HDAC Inhibitors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.5 Billion |

| Market Size (2031) | USD 2.40 Billion |

| Growth Rate (2026 - 2031) | 9.11% CAGR |

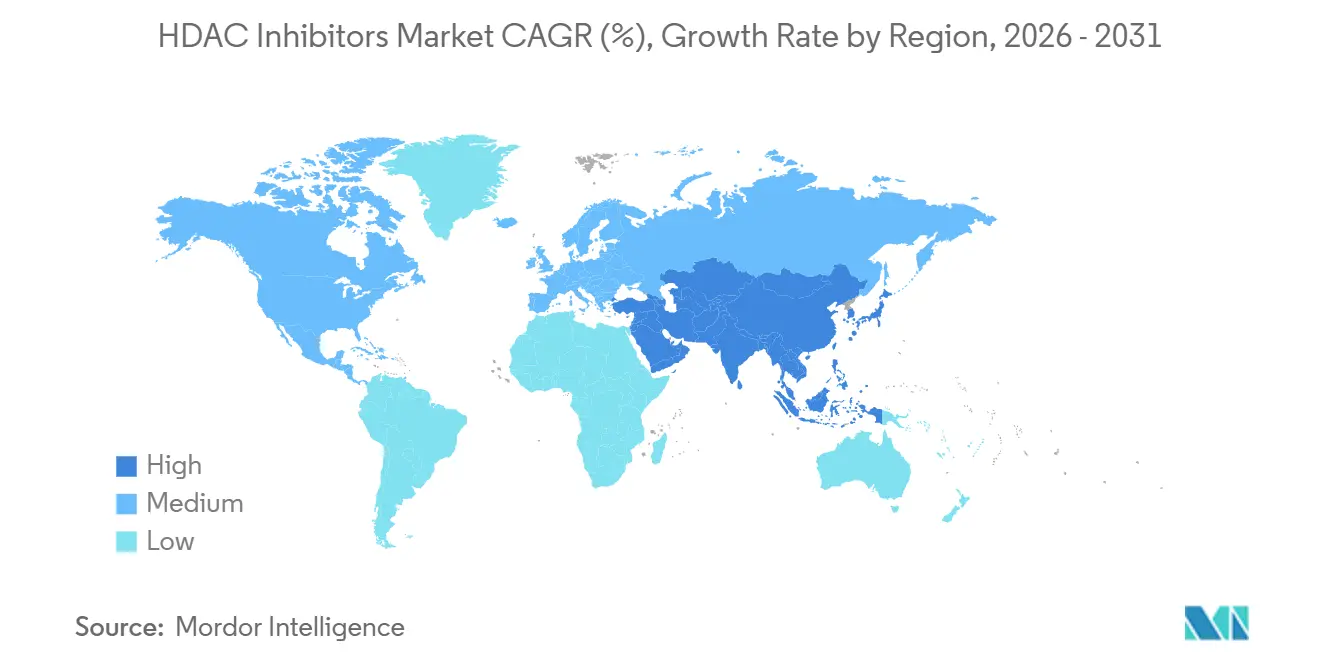

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HDAC Inhibitors Market Analysis by Mordor Intelligence

The HDAC Inhibitors Market size is projected to expand from USD 1.40 billion in 2025 and USD 1.5 billion in 2026 to USD 2.40 billion by 2031, registering a CAGR of 9.11% between 2026 to 2031.

Hospitals are layering histone deacetylase agents into combination regimens, while regulators are rewarding isoform-selective pipelines that lower hematologic and cardiac risks. North America dominates revenue, but Asia-Pacific is accelerating after the 2025 dual-catalog reform in China preserved commercial pricing for innovative molecules. The March 2024 approval of givinostat for Duchenne muscular dystrophy opened a non-oncology runway that could reshape lifetime sales curves [1]U.S. Food and Drug Administration, “DUVYZAT (givinostat) Label,” FDA.gov. Investors signaled confidence when Celgene agreed in February 2026 to pay Acetylon USD 100 million upfront for selective scaffolds, with milestones that could reach USD 1.6 billion.

Key Report Takeaways

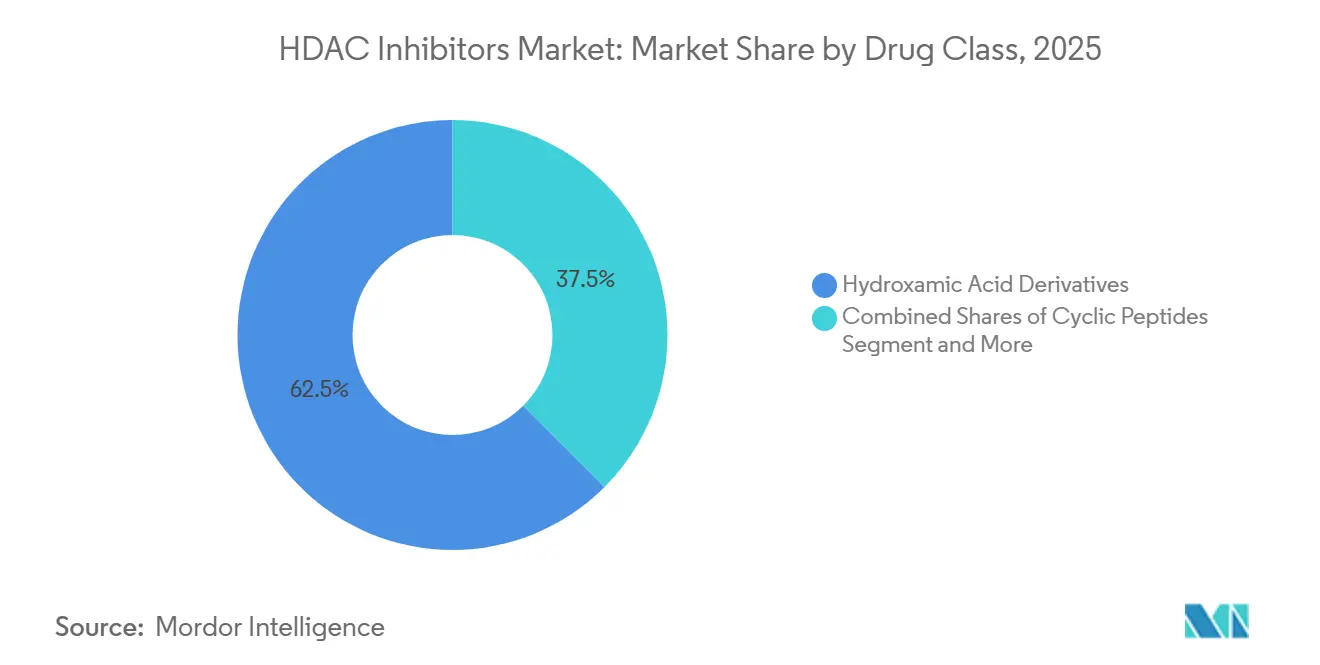

- By drug class, hydroxamic acid derivatives led the HDAC inhibitor market with 62.50% market share in 2025 and are forecast to grow at 9.50% through 2031.

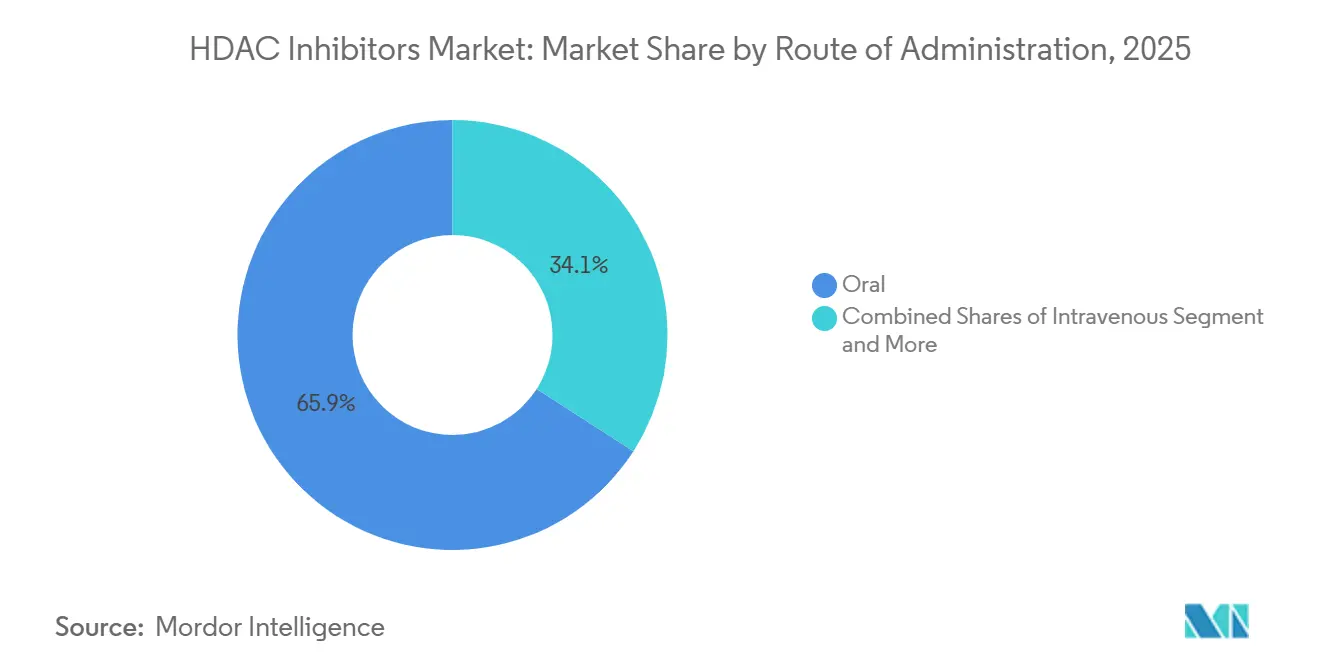

- By route of administration, intravenous formulations are advancing at a 9.40% CAGR to 2031, the fastest among all routes. Whereas the oral segment led with 65.91% market share in 2025.

- By application, oncology retained 78.19% revenue share in 2025, and is expected to reach the highest CAGR of 9.35% by 2031.

- By distribution channel, hospital pharmacies accounted for 68.71% of the HDAC inhibitor market in 2025 and are expected to grow at a 9.28% CAGR.

- By geography, Asia-Pacific records the fastest CAGR of 9.37%, whereas North America led the market with 58.17% market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HDAC Inhibitors Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding oncology indications and orphan approvals | +1.8% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Shift toward oral HDAC inhibitors for greater convenience and adherence | +1.5% | Global, particularly Asia-Pacific (China, Japan) | Short term (≤ 2 years) |

| Combination regimens with immune checkpoint inhibitors and proteasome inhibitors | +2.1% | North America and EU leading; APAC following | Medium term (2-4 years) |

| Expanding clinical pipeline and trial footprint | +1.4% | Global | Long term (≥ 4 years) |

| Non-oncology expansion (e.g., DMD) broadening patient base | +1.6% | North America and EU initially; global expansion | Medium term (2-4 years) |

| Rise of HDAC6-selective agents enabling chronic and combination use | +1.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Oncology Indications and Orphan Approvals

Orphan designations grant 7 years of exclusivity and waive multi-million-dollar fees, tilting the HDAC inhibitor market toward rare cancers. Cereno won orphan status for CS1 in pulmonary arterial hypertension, and China cleared tucidinostat for biomarker-defined diffuse large B-cell lymphoma, illustrating regulators’ appetite for precision labels [2]Chipscreen Biosciences, “Tucidinostat Approved for DLBCL in China,” Chipscreen.com. Givinostat’s mutation-agnostic nod in Duchenne muscular dystrophy shows that broad eligibility can coexist with orphan pricing, though payers are beginning to compare costs against low-priced corticosteroids.

Shift Toward Oral HDAC Inhibitors for Greater Convenience and Adherence

Oral products accounted for 65.91% of 2025 volume, yet hospitals still favor infusions when drugs pair with cytotoxics that require synchronized monitoring. Tucidinostat’s 17-hour half-life supports once-daily tablets, while ivaltinostat demonstrated acceptable exposure despite 10.6% oral bioavailability, proving that formulation workarounds can offset low permeability. Reimbursement barriers persist because specialty pharmacies enforce REMS protocols, effectively transforming “oral” convenience into monitored therapy.

Combination Regimens with Immune Checkpoint Inhibitors and Proteasome Inhibitors

Monotherapy ceilings push sponsors toward epigenetic-immuno combos. Tucidinostat plus nivolumab is in Phase III non-small-cell lung cancer trials aimed at reversing T-cell exhaustion, with interim futility reviews scheduled for 2027. Belinostat’s halted trial with tazemetostat underlines operational risk when overlapping hematologic toxicities force protocol changes. Developers now prioritize partners with non-overlapping safety profiles, especially PD-1 inhibitors.

Expanding Clinical Pipeline and Trial Footprint

Twelve new INDs were filed between 2024 and 2026, 40% of which target HDAC6. Karus established a maximum tolerated dose for KA2507 using acetylated-tubulin biomarkers, but has yet to release Phase II timelines, suggesting fund-raising hurdles. Over 60% of the 2025 trial starts enrolled East-Asian sites, leveraging faster ethics approvals and China’s conditional pathway that accepts foreign data for rare disorders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Class toxicity and narrow therapeutic window limit dosing | -1.2% | Global | Short term (≤ 2 years) |

| Modest monotherapy efficacy in solid tumors slows uptake | -0.9% | Global, particularly North America and EU | Medium term (2-4 years) |

| Indication withdrawals narrow labels and dampen confidence | -0.7% | North America and EU | Short term (≤ 2 years) |

| Cardiac/QT and drug-drug interaction risks constrain use | -1.0% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Class Toxicity and Narrow Therapeutic Window Limit Dosing

QT prolongation emerges from altered ion-channel trafficking rather than direct hERG block, creating delayed arrhythmia risk that complicates ECG scheduling. WHO VigiAccess lists seven torsades reports for vorinostat, none for romidepsin, underscoring scaffold variability. Givinostat requires weekly platelets during the first month of therapy, reflecting thrombocytopenia tied to HDAC1/2 inhibition.

Modest Monotherapy Efficacy in Solid Tumors Slows Uptake

Objective response rates below 10% in lung, breast, and colorectal studies have prompted developers to adopt combination designs. Panobinostat lost its multiple myeloma label in 2021 after confirmatory survival data failed to materialize. Romidepsin followed with a PTCL withdrawal, reminding investors that surrogate endpoints invite regulatory rollback [3]Bristol Myers Squibb, “ISTODAX Prescribing Information,” BMS.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Hydroxamic Acids Continue to Lead

Hydroxamic acids held a 62.50% share of the HDAC inhibitor market in 2025 and is expected to grow with 9.50% CAGR by 2031, supported by the legacy use of vorinostat, belinostat, and panobinostat. Despite the risk of thrombocytopenia, oncologists value their multi-isoform potency. Cyclic peptides like romidepsin show lower QT liability, but their smaller label portfolio limits volume. Benzamides, led by tucidinostat, gain regional traction after China’s 2024 green-light for diffuse large B-cell lymphoma.

HDAC6-selective pipelines receive venture funding, yet ricolinostat’s stalled neuropathy program and KA2507’s pending Phase II plans temper expectations. Non-hydroxamate zinc binders are attracting partnerships, highlighted by Celgene’s 2026 Acetylon deal, which anchors future portfolio expansion.

By Application: Oncology Dominates but Neurology Emerges

Oncology delivered 78.19% of 2025 revenue and is expected to register 9.35% CAGR by 2031, making it the backbone of the HDAC inhibitors market. Confirmatory trial obligations for belinostat and tucidinostat may reshape this balance after 2030.

Neurology’s foothold strengthened when givinostat won U.S. approval, demonstrating anti-fibrotic benefit in Duchenne muscular dystrophy. Pipeline assets in pulmonary arterial hypertension and idiopathic pulmonary fibrosis suggest a widening therapeutic canvas that supports longer treatment duration and cumulative sales.

By Route of Administration: Orals Lead, Infusions Grow Faster

Orals captured 65.91% of volume, yet intravenous products are growing at the fastest clip, with a 9.40% CAGR, because multi-agent regimens rely on infusion centers. Tucidinostat’s once-daily tablet offers home dosing, but reimbursement puts most prescriptions through specialty channels, mirroring infusion economics. Topicals such as remetinostat remain investigational. Controlled-release technology, exemplified by Cereno’s CS1, maintains trough levels sufficient for vascular remodeling without nausea spikes.

By Distribution Channel: Hospital Pharmacies Retain Control

Hospital pharmacies controlled 68.71% of 2025 sales and is expected to grow at 9.28% CAGR through 2031, reflecting REMS, ECG, and platelet monitoring requirements. Specialty pharmacies service chronic neuromuscular prescriptions, yet high-touch oversight still dominates economics.

Online channels remain negligible because regulators prohibit dispensing epigenetic cytotoxics without pharmacist counseling. Integrated delivery networks are bundling drugs, infusions, and labs into single codes, a model that favors hospital systems.

Geography Analysis

North America contributed 58.17% revenue in 2025, helped by orphan pricing and specialty-pharmacy infrastructure. Givinostat’s launch adds a chronic neuromuscular revenue stream with therapy costs exceeding USD 300,000 annually. Post-marketing withdrawals for romidepsin and panobinostat trimmed oncology growth, prompting sponsors to deepen real-world evidence collection at academic centers.

Asia-Pacific posts the fastest 9.37% CAGR, driven by China’s 2025 dual-catalog reform that shielded innovative agents from volume-based price cuts. Tucidinostat has enjoyed NRDL presence since 2017 and new lymphoma approvals, while Japan’s April 2025 price cut still leaves room for uptake in its aging population.

Europe trails but could accelerate if the EMA clears resminostat for cutaneous T-cell lymphoma mid-2025, based on the RESMAIN study’s 8.3-month progression-free survival. Conditional givinostat approval in June 2025 adds non-oncology depth that may unlock reimbursement conversations in member states.

Competitive Landscape

Four approved agents dominate current prescribing: vorinostat, romidepsin, belinostat, and panobinostat, while fifteen clinical-stage programs jostle for orphan designations. Large pharma has shed pan-HDAC assets, as illustrated by Novartis and Bristol exits, whereas biotech entrants are pursuing isoform-selective playbooks. Celgene’s February 2026 Acetylon pact shows that big-cap acquirers still see combination leverage in selective inhibition.

Regional champions include Chipscreen, riding Chinese reimbursement, and 4SC, which awaits the EMA verdict on resminostat. Pipeline diversity extends to pulmonary vascular and fibrotic diseases through Cereno's assets, broadening the addressable patient population beyond relapsed hematologic niches. Pharmacogenomic dosing and controlled-release matrices are next-generation differentiation levers, but high trial costs and survival-endpoint mandates temper speed to market.

HDAC Inhibitors Industry Leaders

Novartis AG

Bristol Myers Squibb

Merck & Co., Inc

Shenzhen Chipscreen Biosciences Co., Ltd.

Acrotech Biopharma LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Purdue Pharma and the Global Coalition for Adaptive Research (GCAR) announced the activation of tinostamustine in the GBM AGILE trial for patients with newly diagnosed glioblastoma.

- November 2025: Novelwise Pharmaceutical Corporation initiated studies to determine optimal dosing for this investigational HDAC inhibitor in patients with metastatic uveal melanoma

- May 2025: Amylyx Pharmaceuticals reported positive Week 48 data from its Phase II HELIOS trial for adults with Wolfram syndrome.

Global HDAC Inhibitors Market Report Scope

As per the scope of the report, histone deacetylase (HDAC) inhibitors are a significant class of compounds that function as epigenetic modifiers by blocking the removal of acetyl groups from histones and non-histone proteins. In a healthy cellular state, the balance between histone acetyltransferases (HATs), which add acetyl groups to loosen chromatin for gene transcription, and HDACs, which remove them to condense chromatin and silence genes, is tightly regulated.

The HDAC inhibitors market is segmented by drug class, application, route of administration, distribution channel, and geography. Based on drug class, the market is segmented into hydroxamic acid derivatives, cyclic peptides, benzamides, HDAC6-selective inhibitors, and short-chain fatty acids. By applications, the market is segmented into oncology, neurology, and others. Based on the route of administration, the market is segmented into oral, intravenous, and topical. Based on the distribution channel, the market is segmented into hospital pharmacies, retail & specialty pharmacies, and online pharmacies.

Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Hydroxamic Acid Derivatives |

| Cyclic Peptides |

| Benzamides |

| HDAC6-Selective Inhibitors |

| Short-Chain Fatty Acids |

| Oncology |

| Neurology |

| Others |

| Oral |

| Intravenous |

| Topical |

| Hospital Pharmacies |

| Retail & Specialty Pharmacies |

| Online pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of APAC | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of MEA | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Hydroxamic Acid Derivatives | |

| Cyclic Peptides | ||

| Benzamides | ||

| HDAC6-Selective Inhibitors | ||

| Short-Chain Fatty Acids | ||

| By Application | Oncology | |

| Neurology | ||

| Others | ||

| By Route of Administration | Oral | |

| Intravenous | ||

| Topical | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail & Specialty Pharmacies | ||

| Online pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of APAC | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of MEA | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is revenue growing for HDAC inhibitors between 2026 and 2031?

Sales are projected to rise from USD 1.5 billion to USD 2.4 billion, delivering a 9.11% CAGR over the five-year span.

Which drug class currently holds the largest commercial footprint?

Hydroxamic acid derivatives captured 62.5% of 2025 revenue, supported by entrenched use of vorinostat, belinostat, and panobinostat.

Why is Asia-Pacific the fastest-growing region?

China’s 2025 reimbursement reform protected innovative epigenetic drugs from deep price cuts, lifting volume and sustaining price realization.

What did the 2026 Celgene–Acetylon deal signify?

The USD 100 million upfront payment validated industry belief that isoform-selective inhibitors can unlock chronic, non-oncology markets.

Page last updated on: