Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.93 Billion |

| Market Size (2026) | USD 3.03 Billion |

| Market Size (2031) | USD 3.56 Billion |

| Growth Rate (2026 - 2031) | 3.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Printed Circuit Board Market Analysis by Mordor Intelligence

The Europe printed circuit board market size ize was valued at USD 2.93 billion in 2025 and is estimated to grow from USD 3.03 billion in 2026 to reach USD 3.56 billion by 2031, at a CAGR of 3.28% during the forecast period (2026-2031). Demand pivots toward high-density interconnect (HDI) and IC substrates as automotive electrification, on-shore semiconductor packaging, and data-center upgrades reshape ordering patterns. Flexible circuits for medical wearables, low-loss laminates for telecom gear, and rigid-flex formats for defense systems are capturing capital even while copper-price volatility and Asia-centric laminate sourcing weigh on gross margins. Tier-1 suppliers with IATF 16949 and AS9100 certifications are consolidating automotive and aerospace volumes, whereas dozens of quick-turn specialists still thrive on prototype and low-volume industrial demand. National subsidy programs under the European Chips Act lower the effective cost of capital for new substrate fabs and encourage regional co-location with test and assembly houses.

Key Report Takeaways

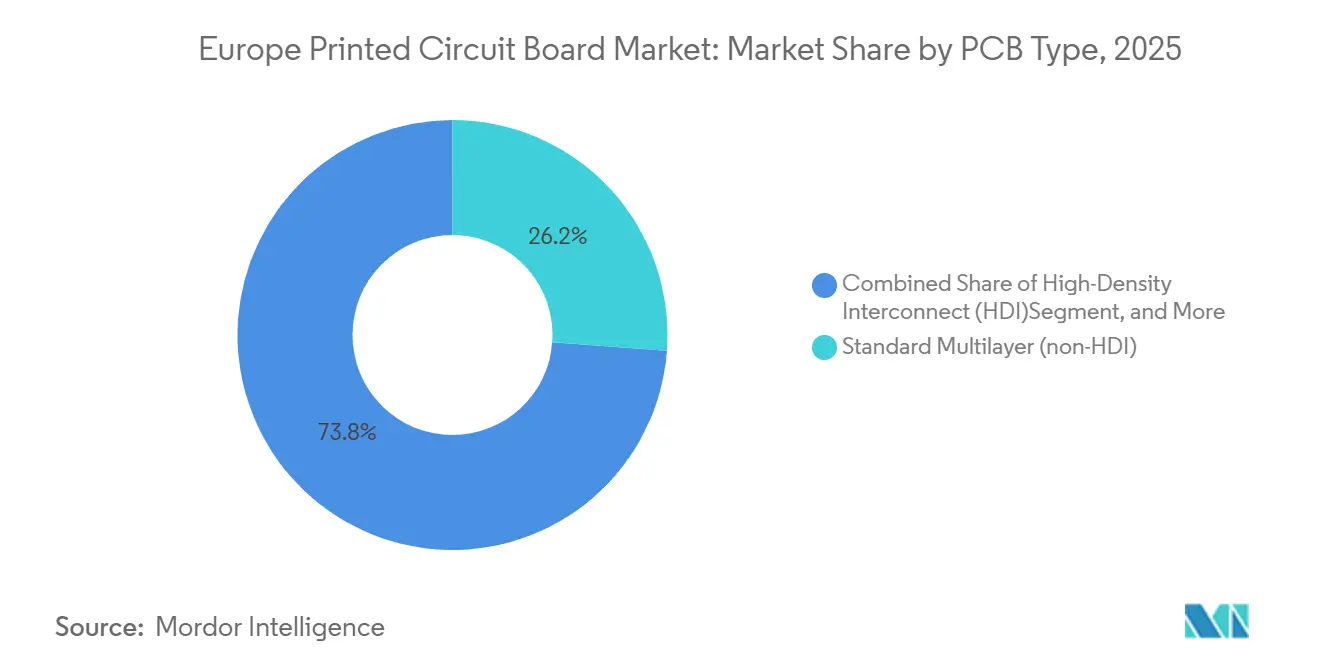

- By PCB type, standard multilayer boards held 26.15% of the Europe printed circuit board market share in 2025, while flexible circuits are forecast to expand at a 4.62% CAGR through 2031.

- By substrate material, glass-epoxy FR-4 captured 41.59% revenue in 2025, and high-speed low-loss laminates are projected to grow at a 4.41% CAGR over 2026-2031.

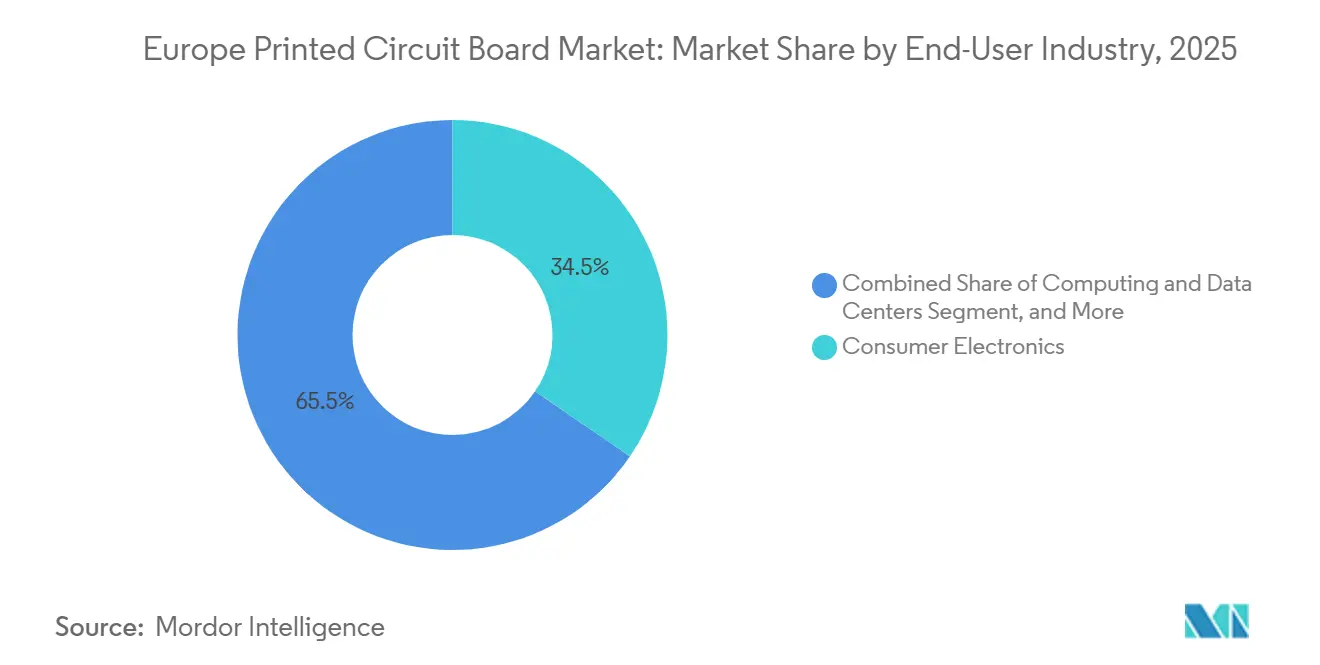

- By end-user industry, consumer electronics accounted for 34.53% demand in 2025, whereas automotive and electric-vehicle applications are advancing at a 4.86% CAGR during the same horizon.

- By geography, Germany commanded 43.77% of 2025 revenue and the United Kingdom is set to register the fastest growth at a 4.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Miniaturization and High-Density Interconnect PCBs | +1.2% | Germany, United Kingdom, Italy, Rest of Europe | Medium term (2-4 years) |

| Rapid Proliferation of Electric Vehicles Requiring Advanced Automotive PCBs | +1.5% | Germany, Italy, Rest of Europe | Medium term (2-4 years) |

| Increasing Research and Development Investment in European PCB Fabs | +0.8% | Germany, United Kingdom, Rest of Europe | Long term (≥ 4 years) |

| Government Subsidies for On-Shore Semiconductor and Packaging Capacity | +0.9% | Germany, Italy, United Kingdom | Long term (≥ 4 years) |

| Regulatory Push for REACH-Compliant Halogen-Free Laminates | +0.4% | Germany, United Kingdom, Italy, Rest of Europe | Short term (≤ 2 years) |

| Surging Adoption of Bio-Compatible Flexible PCBs for Implantable Medical Devices | +0.6% | Germany, United Kingdom, Rest of Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Proliferation of Electric Vehicles Requiring Advanced Automotive PCBs

Electric-vehicle platforms expose boards to -40 °C to 150 °C thermal cycles, 400-ampere currents, and multi-gigabit sensor backbones. European automakers shipped 2.8 million battery-electric and plug-in hybrids in 2025, elevating PCB content per vehicle as 800-volt zone-controller topologies proliferate. AT&S reported 22% year-over-year automotive revenue growth on battery-management and central-computing wins, validating a migration toward HDI and rigid-flex lines that carry gross margins 8-10 points above commodity rigid boards in the Europe PCB market.[1]AT&S Austria Technologie und Systemtechnik AG, “Annual Report 2025,” ats.net

Growing Demand for Miniaturization and High-Density Interconnect PCBs

Wearables and IoT nodes compress board real estate, driving line-and-space targets below 50 µm and via diameters under 100 µm. Würth Elektronik qualified a laser-direct-imaging system capable of 25 µm features in early 2025, supporting power-management modules for industrial and medical gear.[2]Würth Elektronik Group, “Press Release: New Laser Direct Imaging System Qualified,” we-online.com Any-layer HDI and coreless substrates blur the boundary between traditional boards and IC packages, locking suppliers with sequential lamination and modified semi-additive plating into long design-in cycles.

Government Subsidies for On-Shore Semiconductor and Packaging Capacity

The European Chips Act directs EUR 43 billion (USD 48.4 billion) to double the bloc’s semiconductor share by 2030, with sizable tranches earmarked for advanced packaging. Germany budgeted EUR 2 billion (USD 2.25 billion) for pilot packaging lines, while Italy committed EUR 500 million (USD 563 million) to expand IC-substrate output at Agrate Brianza, lowering capital hurdles for PCB makers that co-locate with assembly houses in the Europe PCB Market.

Increasing Research and Development Investment in European PCB Fabs

Fabricators spent EUR 850 million (USD 957 million) on process R&D during 2025, up 37% from 2023. AT&S channeled EUR 120 million (USD 135 million) into glass-core substrates for high-performance computing, and Schweizer Electronic partnered with Fraunhofer IZM on embedded-component boards that cut area by 30%.[3]Fraunhofer IZM, “Embedded-Component PCB Pilot Project,” izm.fraunhofer.de These projects target automotive power electronics, AI accelerators, and implantable devices with gross-margin potential above 35%.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Copper and Laminate Prices Squeezing Margins | -0.9% | Germany, United Kingdom, Italy, Rest of Europe | Short term (≤ 2 years) |

| High Capital Intensity of Next-Gen HDI Production Lines | -0.6% | Germany, United Kingdom, Rest of Europe | Medium term (2-4 years) |

| Extended Lead Times Due to Asia-Centric Laminate Supply | -0.5% | Germany, United Kingdom, Italy, Rest of Europe | Short term (≤ 2 years) |

| PFAS Phase-Out Compliance Costs Across the Value Chain | -0.4% | Germany, United Kingdom, Italy, Rest of Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Copper and Laminate Prices Squeezing Margins

Copper futures averaged USD 9,200 per metric ton in 2025, swinging nearly USD 1,700 inside a quarter and complicating fixed-price contracts. FR-4 sheet quotations rose 14% through Q3 2025 before easing as consumer-electronics demand cooled. Mid-tier board shops running 12-15% gross margins absorbed cost spikes when automotive customers resisted mid-contract adjustments, accelerating consolidation toward scale players that hedge raw materials on the London Metal Exchange impacting the Europe PCB market.[4]London Metal Exchange, “Copper Futures Data 2025,” lme.com

High Capital Intensity of Next-Gen HDI Production Lines

A greenfield 1-N-1 HDI line requires EUR 40-60 million (USD 45-68 million) for laser drilling, sequential lamination, and automated inspection. Schweizer Electronic invested EUR 25 million (USD 28 million) in 2025 to qualify automotive HDI programs, pushing return on invested capital below its weighted-average cost for the year.[5]Schweizer Electronic AG, “Annual Report 2025,” schweizer.ag Smaller fabricators instead focus on quick-turn prototypes, ceding high-volume opportunities to vertically integrated peers in the Europe PCB market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Flexible Circuits Lead Growth Amid Medical and Wearable Demand

Flexible circuits are forecast to expand at a 4.62% CAGR through 2031, the fastest-growing category within the Europe printed circuit board market. Medical wearables, implantable cardiac monitors, and foldable displays rely on polyimide substrates that survive thousands of bend cycles without trace fracture. Standard multilayer boards still commanded 26.15% of Europe printed circuit board market share in 2025, dominating automotive body electronics and industrial automation. Yet design wins are gravitating to HDI formats in smartphones and advanced driver-assistance modules, where layer-count reduction offsets a 2-3× unit-cost premium.

Rigid 1-2 sided boards stay relevant for power supplies and LED lighting, and IC substrates are gaining traction as on-shore packaging lines ramp under Chips Act funding. Rigid-flex boards retain niche appeal in aerospace flight controls and implantable devices, commanding gross-margins above 30% but requiring AS9100 or IATF 16949 certification. Aspocomp reported 31% year-over-year growth in medical-grade flexible revenue after landing a Scandinavian OEM supply deal, underscoring how regulated niches shield suppliers from price competition and enrich the Europe printed circuit board market.

By Substrate Material: High-Speed Low-Loss Laminates Gain Share in Telecom and Data Centers

Glass-epoxy FR-4 accounted for 41.59% revenue in 2025, underscoring its cost efficiency in the Europe printed circuit board market size equation. Yet 5G base stations, 400-GbE switches, and AI accelerators require low-loss materials with dielectric constants below 3.5 and dissipation factors under 0.005. Rogers RO4000 and Isola I-Speed laminates, already qualified by Würth Elektronik for European telecom infrastructure, are projected to expand at a 4.41% CAGR.

Polyimide substrates support under-hood automotive electronics and avionics thanks to glass-transition temperatures above 250 °C. Packaging films such as ajinomoto build-up enable chiplet integration on coreless interposers, fetching 3-5× the price per square meter of FR-4 but unlocking fine-line geometries demanded by advanced packaging. Ceramic and PTFE compounds fill microwave and satellite niches. Hyperscale cloud providers insist on low-loss laminates for 112-Gbps PAM4 backplanes, pushing hybrid stack-ups that marry FR-4 power planes with premium signal layers and elevating average selling prices across the Europe printed circuit board market.

By End-User Industry: Automotive and Electric Vehicles Outpace Consumer Electronics

Consumer electronics contributed 34.53% of 2025 revenue, yet its growth is moderating as smartphone saturation and system-in-package adoption reduce board area per device. Automotive and electric-vehicle systems, by contrast, are projected to grow at 4.86% CAGR through 2031, becoming the prime accelerator for Europe printed circuit board market demand. Battery-management, zone-controller, and 800-volt inverter boards require 0.2 mm microvias, heavy-copper layers, and conformal coatings that justify premium pricing.

Computing and data-center equipment benefit from AI server deployments that demand 20-plus layer stack-ups with controlled impedance. Telecommunications spending on Open RAN densification keeps base-station board demand steady, while industrial automation and renewable-energy inverters deliver mid-single-digit growth. Aerospace and defense remain low-volume but high-margin, shielding qualified suppliers from commoditization. Jabil cited 19% automotive PCB growth in its 2025 report, far above its overall electronics-manufacturing expansion, signaling how electrification pulls the Europe printed circuit board market toward higher value content.

Geography Analysis

Germany generated 43.77% of Europe printed circuit board market revenue in 2025, anchored by automotive platforms that consumed roughly two-thirds of local output. Mittelstand fabricators combine quick-turn prototypes with IATF-qualified HDI mass production, enabling sub-two-week delivery for Tier-1 suppliers. Federal subsidies of EUR 2 billion (USD 2.25 billion) for advanced-packaging pilot lines in Dresden and Munich further strengthen domestic capacity, while battery-electric vehicle production hit 1.2 million units, intensifying demand for zone-controller and battery-management boards.

The United Kingdom is predicted to clock a 4.34% CAGR through 2031, the fastest in the region. A 12% jump in 2025 defense-electronics procurement and GBP 4.2 billion (USD 5.3 billion) in 5G densification outlays are redirecting prototype and small-batch volumes to domestic board shops with AS9100 certification. Defense mandates on secure supply chains favor fabricators such as Exception PCB, while telecom operators specify low-loss laminates for millimeter-wave small cells.

Italy’s concentration in Lombardy and Piedmont leverages proximity to automotive suppliers and industrial machinery builders. STMicroelectronics’ EUR 500 million (USD 563 million) IC-substrate project at Agrate Brianza anchors a budding advanced-packaging cluster set to unlock local rigid-flex and substrate demand from 2027 onward. Rest-of-Europe markets, including Finland, Sweden, Switzerland, Iberia, and Central Europe, collectively supply specialized niches. Finland’s medical-device ecosystem drives biocompatible flexible boards from Aspocomp, Sweden’s NCAB Group orchestrates multisource production for lead-time agility, and Switzerland’s Cicor focuses on HDI rigid-flex assemblies with sub-three-week cycles.

Competitive Landscape

The Europe printed circuit board market balances moderate consolidation at the top with lengthy fragmentation below. AT&S, Würth Elektronik, Schweizer Electronic, NCAB Group, and Aspocomp captured 38% of 2025 revenue, leaving the rest to scores of regional specialists. Automotive and aerospace buyers increasingly single-source from Tier-1 suppliers holding zero-defect track records and embedded-component know-how, while prototype and industrial customers continue to prize lead-time agility over scale.

Technology capability is the chief separator. Market leaders deploy laser direct imaging, modified semi-additive plating, and embedded-passive integration to reach sub-50 µm line widths, enabling them to address high-speed switches, 800-V powertrains, and implantables. AT&S earmarked EUR 300 million (USD 338 million) for an IC-substrate line in Leoben, pursuing vertical integration that moves it closer to chiplet packaging. Würth Elektronik adopts a hybrid model, adding German HDI capacity while leveraging Asian partners for consumer volumes. NCAB’s digital platform aggregates demand across a certified network, trading premium margins for a light asset base that insulates it from capital swings.

White-space opportunities emerge in biocompatible flexible circuits, on-shore IC substrates, and ultra-high-frequency microwave boards where regulatory barriers and process complexity shrink the eligible supplier pool to fewer than ten European plants. IPC-6012 Class 3 and ISO 9001 remain baseline, but competitive advantage now rests on long-term R&D programs and the ability to co-locate with customer engineering teams for rapid iteration.

Europe Printed Circuit Board Industry Leaders

KSG GmbH

Wurth Elektronik Group (Wurth Group)

AT&S Austria Technologie und Systemtechnik AG

NCAB Group AB

Schweizer Electronic AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: AT&S completed a EUR 180 million (USD 203 million) expansion in Leoben, adding 25,000 m² of cleanroom space for IC-substrate production targeting automotive and high-performance computing customers.

- January 2026: Schweizer Electronic and Infineon launched a joint program to embed gallium-nitride transistors directly into PCB substrates for 800-V inverters and data-center power supplies, with prototype validation slated for mid-2026.

- December 2025: Würth Elektronik inaugurated a EUR 45 million (USD 51 million) HDI line in Niedernhall, qualified for 1-N-1 and 2-N-2 automotive stack-ups and an annual capacity of 120,000 m².

- November 2025: NCAB Group acquired a 35% stake in a Polish fabricator for EUR 12 million (USD 13.5 million) to tighten European lead times for automotive and industrial clients.

Europe Printed Circuit Board Market Report Scope

A printed circuit board, or PCB, helps mechanically and electrically connect electronic components utilizing conductive pathways, tracks, or signal traces engraved from copper sheets laminated onto a non-conductive substrate. PCBs dominate electronic devices and can be easily identified as green-colored boards.

The Europe Printed Circuit Board Market Report is Segmented by PCB Type (Standard Multilayer, Rigid 1-2 Sided, High-Density Interconnect, Flexible Circuits, IC Substrates, Rigid-Flex, and Other PCB Types), Substrate Material (Glass Epoxy FR-4, High-Speed Low-Loss, Polyimide, Packaging Resins, and Other Substrate Materials), End-user Industry (Consumer Electronics, Computing and Data Centers, Telecommunications and 5G, Automotive and EV, Industrial and Power, Healthcare Medical, Aerospace and Defense, and Other End-user Industries), and Geography (Germany, United Kingdom, Italy, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Category

| Standard Multilayer PCBs |

| Rigid 1-2-sided PCBs |

| HDI / Micro-via / Build-up |

| Flexible PCBs |

| Rigid-Flex PCBs |

| Other Categories |

By End-User Vertical

| Industrial Electronics |

| Aerospace and Defense |

| Consumer Electronics |

| Communications |

| Automotive |

| Medical |

| Other End-User Verticals |

By PCB Substrate

| FR-4 |

| Metal Core |

| Polyimide |

| Ceramic |

| Other PCB Substrates |

By Layer Count

| 1-2 Layers |

| 4-6 Layers |

| 8-10 Layers |

| more than 10 Layers |

By Assembly Type

| Surface-Mount Technology |

| Through-Hole Technology |

| Mixed Assembly |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Category | Standard Multilayer PCBs |

| Rigid 1-2-sided PCBs | |

| HDI / Micro-via / Build-up | |

| Flexible PCBs | |

| Rigid-Flex PCBs | |

| Other Categories | |

| By End-User Vertical | Industrial Electronics |

| Aerospace and Defense | |

| Consumer Electronics | |

| Communications | |

| Automotive | |

| Medical | |

| Other End-User Verticals | |

| By PCB Substrate | FR-4 |

| Metal Core | |

| Polyimide | |

| Ceramic | |

| Other PCB Substrates | |

| By Layer Count | 1-2 Layers |

| 4-6 Layers | |

| 8-10 Layers | |

| more than 10 Layers | |

| By Assembly Type | Surface-Mount Technology |

| Through-Hole Technology | |

| Mixed Assembly | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How large will the Europe printed circuit board market be by 2031?

It is projected to reach USD 3.56 billion, growing at a 3.28% CAGR between 2026 and 2031.

Which PCB type is expanding the fastest in Europe?

Flexible circuits, benefiting from medical wearables and foldable devices, are forecast to grow at a 4.62% CAGR through 2031.

Why is automotive demand important for European PCB suppliers?

Electric-vehicle architectures need HDI and rigid-flex boards that carry higher margins and longer design-in cycles, pushing automotive applications to a 4.86% CAGR.

What materials are gaining share in high-speed telecom boards?

Low-loss laminates such as Rogers RO4000 and Isola I-Speed are replacing FR-4 in 5G and data-center hardware due to superior signal integrity.

Which country will grow the quickest within Europe?

The United Kingdom is set to post the fastest growth at a 4.34% CAGR through 2031, propelled by defense electronics and 5G densification.

How concentrated is competition in the region?

The top five suppliers account for 38% of revenue, indicating moderate concentration with room for niche and quick-turn specialists.

Page last updated on: