Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

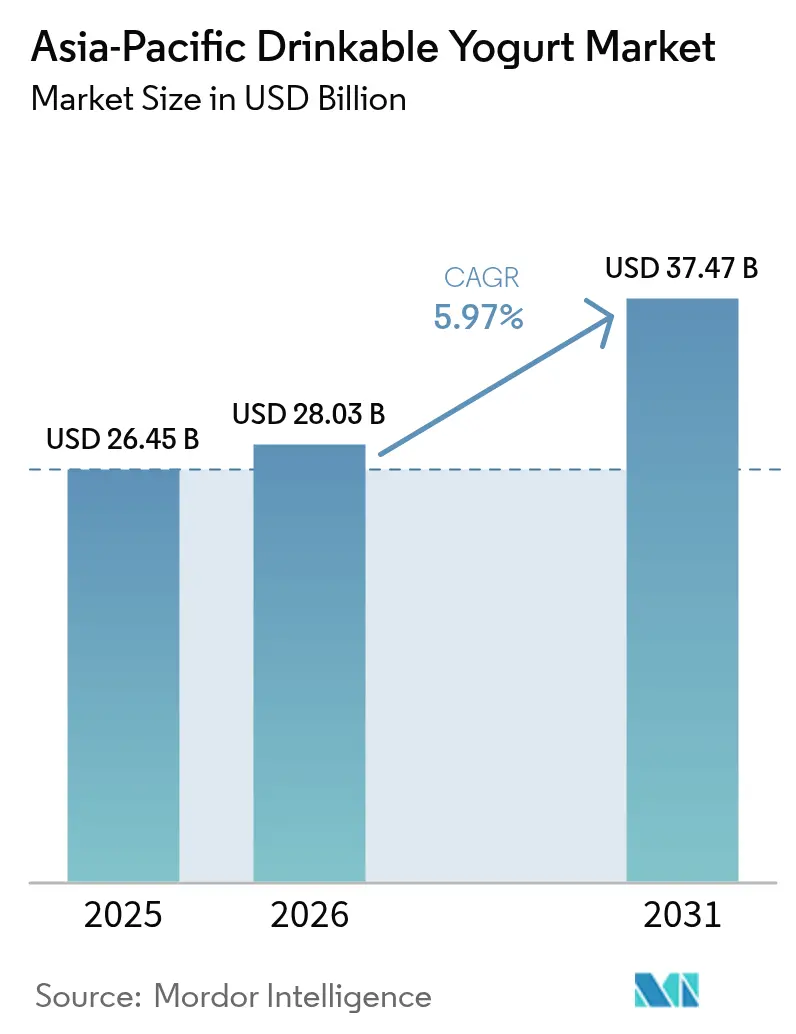

| Base Year Market Size (2025) | USD 26.45 Billion |

| Market Size (2026) | USD 28.03 Billion |

| Market Size (2031) | USD 37.47 Billion |

| Growth Rate (2026 - 2031) | 5.97% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Drinkable Yogurt Market Analysis by Mordor Intelligence

The Asia-Pacific drinkable yogurt market size was valued at USD 26.45 billion in 2025 and estimated to grow from USD 28.03 billion in 2026 to reach USD 37.47 billion by 2031, at a CAGR of 5.97% during the forecast period (2026-2031). Growth is supported by a sustained shift toward health-focused dietary habits, with consumers increasingly choosing probiotic-rich and functional beverages. Rapid urbanization is broadening the consumer base, particularly as busy lifestyles drive demand for convenient, ready-to-drink nutrition formats. Modern retail expansion, spanning supermarkets, convenience stores, and strengthened e-commerce channels, is improving product availability and accelerating premiumization across diverse markets. Together, these structural and behavioral factors are reinforcing steady, multi-country growth across the region.

Key Report Takeaways

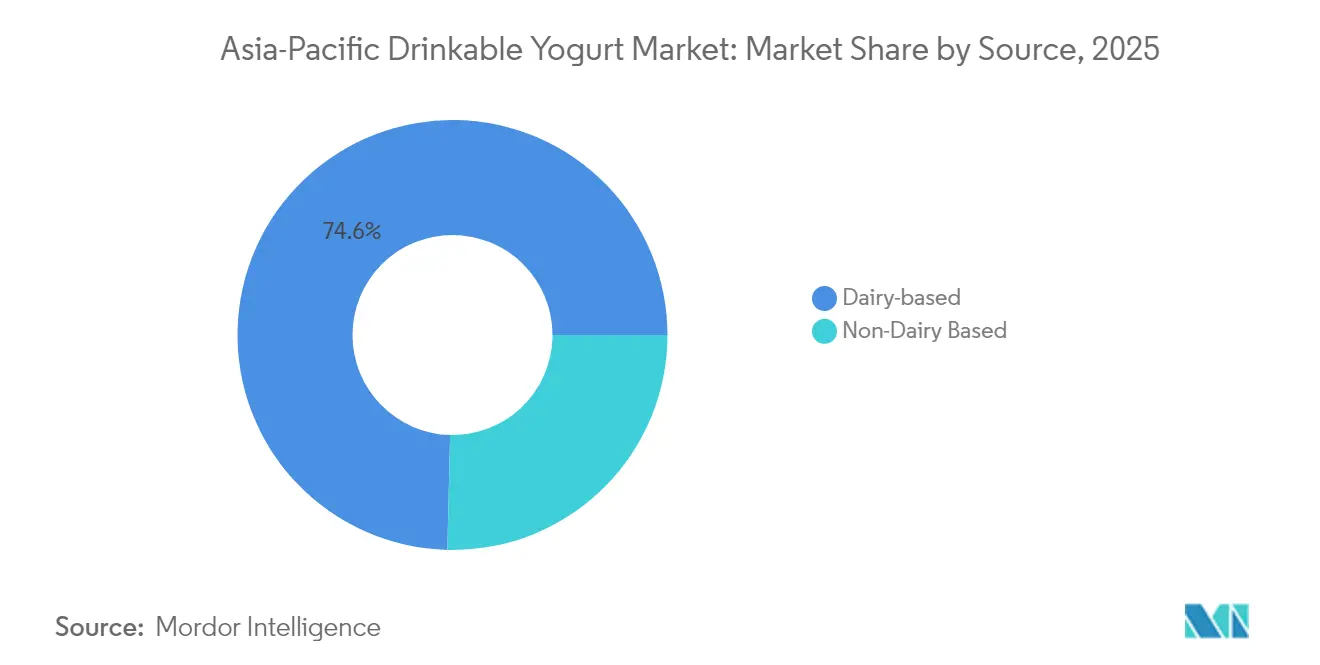

- By source, dairy-based offerings led with 74.62% revenue share in 2025; non-dairy alternatives are projected to advance at 7.69% CAGR through 2031.

- By flavor, flavored variants captured 71.12% share in 2025; un-flavored products are forecast to expand at 7.29% CAGR to 2031.

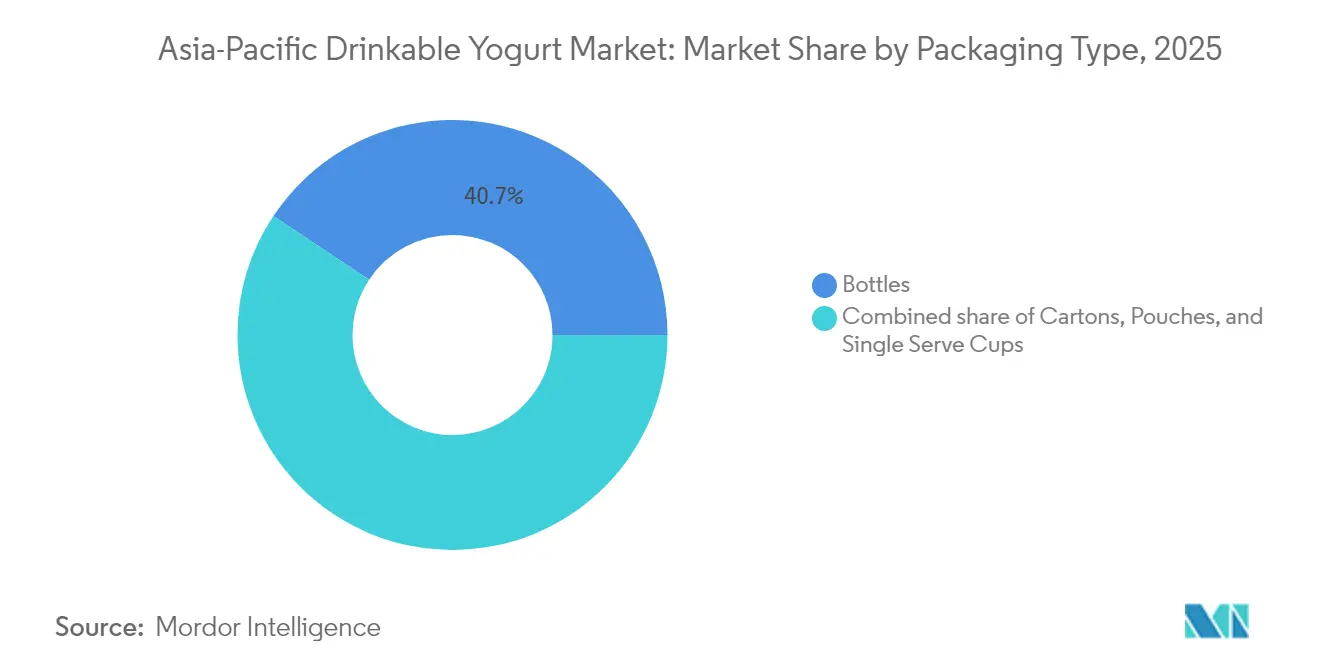

- By packaging, bottles dominated with 40.67% share in 2025; single-serve cups are set to rise at 8.34% CAGR over the forecast horizon.

- By distribution, off-trade channels secured 84.54% share in 2025; on-trade venues are expected to post an 7.78% CAGR through 2031.

- By geography, China accounted for 37.36% of regional value in 2025; South Korea is anticipated to record the fastest 7.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Drinkable Yogurt Market Trends and Insights

Drivers Impact Analysis*

| Increasing consumer health consciousness, leading to demand for probiotic-rich and functional beverages | +1.8% | Global, with concentration in Japan, South Korea, urban China | Medium term (2-4 years) |

| Rising preference for convenient, on-the-go food and beverage options | +1.5% | Urban centers across China, India, Southeast Asia | Short term (≤ 2 years) |

| Urbanization and lifestyle changes leading to adoption of Western dietary habits | +1.3% | Tier-1 and Tier-2 cities in China, India, Indonesia, Vietnam | Long term (≥ 4 years) |

| Expansion of e-commerce and digital sales channels | +1.0% | China, India, Southeast Asia with mobile-first consumers | Medium term (2-4 years) |

| Growing awareness of lactose intolerance and demand for lactose-free or plant-based yogurts | +0.9% | Japan, South Korea, urban India, Australia | Medium term (2-4 years) |

| Rising popularity of clean label and natural ingredients | +0.7% | Japan, Australia, Singapore, affluent urban segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Consumer Health Consciousness Drives Probiotic Innovation

Probiotic-enriched drinkable yogurts have shifted from being niche wellness products to widely accepted functional beverages, driven by growing clinical evidence connecting gut microbiota to immune health, mental well-being, and metabolic regulation. In 2024, Yakult Honsha's Yakult 1000 variant gained significant popularity in Japan. Each bottle contains 100 billion colony-forming units of the Lactobacillus casei Shirota strain, with its sleep-quality benefits supported by peer-reviewed studies. Similarly, in March 2025, Meiji Holdings launched Double Skincare Yogurt, a 112-gram drinkable product formulated with SC-2 lactic acid bacteria, collagen peptides, and sphingomyelin. This product aims to improve UV protection and skin moisture retention, backed by clinical trials involving 67 and 94 participants. The premiumization of such products and the repeat-purchase behavior of health-conscious consumers contributed 1.8 percentage points to the overall 6.05% CAGR.

On-the-Go Convenience Reshapes Packaging and Distribution

Urbanization and shifting commuting habits have made single-serve, portable packaging the fastest-growing segment, with a robust CAGR of 8.75% projected through 2030. In 2024, CJ CheilJedang partnered with GS25 convenience stores in South Korea to launch the Yo-A-Jeong drinkable yogurt, achieving impressive weekly sales of 200,000 units. This highlights the effectiveness of placing products in high-traffic transit areas to attract impulse buyers. In March 2025, Huhtamaki introduced ProDairy recyclable single-coated cups, which reduced plastic content to less than 10% while maintaining cold-chain reliability. This innovation addresses the growing sustainability regulations in markets like Japan and Australia. In Indonesia, the extensive convenience-store networks of Indomaret, with 23,000 outlets, and Alfamart, with 19,000 outlets, provide exceptional distribution for grab-and-go products, catering to the needs of the country’s growing middle class.

E-Commerce Platforms Democratize Access to Premium Formats

Digital sales channels have removed geographic and socioeconomic barriers, making premium drinkable yogurts more accessible. This shift has enabled direct-to-consumer models that eliminate traditional distributor markups. In China, e-commerce platforms like Alibaba's Tmall and JD.com have supported Mengniu's direct sales of YO!FINE DIARY, a high-protein drinkable yogurt. Through targeted digital campaigns and subscription bundles, the product achieved significant revenue growth in 2024. In Indonesia, the Free Nutritious Meals Program, which is expected to increase UHT milk demand by 741,000 metric tons in 2025, is increasingly relying on online procurement platforms[1]Indonesia Ministry of Education. "Free Nutritious Meals Program.", kemdikbud.go.id . These platforms connect smallholder dairy cooperatives, indirectly improving the supply of raw materials for yogurt production. Fonterra launched its probiotic drink, Nurture Digestion+Immunity, in Singapore in 2023 and plans to expand to Indonesia, Malaysia, and Thailand. The company is using e-grocery partnerships to reach health-conscious millennials living in urban high-rise areas. The 1.0 percentage-point CAGR growth highlights the benefits of digital channels, including lower customer-acquisition costs and higher average order values compared to traditional retail stores.

Growing awareness of lactose intolerance and demand for lactose-free or plant-based yogurts

Growing awareness of lactose intolerance is becoming a significant demand catalyst for the Asia-Pacific drinkable yogurt market, as consumers increasingly seek products that offer digestive comfort without compromising taste or nutritional value. Countries such as China, Japan, South Korea, and Southeast Asian nations have high lactose-intolerant populations, pushing manufacturers to expand lactose-free dairy options and accelerate innovation in plant-based formats such as soy-, coconut-, and oat-based drinkable yogurts. This shift is reinforced by rising health consciousness and the preference for “cleaner” labels, encouraging brands to position plant-based and lactose-free variants as healthier, lighter, and gut-friendly alternatives. The availability of these products through modern retail and e-commerce is further strengthening adoption, especially among young urban consumers seeking convenient, functional beverages. As a result, this driver is reshaping product portfolios and intensifying competition, with both global and regional players investing in dairy-free formulations, probiotics, and fortified options to capture emerging demand pockets across the region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain and cold storage infrastructure challenges | -0.9% | Indonesia, Vietnam, Thailand, rural India | Short term (≤ 2 years) |

| Regulatory hurdles and food safety compliance | -0.6% | China, India, Indonesia (halal certification) | Medium term (2-4 years) |

| Shelf life and perishability issues | -0.5% | Southeast Asia, rural markets with intermittent refrigeration | Short term (≤ 2 years) |

| Price sensitivity in emerging markets | -0.7% | India, Indonesia, Vietnam, lower-tier Chinese cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cold-Chain Fragmentation Constrains Market Penetration

In Southeast Asia, the lack of adequate refrigerated logistics remains a significant challenge, particularly during last-mile deliveries, where temperature fluctuations affect the quality and viability of probiotics. In Indonesia, 80% of dairy raw materials are imported, but cold-storage capacity falls short of demand[3]Indonesia Ministry of Agriculture., "Dairy Sector Statistics and Policies.", Pertanian.go.id. As a result, manufacturers focus distribution efforts on Java and Bali, leaving eastern provinces underserved. Similarly, Thailand's dairy sector, which depends heavily on imports from New Zealand, faces supply-chain disruptions during the monsoon season, causing delays in inventory replenishment for drinkable yogurt producers. In India, the cold-chain network covers only 4% of perishable food production. To address this, Yakult has invested in its own fleet of refrigerated trucks and direct-store delivery systems to maintain product quality in tier-2 cities. These logistical constraints reduce the CAGR by 0.9 percentage points, particularly in regions where ambient-temperature alternatives like UHT milk and shelf-stable yogurt capture market share that would otherwise belong to chilled drinkable products.

Regulatory Compliance Complexity Elevates Market-Entry Costs

In the Asia-Pacific region, differing food-safety standards and probiotic-labeling requirements create significant compliance challenges, particularly for smaller manufacturers and new entrants. In India, the Food Safety and Standards Authority requires probiotic claims to be supported by shelf-life stability studies. These studies must confirm a minimum of 10 million CFU per gram at the product's expiration date and require validation from accredited laboratories, costing approximately USD 50,000 per product variant[2]FSSAI. "Food Safety Standards for Probiotic Products.", fssai.gov.in. In Indonesia, all dairy products must secure halal certification, which involves facility audits and ingredient traceability. This process often delays product launches by 6 to 12 months. Similarly, in 2024, South Korea's Ministry of Food and Drug Safety introduced stricter rules for nutrient-content claims, requiring clinical evidence for immune-support assertions. This change benefits established companies like Yakult and Meiji, which have strong R&D capabilities, while putting regional competitors at a disadvantage. These regulatory hurdles have reduced the CAGR by 0.6 percentage points. However, harmonization efforts under the ASEAN Economic Community framework are expected to gradually ease compliance challenges in the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Dairy Dominance Meets Plant-Based Disruption

In 2025, dairy-based drinkable yogurts dominated the market with a 74.62% share, bolstered by well-established supply chains, consumer familiarity, and the compatibility of probiotic strains with bovine milk substrates. Yili Group's Ambrosial brand, a leader in the dairy-based sector, raked in USD 4.2 billion in sales in 2024. Their success stemmed from employing normal-temperature processing, a technique that prolongs shelf life without refrigeration. This innovation proved pivotal for penetrating China's lower-tier cities, which often lack robust cold-chain infrastructure. In 2024, Mengniu's newly commissioned digitalized factory in Ningxia showcased the power of automation. With automated fermentation monitoring and predictive maintenance algorithms, the factory boasted a remarkable 20-fold increase in labor productivity and a 43% reduction in energy consumption. This move underscored how industry incumbents harness scale economies to fortify their dairy-based market share.

Looking ahead, non-dairy alternatives are set to expand at a robust 7.69% CAGR from 2026 to 2031. This growth is largely attributed to the high prevalence of lactose intolerance, estimated between 70% to 90%, in East Asian populations, coupled with younger consumers' rising concerns for environmental sustainability. In March 2024, Bored Cow unveiled a drinkable yogurt alternative, blending fermentation-derived milk protein with coconut cream and probiotics. With an eye on the Asia-Pacific market, the company is gearing up for distribution. Monash University introduced a novel yogurt crafted from lupin and oat, fermented with probiotics. This product not only boasts a 7-day refrigeration stability but also offers superior nutrient density and reduced saturated fat compared to its dairy counterparts, making it an attractive option for Australia's flexitarian consumers. In a clear indication of the shifting landscape, Megmilk Snow Brand made its foray into the plant-based segment in 2024. This move underscores a broader trend: established dairy giants increasingly view non-dairy options as a valuable addition to their portfolios, rather than a direct competition.

By Flavor: Taste Differentiation Versus Clean-Label Minimalism

In 2025, flavored drinkable yogurts held a dominant 71.12% market share, reflecting strong consumer demand for varied tastes. Manufacturers effectively masked the tanginess of probiotics by incorporating fruit essences, sweeteners, and flavor compounds. In China, Haihe Dairy targeted Gen Z consumers in 2024 with unique flavors like coriander and avocado. The company partnered with Xianghe Bobo Shop, Tianjin Museum, and De Yun She to create limited-edition releases that gained significant attention on social media. Yakult India introduced a mango-flavored variant in 2024, leveraging local fruit preferences to aim for a 50% sales increase. This highlights how adapting flavors to local tastes can accelerate market growth in culturally diverse regions.

Un-flavored drinkable yogurts are projected to grow at a 7.29% CAGR from 2026 to 2031, driven by increasing demand from clean-label advocates who prefer minimally processed products with transparent ingredient lists. In 2024, South Korean consumers showed a strong preference for zero- and low-sugar beverages, boosting the demand for un-flavored yogurts that rely on the natural sweetness of dairy instead of added sugars. CJ CheilJedang's production of allulose, a low-calorie sweetener with 70% of sucrose's sweetness and minimal glycemic impact, supports the development of un-flavored yogurts that meet clean-label standards while maintaining taste. In Japan, the aging population is prioritizing functional benefits over flavor indulgence. Morinaga's Bifidus Yogurt Bone Density drink, launched in March 2024 in Pomegranate and Muscat flavors, focuses on improving bifidobacteria levels and calcium absorption for women over 50, addressing their specific health needs rather than emphasizing sweetness.

By Packaging Type: Bottles Yield to Single-Serve Convenience

In 2025, bottles captured a dominant 40.67% share of the market, leveraging a well-established manufacturing base, achieving cost efficiencies at scale, and enjoying deep-rooted consumer trust across generations. Yakult's iconic 65-milliliter bottle, a staple for decades, served up around 40 million servings daily worldwide in 2024. Its compact cylindrical design not only optimizes refrigerator space but also streamlines home delivery. Mengniu's Yoyi C drinkable yogurt comes in 250-milliliter PET bottles with twist-off caps, allowing for one-handed consumption on the go, all while ensuring probiotic viability thanks to oxygen-barrier coatings. Yili's INIKIN ready-to-drink tea, making its debut in 2024 with twist-cap technology, showcases how bottle innovations are branching out from yogurt to other functional beverages in the portfolios of dairy giants.

From 2026 to 2031, single-serve cups are set to expand at a robust 8.34% CAGR. This growth is fueled by urbanization, a surge in workplace consumption, and a push for sustainability, with recyclable formats taking center stage. Huhtamaki's ProDairy cups, rolled out in March 2025, boast a single-coated paperboard design with under 10% plastic content. These cups are strategically aimed at the Europe-Asia-Oceania markets, where regulations penalize multi-material packaging due to extended producer responsibility mandates. In 2024, GS25 convenience stores in South Korea moved a staggering 200,000 units weekly of CJ CheilJedang's Yo-A-Jeong drinkable yogurt, packaged in single-serve cups. This success tapped into the impulse buying tendencies of commuters at the point of purchase. Liquibox, in June 2024, unveiled self-sealing caps for bag-in-box formats. This innovation caters to foodservice operators, emphasizing portion control and minimizing packaging waste, even as the format remains on the fringes of retail channels.

By Distribution Channel: Off-Trade Dominance Faces On-Trade Incursion

In 2025, off-trade channels spanning supermarkets, hypermarkets, convenience stores, and online retail commanded an impressive 84.54% market share, underscoring the perception of drinkable yogurt as a staple grocery item. In Indonesia, the convenience-store landscape is dominated by a duopoly: Indomaret boasts 23,000 outlets, while Alfamart follows closely with 19,000. This extensive network offers unmatched distribution density for off-trade sales. Notably, both chains have expanded their refrigerated sections to prominently feature probiotic beverages. Meanwhile, in China, e-commerce giants Tmall and JD.com have paved the way for Mengniu's direct-to-consumer sales of YO!FINE DIARY. This strategy not only sidesteps traditional distributor margins but also introduces subscription bundles, significantly boosting customer lifetime value.

Forecasts indicate that on-trade venues—ranging from cafes and quick-service restaurants to corporate canteens and hotels—will witness an 7.78% CAGR growth from 2026 to 2031. This surge is attributed to foodservice operators increasingly incorporating probiotic beverages into wellness-centric menus and beverage pairings. A testament to the potential of branded on-trade concepts, Yakult's Gohonmaru Cafe in Japan reported daily sales of 20,000 ice creams in 2024, highlighting the ability of such venues to influence off-trade purchase intentions. In Malaysia, Farm Fresh debuted its Jom Cha yogurt soft-serve in 2024, ingeniously merging drinkable yogurt with tea flavors. This move targets cafe-loving millennials in search of Instagram-worthy, functional treats. Nestle forged a collaboration with Cha Yan Yue Se, a prominent Chinese milk-tea chain, rolling out healthier drinkable yogurt-based beverages in 2024. This partnership capitalizes on the chain's expansive network of over 4,000 outlets, aiming to make probiotic consumption a norm among Gen Z.

Geography Analysis

In 2025, China held a 37.36% market share, driven by Yili Group and Mengniu Dairy's dominance in normal-temperature and chilled yogurt. Yili, valued at USD 11.6 billion, remained the world's top dairy brand for the fifth year, with Ambrosial yogurt generating over USD 4.2 billion in sales. Bright Dairy led in East China, while smaller players like Haihe Dairy and Blue Sea Dairy targeted Gen Z with unique flavors such as coriander and avocado, along with co-branding initiatives. Junlebao's 2023 acquisition of a 30% stake in More Yogurt, a chain with 1,600+ stores, highlighted its focus on vertical integration to optimize distribution and retail margins. In July 2024, China's National Health Commission approved Morinaga's Bifidobacterium infantis M-63 for infant foods, marking the third probiotic strain approved after M-16V in 2016 and BB536 in 2022, emphasizing innovation in functional ingredients.

South Korea is projected to grow at a 7.35% CAGR from 2026 to 2031, fueled by demand for protein-rich and low-sugar products. In 2024, CJ CheilJedang's Yo-A-Jeong drinkable yogurt sold 200,000 units weekly through GS25 convenience stores, leveraging the country's 50,000+ convenience outlets. By 2024, 73% of consumers preferred zero- and low-sugar options, prompting manufacturers to use allulose, a low-calorie sweetener produced by CJ, Daesang, and Samyang. The fermented milk market is expected to register a positive growth in 2025, with drinkable formats gaining share over spoonable yogurts. Yonsei Dairy acquired Purmil's Jeonju yogurt facilities in December 2023, relocating production to its Asan plant and starting operations in Q2 2024, reflecting consolidation trends among mid-tier players.

Australia, Thailand, Singapore, and the Rest of Asia-Pacific present growth opportunities. In 2024, Fonterra began divesting its Australian consumer business, with FrieslandCampina as a potential buyer, signaling a shift toward ingredients and foodservice. Chobani Australia reduced plastic packaging by 50% in 2024, aligning with stricter recycling regulations. In 2023, Fonterra distributed Anchor Actif-Fiber and Anchor Beaute through Thailand's 7-Eleven stores, using single-serve cups to highlight functional benefits. Thailand-based Yoguruto expanded to the Philippines, Myanmar, Indonesia, Singapore, and Malaysia in 2024, offering customizable drinkable yogurt bowls that combine beverage and meal replacement. Yo-Chi opened its first international outlet in Singapore in August 2025, targeting the health-conscious, high-income market to test demand for frozen yogurt.

Competitive Landscape

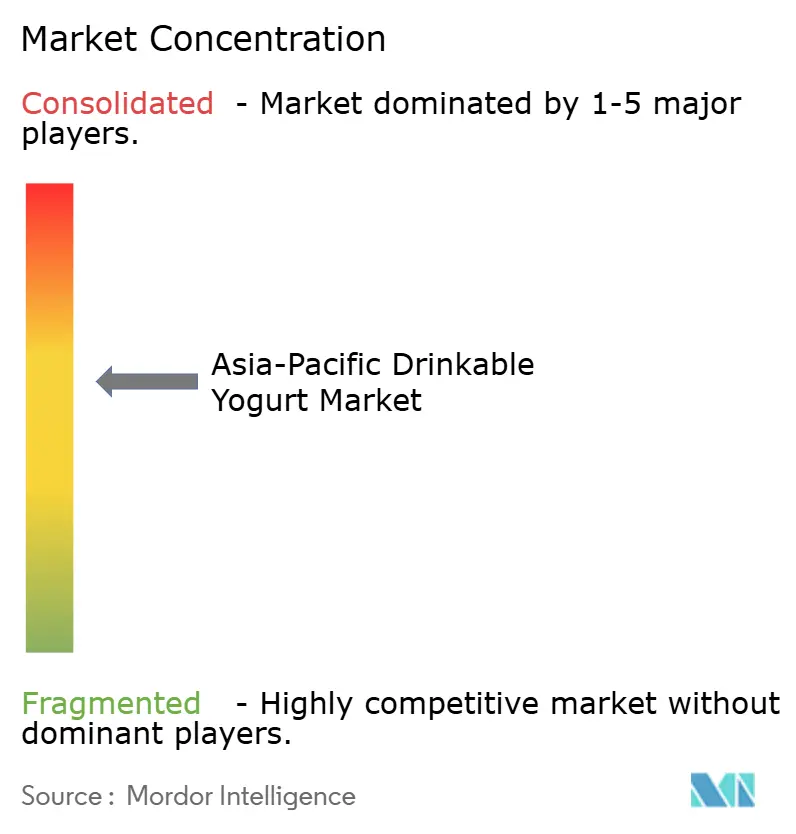

The Asia-Pacific drinkable yogurt market is moderately concentrated, with five major players leading the competition. These key players include Inner Mongolia Yili Industrial Group Co., Ltd. (Yili Group), China Mengniu Dairy Company Limited, Yakult Honsha Co., Ltd., Danone S.A., and Meiji Holdings Co., Ltd. These companies focus on strategies such as mergers, expansions, acquisitions, partnerships, and new product launches to strengthen their brand presence and maintain a competitive edge in the market.

Opportunities remain in the plant-based drinkable yogurt segment, where non-dairy alternatives account for only 24.79% of the market share in 2024. This is despite the fact that over 70% of East Asians are lactose intolerant. The reluctance of established players to shift focus from their dairy-based portfolios has created room for specialized entrants like Bored Cow and Monash University, which are introducing innovative products such as lupin-oat formulations to cater to this demand.

Smaller players, including Haihe Dairy and Blue Sea Dairy, are adopting creative strategies to capture consumer attention. They are forming co-branding partnerships with popular names like Xianghe Bobo Shop, Tianjin Museum, and De Yun She. These collaborations are driving social media buzz and attracting Gen Z consumers. By leveraging influencer marketing and launching limited-edition products, these companies are effectively reducing traditional advertising costs while increasing brand visibility.

Asia-Pacific Drinkable Yogurt Industry Leaders

-

Inner Mongolia Yili Industrial Group Co., Ltd. (Yili Group)

-

China Mengniu Dairy Company Limited

-

Yakult Honsha Co., Ltd.

-

Danone S.A.

-

Meiji Holdings Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Meiji has expanded its product line with the launch of its new functional yogurt targeting UV protection and skin hydration. According to the brand, this 112g drinkable yogurt is designed for easy consumption, aligning with current consumer preferences for convenient and health-focused food options.

- August 2024: Meiji Co., Ltd., a wholly-owned subsidiary of Meiji (China) Investment Co., Ltd., launched a new drinkable yogurt product made using a proprietary lactobacillus discovered in raw milk from Tokachi, Hokkaido.

- January 2024: Kirin Beverage Company, Limited, launched its new Kirin iMUSE Karada Omoi Yogurt Taste, a functional drinkable yogurt containing Kirin's proprietary L. lactis strain plasma.

Asia-Pacific Drinkable Yogurt Market Report Scope

The drinkable yogurt market in Asia-Pacific has been segmented by category into dairy-based and non-dairy based; by type into plain and flavored yogurt; and by distribution into hypermarket/supermarket, convenience stores, specialty stores, online channel and others. Also, the study provides an analysis of the drinkable yogurt market in the emerging and established markets across Asia-Pacific, including China, Japan, India, Australia, and Rest of Asia-Pacific.

Source

| Dairy-based |

| Non-dairy based |

Flavour

| Flavoured |

| Un-flavoured |

Packaging Type

| Bottles |

| Cartons |

| Pouches |

| Single-serve cups |

Distribution Channel

| On-trade | |

| Off-trade | Convenience Stores |

| Specialist Retailers | |

| Supermarkets and Hypermarkets | |

| On-line Retail | |

| Others |

Country

| China |

| India |

| Japan |

| Australia |

| Indonesia |

| South Korea |

| Thailand |

| Singapore |

| Rest of Asia-Pacific |

| Source | Dairy-based | |

| Non-dairy based | ||

| Flavour | Flavoured | |

| Un-flavoured | ||

| Packaging Type | Bottles | |

| Cartons | ||

| Pouches | ||

| Single-serve cups | ||

| Distribution Channel | On-trade | |

| Off-trade | Convenience Stores | |

| Specialist Retailers | ||

| Supermarkets and Hypermarkets | ||

| On-line Retail | ||

| Others | ||

| Country | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How large is the Asia-Pacific drinkable yogurt market in 2026?

The Asia-Pacific drinkable yogurt market size reached USD 28.03 billion in 2026.

What CAGR is projected for Asia-Pacific drinkable yogurt through 2031?

The market is forecast to register a 5.97% CAGR from 2026 to 2031.

Which country contributes the most value?

China accounted for 37.36% of regional sales in 2025.

Which packaging format is growing fastest?

Single-serve cups are projected to expand at an 8.34% CAGR as commuters favor portable options.

Page last updated on: