Global Cardiac Pacemakers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

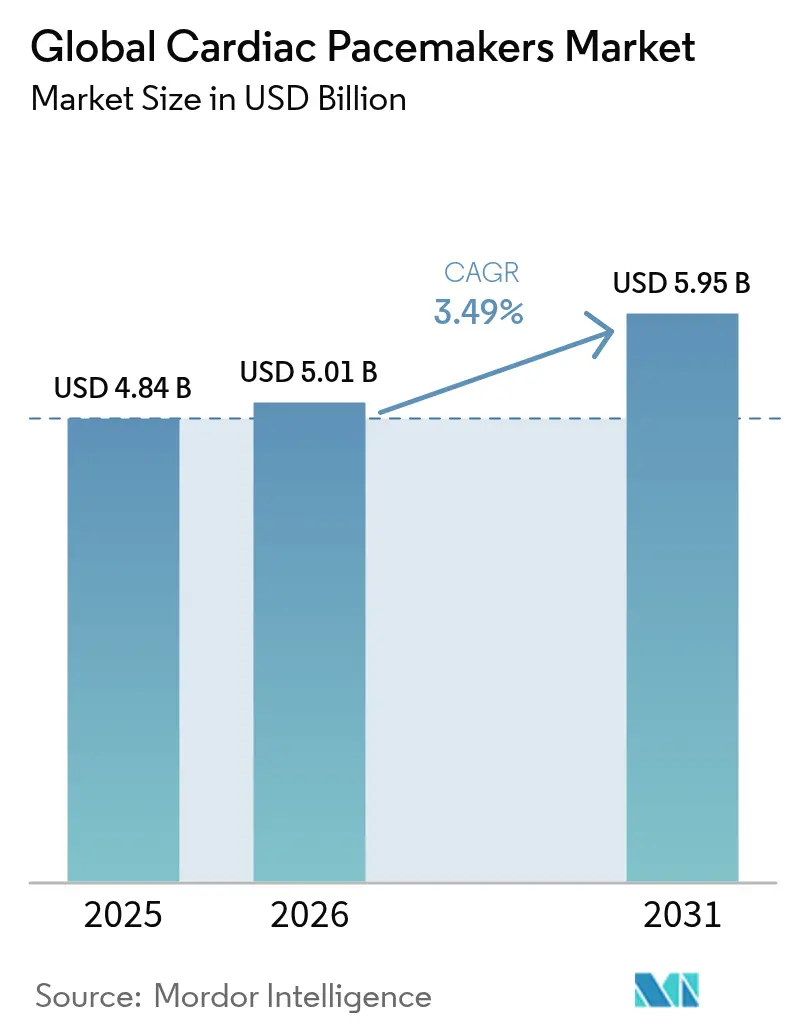

| Market Size (2026) | USD 5.01 Billion |

| Market Size (2031) | USD 5.95 Billion |

| Growth Rate (2026 - 2031) | 3.49% CAGR |

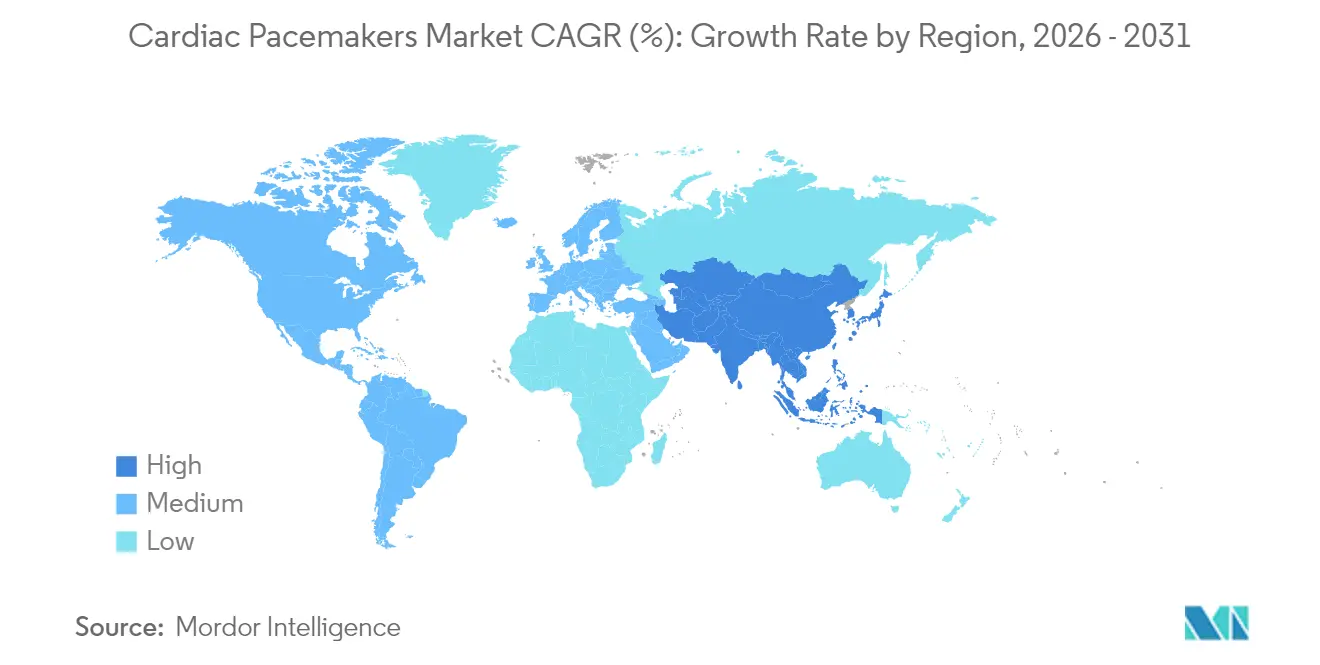

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Cardiac Pacemakers Market Analysis by Mordor Intelligence

The cardiac pacemaker market size is expected to grow from USD 4.84 billion in 2025 to USD 5.01 billion in 2026 and is forecast to reach USD 5.95 billion by 2031 at 3.49% CAGR over 2026-2031. Growth stems from a steadily enlarging elderly population, rising incidence of bradyarrhythmia and heart block, and a decisive shift from hardware-driven volume gains to software-enabled performance upgrades that emphasize leadless designs, MRI-conditional platforms, and AI-guided programming [1]Source: American Heart Association, “Heart Disease and Stroke Statistics 2025,” heart.org . North America continues to lead the cardiac pacemaker market through robust reimbursement schemes that accelerate adoption of premium technology, while Asia-Pacific shows the quickest uptake as governments fund wider access and local manufacturers enter value tiers. Dual-chamber systems remain the clinical workhorse, yet leadless devices and physiologic pacing concepts are rapidly eroding the incumbent’s dominance, marking the market’s evolution toward minimally invasive, extraction-free solutions. Competitive positioning hinges on end-to-end ecosystems that combine devices, remote monitoring, analytics, and cybersecurity safeguards. Meanwhile, supply chain shortages in tantalum and microchips, combined with stringent FDA cybersecurity rules, add complexity and cost pressures to an otherwise resilient demand landscape.

Key Report Takeaways

- By geography, North America held 38.22% of the cardiac pacemaker market share in 2025; Asia-Pacific is advancing at a 5.45% CAGR through 2031.

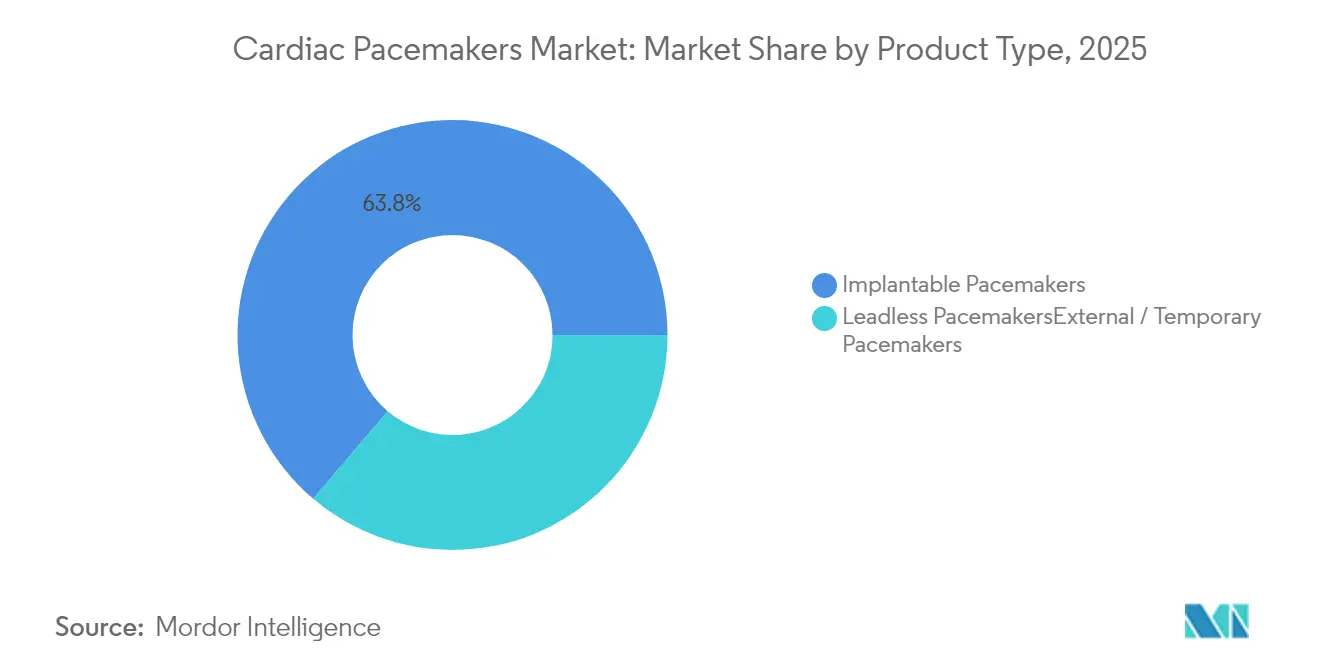

- By product type, implantable pacemakers led with 63.78% revenue share in 2025, while leadless devices post the fastest 5.42% CAGR to 2031.

- By technology, dual-chamber platforms accounted for 45.05% share of the cardiac pacemaker market size in 2025; leadless technology registers the highest 5.42% CAGR to 2031.

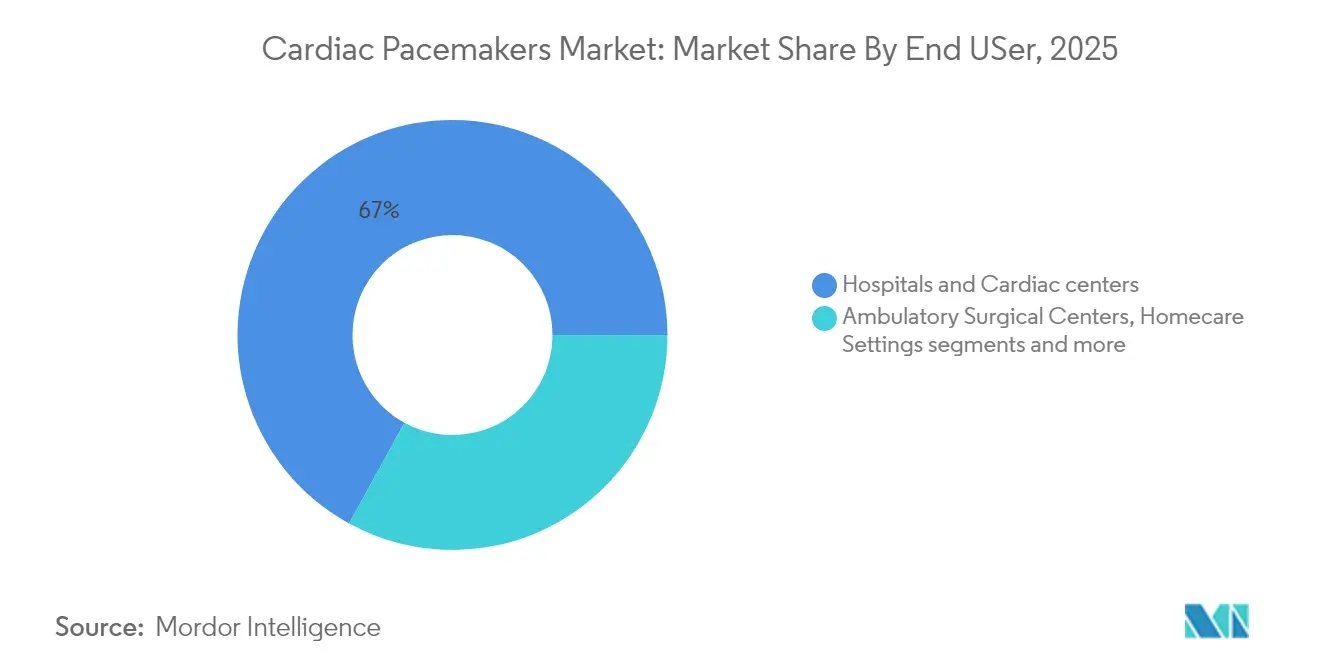

- By end user, hospitals and cardiac centers commanded 67.02% of the cardiac pacemaker market size in 2025; ambulatory surgical centers are expanding at a 5.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cardiac Pacemakers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of bradyarrhythmia & heart block | 0.80% | Global, higher in aging North America and Europe | Long term (≥ 4 years) |

| Growing elderly population | 0.70% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Advancements in MRI-conditional & leadless devices | 0.60% | North America & EU leading, APAC accelerating | Medium term (2-4 years) |

| AI-driven pacemaker programming platforms | 0.40% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Reimbursement expansion for remote monitoring | 0.30% | North America primary, EU selective markets | Short term (≤ 2 years) |

| Emerging-market governmental tender programs | 0.20% | APAC core, Latin America and MEA selective | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Bradyarrhythmia & Heart Block

Epidemiological studies project atrioventricular block cases to climb 41%, moving from 378,816 individuals in 2020 to 535,076 by 2060, propelled by an aging global population and widespread cardiovascular risk factors. Complete heart block constitutes 76% of permanent pacemaker indications in clinical registries, ensuring persistent demand across all product classes. Concomitant rises in atrial fibrillation—from a 24.2% to 30.9% lifetime risk between 2000 and 2022—further expand the candidate pool for pacing therapy as conduction disorders supervene. Mortality tied to sick sinus syndrome has also climbed among seniors, highlighting the need for timely intervention. Survival data underscore pacemaker benefit, with paced patients experiencing 2.7-fold higher survival than untreated counterparts in severe bradycardia cohorts.

Growing Elderly Population

Cardiovascular disease is forecast to affect 61% of US adults by 2050, reinforcing the structural tailwind behind the cardiac pacemaker market. The ≥85-year cohort already represents over 40% of US implants and is on track to triple by 2060. Outcome analyses reveal that conduction-system pacing maintains equivalent efficacy across age groups, debunking concerns over geriatric procedural risk. Health systems respond by building geriatric cardiology units and refining device selection for frail patients, with leadless options showing particular appeal in reducing infection risk. Long-term care considerations increasingly guide payer and clinician preference toward systems offering longevity and low maintenance demands.

Advancements in MRI-Conditional & Leadless Devices

Five-year data confirm that leadless pacemakers deliver safety and efficacy on par with conventional models while eliminating lead-related complications. Abbott’s AVEIR DR platform achieved 95% mean atrioventricular synchrony across postures, demonstrating full functional equivalence to dual-chamber systems. MRI-conditional status is now standard, exemplified by BIOTRONIK’s Amvia Edge, which auto-activates MRI mode and removes cumbersome reprogramming. Medtronic’s upgraded Micra boasts 40% greater battery life, extending predicted service to 17 years and potentially making lifetime single-implant therapy realistic. As retrieval proficiency and longitudinal datasets accumulate, physicians increasingly view leadless technology as first-line rather than niche.

AI-Driven Pacemaker Programming Platforms

Artificial intelligence reshapes follow-up models by curbing false alarms and predicting decompensation. Medtronic’s AccuRhythm AI cuts erroneous atrial fibrillation alerts 88.2% while preserving 99% of true events, freeing clinicians from 400+ hours of review time per 200 patients each year. FDA clearance for Implicity’s SignalHF heart-failure algorithm illustrates regulatory momentum for predictive analytics that offer two-week early warning of worsening status. Algorithms trained on more than 1 million rhythm episodes elevate diagnostic specificity, trimming unnecessary interventions without sacrificing safety. Seamless integration with electronic health records completes a closed-loop workflow that delivers decision support, documentation, and billing efficiency in a single pass.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device cost in low-income regions | -0.90% | APAC emerging markets, Latin America, MEA | Long term (≥ 4 years) |

| Device-related complications & recalls | -0.40% | Global, higher where regulation is strict | Short term (≤ 2 years) |

| Supply-chain shortage of tantalum & semiconductors | -0.30% | Global production hubs | Medium term (2-4 years) |

| Evolving cybersecurity compliance burden | -0.20% | North America & EU first, expanding global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Device Cost in Low-Income Regions

Unit prices of USD 2,500-3,000 lock many patients out of treatment in emerging economies, where implant rates hover at 4 devices per million compared with 782 per million in developed France heart.. Cost barriers translate into an estimated 1 million preventable deaths each year, and 27% of indicated patients in resource-limited settings remain untreated. Device reuse programs report safety parity with new implants but face regulatory hesitancy and cultural resistance . Government tenders, philanthropic donations, and tiered pricing bring some relief, yet sustainable solutions depend on fundamental cost innovation, local assembly, and supply chain rationalization. The Pan-African Society of Cardiology’s device reuse initiative highlights what can be achieved when regulatory, clinical, and industry stakeholders align heart.

Device-Related Complications & Recalls

Boston Scientific’s Class I recall of 203,000 Accolade units, linked to premature battery depletion that caused 832 injuries and 2 deaths, underlines quality risks that erode clinician confidence and inflate lifetime therapy costs. Longitudinal surveillance shows device complication rates mounting from 8% at nine years to 49% at 11 years for particular cohorts, spotlighting the burden of late-stage failures hrsonline.org. Management expenditure can equal the cost of a fresh implant, pressuring payers and patients alike. Regulatory agencies have reacted by tightening post-market vigilance and cementing cybersecurity compliance as a core design requirement. Industry answers with predictive analytics, smarter battery chemistries, and more rigorous supplier audits, but reputational damage lingers and can influence physician brand choices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Leadless Innovation Drives Premium Segment

Implantable systems captured 63.78% revenue in 2025, underscoring their entrenched position across broad clinical indications ihrs.co.in. However, leadless models post the highest 5.42% CAGR and are eroding share as physicians gravitate toward minimally invasive options with lower complication profiles. Single-chamber implantables remain standard for straightforward bradycardia, whereas dual-chamber configurations dominate complex atrioventricular conditions. Biventricular resynchronization pacing serves heart-failure cohorts with conduction delays, a specialized group yet one that benefits from increasingly compact hardware designs. Temporary and external pacemakers fill acute postoperative or emergency gaps, ensuring continuity of care until permanent implantation is feasible.

Leadless expansion marks a structural pivot within the cardiac pacemaker market, buoyed by data showing 98.3% procedural success and 97% synchronization in Abbott’s AVEIR DR trial. Form-factor reductions, battery gains, and retrieval enhancements collectively sharpen value, while Northwestern University’s dissolvable devices hint at future pediatric and short-term opportunities sciencenews.org. As value-based care pressures intensify, payers welcome the elimination of pocket- and lead-related revisions, positioning leadless technology as a cost-effective choice over a lifetime horizon.

By Technology: Dual-Chamber Dominance Challenged by Leadless Innovation

Dual-chamber pacing accounted for 45.05% of 2025 revenue, reflecting its capacity to maintain atrioventricular synchrony and avoid pacemaker syndrome acc.org. Yet the 5.42% CAGR logged by leadless systems signals a transitional era in which form factor, infection avoidance, and MRI compatibility override historic preference. Single-chamber devices remain vital for ventricular-only indications or chronic atrial fibrillation, whereas cardiac resynchronization therapy populates the heart-failure niche. Rate-responsive sensors that tailor output to physiologic demand are increasingly embedded across all categories, improving quality of life for active patients.

Physiologic pacing, including conduction-system methods, gains traction following the European Society of Cardiology’s 2025 guidance that frames left bundle branch pacing as a viable alternative to right ventricular leads. Medtronic’s OmniaSecure 4.7 F lead validates the approach, securing 100% defibrillation success in bundle branch placement while preserving future venous access. Such breakthroughs imply incremental share erosion for legacy platforms as physicians reorient toward technologies that replicate native conduction pathways.

By End User: Hospital Dominance with ASC Growth Acceleration

Hospitals and cardiac centers owned 67.02% of 2025 revenue, supported by multidisciplinary teams and the ability to handle complex cases and emergent complications ncbi.nlm.nih.gov. Ambulatory surgical centers post the fastest 5.71% CAGR, catalyzed by same-day discharge protocols enabled by smaller incisions and fewer post-operative restrictions, especially with leadless systems. Homecare settings leverage remote monitoring to manage follow-up, while academic institutes drive clinical trial enrollment and physician training, maintaining a steady yet modest revenue share.

Tighter reimbursement environments spur hospitals to shift lower-risk cases to outpatient channels, freeing in-patient capacity and trimming costs. Medicare policies that reimburse remote patient monitoring create financial underpinnings that allow ambulatory centers to provide comprehensive aftercare. As outcome data normalize outpatient safety, insurers broaden coverage, accelerating volume away from inpatient suites. Consequently, device manufacturers refine training kits and workflow tools tailored to ASC settings, further energizing the shift.

Geography Analysis

North America remains the leading revenue generator, holding 38.22% share in 2025, anchored by sophisticated payer frameworks, high public awareness, and early adoption of AI-enabled remote monitoring cms.gov. Medicare’s separate payments for pacing leads and real-time monitoring sustain technology uptake, while FDA fast-track pathways foster rapid commercialization of breakthroughs such as dual-chamber leadless systems and predictive analytics engines. Canadian and Mexican public health programs are widening access through bulk tenders that favor value-based procurement, nudging manufacturers to present lifecycle economics rather than sticker price alone.

Europe leverages cohesive reimbursement systems and strong clinical guideline influence from entities such as the European Society of Cardiology, driving homogeneity in practice standards. Germany, France, and the United Kingdom lead implantation volumes thanks to robust electrophysiology networks and high per-capita diagnostic rates. Brexit has introduced trade documentation friction, but parallel regulatory frameworks continue to recognize CE-marked pacemakers, ensuring patient access. Over the medium term, EU Medical Device Regulation (MDR) will demand deeper post-market surveillance, pushing smaller manufacturers to partner or exit due to compliance overhead.

Asia-Pacific provides the fastest 5.45% CAGR to 2031, propelled by aging demographics, urban lifestyle disease, and government initiatives that expand cardiac device reimbursement. China’s reformed National Medical Products Administration (NMPA) process expedites foreign device approvals, while its volume-based procurement program negotiates prices down, enlarging installed base penetration cisema.com. India confronts cost obstacles yet shows rising implant numbers as public-private partnerships fund indigent care, especially in tier-2 cities pubmed.ncbi.nlm.nih.gov. Japan and South Korea sustain high per-capita implant rates due to universal coverage and tech-savvy specialists, while Australia and Singapore act as regional testbeds for AI-driven screening programs.

The Middle East and Africa trail in volume but offer latent opportunity as cardiac disease burden climbs and public health policies pivot toward noncommunicable disease management. Government-led tenders in Saudi Arabia and the United Arab Emirates allocate budget for modern pacing technologies, and philanthropic device reuse programs are reducing waitlists in sub-Saharan regions heart. Latin America shows mixed progress as Brazil and Mexico modernize their electrophysiology capacity while smaller economies wrestle with currency volatility that complicates import financing.

Competitive Landscape

The cardiac pacemaker market demonstrates moderate consolidation, with Medtronic, Abbott, and Boston Scientific holding the lion’s share through broad portfolios that span implantables, leadless devices, diagnostics, and software. These firms deploy steady R&D outlays exceeding 8% of cardiac segment revenue to safeguard technological edge, focusing on longevity gains, physiologic pacing, and AI harmonization. Abbott’s AVEIR suite, which integrates conduction-system and dual-chamber leadless pacing, secured breakthrough device designation, underscoring the firm’s innovation momentum.

Competition increasingly revolves around integrated ecosystems that fuse hardware reliability with software intelligence. Medtronic’s CareLink and AccuRhythm platforms exemplify the strategy by delivering predictive analytics within a secure cloud workspace, a capability that locks in providers through workflow entrenchment. Boston Scientific, while navigating legacy recall fallout, is doubling down on dual-therapy synergies that merge pacing with novel ablation technologies, aiming to provide end-to-end arrhythmia care pipelines. BIOTRONIK differentiates via automatic MRI mode devices, opening avenues in geographies that mandate universal MRI compatibility.

Strategic alliances and acquisitions extend competitive reach into specialist niches. PaceMate’s purchase of Medtronic’s Paceart Optima system aggregates nearly 1,000 monitoring hubs, highlighting the convergence of device and data management players. EBR Systems’ WiSE wireless CRT implant introduces direct competition in heart-failure pacing, a segment historically dominated by lead-based solutions. Further, local manufacturers in China and India are scaling cost-efficient production to serve domestic reimbursement ceilings, applying pressure on multinational pricing strategies without yet matching premium-tier technology.

Global Cardiac Pacemakers Industry Leaders

Medtronic PLC

Biotronik SE & Co. KG

Boston Scientific Corporation

Lepu Medical Co . Ltd

Abbott Laboratories (ST Jude Medical)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: EBR Systems obtained FDA approval for the WiSE wireless CRT system, slated for US launch in early 2026.

- May 2025: Edwards Lifesciences received FDA clearance to expand SAPIEN 3 TAVR indications to asymptomatic severe aortic stenosis, potentially lifting pacemaker demand post-procedure

- April 2025: Medtronic secured FDA approval for the OmniaSecure 4.7 F defibrillation lead following 100% success in left bundle branch trials

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the cardiac pacemakers market as all newly manufactured implantable, leadless, and external generators that deliver timed electrical impulses to regulate brady- or tachy-arrhythmic heart rates; accessories, disposables, replacement leads, and CRT-defibrillators sit outside this boundary, so revenue from those items has not been counted.

Scope exclusion: Internal cardioverter-defibrillators, CRT-D devices, and aftermarket service contracts remain beyond the present valuation.

Segmentation Overview

- By Product Type

- Implantable Pacemakers

- Single Chamber Implantable

- Dual Chamber Implantable

- Biventricular / CRT-P

- Leadless Pacemakers

- Leadless PacemakersExternal / Temporary Pacemakers

- External / Temporary Pacemakers

- Implantable Pacemakers

- By Technology

- Single Chamber Technology

- Dual Chamber Technology

- Cardiac Resynchronization Therapy (CRT-P)

- Leadless Technology

- Rate-Responsive Pacemakers

- By End User

- Hospitals & Cardiac Centers

- Ambulatory Surgical Centers

- Homecare Settings

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Cardiac electrophysiologists, biomedical engineers, and purchasing heads across North America, Europe, Asia-Pacific, and the Gulf were interviewed. Their insights let us adjust device life-cycle assumptions, leadless adoption curves, and regional ASP spreads before locking the model.

Desk Research

We began by mapping disease prevalence and procedural volumes drawn from open databases such as the WHO Global Health Observatory, the American Heart Association, Eurostat, and the Japanese MHLW. Regulatory approval logs from the FDA, EMA, and China NMPA helped us time product launches and recall events that shift annual demand.

Next, we layered company 10-Ks, hospital procurement data, clinical-trial registries, and trade-association newsletters, then validated revenue breakouts through paid assets like D&B Hoovers, Dow Jones Factiva, and Questel patent analytics. These illustrate pricing corridors, unit shipments, and pipeline momentum; the list here is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down build starts with country-level implant counts reconstructed from surgical registries and import-export codes, which are then multiplied by verified average selling prices. Supplier roll-ups and sampled distributor checks provide a selective bottom-up cross-check to fine-tune totals. Key variables tracked include diagnosed bradyarrhythmia incidence, geriatric population growth, MRI-safe device penetration rates, public reimbursement ceilings, and lithium battery price trends. A multivariate regression blends these drivers to project 2026-2030 demand; scenarios are stress-tested with primary experts to reflect technology shifts and delayed elective surgeries. Gaps in bottom-up geographies are filled by benchmarking against nearby markets with analogous implant volumes and income levels.

Data Validation & Update Cycle

Before sign-off, analysts run anomaly checks, variance thresholds, and peer reviews; discrepancies trigger re-contact with source respondents. Reports refresh each year, and mid-cycle updates issue when recalls, reimbursement changes, or major product approvals materially move the baseline.

Why Mordor's Cardiac Pacemakers Baseline Inspires Confident Decisions

Published figures often diverge because firms choose dissimilar device baskets, pricing proxies, and refresh cadences. We flag these elements up front so buyers see exactly what is and is not in scope.

Key gap drivers include whether CRT-Ps are blended with pacemakers, the use of list versus blended ASPs, and the frequency with which geriatric population data are updated.

According to Mordor Intelligence, consistent scope selection and annual refreshes narrow uncertainty and keep conversion factors current for every major currency.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.84 B | Mordor Intelligence | |

| USD 5.90 B | Global Consultancy A | Adds CRT devices and replacement leads to core market |

| USD 5.66 B | Industry Association B | Relies solely on hospital procurement, ignores cross-border trade and ASP variation |

Differences show that wider device baskets or single-channel data streams inflate totals. Our disciplined blend of verified volumes, granular pricing, and twice-validated assumptions delivers a balanced, transparent baseline clients can track and replicate with ease.

Key Questions Answered in the Report

What is the current size of the cardiac pacemaker market?

The cardiac pacemaker market was valued at USD 5.01 billion in 2026 and is projected to reach USD 5.95 billion by 2031.

Which region leads the cardiac pacemaker market?

North America leads with 38.22% share in 2025 thanks to strong reimbursement frameworks and rapid adoption of AI-enabled remote monitoring solutions.

Which product segment is growing the fastest?

Leadless pacemakers are expanding at a 5.42% CAGR, the highest among product categories, driven by lower complication rates and improving long-term data.

How are AI platforms impacting pacemaker management?

AI algorithms such as Medtronic’s AccuRhythm reduce false alerts by over 88%, saving hundreds of clinician hours annually and enhancing remote monitoring accuracy.

What are the main restraints facing the market?

High device costs in low-income regions, supply-chain shortages of key materials, and evolving cybersecurity compliance demands are the foremost challenges.

Who are the leading companies in this market?

Medtronic, Abbott, and Boston Scientific collectively hold the largest global shares, with BIOTRONIK and several regional manufacturers making competitive inroads.

Page last updated on: