Market Overview

| Study Period | 2019 - 2030 |

|---|---|

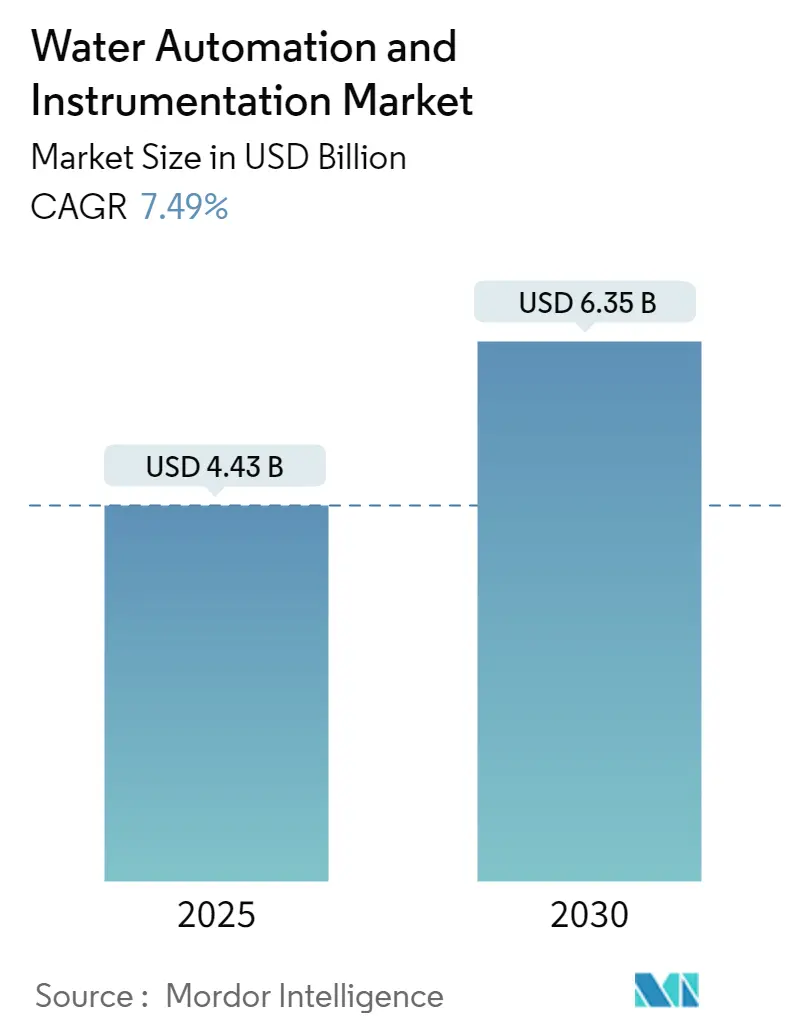

| Market Size (2025) | USD 4.43 Billion |

| Market Size (2030) | USD 6.35 Billion |

| Growth Rate (2025 - 2030) | 7.49% CAGR |

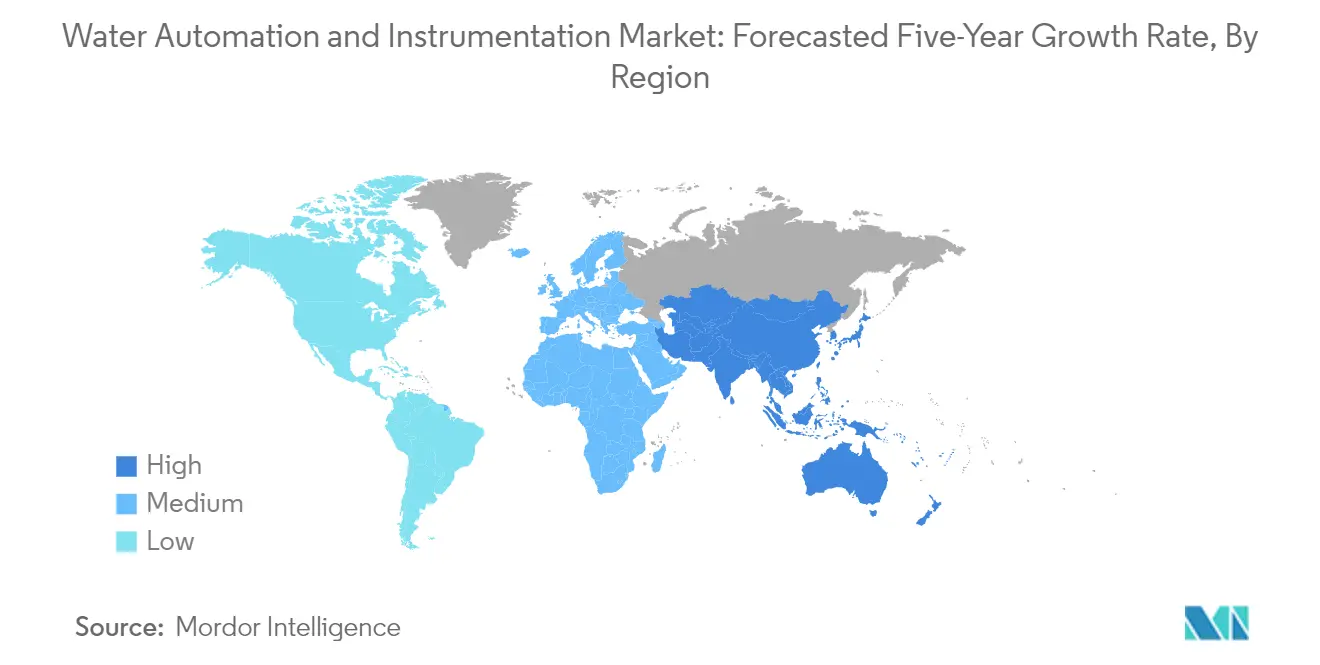

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Water Automation and Instrumentation Market Analysis by Mordor Intelligence

The Water Automation and Instrumentation Market size is estimated at USD 4.43 billion in 2025, and is expected to reach USD 6.35 billion by 2030, at a CAGR of 7.49% during the forecast period (2025-2030).

The water automation and instrumentation industry is experiencing significant transformation driven by the pressing need to address global water infrastructure challenges. According to the American Water Works Association, the repair, maintenance, and expansion of water services are projected to require approximately USD 1 trillion in investments over the next 25 years. This substantial investment requirement reflects the aging infrastructure and growing demand for modern water management system solutions. The American Society of Civil Engineers (ASCE) forecasts a 23% increase in wastewater treatment requirements by 2030, while the EPA projects necessary investments of USD 271 billion to address potential wastewater demands.

The industry is witnessing a surge in strategic partnerships and acquisitions aimed at enhancing digital capabilities and service offerings. In March 2023, SUEZ and Schneider Electric announced the creation of a joint venture focused on developing innovative digital solutions for smart water management, demonstrating the industry's shift toward integrated digital solutions. This collaboration aims to accelerate digital transformations by providing comprehensive software solutions for infrastructure planning, maintenance, and optimization. Similarly, Autodesk's acquisition of Innovyze for USD 1 billion represents a significant move toward end-to-end water instrumentation solutions and digital transformation.

Non-revenue water (NRW) remains a critical challenge facing the industry, with the World Bank estimating global costs to water utilities at approximately USD 141 billion annually. The efficiency of water management systems varies significantly across regions, with some countries like the Netherlands maintaining water losses at 4%, while others struggle with losses of up to 50% of total supplied water. This disparity has led to increased adoption of advanced water monitoring systems, particularly in regions with high water stress.

Technological innovation is reshaping the water automation landscape through the integration of smart monitoring technologies and advanced analytics. Ultrasonic technology has become the industry standard for liquid level requirements, offering enhanced performance and functionality for water and wastewater applications. The industry is witnessing the emergence of new solutions combining pressure and acoustic sensors with wireless monitoring systems, enabling predictive maintenance and real-time leak detection. These advancements are particularly crucial as tracking data and scientific understanding continue to improve, leading to optimized wastewater processing and recycling capabilities.

Global Water Automation and Instrumentation Market Trends and Insights

Government Regulation to Save Water Resources and Energy

The US Environmental Protection Agency (EPA) has implemented stringent regulations requiring municipalities to reduce pollution and the volume of stormwater runoff while preventing unlawful discharges of raw sewage that could negatively impact water quality monitoring. These regulations have become increasingly strict, with treatment plants now being limited to specific overflow allowances per year compared to previously allowing multiple overflows per month. This has driven water treatment facilities to implement comprehensive control systems with enhanced data insights and reporting capabilities to increase capacity, improve maintenance, and ensure regulatory compliance. In Europe, water management is regulated through multiple directives, including the Water Framework Directive, Urban Wastewater Treatment Directive, Groundwater Directive, and Environmental Quality Standards Directive, which collectively govern industrial wastewater generation and management practices.

The American Water Works Association projects that the repair, maintenance, and expansion of water services infrastructure will require approximately USD 1 trillion in investments over the next 25 years. Additionally, the American Society of Civil Engineers (ASCE) forecasts a 23% increase in wastewater treatment requirements by 2030, with the EPA estimating necessary investments of USD 271 billion to address potential wastewater demands. These regulatory pressures and infrastructure needs have compelled water treatment facilities to adopt automated monitoring systems that can help future-proof their operations through better data insights, remote access capabilities, and improved reporting functionalities. The regulations have also driven innovations in areas like overflows into natural water sources, requiring plants to significantly improve efficiency through remote monitoring systems and robust control system upgrades. The integration of water sensor technology is crucial in achieving these improvements.

Understand The Key Trends Shaping This Market

Download PDF

Increase in Adoption of Smart Water Technologies

The proliferation of IoT and smart cities across various regions has transformed water management capabilities through the integration of advanced instrumentation and communication solutions. According to the Global Water Intelligence study of the world's top 40 water markets, while countries like the Netherlands, Denmark, and Japan have effectively managed water losses to 4%, 6%, and 7% respectively through smart technologies, other regions like India continue to face challenges with almost 50% water loss of total supplied water. This stark contrast has driven increased adoption of automation technologies such as water SCADA systems and IoT strategies to address critical challenges around water scarcity, water quality monitoring, and consumption management through the development of smart water management networks.

The water management ecosystem has evolved to incorporate sophisticated equipment, communication infrastructure, and supporting software that enables two-way communication for gathering actionable information. Organizations like the Internet of Water have emerged to help modernize water data infrastructure by providing tools that improve the discoverability, accessibility, and usability of water data for decision-makers. The implementation of IoT-based remote monitoring offers real-time information without manual intervention through sensors, allowing not only effective monitoring and management on the ground but also enabling real-time visibility to operators. This technological transformation has delivered significant gains in operational efficiencies, cost reduction, grievance redressal, and transparency in managing natural water assets while driving improvements in delivery systems through enhanced data harnessing capabilities. The adoption of a water management system is pivotal in achieving these advancements.

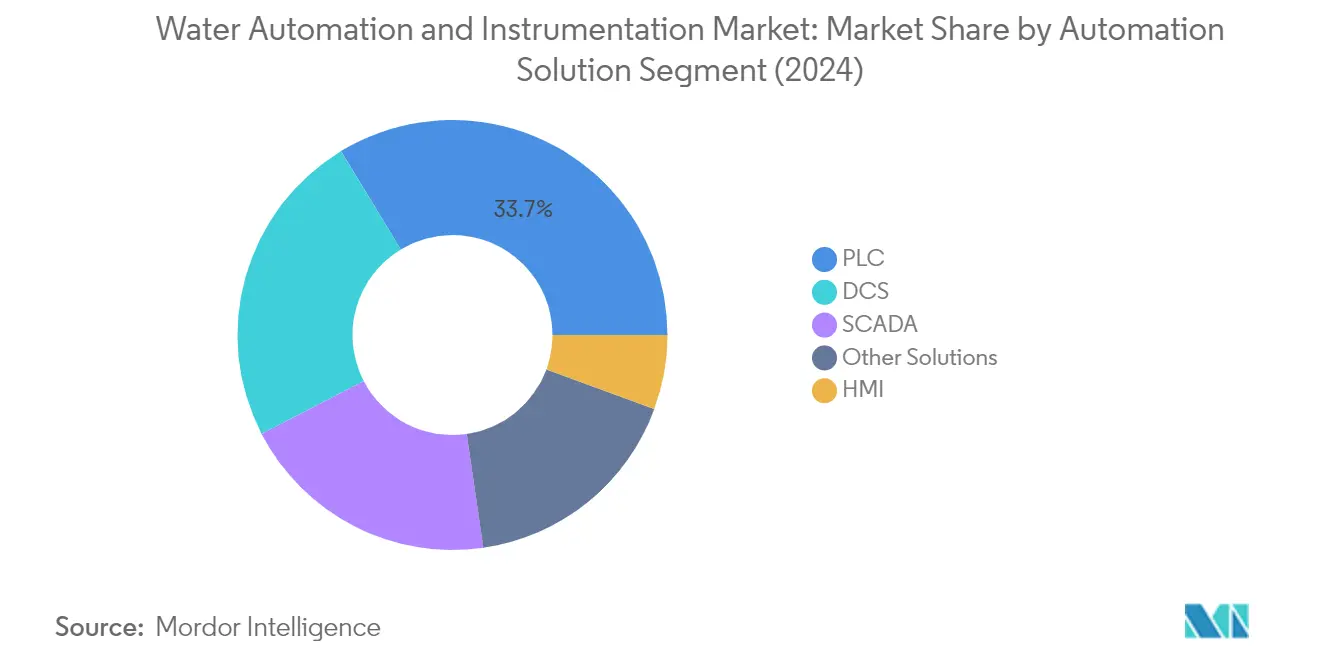

Segment Analysis: By Water Automation Solution

PLC Segment in Water Automation and Instrumentation Market

The Programmable Logic Controller (PLC) segment dominates the water automation and instrumentation market, holding approximately 30% market share in 2024. PLCs play a crucial role in simplifying water control systems by improving flexibility and reducing complexity in control operations. These microprocessor-based devices are extensively utilized to control industrial processes and machines, offering advanced functions including monitoring and communications capabilities to share data over networks. The expanding features of PLCs are increasingly being leveraged to enhance operational efficiency, allowing operators access to more comprehensive data. Their versatility enables them to handle various applications, from controlling pump station motor contactors and stirrer motors to measuring pressure transmitters in water systems. The integration capabilities of PLCs with SCADA systems further enhance their value proposition, making them an indispensable component in modern water automation infrastructure.

HMI Segment in Water Automation and Instrumentation Market

The Human Machine Interface (HMI) segment is emerging as the fastest-growing segment in the water automation and instrumentation market, projected to grow at approximately 10% CAGR from 2024 to 2029. This remarkable growth is driven by the increasing demand for intuitive user interfaces that can effectively monitor and control water treatment processes. Modern HMI solutions are incorporating advanced features such as remote monitoring capabilities, touch screen interfaces, and mobile device compatibility, making them increasingly essential for efficient plant operations. The segment's growth is further fueled by the integration of IoT capabilities, cloud connectivity, and real-time data visualization features, enabling operators to make more informed decisions and respond quickly to operational changes. The adoption of high-performance HMIs has significantly improved plant visualization capabilities, allowing operators to access comprehensive plant views with historical information and enhanced navigation menus.

Remaining Segments in Water Automation Solutions

The water automation solutions market encompasses several other significant segments including Distributed Control Systems (DCS), Supervisory Control and Data Acquisition (SCADA), and other automation solutions. DCS systems are particularly valued for their ability to control complex, large, and geographically distributed applications in industrial processes, while SCADA systems excel in providing comprehensive monitoring and control capabilities for water distribution networks. These segments collectively contribute to the market's robust ecosystem, each serving specific operational needs in water treatment and distribution processes. The other automation solutions segment includes specialized technologies such as laboratory information management systems and manufacturing execution systems, which provide additional layers of control and optimization in water treatment operations.

Segment Analysis: By Water Instrumentation Solution

Flow Sensors/Transmitters Segment in Water Automation and Instrumentation Market

The Flow Sensors/Transmitters segment continues to dominate the water automation and instrumentation market, commanding approximately 49% of the market share in 2024. This significant market position is driven by the increasing adoption of flow measurement technologies across various water treatment and distribution applications. The segment's prominence is particularly evident in wastewater monitoring and sewage management systems, where these water sensors play a crucial role in preventing blockages and build-ups. The growing demand for smart monitoring technologies and the implementation of water infrastructure projects across major economies has further strengthened this segment's market leadership. Additionally, the rising focus on reducing non-revenue water losses and improving operational efficiency in water utilities has led to increased deployment of flow measurement solutions.

Leakage Detection Systems Segment in Water Automation and Instrumentation Market

The Leakage Detection Systems segment is emerging as the fastest-growing category in the water automation and instrumentation market, projected to grow at approximately 7% CAGR during 2024-2029. This remarkable growth is primarily attributed to the increasing focus on water conservation and the rising need to minimize water losses in distribution networks. The segment's growth is further accelerated by the integration of advanced technologies such as acoustic sensors, pressure monitoring systems, and smart analytics for early leak detection. Water utilities and industrial facilities are increasingly investing in these systems to improve their infrastructure reliability and reduce operational costs. The adoption of digital technologies and IoT-enabled leak detection solutions has also contributed to the segment's rapid expansion, as organizations seek more efficient ways to monitor and maintain their water infrastructure.

Remaining Segments in Water Automation and Instrumentation Market

The water automation and instrumentation market encompasses several other crucial segments including Level Transmitters, Pressure Transmitters, Temperature Transmitters, Liquid Analyzers, and Gas Analyzers. Level Transmitters play a vital role in monitoring and controlling fluid levels in various containers and tanks, while Pressure Transmitters ensure accurate pressure measurements across water distribution networks. Temperature Transmitters provide critical temperature monitoring capabilities for water process control applications. Liquid and Gas Analyzers contribute to maintaining water quality standards and ensuring regulatory compliance. These segments collectively form an integral part of comprehensive water management solutions, each serving specific functions in water treatment, distribution, and monitoring applications.

Segment Analysis: By End-User Industry

Utilities Segment in Water Automation and Instrumentation Market

The utilities segment represents the largest share of the water automation and instrumentation market in 2024, driven by the critical role of water management in power generation and distribution facilities. Digital technologies are making utility systems more efficient, connected, intelligent, sustainable, and reliable worldwide. Water plays a vital role in utility operations, from monitoring temperature variations in steam generation to managing water scalability in pipelines and heat transmission. The implementation of advanced automation solutions like SCADA systems enables utilities to achieve real-time monitoring of their extensive water pipeline networks while optimizing energy consumption. Modern distributed control systems (DCS) in utilities now include enhanced capabilities such as asset diagnostics, performance monitoring, fleet management, and sophisticated alarm handling, allowing for online updates without shutting down plants.

Manufacturing Segment in Water Automation and Instrumentation Market

The manufacturing segment is experiencing the fastest growth rate from 2024 to 2029, propelled by increasing adoption of Industry 4.0 technologies and smart manufacturing practices. The sector's expansion is driven by the critical need for water management in production processes, where industrial water is essential for fabrication, washing, cooling, boiling, and sanitation purposes. Manufacturing facilities are increasingly implementing automated wastewater treatment systems to remain compliant with environmental regulations while reducing treatment, labor, and disposal costs. The integration of in-line water quality testing monitors, analyzers, controllers, and transmitters throughout manufacturing processes enables efficient data collection and real-time monitoring. This trend is further accelerated by the growing emphasis on sustainable manufacturing practices and the need to optimize water usage across operations.

Remaining Segments in End-User Industry

The chemical industry segment is characterized by its need for precise water management in handling harmful effluents and maintaining strict quality standards. The food and beverage sector emphasizes water automation for ensuring product quality and operational reliability, while the paper and pulp industry relies heavily on water automation for various processes requiring close monitoring of temperature and chemical content. These segments collectively drive innovation in water automation technologies, particularly in areas such as process control, quality monitoring, and compliance management. Each industry brings unique requirements and challenges that continue to shape the development of specialized automation solutions, from advanced analytical instruments to sophisticated control systems.

Water Automation and Instrumentation Market Geography Segment Analysis

Water Automation and Instrumentation Market in North America

North America represents a mature water automation and instrumentation market, driven by stringent environmental regulations and the need to upgrade aging water infrastructure. The United States and Canada are the key markets in this region, with both countries showing strong adoption of advanced water automation technologies. The region's growth is supported by increasing investments in smart water management systems and the need for efficient water resource management across industrial and municipal sectors.

Water Automation and Instrumentation Market in the United States

The United States dominates the North American water automation and instrumentation market, accounting for approximately 82% of the region's market share in 2024. The country's market is characterized by extensive water and wastewater infrastructure, with approximately 26 miles of water mains and 1.2 million miles of water supply mains for every mile of interstate highway. The growth is driven by the need to comply with EPA regulations, increasing adoption of smart water monitoring systems, and the implementation of advanced water control systems across various industries.

Water Automation and Instrumentation Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 6% during 2024-2029. The country's market is driven by its robust food and beverage processing industry, which accounts for 17% of total manufacturing sales. The increasing focus on hydropower projects, with Canada being the world's fourth-largest producer of hydroelectricity, further drives the demand for water automation solutions. The government's active investments in water and wastewater infrastructure modernization projects are creating new opportunities for market growth.

Water Automation and Instrumentation Market in Europe

Europe represents a significant market for water automation and instrumentation solutions, characterized by advanced water treatment technologies and stringent environmental regulations. The region's market is driven by countries like Germany, the United Kingdom, France, and Italy, each contributing significantly to the overall market growth. The European Union's Water Framework Directive and various water quality standards continue to shape the market landscape, promoting the adoption of sophisticated automation solutions.

Water Automation and Instrumentation Market in Germany

Germany leads the European market, commanding approximately 28% of the region's market share in 2024. The country's leadership position is attributed to its exceptional drinking water quality standards and advanced wastewater treatment infrastructure. German industries are increasingly adopting digital technologies and Industry 4.0 solutions in their water instrumentation systems, driving the demand for sophisticated automation and instrumentation solutions.

Water Automation and Instrumentation Market in France

France demonstrates the highest growth potential in the European region, with an expected growth rate of approximately 8% during 2024-2029. The country's market is driven by increasing digital transformation initiatives in water management systems and growing partnerships between technology providers and water utilities. The focus on reducing non-revenue water losses and improving operational efficiency through automation is creating significant opportunities for market expansion.

Water Automation and Instrumentation Market in Asia-Pacific

The Asia-Pacific region represents a dynamic water automation and instrumentation market, with diverse needs across developed and developing economies. Countries like China, Japan, India, and Australia are driving the market growth through various initiatives in water conservation and management. The region's rapid industrialization, urbanization, and increasing focus on water quality and conservation are creating substantial opportunities for market expansion.

Water Automation and Instrumentation Market in China

China dominates the Asia-Pacific market, driven by significant investments in water infrastructure and the implementation of advanced water management systems. The country's focus on addressing water scarcity through projects like the South-to-North Water Diversion project and the rapid expansion of wastewater treatment facilities demonstrates its commitment to water automation. The adoption of smart water technologies and the integration of IoT-based monitoring systems are further accelerating market growth.

Water Automation and Instrumentation Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, driven by increasing investments in water treatment infrastructure and the adoption of automation solutions. The country's focus on reducing water losses, improving operational efficiency, and meeting growing industrial water demands is creating significant opportunities. The implementation of advanced monitoring and control systems in water treatment plants, coupled with government initiatives for water conservation, is driving market expansion.

Water Automation and Instrumentation Market in Latin America

Latin America's water automation and instrumentation market is characterized by growing industrial applications and increasing focus on water conservation. The region's market growth is driven by the need for efficient water management solutions across various industries, particularly in manufacturing and food processing sectors. While facing challenges in infrastructure development, the region shows promising growth potential through increasing adoption of digital solutions and automation technologies. The market is seeing significant developments in countries focusing on industrial water treatment and management systems.

Water Automation and Instrumentation Market in the Middle East and Africa

The Middle East and Africa region presents unique opportunities in the water automation and instrumentation market, driven by water scarcity challenges and increasing investments in water management infrastructure. Saudi Arabia leads the regional market, while the United Arab Emirates shows the fastest growth potential. The region's focus on water conservation, desalination projects, and industrial water management is driving the adoption of advanced automation solutions. The implementation of smart water technologies and the modernization of water infrastructure continue to create new opportunities for market expansion.

Competitive Landscape

Top Companies in Water Automation and Instrumentation Market

The water automation and instrumentation market is characterized by continuous product innovation across both hardware and software solutions. Leading companies are heavily investing in developing advanced SCADA systems, distributed control systems, and smart sensors while incorporating IoT and AI capabilities into their offerings. There is a strong focus on developing integrated solutions that enable remote monitoring, predictive maintenance, and data-driven decision-making. Companies are demonstrating operational agility through rapid digitalization of their product portfolios and service delivery models. Strategic partnerships, particularly in digital transformation initiatives, have become increasingly common as companies seek to enhance their technological capabilities. Geographic expansion, especially in emerging markets across the Asia-Pacific and Middle East regions, remains a key growth strategy with companies establishing local manufacturing facilities and strengthening their distribution networks.

Market Dominated by Diversified Industrial Conglomerates

The competitive landscape is primarily dominated by large industrial conglomerates with comprehensive automation portfolios, including companies like ABB, Siemens, Schneider Electric, and Rockwell Automation. These players leverage their extensive R&D capabilities, global presence, and deep industry expertise to maintain their market positions. The market structure shows moderate consolidation, with major players controlling significant market share while numerous specialized regional players serve specific geographic markets or niche applications. The presence of both global leaders and regional specialists creates a dynamic competitive environment where companies compete on technology innovation, service quality, and local market understanding.

The market has witnessed significant merger and acquisition activity as companies seek to expand their technological capabilities and geographic reach. Major players are actively acquiring specialized technology companies to strengthen their digital offerings and enhance their smart water management solutions. Strategic partnerships between automation companies and water utility specialists have become increasingly common, enabling integrated solution offerings. Regional players are forming alliances with global leaders to enhance their market access and technological capabilities, while global players are partnering with local companies to strengthen their presence in emerging markets.

Innovation and Customer Focus Drive Success

Success in the water automation and instrumentation market increasingly depends on companies' ability to deliver comprehensive, integrated solutions that address specific industry challenges. Incumbent players are focusing on developing end-to-end solutions that combine hardware, software, and services while investing in digital capabilities to enhance their value proposition. Customer relationship management and local market presence have become crucial differentiators, with successful companies establishing strong service networks and technical support capabilities. The ability to provide customized solutions while maintaining cost competitiveness has emerged as a key success factor, particularly in price-sensitive markets.

For contenders looking to gain market share, specialization in specific applications or regional markets offers a viable entry strategy. Companies are focusing on developing innovative solutions for specific industry challenges while building strong relationships with local water utilities and industrial customers. The regulatory environment, particularly regarding water conservation and quality monitoring, continues to shape market dynamics and create opportunities for companies with compliant solutions. While the risk of substitution remains relatively low due to the specialized nature of water automation solutions, companies must continuously innovate to maintain their competitive edge and address evolving customer needs.

Water Automation and Instrumentation Industry Leaders

ABB Group

Siemens AG

Schneider Electric SE

GE Corporation

Rockwell Automation Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2021 - Schneider Electric partnered with Roca Group to accelerate decarbonization. Roca Group, a world leader in the design, production, and commercialization of products, defines a new roadmap toward decarbonization, establishing a single, global strategy across the Group.

- March 2021 - General Electric Company unveiled enhancements to its CIMPLICITY and Tracker software that provide critical decision support for operators to make them more efficient. CIMPLICITY is an ideal solution for industrial companies building remote operations centers, including power and water utilities with multiple locations. New releases deliver increased integration with Proficy Operations Hub and Proficy Historian to provide centralized web-based visualization, control, and data in context.

Global Water Automation and Instrumentation Market Report Scope

The water automation system and instrumentation is based on real-time operating systems and programming toolkit that solves the current global issues, such as potable water shortage, poor water quality, high processing monitors, energy savings, and supply costs. The study covers the dynamics of multiple water automation solutions, such as DCS, SCADA, PLC, and water instruments, such as pressure transmitters, level transmitters, and liquid and gas analyzers.

Water Automation Solution

| DCS |

| SCADA |

| PLC |

| IAM |

| HMI |

| Other Water Automation Solutions |

Water Instrumentation Solution

| Pressure Transmitter |

| Level Transmitter |

| Temperature Transmitter |

| Liquid Analyzers |

| Gas Analyzers |

| Leakage Detection Systems |

| Flow Sensors/Transmitters |

| Other Water Instrumentation Solutions |

End-user Industry

| Chemical |

| Manufacturing |

| Food and Beverages |

| Utilities |

| Paper and Pulp |

| Other End-user Industries |

Geography

| North America | United States |

| Canada | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia Pacific | Australia |

| China | |

| Japan | |

| India | |

| Rest of Asia Pacific | |

| Latin America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| Water Automation Solution | DCS | |

| SCADA | ||

| PLC | ||

| IAM | ||

| HMI | ||

| Other Water Automation Solutions | ||

| Water Instrumentation Solution | Pressure Transmitter | |

| Level Transmitter | ||

| Temperature Transmitter | ||

| Liquid Analyzers | ||

| Gas Analyzers | ||

| Leakage Detection Systems | ||

| Flow Sensors/Transmitters | ||

| Other Water Instrumentation Solutions | ||

| End-user Industry | Chemical | |

| Manufacturing | ||

| Food and Beverages | ||

| Utilities | ||

| Paper and Pulp | ||

| Other End-user Industries | ||

| Geography | North America | United States |

| Canada | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | Australia | |

| China | ||

| Japan | ||

| India | ||

| Rest of Asia Pacific | ||

| Latin America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Water Automation and Instrumentation Market?

The Water Automation and Instrumentation Market size is expected to reach USD 4.43 billion in 2025 and grow at a CAGR of 7.49% to reach USD 6.35 billion by 2030.

What is the current Water Automation and Instrumentation Market size?

In 2025, the Water Automation and Instrumentation Market size is expected to reach USD 4.43 billion.

Who are the key players in Water Automation and Instrumentation Market?

ABB Group, Siemens AG, Schneider Electric SE, GE Corporation and Rockwell Automation Inc. are the major companies operating in the Water Automation and Instrumentation Market.

Which is the fastest growing region in Water Automation and Instrumentation Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Water Automation and Instrumentation Market?

In 2025, the North America accounts for the largest market share in Water Automation and Instrumentation Market.

What years does this Water Automation and Instrumentation Market cover, and what was the market size in 2024?

In 2024, the Water Automation and Instrumentation Market size was estimated at USD 4.10 billion. The report covers the Water Automation and Instrumentation Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Water Automation and Instrumentation Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: