn sequencing into a standardized care pathway. Regulators have also not embedded resistance testing or molecular monitoring into major labels, so the hedgehog pathway inhibitors market continues to depend on physician discretion rather than a codified resistance-management framework.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Oral SMO Inhibitors Anchor Revenue While Glasdegib Gains Momentum

Vismodegib retained 42.31% of the hedgehog pathway inhibitors market share in 2025, reflecting its first-mover position and its durable use in locally advanced BCC where physician familiarity remains high. Its position in the hedgehog pathway inhibitors market is still supported by broad clinical recognition in BCC and by a long-established prescribing base that newer agents must displace case by case. Real-world data also continue to confirm that vismodegib remains clinically active in advanced BCC, which explains why share has held despite the class-wide toxicity profile. Sonidegib competes with a clearer tolerability message, and real-world analysis showed sonidegib-treated patients were 52% less likely to experience muscle spasms and 71% less likely to develop taste-related conditions than vismodegib-treated patients over nine months of follow-up. That difference does not overturn vismodegib’s entrenched base, but it does give the hedgehog pathway inhibitors market a visible product-level split between scale and tolerability.

Glasdegib is the fastest-growing drug type in the hedgehog pathway inhibitors market at a 12.38% CAGR from 2026 to 2031. Its growth is linked to investigation across leukemia settings beyond AML, including myelofibrosis, myelodysplastic syndromes, and chronic myelomonocytic leukemia, which broadens the clinical narrative around the class without relying on additional BCC exposure. The hedgehog pathway inhibitors industry also gains a useful diversification point from glasdegib because its hematology role reduces dependence on skin cancer alone. A real-world study across U.S. community oncology practices reported a 50% combined remission rate in first-line glasdegib-treated AML patients, which supports the product’s utility beyond academic trial centers. The “other hedgehog pathway inhibitors” bucket remains small today, but taladegib’s orphan designation in idiopathic pulmonary fibrosis shows how the hedgehog pathway inhibitors market is extending into adjacent disease areas that could become commercially meaningful over time.

By Application: Basal Cell Carcinoma Remains the Foundation, Gorlin Syndrome Leads Growth

Basal cell carcinoma accounted for 76.24% of the hedgehog pathway inhibitors market size in 2025, which shows how heavily current revenue still depends on advanced BCC treatment pathways. This concentration exists because drug therapy mainly enters when surgery or radiation cannot be used, which gives the hedgehog pathway inhibitors market a protected base in a clearly defined unmet-need population. Coverage rules reinforce that structure, and prior authorization frameworks continue to tie reimbursement closely to labeled use and specialist oversight rather than broad community prescribing[3]“Odomzo (Sonidegib) Prior Authorization/Notification, UnitedHealthcare Commercial Plans,” UnitedHealthcare, uhcprovider.com. AML remains a distinct secondary application within the hedgehog pathway inhibitors market because glasdegib serves older or medically frail patients who are not candidates for intensive chemotherapy, which places the product in a clinically different and institutionally concentrated segment. Medulloblastoma is smaller in current revenue terms, but response rates near 50% in PTCH1-variant SHH-subgroup tumors show why genotype-gated use remains relevant in selected cases.

Gorlin syndrome is the fastest-growing application in the hedgehog pathway inhibitors market at a 13.52% CAGR from 2026 to 2031. The segment stands out because it requires indefinite suppression of new lesion formation, so revenue can build from repeated prevention rather than from episodic treatment lines alone. That profile makes Gorlin syndrome one of the most underpenetrated parts of the hedgehog pathway inhibitors market, especially if topical prevention therapy reaches approval. Sol-Gel Technologies completed enrollment in the Phase 3 SGT-610 study, and top-line results are expected in Q4 2026, which keeps the first prevention-focused commercial pathway firmly in view. If approved, that therapy would open a prevention pool distinct from the existing advanced BCC treatment pool, which would let the hedgehog pathway inhibitors market expand without relying on the same reimbursement logic that governs current oncology use.

By Route of Administration: Oral Routes Lead but Topical Formulations Are Reshaping the Pipeline

The oral route held 54.52% revenue share in 2025, which reflects the current commercial reality that vismodegib, sonidegib, and glasdegib are all oral products. Oral dominance in the hedgehog pathway inhibitors market is therefore a function of approved product mix rather than a clean preference signal from physicians or patients. Real-world safety follow-up from the NISSO post-authorization study showed that adverse events with oral sonidegib can be managed through intermittent dosing, which supports continued oral use even under tolerability pressure. Injectable use is still limited, but it has strategic relevance inside the hedgehog pathway inhibitors market because glasdegib is used with low-dose cytarabine in AML, which keeps the class connected to supervised hematology regimens rather than only to dermatology practice. As long as all approved agents remain oral, this segment will keep leading revenue even while the pipeline moves in other directions.

Topical delivery is the fastest-growing route of administration in the hedgehog pathway inhibitors market at a 13.25% CAGR from 2026 to 2031. This growth outlook is supported by formulation work showing that laser-assisted topical vismodegib delivery can achieve clinically relevant concentrations at dermal depths of 300 to 900 µm, which directly addresses a historic penetration barrier. The commercial case is stronger than a simple convenience argument because topical delivery can separate anti-tumor activity from the systemic toxicity that has limited long-duration oral exposure. The hedgehog pathway inhibitors market also gains regulatory momentum here, since patidegib gel has a patented vehicle and orphan designations from both the FDA and EMA, with the program now anchored by a pivotal late-stage study. If topical therapy reaches the market, route mix in the hedgehog pathway inhibitors market will start to reflect not only existing labels but also a broader attempt to preserve efficacy while lowering systemic burden.

By Distribution Channel: Specialty Pharmacies Anchor Current Volume as Digital Channels Accelerate

Hospital pharmacies held a 58.24% revenue share in 2025, which reflects the controlled dispensing environment around AML care and the specialist oversight required for branded oncology therapies. This channel structure keeps a large part of the hedgehog pathway inhibitors market tied to oncology centers, where prescribing, insurance verification, and follow-up are more centralized. Retail pharmacies remain a secondary route, especially for community-based BCC management outside the most tightly organized specialty systems. Prior authorization and specialty-drug controls also reinforce hospital-centered distribution in the hedgehog pathway inhibitors market by routing use through dermatology and oncology specialists rather than general practice. As a result, current channel leadership still reflects clinical complexity and payer design more than consumer access patterns.

Online pharmacies are the fastest-growing distribution channel in the hedgehog pathway inhibitors market at a 14.52% CAGR from 2026 to 2031. That growth does not mean direct-to-consumer oncology retail is becoming the main model, because most of the activity still runs through licensed specialty dispensing networks and manufacturer-linked support systems. The shift instead comes from prescription management portals, tele-dermatology links, digital refill tools, and patient-support programs that increasingly interface with the formal specialty pharmacy ecosystem. This matters for the hedgehog pathway inhibitors market because refill persistence is one of the main pressure points in long-course therapy, especially when adverse events already threaten continuity. As more dispensing flows become digitally coordinated, the hedgehog pathway inhibitors market can improve realized therapy duration even if the treated population itself does not change as quickly.

By End User: Hospitals Lead While Research Institutes Drive Novel Application Discovery

Hospitals represented 60.44% of end-user revenue in 2025, which confirms that institutional care settings remain the main gateway into treatment. Hospital leadership in the hedgehog pathway inhibitors market is tied to the AML pathway, where older or medically frail patients often require monitored initiation, and to advanced BCC care, where multidisciplinary dermatology and oncology teams manage complex cases. These settings also handle much of the insurance verification and prior authorization work that supports access to high-cost branded therapies. Specialty clinics remain a meaningful secondary end-user group in the hedgehog pathway inhibitors market, particularly for ambulatory management of vismodegib and sonidegib in locally advanced BCC. Even so, the institutional role of hospitals keeps the largest share of current demand inside structured oncology units rather than dispersed outpatient channels.

Research institutes are the fastest-growing end-user segment in the hedgehog pathway inhibitors market at a 12.68% CAGR from 2026 to 2031. This growth reflects the expanding use of biomarker-stratified investigator-led studies in glioblastoma, idiopathic pulmonary fibrosis, chronic myeloid leukemia, and pancreatic cancer, where academic centers act as both trial sites and early product validators. The hedgehog pathway inhibitors industry gains future demand from these centers because they are the main places where non-canonical use cases are tested and refined before broader commercial uptake. Work on dual targeting of SMO and BCR-ABL1 in chronic myeloid leukemia showed stronger elimination of imatinib non-responder stem and progenitor cells in preclinical PDX models, which captures the kind of translational activity now centered in research institutions. As translational studies move further into disease areas outside BCC and AML, research institutes will keep shaping the outer edge of the hedgehog pathway inhibitors market even before those uses produce major commercial revenue.

Geography Analysis

North America held 41.52% of the hedgehog pathway inhibitors market share in 2025, making it the clear regional leader. The United States drove most of that position because it recorded the world’s highest BCC incidence burden. The region also benefits from a specialist oncology infrastructure that is well aligned with referral of locally advanced BCC and with branded oncology reimbursement. Regulatory support has helped as well, and the 2025 draft-guidance update around accelerated approval and post-marketing confirmation reinforced a framework that can still support earlier entry for oncology drugs while maintaining evidence requirements.

Asia-Pacific within the hedgehog pathway inhibitors market size is projected to expand at a 13.55% CAGR from 2026 to 2031, making it the fastest-growing regional block. Growth is being supported by aging populations in China and Japan, rising UV-linked exposure in several outdoor-working populations, and stronger access to specialty oncology medicines. China’s regulatory reforms have shortened local approval timelines for oncology products with prior Western approvals, which improves the path from global evidence to local commercialization. Japan has also added region-specific support, with a Phase Ib/II glasdegib study in AML patients ineligible for intensive chemotherapy reporting a disease-modifying response rate of 46.7% in the expansion cohort. China’s BCC caseload among adults aged 55 and above shows how demographic change is creating a much larger future base for the hedgehog pathway inhibitors market in the region.

The remaining geographies remain smaller in current revenue terms, but they are becoming more relevant to the hedgehog pathway inhibitors market over time. The Gulf Cooperation Council countries combine high UV exposure with improving oncology capacity, although reimbursement remains fragmented across systems. South Africa remains the most developed sub-Saharan entry point for the hedgehog pathway inhibitors market because private healthcare channels and academic medical centers provide the clearest route to specialized oncology use.

Competitive Landscape

The hedgehog pathway inhibitors market shows moderate concentration because three approved molecules, vismodegib, sonidegib, and glasdegib, still generate most current commercial revenue. Roche’s Erivedge remains the core BCC anchor, Pfizer’s Daurismo holds the AML position, and Sun Pharmaceutical Industries markets Odomzo in the United States as the main tolerability-focused alternative within the class. Competitive behavior in the hedgehog pathway inhibitors market has shifted away from broad label expansion and toward real-world evidence generation, biomarker-led positioning, and formulation work that can improve persistence or open new care settings. That shift is rational because the current class already serves clearly defined oncology niches, so new share gains depend more on staying power and differentiated use than on simple physician awareness.

Sol-Gel Technologies is one of the clearest examples of how the hedgehog pathway inhibitors market is moving, because it has advanced SGT-610 toward a prevention-focused role in Gorlin syndrome while also building a long patent runway for the topical platform. Endeavor BioMedicines provides a second example, with taladegib receiving orphan designation from the FDA and European Commission for idiopathic pulmonary fibrosis, which extends hedgehog pathway inhibition well beyond oncology. These programs matter because the white space in the hedgehog pathway inhibitors market is concentrated in post-resistance sequencing, prevention in genetic BCC syndromes, and non-oncology uses where pathway modulation still has mechanistic relevance. They also show that emerging competitors are not trying to win by copying first-generation oral SMO inhibitors alone. Instead, they are targeting the specific gaps that current products have left open in durability, tolerability, and indication scope.

A third competitive thread in the hedgehog pathway inhibitors market is the search for non-SMO-binding or resistance-resilient chemotypes. Structure-activity work using molecular docking at the Smoothened receptor has identified antagonist chemotypes that retain activity against resistance variants such as the vismodegib-associated D473 mutation, which points to a real route for differentiated follow-on products. Delivery technology is also becoming a competitive weapon in the hedgehog pathway inhibitors market, because a protected topical platform can create a moat that generic oral products cannot easily cross. The result is a market that is concentrated enough for established companies to matter, but open enough for clinical-stage entrants to reshape future competition if they solve resistance, local delivery, or prevention more effectively than the current leaders.

Hedgehog Pathway Inhibitors Industry Leaders

Roche Holding AG

Novartis AG

Pfizer Inc.

Sun Pharmaceutical Industries Ltd.

BridgeBio Pharma Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: A real-world, longitudinal study published in Dermatology and Therapy found that patients with basal cell carcinoma (BCC) treated with sonidegib have longer treatment persistence, more time on treatment, delayed discontinuation, and lower rates of significant pharmacological conditions compared to those treated with vismodegib.

- November 2025: Endeavor BioMedicines announced that the European Medicines Agency (EMA) granted PRIority MEdicines (PRIME) designation for its investigational therapy, taladegib (ENV-101) a Hedgehog signaling pathway inhibitor, for the treatment of idiopathic pulmonary fibrosis (IPF).

Global Hedgehog Pathway Inhibitors Market Report Scope

As per the scope of the report, hedgehog pathway inhibitors are a class of drugs that specifically target and block components of the Hedgehog signaling pathway. This pathway is crucial in embryonic development, cell differentiation, and tissue patterning, but its abnormal activation has been linked to the development and progression of certain cancers, such as basal cell carcinoma and medulloblastoma. Hedgehog Pathway Inhibitors are used therapeutically to suppress this pathway's activity, thereby inhibiting tumor growth and proliferation.

The segmentation of the Hedgehog Pathway Inhibitors Market is categorized by drug type, application, route of administration, distribution channel, end user, and geography. By drug type, the market includes vismodegib, sonidegib, glasdegib, and other hedgehog pathway inhibitors. By application, it is segmented into basal cell carcinoma, acute myeloid leukemia, medulloblastoma, Gorlin syndrome, and other applications. Based on the route of administration, the market is divided into oral, topical, and injectable. By distribution channel, it comprises hospital pharmacies, retail pharmacies, online pharmacies, and other distribution channels. By end user, the segmentation includes hospitals, specialty clinics, research institutes, and homecare settings. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Vismodegib |

| Sonidegib |

| Glasdegib |

| Other Hedgehog Pathway Inhibitors |

| Basal Cell Carcinoma |

| Acute Myeloid Leukemia |

| Medulloblastoma |

| Gorlin Syndrome |

| Other Applications |

| Oral |

| Topical |

| Injectable |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Other Distribution Channels |

| Hospitals |

| Specialty Clinics |

| Research Institutes |

| Homecare Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Type | Vismodegib | |

| Sonidegib | ||

| Glasdegib | ||

| Other Hedgehog Pathway Inhibitors | ||

| By Application | Basal Cell Carcinoma | |

| Acute Myeloid Leukemia | ||

| Medulloblastoma | ||

| Gorlin Syndrome | ||

| Other Applications | ||

| By Route of Administration | Oral | |

| Topical | ||

| Injectable | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Other Distribution Channels | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Research Institutes | ||

| Homecare Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in hedgehog pathway inhibitors through 2031?

Growth is being supported by rising BCC and AML burden in older populations and a move toward topical delivery that can improve treatment persistence. The Hedgehog pathway inhibitors market size is expected to increase from USD 0.79 billion in 2025 to USD 0.88 billion in 2026 and reach USD 1.52 billion by 2031.

Why does basal cell carcinoma remain the main revenue application?

Basal cell carcinoma contributed 76.24% of revenue in 2025 because hedgehog inhibitors are used when surgery or radiation is not suitable, and there are limited approved alternatives for those advanced cases.

Which drug leads current sales and which one is growing fastest?

Vismodegib led 2025 revenue with a 42.31% share, while glasdegib is projected to post the fastest growth at a 12.38% CAGR through 2031.

Why is Asia-Pacific growing faster than North America?

Asia-Pacific is forecast to grow at 13.55% CAGR through 2031 because of aging populations, expanding specialty oncology access, improving approval pathways, and a rising BCC caseload in countries such as China and Japan.

How important is topical delivery for future demand?

Topical reformulations are projected to grow at a 13.25% CAGR through 2031 because they aim to separate anti-tumor benefit from systemic toxicity and may open prevention use in Gorlin syndrome.

Is the competitive environment fragmented or concentrated?

The space is moderately concentrated. Three approved molecules anchor most current revenue, but pipeline entrants in prevention, fibrosis, resistance management, and novel delivery keep competition active.

Page last updated on: