Veterinary Point-of-Care (POC) Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

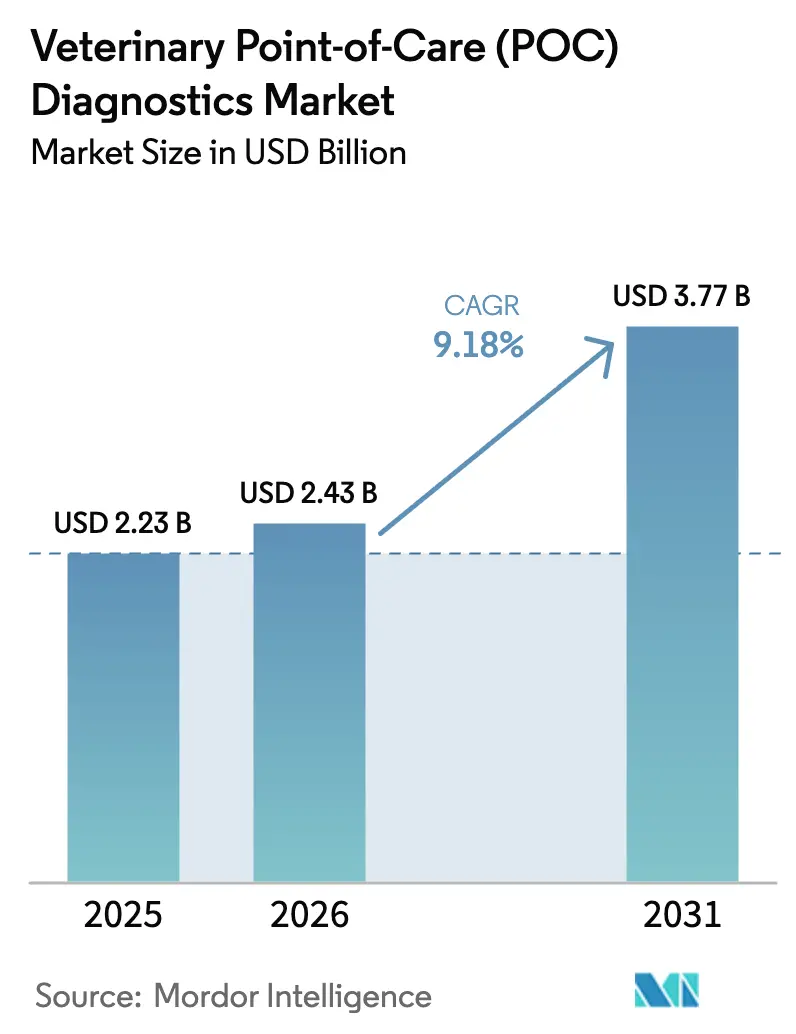

| Market Size (2026) | USD 2.43 Billion |

| Market Size (2031) | USD 3.77 Billion |

| Growth Rate (2026 - 2031) | 9.18% CAGR |

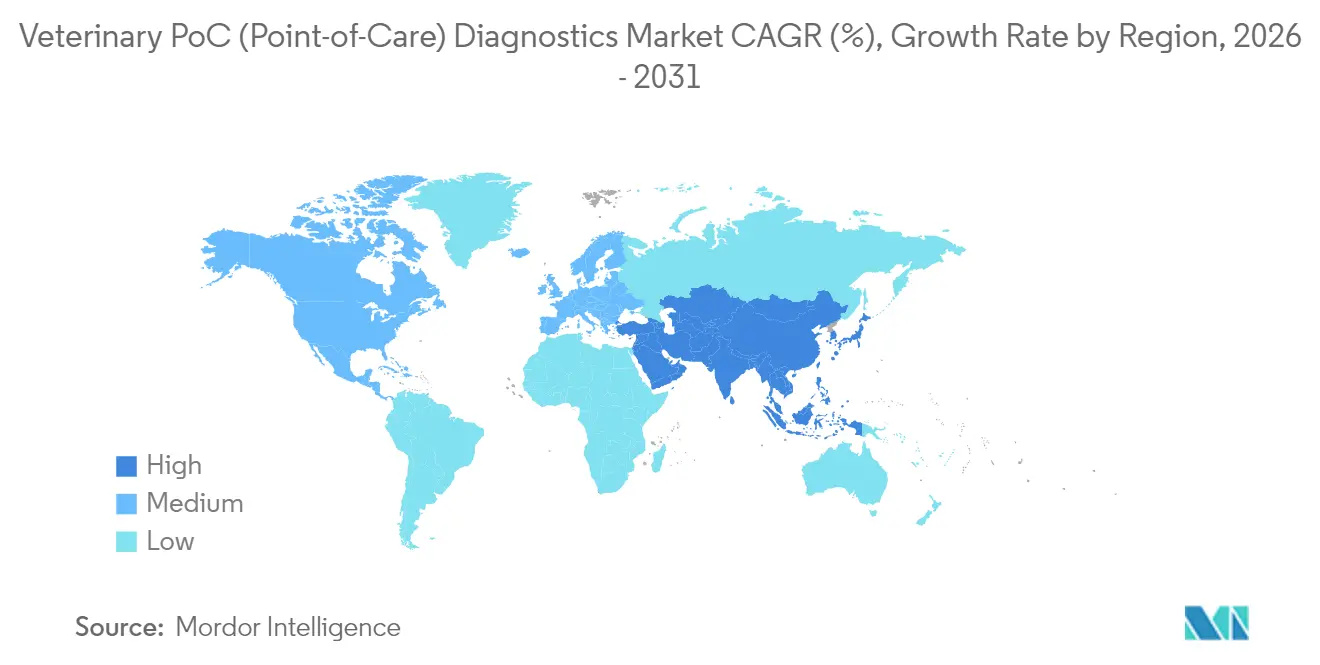

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Point-of-Care (POC) Diagnostics Market Analysis by Mordor Intelligence

The veterinary point of care diagnostics market size is expected to grow from USD 2.23 billion in 2025 to USD 2.43 billion in 2026 and is forecast to reach USD 3.77 billion by 2031 at 9.18% CAGR over 2026-2031. Strong pet humanization in mature economies, rapid livestock disease surveillance needs in developing regions, and sustained technological miniaturization are together fuelling demand for near-patient testing. Molecular platforms are advancing fastest at a 12.13% CAGR thanks to isothermal amplification and CRISPR innovations that cut turn-around times to minutes. Diagnostic instruments retain the largest revenue slice, yet single-use test kits are scaling quicker as cost-sensitive clinics seek flexible menus. Antimicrobial-stewardship regulations are accelerating adoption in food-animal practice, while AI integration into imaging and hematology workflows is reshaping practice economics.

Key Report Takeaways

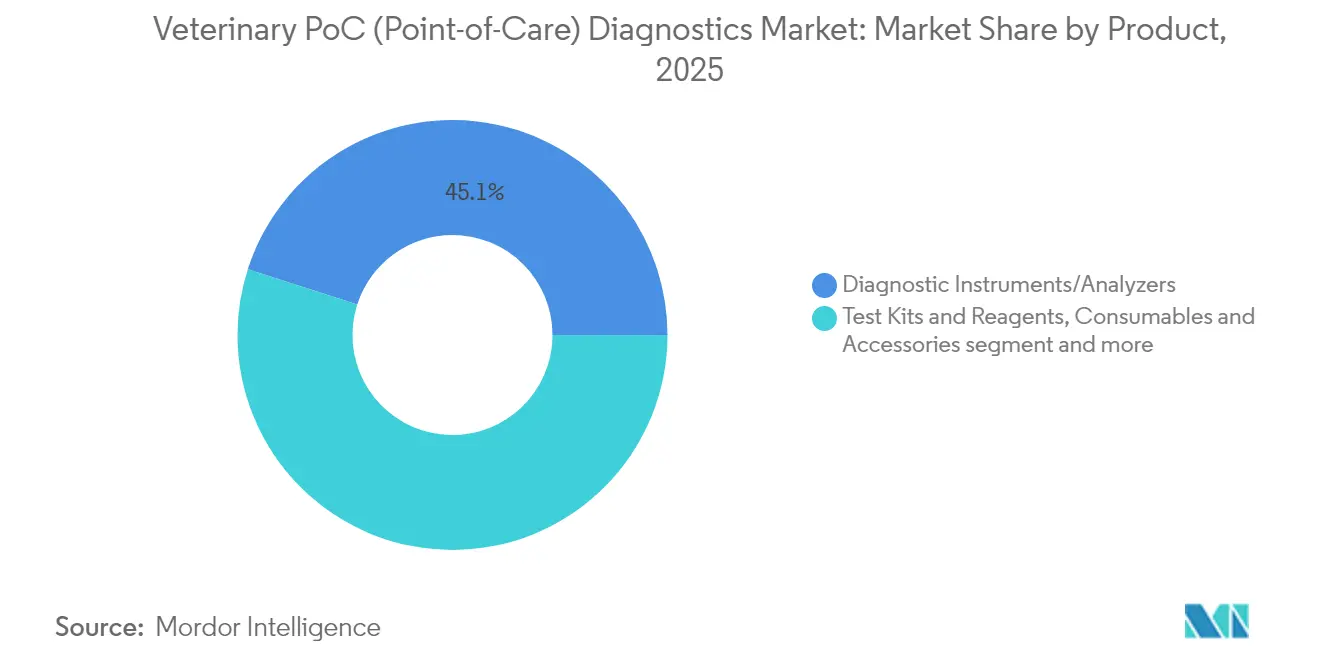

- By product, diagnostic instruments and analyzers led with 45.05% revenue share in 2025; test kits and reagents are projected to expand at a 10.12% CAGR through 2031.

- By technology, clinical chemistry commanded 33.10% of the veterinary point of care diagnostics market share in 2025; molecular diagnostics is poised for the fastest 11.64% CAGR.

- By animal type, companion animals represented 58.00% of the market in 2025, while livestock testing is forecast to grow at a 11.72% CAGR to 2031.

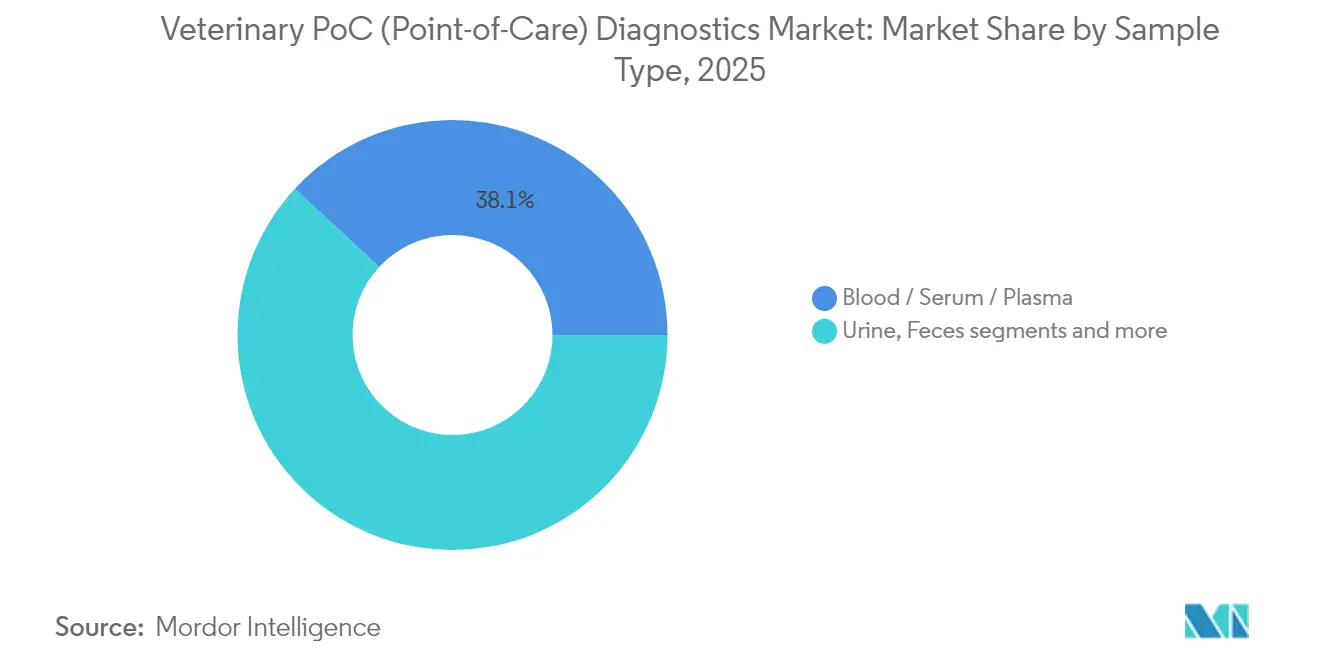

- By sample type, blood, serum, and plasma accounted for 38.10% of the market in 2025; urine testing shows the highest 11.98% CAGR potential.

- By indication, infectious diseases dominated with 46.10% share in 2025; reproductive and pregnancy management is advancing at a 12.58% CAGR.

- By end-user, veterinary clinics and hospitals controlled 64.00% of 2025 revenue; diagnostic laboratories record the fastest 10.35% CAGR outlook.

- By geography, North America held a 42.10% revenue lead in 2025; Asia-Pacific is the fastest-growing region at 10.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Point-of-Care (POC) Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Companion Animal Ownership | +2.50% | Global, with highest impact in North America and Europe | Short term (≤2 Years) |

| Rising Prevalence of Zoonotic & Transboundary Livestock Diseases | +2.10% | Global, with significant impact in Asia-Pacific and Africa | Medium term (2-5 Years) |

| Technological Miniaturization of Diagnostic Platforms | +1.80% | Global, with early adoption in North America and Europe | Medium term (2-5 Years) |

| Regulatory Push for Antimicrobial Stewardship | +2.30% | Global, with highest impact in Europe and North America | Medium term (2-5 Years) |

| Growth of Tele-Veterinary Services | +1.60% | Global, with highest adoption in North America | Long term (≥5 Years) |

| Source: Mordor Intelligence | |||

Increasing Companion Animal Ownership Driving On-site Diagnostic Demand

Sustained growth in pet adoption elevates owners’ willingness to fund sophisticated care, shifting expectations toward real-time results during appointments. US households keep 70% pet ownership, and clinics report that roughly 30% of veterinarians now deploy AI tools for imaging interpretation and record management[1]Source: American Veterinary Medical Association, “Artificial intelligence poised to transform veterinary care,” avma.org. Platforms such as Zoetis Vetscan Imagyst deliver cytology, fecal, and blood smear results in under 10 minutes, shrinking revisit rates and boosting case throughput. Clinics leveraging same-visit answers capture higher compliance on follow-up therapies and wellness panels, reinforcing revenue per patient metrics. The trend also fuels upsell opportunities for preventive screens that were once feasible only at reference labs.

Rising Prevalence of Zoonotic & Transboundary Livestock Diseases Prompting Rapid Field Testing Adoption

African swine fever flare-ups, avian influenza incursions, and brucellosis outbreaks are pushing producers to invest in portable diagnostics that confirm infection status on-farm. The US FDA’s 2024 policy that re-classified laboratory-developed tests as devices tightens validation standards and propels firms to innovate compliant, ruggedized kits for barns and trucks. CRISPR-Cascade assays under development at University of California detect bloodstream pathogens in minutes without thermal cyclers, emphasising sensitivity useful for herd surveillance. Speedy confirmation shortens quarantine windows, cuts unintended culling, and safeguards export accreditation, creating a business case for higher-priced molecular cartridges in food-animal settings

Technological Miniaturization of Immunoassay & Molecular Platforms Enabling Portable Vet Devices

Shrinking biosensors and microfluidic cartridges let practices host lab-grade analytics within benchtop footprints. Zoetis Vetscan OptiCell exemplifies this shift, offering automated complete blood counts in a handheld device that processes 50 µL of whole blood and returns results in 4 minutes. bioMérieux’s SpinChip acquisition adds a 10-minute cardiac marker readout from unprocessed blood, foreshadowing multi-analyte panels in a credit-card-sized disc. Lower reagent volumes reduce per-test cost, while sealed cartridges curb biohazard risks and maintenance downtime. Clinics in urban settings adopt such platforms first, but falling hardware prices are widening access in mixed-practice and mobile clinics.

Regulatory Push for Antimicrobial Stewardship Requiring Immediate Diagnostics in Food-Producing Animals

Governments are tightening prescription rules to curb resistance, making culture-guided therapy a prerequisite for high-priority antibiotics. A survey of US vet clinics found antibiotics written in 29.2% of consultations, yet only 17.5% of critical prescriptions had associated culture and susceptibility tests. Real-time POC tests enable evidence-based choices before animals leave the chute, limiting empirical treatments. Europe’s stringent stewardship guidelines have spurred sales of rapid mastitis and respiratory pathogen panels, and US feedlot practitioners have begun adopting 30-minute PCR kits during processing days. Manufacturers responding with bundled stewardship software create audit trails that satisfy both regulators and producers.

Restraints Impact Analysis*

| Restarint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Per-Test Costs | -1.90% | Global, with highest impact in developing regions | Short term (≤2 Years) |

| Limited Reimbursement Frameworks | -1.50% | Global, with varying impact based on insurance penetration | Medium term (2-5 Years) |

| Stringent Regulatory Approval Processes | -1.35% | North America, Europe, Asia-Pacific | Medium term (2-5 Years) |

| Source: Mordor Intelligence | |||

High Capital & Per-Test Costs of Advanced POC Analyzers Limiting Uptake in Price-Sensitive Regions

Multimodal analyzers routinely list between USD 10,000 and USD 40,000, and cartridges can exceed USD 25 apiece, straining cash-flow for small rural clinics. Consumable spending escalates with quality-control materials and calibration tapes, and service contracts add 8-10% of unit price per year. IDEXX’s USD 15 canine lymphoma panel demonstrates the demand for lower-priced molecular tests. Leasing programs and reagent-rent models are gaining traction, yet barriers persist where average ticket size of companion-animal visits is below USD 100. In livestock sectors, capital budgeting competes with husbandry investments, delaying analyzer acquisition despite documented ROI on reduced antimicrobial costs.

Limited Reimbursement Frameworks for In-Clinic Veterinary Diagnostics Curbing Volume Growth

Pet insurance penetration remains under 4% of pets globally, and policies often cap diagnostic reimbursements. Owners faced with full out-of-pocket fees sometimes defer culture tests, as evidenced by the low 17.5% test pairing with key antibiotic prescriptions in US practices. Absence of structured reimbursement also disincentivises routine wellness panels in emerging markets. While corporatised hospital chains negotiate wellness-plan bundles, independent clinics encounter margin pressure that tempers analyzer utilisation rates. Broader insurance adoption and inclusion of diagnostics as standard benefits would unlock deferred demand and lift test frequency per patient visit

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Analyzers Dominate While Test Kits Gather Pace

Veterinary point of care diagnostics market size for diagnostic instruments and analyzers reached USD 1.01 billion in 2025 and maintained a 45.05% slice of global revenue. These platforms deliver comprehensive chemistry, hematology, and immunoassay panels from minimal volumes, aligning with workflow efficiency goals. Modular systems such as VETSCAN VS2 can process 12 panels in 12 minutes, freeing technicians for patient care duties. Premium analyzers incorporate AI algorithms that flag spurious results and suggest confirmatory tests, enhancing clinical confidence.

Test kits and reagents, valued at USD 0.74 billion in 2025, are slated for a 10.12% CAGR through 2031, the fastest among product lines. Cartridge-based formats require no external calibration and suit mixed-practice vans or dairy parlors. IDEXX Cancer Dx underscores how single-disease panels priced at USD 15 unlock new screening programs that boost early detection rates. Consumables and accessories, though a smaller revenue pool, provide annuity-style income that smooths vendor cash flow and supports service bundling strategies.

By Technology: Clinical Chemistry Leads, Molecular Diagnostics Accelerates

Clinical chemistry produced USD 0.74 billion revenue and 33.10% of the veterinary point of care diagnostics market in 2025, rooted in its ability to profile organ function across species. Portable photometric and electrochemical sensors now deliver aspartate aminotransferase or bile acid panels from 50 µL samples, expanding feasibility in exotics practice. Integration of automated quality-control cycles maintains accuracy comparable with reference labs, reassuring clinicians when making anesthetic decisions.

Molecular diagnostics tracking the highest 11.64% CAGR to 2031. Isothermal amplification kits bypass thermal cyclers, compressing workflow into battery-powered handhelds. CRISPR-Cascade prototypes clock attomolar sensitivity, revealing co-infections invisible to lateral-flow devices. Immunodiagnostics continues evolving with multiplexed fluorescence assays that identify endocrine markers, while hematology advances through optical-flow cytometers that grade reticulocytes and platelets simultaneously

By Animal Type: Companion Animals Command Spending, Livestock Gains Momentum

Companion animals generated USD 1.29 billion in sales and a 58.00% share of the veterinary point-of-care diagnostics market in 2025 as owners prioritize longevity and quality of life. Canine wellness plans bundle biannual complete blood counts and SDMA assessments, driving repeat test volume. Feline practitioners leverage AI-enhanced fecal imaging to detect rare cestodes without specialist referral, improving client satisfaction during single-visit outcomes.

Dairy herds adopt milk-based pregnancy tests that offer same-day breeding decisions and reduce open-day losses. Feedlot managers implement respiratory PCR panels at induction to segment metaphylaxis programs, trimming drug spend while protecting gain-per-day metrics. Government subsidies linked to export accreditation further incentivise herd-level surveillance, bolstering demand amid biosecurity threats.

By Sample Type: Blood Maintains Primacy, Urine Testing Surges

Blood, serum, and plasma remain the gold standard, accounting for USD 0.85 billion and 38.10% of 2025 revenue. Capillary sampling advances cut required volume from 100 µL to 30 µL, improving compliance in toy breeds. Cartridge chemistry eliminates cold-chain reagent storage, streamlining mobile practice vehicle inventories. Yet blood handling still needs deproteinisation and centrifugation steps that add workflow complexity.

Urine testing, currently a USD 0.34 billion line, is scaling at a 11.98% CAGR. The Vetscan Imagyst AI urine sediment module offers automated cast and crystal categorisation within 120 seconds. Non-invasive collection appeals to feline owners who resist venipuncture, and early chronic kidney disease detection supports preventive nutrition sales. Fecal, milk, and saliva assays diversify sampling strategies, with saliva cortisol panels gaining traction for stress and welfare audits on equine rehabilitation farms.

By Indication: Infectious Diseases Top, Reproductive Management Rises Fast

Infectious disease panels produced USD 1.03 billion revenue and 46.10% share in 2025, reflecting persistent biosecurity threats. The FDA’s device re-classification compels manufacturers toward robust validation pathways, favouring established players able to finance multi-species trials. Multiplex PCR suites detect parvovirus, distemper, and adenovirus concurrently, cutting isolation room backlog in shelters.

Reproductive and pregnancy management, worth USD 0.24 billion, is forecast for a 12.58% CAGR. Timely confirmation of conception in beef cattle averts feed waste, with economic losses from infertility ranging between USD 2,800 and USD 13,200 per 100 cows. Portable ultrasound heads paired with AI fetal staging algorithms refine calving forecasts. Companion animal clinics are piloting luteinising hormone bedside tests to optimise breeding timing, opening new service revenues.

By End-User: Clinics & Hospitals Dominate, Labs Capture High-Complexity Growth

Veterinary clinics and hospitals accounted for USD 1.43 billion and 64.00% of 2025 sales, relying on in-house labs to expedite case resolution. Corporate groups such as VetPartners plan to invest heavily in POC hematology and microbiology suites after acquisition by EQT, signalling scalability of analyser fleets across 267 hospitals. AI triage dashboards help front-desk teams slot urgent cases based on real-time lactate or cTnI results, improving workflow.

IDEXX operates more than 90 labs worldwide and posted 6.56% year-on-year revenue growth by cross-selling POC devices with mail-in specialty tests. Home-care markets remain nascent but show promise for glucose and ketone strip outsourcing to pet owners managing chronic conditions under tele-supervision.

Geography Analysis

North America generated USD 0.94 billion and 42.10% of 2025 global revenue, benefitting from high pet insurance uptake and mature distributor networks. Early adopters of AI imaging drive incremental spend per visit, and stewardship policies spur adoption in cattle and swine sectors. The veterinary point of care diagnostics market size for North America is expected to climb at 8.25% CAGR to 2031 as clinics refresh ageing benchtops with cartridge-powered units.

Stringent antimicrobial oversight mandates diagnostic confirmation before prescribing Category B antibiotics, driving lab scanner placements in mixed-practice settings. Low-to-moderate resistance levels in canine and feline urinary pathogens (1–20%) demonstrate the positive feedback loop between testing and stewardship. EU sustainability programs that tie subsidy payments to health monitoring bolster demand in sheep and goat production systems.

Asia-Pacific exhibits the fastest 10.92% CAGR through 2031. Rapid urbanisation increases disposable income available for pet healthcare, while governments prioritise traceability in pork and poultry exports. Local biotech clusters in South Korea and Singapore are licensing mRNA and gene-editor platforms first applied to human vaccines for animal diagnostic reagents, accelerating technology diffusion. Regional service providers bundle telehealth with home sample pickup to overcome clinic scarcity in secondary cities, widening addressable reach.

Competitive Landscape

The market shows moderate concentration with the top five players controlling half of the market revenue. IDEXX leads and routinely outperforms sector growth by leveraging a closed-loop ecosystem of analyzers, reference labs, and cloud practice management. Zoetis follows closely, differentiating through embedded AI that augments its consumable cartridge pull-through. Heska integrates companion-animal diagnostics with its Antech lab network to capture multi-channel synergies.

Strategic acquisitions are proliferating. Mars’s July 2024 purchase of Cerba Vet and ANTAGENE expands proprietary genomic capabilities and deepens European reach. bioMérieux’s January 2025 acquisition of SpinChip Diagnostics injects ultra-rapid cardiac panels into its portfolio, enabling cross-selling to companion cardiology specialists[2]Source: bioMérieux, “bioMérieux acquires SpinChip Diagnostics,” biomerieux.com . Zoetis is doubling down on AI, announcing the launch of AI Masses for lymph-node cytology that integrates into existing Imagyst scanners in 2025.

Price competition is tempered by switching costs embedded in analyser-consumable ecosystems, while innovation races centre on assay breadth and cloud-based decision support. Regional players compete on affordability, especially in Asia, but often partner with multinationals for reagent supply. Regulatory tightening on LDTs is likely to favour companies with robust quality-system infrastructure, reinforcing incumbent advantage.

Veterinary Point-of-Care (POC) Diagnostics Industry Leaders

IDEXX

Zoetis

Virbac

Thermo Fisher Scientific Inc.

Antech Diagnostics, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: IDEXX launched IDEXX Cancer Dx, a USD 15 canine lymphoma panel delivering results in 2–3 days.

- January 2025: Zoetis unveiled AI Masses for rapid lesion screening, slated for Q2 2025 rollout on Vetscan Imagyst.

Global Veterinary Point-of-Care (POC) Diagnostics Market Report Scope

As per the scope of the report, Veterinary PoC (Point-of-Care) is diagnostic testing of animals in which the testing is done near the place of treatment, such as a hospital, clinic, etc. The result of the PoC test may change the treatment and care regime of a diseased animal. The Veterinary PoC (Point-of-Care) Diagnostics Market is segmented by Product Type (Consumables, Reagents & Kits, and Analyzing Instruments & Devices), By Animal Type (Companion Animals (Dogs, Cats, Horses, and Others), and by Livestock Animals (Cattle, Swine, Poultry, and Others)), By Sample Type (Blood/Plasma/Serum, Urine, Fecal, and Others), By Test Type (Molecular Diagnostics, Immunodiagnostics, Hematology, Urinalysis, Clinical Biochemistry, and Other Technologies), By End User (Veterinary Hospitals & Clinics, and Home Care Settings), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Diagnostic Instruments/Analyzers |

| Test Kits & Reagents |

| Consumables & Accessories |

| Immunodiagnostics |

| Molecular Diagnostics (PCR, Isothermal) |

| Hematology |

| Clinical Chemistry |

| Urinalysis |

| Microbiological Culture & Parasitology (Rapid) |

| Others |

| Companion Animals | Dogs |

| Cats | |

| Equine | |

| Others | |

| Livestock | Cattle |

| Swine | |

| Poultry | |

| Small Ruminants | |

| Others |

| Blood / Serum / Plasma |

| Urine |

| Feces |

| Milk |

| Saliva |

| Others |

| Infectious Diseases |

| Metabolic & Endocrine Disorders |

| Reproductive & Pregnancy Management |

| Gastrointestinal & Hepatic Conditions |

| Cardio-Respiratory Disorders |

| Renal & Urinary Disorders |

| Others |

| Veterinary Clinics & Hospitals |

| Diagnostic Laboratories |

| Home care settings |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Diagnostic Instruments/Analyzers | |

| Test Kits & Reagents | ||

| Consumables & Accessories | ||

| By Technology | Immunodiagnostics | |

| Molecular Diagnostics (PCR, Isothermal) | ||

| Hematology | ||

| Clinical Chemistry | ||

| Urinalysis | ||

| Microbiological Culture & Parasitology (Rapid) | ||

| Others | ||

| By Animal Type | Companion Animals | Dogs |

| Cats | ||

| Equine | ||

| Others | ||

| Livestock | Cattle | |

| Swine | ||

| Poultry | ||

| Small Ruminants | ||

| Others | ||

| By Sample Type | Blood / Serum / Plasma | |

| Urine | ||

| Feces | ||

| Milk | ||

| Saliva | ||

| Others | ||

| By Indication | Infectious Diseases | |

| Metabolic & Endocrine Disorders | ||

| Reproductive & Pregnancy Management | ||

| Gastrointestinal & Hepatic Conditions | ||

| Cardio-Respiratory Disorders | ||

| Renal & Urinary Disorders | ||

| Others | ||

| By End-User | Veterinary Clinics & Hospitals | |

| Diagnostic Laboratories | ||

| Home care settings | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the veterinary point of care diagnostics market?

The market is valued at USD 2.43 billion in 2026 and is projected to reach USD 3.77 billion by 2031.

Which technology segment is growing fastest in this market?

Molecular diagnostics is expanding at a 11.64% CAGR, outpacing all other technology segments due to rapid, high-sensitivity pathogen detection.

Why is Asia-Pacific considered the fastest-growing region?

Rising pet ownership, expanding veterinary infrastructure, and government focus on livestock disease surveillance support an 10.92% CAGR outlook for the region.

How are antimicrobial-stewardship rules influencing equipment adoption?

Stricter regulations require diagnostic confirmation before prescribing critical antibiotics, pushing clinics and farms to install rapid point-of-care analyzers.

Page last updated on: