Ghana Grain Market Analysis by Mordor Intelligence

The Ghana grain market size was valued at USD 6.08 billion in 2025 and estimated to grow from USD 6.29 billion in 2026 to reach USD 7.51 billion by 2031, at a CAGR of 3.57% during the forecast period (2026-2031). Robust policy backing, rising feed industry demand, and a national push toward food self-sufficiency are the primary growth engines. Drought-driven supply shocks in 2024 exposed the constraints of rain-fed farming, intensifying public and private investments in irrigation, climate-smart seeds, and mechanization. Digital advisory tools such as Farmerline’s Mergdata platform shorten information gaps, lifting yields and incomes, and improving smallholder resilience. Meanwhile, regional supply disruptions, including Burkina Faso’s February 2025 cereal export ban and Red Sea freight cost surges, have magnified the strategic value of domestic output diversification and post-harvest infrastructure. Competitive dynamics are shifting as multinational processors, local millers, and ag-tech firms race to secure grain offtake agreements, warehouse capacities, and input distribution networks.

Key Report Takeaways

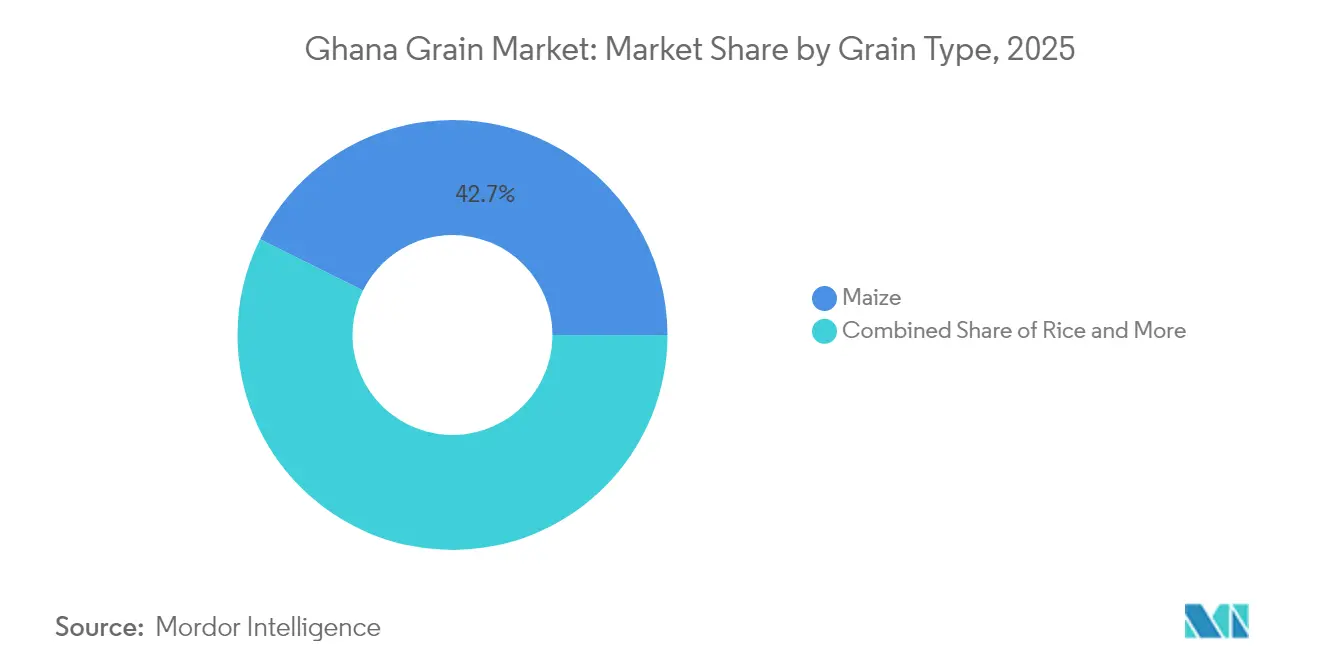

- By grain type, maize led with 42.65% of the Ghana grain market share in 2025, while rice is projected to register the fastest 5.57% CAGR through 2031, outpacing all other grains.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Ghana Grain Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed input-credit schemes | +0.8% | National, concentration in Northern and Upper regions | Medium term (2-4 years) |

| Expansion of grain warehousing receipt system | +0.6% | National, early deployment in Ashanti and Eastern regions | Long term (≥ 4 years) |

| Emergence of commodity exchanges in West Africa | +0.4% | Regional, Ghana–Nigeria corridor emphasis | Long term (≥ 4 years) |

| Mobile-enabled agronomy advisory platforms | +0.7% | National, higher penetration in Southern Ghana | Short term (≤ 2 years) |

| Pivot to climate-resilient seed varieties | +0.9% | National, priority in drought-prone Northern regions | Medium term (2-4 years) |

| Surge in regional demand from feed mills | +0.5% | West Africa, Ghana as a supply hub | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-backed input-credit schemes

The April 2025 Feed Ghana Programme marked a structural shift toward commercial farming, earmarking GHS 1,000 (USD 83.3) per hectare compensation for drought-hit growers and mobilizing USD 500 million for subsidized inputs.[1]Source: Ministry of Food and Agriculture, “Feed Ghana Programme to Create Jobs and Strengthen the Agro-Industry,” MOFA.gov.gh The initiative aligns with the National Agriculture Investment Plan, which channels no less than 10% of the national budget into agriculture to sustain 6% annual sector growth. Newly formed farmer cooperatives broaden collective bargaining power for credit, mechanization services, and certified seeds. Digital extension support strengthens program effectiveness, with a significant majority of mobile-advised farmers adopting climate-smart practices compared to noticeably lower rates among non-users.

Expansion of grain warehousing receipt system

Rolled out in 2024, the warehouse receipt system allows farmers to collateralize stored grain, reducing distress sales and easing working-capital shortages. Linkage with the Ghana Commodity Exchange introduces transparent electronic bidding, diminishing rural information asymmetries that once depressed farm-gate prices. Ongoing debate over optimal silo placement escalates the policy spotlight on logistics corridors serving major surplus zones.

Mobile-enabled agronomy advisory platforms

Farmerline now serves 2.2 million growers via vernacular voice messaging, short messaging, and smartphone dashboards. Complementary initiatives, including MTN Ghana’s Iska Weather service, deliver field-level climate intelligence directly to feature phones, boosting adoption of row planting, zero tillage, and drought-tolerant seeds by up to 47.2% compared with non-users. National Artificial Intelligence Strategy priorities align with these solutions, incentivizing public–private partnerships in predictive agronomy and logistics optimization.

Pivot to climate-resilient seed varieties

Relentless drought episodes have catalyzed the adoption of drought-resilient maize, sorghum, and millet lines promoted by the Council for Scientific and Industrial Research-Savanna Agricultural Research Institute (CSIR-SARI). Field trials in Gushegu show a significant yield increment per acre and notable income gains, illustrating strong returns on seed replacement. Integration of certified seed programs with digital extension channels expands outreach, while rising feed mill demand quickens commercial uptake across poultry and aquaculture supply chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent post-harvest losses | −1.2% | National, higher impact in Northern and Upper regions | Short term (≤ 2 years) |

| Limited mechanized irrigation coverage | −0.9% | National, acute impact in drought-prone areas | Long term (≥ 4 years) |

| Volatile farm-gate pricing | −0.7% | National, rural areas most affected | Short term (≤ 2 years) |

| Escalating ocean-freight rates after Red Sea route disruptions | −0.5% | Global, import-dependent segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited mechanized irrigation coverage

Only 10,262 hectares, less than 2% of Ghana’s estimated 1.9 million-hectare irrigable area, benefit from controlled water delivery, leaving 74% of rice growers reliant on erratic rainfall. The 2024 drought shrank corn output projections to 2.6 million metric tons, 19% below the five-year average.[2]Source: U.S. Department of Agriculture, “Ghana Grain and Feed – Update – 2024,” USDA.gov High capital costs, scarce spare parts, and limited long-term credit inhibit uptake of water-lifting pumps and drip systems. The 3,000-hectare Kpong refurbishment and donor-backed community schemes offer incremental gains but cannot close the vast deficit alone. National water withdrawal for irrigation, 652 million cubic meters, suggests that a resource is available, but distribution infrastructure and affordable finance are missing.

Escalating ocean-freight rates after Red Sea route disruptions

Attacks on container vessels navigating the Suez–Red Sea corridor increase the freight rates. Ghana, which imports its major wheat requirement, faced surging bread prices alongside foreign exchange pressures. Higher import parity prices funnel demand toward local maize, rice, and sorghum, yet they also inflate fertilizer and machinery costs, stressing farm budgets. Longer transit times further complicate inventory planning for millers and feed formulators that operate on thin working-capital margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grain Type: Maize Dominance Faces Climate Resilience Pressure

Maize retained a commanding 42.65% share of total consumption value in 2025, underscoring its staple status in human diets and feed rations within the Ghana grain market. Input inflation has been severe: production costs jumped 600% from GHS 1,200 to GHS 8,100 (USD 100 to USD 675) per acre between 2020 and 2024, prompting many smallholders to cut fertilizer application rates. As a result, the Ghana grain market size for maize could face downside risk in 2025 if yield recovery initiatives lag behind climate shocks. The Feed Ghana Programme’s subsidy packages and the warehouse receipt system partially cushion growers, while forward contracting with poultry and aquaculture integrators stabilizes offtake. Expansion of silage-based feeding systems among cattle producers offers a nascent new demand pocket.

Rice constitutes the fastest-growing share of the Ghana grain market, with a 5.57% CAGR projected through 2031, driven by shifting urban consumption patterns and government import-substitution ambitions.The Ghana grain market size for rice is projected to climb as millers invest in color sorting, parboiling lines, and packaging automation to meet rising quality expectations. CSIR-SARI climate-smart cultivars deliver yield stability in low-rainfall zones, enhancing farmer uptake. Millet remains niche but strategically vital in semi-arid districts. Modest productivity gains combined with higher drought resilience position the crop as an insurance hedge within the Ghana grain market. Wide adoption of zero tillage, row spacing, and residue management could raise aggregate millet and sorghum yields by up to 30% by 2030.

Geography Analysis

Northern, Upper East, and Upper West regions command the largest cultivated area for maize, sorghum, and millet, yet suffer the highest exposure to drought-induced shortfalls. The 2024 dry spell cut corn yields by up to 30% in these zones, emphasizing the need for accelerated irrigation pump financing and weather-indexed insurance. Southern regions (Ashanti, Eastern, Volta, and Central) concentrate commercial rice paddies and benefit from better road networks, enabling rapid market access and higher farm-gate prices. Nevertheless, post-harvest losses remain elevated where drying platforms and paved feeder roads are scarce.

Cross-border trade links are recalibrating after Burkina Faso halted cereal exports in February 2025, disrupting flows via the Paga and Hamile corridors. Ghana’s strategic alliance with Nigeria through the commodity exchange and forthcoming twenty-four-hour port operations in Tema and Takoradi recasts the country as a potential staple hub for the Gulf of Guinea. Planned barge services on the Volta Lake could slash North–South transport cost by 20%, improving competitiveness for Northern producers.

International supply shocks now reverberate more acutely in coastal urban centers where imported wheat is milled. Freight spikes via the Red Sea and longer Cape routing elevate landed costs, spurring consumer substitution toward locally milled rice and composite flour blends. The government’s USD 25 billion Climate Futures initiative allocates substantial funds for ecosystem restoration across 12 million hectares, with watershed rehabilitation anticipated to stabilize water tables in food-producing zones.

Recent Industry Developments

- June 2025: Ghana plans to construct a rice mill in the Northeast region with an annual processing capacity of 30,000 metric tons of paddy rice. The facility aims to minimize post-harvest losses and decrease the country's dependence on rice imports. The World Food Program-supported initiative intends to reinforce Ghana's domestic rice value chain and improve food security.

- May 2025: The Ministry of Food and Agriculture in Ghana implemented a nationwide farmer cooperative program under the Feed Ghana initiative to enhance food security and agricultural business development. The program provides smallholder grain-growing farmers with access to mechanization services, financial resources, agricultural training, and market connections to strengthen the country's agricultural sector.

Ghana Grain Market Report Scope

Grain is the harvested seed of grasses, such as wheat, oats, rice, corn, etc. The Ghana Grain Market Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Export Analysis (Value and Volume), Import Analysis (Value and Volume), and Price Trend Analysis. The Market is Segmented by Crop Type (Maize, Millet, Sorghum, and Rice). The report offers market size and forecast based on value (USD) and volume (metric tons) for the above segments.

By Grain Type (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis)

| Maize |

| Rice |

| Sorghum |

| Millet |

| By Grain Type (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis) | Maize |

| Rice | |

| Sorghum | |

| Millet |

Key Questions Answered in the Report

What is the current value of the Ghana grain market and its forecast growth rate?

The market is valued at USD 6.29 billion in 2026 and is projected to expand at a 3.57% CAGR to USD 7.51 billion by 2031.

Which grain holds the largest share of domestic consumption?

Maize leads with 42.65% of consumption value in 2025.

Why are warehouse receipt systems important for Ghanaian farmers?

They allow farmers to use stored grain as collateral, reducing forced sales and improving access to affordable credit.

What are the key challenges limiting grain output growth?

High post-harvest losses, limited irrigation coverage, volatile farm-gate prices and elevated freight costs constrain expansion.

Page last updated on: