Glyphosate Herbicide Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

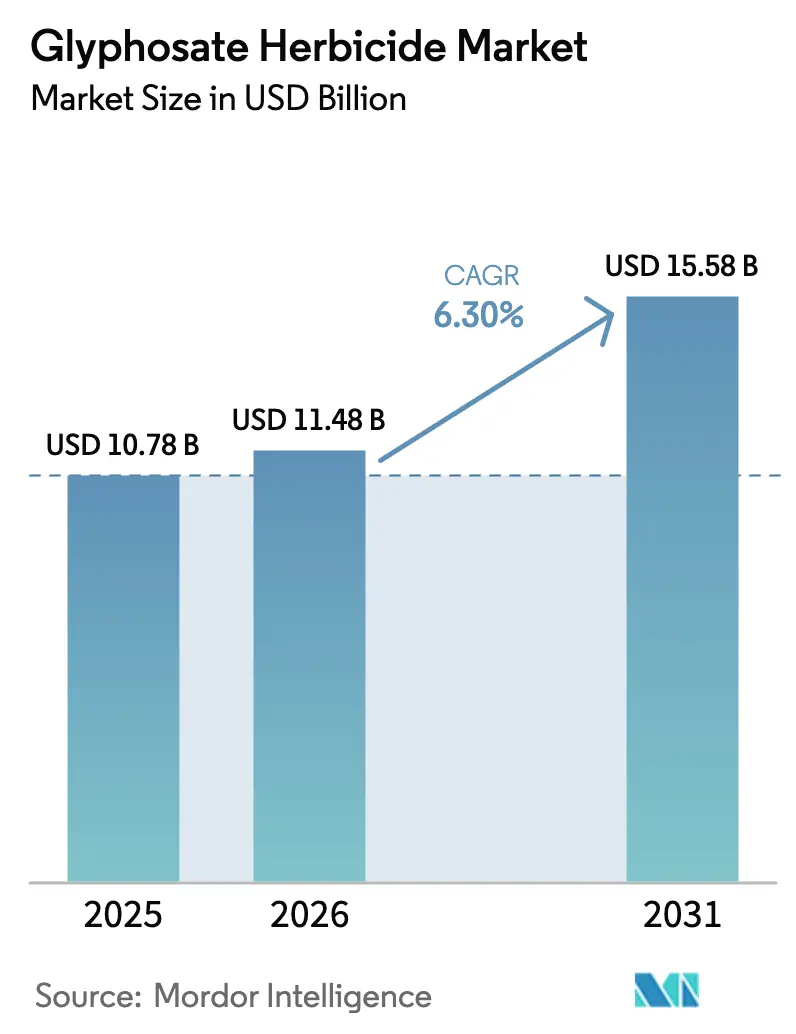

| Market Size (2026) | USD 11.48 Billion |

| Market Size (2031) | USD 15.58 Billion |

| Growth Rate (2026 - 2031) | 6.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

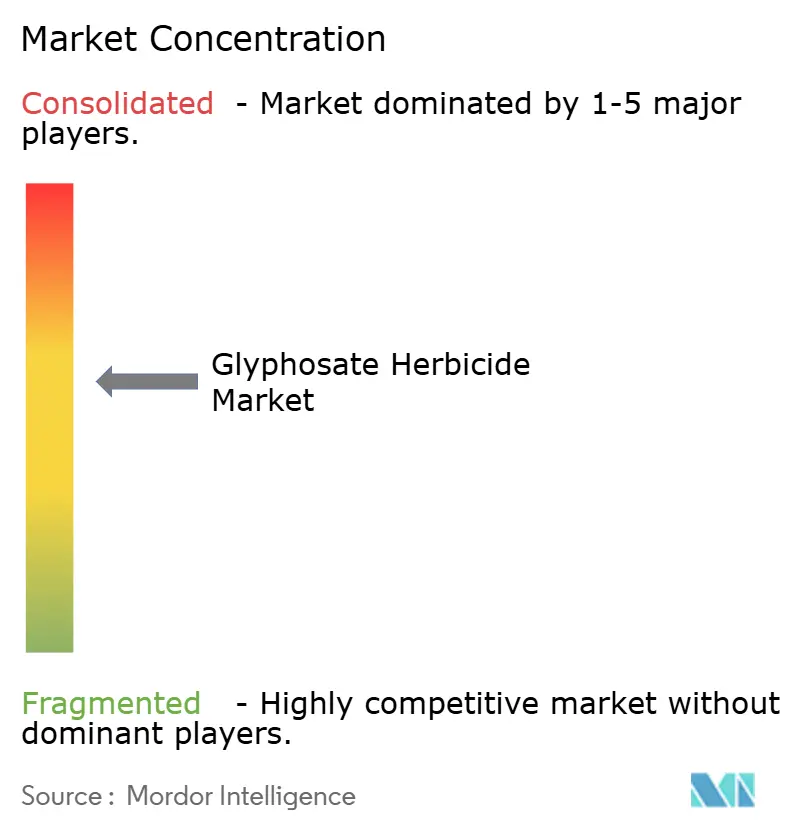

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glyphosate Herbicide Market Analysis by Mordor Intelligence

The glyphosate herbicide market size is projected to expand from USD 10.78 billion in 2025 and USD 11.48 billion in 2026 to USD 15.58 billion by 2031, registering a CAGR of 6.3% between 2026 to 2031. The outlook is underpinned by entrenched use of glyphosate-tolerant crops, capacity consolidation that steadies pricing, and gene-editing pipelines that keep the molecule relevant even as litigation and resistance pressures mount. Branded suppliers are pivoting toward over-the-top applications in the Americas, where farmers' willingness to pay a premium for consistent formulations persists. Meanwhile, stabilized technical prices offer producers margin visibility, and regenerative no-till programs supported by carbon credits reinforce baseline demand in North America and parts of Europe. In emerging regions, incremental acreage additions in Africa and the Sahel, combined with rising labor costs that favor chemical weed control, further propel market growth.

Key Report Takeaways

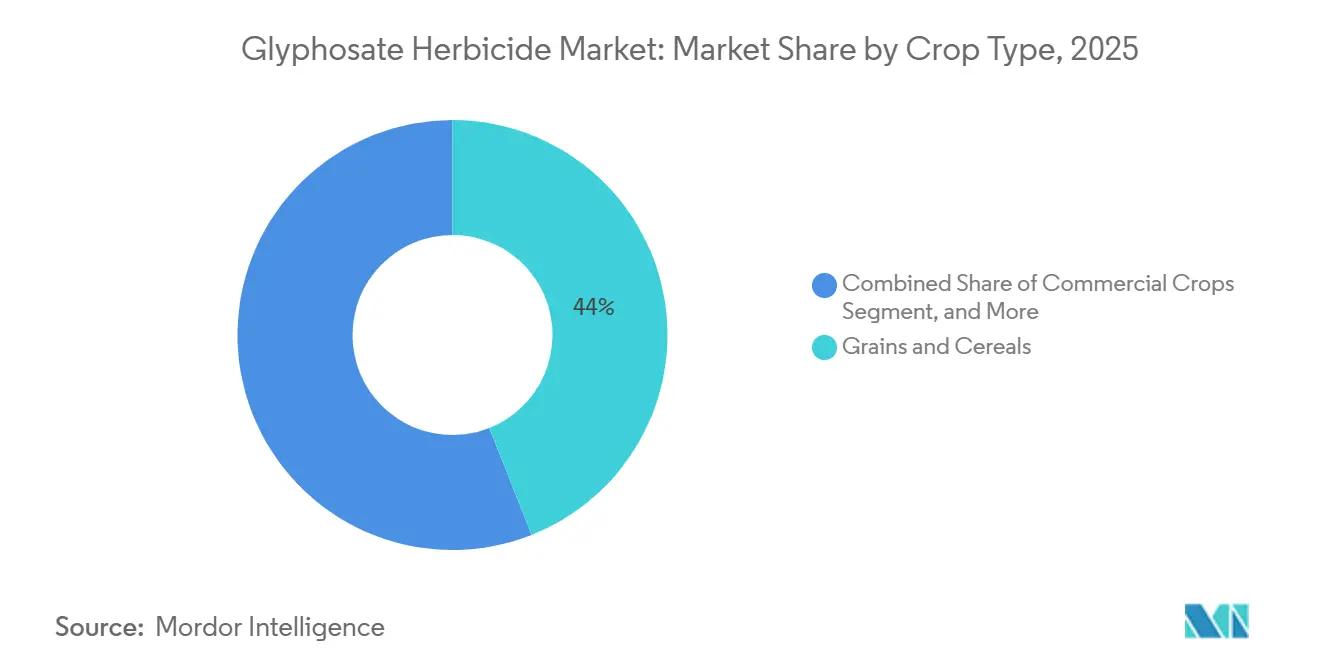

- By crop type, grains and cereals accounted for 44.0% of the glyphosate herbicide market share in 2025, while commercial crops are projected to advance at a 6.8% CAGR through 2031.

- By biotechnology adoption, genetically modified crops represented 60.0% of the glyphosate herbicide market share in 2025, and are projected to grow at a 6.5% CAGR through 2031.

- By formulation, liquid formulations commanded a 73.0% market share in 2025, and dry formulations are forecast to grow at a 7.3% CAGR through 2031.

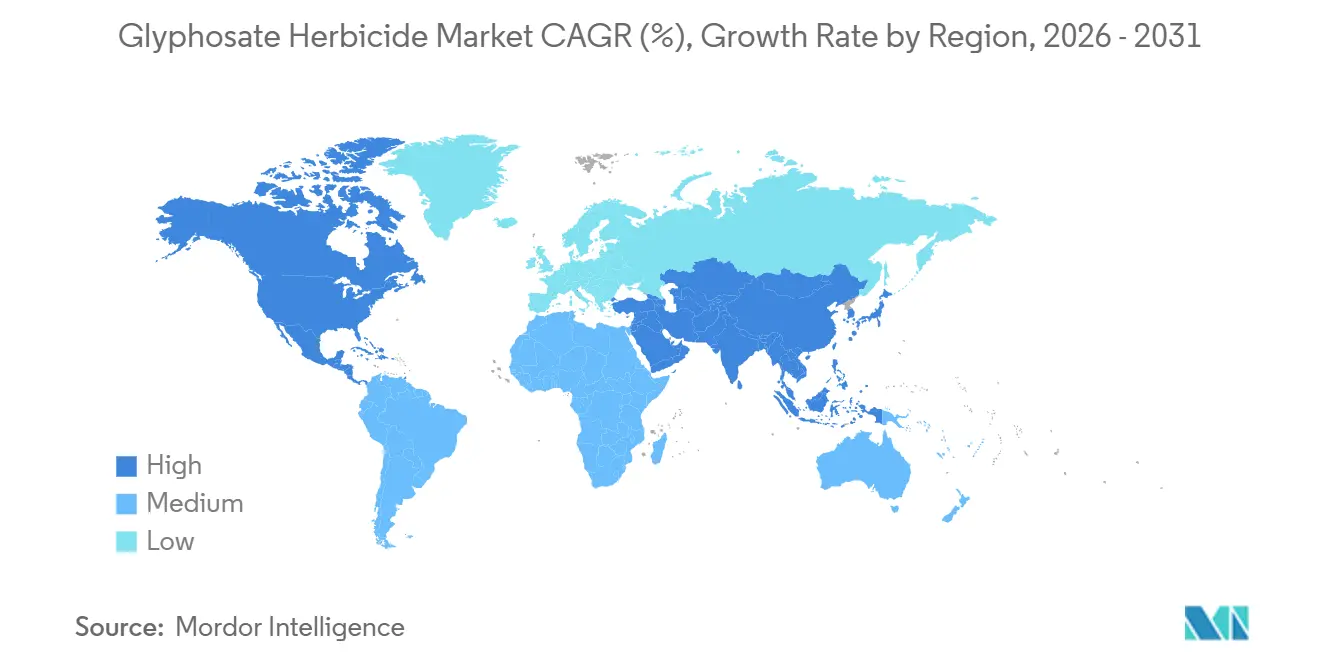

- By geography, North America held a 30% share of the glyphosate herbicide market in 2025, while Asia-Pacific is projected to deliver the fastest regional growth at a 6.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Glyphosate Herbicide Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commercialization of Genetically Modified (GM) herbicide-tolerant crops | +1.8% | North America, South America, and Asia-Pacific | Long term (≥ 4 years) |

| Rising demand for effective weed-control solutions | +1.2% | Asia-Pacific, Africa, and South America | Medium term (2-4 years) |

| Expansion of agricultural land and intensified farming | +1.0% | South America, Africa, and Asia-Pacific | Medium term (2-4 years) |

| Capacity consolidation stabilizes long-term prices | +0.9% | North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Carbon-credit backed regenerative no-till acreage | +0.7% | North America, Europe, and select South America | Long term (≥ 4 years) |

| Clustered Regularly Interspaced Short Palindromic Repeats (CRISPR)-based stacked-trait pipelines | +0.6% | North America, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Commercialization of Genetically Modified (GM) Herbicide-Tolerant Crops

The ongoing regulatory approvals and increasing adoption of genetically modified herbicide-tolerant crops by farmers are driving glyphosate demand as growers integrate into seed-and-chemistry systems. In June 2025, Argentina's Secretaría de Agricultura approved the commercial release of the stacked maize event MON-87427-7 x MON-94804-4 x MON-00603-6. This event combines reduced plant height with glyphosate tolerance, following favorable evaluations by the National Advisory Commission on Agricultural Biotechnology (CONABIA) and the National Service of Agri-Food Health and Quality (SENASA), which concluded that the stacked event poses no additional risks compared to conventional maize[1]Source: Ministerio de Economía, “Resolución 91/2025,” boletinoficial.gob.ar. As seed companies incorporate more traits into glyphosate-tolerant crops, glyphosate becomes a standard input, stabilizing demand against short-term price fluctuations and competition from alternative herbicides.

Rising Demand for Effective Weed-Control Solutions

Labor shortages and increasing wages in key agricultural regions are encouraging growers to adopt chemical weed control as a cost-effective alternative to manual or mechanical methods. This trend is particularly evident in the Asia-Pacific region, where smallholder farms face rising opportunity costs for family labor, and in Africa, where commercial agriculture is expanding faster than the availability of seasonal workers. Glyphosate's broad-spectrum efficacy and relatively low application cost per hectare make it a preferred choice for pre-plant burndown and post-emergence weed control in both genetically modified (GM) and non-genetically modified (non-GM) cropping systems. Its systemic action, which translocates to roots and rhizomes, effectively controls perennial weeds such as Cynodon dactylon and Cyperus rotundus, which are often resistant to mechanical tillage. For example, product labels in Argentina now include warnings about resistant Sorghum halepense biotypes and recommend consulting technical advisors for resistance management and combination strategies.

Expansion of Agricultural Land and Intensified Farming

The expansion of soybean and maize cultivation in South America and Africa is increasing herbicide application rates as growers shift from extensive grazing or fallow land to intensive row-crop farming. In Brazil and Argentina, the conversion of cerrado and pampas into soybean plantations has led to more frequent glyphosate applications to manage volunteer crops and invasive grasses during the establishment phase. Similarly, African countries expanding cotton and maize production in the Sahel and East Africa are adopting herbicide-based weed control to achieve export-competitive yields. This intensification of land use reduces fallow periods, limiting natural weed suppression and necessitating chemical interventions to maintain uniform crop stands. Higher yields justify the additional cost of herbicide inputs, and as farm mechanization increases, the convenience of glyphosate spraying compared to manual weeding or inter-row cultivation becomes more appealing.

Capacity Consolidation Stabilizes Long-Term Prices

Recent mergers and asset divestitures have addressed global glyphosate overcapacity, leading to improved producer margins and stabilized prices following the volatility experienced between 2020 and 2023. BASF's acquisition of Bayer's glufosinate business and certain European glyphosate-based herbicides, valued at EUR 7.6 billion (USD 9.0 billion), was part of a divestiture package required by the European Commission to preserve competition after Bayer's acquisition of Monsanto. This transaction streamlined production assets and R&D pipelines, reducing the number of independent suppliers and enabling more efficient utilization of capacity. According to Bayer's 2024 investor presentation, Chinese generic glyphosate technical prices have returned to the 15-year historical median, while prices for branded glyphosate-based herbicides have stabilized following a significant post-pandemic correction.

Restraints Impact Analysis of Glyphosate Herbicide Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory restrictions and phased bans | −1.1% | Europe, spillover to Middle East and select Asia | Medium term (2-4 years) |

| Accelerating weed resistance in major crop belts | −0.8% | North America, South America, and Asia-Pacific | Short term (≤ 2 years) |

| Litigation-driven exit risk for branded suppliers | −0.6% | North America, and Europe | Medium term (2-4 years) |

| Venture funding shift to bio-herbicide start-ups | −0.4% | North America, and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Restrictions and Phased Bans

European Union and sub-national regulatory actions are trimming long-term demand by restricting glyphosate use in public spaces, near water bodies, and in organic-certified production systems. The European Food Safety Authority conducted a comprehensive risk assessment and peer review of glyphosate in 2023, concluding that no critical areas of concern were identified, and data gaps remained[2]Source: European Food Safety Authority, “La EFSA explica la evaluación científica del glifosato,” efsa.europa.eu. Despite this scientific assessment, political pressure and precautionary-principle interpretations have led several member states to impose partial bans or require integrated pest management plans that prioritize non-chemical alternatives. These restrictions reduce the addressable market size in Europe and create regulatory uncertainty that discourages long-term investment in glyphosate production capacity. Compliance with these evolving frameworks requires manufacturers to maintain multiple product formulations and labeling variants, which increases administrative costs and complicates supply-chain logistics.

Accelerating Weed Resistance in Major Crop Belts

Resistant Amaranthus and Ryegrass species are forcing higher doses and tank-mix combinations, eroding the cost advantage that made glyphosate the default choice for weed control. Peer-reviewed research documented in Argentina identified glyphosate-resistant biotypes of Sorghum halepense in core soybean regions, with resistance mechanisms including target-site mutations in the EPSPS enzyme, gene amplification, and reduced translocation to meristematic tissues. Agronomists are responding by recommending pre-emergence residual herbicides, post-emergence tank mixes with alternative modes of action, and mechanical weed control during critical crop-establishment windows. While these integrated approaches sustain total herbicide demand, they dilute glyphosate's market share and reduce per-hectare profitability for manufacturers. The resistance dynamic also accelerates the commercial adoption of herbicide-tolerant traits for alternative chemistries, such as dicamba and 2,4-D, which directly compete with glyphosate for acreage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Glyphosate Herbicide Market Segment Analysis

By Crop Type:

Commercial Crops Outpace Staple GrainsGrains and cereals held a 44.0% glyphosate herbicide market share in 2025. This dominance is attributed to the cultivation of soybeans and maize in North and South America, where glyphosate-tolerant varieties are widely used, and pre-plant burndown applications are a common practice. Pulses and oilseeds held a notable secondary share, driven by the use of glyphosate for pre-harvest desiccation in crops such as lentils, chickpeas, and canola. This practice facilitates synchronized maturity and reduces harvest moisture content. Fruits and vegetables represent a smaller segment of the market, as many high-value crops are cultivated under organic or integrated pest management systems that limit the use of glyphosate. Some tree-fruit orchards utilize glyphosate for under-canopy weed control.

Commercial crops, including cotton, sugarcane, and plantation crops, are forecast to grow at a 6.8% CAGR through 2031. This growth is driven by the adoption of desiccation protocols that enhance fiber quality in cotton and streamline harvest scheduling in sugarcane. In Argentina, the regulatory framework supports this expansion by authorizing glyphosate-tolerant cotton varieties and enforcing residue compliance through the National Service of Agri-Food Health and Quality (SENASA), providing legal assurance for growers and exporters[3]Source: ATANOR S.C.A., “etiq Glifosato II x 20L,” atanor.com.ar . Other crops, such as pastures and forestry, along with non-agricultural applications like railway and roadside maintenance, contribute a stable but slower-growing share of the market. Infrastructure maintenance budgets and public-sector procurement cycles influence demand in these segments.

By Biotechnology Adoption:

Trait Systems Lock in DemandGenetically Modified (GM) crops accounted for 60.0% of the glyphosate herbicide market size in 2025 and are projected to grow at a 6.5% CAGR through 2031. The expansion of this segment highlights the institutional adoption of herbicide-tolerant traits in major exporting countries. Seed companies in these regions integrate glyphosate tolerance with other traits, including insect resistance, drought tolerance, and yield enhancement, creating comprehensive systems that are challenging for farmers to separate.

The segmentation of the glyphosate herbicide market reveals a strategic divide within the global seed industry. In regions where Genetically Modified (GM) crops are widely accepted, such as the Americas and parts of Asia, seed companies are focusing on next-generation trait stacks. These stacks extend glyphosate's commercial relevance by incorporating tolerance into CRISPR-edited backgrounds that provide additional agronomic benefits. Conversely, in regions where the adoption of Genetically Modified (GM) crops is restricted, such as Europe and parts of Africa, manufacturers are prioritizing improvements in glyphosate formulations and application technologies to enhance its effectiveness in conventional cropping systems.

By Formulation:

Dry Products Gain Ground in Logistics-Constrained RegionsLiquid formulations commanded 73.0% of the glyphosate herbicide market share in 2025, driven by their ease of tank-mixing, compatibility with precision-spray equipment, and established distribution infrastructure. These formulations also offer lower per-hectare application costs due to reduced labor requirements for handling and mixing compared to dry products. The choice of formulation has strategic implications for manufacturers and distributors. Liquid products necessitate investments in bulk storage tanks, filling lines, and hazardous-material transport certifications, creating entry barriers for smaller regional players. Meanwhile, the growing preference for dry formulations in emerging markets reflects a shift toward decentralized distribution, where smallholder farmers procure inputs from village-level retailers instead of manufacturers or large agri-retailers.

Dry formulations are forecast to grow at a 7.3% CAGR through 2031, driven by increasing adoption in Africa and parts of the Asia-Pacific. Distributors in these regions favor granular products due to their reduced transport weight, minimized storage requirements, and ease of handling in areas with limited cold-chain infrastructure. Additionally, dry formulations are advantageous in markets with unreliable water quality, as they can be pre-mixed with known water volumes, avoiding compatibility issues that may arise when liquid concentrates are diluted with hard or saline water. These formulations can also be packaged in smaller units and distributed through general agricultural-input retailers, reducing the capital intensity of market entry. This approach requires more extensive dealer training to ensure proper reconstitution and application.

Geography Analysis

North America Glyphosate Herbicide Market

North America’s 30% share of the glyphosate herbicide market in 2025 is driven by the widespread adoption of no-till soy and corn farming systems. Over 80% of growers in the region rely on herbicides for burndown and in-crop applications. In Canada, similar practices are observed in prairie wheat and canola farming, while Mexico's shift to mechanized maize farming is contributing to steady incremental demand. Litigation poses a significant risk to the market, as pending cases could impact domestic supply if Bayer were to exit the market. To address this, state-level liability shields, such as those enacted in Georgia, aim to ensure continued production. The United States remains the largest single-country market, supported by carbon-credit programs that incentivize no-till farming. These programs sustain pre-plant glyphosate applications, even as increasing weed resistance necessitates higher doses and tank-mix combinations.

APAC Glyphosate Herbicide Market

The Asia-Pacific region is projected to deliver the fastest regional growth, at a 6.90% CAGR, by 2031. In China, pesticide volumes have stabilized at approximately 240-250 million metric tons, with glyphosate remaining among the top 10 active ingredients. India's agrochemical value chain is expanding, with increasing volumes of generic glyphosate as farmers adopt cost-effective weed control methods. Countries such as Indonesia, Vietnam, and Thailand are increasingly adopting pre-plant burndown practices to support double cropping. In Australia, broadacre cereal farms exhibit mature but steady demand, bolstered by precision guidance systems that optimize the application of inputs. India's regulatory environment remains cautious, with periodic reviews of glyphosate registrations and state-level restrictions in areas where environmental advocacy groups have raised concerns about groundwater contamination.

South America Glyphosate Herbicide Market

South America ranks second in glyphosate consumption, largely due to Brazil's projected 322.3 million metric ton grain harvest in 2025, which drives high herbicide usage. No-till farming spans over 35 million hectares in the region, making glyphosate essential for controlling grass weeds prior to planting. In Argentina, currency challenges have heightened price sensitivity but have not reduced reliance on glyphosate. Regional technological advancements, such as Syngenta's USD 65 million facility in Paulínia, focus on developing tropical-climate formulations to maintain efficacy under high humidity, supporting long-term market growth. In Brazil's cerrado region, the conversion of pasture and savanna into soybean plantations continues to drive incremental demand for glyphosate in pre-plant burndown and post-emergence weed control. Both Brazil and Argentina face increasing weed resistance, particularly in species like Amaranthus and Sorghum halepense. This has led agronomists to advocate for integrated weed management programs that combine residual herbicides with mechanical control methods.

Competitive Landscape

The glyphosate herbicide market exhibits moderate concentration, with key players such as Bayer AG, Zhejiang Xinan Chemical Industrial Group Co., Ltd., BASF SE, Syngenta Group Co., Ltd., and UPL Limited accounting for a significant share of technical-grade production. Bayer's USD 16 billion litigation provisions have introduced considerable uncertainty regarding its market position. Any potential withdrawal by Bayer could significantly disrupt supply chains for formulators and pose challenges for downstream manufacturers.

Chinese manufacturers have undertaken coordinated facility shutdowns in response to strict environmental audits. These measures have effectively reduced market oversupply and contributed to price stability within the industry. Companies with diversified product portfolios have demonstrated greater operational flexibility. For instance, in 2025, FMC Corporation's strategic partnership with Bayer to distribute Isoflex herbicide across 30 million hectares of European Union cereal crops successfully integrated new modes of action with existing glyphosate applications.

Industry organizations, such as the Modern Ag Alliance, continue to advocate for science-based regulatory assessments to ensure the continued availability of glyphosate in agricultural markets. Additionally, digital agriculture platforms have enhanced the value proposition of glyphosate products by offering features such as comprehensive tank-mix guidance, detailed residual analysis, and advanced drift-control recommendations. These advancements have strengthened customer relationships and promoted sustainability throughout the supply chain.

Glyphosate Herbicide Industry Leaders

Bayer AG

Zhejiang Xinan Chemical Industrial Group Co., Ltd.

BASF SE

Syngenta Group Co., Ltd.

UPL Limited

- *Disclaimer: Major Players sorted in no particular order

Glyphosate Herbicide Market Companies Covered in this Report

- Bayer AG

- Zhejiang Xinan Chemical Industrial Group Co., Ltd

- BASF SE

- Syngenta Group Co., Ltd.

- UPL Limited

- Corteva, Inc.

- FMC Corporation

- Nufarm Limited

- Albaugh LLC

- Zhejiang Jiangshan Agrochemical & Chemical Co., Ltd.

- Jiangsu Yangnong Chemical Group Co., Ltd. (Sinochem Holdings Corporation Ltd.)

- ADAMA Ltd.

- Bharat Rasayan Limited

- Jiangsu Good-Harvest Weien Agrochemical Co., Ltd.

- Anhui Huaxing Chemical Industry Co., Ltd.

Recent Industry Developments in Glyphosate Herbicide Market

- May 2025: FMC and Bayer partner to commercialize Isoflex herbicide on 30 million hectares of winter cereals in the European Union. This collaboration involves FMC commercializing its own Isoflex formulations and Bayer registering and distributing mixtures, expanding access to the technology for growers facing tough weed challenges and contributing to food security.

- March 2025: Syngenta acquired Novartis's repository of natural compounds and genetic strains for agricultural use, while Novartis retained pharmaceutical rights. Syngenta also established a biologicals production facility in Orangeburg, South Carolina, to serve the Americas. The transaction highlights Syngenta's focus on biological alternatives to glyphosate.

- March 2023: Albaugh, LLC acquired Corteva Agriscience's glyphosate business. The acquisition encompasses intangible assets, including formulations, trade names, regulatory data, registrations, patents, and know-how utilized globally in Corteva's straight-goods glyphosate business.

Glyphosate Herbicide Market Report Scope and Research Methodology

Market Definition and Coverage

Mordor Intelligence defines the glyphosate herbicide market as the sale value of technical-grade and formulated glyphosate products used for crop and non-crop weed control, tracked at the point they leave manufacturers or major formulators and flow through agricultural input channels worldwide.

Scope exclusion: Products blended with other active ingredients where glyphosate is less than 50 percent of the formulation are kept out to avoid double counting.

Segments Covered in This Report

- By Crop Type

- Grains and Cereals

- Pulses and Oilseeds

- Fruits and Vegetables

- Commercial Crops

- Other Crops

- By Biotechnology Adoption

- GM Crops

- Non-GM Crops

- By Formulation

- Liquid

- Dry

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- Italy

- Spain

- United Kingdom

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor interview teams spoke with farm-input distributors, large growers, regional procurement heads, and regulatory officers across North America, Latin America, Europe, Asia-Pacific, and Africa. These dialogues verified application rates, discount structures, and impending policy shifts, filling gaps left by desk work and guiding our final assumptions.

Desk Research

Our analysts began with tier-1 public datasets such as FAOSTAT planted-area files, USDA-NASS pesticide use surveys, Eurostat COMEXT trade codes, and ISAAA biotech-acreage briefs, which anchor volume estimates across regions. We layered these with regulatory dockets from the US EPA, EFSA, and Brazil's MAPA to flag ban or usage-cap timelines, and then scanned academic journals like Weed Science for resistance-incidence trends. Company disclosures, investor decks, and press releases provided pricing guidance, which was cross-checked in D&B Hoovers and shipment traces from Volza. The sources cited above illustrate the mix; many others informed smaller clarifications.

Market-Sizing & Forecasting

A top-down model converted production, import, and export tonnage into formulated-product revenue through regional average selling prices. Supplier roll-ups and distributor channel checks provided a bottom-up sense check, and the two views were reconciled. Key variables, including GM-crop acreage, glyphosate technical price index, Chinese capacity additions, weed-resistance prevalence, and exchange-rate movements, drive the base year and enable forecasts. Multivariate regression projects demand, while scenario analysis tests regulatory or price-shock sensitivities. Where bottom-up gaps appeared (for example, minor African distributors), we applied regional ratios derived from interviews before re-testing totals.

Data Validation & Update Cycle

Outputs pass variance screens against historical price-volume elasticities, peer reviews by senior analysts, and anomaly checks versus independent indicators. The model refreshes each year, and mid-cycle updates trigger when major regulatory or supply events occur.

How Mordor Intelligence's Glyphosate Herbicide Market Size Compares to Other Published Estimates

Published estimates often diverge because firms vary in scope choices, price assumptions, and refresh timing.

Key gap drivers include whether non-crop uses are bundled, how branded mark-ups are handled, and if Chinese export volumes are fully captured. Some publishers also roll forward earlier datasets without live interviews, whereas Mordor analysts revisit acreage, price, and policy inputs every cycle.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.5 B (2025) | Mordor Intelligence | - |

| USD 8.98 B (2024) | Global Consultancy A | Omits roadside and rail-corridor applications, narrower scope |

| USD 10.92 B (2024) | Regional Consultancy B | Adds distributor mark-ups and bundled salts, inflating value |

| USD 9.51 B (2024) | Trade Journal C | Limited primary validation; projects high CAGR from unverified resistance data |

In sum, Mordor's discipline in aligning clear scope, multi-source variables, and annual interview loops delivers a balanced, transparent baseline that decision-makers can retrace and trust.

Key Questions Answered in the Report

How large is the glyphosate herbicide market in 2026?

The market generated USD 11.48 billion in 2026 and is forecast to reach USD 15.58 billion by 2031.

Which crop type generates the most demand for glyphosate products?

Grains and cereals led with a 44.0% revenue share in 2025, primarily due to the widespread adoption of glyphosate-tolerant soybeans and maize.

How are litigation risks influencing supplier strategies?

Branded manufacturers support state shield laws and may limit retail sales to manage exposure, potentially opening share for generics.

What role do carbon credits play in glyphosate demand?

No-till acreage eligible for carbon payments relies on glyphosate for weed control, reinforcing baseline use in North American and European programs.

Page last updated on: