Hardcopy Peripherals And Printing Consumables Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

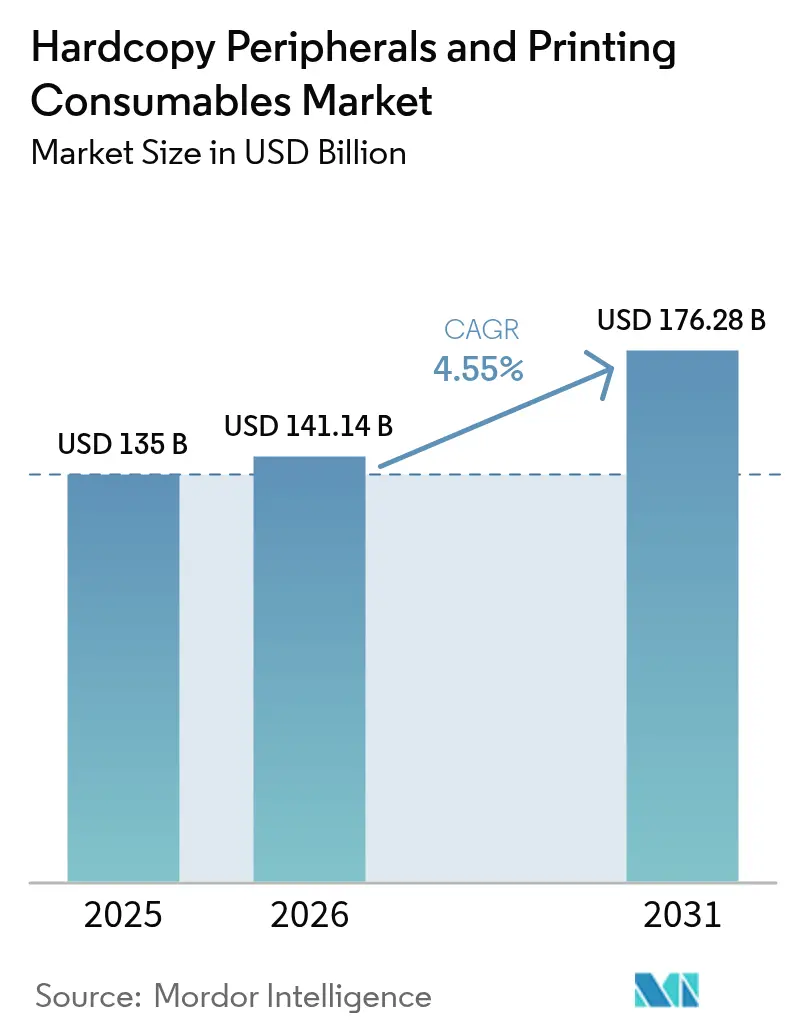

| Market Size (2026) | USD 141.14 Billion |

| Market Size (2031) | USD 176.28 Billion |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hardcopy Peripherals And Printing Consumables Market Analysis by Mordor Intelligence

The Hardcopy peripherals and printing consumables market size is expected to grow from USD 135 billion in 2025 to USD 141.14 billion in 2026 and is forecast to reach USD 176.28 billion by 2031 at 4.55% CAGR over 2026-2031. Expansion persists despite paper-reduction mandates because hybrid work, e-commerce packaging, and subscription Print-as-a-Service (PraaS) deals sustain device and supplies demand. Managed print services (MPS) adoption lets enterprises cut 20-30% of fleet cost while shifting spend from capex to opex.[1]“Managed Print Services,” Xerox Corp., xerox.com Energy-efficient fusing units and refillable ink tanks help vendors defend price premiums as ESG reporting expands. Semiconductor shortages still disrupt hardware availability, yet print suppliers buffer risk by redesigning boards for easier component sourcing.

Key Report Takeaways

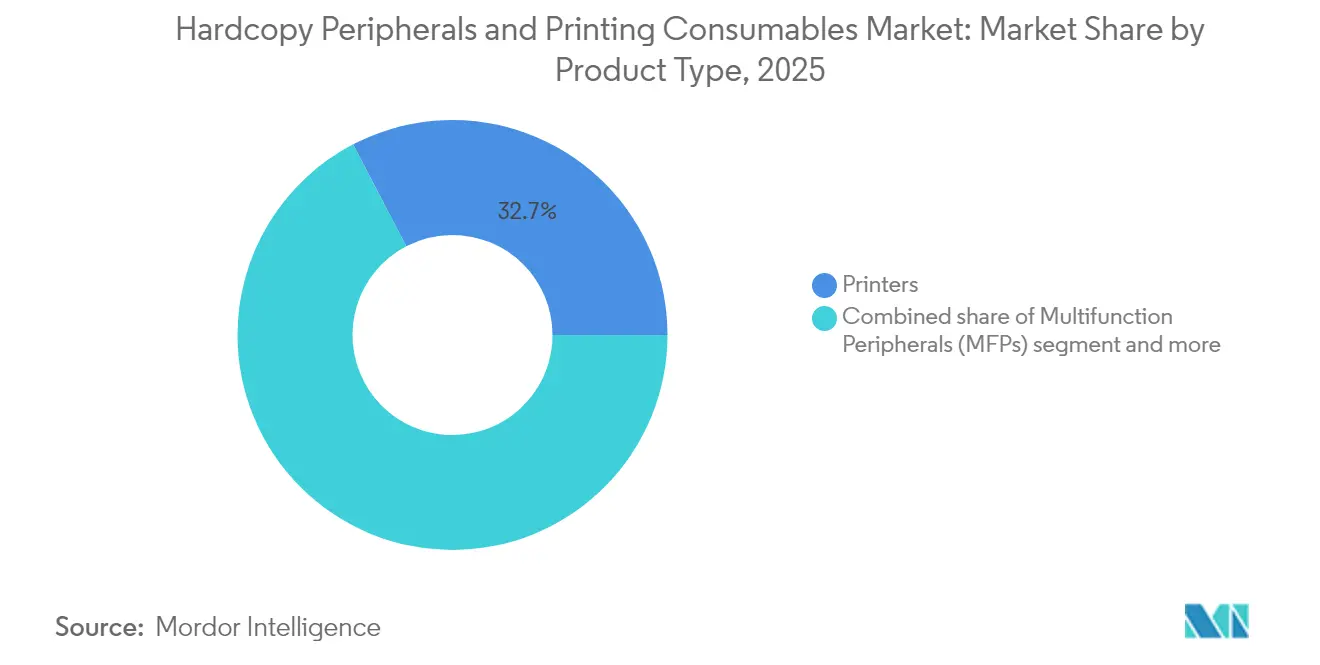

- By product type, printers held 32.65% of 2025 revenue, whereas wide-format/production printers are forecast to post a 4.95% CAGR through 2031.

- By technology, inkjet commanded 44.60% of the Hardcopy peripherals & printing consumables market share in 2025, while laser printing is slated to grow 5.85% CAGR to 2031.

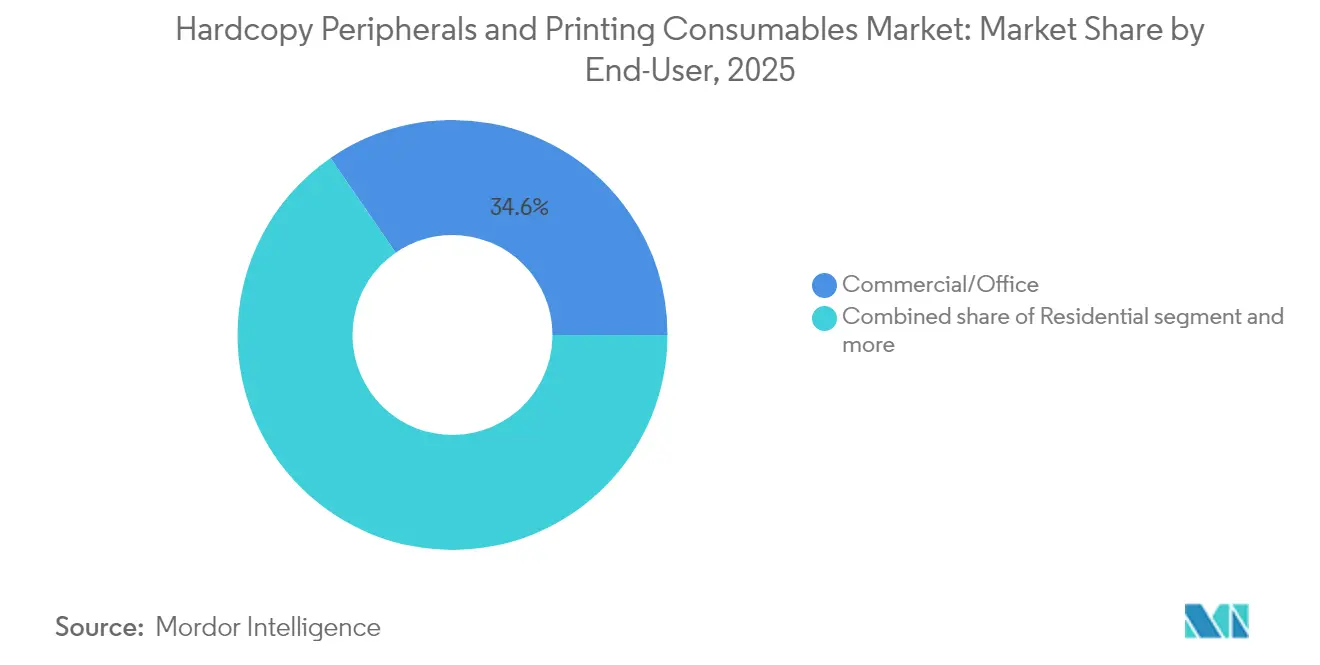

- By end-user, commercial/office accounted for 34.60% of the Hardcopy peripherals & printing consumables market size in 2025; educational institutions show the fastest 4.75% CAGR outlook.

- By distribution, direct/contractual channels secured 46.10% revenue in 2025; MPS leads growth at a 5.15% CAGR.

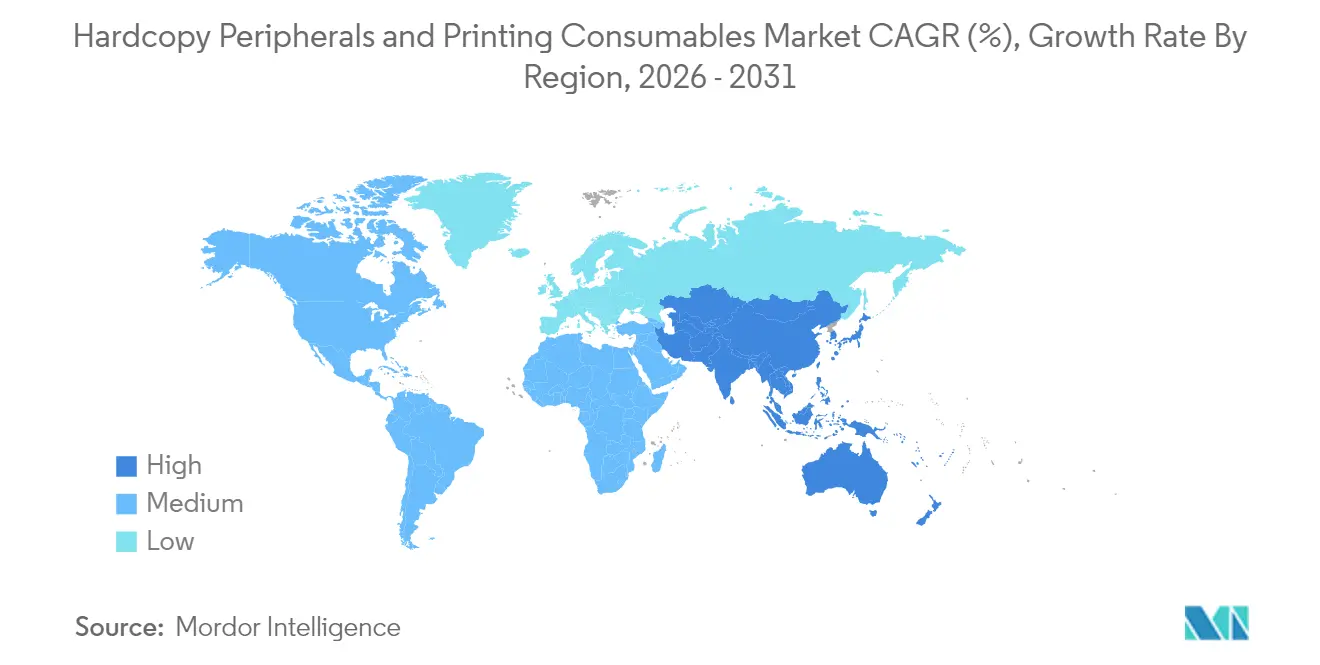

- Geographically, North America dominated with a 36.70% share in 2025, whereas Asia-Pacific is projected to expand 5.80% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hardcopy Peripherals And Printing Consumables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in production digital-printing colour volume | +1.2% | North America and Western Europe | Medium term (2-4 years) |

| Decorative/tactile print enhancements | +0.8% | North America, Europe, high-income APAC | Medium term (2-4 years) |

| SME switch to low-CPP ink-tank printers | +0.9% | Global with APAC focus | Short term (≤ 2 years) |

| E-commerce packaging and in-house label printing | +1.0% | Global with NA and EU hubs | Medium term (2-4 years) |

| Hybrid-work fleets of distributed A4 MFPs | +0.7% | Developed markets | Short term (≤ 2 years) |

| Subscription Print-as-a-Service adoption | +0.6% | NA, Europe, advanced APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in Production Digital-Printing Colour Volume

Digital presses now account for only 3.8% of printed pages but capture 25% of print value as brands pay premiums for short-run customisation.[2]Canon Inc., “Integrated Report 2024,” global.canon Canon’s Colorado series trimmed turnaround time by 60%, letting PSPs deliver 22,000 transit-stop signs in 3 months instead of 12 months. When workflow automation improves by 10 points, output efficiency rises nearly 15%, strengthening ROI on colour devices. This shift channels high-margin inks and coatings into the Hardcopy peripherals and printing consumables market, widening the supply's profit pool.

Demand for Decorative / Tactile Print Enhancements

Retail packs with spot-varnish, raised-foil, or texture earn 30-50% higher unit price than standard CMYK labels, enabling PSPs to offset flat run lengths. Inline embellishment modules bolt onto many digital presses, removing extra passes and labour. Luxury and personal-care firms in Europe are the early adopters, yet mid-tier brands in North America are now piloting quarterly limited-edition launches that require smaller runs but more complex finishes. This behaviour pushes niche varnishes, foils, and compatible substrates, bolstering the Hardcopy peripherals and printing consumables market.

SME Shift to Low-CPP Ink-Tank Devices

Ink-tank hardware slashes operating expense by up to 90% compared with cartridges, a decisive factor for budget-sensitive SMEs. Epson recorded 7.8% unit growth in high-capacity tank printers during 2024 despite a fall in cartridge demand. In India and Southeast Asia, ink-tank penetration already surpasses 50% of annual A4 sales. Vendors accept lower hardware margin, then monetise refill-bottle sales and three-year service contracts. Shifted revenue timing but stabilised lifetime value keeps the Hardcopy peripherals and printing consumables market resilient.

E-Commerce Packaging and In-House Label Printing

Online retail volumes have grown 40% since 2019, prompting merchants to print labels and branded cartons internally for just-in-time dispatch. Variable-data presses handle address data and versioned artwork in one pass, reducing external lead times. Small coffee roasters and cosmetic start-ups now deploy benchtop colour label printers costing under USD 5,000, expanding the addressable installed base for supply vendors. Premium matte and recyclable laminates attach higher margins, supporting the Hardcopy peripherals and printing consumables market even when page counts plateau.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corporate ESG paper-reduction mandates | -0.6% | NA, EU, developed APAC | Medium term (2-4 years) |

| Semiconductor supply-chain volatility | -0.5% | Global | Short term (≤2 years) |

| Decline of legacy print manufacturing | -0.7% | Developed markets | Long term (≥4 years) |

| IP enforcement on third-party supplies | -0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Corporate ESG Paper-Reduction Mandates

Businesses pledge net-zero targets that restrict paper use, cutting fleet page volumes year over year. Seventy-eight percent of enterprises still call print essential in 2024, yet projections show that ratio sliding to 64% by 2025. Manufacturers counter with low-energy fusers and closed-loop cartridge return schemes such as HP Planet Partners, which recycled 398 million cartridges by 2024. Even with greener consumables, absolute sheet reduction trims growth, curbing the Hardcopy peripherals and printing consumables market by an estimated 0.6 percentage point.

Semiconductor Supply-Chain Volatility

Laser diodes, power-management ICs, and MEMS sensors remain under allocation, extending printer lead times beyond 12 weeks on some SKUs. HP redesigned controller boards to accept alternative drivers, yet the BOM cost rose. Canon adopted dual-sourcing for image sensors to stabilise its roadmap. Component tightness depresses near-term shipments, restraining the Hardcopy peripherals and printing consumables market even while service revenue climbs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wide-Format Drives Premium Growth

Printers provided 32.65% of 2025 revenue. Wide-format and production presses are projected to outpace the overall Hardcopy peripherals and printing consumables market at 4.95% CAGR, energised by retail banners, vehicle wraps, and corrugated displays. The segment’s contribution to the Hardcopy peripherals & printing consumables market size is poised to climb because UV-LED ink enables sustainable substrates and instant cure. Automation - cutting, and stacking - lets 59% of PSPs quote next-day delivery, a service premium feeding consumables demand.

A4-MFP refresh cycles accelerate under hybrid work. Compact models add card-reader security and cloud connectors, encouraging distributed print architecture. Copiers still serve high-volume campus hubs; 3D printers remain experimental but are now present in 18% of secondary schools across North America. All together, the category maintains steady baseline sheets, ensuring hardware-plus-supplies loops that define the Hardcopy peripherals and printing consumables market.

By Technology: Laser Advances Through Efficiency Gains

Inkjet technology occupied 44.60% of revenue in 2025. Laser is advancing faster at 5.85% CAGR as lower-melting-point toners cut energy by 25% per print job. Educational districts favour lasers for rugged duty cycles and near-instant duplexing. Meanwhile, refillable ink tanks solidify the inkjet foothold in SOHO. Solid-ink engines serve graphics-rich uses, whereas thermal heads dominate logistics labelling with 15-year archive life.

Advanced controllers embed AI that predicts part wear, reducing downtime by up to 30%. Predictive analytics create new service SKUs and lock-in for branded consumables, increasing recurring sales inside the Hardcopy peripherals and printing consumables market.

By End-User: Educational Institutions Embrace Digital Transformation

Commercial/office environments represented a 34.60% share in 2025. Financial and healthcare organisations sustain physical forms for compliance, but migrate to MPS portals that enforce pull-print security. Educational institutions show the highest 4.75% CAGR as hybrid classrooms require on-demand colour course packs and 3D printed lab aids. Government departments keep a steady demand, replacing fleets every five years to satisfy data confidentiality standards.

Residential users pivoted to Wi-Fi ink tanks during lockdowns and keep those devices for home-based micro-businesses. Specialty verticals such as retail pharmacy and quick-service restaurants deploy thermal labelers to speed checkout. Each workflow layer adds niche consumables, protecting value in the Hardcopy peripherals and printing consumables market.

By Distribution Channel: MPS Transforms Business Models

Direct/contractual routes garnered 46.10% of 2025 sales, with enterprises demanding custom SLAs and onsite support. Managed print services expand 5.15% CAGR, providing analytics dashboards and proactive toner replacement. Cloud MPS now runs in 69% of firms, up from 55% in 2023, driven by zero-trust architecture requirements. Subscription PraaS is spreading to mid-market customers: 37% of enterprises already treat print as opex, reducing upfront spend while locking in multi-year consumables flows.

Retail and e-commerce continue to serve SOHO, where fast delivery and price transparency remain critical. Vendors use channel sales data to forecast demand, trimming inventory by 12 days on hand in 2024, improving working-capital efficiency across the Hardcopy peripherals and printing consumables market.

Geography Analysis

North America led with 36.70% of 2025 revenue. The United States generated USD 13.2 billion, propelled by regulated sectors requiring secure print and by subscription PraaS contracts that align spend with ESG objectives. Canada mirrors these patterns, with distributed A4 MFPs replacing A3 copiers as offices downsize. Energy-Star certified laser units qualify for tax rebates, further fuelling upgrades. Together, these factors keep the Hardcopy peripherals and printing consumables market vibrant in the region.

Asia-Pacific will grow fastest at 5.80% CAGR through 2031. China and India issue new industrial permits that call for track-and-trace labels, lifting consumables volumes. India installed 3,400 digital presses across tier-2 cities in 2024, a tenfold rise in four years. Japan remains a technology bellwether, commercialising high-viscosity pigment ink for textiles and ceramics. ASEAN nations leverage government “Industry 4.0” grants to buy cloud-connected MFPs, embedding lifelong consumables demand inside the Hardcopy peripherals and printing consumables market.

Europe shows mature but green-driven evolution. Germany, France, and the United Kingdom push water-based and de-inkable toners to meet circular-economy directives. GDPR steers adoption of secure pull-print, adding license revenue for authentication software. Universities invest in additive manufacturing labs to support STEM research, increasing 3D material purchases. Southern Europe’s tourism rebound fuels hospitality signage, supporting wide-format ink volumes. These trends safeguard the Hardcopy peripherals and printing consumables market size across the continent.

South America and the Middle East and Africa present longer-term upside. Brazil’s growing e-commerce sector requires parcel labels and corrugated printing, lifting entry-level press sales. Colombia’s finance and education verticals drove Kyocera’s 38.2% market share in 2024. Gulf states modernise government services, adding secure MFP clusters. South Africa serves as a regional distribution hub, shortening supply lead times and improving device maintenance KPIs in the Hardcopy peripherals and printing consumables market.

Competitive Landscape

The Hardcopy peripherals & printing consumables market remains moderately concentrated: HP, Canon, Epson, Brother, and Xerox together hold about 70% global revenue. Hardware differentiation flattens as page cost, analytics, and sustainability shape value. HP’s quantum-resistant firmware and AI “perfect print” technology set new security benchmarks. Canon’s Fiery acquisition bolsters end-to-end colour management, deepening workflow integration. Epson rides refillable tanks, shipping 80 million EcoTank units since launch.

Ricoh owns 37.7% of the U.S. continuous-feed inkjet field and 60% in Canada, reflecting a successful vertical focus on transaction and book printing[5]“AI in Print Drives Service Innovation,” Ricoh USA, ricoh-usa.com.

Chinese challengers Pantum and Ninestar exploit cost leadership and rapid firmware updates, widening footprint in Latin America and Africa. Heidelberg partners with Canon to deliver fibre-based packaging lines, targeting brands replacing plastic. Vendors that combine low-carbon devices, predictive service, and secure cloud APIs will gain share as the Hardcopy peripherals & printing consumables market pivots to outcome-based contracts.

Hardcopy Peripherals And Printing Consumables Industry Leaders

HP Inc.

Canon Inc.

Seiko Epson Corporation

Brother Industries Ltd.

Xerox Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: HP launched the AI-powered Amplify 2025 initiative, introducing over 60 new AI PC platforms plus quantum-resistant printers and advanced malware protection, aiming to integrate PCs, print, and collaboration tools, Techaisle.

- April 2025: Ricoh secured the no. 1 position for continuous-feed inkjet in the U.S. (37.7%) and Canada (60.0%), marking its second year at the top Ricoh USA, Inc.

- March 2025: Canon published its Sustainability Report 2025, pledging net-zero CO₂ by 2050 and noting a 12.8% Scope 1-2 and 17.7% Scope 3 reduction versus 2022 Canon Inc.

- February 2025: Kyocera captured 38.2% of Colombia’s print market, installing 70,000 devices with partner Datecsa Kyocera Document Solutions.

- January 2025: Heidelberg unveiled a strategy to add EUR 300 million in sales by 2029, focusing on packaging and digital printing Heidelberg AG.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the hardcopy peripherals and printing consumables market as all new printers, copiers, and multifunction systems (A3-A4, inkjet, laser, and specialty wide-format) sold together with recurring consumables such as ink and toner cartridges, drums, fusers, and maintenance kits, all valued in USD terms. According to Mordor Intelligence, used equipment, stand-alone scanners, and non-printing PC peripherals remain outside this boundary.

Scope exclusion: devices like monitors, keyboards, external drives, and other non-imaging peripherals are not counted.

Segmentation Overview

- By Product Type

- Printers

- Copiers

- Multifunction Peripherals (MFPs)

- Wide-format / Production Printers

- 3-D Printers

- By Technology

- Inkjet

- Laser

- Solid-ink

- Thermal

- By End-User

- Residential

- Commercial / Office

- Educational Institutions

- Government and Public Sector

- Other Applications

- By Distribution Channel

- Direct / Contractual

- Retail and E-commerce

- Managed Print Services (MPS)

- By Geography

- North America

- United States

- Canada

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed hardware OEM managers, tier-one cartridge remanufacturers, managed print service providers, and leading distributors across North America, Europe, and Asia-Pacific. These conversations grounded our assumptions on install-base refresh cycles, cartridge-to-hardware attach rates, and page-volume recovery in hybrid workplaces.

Desk Research

We started with trade and customs data released by UN Comtrade, Eurostat, and the US International Trade Commission, which reveal hardware and cartridge shipment flows by HS code. Statistics from national bureaus (for example, U.S. Census' Quarterly ICT Survey) helped us quantify domestic output, while industry trackers such as IDC's Quarterly Hardcopy Peripherals reports supplied unit mix trends. Vendor 10-K filings, patent portal Questel, and association portals such as the Imaging Supplies Coalition enriched our view on price erosion, channel inventories, and counterfeit exposure. Select paid databases like D&B Hoovers provided revenue splits for second-tier OEMs. This list is illustrative; many other public and paid sources supported fact-checking and clarification.

Market-Sizing & Forecasting

A top-down and bottom-up exercise begins with global hardware shipments from customs and IDC, multiplied by weighted average selling prices extracted from public filings, then layered with modeled cartridge replenishment volumes. Bottom-up roll-ups of sampled supplier revenues and channel checks were used to cross-verify totals before adjustments. Key variables include office employment growth, GDP per capita, remote-work penetration, ink-tank adoption, MPS contract share, and cartridge yield improvements. A multivariate regression, refreshed annually, projects those drivers to 2030, while scenario analysis tests supply-chain or macro shocks. Missing data points, such as smaller country ASPs, were interpolated from nearest proxy markets and validated with regional distributors.

Data Validation & Update Cycle

Every run is triple-checked: analysts compare figures with independent shipment trackers, flag anomalies, discuss variances in weekly peer review, and update the model when material events (major plant closures, regulatory shifts) occur. The published report is refreshed yearly; urgent market moves trigger interim notes before client delivery.

Why Mordor's Hardcopy Peripherals & Printing Consumables Baseline Deserves Your Confidence

Published estimates often diverge because firms pick different device sets, bundle consumables unevenly, or apply distinct currency conversions.

Key gap drivers include varying inclusion of specialty media, differing treatment of subscription ink services, and contrast between our balanced base-case demand outlook and others' single-scenario projections.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 135 B (2025) | Mordor Intelligence | |

| USD 138.6 B (2024) | Comprehensive Consultancy A | Adds ribbons, photo paper, and uses a 2024 base, inflating the figure |

| USD 48.3 B (2023) | Industry Analytics B | Counts printers only, values units with a single global ASP, and omits consumables |

The comparison shows how scope breadth and pricing logic create wide swings; Mordor's disciplined variable selection, multi-step validation, and annual refresh provide a transparent, repeatable baseline for confident planning.

Key Questions Answered in the Report

What is the current value of the Hardcopy peripherals & printing consumables market?

The Hardcopy peripherals & printing consumables market stands at USD 141.14 billion in 2026 and is forecast to reach USD 176.28 billion by 2031.

Which technology is growing fastest?

Laser devices post the quickest rise, advancing at a projected 5.85% CAGR through 2031 thanks to energy-efficient toner and improved total cost of ownership.

Why are managed print services gaining traction?

MPS save organisations 20-30% of printing cost, automate supplies replenishment and incorporate security analytics, prompting a 5.15% CAGR in the distribution segment.

How does hybrid work influence fleet design?

Decentralised teams need secure A4 multifunction printers near workpoints, replacing large A3 copiers and boosting demand for compact, cloud-connected models.

What role do ESG goals play?

Corporate paper-reduction and carbon-footprint targets drive adoption of low-energy devices, refillable consumables and closed-loop recycling, reshaping purchase criteria across the Hardcopy peripherals & printing consumables market.

Which region offers the strongest growth outlook?

Asia-Pacific leads with a 5.80% CAGR to 2031, fuelled by industrial expansion in China and India and rising investments in digital printing infrastructure.

Page last updated on: