Fetal Heart Rate Monitoring Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

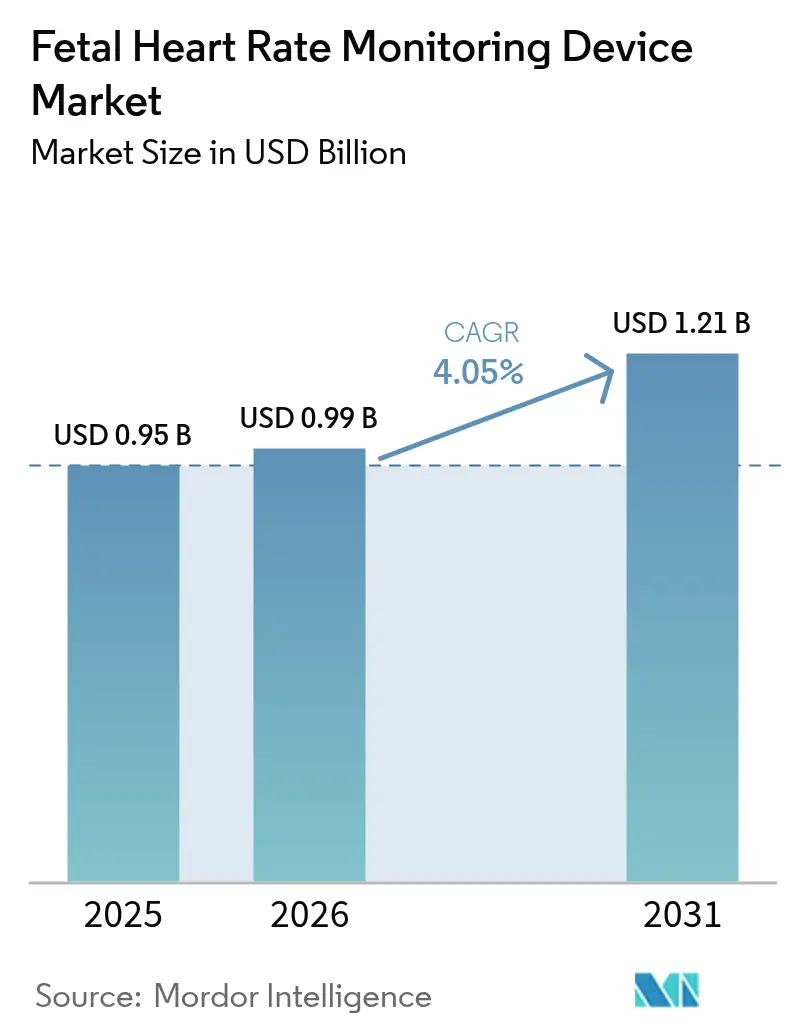

| Market Size (2026) | USD 0.99 Billion |

| Market Size (2031) | USD 1.21 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fetal Heart Rate Monitoring Device Market Analysis by Mordor Intelligence

The fetal heart rate monitoring devices market size was valued at USD 0.95 billion in 2025 and estimated to grow from USD 0.99 billion in 2026 to reach USD 1.21 billion by 2031, at a CAGR of 4.05% during the forecast period (2026-2031). Steady gains stem from rising global births, widening adoption of wireless patch monitors, and expanding government spending on maternal health, especially in Asia-Pacific where multi-tier public hospitals modernize perinatal care. Demand also benefits from defensive medicine practices in North America that favor comprehensive surveillance to mitigate litigation risk. Technology suppliers concentrate on AI-driven signal cleaning, interoperability, and cloud connectivity rather than price, reflecting provider preference for diagnostic accuracy over cost cutting. Portable and wearable platforms catalyze new revenue streams in home monitoring programs reimbursed under tele-obstetric codes, while stringent multi-region device approvals and patchy reimbursement regimes temper growth in certain emerging markets.

Key Report Takeaways

- By product type, external monitors led with 63.68% revenue share in 2025; wearable patch-based devices are projected to expand at an 10.62% CAGR to 2031.

- By technology, Doppler ultrasound held 50.94% of fetal heart rate monitoring devices market share in 2025, while fetal electrocardiography is set to grow at an 11.18% CAGR through 2031.

- By portability, mobile systems accounted for 62.10% share of the fetal heart rate monitoring devices market size in 2025 and will advance at a 8.74% CAGR to 2031.

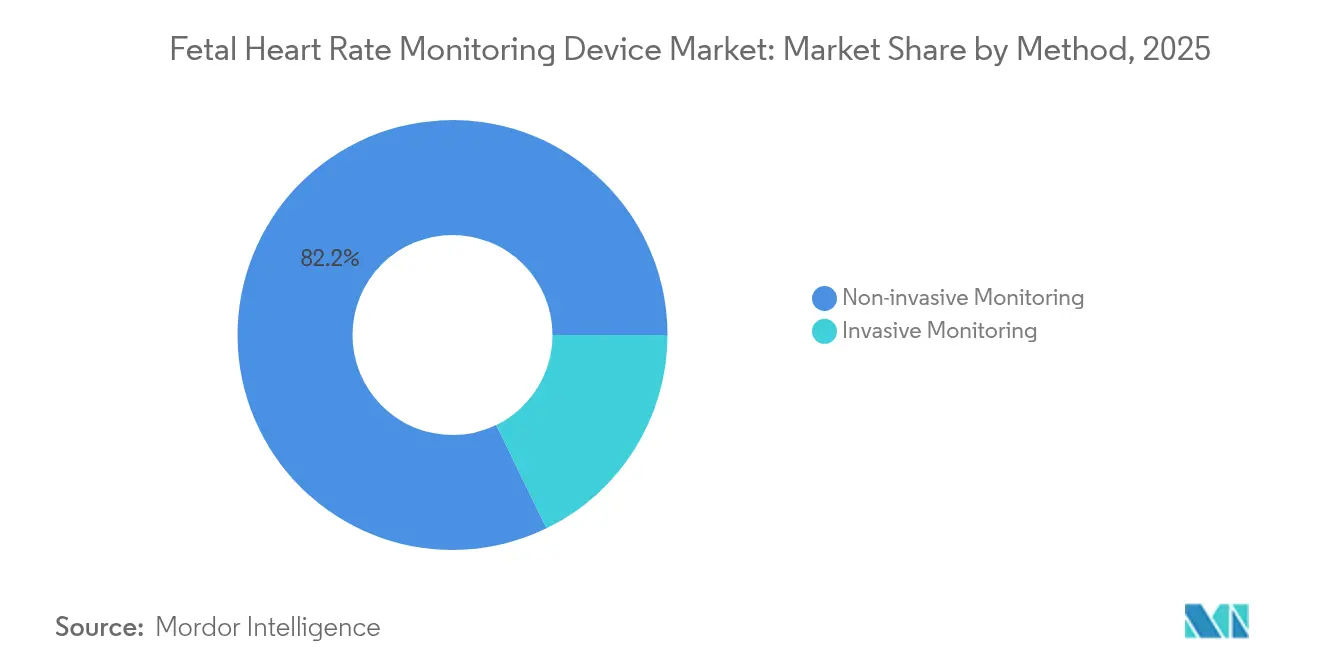

- By method, non-invasive solutions dominated with 82.20% share in 2025; invasive approaches remain confined to high-risk deliveries.

- By end user, hospitals owned 64.75% of demand in 2025, whereas home-care settings record the fastest 10.93% CAGR to 2031.

- By geography, North America led with 42.10% revenue share in 2025 and Asia-Pacific is forecast to expand at a 8.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fetal Heart Rate Monitoring Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological Breakthroughs In Wireless & Wearable Monitors | +1.2% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Rising Global Birth-Rate & Pre-Term Deliveries | +0.8% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Government & NGO Maternal-Health Programs | +0.7% | Global, concentrated in emerging markets | Long term (≥ 4 years) |

| Surge In Home-Use Doppler Adoption | +0.6% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| AI-Driven Signal-Cleaning Cuts False Positives | +0.5% | Global, led by developed markets | Short term (≤ 2 years) |

| Tele-Obstetric Reimbursement Expansion | +0.4% | North America, selective EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technological Breakthroughs in Wireless & Wearable Monitors

Wireless patch monitors allow continuous tracking without restricting maternal mobility. GE HealthCare’s Novii+ waterproof patch captures fetal heart rate, maternal heart rate, and uterine activity from 34 weeks gestation, maintaining signal integrity across body-mass indices[1]GE HealthCare, “Novii Wireless Patch System Fetal Monitor,” gehealthcare.com. Philips’ Avalon CL system, rapidly cleared during the COVID-19 emergency, accelerated hospital adoption of cordless pods that reduce nurse repositioning time. Hospitals report higher patient comfort scores and shorter admission-to-delivery intervals, reinforcing reimbursement incentives tied to satisfaction metrics. Remote data streaming to electronic medical records aligns with value-based care models that reward timely clinical decisions. The trend also supports the shift toward decentralized labor suites configured for family-centered birthing experiences.

Rising Global Birth-Rate & Pre-Term Deliveries

Asia-Pacific facilities face increasing institutional deliveries as urban families choose hospital births. China’s 26,000-facility maternal network guarantees 90% of households a clinic within 15 minutes, boosting equipment installations. Roughly 15 million annual pre-term births need continuous fetal surveillance, lifting demand for high-acuity monitors. A University of Helsinki study of 214,000 births linked external monitoring plus maternal pulse recording to lower neonatal encephalopathy incidence. Evidence-based guidelines consequently broaden monitoring protocols in secondary hospitals across India and Indonesia, supporting further device uptake.

Government & NGO Maternal-Health Programs

WHO’s 2025 World Health Day theme “Healthy beginnings, hopeful futures” mobilizes funding to curb 300,000 annual maternal deaths. UNFPA’s 2025-2030 strategy highlights digital tools for prenatal surveillance, guiding procurement toward interoperable monitors[2]United Nations Population Fund, “Start with Her: UNFPA Strategy for Reproductive, Maternal and Newborn Health and Well-Being 2025–2030,” unfpa.org. Mozambique’s community health program, supported by WHO and UNICEF, trains workers on essential childbirth monitoring, spurring grassroots demand for durable Doppler units. These initiatives channel grant financing to local clinics, reducing upfront capital barriers.

AI-Driven Signal Cleaning Reduces False Positives

Artificial intelligence tackles misinterpretation and high cesarean rates linked to cardiotocography. Mayo Clinic researchers built an AI-enabled stethoscope that doubled peripartum cardiomyopathy diagnostic accuracy. The Society for Maternal-Fetal Medicine showed AI improved congenital heart-defect detection in routine scans, aiding facilities with limited fetal cardiology expertise. BrightHeart’s 2024 FDA clearance for AI ultrasound software signals regulatory trust in algorithmic tools. As 95.5% of obstetricians practice defensive medicine amid malpractice fears, technologies that cut false alarms carry strong purchasing appeal.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-region device approvals | -0.9% | Global; most severe in EU post-MDR | Long term (≥ 4 years) |

| High capex & uneven reimbursement | -0.7% | Worldwide; acute in emerging markets | Medium term (2-4 years) |

| CTG-linked litigation risk | -0.5% | North America & EU | Long term (≥ 4 years) |

| Cloud-platform data privacy concerns | -0.3% | Global; strictest in EU under GDPR | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Region Device Approvals

Divergent regulatory regimes raise development costs and prolong time-to-market. The EU Medical Device Regulation imposes rigorous clinical evidence and post-market surveillance, while the FDA’s 2024 Quality System Regulation amendments align with ISO 13485 yet introduce new documentation layers. Japan demands domestic clinical datasets, straining foreign entrants. User fees that reach USD 365,657 for premarket approvals weigh heavily on start-ups, limiting diversity in the fetal heart rate monitoring devices market[3]Federal Register, “Medical Devices; Quality System Regulation Amendments,” federalregister.gov.

High Capex & Patchy Reimbursement

Full-featured bedside monitors cost hospitals more than USD 40,000 per unit, while reimbursement pathways lag technological advances. NIH’s Reimbursement Knowledge Guide notes that FDA clearance does not guarantee payer coverage. Aetna labels home uterine activity monitoring experimental, blocking payment for many outpatient programs. Cigna only funds remote physiologic devices with automated data transmission, excluding low-end Dopplers. Consequently, some hospitals defer upgrades or shift purchasing to lower-spec models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: External Monitors Retain Primacy, Wearables Surge

External devices generated 63.68% of 2025 revenues, underscoring entrenched clinician confidence in belt-based Doppler and CTG systems. The fetal heart rate monitoring devices market size for external monitors is poised to rise at a conservative 3.32% CAGR as replacement demand follows typical seven-year capital cycles. Wearable patches, though niche in absolute dollars, log an 10.62% CAGR as midwives embrace cable-free mobility that shortens labor-room turnovers. Masimo’s over-the-counter Stork monitor illustrates regulatory momentum toward consumer-friendly prenatal tracking. Hospitals integrate patches into hybrid workflows—initial triage on belts followed by patches to maintain surveillance during ambulation. Internal scalp electrodes conserve a small share for complicated labors requiring direct R-wave acquisition.

User comfort and workflow efficiency drive preference shifts. Wearables eliminate gel reapplication and belt adjustments, reducing nurse workload during peak delivery periods. INVU’s cloud platform lets physicians review live traces from remote clinics, widening access in obstetric deserts. Academic prototypes such as Electric Potential Sensing promise gel-free external ECG, signaling a longer-term pathway for non-adhesive wearables. As reimbursement codes coalesce around home monitoring, suppliers position subscription models bundling hardware, analytics, and teleconsulting.

By Technology Type: Doppler Dominates, Fetal ECG Accelerates

Doppler ultrasound retained 50.94% share in 2025, benefiting from well-established training curricula and ubiquitous repair networks. Nonetheless, the fetal electrocardiography (FECG) segment records an 11.18% CAGR through 2031 as objective waveform analysis addresses observer variability fears. The fetal heart rate monitoring devices market share held by Doppler is expected to dip marginally as tertiary centers pilot multichannel FECG combined with AI prediction modules. Huntleigh’s 2025 CTG Analysis clearance demonstrates continued Doppler software refinement rather than hardware displacement.

Clinical evidence fuels FECG momentum. Literature reviews highlight reduced false alarms and clearer arrhythmia detection compared with Doppler. Yet upfront costs and learning curves confine adoption to high-risk units. Magnetocardiography remains restricted to research owing to shielded facility requirements and multimillion-dollar price tags. CTG stays routine for twin gestations where dual fetal heart tracing is necessary, and newer algorithms now auto-segregate signals even with overlapping heart rates.

By Portability: Mobile Platforms Anchor Both Present and Future Growth

Portable monitors captured 62.10% of 2025 sales and post a 8.74% CAGR, indicating the dual advantage of incumbency and expansion. Battery life exceeding 10 hours and Wi-Fi connectivity permit continuous observation outside traditional labor wards, crucial for mid-wife-led birthing centers. Melody International’s iCTG, deployed across 16 nations, illustrates the global reach of handheld fetal ECG-plus-Doppler hybrids. Non-portable consoles persist in high-dependency units where integration with central monitoring dashboards outweighs mobility considerations.

The trend aligns with hospital redesigns that favor single-room maternity suites. Portable devices accompany expectant mothers from triage through postpartum recovery, reducing device hand-offs that risk data gaps. Emerging epidermal biosensors detailed in Nature Communications suggest an eventual continuum wherein ultrathin patches feed data to bedside monitors or smartphones without disconnection. Suppliers respond by embedding Bluetooth Low Energy and WPA3 encryption to satisfy cybersecurity audits.

By Method: Non-Invasive Techniques Maintain Market Command

Non-invasive monitoring held 82.20% of 2025 revenue and expands at 7.83% CAGR as safety and patient experience remain paramount. The fetal heart rate monitoring devices market size for non-invasive solutions benefits from AI algorithms that filter maternal heart interference, narrowing the accuracy gap with invasive electrodes. Invasive methods, while indispensable in meconium-stained or obese cases where external signals degrade, see flat demand due to specialist staffing requirements.

Clinical debates continue. An Ethiopian cohort showed continuous EFM increased cesarean frequency without neonatal benefit in low-risk pregnancies. Conversely, high-risk centers cite FECG’s real-time ST-segment analysis for intrapartum hypoxia detection. Industry R&D thus pursues hybrid systems: adhesive electrodes activated only upon external signal loss, minimizing unnecessary invasiveness while preserving backup capability.

By End User: Hospitals Lead, Home Monitoring Climbs

Hospitals generated 64.75% of 2025 demand, anchored by mandatory intrapartum surveillance protocols. Home-care channels, however, register an 10.93% CAGR as public and private payers widen tele-obstetric reimbursement. CMS policy updates in late 2024 reward virtual prenatal consultation models that rely on patient-operated Dopplers streaming data to clinicians. Specialty clinics employ hybrid pathways—initial visits onsite, followed by remote assessments for low-risk cases—reducing travel burdens for rural populations.

Consumer trust hinges on data security. HIPAA rule changes tighten encryption mandates for reproductive health information, prompting manufacturers to certify end-to-end encryption stacks. Japan’s MamaWell program integrates wearable vitals with midwife chat support, illustrating insurer-sponsored tele-monitoring models in advanced economies. As remote prenatal episodes rise, platform providers bundle analytics dashboards, user training, and 24/7 helplines to satisfy payer quality metrics.

Geography Analysis

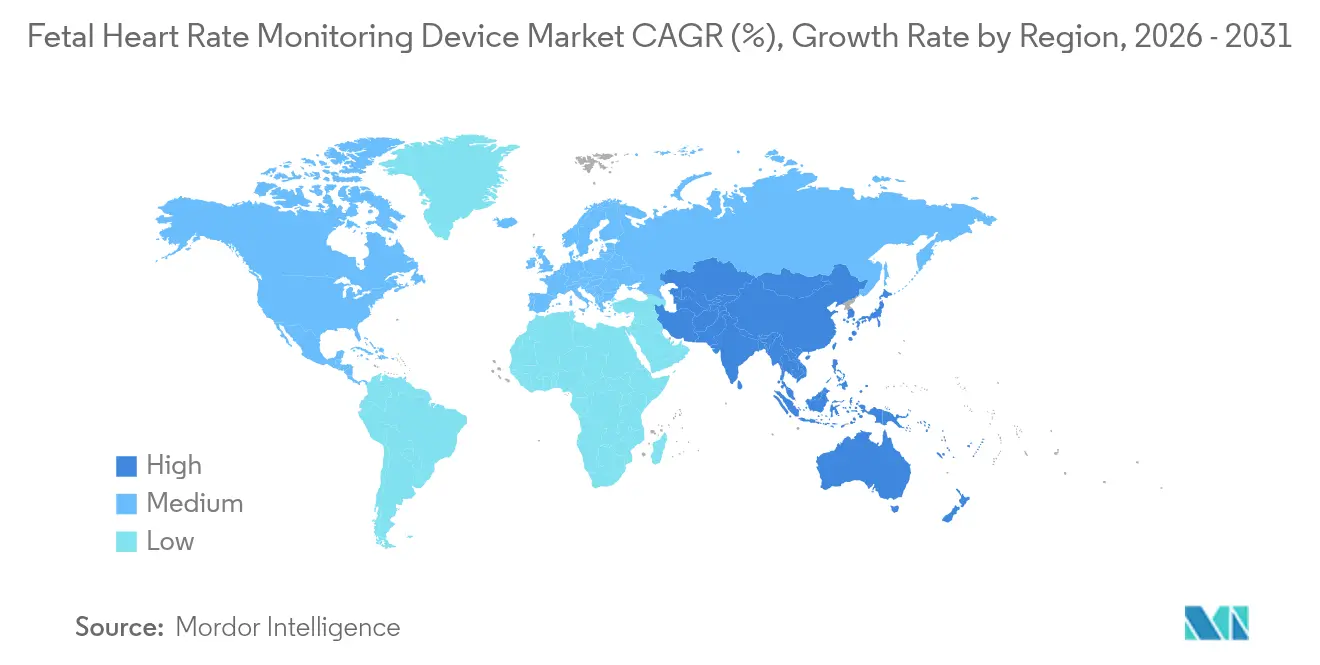

North America accounted for 42.10% of 2025 revenue due to comprehensive Medicare and private-payer coverage policies that absorb capital costs for next-generation monitors. High malpractice awards, exemplified by a USD 120 million verdict over delayed cesarean, keep hospitals vigilant about trace quality and documentation. Federal initiatives to reduce maternal deaths incentivize procurement of AI-enhanced systems, while tightened HIPAA provisions bolster confidence in cloud storage. Vendor service contracts prioritizing uptime protect against ransomware incidents flagged by the proposed Security Rule revisions.

Asia-Pacific is the fastest-growing region with a 8.71% CAGR through 2031, propelled by demographic pressures and large-scale public health investments. China’s maternal network ensures near-universal physical access, and hospital accreditation upgrades require modern fetal monitors. India’s Ayushman Arogya Mandirs integrate fetal monitoring into primary care, supported by National Health Mission funding. Regional start-ups leverage low-cost mobile CTG to serve rural clinics without mains electricity, broadening the addressable customer base. Nonetheless, varied device approval timelines and fragmented reimbursement slow uniform adoption.

Europe maintains moderate expansion as MDR compliance lengthens product refresh cycles. Hospitals weigh investment in AI-equipped monitors against budget constraints imposed by national health systems. GDPR influences system design: suppliers incorporate on-premise servers or EU-hosted clouds to meet data-sovereignty rules. Scandinavian pilot projects such as Norway’s Mum-Care smartphone app illustrate the region’s embrace of digital prenatal support, yet commercialization hinges on multicountry reimbursement alignment. Middle-East and Africa see pockets of innovation; Jordan’s digital reproductive health registry shows data-driven service planning, while Ugandan midwives apply AI ultrasound to offset specialist shortages.

Competitive Landscape

Leading suppliers rely on broad product portfolios, proprietary analytics, and hospital integration expertise rather than price undercutting. GE HealthCare’s seven-year partnership with Sutter Health rolls out AI-powered maternal-infant imaging across 24 facilities, demonstrating value-added service strategies. Philips embeds Avalon monitors into enterprise dashboards that unify obstetric, neonatal, and anesthesia data streams.

Challenger firms pursue niche opportunities. Nuvo collaborates with maternal-fetal medicine practices to embed its INVU wearable into tele-prenatal pathways, bundling per-patient subscription fees. Melody International targets humanitarian and disaster-relief markets with solar-charging handheld CTG. BrightHeart and Huntleigh secure FDA nods for software-only solutions, signaling a shift toward algorithm-centric competition. Cybersecurity emerges as a differentiator; hospitals increasingly demand ISO 27001-certified cloud platforms as ransomware attacks threaten patient safety.

M&A activity remains selective as established players acquire AI analytics firms to accelerate feature roadmaps. Venture funding gravitates to start-ups that combine sensor innovation with reimbursement-ready service models. Regional OEMs in India and China compete on cost but face export limitations under stricter post-market surveillance rules. Overall, competitive dynamics hinge on technology validation and regulatory compliance breadth more than on manufacturing scale.

Fetal Heart Rate Monitoring Device Industry Leaders

GE Healthcare

Siemens Healthineers

MedGyn Products Inc.

Cooper Companies, Inc

Fujifilm Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Huntleigh Healthcare received FDA 510(k) clearance for its CTG Analysis device, confirming safety and effectiveness for intrapartum monitoring.

- November 2024: BrightHeart obtained FDA 510(k) clearance for prenatal ultrasound software that enhances fetal heart rate assessment accuracy.

Global Fetal Heart Rate Monitoring Device Market Report Scope

As per the scope of the report, fetal heart rate monitoring refers to the process of measuring the heart rate and rhythm of the fetus during late pregnancy and labor to monitor and check the condition of the fetus with special equipment. The monitoring helps healthcare professionals to identify any risk factors earlier and reassure normal conditions.

The fetal heart rate monitoring device market is segmented by product type (internal fetal heart rate monitoring device and external fetal heart rate monitoring device), technology type (Doppler ultrasound device and electronic fetal monitoring device), portability of device (portable and non-portable), and geography (North America, Europe, Asia-Pacific, and Rest of the World). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the aforementioned segments.

| Internal FHR Monitoring Devices |

| External FHR Monitoring Devices |

| Wearable Patch-based Monitors |

| Remote/Home-use Doppler Monitors |

| Doppler Ultrasound Devices |

| Electronic Fetal Monitoring (CTG) |

| Fetal Electrocardiography (FECG) |

| Magnetocardiography |

| Portable Devices |

| Non-portable Devices |

| Non-invasive Monitoring |

| Invasive Monitoring |

| Hospitals |

| Specialty Maternity Clinics |

| Home-care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Internal FHR Monitoring Devices | |

| External FHR Monitoring Devices | ||

| Wearable Patch-based Monitors | ||

| Remote/Home-use Doppler Monitors | ||

| By Technology Type | Doppler Ultrasound Devices | |

| Electronic Fetal Monitoring (CTG) | ||

| Fetal Electrocardiography (FECG) | ||

| Magnetocardiography | ||

| By Portability | Portable Devices | |

| Non-portable Devices | ||

| By Method | Non-invasive Monitoring | |

| Invasive Monitoring | ||

| By End User | Hospitals | |

| Specialty Maternity Clinics | ||

| Home-care Settings | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the fetal heart rate monitoring devices market?

The market is worth USD 0.99 billion in 2026 and is projected to reach USD 1.21 billion by 2031 at a 4.05% CAGR.

Which technology segment is growing the fastest?

Fetal electrocardiography leads growth with an 11.18% CAGR owing to superior signal accuracy and reduced observer variability.

Why are wearable patch monitors gaining traction?

They allow continuous, cable-free monitoring, enhance maternal comfort, and integrate seamlessly with tele-obstetric reimbursement frameworks.

Which region shows the highest growth potential?

Asia-Pacific records the fastest 8.71% CAGR driven by large birth cohorts and heavy public investment in maternal health infrastructure.

How do regulatory changes affect market entrants?

Stringent EU MDR and elevated FDA user fees increase compliance costs and lengthen approval timelines, especially for small manufacturers.

Page last updated on: