ECG Patch Holter Monitor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.44 Billion |

| Market Size (2031) | USD 5.99 Billion |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

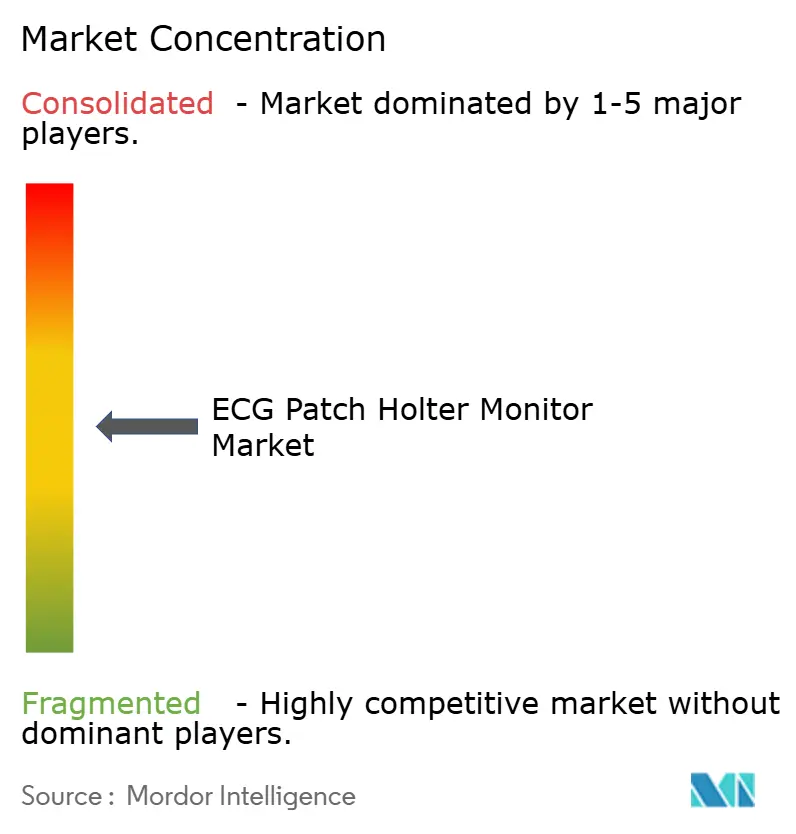

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ECG Patch Holter Monitor Market Analysis by Mordor Intelligence

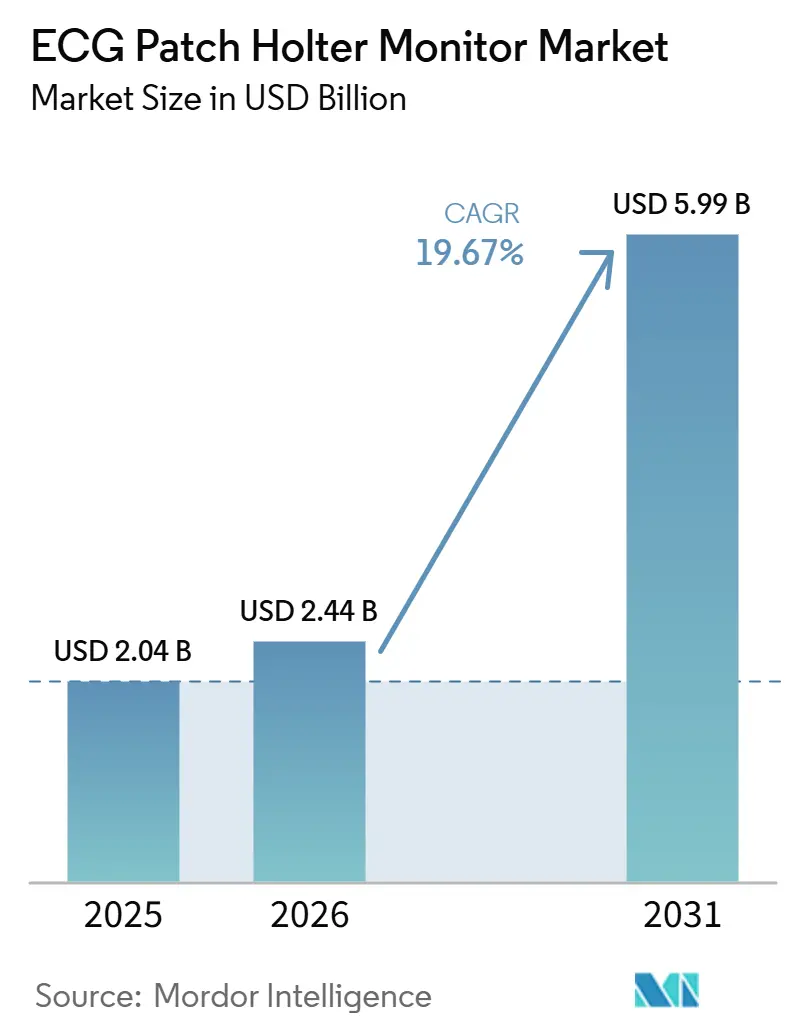

The ECG Patch Holter Monitor Market size is expected to grow from USD 2.04 billion in 2025 to USD 2.44 billion in 2026 and is forecast to reach USD 5.99 billion by 2031 at 19.67% CAGR over 2026-2031.

The ECG patch Holter monitor market is shifting toward longer-duration ambulatory cardiac monitoring as providers adopt continuous solutions that support routine use beyond clinical settings. The rising burden of cardiovascular disease continues to drive demand for scalable monitoring tools, while aging populations in North America, Europe, and East Asia are expanding the patient base for rhythm surveillance. Broader healthcare access, lower device costs, reimbursement updates in the United States, and stricter clinical evidence standards in Europe are supporting adoption and favoring established medical device companies with integrated hardware, analytics, and reporting capabilities. Growth is also supported by outpatient care migration, AI-enabled signal review, and wider monitoring use among patients with diabetes, obesity, chronic kidney disease, and stroke risk.

Key Report Takeaways

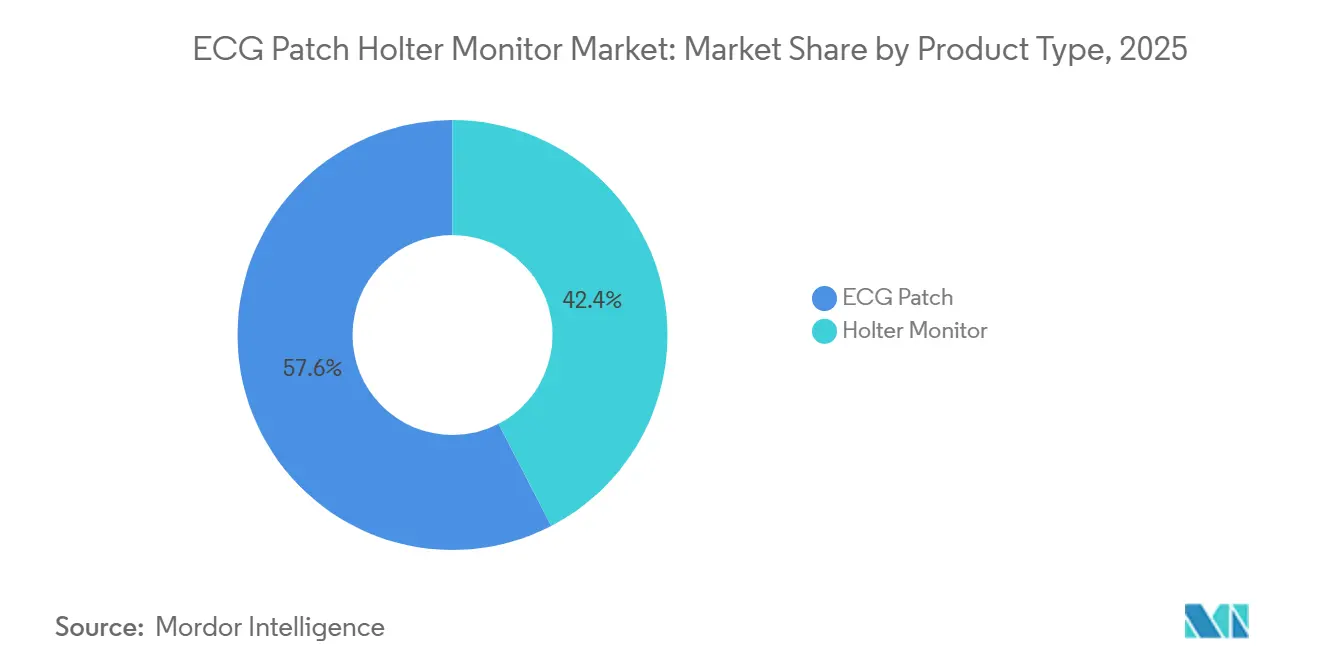

- By product type, ECG patches held 57.60% of the ECG patch Holter monitor market share in 2025, while ECG patches are expected to have the fastest growth at a CAGR of 23.73% through 2031.

- By lead type, 3-lead systems led with 55.55% share in 2025, while 12-lead systems are projected to grow fastest at a CAGR of 21.76% through 2031.

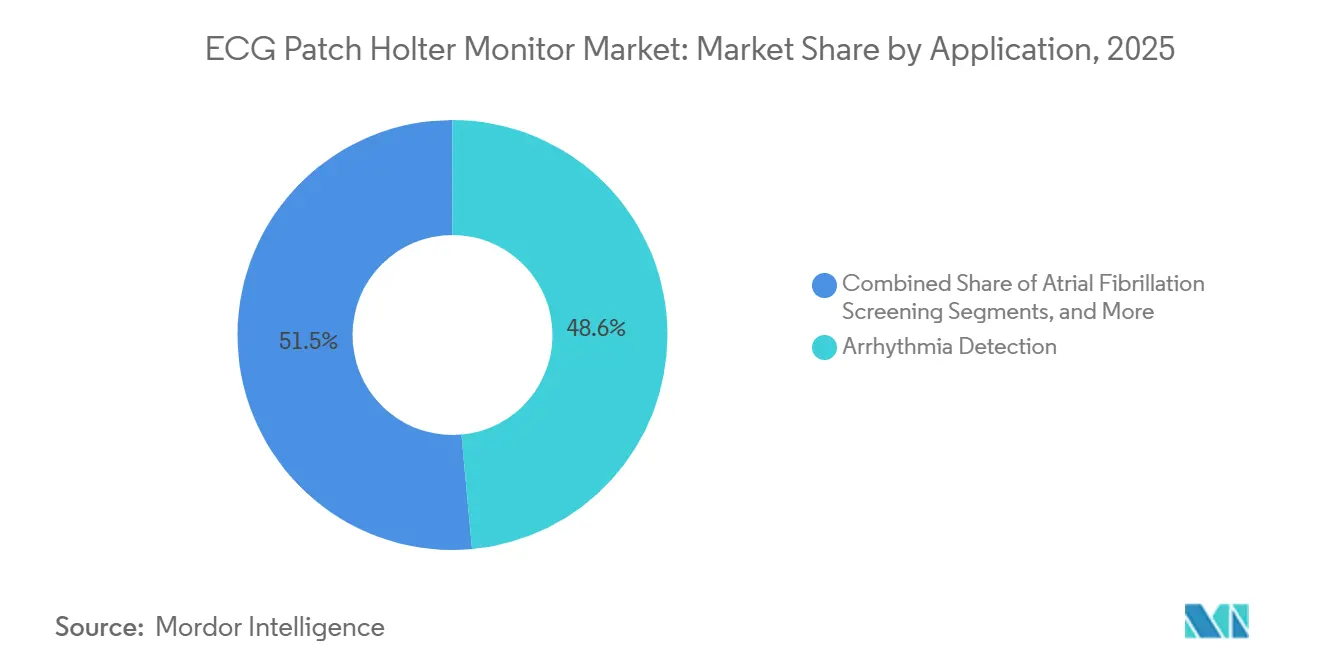

- By application, arrhythmia detection accounted for 48.55% of the ECG patch Holter monitor market size in 2025, while atrial fibrillation screening is projected to grow at a CAGR of 22.89% through 2031.

- By end user, hospitals held 47.89% share in 2025, while ambulatory surgical centers are projected to expand fastest at a CAGR of 20.53% through 2031.

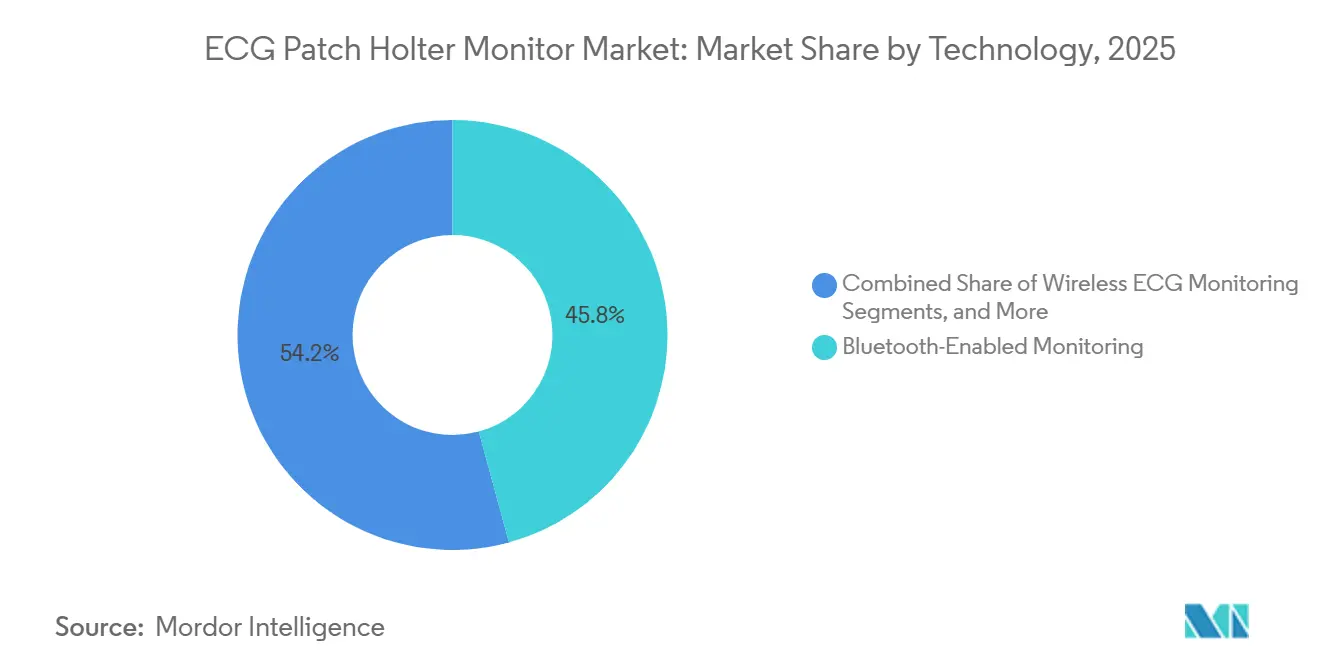

- By technology, Bluetooth-enabled monitoring captured 45.76% share in 2025, while wireless ECG monitoring is projected to grow at a CAGR of 21.55% through 2031.

- By distribution channel, direct sales represented 58.78% share in 2025, while distributors and dealers are expected to record the fastest CAGR of 20.85% through 2031.

- By geography, North America held 42.95% of the market share in 2025, while Asia-Pacific is projected to grow at 22.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global ECG Patch Holter Monitor Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Expanding ambulatory arrhythmia screening programs | +3.2% | North America and Europe, with spillover into Asia-Pacific | Medium term (2-4 years) |

| Shift from in-clinic holter use to at-home continuous monitoring | +2.8% | North America, with growing relevance in Europe and Asia-Pacific | Medium term (2-4 years) |

| Higher reimbursement support for extended ECG monitoring | +3.5% | North America and Western Europe | Short term (≤ 2 years) |

| Rising atrial fibrillation detection burden in aging populations | +4.1% | Global, with stronger relevance in Asia-Pacific and Europe | Long term (≥ 4 years) |

| AI-driven signal review reducing clinical reading time | +2.9% | Global | Short term (≤ 2 years) |

| Reusable workflow integration with remote patient monitoring platforms | +2.4% | North America and Europe, with early gains in Australia and South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising AF Detection Burden Reshapes Patient Selection Criteria

The ECG patch Holter monitor market is benefiting from a broader screening base, as atrial fibrillation affects an estimated 33.5 million people globally, with prevalence rising to 15% to 20% among adults older than 80 years. A retrospective analysis to be presented at ACC.26 in March 2026 covers 657,147 U.S. patients monitored with 14-day Zio continuous ambulatory ECG and identifies clinically actionable arrhythmias in 48% of patients with chronic kidney disease.[1]E. Fung et al., “Wearable Electrocardiogram Technology: Help or Hindrance to the Modern Doctor?,” JMIR Cardio, cardio.jmir.org This finding expands the addressable candidate pool beyond traditional cardiology referrals and brings nephrology and metabolic care settings into the ECG patch Holter monitor market. As clinicians increasingly treat diabetes, obesity, and chronic kidney disease as independent arrhythmia risk factors, monitoring demand is extending to patients without clear cardiac symptoms.

Expanded Reimbursement Framework Unlocks Near-Term Volume

The ECG patch Holter monitor market is expected to gain near-term momentum when CMS finalizes LCD L40257 for temporary nontherapeutic ambulatory cardiac monitoring devices, effective June 28, 2026. The policy expands Medicare coverage to post-TAVR arrhythmia surveillance and cryptogenic stroke monitoring. CMS is also set to revise CPT codes 93241 to 93248 in January 2025 to update extended-monitoring descriptors, improving billing clarity for studies lasting 7 days or longer. These rules support companies with FDA-cleared Class II devices that can meet coverage-related technical specifications. In Europe, the Medical Device Regulation is pushing AI-enhanced patches toward stronger clinical performance evidence, raising the entry bar and favoring better-funded companies.

AI Signal Analytics Reduce Interpretation Bottlenecks at Scale

AI tools are increasingly shaping the ECG patch Holter monitor market by reducing clinician review time and improving the scalability of high-volume monitoring. Philips is expected to launch its ECG AI Marketplace in July 2025, enabling hospitals to add multiple vendor algorithms, including Anumana's FDA-cleared ECG-AI LEF tool, to existing Philips ECG systems without replacing installed hardware. This model separates software upgrades from device replacement cycles, helping health systems enhance diagnostic capability with less disruption. Research published in Nature Communications in April 2025 showed that motion-unrestricted dynamic ECG systems using flexible electronics achieve morphological agreement with standard 12-lead Holter systems across key inter-peak segments.[2]D. Li et al., “Motion-Unrestricted Dynamic Electrocardiogram System Utilizing Imperceptible Electronics,” Nature Communications, doi.org As device-edge processing improves, the ECG patch Holter monitor market can support broader deployment while limiting the physician reading backlog associated with older full-disclosure workflows.

Ambulatory-First Care Models Accelerate Device Adoption

The ECG patch Holter monitor market is advancing as care delivery shifts from short in-clinic studies toward ambulatory and home-based monitoring. A 2025 qualitative study in BMJ Open reported that smartwatch-based and patch-based single-lead ECG monitoring is feasible and preferred by patients for 7-day ambulatory use compared with traditional Holter monitoring. Adhesive, cable-free patch formats support this model because patients can wear them more easily during normal daily activity, reducing barriers to longer monitoring periods.[3]M. Vanhalewyn et al., “Patient Experiences with a Smartwatch 1L-ECG Versus Traditional Holter Monitoring for Ambulatory Cardiac Rhythm Monitoring: A Qualitative Study,” BMJ Open, doi.org The UK Biobank Cardiac Monitoring Study uses a 14-day patch-based ECG across 27,658 participants, showing that large-scale population monitoring with wearable ECG is operationally possible. Providers that bundle device supply, cloud review, and clinical reporting are better positioned to capture recurring study revenue as outpatient monitoring becomes a more routine part of cardiac care.[4]UK Biobank Cardiac Monitoring Study, “Population-Wide Assessment of Heart Rhythm and Physical Activity from 14-Day Recordings,” Preprint, doi.org

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Skin adhesive intolerance and wear-time drop-off | -2.1% | Global | Short term (≤ 2 years) |

| Fragmented reimbursement across countries and payers | -1.8% | Europe, Asia-Pacific, Middle East and Africa, and South America | Long term (≥ 4 years) |

| Data privacy and cybersecurity constraints on cloud ECG transmission | -1.3% | North America and Europe | Medium term (2-4 years) |

| Under-reported false positive fatigue from high-volume algorithm output | -0.9% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adhesive Performance Gaps Limit Multi-Week Wear Compliance

The ECG patch Holter monitor market continues to face wear-time limitations, as contact dermatitis, sweat-related loosening, and motion stress can shorten monitoring before the prescribed period ends. Vivalink’s redesigned wearable ECG adhesive, cited for September 2025, is optimized for p-wave detection and validated for 7-day wear with water resistance, highlighting manufacturer focus on improving wear compliance. However, older adults, patients with fragile skin, and individuals with varying sweat rates may respond differently to the same adhesive formulation. This variability can reduce diagnostic completeness and complicate outcome-based payment models, while modular sensor-adhesive designs may help improve compliance and control per-patient consumable costs.

Cybersecurity Risks in Cloud-Dependent ECG Platforms Demand Systemic Attention

The ECG patch Holter monitor market relies heavily on cloud-linked workflows, increasing data security exposure beyond the core device. iRhythm’s cybersecurity incident, cited for June 2026, involved the exfiltration of patient health information from third-party-hosted business applications through social engineering, although core device and clinical systems were not breached. The incident shows how peripheral infrastructure can create reputational and operational risk for monitoring providers. GDPR in Europe and HIPAA in the United States also raise multi-country data handling costs, while companies using on-device preprocessing may strengthen their position as health systems prioritize cybersecurity in procurement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: ECG Patches Continue To Replace Traditional Holter Recorders

ECG patches are projected to hold 57.60% of the product type segment in 2025, giving them the largest share of the ECG patch Holter monitor market. Their leadership reflects better wear comfort, cable-free design, and stronger alignment with extended monitoring protocols used by payers and physicians. Patch-based systems increasingly support 7-day to 30-day monitoring pathways, making them better suited to detect paroxysmal arrhythmias that shorter 24-hour to 48-hour recordings may miss. In November 2025, iRhythm reported that its 30-day Zio service delivered 18% higher arrhythmia detection than 14-day protocols, strengthening the clinical case for longer patch-based studies.

ECG patches are forecast to grow at a CAGR of 23.73% through 2031, making them the fastest-growing product format in the ECG patch Holter monitor market. This growth reflects billing updates, wider ambulatory use, stronger patient acceptance, and increasing confidence in extended rhythm surveillance.

By Lead Type: 12-Lead Expansion Broadens Ambulatory Use Cases

The 3-lead configuration is projected to hold 55.55% of the lead type segment in 2025, making it the most established format in the ECG patch Holter monitor market. Its position reflects the continued focus of routine ambulatory ECG use on rhythm detection rather than ischemia workup. The 12-lead segment is forecast to grow at a CAGR of 21.76% through 2031, indicating that the clinical role of ambulatory ECG is widening.

HeartBeam completed the first working prototype of an extended-wear 12-lead ECG ambulatory patch in late 2025 and started a pilot study at two hospitals in Belgrade in June 2026. This development marks an important step toward patch-based ischemia detection outside the clinic. Research published in npj Digital Medicine in 2026 found that wearable device-derived AI ECG age correlated with atrial fibrillation burden, suggesting that richer signal capture may support biomarkers beyond standard rhythm classification. Single-lead and 6-lead devices are expected to maintain defined niches in consumer-facing screening and specialist ambulatory settings, while the strongest strategic shift is toward broader clinical utility from multi-lead patch systems.

By Application: AF Screening Gains Momentum Alongside Core Arrhythmia Detection

Arrhythmia detection is projected to account for 48.55% of the application segment in 2025, making it the largest use case by ECG patch Holter monitor market size. This share reflects the core role of ambulatory ECG in capturing intermittent rhythm disturbances that standard office ECGs may not detect. Arrhythmia detection also remains the most familiar entry point for physicians shifting from short-duration Holter use to longer patch-based protocols.

Atrial fibrillation screening is forecast to grow at a CAGR of 22.89% through 2031, making it the fastest-expanding application in the ECG patch Holter monitor market. CMS coverage now includes AF monitoring for patients with cryptogenic stroke and post-TAVR surveillance under LCD L40257, giving this use case stronger reimbursement support. Syncope evaluation and palpitation workups remain important, as extended ambulatory monitoring can change clinical management in 10% to 35% of patients with unexplained syncope and improve the value of full-disclosure monitoring over event-driven methods.

By End User: Ambulatory Surgical Centers Increase Their Role In Decentralized Monitoring

Hospitals are projected to hold 47.89% of the end user segment in 2025, giving them the largest ECG patch Holter monitor market share among care settings. Their leadership reflects established cardiac monitoring infrastructure, inpatient ECG data systems, and long-standing payer relationships. Hospitals also remain central to complex cases where monitoring connects to broader cardiac workups, specialist oversight, or post-procedure observation.

Ambulatory surgical centers are projected to grow at a CAGR of 20.53% through 2031, the fastest rate among end users in the ECG patch Holter monitor market. This trend follows the broader shift of cardiac care toward lower-cost outpatient settings under value-based contracts and tighter utilization review. Cardiology clinics and diagnostic laboratories are also adopting patch services to reduce the equipment cleaning and battery management burden associated with traditional reusable Holter systems.

By Technology: Wireless Architectures Strengthen The Service Model

Bluetooth-enabled monitoring is projected to capture 45.76% of the technology segment in 2025, making it the largest installed format in the ECG patch Holter monitor market. Bluetooth maintains this position because it integrates with existing hospital IT environments and ambulatory data management platforms with fewer workflow changes. It has also gained from clinician familiarity, especially in settings where near-real-time transmission is not required for every study.

Wireless ECG monitoring is forecast to grow at a CAGR of 21.55% through 2031, indicating a stronger role for real-time and attended surveillance models. CMS billing rules support up to 30 days of mobile cardiac telemetry, creating a clear reimbursement advantage for systems that can transmit data continuously to staffed review centers. SmartCardia received FDA clearance in November 2024 for outpatient cardiac telemetry using its 7-lead ECG patch and cloud platform, showing how connected architectures can move into higher-value monitoring categories.

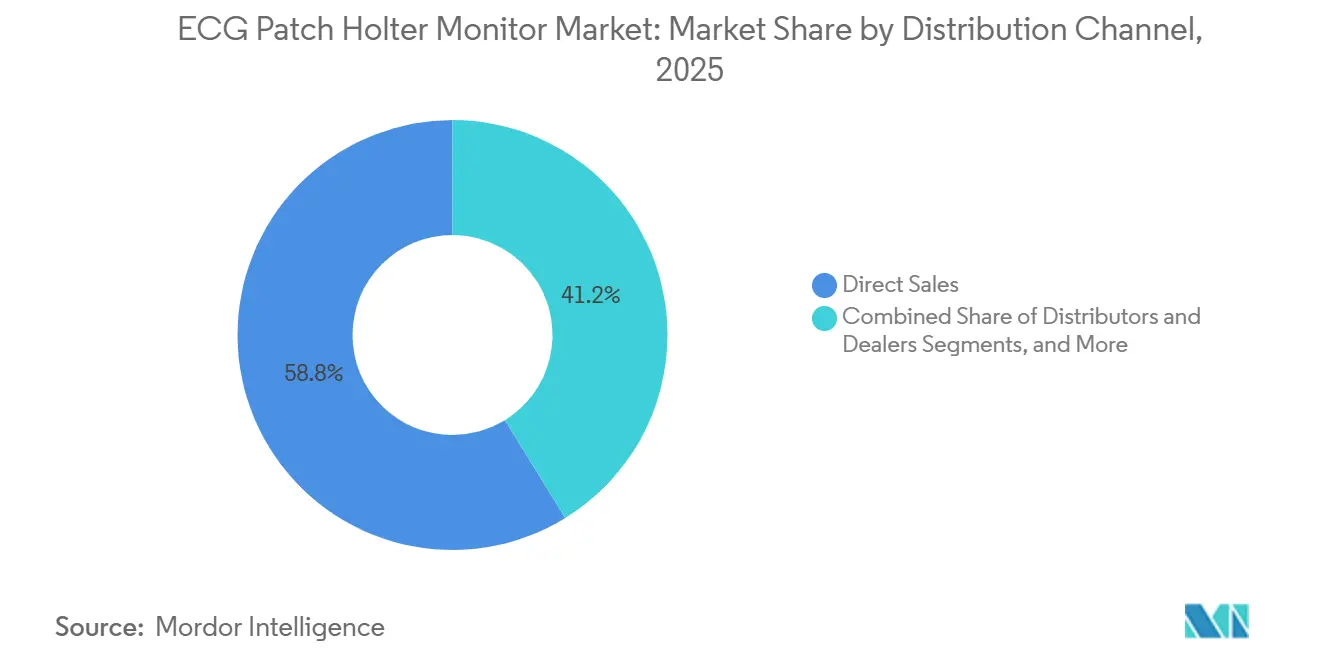

By Distribution Channel: Direct Sales Remain The Core Route To Market

Direct sales are projected to represent 58.78% of the distribution segment in 2025, making them the dominant route in the ECG patch Holter monitor market. This structure reflects that many companies sell a full study workflow rather than only a recorder. These workflows include device supply, reading, reporting, and analytics, with service revenue creating more commercial value than one-time hardware shipments.

Distributors and dealers are expected to grow at a CAGR of 20.85% through 2031, making them the fastest-rising channel as suppliers enter newer regions and non-cardiology accounts. Distributor support becomes more important in markets where suppliers need local representation for approvals and hospital access. Online sales are also gaining traction in physician-dispensed and consumer-adjacent pathways, especially around AliveCor's product line and the reimbursement approval received for Kardia 12L in January 2025.

Geography Analysis

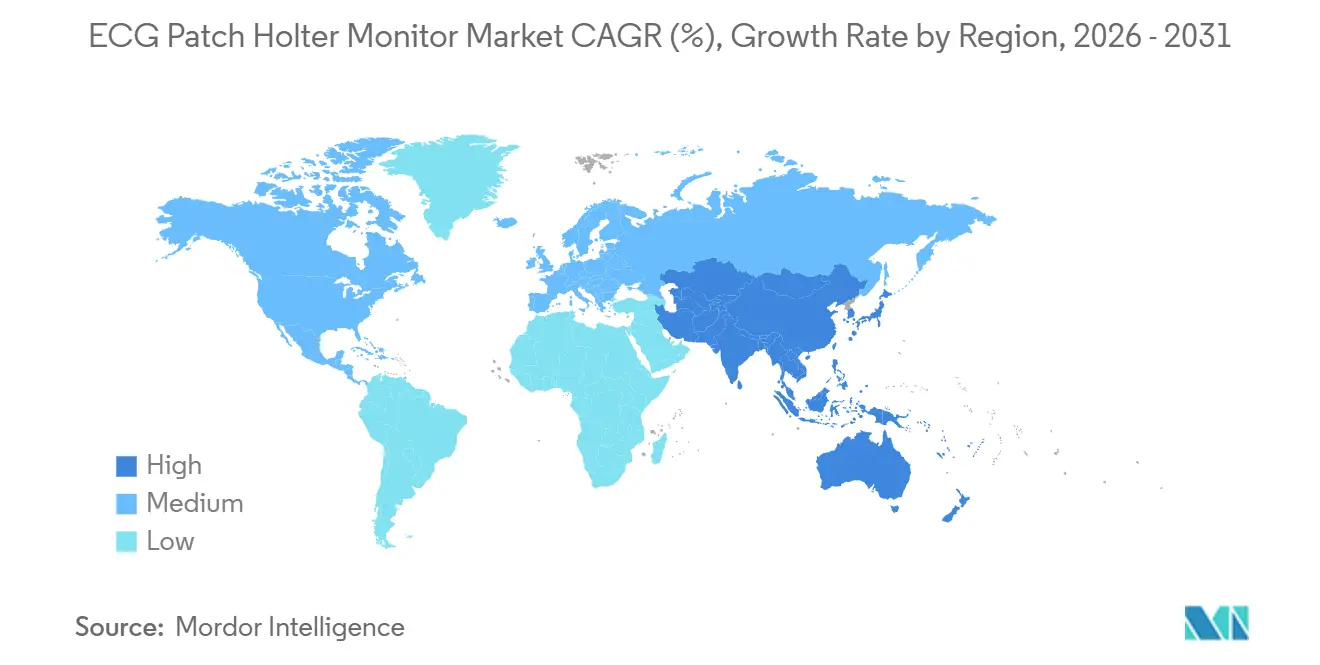

North America is expected to hold 42.95% of the global ECG patch Holter monitor market share in 2025, maintaining its position as the largest regional contributor. The region benefits from a well-established reimbursement framework for ambulatory cardiac monitoring and the broad adoption of iRhythm's Zio platform across primary care and specialist cardiology settings. CMS is set to expand reimbursable indications through LCD L40257, effective June 28, 2026, by adding post-TAVR and embolic stroke-related monitoring, which is expected to increase procedure volume in an already developed market. The United States also provides a defined FDA 510(k) pathway for Class II ambulatory ECG devices, helping cleared innovations move into clinical use with fewer commercial uncertainties.

Asia-Pacific is forecast to expand at a CAGR of 22.34% through 2031, making it the fastest-growing region in the ECG patch Holter monitor market. Japan, South Korea, and Australia are leading early adoption, while China, India, and Southeast Asia are expanding the addressable base through hospital development and digital health investments. Japan revised its medical fee schedule in 2025 and increased reimbursement for Holter recordings of seven days or longer to 2,050 points, compared to 1,750 points for 24-hour studies, improving the value proposition for patch-based formats. Fukuda Denshi is then expected to launch the single-use patch-type Holter ECG “Liz” in April 2026, following PMDA approval in August 2025, providing the region with a strong local product example. AliveCor's July 2025 launch of Kardia 12L in India also indicates that global companies are developing more targeted market entry strategies for the region.

Europe remains a stable demand center in the ECG patch Holter monitor market, supported by its aging population and substantial cardiovascular disease burden. Eurostat projects that people aged 65 years and older will account for 24.8% of the EU population by 2030, supporting sustained demand for ambulatory rhythm monitoring. Cardiovascular disease caused 1.7 million deaths in Europe in 2024, representing 42.5% of all regional deaths and keeping cardiac diagnostics high on public health agendas. EU MDR requirements for AI-enhanced patches also increase the importance of clinical performance evidence, which tends to favor larger incumbents with stronger regulatory resources. The Middle East and Africa and South America remain earlier-stage regions, but healthcare investment programs and broader diagnostic coverage are beginning to expand the future patient pool.

Competitive Landscape

The ECG patch Holter monitor market is moderately concentrated in the premium clinical tier and more fragmented across the mid-market. iRhythm remains the most visible leader in the United States for patch monitoring, supported by a dataset from more than 657,147 monitored patients that strengthens its real-world evidence and algorithm refinement capabilities. Philips competes through a broader platform model that combines ePatch, DigiTrak XT, MCOT, AI tools, and workflow integration for large health systems, rather than relying only on recorder sales.

Recent company moves show how competition is expanding beyond basic arrhythmia capture. Philips launched the ECG AI Marketplace in July 2025 and announced a collaboration with Epic in 2025 to improve ambulatory cardiac monitoring workflows, indicating tighter integration between hospital software environments and ECG services. HeartBeam is advancing toward on-demand 12-lead patch monitoring outside the clinic, while AliveCor expanded Kardia 12L into Europe in April 2026 and broadened FDA-cleared determinations in January 2026.

The broader field remains open in many geographies outside the United States, especially in India, the GCC, and Brazil, where no single company has established leadership across all care settings. In these markets, regulatory readiness, local commercial reach, and ISO 13485-backed quality systems matter almost as much as product design. This dynamic keeps the ECG patch Holter monitor market competitive, allowing regional specialists and channel-led entrants to grow alongside global companies.

ECG Patch Holter Monitor Industry Leaders

iRhythm Technologies, Inc.

Medtronic plc

Koninklijke Philips N.V.

GE HealthCare Technologies Inc.

AliveCor, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: HeartBeam, Inc. initiated a pilot study of its on-demand 12-lead ECG patch in patients with suspected coronary artery disease at 2 hospitals in Belgrade, Serbia.

- April 2026: AliveCor, Inc. launched the AI-powered Kardia 12L ECG System in Europe following CE Mark approval, and the system had previously identified more than 4,000 instances of myocardial infarction and ischemia globally since its 2024 U.S. launch.

- March 2026: HeartBeam, Inc. completed the first working prototype of an extended-wear 12-lead ECG ambulatory patch and initiated commercial account relationships across New York, Dallas, South Florida, and Southern California for its FDA-cleared synthesized 12-lead ECG platform.

- January 2026: AliveCor received FDA clearance expanding the Kardia 12L's cardiac determinations to 39, covering the most common types of cardiac ischemia and acute myocardial infarction.

Global ECG Patch Holter Monitor Market Report Scope

As per the scope of the report, an ECG Patch Holter Monitor is an adhesive, lightweight biosensor worn directly on the chest to continuously record your heart's electrical activity. It upgrades traditional monitors by replacing bulky devices and tangled wires with a single, water-resistant, and wireless wearable.

The ECG patch Holter monitor market is segmented by product type, lead type, application, end user, technology, distribution channel, and geography. By product type, the market includes ECG patch and Holter monitors. By lead type, the market is segmented into single-lead, 3-lead, 6-lead, 12-lead, and other multi-lead configurations. By application, the market is categorized into arrhythmia detection, atrial fibrillation screening, syncope evaluation, palpitation workup, post-ablation and post-procedure monitoring, and other cardiac monitoring applications. By end user, the market is segmented into hospitals, cardiology clinics, ambulatory surgical centers, home care settings, and diagnostic laboratories. By technology, the market includes wireless ECG monitoring, Bluetooth-enabled monitoring, cellular-connected monitoring, and AI-assisted signal analytics. By distribution channel, the market is segmented into direct sales, online sales, and distributors and dealers. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| ECG Patch |

| Holter Monitor |

| Single-Lead |

| 3-Lead |

| 6-Lead |

| 12-Lead |

| Other Multi-Lead Configurations |

| Arrhythmia Detection |

| Atrial Fibrillation Screening |

| Syncope Evaluation |

| Palpitation Workup |

| Post-Ablation and Post-Procedure Monitoring |

| Other Cardiac Monitoring Applications |

| Hospitals |

| Cardiology Clinics |

| Ambulatory Surgical Centers |

| Home Care Settings |

| Diagnostic Laboratories |

| Wireless ECG Monitoring |

| Bluetooth-Enabled Monitoring |

| Cellular-Connected Monitoring |

| AI-Assisted Signal Analytics |

| Direct Sales |

| Online Sales |

| Distributors and Dealers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | ECG Patch | |

| Holter Monitor | ||

| By Lead Type | Single-Lead | |

| 3-Lead | ||

| 6-Lead | ||

| 12-Lead | ||

| Other Multi-Lead Configurations | ||

| By Application | Arrhythmia Detection | |

| Atrial Fibrillation Screening | ||

| Syncope Evaluation | ||

| Palpitation Workup | ||

| Post-Ablation and Post-Procedure Monitoring | ||

| Other Cardiac Monitoring Applications | ||

| By End User | Hospitals | |

| Cardiology Clinics | ||

| Ambulatory Surgical Centers | ||

| Home Care Settings | ||

| Diagnostic Laboratories | ||

| By Technology | Wireless ECG Monitoring | |

| Bluetooth-Enabled Monitoring | ||

| Cellular-Connected Monitoring | ||

| AI-Assisted Signal Analytics | ||

| By Distribution Channel | Direct Sales | |

| Online Sales | ||

| Distributors and Dealers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value and 2031 outlook for ECG patch Holter monitors?

The ECG patch Holter monitor market size stands at USD 2.44 billion in 2026 and is projected to reach USD 5.99 billion by 2031 at a CAGR of 19.67%.

Which product type leads revenue generation?

ECG patches led product type demand with 57.60% share in 2025, supported by better wear comfort and stronger fit with extended monitoring protocols.

Which application is growing the fastest?

Atrial fibrillation screening is the fastest-growing application, with a projected CAGR of 22.89% through 2031, helped by stroke prevention programs and reimbursement support.

Which region has the strongest growth outlook?

Asia-Pacific is expected to post the fastest regional growth at a CAGR of 22.34% through 2031, supported by hospital expansion, policy support, and new product launches.

Why are hospitals still the largest end users if care is moving outward?

Hospitals held 47.89% share in 2025 because they still control infrastructure, data systems, and payer relationships, even as ambulatory surgical centers grow faster.

What is shaping competition among major suppliers?

Competition is shifting toward companies that combine cleared devices, AI-supported analytics, reimbursement readiness, and reporting workflows, rather than relying on recorder hardware alone.

Page last updated on: