Healthcare Courier Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

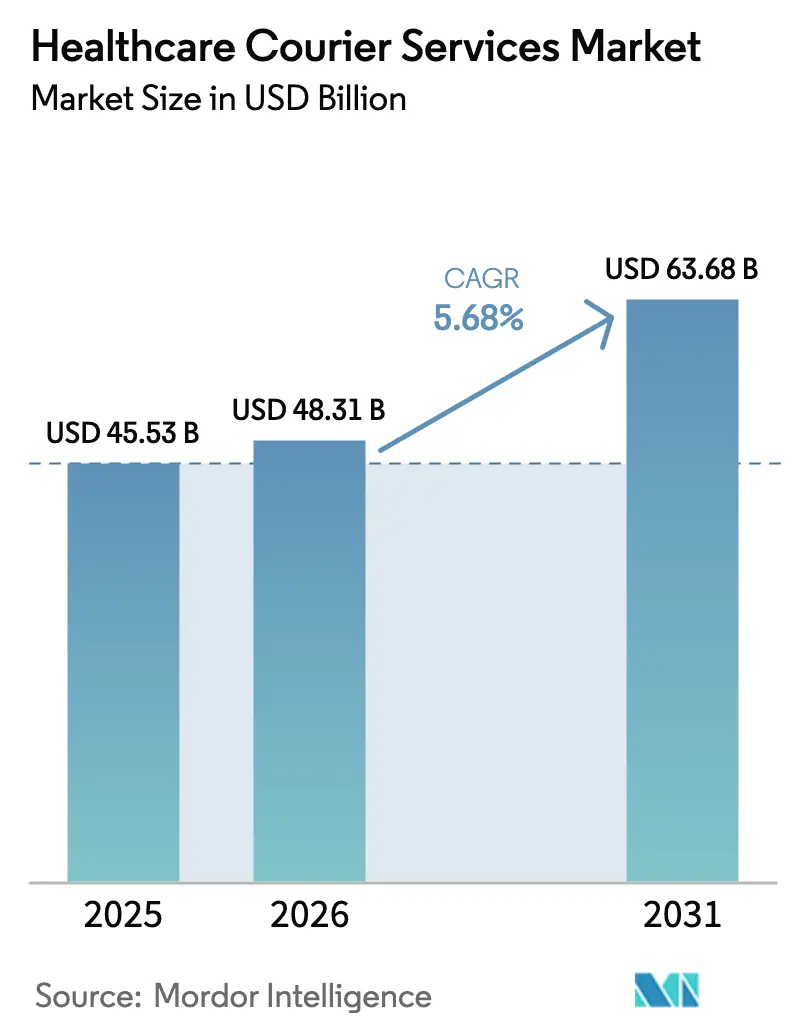

| Market Size (2026) | USD 48.31 Billion |

| Market Size (2031) | USD 63.68 Billion |

| Growth Rate (2026 - 2031) | 5.68% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Courier Services Market Analysis by Mordor Intelligence

The Healthcare Courier Services Market size was valued at USD 45.53 billion in 2025 and is estimated to grow from USD 48.31 billion in 2026 to reach USD 63.68 billion by 2031, at a CAGR of 5.68% during the forecast period (2026-2031).

Market expansion is linked to aging populations that raise diagnostic volumes, rapid uptake of biologics and cell therapies that require validated cold chains, and enforcement of serialization mandates such as the U.S. Drug Supply Chain Security Act. Providers that demonstrate real-time chain-of-custody capabilities and IATA CEIV Pharma certification are consolidating premium contracts, while capital-intensive cold-chain fleets create visible barriers for new entrants. Express courier demand benefits from the rise of decentralized clinical trials and hospital compounding hubs, and home healthcare shifts are steadily redirecting shipment destinations from hospital docks to patient doorsteps. Competitive focus now centers on end-to-end visibility, temperature assurance, and cyber-secure data flows, all of which push smaller couriers toward technology partnerships or acquisition by larger integrators.

Key Report Takeaways

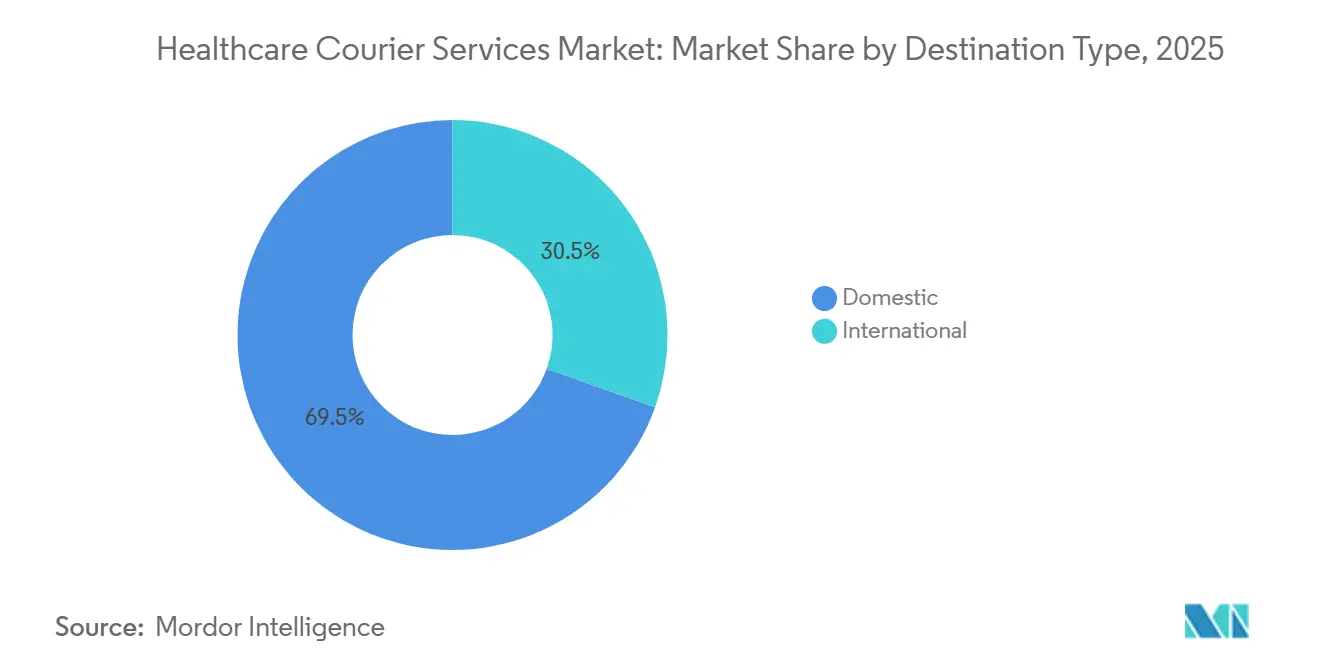

- By destination, domestic routes held 69.54% of the healthcare courier services market size in 2025. International shipments are forecast to expand at a 6.07% CAGR between 2026-2031.

- By speed of delivery, non-express services accounted for 65.51% of the healthcare courier services market share in 2025. Express services are the fastest-growing segment with a 6.53% CAGR between 2026-2031.

- By temperature control, non-temperature-controlled logistics commanded 80.70% of the 2025 volume. Temperature-controlled services are slated for a 6.35% CAGR between 2026-2031.

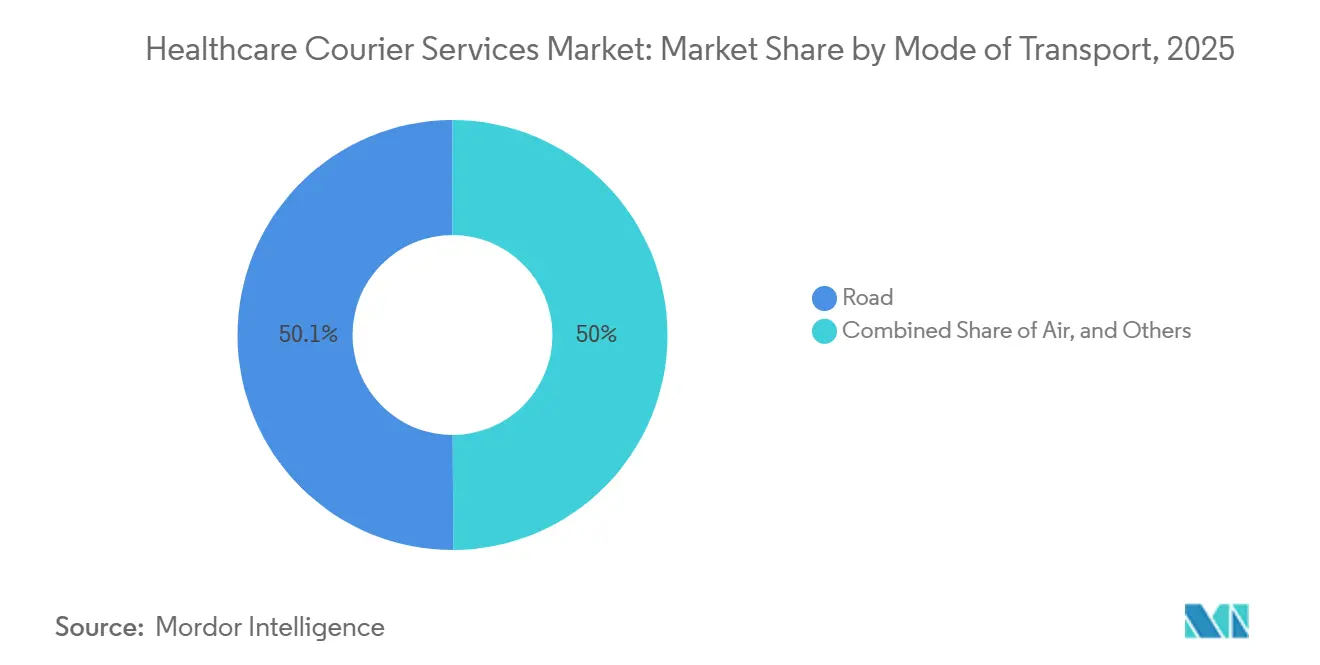

- By mode of transportation, road transport contributed 50.05% of 2025 revenue, while air freight is on track for a 6.16% CAGR between 2026-2031.

- By end-user, hospitals and clinics led with 56.45% of 2025 revenue. Home healthcare providers represent the fastest-growing user group with a 6.28% CAGR between 2026-2031.

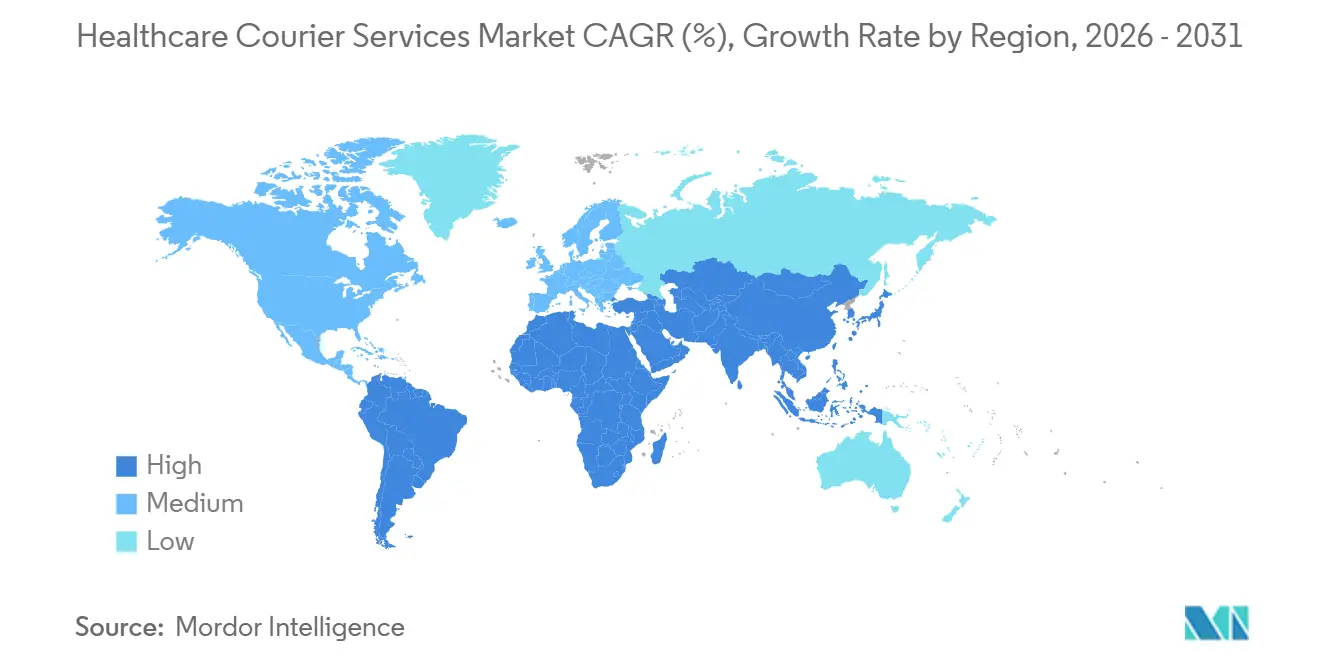

- By geography, North America captured 36.79% share in 2025. Asia-Pacific is expected to post a 7.70% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Courier Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population and chronic disease burden boosting specimen volumes | +1.2% | Global, with acute pressure in North America, Europe, and Japan | Long term (≥ 4 years) |

| Biologics, cell and gene therapies requiring temperature-controlled logistics | +1.5% | North America and EU core, expanding to APAC manufacturing hubs | Medium term (2-4 years) |

| Regulatory push for end-to-end traceability driving specialized couriers | +0.9% | Global, led by U.S. DSCSA and EU Falsified Medicines Directive | Short term (≤ 2 years) |

| Expansion of on-demand health e-commerce platforms in emerging markets | +0.7% | APAC (India, Southeast Asia), MEA, Latin America | Medium term (2-4 years) |

| Surge in decentralized and at-home clinical trials needing DTP logistics | +1.0% | North America and EU, with pilot programs in APAC | Short term (≤ 2 years) |

| Hospital pharmacy off-site compounding hubs increasing STAT loops | +0.6% | North America, Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population and Chronic Disease Burden Boosting Specimen Volumes

Global life expectancy gains translate into higher diagnostic demand because chronic ailments such as diabetes and cardiovascular disease require continuous laboratory monitoring. The World Health Organization recorded 1.4 billion people aged 60 and above in 2024, a group projected to reach 2.1 billion by 2050, and each additional year of life expectancy increases laboratory test orders by 3-5%. Japan illustrates the trend as 29% of its residents were over 65 in 2025, straining hospital courier loops due to a 22% rise in outpatient diagnostics. U.S. data show 6 in 10 adults living with at least one chronic illness, driving roughly 14 billion tests per year. High specimen volume favors specialized couriers that maintain validated cold-chain handling and HIPAA-compliant data systems. Rural routes encounter additional cost pressure, making route optimization software and low-emission vehicles critical for profitability in aging-heavy regions[1]“Ageing and Health,” World Health Organization, who.int .

Biologics, Cell and Gene Therapies Requiring Temperature-Controlled Logistics

Advanced therapies impose strict temperature windows that exclude general freight. The European Medicines Agency cleared 92 new biologics in 2024, nearly all needing 2 °C to 8 °C transport, while many cell therapies require cryogenic conditions below −150 °C. IATA certified 450 new CEIV Pharma facilities in 2024, reflecting shipper insistence on documented cold-chain credentials. Capital investment is steep: pharmaceutical-grade vehicles demand real-time monitoring equipment and backup power systems, deterring new entrants and encouraging vertical integration. Shipment failure risks remain elevated as patient-specific therapies can exceed USD 400,000 per dose, prompting sponsors to demand redundant refrigeration and high product-liability coverage[2]“Advanced Therapy Medicinal Products,” European Medicines Agency, ema.europa.eu.

Regulatory Push for End-to-End Traceability Driving Specialized Couriers

Full implementation of the DSCSA in November 2024 obliges every handoff to capture serialized identifiers electronically. The EU Falsified Medicines Directive enforces comparable serialization and tamper checks. Couriers unable to integrate handheld scanners with track-and-trace platforms are excluded from hospital and pharmacy tenders. Compliance extends to audited SOPs aligned with WHO guidelines for temperature-sensitive pharmaceuticals, reinforcing a regulatory moat that favors incumbents.

Expansion of On-Demand Health E-Commerce Platforms in Emerging Markets

Tele-pharmacy models are bypassing traditional drugstores across Asia and Africa, generating courier demand in underserved areas. India’s leading e-pharmacy apps now promise same-day delivery across tens of thousands of postal codes, but informal addressing systems force couriers to spend extra time locating recipients. The World Bank has noted that last-mile logistics can represent up to 70% of supply-chain costs in sub-Saharan Africa because of unpaved roads and inconsistent GPS data. Hybrid solutions that combine motorcycles, community pickup points, and drone pilots are emerging to balance service quality and cost.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cold-chain fleet and compliance costs | -0.8% | Global, most acute in emerging markets with limited infrastructure | Medium term (2-4 years) |

| Driver shortages and high turnover impacting service reliability | -0.6% | North America, Western Europe, with spillover to APAC urban centers | Short term (≤ 2 years) |

| Fragmented address systems and poor roads in emerging markets | -0.5% | APAC (India, Southeast Asia), sub-Saharan Africa, parts of Latin America | Long term (≥ 4 years) |

| Rising cyber-security risk around protected health information | -0.3% | Global, with heightened regulatory scrutiny in North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cold-Chain Fleet and Compliance Costs

Pharmaceutical-grade refrigerated vans cost close to USD 150,000, far higher than ambient vehicles, and annual audits for CEIV Pharma or WHO prequalification add significant overhead. In regions with unreliable electricity, couriers must install generators at warehouses, while extreme ambient temperatures raise equipment failure risks. These expenses concentrate capacity in high-value urban corridors, leaving rural zones to rely on ambient-stable drugs or batch deliveries[3]“Infrastructure Development in Emerging Markets,” World Bank, worldbank.org .

Driver Shortages and High Turnover Impacting Service Reliability

Transportation workforce gaps in North America left hundreds of thousands of roles unfilled in 2024, and healthcare courier drivers need specialized training in specimen handling and privacy regulations. High churn inflates recruitment costs and causes service lapses that erode contract renewals. Automation pilots such as campus robots are emerging, but full scale adoption remains several years away[4]“Breach Portal,” U.S. Department of Health and Human Services, hhs.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Destination: International Shipments Gain Momentum

Domestic routes accounted for 69.54% of revenue in 2025, a reflection of dense intra-city specimen loops and pharmacy restocking. International traffic is forecast to grow at a 6.07% CAGR (2026-2031) as global clinical trials expand patient recruitment across borders and as biologic exports accelerate. Customs requirements for biological samples intensify documentation needs, making pre-cleared trade lanes a competitive differentiator.

International growth enlarges the Healthcare Courier Services market opportunity in customs brokerage, and carriers that pair validated cold-chain packaging with 24-hour regulatory clearance teams are positioned to capture premium contracts. As a result, the Healthcare Courier Services market size attributable to cross-border movements is on a steeper growth path than domestic services through 2031.

By Speed of Delivery: Express Leads Growth Trajectory

Non-express services retained a 65.51% revenue share in 2025 because routine clinic and pharmacy deliveries tolerate 24- to 48-hour transits. Express options are projected to notch a 6.53% CAGR (2026-2031) as decentralized trials and hospital STAT loops demand same-day pickups and next-flight-out transport.

Express expansion widens the Healthcare Courier Services market share for operators that maintain real-time tracking and time-definite guarantees. Upgrades in route-planning software and redundant driver pools are translating into higher price realizations, supporting above-market profit prospects.

By Temperature Control: Cold-Chain Outpaces Ambient Growth

Non-temperature-controlled logistics held 80.70% of the 2025 value, yet chilled and frozen services will rise at a 6.35% CAGR (2026-2031) on the back of biologics approvals and mRNA platform adoption. IATA CEIV Pharma certification is becoming a threshold requirement for many tenders, pushing ambient-only players toward partnership or exit.

Cold-chain gains enlarge the Healthcare Courier Services market size for certified lanes, especially in Europe and North America, where regulation is strictest. The premium pricing available in frozen and cryogenic sub-segments offsets fleet capital costs and smooths profit volatility.

By Mode of Transportation: Air Freight Supports Time-Sensitive Biologics

Road transport supplied 50.05% of 2025 revenue due to its door-to-door flexibility. Air freight is expected to expand at a 6.16% CAGR (2026-2031) as biologic pipelines depend on rapid, temperature-protected international moves. Cargo-aircraft climate-control features and dedicated cool-chain terminals accelerate adoption.

The Healthcare Courier Services market share of multimodal operators is rising because they integrate air legs with first- and last-mile road services, enabling single-contract accountability for temperature compliance across continents.

By End-User: Home Healthcare Emerges as Fastest Expanding Segment

Hospitals and clinics delivered 56.45% of 2025 revenue. Home healthcare providers will see a 6.28% CAGR between 2026-2031 after Medicare expanded reimbursement for at-home infusions and biologic injections. Each patient episode triggers both forward and reverse logistics needs, from medication delivery to sharps disposal.

As home-based care accelerates, patient-facing digital interfaces and driver etiquette training become core to winning contracts, further reshaping the Healthcare Courier Services market landscape in favor of tech-forward operators.

Geography Analysis

North America controlled 36.79% of 2025 revenue, powered by stringent DSCSA enforcement and high per-capita pharmaceutical spending. Serialized track-and-trace requirements pushed non-compliant carriers out of hospital and pharmacy networks, consolidating volume among certified couriers. Persistent driver turnover above 30% in 2024 tightened capacity but also raised wage floors, encouraging automation trials on hospital campuses.

Asia-Pacific is projected to register the fastest 7.70% CAGR between 2026-2031. China’s rapidly aging population and rising domestic biologics output stimulate investment in compliant cold-chain networks. India’s tele-pharmacy boom broadens last-mile demand despite fragmented addressing systems. Japan, South Korea, and Australia offer high-value routes where temperature compliance enables premium rates. Southeast Asia remains capacity-constrained but promises longer-term upside as public-sector health funding increases.

The Middle East and Africa, along with South America, contribute smaller shares yet present pockets of momentum. Gulf Cooperation Council economies invest heavily in medical tourism and specialty care, requiring international corridors to Europe and North America. Sub-Saharan Africa contends with limited paved-road coverage, elevating service costs and necessitating motorcycle fleets and micro-depots. Brazil and Argentina supply regional biologics, but currency volatility compresses courier margins and complicates fleet financing.

Competitive Landscape

The Healthcare Courier Services market is moderately fragmented, with global integrators such as DHL, FedEx, and UPS competing against regional specialists. High-value niches like cryogenic gene-therapy shipments show increasing consolidation because CEIV Pharma certification, redundant refrigeration, and cyber-secure data platforms demand large capital commitments. Technology is now the core battleground: larger players deploy IoT sensors with blockchain logs for immutable chain-of-custody records, whereas smaller couriers still rely on manual temperature checks, producing a service quality gap visible to shippers.

Vertical integration is accelerating. Pharmaceutical distributors have expanded captive courier arms to safeguard capacity, as demonstrated by AmerisourceBergen’s World Courier and Cardinal Health’s OptiFreight. White-label partnerships allow hospital systems to outsource logistics while retaining patient-facing branding. Cyber-security has emerged as a contract differentiator following health data breaches tallied by HHS in 2024. Couriers that achieve SOC 2 Type II certification and carry substantial cyber-liability insurance can price at a premium, especially on clinical-trial lanes.

Regional specialists defend share through last-mile density and intimate knowledge of local regulations. In North America, dedicated hospital loop providers leverage facility-specific expertise. In Europe, country-focused couriers benefit from labor rules that discourage cross-border driver rotations. Across Asia-Pacific, flexible fleets of motorcycles and small vans overcome narrow roads and heavy traffic. Mergers and acquisitions continue as integrators buy niche players to add geography coverage or specialized capabilities.

Healthcare Courier Services Industry Leaders

DHL Group

FedEx

CENCORA (World Courier)

United Parcel Service of America, Inc.

Kuehne+Nagel (including QuickSTAT)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: UPS acquired Andlauer Healthcare Group for USD 1.6 billion, aiming to double healthcare revenue to USD 20 billion by 2026.

- March 2025: DHL Group completed the purchase of CRYOPDP, integrating cell and gene therapy capabilities into its Pharma Specialized Network.

- November 2024: FedEx expanded its Asia-Pacific life sciences network, adding temperature-controlled capacity for clinical trial shipments.

- February 2024: DHL Supply Chain earmarked USD 200 million for five new temperature-controlled sites in Pennsylvania and North Carolina to support clinical-trial logistics.

Global Healthcare Courier Services Market Report Scope

Healthcare courier services are specialized logistics providers focused on the transportation of medical items, ensuring safe and timely delivery of sensitive materials essential for patient care. These services are critical in the healthcare sector, addressing the unique needs associated with transporting medical supplies, specimens, and equipment.

The market is segmented by by Destination (Domestic, International), by Temperature Control (Cold Chain, Non-Temperature Sensitive), by Service Type (Standard Services, Rush and On-Demand Services), by End-User (Hospitals and Clinics, Diagnostic Labs, Pharmaceutical and Biotechnology Companies, and Home Healthacare Providers) and by Region (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The Report Offers Market Size and Forecast Values (USD Billion) for all the Above Segments.

| Domestic |

| International |

| Express (Time-Definite-Delivery and Day-Definite-Delivery) |

| Non-Express (Standard and Deferred) |

| Temperature Controlled (Cold Chain) | Chilled (0-5 °C) |

| Frozen (-18-0 °C) | |

| Ambient | |

| Deep-Frozen / Ultra-Low (less than-20 °C) | |

| Non-Temperature Controlled (Non-Cold Chain) |

| Air |

| Road |

| Others |

| Hospitals and Clinics |

| Diagnostic Labs |

| Pharmaceutical and Biotechnology Companies |

| Blood and Tissue Banks |

| Home Healthcare Providers |

| Other End User (Clinical Research Centres, Blood Bank etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| Destination | Domestic | |

| International | ||

| Speed of Delivery | Express (Time-Definite-Delivery and Day-Definite-Delivery) | |

| Non-Express (Standard and Deferred) | ||

| Temperature Control | Temperature Controlled (Cold Chain) | Chilled (0-5 °C) |

| Frozen (-18-0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| Non-Temperature Controlled (Non-Cold Chain) | ||

| Mode of Transportation | Air | |

| Road | ||

| Others | ||

| End-user | Hospitals and Clinics | |

| Diagnostic Labs | ||

| Pharmaceutical and Biotechnology Companies | ||

| Blood and Tissue Banks | ||

| Home Healthcare Providers | ||

| Other End User (Clinical Research Centres, Blood Bank etc.) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Healthcare Courier Services market in 2026?

How large is the Healthcare Courier Services market in 2026?

Which region currently generates the highest courier revenue?

Which region currently generates the highest courier revenue?

Which segment is expanding fastest by destination?

Which segment is expanding fastest by destination?

Why is cold-chain logistics gaining share?

Why is cold-chain logistics gaining share?

What is the biggest operational challenge for couriers?

What is the biggest operational challenge for couriers?

How does home healthcare affect courier demand?

How does home healthcare affect courier demand?

Page last updated on: