Size and Share of Chemical Industry Valves Market

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.4 Billion |

| Market Size (2031) | USD 18.87 Billion |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

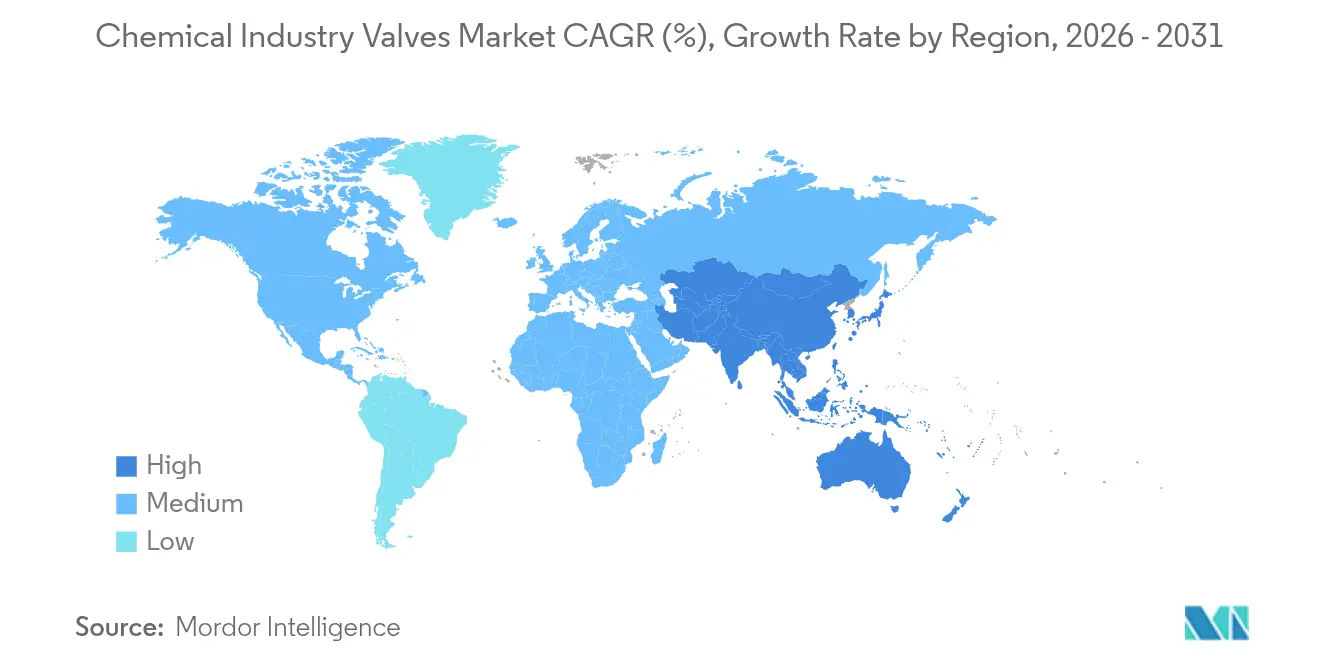

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

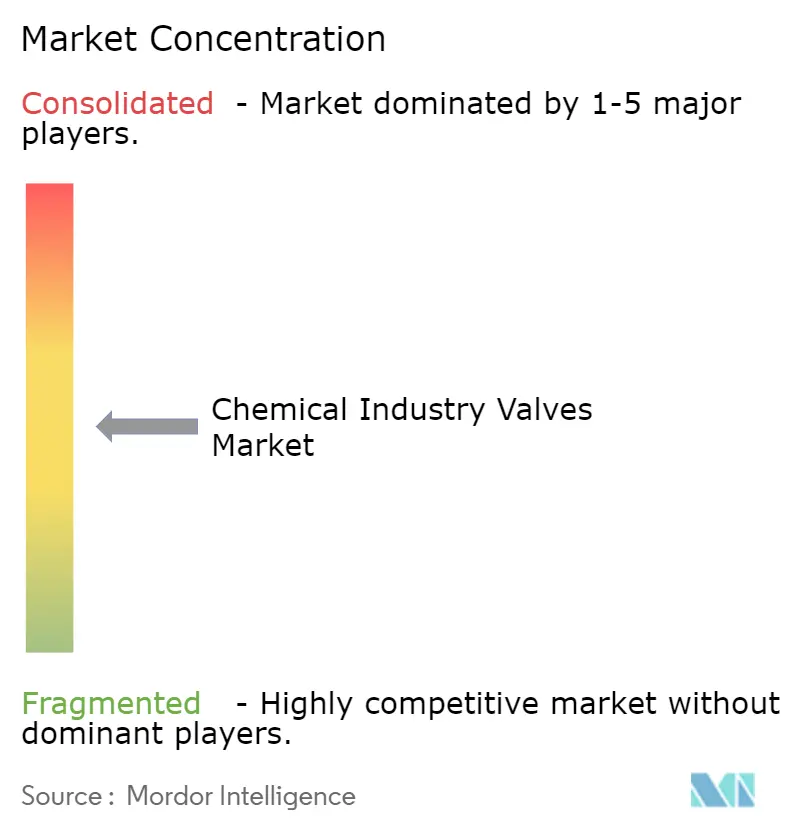

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Chemical Industry Valves Market by Mordor Intelligence

The chemical industry valves market size is expected to grow from USD 14.79 billion in 2025 to USD 15.4 billion in 2026 and is forecast to reach USD 18.87 billion by 2031 at 4.15% CAGR over 2026-2031. Robust capital expenditure on specialty-chemical capacity in Asia-Pacific, accelerating digitization of plant assets, and stricter fugitive-emission standards collectively underpin the expansion path. Suppliers that couple broad valve portfolios with smart IoT-enabled diagnostics are securing long-term frame agreements as producers pursue predictive maintenance strategies. Meanwhile, hydrogen-ready specifications and exotic-alloy demand are reshaping product mixes, even as raw-material price swings and cybersecurity costs temper near-term adoption of fully connected valve architectures.

Key Report Takeaways

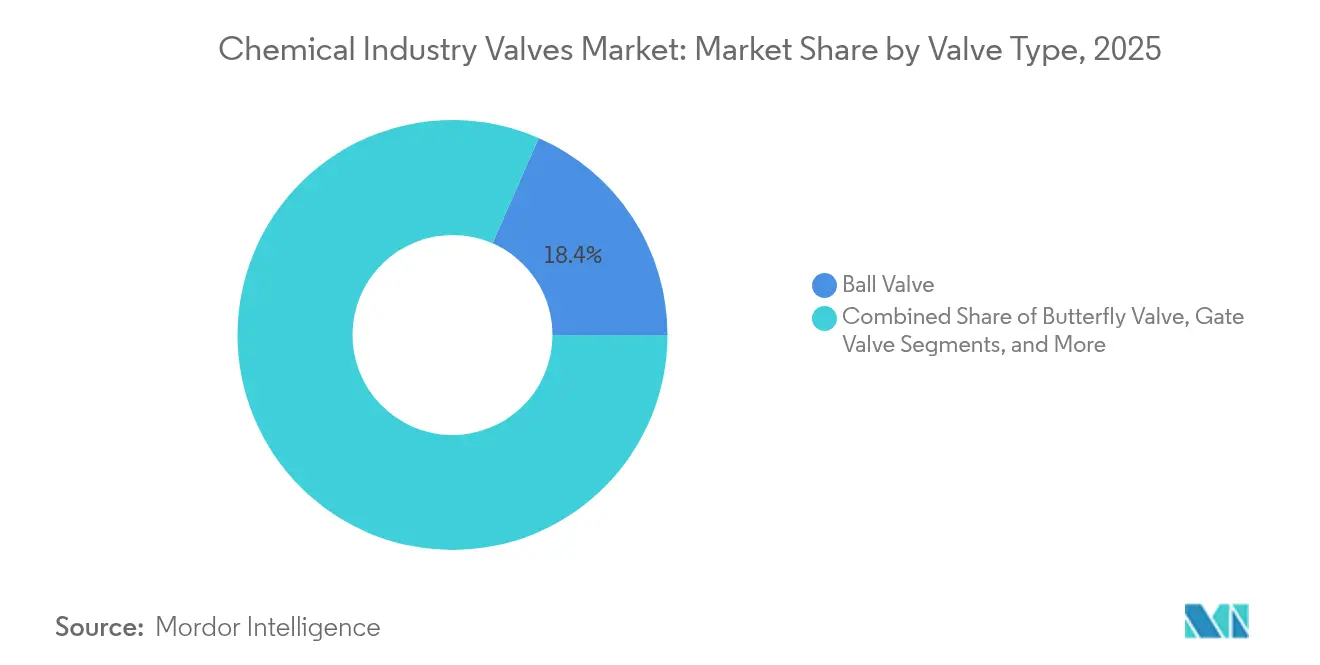

- By valve type, ball valves commanded 18.44% of chemical industry valves market share in 2025, whereas vacuum valves are set to deliver the fastest 4.92% CAGR through 2031, buoyed by semiconductor and pharmaceutical uses.

- By material, stainless steel captured 41.29% share in 2025 in chemical industry valves market, yet exotic alloys led by titanium and Hastelloy are expanding at a 5.58% CAGR as green-hydrogen projects require superior corrosion resistance.

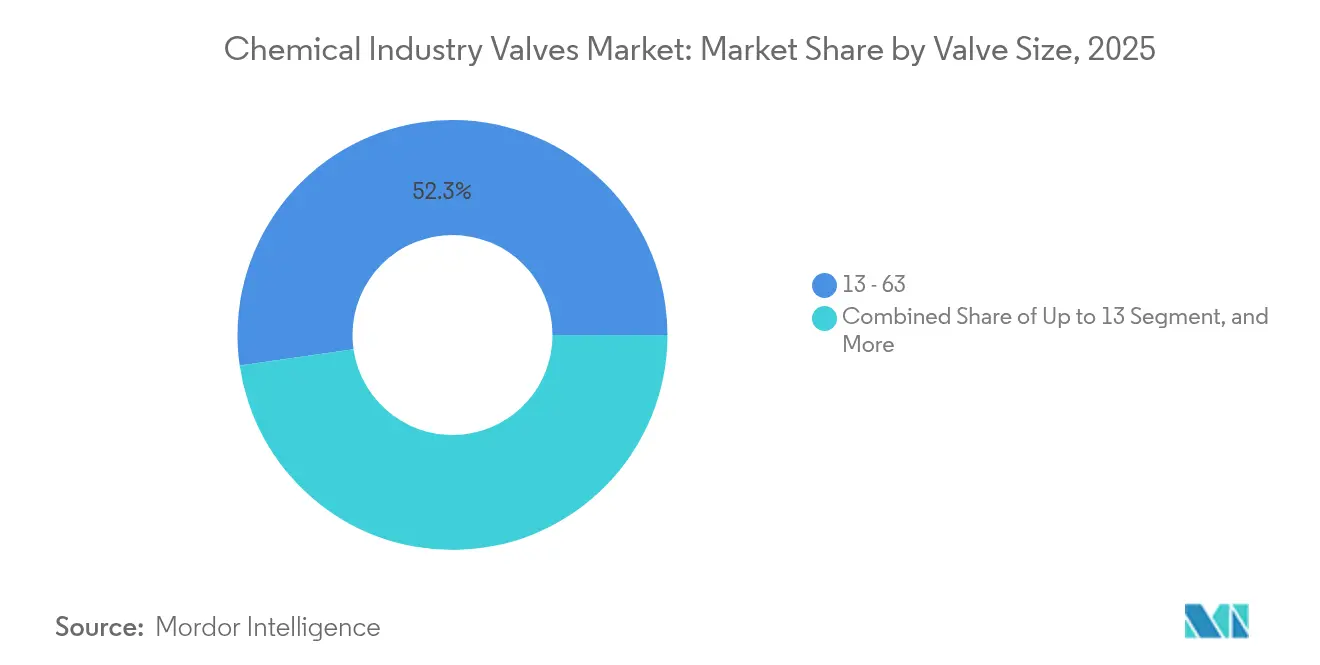

- By valve size, vid-range 1-6 inch products accounted for 52.27% of the chemical industry valves market size in 2025, but above-50 inch valves will post the strongest 5.79% CAGR on the back of mega-petrochemical plant builds.

- By actuation technology, pneumatic actuation held 59.19% share in 2025 in chemical industry valves market, while smart IoT-enabled systems are projected to grow 6.12% annually as operators link assets to plant-wide analytics platforms.

- By geography, Asia-Pacific generated 38.75% of 2025 revenue and is anticipated to compound at 5.35% through 2031 in chemical industry valves market, powered by China’s fine-chemical investments and India’s API production scale-up

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Insights and Trends of Chemical Industry Valves Market

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising automation in water and wastewater facilities | +1.2% | Global, with APAC and North America leading adoption | Medium term (2-4 years) |

| Tightening discharge-quality limits drive upgrades | +0.8% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Ageing municipal infrastructure replacement cycle | +0.9% | North America and Europe core, emerging in APAC urban centers | Long term (≥ 4 years) |

| Surge in desalination CAPEX, esp. GCC and Australia | +0.7% | GCC, Australia, with spillover to Mediterranean and California | Medium term (2-4 years) |

| Low-power IIoT actuators cut OPEX | +0.4% | Global, concentrated in developed markets initially | Short term (≤ 2 years) |

| Circular-economy push for recyclable valve bodies | +0.3% | EU leading, North America following, APAC selective adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Adoption of Industry 4.0 and Smart Control

Digitally enabled valves equipped with pressure, vibration, and position sensors now integrate seamlessly with distributed control systems, allowing predictive maintenance that cuts unplanned downtime by 25–30% while providing the audit trail demanded under API 624 low-emission rules.[1]Emerson Electric Co., “DeltaV Distributed Control System Integration,” Emerson, emerson.com Operators are layering blockchain-based authentication on valve firmware to deter cyber-intrusions, yet annual cyber-insurance outlays ranging from USD 50,000 to 200,000 remain a barrier for smaller chemical plants.[2]Flowserve Corporation, “Smart Valve Technologies and Cybersecurity Solutions,” Flowserve, flowserve.com Vendors are responding with air-gapped architectures that isolate critical safety loops from enterprise networks, balancing performance with risk mitigation. Smart-valve retrofits also streamline workforce allocation as aging technicians retire, easing the chemical industry valves market’s chronic skills shortage. As proof-of-concept pilots convert into multi-site rollouts, the addressable installed base grows rapidly across Asia-Pacific and North America.

Tightening Global HSE Regulations and Emission Norms

API 641, ISO 15848, and the European Union Industrial Emissions Directive have reframed procurement criteria, elevating triple-offset butterfly and metal-seated ball valves capable of leakage rates below 100 ppm.[3]European Commission, “Industrial Emissions Directive 2010/75/EU,” European Commission, europa.eu Fines of USD 100,000-500,000 per violation push operators toward fully certified portfolios, widening the competitive gap between multinationals with extensive qualification data and niche firms facing test costs surpassing USD 2 million per valve family. Compliance mandates are shortening replacement cycles in mature plants and stimulating greenfield demand for hydrogen-ready solutions in Europe and North America. Premium pricing of 20–30% on low-emission designs is offset by avoided penalties and reduced fugitive-emission taxes, reinforcing spec-in momentum.

Specialty-Chemical Capacity Surge in APAC

Asia-Pacific’s fine-chemical build-out features landmark investments such as BASF-PETRONAS’s USD 3.1 billion Malaysian complex that installed more than 15,000 valves, and Rongsheng Petrochemical’s USD 12.2 billion Zhejiang refinery-petrochemical integration consuming nearly 25,000 units. Output of electronic and pharmaceutical intermediates rose 8.2% in China during 2024, fueling demand for exotic alloys tolerant of aggressive media. Although smart-valve penetration lags due to maintenance-skill gaps, rising production complexity is nudging operators toward condition-based monitoring, splitting the regional market between cost-focused pneumatic products and premium digital offerings.

Lifecycle-Cost Optimization Favoring Corrosion-Resistant Valves

Total cost-of-ownership models that capture 15-20-year asset lifecycles reveal that exotic alloys cost 300-400% more than stainless steel yet deliver 5–7× service life in high-acid or chlor-alkali streams. Digital twins simulate degradation paths, enabling valve replacement before wall-thickness thresholds are reached, while extending service intervals by up to 50%. With continuous-process shutdowns costing USD 500,000–2 million per day, the economics favor corrosion-resistant designs, pushing the chemical industry valves market toward lifecycle-value pricing rather than upfront cost comparisons.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain volatility in nickel and copper alloys | -0.6% | Global, with particular impact on stainless steel and duplex alloy valve production | Short term (≤ 2 years) |

| Skilled-labour shortage delays retrofits | -0.4% | North America and Europe primarily, emerging in APAC developed markets | Medium term (2-4 years) |

| Cyber-security concerns slow smart-valve adoption | -0.3% | Global, concentrated in developed markets with advanced infrastructure | Medium term (2-4 years) |

| Rising PFAS-focused regulations increase qualification costs | -0.2% | North America and EU leading, expanding to APAC regulatory frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Nickel/Molybdenum Prices Inflating Alloy Costs

Nickel prices swung 35–40% and molybdenum 25–30% during 2024, driving an 18% hike in nickel-alloy valve quotations according to Shanghai Metals Market. With raw materials representing up to 70% of exotic valve manufacturing cost, suppliers have adopted quarterly price escalators and minimum order sizes to preserve margins. End-users counter by lengthening bid cycles and forward-buying during price dips, injecting demand volatility that complicates production planning. The restraint constrains the uptake of corrosion-resistant materials in cost-sensitive projects, marginally diluting the chemical industry valves market growth trajectory in the short term.

Cyber-Insurance Premiums Curbing Full IoT Adoption

Annual cyber-insurance policies now run USD 50,000–200,000 for chemical facilities deploying connected valve networks, often adding 15–20% to smart-valve total project costs. Carriers also mandate extensive audits and network segmentation that stretch implementation schedules. Smaller producers with limited OT security staff favor partial connectivity and air-gapped critical loops, delaying comprehensive digitization and constraining the installed base for analytics software. Industry groups such as the Chemical Industry Data Exchange are drafting standardized frameworks to lower premiums, but near-term rollout pace remains uneven across regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Valve Type: Ball Valves Retain Leadership Amid Vacuum-Valve Momentum

The chemical industry valves market size for ball valves represented USD 2.73 billion in 2025 and held the highest 18.44% share, sustained by reliable shut-off across corrosive media and broad ANSI pressure classes. Multiport and cryogenic variants have further entrenched presence in continuous and batch processes. Vendors bundle ball valves with smart digital positioners that trim maintenance labor by 20%, cementing loyalty among large petrochemical accounts.

Vacuum valves however are projected to outpace all other categories at a 4.92% CAGR through 2031. Semiconductor chemical vapor deposition lines and pharmaceutical freeze-drying chambers demand ultra-low leak rates that gate valves or traditional shuts cannot deliver. Flowserve’s spring-less designs featuring high-purity stainless internals illustrate the capability leap favored by fabs targeting parts-per-billion contamination thresholds. The surge is further supported by governments courting chip investments in China, Japan, and the United States, priming a multiyear vacuum-valve upgrade cycle.

By Material: Stainless Steel Dominance Faces Exotic-Alloy Upswing

Stainless steel retained a commanding 41.29% of chemical industry valves market share in 2025 on its balance of corrosion resistance and cost efficiency. 316L remains the default in neutral-pH organics, while duplex grades expand in chloride-laden streams. Combined spare-parts commonality and global stocking networks reinforce preference among multi-plant operators.

Exotic-alloy demand, particularly titanium and Hastelloy, is set to register a 5.58% CAGR, reflecting green-hydrogen electrolyzer requirements and sulfuric-acid based specialty production. Titanium’s biocompatibility aligns with active pharmaceutical ingredient lines, whereas Hastelloy C-276 delivers longevity in mixed-acid reactors. NACE MR0175 compliance further drives uptake in sour-gas derivatives. The shift widens revenue pools even as price premiums exceed 300%, elevating the chemical industry valves market size for high-alloy categories.

By Valve Size: Mid-Range Volumes Dominate as Mega-Diameter Demand Accelerates

Valves sized 1-6 inches generated over half of 2025 revenue at a 52.27% share, straddling feedstock transfer, utility lines, and auxiliary dosing duties. Their ubiquity enables economies of scale, fostering brisk aftermarket parts turnover and bundled service contracts.

Above-50 inch valves, though niche in unit volume, are forecast to log a 5.79% CAGR, propelled by mega-integrated complexes such as BASF’s acrylic acid lines and Middle East PDH projects. Handling requirements exceeding 10,000 m³/h spur investment in heavy-fabrication shops with robotic submerged-arc welding cells, erecting barriers to entry and raising the chemical industry valves market size premium for large-bore products.

By Actuation Technology: Pneumatic Control Prevails While Smart Platforms Surge

Pneumatic systems represented 59.19% of 2025 revenue thanks to inherent safety in volatile atmospheres and plant-wide compressed-air availability. Fail-safe spring-return designs support safety-integrity-level nodes, while cost points remain attractive in bulk commodity chemicals.

Smart IoT-enabled actuation is forecast for a 6.12% CAGR through 2031. Integrated sensors capture stem-torque trends and seat-wear signatures, enabling operators to defer overhauls by up to 18 months. WirelessHART and ISA-100 gateways lower installation labor, broadening appeal despite cyber-insurance friction. As analytic platforms mature, hardware revenue is increasingly tied to software-as-a-service subscriptions, recalibrating long-term monetization models in the chemical industry valves market.

Geography Analysis

Asia-Pacific generated 38.75% of 2025 revenue, driven by China’s 8.2% rise in specialty-chemical output and India’s pharmaceutical build-out. State-backed projects such as Rongsheng Petrochemical’s Zhejiang complex specify MRI-compliant low-leak valves, while Japanese and South Korean fabs favor ultra-high-purity vacuum variants. Regional OEMs are localizing actuator and casting operations to sidestep import duties, further cementing supply-chain heft.

North America represents the second-largest region, anchored by shale-gas derived petrochemical investments on the U.S. Gulf Coast. Replacement cycles focus on API 624 certified options to satisfy Environmental Protection Agency LDAR programs, with predictive-maintenance retrofits bundling analytics into 2030 budgets. Canada’s blue-hydrogen projects add demand for embrittlement-resistant alloys.

Europe is characterized by regulatory-driven upgrade expenditure under the Industrial Emissions Directive, leading to steady replacement demand for low-fugitive valves. German and Scandinavian chemical clusters are early adopters of additive-manufactured spare parts, while United Kingdom sites prioritize cybersecurity- fortified actuators post-NIS 2 directive.

Competitive Landscape

Competitive intensity in the chemical industry valves market remains moderate. Emerson, Flowserve, and Schlumberger collectively hold a combined 42% revenue share, leveraging digital twin platforms that cut bid-to-delivery lead times by 30%. Flowserve’s 2024 acquisition of Mogas expanded severe-service coverage, underpinning its strategy to upsell high-temperature coking valves. Emerson’s DeltaV integration embeds analytics at the control-system layer, boosting switching costs for end users.

Mid-tier specialists such as Metso, Alfa Laval, and HEROSE target niche growth pockets. Metso’s 2024 purchase of Jindex brought advanced actuator IP, while HEROSE capitalizes on early hydrogen-ready certifications. Additive manufacturing disruptors provide rapid spare-part fulfillment, compressing aftermarket response times and challenging traditional stocking models.

Strategic partnerships between valve OEMs and cloud-platform providers like Microsoft Azure or AWS extend asset-performance dashboards across multi-site portfolios. Vendors that demonstrate certified cybersecurity stacks alongside API 6A, 6D, and ISO 15848 credentials are winning preferred-supplier status. Consequently, inorganic expansion and digital-service layering will shape competitive positioning through 2030.

Leaders of Chemical Industry Valves Market

Emerson Electric Co.

Schlumberger Limited

Alfa Laval Corporate AB

Flowserve Corporation

Crane Holdings, Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: IMI plc introduced a cyber-secure wireless protocol for smart-valve communication, delivering encrypted data transfer and maintaining air-gapped safety loops.

- October 2024: Flowserve Corporation closed its USD 290 million buyout of Mogas Industries, adding high-temperature delayed-coking valves.

- September 2024: Emerson Electric rolled out DeltaV control-system integration for smart positioners, cutting maintenance spend by 25–30%.

- August 2024: BASF PETRONAS commissioned its USD 3.1 billion Malaysian complex with 15,000 specialty valves.

Scope of Report on Chemical Industry Valves Market

Valves are mechanical devices and a critical element in the industry where the movement of liquid or gas through the piping systems while controlling the flow, protecting the equipment, and providing safety in emergency situations. The Valves Market in Chemical Industry is segmented By Type (Ball, Butterfly, Gate/Globe/Check, Plug, Control) and Geography.

| Ball |

| Butterfly |

| Gate |

| Globe |

| Check |

| Plug |

| Diaphragm |

| Vacuum |

| Hybrid |

| Other Valve Types |

| Stainless Steel |

| Cast Iron |

| Alloy-Based |

| Plastic / PVC |

| Cryogenic-Grade |

| Exotic Alloys (Ti, Hastelloy) |

| Up to 1″ |

| 1″ – 6″ |

| 6″ – 25″ |

| 25″ – 50″ |

| Above 50″ |

| Manual |

| Pneumatic |

| Electric |

| Hydraulic |

| Smart (IoT-enabled) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Valve Type | Ball | ||

| Butterfly | |||

| Gate | |||

| Globe | |||

| Check | |||

| Plug | |||

| Diaphragm | |||

| Vacuum | |||

| Hybrid | |||

| Other Valve Types | |||

| By Material | Stainless Steel | ||

| Cast Iron | |||

| Alloy-Based | |||

| Plastic / PVC | |||

| Cryogenic-Grade | |||

| Exotic Alloys (Ti, Hastelloy) | |||

| By Valve Size (Inches) | Up to 1″ | ||

| 1″ – 6″ | |||

| 6″ – 25″ | |||

| 25″ – 50″ | |||

| Above 50″ | |||

| By Actuation Technology | Manual | ||

| Pneumatic | |||

| Electric | |||

| Hydraulic | |||

| Smart (IoT-enabled) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the chemical industry valves market expected to grow through 2031?

Revenue is forecast to rise from USD 15.4 billion in 2026 to USD 18.87 billion by 2031, posting a 4.15% CAGR.

Which valve type contributes the most revenue today?

Ball valves lead with 18.44% share of 2025 sales, owing to versatile shut-off performance across corrosive chemistries.

What is driving demand for exotic-alloy valves?

Green-hydrogen electrolyzer build-outs and aggressive acid processes demand titanium and Hastelloy designs that last 5–7× longer than stainless steel.

Why are cyber-insurance costs a concern for smart-valve adoption?

Policies run USD 50,000-200,000 annually and add 15-20% to project budgets, pushing smaller plants toward partial connectivity.

Which region offers the strongest growth outlook?

Asia-Pacific is projected to record a 5.35% CAGR through 2031, powered by specialty-chemical and pharmaceutical investments.

Page last updated on: