Green Petroleum Coke And Calcined Petroleum Coke Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

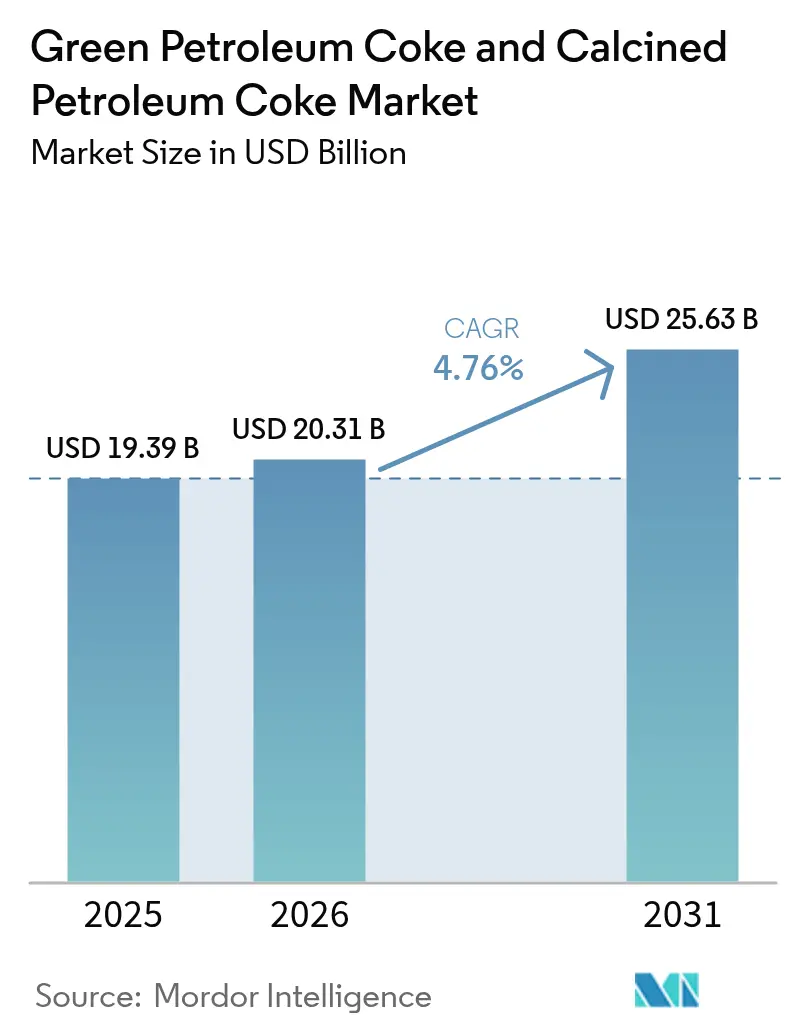

| Market Size (2026) | USD 20.31 Billion |

| Market Size (2031) | USD 25.63 Billion |

| Growth Rate (2026 - 2031) | 4.76% CAGR |

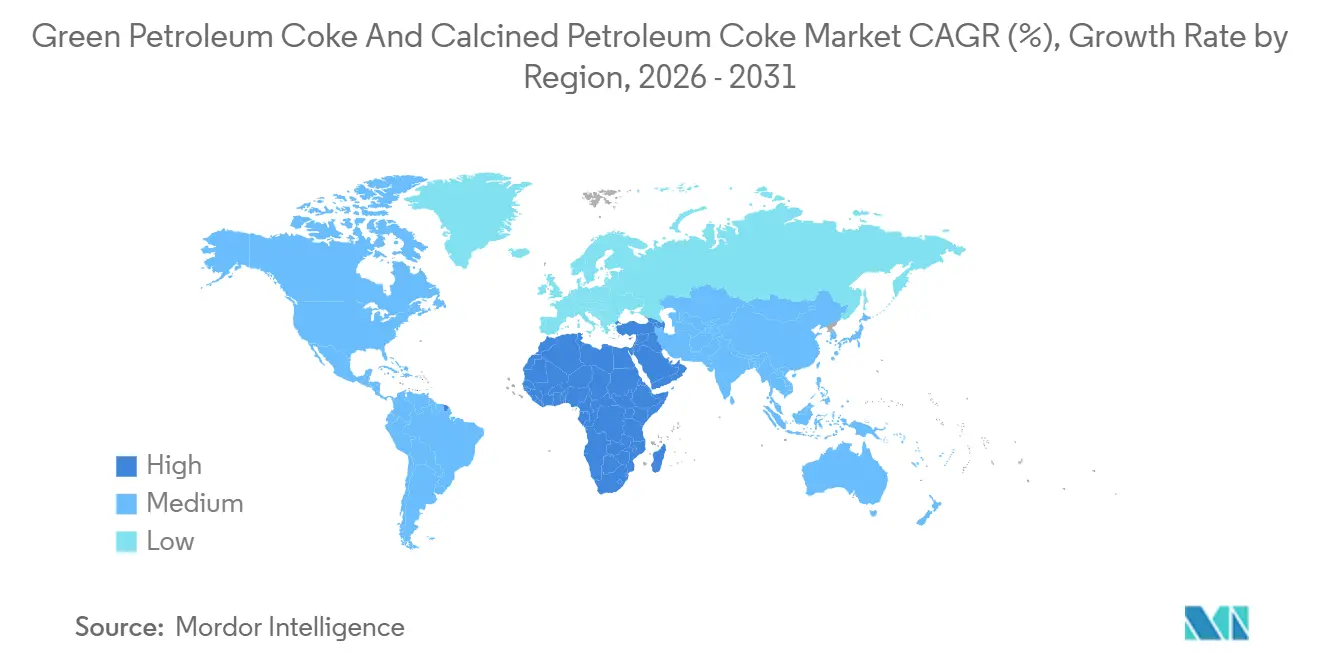

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Green Petroleum Coke And Calcined Petroleum Coke Market Analysis by Mordor Intelligence

The Green Petroleum Coke and Calcined Petroleum Coke Market size is expected to grow from USD 19.39 billion in 2025 to USD 20.31 billion in 2026 and is forecast to reach USD 25.63 billion by 2031 at a 4.76% CAGR over 2026-2031. In price-sensitive regions, the economics of kilns still depend on fuel-grade materials. However, premium ultra-low-sulfur calcined grades are now accessing new value streams, particularly in aluminum anodes, graphite electrodes, and battery materials. In 2025, the Asia-Pacific region had anchored demand, primarily driven by China's aluminum production and India's cement capacity. Middle-East refiners are shifting from exporting crude to in-house delayed coking, which is tightening the global supply of sponge coke. At the same time, the European Union's Carbon Border Adjustment Mechanism (CBAM) and China's stringent ultra-low-emission standards are redirecting trade flows toward markets with less stringent regulations.

Key Report Takeaways

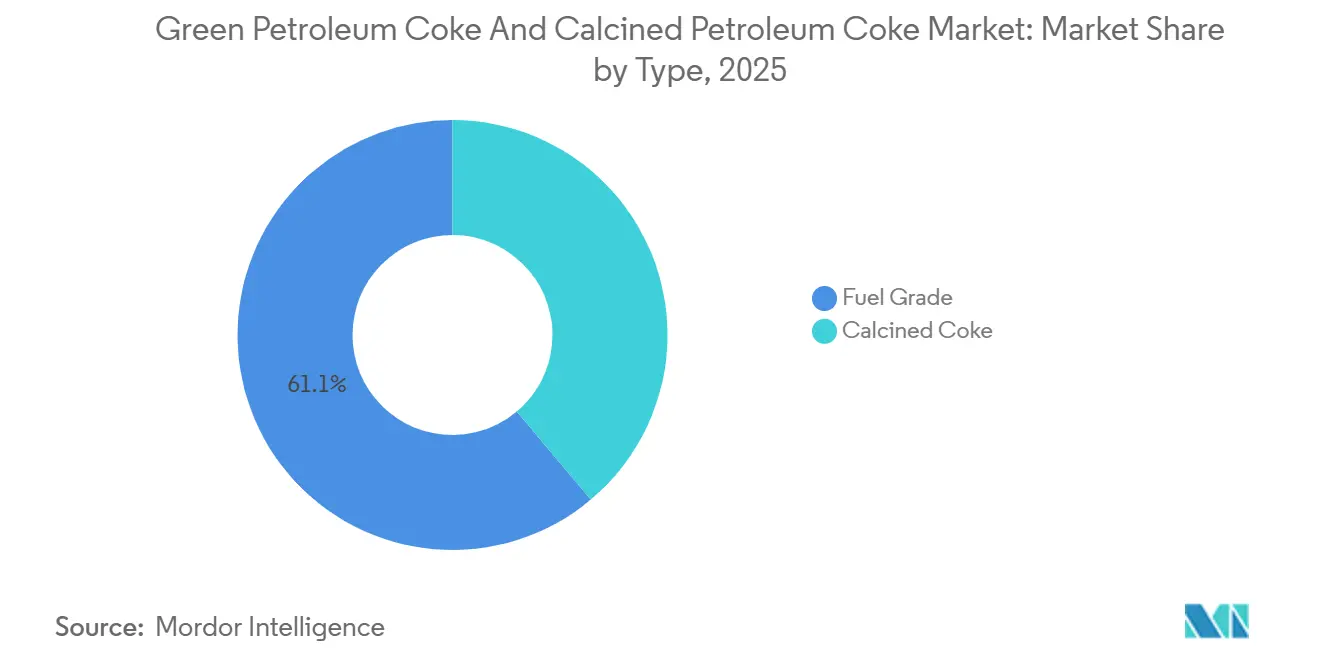

- By type, fuel-grade led with 61.12% green petroleum coke and calcined petroleum coke market share in 2025. Further, calcined coke is forecast to post the fastest growth, advancing at a 5.79% CAGR through 2031.

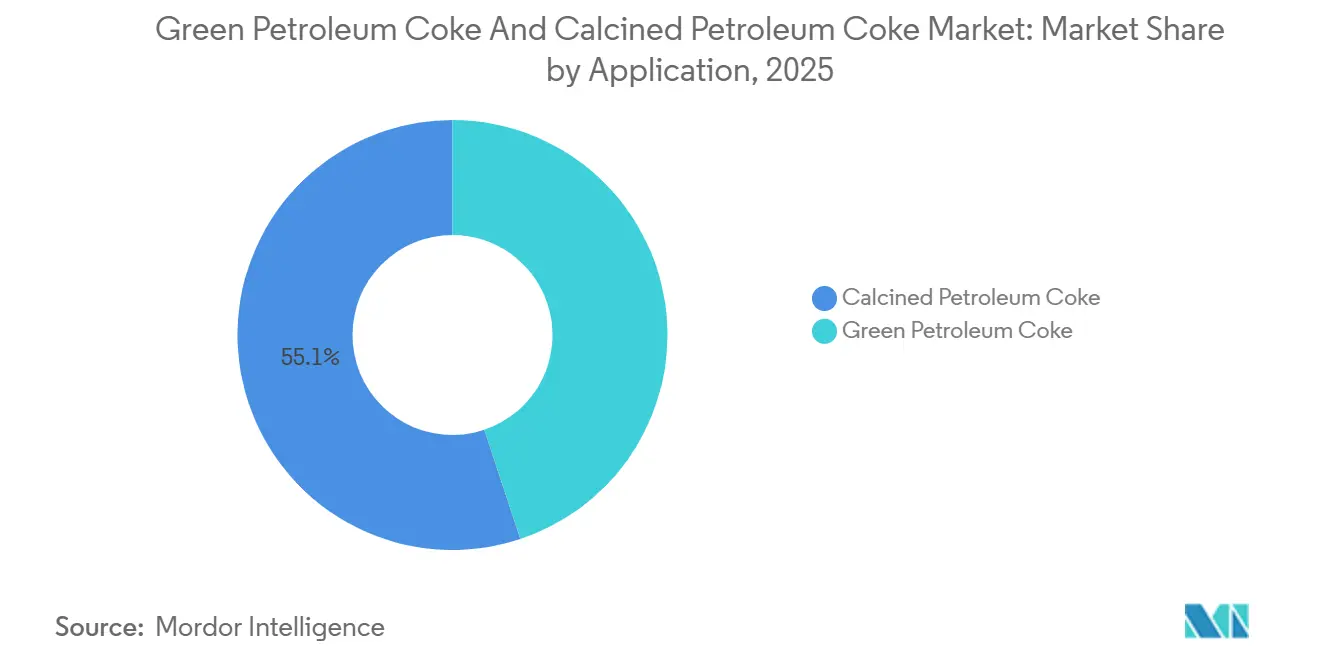

- By application, calcined petroleum coke led with 55.13% green petroleum coke and calcined petroleum coke market share in 2025. Further, green petroleum coke is forecast to post the fastest growth, advancing at a 5.88% CAGR through 2031.

- By geography, Asia-Pacific commanded 48.12% of 2025 revenue, while the Middle-East and Africa segment is projected to record the highest regional CAGR at 5.69% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Green Petroleum Coke And Calcined Petroleum Coke Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fuel-grade petcoke cost advantage in cement kilns | +1.20% | ASEAN core, South Asia, Latin America | Short term (≤ 2 years) |

| Refinery delayed-coking build-outs in Middle-East | +0.90% | Middle-East and Africa, spillover to Asia-Pacific | Medium term (2-4 years) |

| Needle-grade CPC demand for EAF electrodes | +0.70% | Global, concentrated in China, India, Turkey | Medium term (2-4 years) |

| Shift to graphitized cathodes in Chinese Al | +1.10% | China, spillover to Middle-East | Long term (≥ 4 years) |

| Ultra-low-S CPC for Li-ion battery anodes | +0.60% | Asia-Pacific, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fuel-Grade Petcoke Cost Advantage in Cement Kilns

In early 2026, kilns in Vietnam, Thailand, and Indonesia secured contracts for fuel-grade materials at significantly lower costs than thermal-coal equivalents. This led to a reduction in clinker cash costs, even with a decline in construction demand. Thailand's sulfur dioxide limits, set at higher levels compared to the stringent standards in coastal China, allow high-sulfur coke to be transported from U.S. Gulf Coast refineries to Asia-Pacific buyers. This supports a robust U.S. export channel. Semen Indonesia, one of the major players in Indonesia, achieved significant cost savings during the year leading up to 2025. These savings, realized despite kiln utilization rates falling below optimal levels, were strategically reinvested into expansion initiatives.

Refinery Delayed-Coking Build-Outs in Middle-East

By late 2025, Saudi Aramco's Jazan coker and ADNOC's expanded Ruwais unit jointly boosted their capacity for green petcoke. This move allowed them to internalize the value that previously flowed to processors in Asia. Meanwhile, Aluminium Bahrain's Line 6, which utilizes CPC, showcases a seamless transition from refining to smelting, underscoring the trend of vertical integration in the industry.

Shift to Graphitized Cathodes in Chinese Aluminum

Graphitized cathodes reduce cell voltage, leading to significant electricity savings. This has increased demand for CPC with sulfur content below 0.3%, which is priced higher than standard grades. Aluminium Bahrain adopted this technology and successfully reduced its specific energy consumption for aluminum production.

Ultra-Low-S CPC for Li-Ion Battery Anodes

In early 2025, POSCO Future M secured the first-article approval for its new graphitization line, targeting needle coke with low sulfur content. This material is suitable for synthetic-graphite anodes with high energy density. Meanwhile, Phillips 66 allocated significant investment to modify its coker, aiming to increase battery-grade output in 2026.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tighter SOx/PM and EU CBAM regulations | -0.80% | Europe, coastal China, select North American areas | Short term (≤ 2 years) |

| Stricter caps on high-S petcoke combustion | -0.50% | Global, acute in EU, China, California | Medium term (2-4 years) |

| Trade-tariff disruptions (e.g., Brazil-US) | -0.30% | Latin America, spillover to North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tighter SOx/PM and EU CBAM Regulations

As of January 2026, CBAM mandates that importers hand over certificates based on a default emission rate of 3.46 tons CO₂ per ton of petcoke. This regulation has effectively raised the landed cost. As a result, a significant volume of coke from Russia and the United States has been sidelined from EU kilns[1]European Commission, “Carbon Border Adjustment Mechanism,” europa.eu . Meanwhile, China's stringent cement regulations cap SO₂ emissions at less than or equal to 50 mg/Nm³. This has led to costly retrofits for Flue Gas Desulfurization (FGD) systems or, alternatively, a shift to low-sulfur CPC[2].

Stricter Emission Caps on High-S Petcoke Combustion

From 2025, California's South Coast AQMD prohibited solid fuels containing more than 0.5% sulfur. This decision aligns with global trends, dividing the market into high-sulfur fuel streams for the Asia-Pacific region and low-sulfur calcined inputs designed for metals and batteries. Meanwhile, Brazil's proposed sulfur cap is expected to increase petcoke fuel expenses for kilns in São Paulo.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fuel-Grade Dominance Meets Calcined-Coke Momentum

Fuel-grade captured 61.12% of the 2025 value but now grapples with policy-induced contractions in Europe and coastal China. Meanwhile, calcined grades, driven by demand from aluminum, EAF electrodes, and battery applications, are expected to grow at a CAGR of 5.79% during the forecast period of 2026-2031, thanks to their preference for low-sulfur feed. The market for green and calcined petroleum coke, particularly calcined coke, is set to expand, buoyed by new capacities from Gulf and Indian players. Integrated projects in the Gulf are ensuring a steady supply of sponge-coke feedstock with sulfur content at or below 2%. This not only boosts regional self-sufficiency but also curbs price fluctuations. Consequently, there is a noticeable widening in price spreads: fuel-grade coke with 5% to 6% sulfur trades at lower rates, while the anode-grade CPC, boasting less than 0.5% sulfur, commands significantly higher prices. As the European Union's Carbon Border Adjustment Mechanism (CBAM) and emission caps in Asia have tightened, U.S. refiners are redirecting their high-sulfur volumes to the less-regulated ASEAN markets. Simultaneously, they are selling sponge grades into calcination at a premium, highlighting a significant shift in the product mix of the green and calcined petroleum coke market.

By Application: Green Petcoke Fuel and Reductant Uses

Calcined petroleum coke led with 55.13% in 2025, whereas green petroleum coke is projected to grow at a 5.88% CAGR through the forecast period of 2026-2031. This growth is supported by the kiln substitution rates in Vietnam and India, which deliver significant clinker savings. In the iron and steel sector, Indian blast furnaces have adopted the practice of injecting petcoke per ton of hot metal, thereby reducing their reliance on traditional coke ovens. Meanwhile, in the aluminum sector, Söderberg anode applications have been declining as older Chinese smelters transition to the more efficient prebaked technology, which favors calcined coke.

In 2025, aluminum producers consumed a significant portion of calcined petroleum coke (CPC), accounting for the majority of the total calcined output, and maintained a consistent ratio of CPC per ton of aluminum. Titanium dioxide manufacturers utilized CPC, showing a preference for shot coke due to its bulk-density benefits. Needle coke, a key ingredient in electrodes and batteries, has enabled calciners with an exceptionally low coefficient of thermal expansion (CTE) to carve out a profitable niche in the market. Such dynamics highlight the premium market share available for producers of green and calcined petroleum coke who adhere to ISO 6999 specifications.

Geography Analysis

Asia-Pacific led revenue with 48.12% in 2025. However, regulatory crackdowns in coastal China dampened the demand for high-sulfur fuel coke, while simultaneously driving up premiums for ultra-low-sulfur CPC. India, leveraging a cost advantage over domestic coal, imported significant volumes under DGFT quotas, even with the imposed sulfur cap. ASEAN nations purchased substantial quantities, with Vietnamese kilns achieving savings by blending petcoke. Japan and South Korea, although importing modest amounts of needle and ultra-low-sulfur CPC for electrodes and batteries, highlighted the high-value segment of the market. These varied demand hubs ensured a balance in the green petroleum coke and calcined petroleum coke market, juxtaposing bulk fuel volumes against specialty-grade premiums.

The Middle-East and Africa segment is poised for the fastest growth at 5.69% CAGR during the forecast period of 2026-2031. This surge was bolstered by new outputs of green petcoke from Jazan and Ruwais, alongside a planned calciner capacity. Furthermore, regional expansions in aluminum, notably at Alba and Emirates Global Aluminium, anchored a captive offtake for CPC, thereby amplifying the market size for both green and calcined petroleum coke in the Gulf.

In 2025, North America produced significant volumes of petcoke, with a large portion designated as fuel-grade. A significant amount was exported, predominantly heading to Asia and Latin America, a move largely driven by domestic SO₂ limits. Phillips 66, with a focus on the future, allocated a substantial investment for 2026 capital expenditure, concentrating on enhancing coker reliability at its Wood River and Borger facilities. This strategic move ensured flexibility as the demand for heavier Permian barrels increased. Meanwhile, Europe's Carbon Border Adjustment Mechanism (CBAM) reduced demand in cement kilns, redirecting consumption predominantly to aluminum smelters and TiO₂ plants, which together accounted for a notable share in 2025.

Competitive Landscape

The green petroleum coke and calcined petroleum coke market is moderately fragmented. Upstream delayed-coking is primarily dominated by integrated refiners such as ExxonMobil, Chevron, Marathon, and Saudi Aramco. Meanwhile, mid-stream specialists like Rain Carbon, Oxbow, and SCPC are actively converting sponge coke into both anode and needle-grade CPC. Companies in the Middle-East are focusing on achieving deeper vertical integration. For instance, Alba is sourcing significant volumes from SCPC’s kiln in Jubail, and ADNOC’s Ta’ziz unit is set to supply Emirates Global Aluminium. This strategic move shields the region from potential supply disruptions from the United States and China. Phillips 66 strengthened its position with the strategic acquisition of WRB, enhancing its coker capacity. Furthermore, a significant revamp at Ponca City is aimed at producing battery-grade coke by 2026. The industry is increasingly leaning towards technology, focusing on kiln automation and sulfur-recovery processes to adhere to stringent sulfur specifications. Mexico’s Dos Bocas refinery is carving a niche as an emerging exporter, albeit with pricing limitations due to a higher metals content. In summary, while the green and calcined petroleum coke markets showcase moderate concentration, there is a burgeoning opportunity for new calciners in Africa and South Asia to cater to the unmet demand for specialty grades.

Green Petroleum Coke And Calcined Petroleum Coke Industry Leaders

Aluminium Bahrain B.S.C. (Alba)

BP p.l.c

Oxbow Corporation

Phillips 66 Company

Rain Carbon Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Indian chemical producer Epsilon Advanced Materials entered a supply agreement with Phillips 66 for anode-grade green and needle coke sourced from the Lake Charles refinery, underpinning a planned 30,000 t/y graphite-anode plant in North Carolina.

- April 2025: CNOOC Limited lifted petroleum-coke list prices to CNY 4,500/t in Taizhou and CNY 4,320/t in Zhoushan, continuing a multi-month uptrend as domestic supply tightened and low-sulfur demand intensified.

Global Green Petroleum Coke And Calcined Petroleum Coke Market Report Scope

Petroleum coke is a byproduct of oil refineries, and around 75% of petroleum coke produced globally is used as fuel, while the rest is usually either calcined for usage in the aluminum industry or treated for use as metallurgical coke in steel making.

The Green Petroleum Coke And Calcined Petroleum Coke Market is segmented by type, application, and geography. By type, the market is segmented into fuel grade and calcined coke. By application, the market is segmented into green petroleum coke (aluminum, fuel, iron and steel, silicon metal, and others (bricks, glass, carbon products, and others)) and calcined petroleum coke (aluminum, titanium dioxide, re-carburizing market, and others (needle coke, carbon products, etc.)). The report also covers the market size and forecasts for the green petroleum coke and calcined petroleum coke in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Fuel Grade |

| Calcined Coke |

| Green Petroleum Coke | Aluminum |

| Fuel | |

| Iron and Steel | |

| Silicon Metal | |

| Others (Bricks, Glass, Carbon Products, etc.) | |

| Calcined Petroleum Coke | Aluminum |

| Titanium Dioxide | |

| Re-carburizing Market | |

| Others (Needle Coke, Carbon Products, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| Type | Fuel Grade | |

| Calcined Coke | ||

| Application | Green Petroleum Coke | Aluminum |

| Fuel | ||

| Iron and Steel | ||

| Silicon Metal | ||

| Others (Bricks, Glass, Carbon Products, etc.) | ||

| Calcined Petroleum Coke | Aluminum | |

| Titanium Dioxide | ||

| Re-carburizing Market | ||

| Others (Needle Coke, Carbon Products, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the green petroleum coke and calcined petroleum coke market in 2031?

The green petroleum coke and calcined petroleum coke stand at USD 20.31 billion in 2026, and it is projected to reach USD 25.63 billion by 2031 at a 4.76% CAGR.

Which region is expected to record the fastest growth through 2031?

The Middle-East and Africa segment is projected to post a 5.69% CAGR, the highest among all regions.

Why are calcined grades growing faster than fuel-grade petcoke?

Calcined coke meets low-sulfur specifications for aluminum anodes, graphite electrodes, and battery materials, segments that command price premiums and stricter quality requirements.

How does the EU’s CBAM affect petcoke trade?

CBAM adds EUR 15-20 per ton to high-carbon petcoke landing costs, effectively curbing imports into EU cement kilns and redirecting volumes to less-regulated markets.

What is the main driver for needle-grade CPC demand?

Rising electric-arc-furnace steelmaking increases consumption of ultra-high-power graphite electrodes manufactured from needle coke.

Which companies are integrating calcination with aluminum smelting?

Aluminium Bahrain and Emirates Global Aluminium, supported by SCPC and ADNOC’s Ta’ziz calciner, are prime examples of vertical integration.

Page last updated on: