Proton Pump Inhibitors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

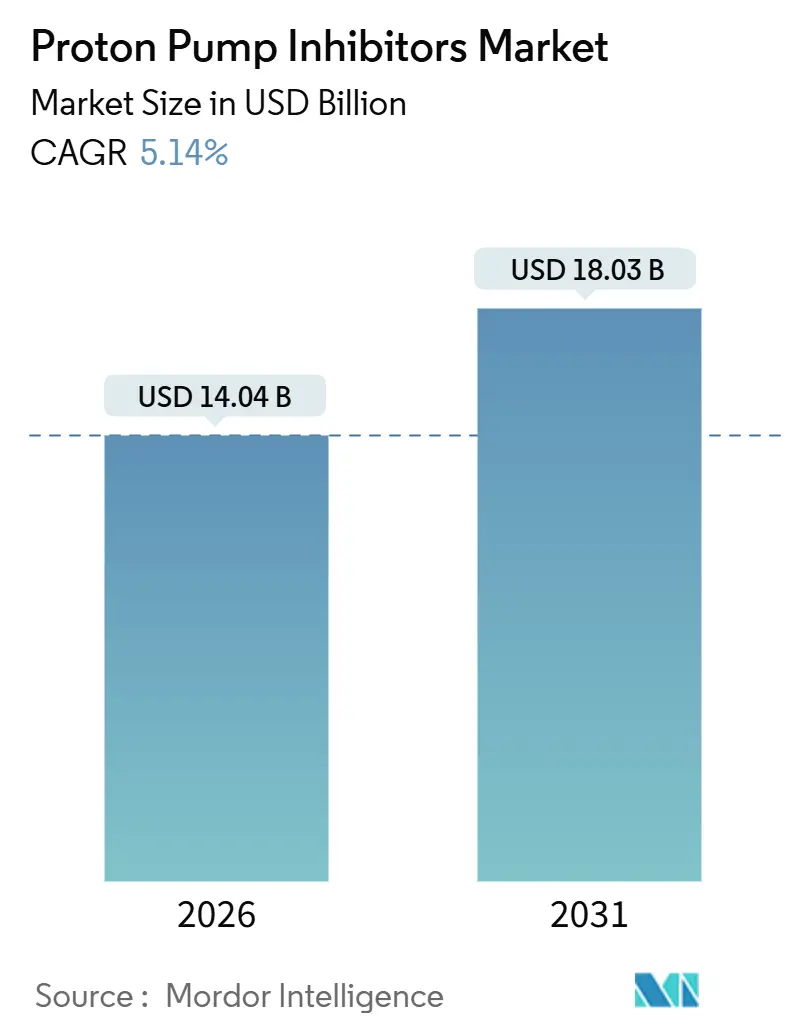

| Market Size (2026) | USD 14.04 Billion |

| Market Size (2031) | USD 18.03 Billion |

| Growth Rate (2026 - 2031) | 5.14% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Proton Pump Inhibitors Market Analysis by Mordor Intelligence

The Proton Pump Inhibitors Market size is estimated at USD 14.04 billion in 2026, and is expected to reach USD 18.03 billion by 2031, at a CAGR of 5.14% during the forecast period (2026-2031).

Current dynamics are shaped by falling branded prices after patent expiries, rapid adoption of intravenous formulations in critical-care wards, and mounting demand from post-operative bariatric patients who require high-dose acid suppression. Expanded over-the-counter (OTC) access, coupled with self-medication trends, has broadened consumer reach, though it simultaneously compresses unit margins. In parallel, undiagnosed gastroesophageal reflux disease (GERD) remains prevalent across the Asia-Pacific, where rising disposable income and aggressive generic manufacturing are accelerating prescription volumes. While mature demand in North America and Western Europe stabilizes aggregate revenue, growth corridors in India, China, and selected Middle East markets are redefining competitive focus.

Key Report Takeaways

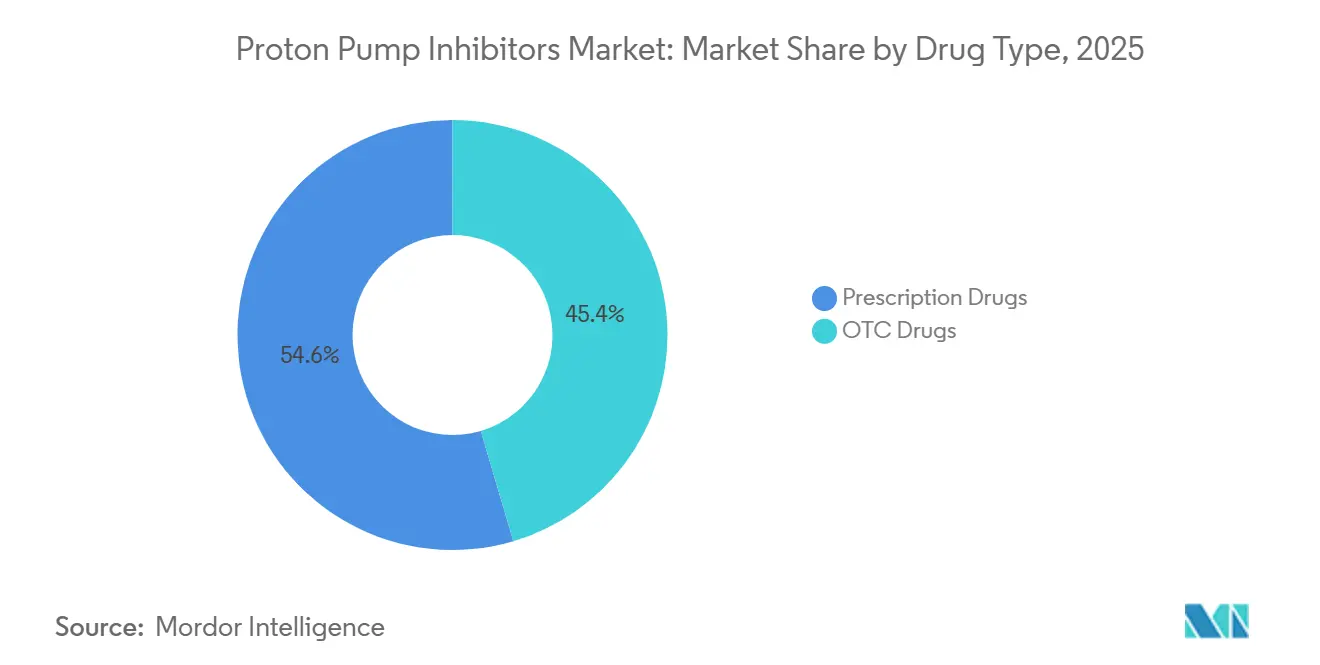

- By drug type, OTC formulations held 45.43% of the proton pump inhibitors market share in 2025, while prescription drugs are projected to advance at a 7.54% CAGR through 2031.

- By route of administration, oral products captured 58.65% share of the proton pump inhibitors market size in 2025, whereas the intravenous segment is projected to expand at a 7.65% CAGR through 2031.

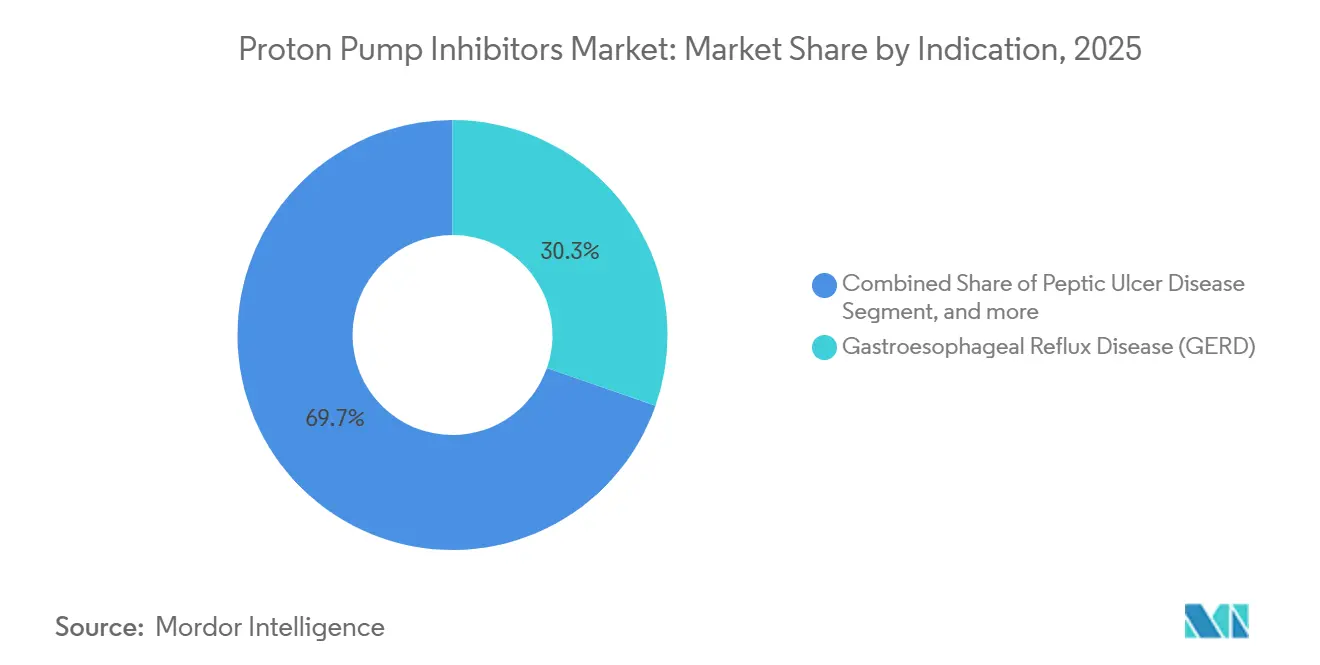

- By indication, gastroesophageal reflux disease led with a 30.34% revenue share in 2025; Zollinger-Ellison syndrome treatments are projected to grow at an 8.01% CAGR through 2031.

- By distribution channel, hospital pharmacies accounted for 60.34% of the proton pump inhibitors market size in 2025; however, online pharmacies recorded the fastest CAGR of 8.32% for the same period.

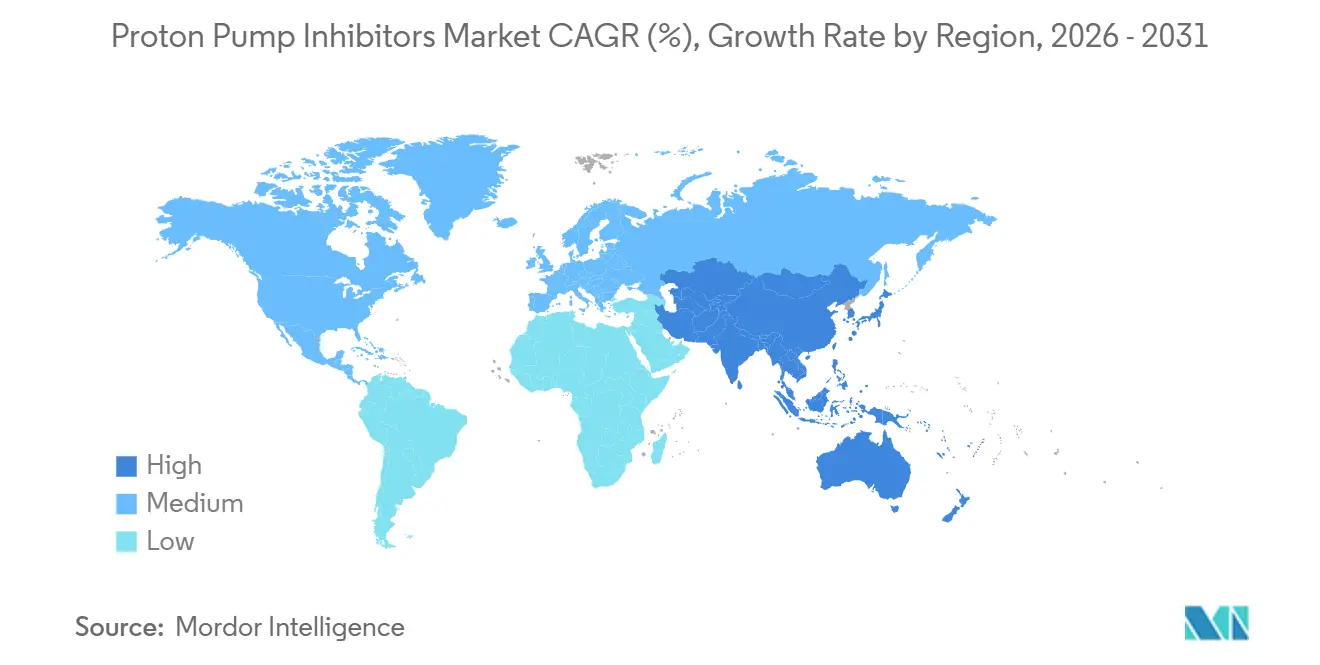

- By geography, North America retained 42.65% proton pump inhibitors market share in 2025, while Asia-Pacific is pacing ahead with a 6.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Proton Pump Inhibitors Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population with higher G.I. disorder prevalence | +0.9% | Global, peak impact in North America, Europe, Japan | Long term (≥ 4 years) |

| Increasing burden of GERD and peptic ulcer disease | +1.2% | Global, pronounced in Asia-Pacific urban centers | Medium term (2-4 years) |

| Expanded OTC switches and self-medication trends | +0.7% | North America and leading EU states, emerging in Latin America | Short term (≤ 2 years) |

| Growing availability of low-cost generics in emerging markets | +1.0% | Asia-Pacific core, spill-over to Middle East and South America | Medium term (2-4 years) |

| Rising prevalence of bariatric surgery requiring post-operative acid suppression | +0.5% | North America, Western Europe, select Middle East hubs | Medium term (2-4 years) |

| Adoption of quadruple H. pylori therapies incorporating PPIs | +0.6% | Global, highest uptake in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population with Higher G.I. Disorder Prevalence

Older adults experience double the incidence of reflux symptoms and peptic complications compared with younger cohorts. Declining lower esophageal sphincter tone, polypharmacy-induced mucosal injury, and the prevalence of hiatal hernia compound this risk. The worldwide population aged 60 years and above is on track to exceed 1.4 billion by 2030, with Asia-Pacific driving the steepest gains[1]World Health Organization, “Ageing and Health,” who.int. This demographic surge elevates prescription volumes because elderly patients often need higher or prolonged dosing due to reduced acid clearance and concurrent NSAID therapy.

Increasing Burden of GERD And Peptic Ulcer Disease

Urbanization and dietary Westernization have pushed global GERD prevalence to roughly 13%, while metropolitan Asia has climbed from historical baselines below 5% to more than 10%[2]Nature Communications, “Global Trends in Gastroesophageal Reflux Disease,” nature.com. Peptic ulcer disease persists among chronic NSAID users, a cohort expanding alongside aging populations. The result is split demand: low-dose short courses for uncomplicated GERD versus high-dose prolonged regimens for ulcer management, favoring firms with diverse dosage strengths.

Expanded OTC Switches and Self-Medication Trends

Regulatory reclassifications enable consumers to purchase 20 mg esomeprazole and pantoprazole without a prescription across much of Europe[3]European Medicines Agency, “Nexium Control Product Information,” ema.europa.eu. In the United States, OTC omeprazole and lansoprazole are the most prevalent medications on retail shelves. While broad access boosts unit volumes, it compresses margins and raises concerns over unsupervised chronic use, prompting regulators to strengthen label warnings and duration limits.

Growing Availability of Low-Cost Generics in Emerging Markets

Vertically integrated manufacturers in India and China supply omeprazole and pantoprazole at less than USD 0.10 per daily dose, thereby challenging the originator's pricing power. Licensing models, such as Takeda’s non-exclusive vonoprazan agreements, monetize intellectual property via royalties instead of direct commercialization, accelerating penetration but squeezing per-unit revenues.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety concerns over long-term PPI use | -0.8% | Global, highest regulatory scrutiny in North America and EU | Medium term (2-4 years) |

| Patent expiries leading to price erosion | -1.1% | Global, pronounced in North America and Europe | Short term (≤ 2 years) |

| Preference shift toward potassium-competitive acid blockers | -0.4% | Japan, South Korea, early adoption in U.S. specialty channels | Long term (≥ 4 years) |

| Regulatory scrutiny on OTC labeling and duration limits | -0.3% | North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Safety Concerns Over Long-Term PPI Use

A 2024 observational study linked chronic exposure to proton pump inhibitors to higher risks of acute interstitial nephritis, progression of chronic kidney disease, and vitamin B12 deficiency, with hazard ratios ranging from 1.3 to 1.8. The resulting FDA and EMA warnings have prompted physicians to adopt step-down protocols and on-demand dosing, thereby shortening the average treatment duration per patient.

Patent Expiries Leading to Price Erosion

Loss of exclusivity for esomeprazole, pantoprazole, and lansoprazole triggered average selling price declines of 60-80% within two years. The first U.S. generic pantoprazole injection secured FDA clearance in 2024, introducing competition to a segment that had long sheltered premium pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Prescription Therapies Deliver Faster Growth

The prescription segment contributed a smaller base in 2025, yet is forecast to grow at 7.54% annually through 2031, driven by higher-dose requirements for Zollinger-Ellison syndrome and H. pylori eradication. Health-insurance formularies often subsidize prescriptions more heavily than OTC purchases, indirectly steering patients toward clinician-directed therapy. Conversely, the larger OTC block faces intensifying competition from private-label generics that pressure average selling prices. Regulatory OTC switches broadened access but shifted channel economics toward thin margins, obliging manufacturers to balance volume gains against profitability.

Lifecycle management remains pivotal for prescription brands. Combination products pairing proton pump inhibitors with NSAIDs or antibiotics extend protection periods and command higher reimbursement. Regulatory agencies encourage such formulations when evidence supports superior adherence or safety, thereby reinforcing the relevance of branded products even as core molecules lose exclusivity.

By Route Of Administration: Intravenous Use Rises in Critical Care

Oral formulations still account for 58.65% of the 2025 volume, benefiting from their convenience and widespread use in chronic GERD. However, intravenous (IV) demand is rising at a 7.65% CAGR due to stress-ulcer prophylaxis protocols in intensive-care units and post-operative settings that require rapid acid suppression when oral intake is compromised. Hospitals negotiate bulk IV contracts directly with suppliers, often securing steep discounts in exchange for formulary exclusivity, yet the higher complexity of sterile manufacturing creates barriers that favor established producers. Approval of generic pantoprazole injection in 2024 marked a market tipping point that is expected to shift purchasing criteria from brand preference to cost efficiency.

By Indication: GERD Dominates, Zollinger-Ellison Accelerates

GERD held a 30.34% share in 2025, driven by high global prevalence and consumer familiarity with proton pump inhibitors for symptom relief. Zollinger-Ellison syndrome, though rare, is registering the fastest growth rate at 8.01% as diagnostic tools improve and specialized centers screen at-risk patients more effectively. These patients require significantly higher daily doses, boosting revenue per capita despite small volumes. Peptic ulcer disease and H. pylori eradication together remain sizable, supported by protocol-driven quadruple therapies that guarantee fixed treatment windows and predictable demand.

By Distribution Channel: Hospital Pharmacies Still Lead, Online Surges

Hospital pharmacies controlled 60.34% of global sales in 2025, reflecting their role in procuring IV formulations and enforcing standardized protocols. Channel growth moderates as outpatient care expands, yet hospital formularies continue to wield significant negotiating power, favoring suppliers able to bundle IV and oral SKUs. Online pharmacies, although smaller today, are expanding at a rate of 8.32% because telehealth platforms facilitate discreet, subscription-based refills. Regulatory endorsement of electronic prescriptions and verified digital pharmacy certifications mitigates concerns about counterfeit risk, encouraging wider consumer adoption.

Geography Analysis

North America commanded 42.65% global share in 2025, supported by high health-care expenditure and entrenched prescribing habits. FDA safety communications in 2024 tempered chronic use, but did not materially impact overall volume, as clinicians continued to prioritize ulcer prophylaxis in high-risk populations. Canada’s tighter reimbursement rules modestly curtail long-term therapy, chiefly by requiring endoscopic confirmation to extend scripts beyond eight weeks.

The Asia-Pacific region is the fastest-growing, with a 6.43% CAGR projected to 2031. Rising GERD prevalence, escalating middle-class incomes, and extensive generic production underpin this momentum. Indian and Chinese manufacturers leverage cost advantages to widen access, while licensing deals for vonoprazan demonstrate an originator pivot to royalty-based models that suit price-sensitive markets. Regulatory clearance by India’s Drug Controller General for multiple vonoprazan indications confirms an environment conducive to the rapid uptake of this medication.

Europe’s trajectory remains steady but slower, curtailed by stringent EMA labeling that limits the length of self-medication and mandates step-down protocols. The EU’s 2024 delegated regulation on variation procedures eases administrative burdens for label harmonization, potentially accelerating the introduction of reformulated products.

The Middle East and Africa are at an earlier stage of adoption. Gulf Cooperation Council nations expand private insurance coverage, supporting the uptake of premium-branded products in urban hospitals. At the same time, sub-Saharan Africa focuses on essential medicine lists that prioritize low-cost, generic medications. South America exhibits uneven progress, with macroeconomic volatility in Brazil and Argentina impacting price negotiations; nevertheless, large, under-treated patient pools offer long-term upside for cost-efficient suppliers.

Competitive Landscape

The proton pump inhibitors market is moderately fragmented. The top five companies—AstraZeneca, Takeda, Pfizer, Sun Pharmaceutical Industries, and Cipla—hold a combined share of approximately 45–50%. Originators defend legacy brands through lifecycle extensions such as fixed-dose combinations and novel delivery systems, while generic players compete on manufacturing scale and unit cost. Takeda’s decision to license vonoprazan to multiple Indian partners exemplifies a pivot to royalty-stream models in low-price environments. Phathom Pharmaceuticals advanced differentiation via Voquezna, targeting non-erosive reflux disease in the United States with a potassium-competitive mechanism that bypasses competition from traditional PPIs. Fresenius Kabi’s entry into IV generics intensifies hospital segment pricing pressure, yet underscores sustained demand for acute care formulations.

Strategic opportunities reside in securing hospital supply contracts for IV drugs, bundling PPIs with telehealth adherence platforms, and investing in next-generation mechanisms that offer faster onset or superior drug-interaction profiles. Early-stage disruptors focusing on potassium-competitive molecules or alternative acid blockers could reshape market dynamics if clinical superiority translates into reimbursement support.

Proton Pump Inhibitors Industry Leaders

Bayer AG

Pfizer Inc.

Takeda Pharmaceuticals

Cadila Pharmaceuticals

AstraZeneca

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Eisai Co., Ltd. launched “Pariet S,” the First Proton Pump Inhibitor RX-to-OTC. It is a medication for severe heartburn and stomach pain caused by gastric acid reflux. The product is available at pharmacies and drugstores across Japan.

- July 2024: Phathom Pharmaceuticals received FDA approval for its VOQUEZNA (vonoprazan) 10 mg tablets for treating heartburn related to Non-Erosive GERD in adults. This marked the third FDA approval for VOQUEZNA, which is already approved for Erosive Esophagitis and H. pylori eradication. The approval addresses a significant portion of the U.S. GERD patient population.

- August 2024: BHA (British Horseracing Authority) announced updated regulations allowing horses to receive oral proton pump inhibitors, such as omeprazole, up to raceday. These medications can be administered prior to race day but must not be given on raceday until after the horse has run. This change aims to improve gastric ulcer management while ensuring fair racing conditions.

Global Proton Pump Inhibitors Market Report Scope

According to the report's scope, proton pump inhibitors (PPIs) are a class of drugs that primarily inhibit the long-term reduction of gastric acid production. They are the most potent inhibitors of acid secretion available.

The Proton Pump Inhibitors Market is Segmented by Drug Type (OTC Drugs and Prescription Drugs), Route of Administration (Oral and Intravenous), Indication (GERD, Peptic Ulcer Disease, H. Pylori Eradication, Zollinger-Ellison Syndrome, and Other Indications), Distribution Channel (Hospital Pharmacies, Retail Pharmacies & Drug Stores, and Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| OTC Drugs | Omeprazole |

| Lansoprazole | |

| Esomeprazole | |

| Other OTC Drugs | |

| Prescription Drugs | Rabeprazole |

| Dexlansoprazole | |

| Pantoprazole | |

| Other Prescription Drugs |

| Oral |

| Intravenous |

| Gastroesophageal Reflux Disease (GERD) |

| Peptic Ulcer Disease |

| H. Pylori Eradication |

| Zollinger-Ellison Syndrome |

| Other Indications |

| Hospital Pharmacies |

| Retail Pharmacies & Drug Stores |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East And Africa | GCC |

| South Africa | |

| Rest Of Middle East And Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Drug Type | OTC Drugs | Omeprazole |

| Lansoprazole | ||

| Esomeprazole | ||

| Other OTC Drugs | ||

| Prescription Drugs | Rabeprazole | |

| Dexlansoprazole | ||

| Pantoprazole | ||

| Other Prescription Drugs | ||

| By Route Of Administration | Oral | |

| Intravenous | ||

| By Indication | Gastroesophageal Reflux Disease (GERD) | |

| Peptic Ulcer Disease | ||

| H. Pylori Eradication | ||

| Zollinger-Ellison Syndrome | ||

| Other Indications | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies & Drug Stores | ||

| Online Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East And Africa | GCC | |

| South Africa | ||

| Rest Of Middle East And Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How large is the proton pump inhibitors market in 2026?

It stands at USD 14.04 billion with a forecast to reach USD 18.03 billion by 2031.

What is the projected CAGR for proton pump inhibitors between 2026 and 2031?

The market is expected to expand at a 5.14% CAGR over the forecast period.

Which route of administration is growing fastest within proton pump inhibitor therapies?

Intravenous formulations are advancing at a 7.65% CAGR, reflecting rising critical-care use.

Which geographic region shows the strongest growth momentum?

Asia-Pacific leads with a projected 6.43% CAGR through 2031 driven by generic uptake and rising GERD prevalence.

What safety issues are regulators emphasizing for long-term proton pump inhibitor users?

Agencies highlight risks such as kidney injury, vitamin B12 deficiency, hypomagnesemia, and potential infection increases, prompting shorter treatment durations.

How are next-generation acid blockers influencing competitive dynamics?

Potassium-competitive acid blockers like vonoprazan and tegoprazan offer faster onset and meal-independent dosing, gradually capturing share from traditional proton pump inhibitors.

Page last updated on: